Sample Category Title

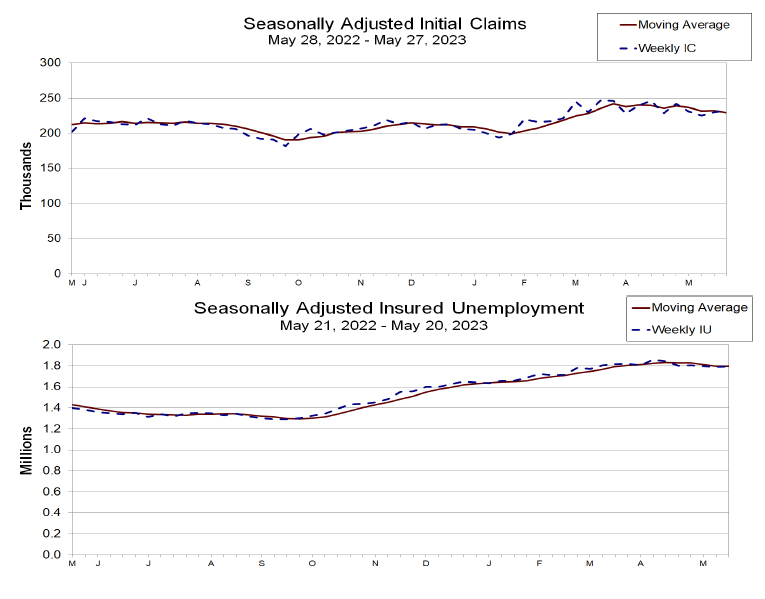

US jobless claims rose to 232k, slightly below expectations

US initial jobless claims rose 2k to 232k in the week ending May 27, slightly below expectation of 236k. Four-week moving average of initial claims dropped -2.5k to 229.5k.

Continuing claims dropped -6k to 1795k in the week ending May 20. Four-week moving average of continuing claims dropped -1.5k to 1789k.

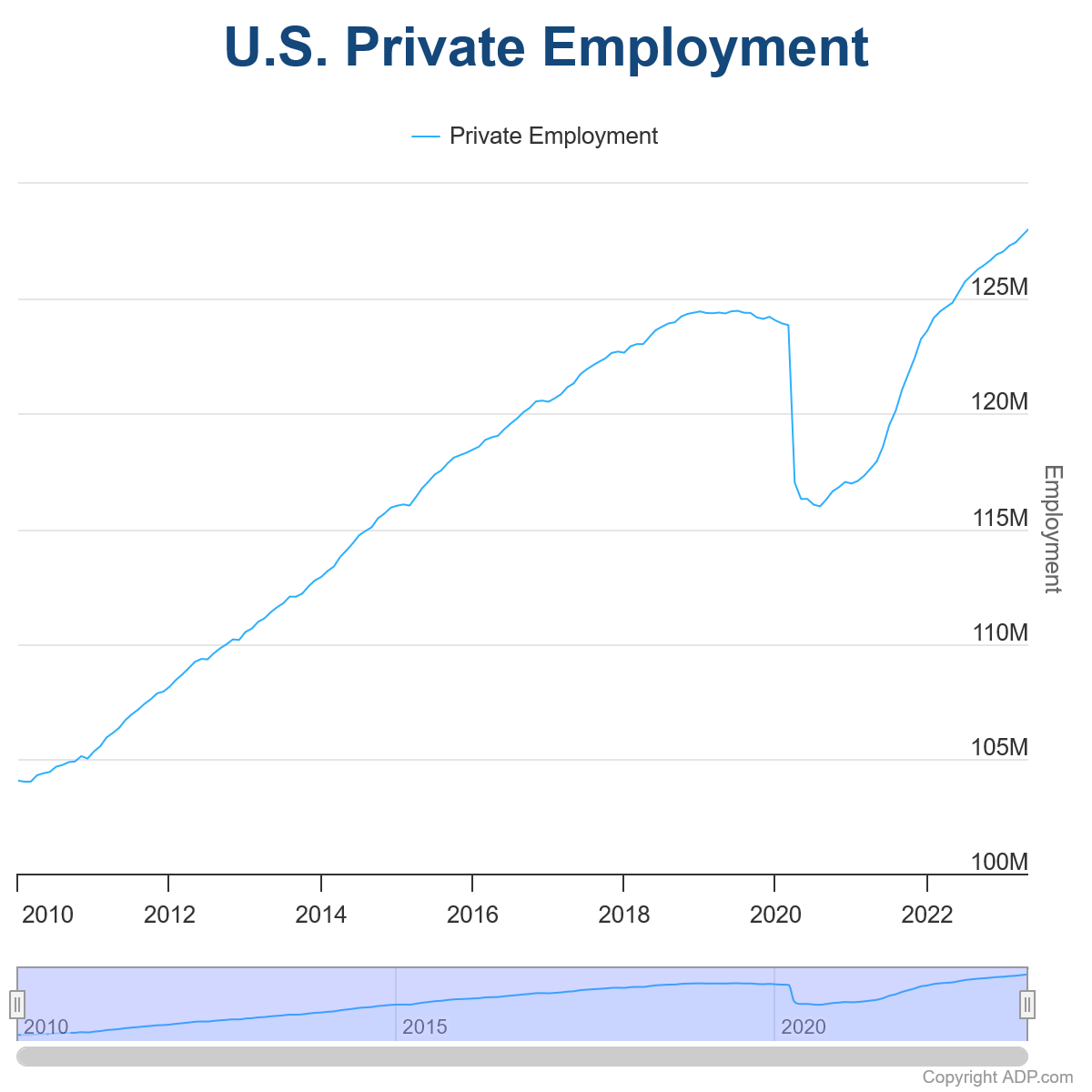

US ADP jobs grew 278k, pay growth slowing substantially

US ADP private employment grew 278k in May, well above expectation of 167k. By sector, goods-producing jobs grew 110k while service-providing jobs grew 168k. By establishment size, small companies added 235k jobs, medium companies added 140k, large companies cut -106k.

Job changers saw a gain of 12.1% yoy, down a full percentage point from April. For job stayers, the increase was 6.5% yoy in May, down from 6.7% yoy.

"This is the second month we've seen a full percentage point decline in pay growth for job changers. Pay growth is slowing substantially, and wage-driven inflation may be less of a concern for the economy despite robust hiring." Nela Richardson, Chief Economist, ADP said.

ECB Set to Continue the Fight Against Inflation Despite Weakening

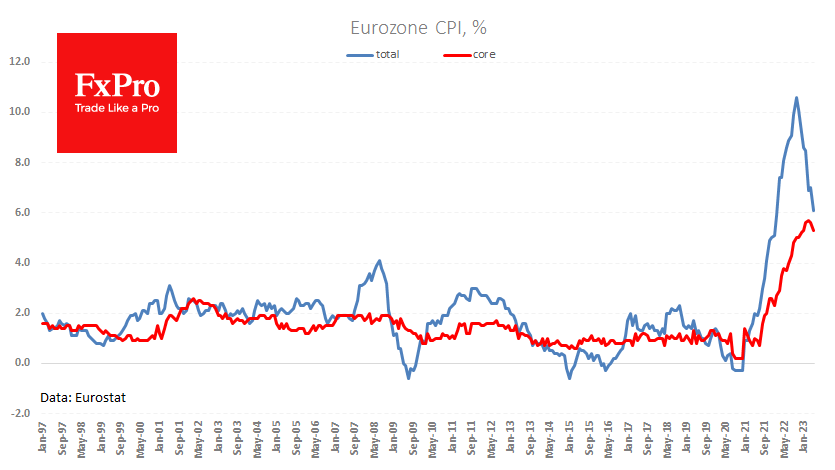

The euro is hovering around the $1.07 level, barely recovering above that mark on Thursday morning despite a sharper-than-expected drop in inflation.

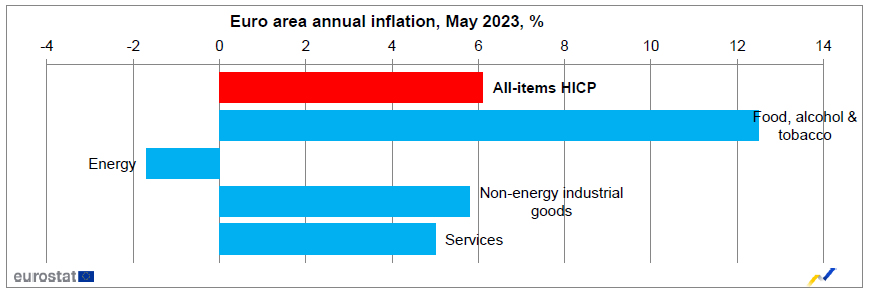

Eurostat’s preliminary estimate showed a decline in annual inflation in May to 6.1% from 7.0% in April. Economists had forecasted a smaller decrease to 6.3% y/y. Core inflation, which excludes volatile energy and food prices, also slowed down from 5.6% to 5.3%, confirming a downward trend.

Earlier statistics from other indicators and CPI data from the major countries suggested similar outcomes, but it is still helpful to have confirmation from the consolidated data.

However, we would like to stress that in these critical times, the regulator’s perception of these facts is more important than the facts themselves. As the statistics were released, ECB President Lagarde reaffirmed in her speech in Hannover that she wanted to continue the cycle of further rate hikes.

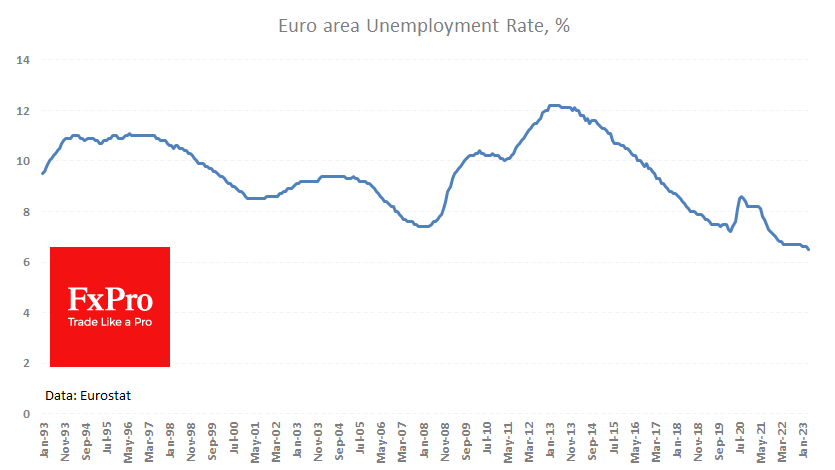

She also said that it needed to be clarified whether the already implemented hikes were enough. The hawkish stance of the ECB is also supported by data from the labour market, where the unemployment rate fell to 6.5% in April, the lowest level since 1993. The tight labour market could create additional price pressures despite falling energy prices and slower growth in food prices.

A strong labour market and a hawkish ECB attitude favour the single currency. We also note that the ECB only has a mandate for an inflation target, while the Fed must maintain maximum employment.

The euro area may be less sensitive to monetary policy than inflation in the US. This was evident in higher rates than in the US before 2008 and lower rates afterwards. Zero-rates era is over, so we expect a return of positive key rate differentials between Europe and the US in the coming years.

Crypto: Correction in Progress

Market picture

The crypto market has lost another 0.8% of its capitalisation in the last 24 hours, rolling back to $1,128, where it was last Friday. Bitcoin is down 1.4%, Ether is down 0.8%, and the top altcoins are mostly down, except for Litecoin, which is up 3%.

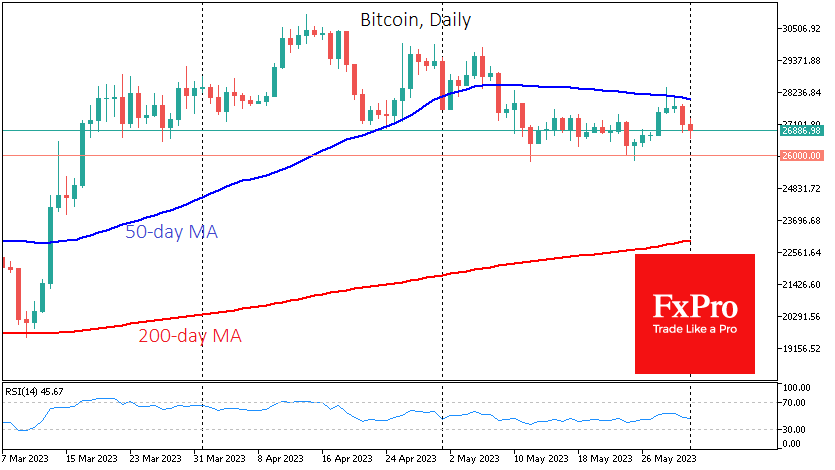

Bitcoin closed the month down 7.6% at $27.0K, having gained every month since the beginning of the year. With further declines, the momentum towards the $25.5-26.0 area is worth a closer look. There is a 50-week average near the lower boundary, while at the top, bitcoin found support on May’s declines.

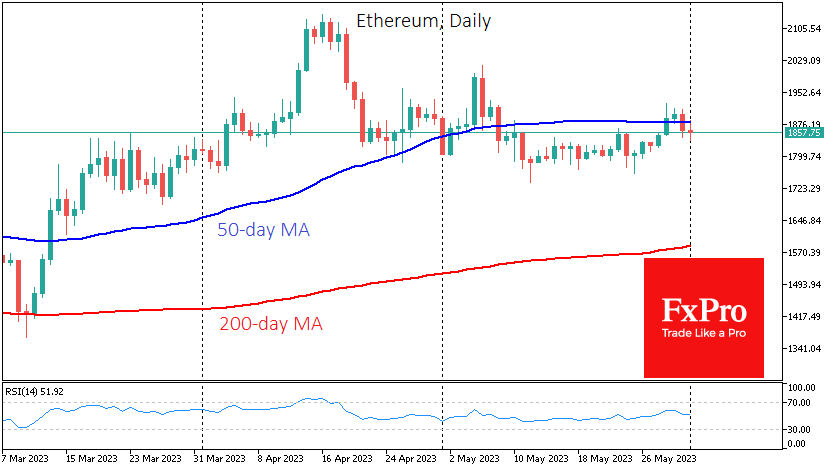

Ethereum failed to stick to levels above its 50-day moving average and pulled back to $1850. The following technical support is at $1800.

A solid move below these areas in Bitcoin and Ether will likely trigger a broader sell-off in altcoins.

Regarding seasonality, June is considered a relatively successful month for BTC. Over the past 12 years, bitcoin has ended the month up seven times (up 16.7% on average) and down five times (-19.2% on average).

News background

According to the Financial Times, the world’s biggest banks, including Standard Chartered, Nomura and Charles Schwab, are developing cryptocurrency trading platforms. Institutional investors remain interested in investing in digital assets but only trust the big banks.

Blockchain industry veteran and Bitcoin Cash supporter Roger Ver believes that Ethereum, despite its smaller capitalisation, has become “a driving force for cryptocurrency adoption worldwide”. According to him, ETH has brought innovations such as NFT, smart contracts, scaling solutions and so on to the industry.

The Binance exchange has expressed support for potential US Republican presidential candidate Ron DeSantis for his intention to oppose any form of cryptocurrency prohibition.

According to Wu Blockchain, the world’s largest cryptocurrency exchange Binance plans to cut a fifth of its staff in June.

Tron developers have patched a critical vulnerability that exposed $500 million in assets.

Eurozone CPI slowed to 6.1% yoy in May, core CPI down to 5.3% yoy

Eurozone CPI slowed from 7.0% yoy to 6.1% yoy in May, below expectation of 6.3% yoy. CPI core (ex-energy, food, alcohol & tobacco) slowed from 5.6% yoy to 5.3% yoy, below expectation of 5.3% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in May (12.5%, compared with 13.5% in April), followed by non-energy industrial goods (5.8%, compared with 6.2% in April), services (5.0%, compared with 5.2% in April) and energy (-1.7%, compared with 2.4% in April).

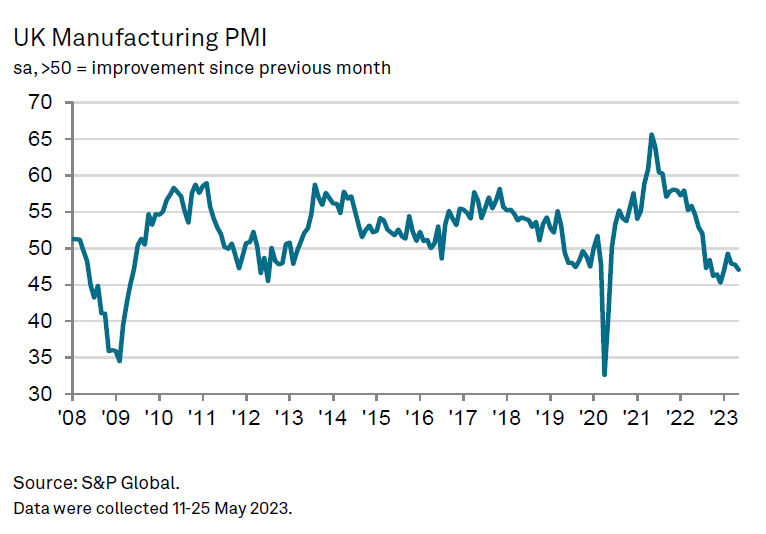

UK PMI manufacturing finalized at 47.1, downturn deepened

UK PMI Manufacturing was finalized at 47.1 in May, down from April's 47.8, hitting the lowest level in four-months. S&P Global noted the output contracted in investment and intermediate goods sectors. Input costs fell and supply chain pressured subsided.

Rob Dobson, Director at S&P Global Market Intelligence, said:

"The UK manufacturing downturn deepened in May, with output, new orders and employment all falling at increased rates. Manufacturers are finding that any potential boost to production from improving supply chains is being completely negated by weak demand, client destocking and a general shift in spending in the UK away from goods to services.

" These factors are also driving a broad decrease in demand from overseas amid reports of lost orders from the US and mainland Europe. The retrenchment in export demand is also being exacerbated by some EU clients switching to more local sourcing to avoid post-Brexit trade complications."

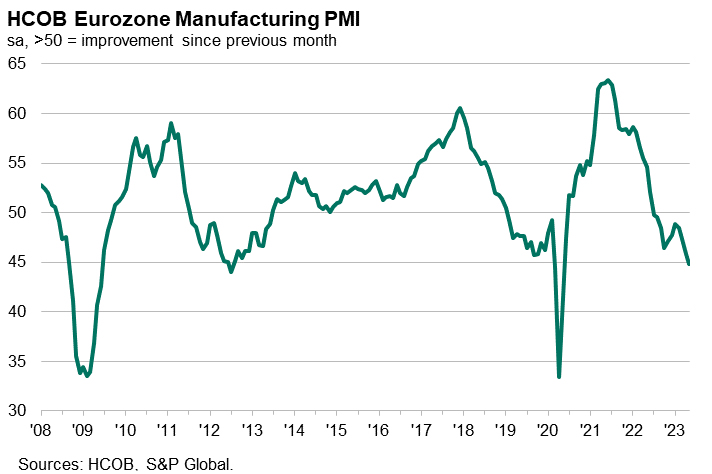

Eurozone PMI manufacturing finalized at 44.8, weakness in demand increasingly evident

Eurozone PMI Manufacturing was finalized at 44.8 in May, down from April's 45.8, hitting the worst level in 36 months. PMI Manufacturing output dropped from 58.5 to 46.4, a 6-month low. Factor gate prices declined fro the first time since September 2020.

Looking at some member states, Ireland (47.5), Italy (45.9), the Netherlands (44.2) and Germany (43.2) were all at 36-month low. Austria hit 37-month low at 39.7. France recovered to 2-month high at 45.7.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said: "The weakness in demand in the manufacturing sector, which has become increasingly evidence since the beginning of the year in falling PMI readings, has now led the surveyed companies to reduce their production for the second month in a row".

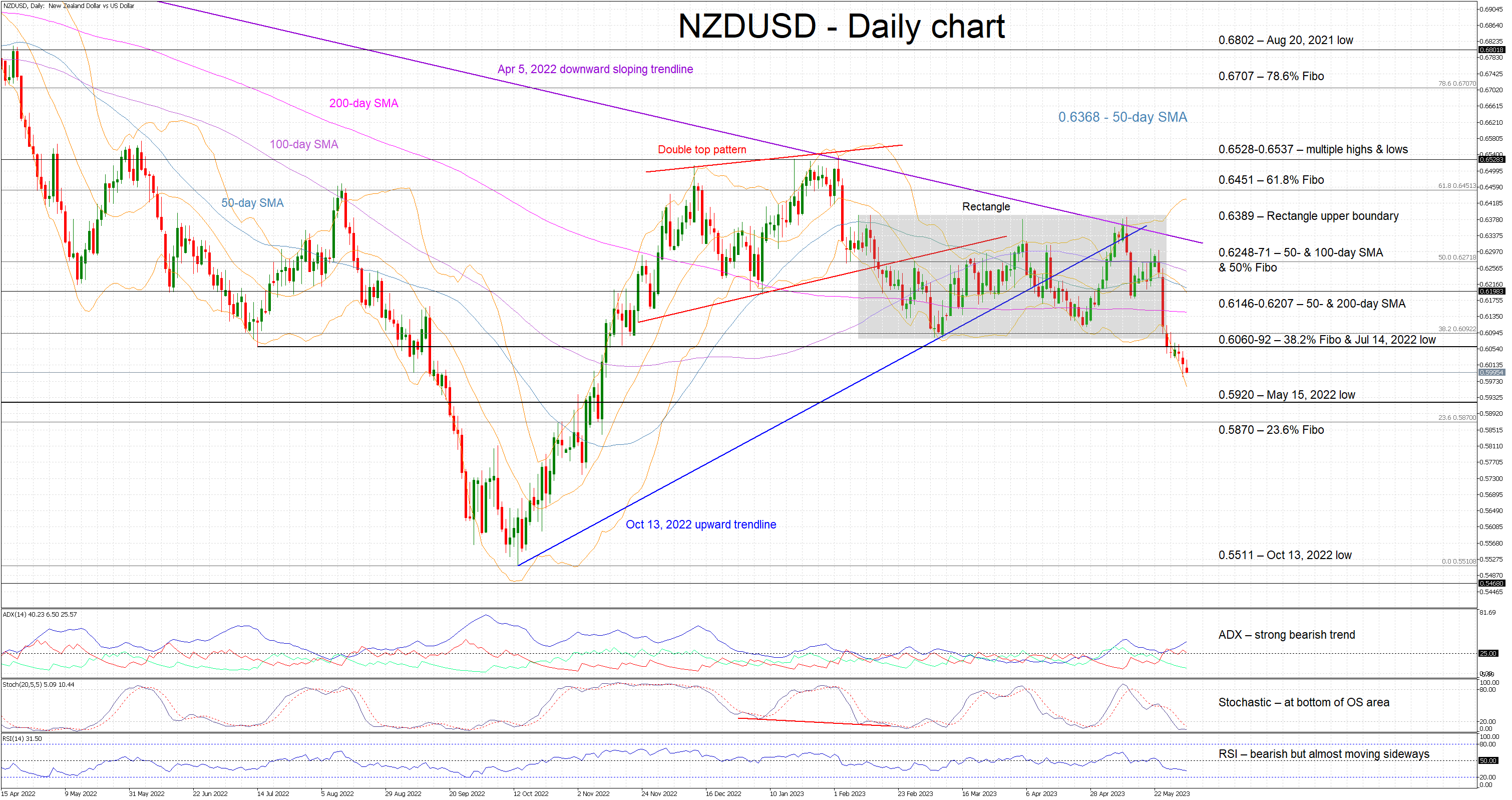

Bearish Breakout in NZDUSD; Will It Last?

NZDUSD has finally managed to break below the rectangle that has been dictating the price action since February 2023, as NZD bears continue to recover part of the losses they have been suffering by the rally that commenced on October 13, 2022. However, the downside breakout has not been impressive as NZD bulls appear determined to halt this correction.

Having said that NZD bears probably feel in control of the market. The Average Directional Movement Index (ADX) is edging higher, signaling a strong bearish trend, and the RSI is hovering well below its 50-midpoint. More interestingly, the stochastic oscillator remains stuck at the lower end of its oversold territory. Although it can hover in this area for a while, its most recent moves are also a sign that the bearish pressure could soon abate.

If the NZD bears try to further capitalize on the bearish breakout, they would target the 0.5920 level set by the May 15, 2022 low. The 23.6% Fibonacci retracement of the April 5, 2022 – October 13, 2022 downtrend at 0.5870 could prove tougher to crack than anticipated. However, if broken, it could open the door for a more sustainable move towards the October 13, 2022 low of 0.5511.

Should the NZD bulls decide to negate the current bearish move, they would have to recapture the 0.6060-0.6092 range populated by the 38.2% Fibonacci retracement and the July 14, 2022 low respectively. A return of the NZDUSD pair back inside the recent rectangle would be a short-term victory for the NZD bulls and quite important for market sentiment.

To sum up, the bearish breakout is significant, but NZD bears have to push for a stronger correction to avoid calls of a false breakout.

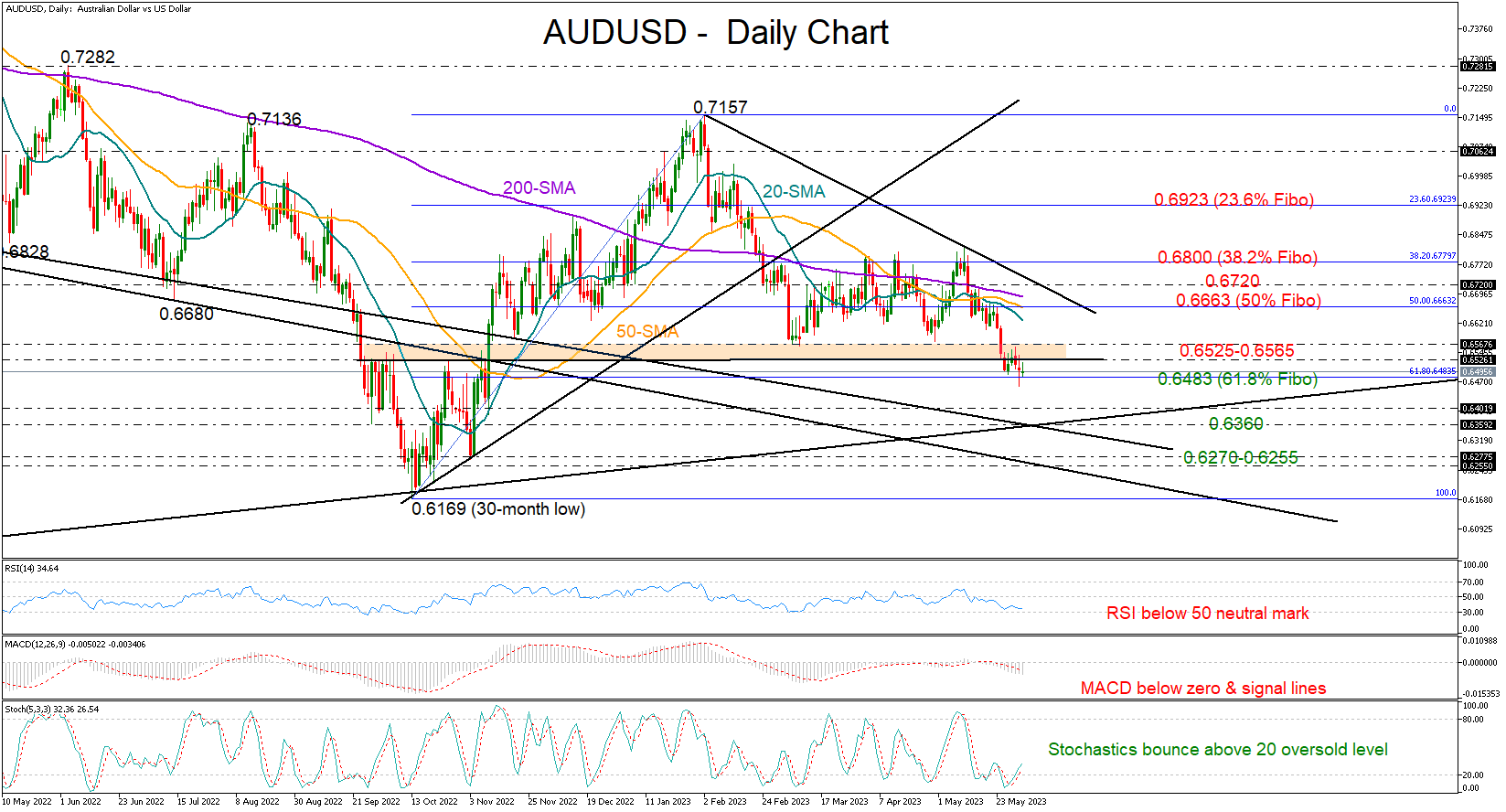

AUDUSD Escapes Bearish Breakdown But Bias Weak

AUDUSD bounced back above the nearby 0.6483 base, which has been buffering selling forces since the start of May, after a flash spike to a new six-month low of 0.6457 on Wednesday.

The rebound in the stochastic oscillator promotes an upside breakout or some stabilization, though stronger bullish signals are required to boost market sentiment. Moreover, the RSI is comfortably below its 50 neutral mark and the MACD remains negatively charged below its red signal line, both suggesting sellers have not abandoned their efforts yet. The negative slope in the simple moving averages (SMA) is another discouraging sign.

A decisive extension above the 0.6525-0.6565 zone and into the former range area could prompt an increase towards the 50% Fibonacci retracement of the 0.6169-0.7157 upleg at 0.6663. The 200-day SMA and the tentative resistance trendline at 0.6720 could be more important obstacles, a break of which may lift the price directly up to the 38.2% Fibonacci and the topside of the range at 0.6800.

Should the bears successfully breach the 0.6485 bar, they may forcefully squeeze the price towards the tentative ascending trendline drawn from the 2020 low at 0.6360. Another failure here could add more fuel to the sell-off, shifting the spotlight straight to the broken support line from August 2021 and the 0.6270-0.6255 constraining region.

In short, negative risks have not evaporated in the AUDUSD market, although a pause in the current bearish wave is likely. A clear close below 0.6483 may generate a more aggressive decline.

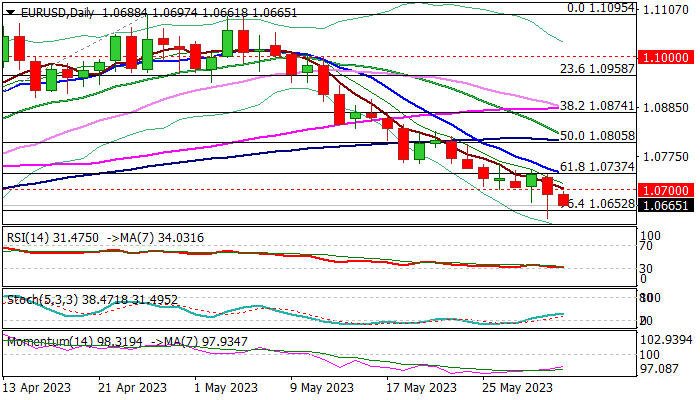

EUR/USD: Bears Hold Grip ahead of EU Inflation Report

The Euro remains at the back foot in early Thursday despite Wednesday’s strong downside rejection and signal of bear-trap formation on daily chart, as well as constructive signals from daily chart (fading bearish momentum/north-heading stochastic / RSI approaching oversold territory).

The action stays below broken psychological level at 1.07 for the second day that adds to negative near-term outlook for renewed attempt through cracked Fibo support at 1.0652 (76.4% of 1.0516/1.1095), clear break of which is needed to signal bearish continuation.

At the upside, 1.07 offers immediate resistance, followed by strong barriers at 1.0737/43 double-Fibo resistance zone (broken 61.8% of 1.0516/1.1095 / 23.6% of 1.1095/1.0635 / falling 10DMA) which should cap extended upticks to keep near-term bias with bears.

Markets await release of the Eurozone inflation report for May, with prevailing optimistic mood after inflation in Germany dropped to the lowest in more than a year.

EU’s harmonized core CPI is expected to dip to 7.2% in May from 7.3% in April, which would add to signals that bloc’s underlying inflation is eventually starting to ease and lower bets for stronger rate hikes by the ECB.

Res: 1.0700; 1.0744; 1.0759; 1.0805.

Sup: 1.0652; 1.0631; 1.0600; 1.0551.