Sample Category Title

Gold Range Tightens Before Fed — Breakout Pressure Builds

Key Highlights

- Gold started a fresh decline from $5,240 and traded below $5,120.

- A major bearish trend line is forming with resistance at $5,075 on the 4-hour chart.

- WTI Crude Oil surged toward $102 before there was a pullback.

- Bitcoin rallied toward $76,000 before it faced some substantial resistance.

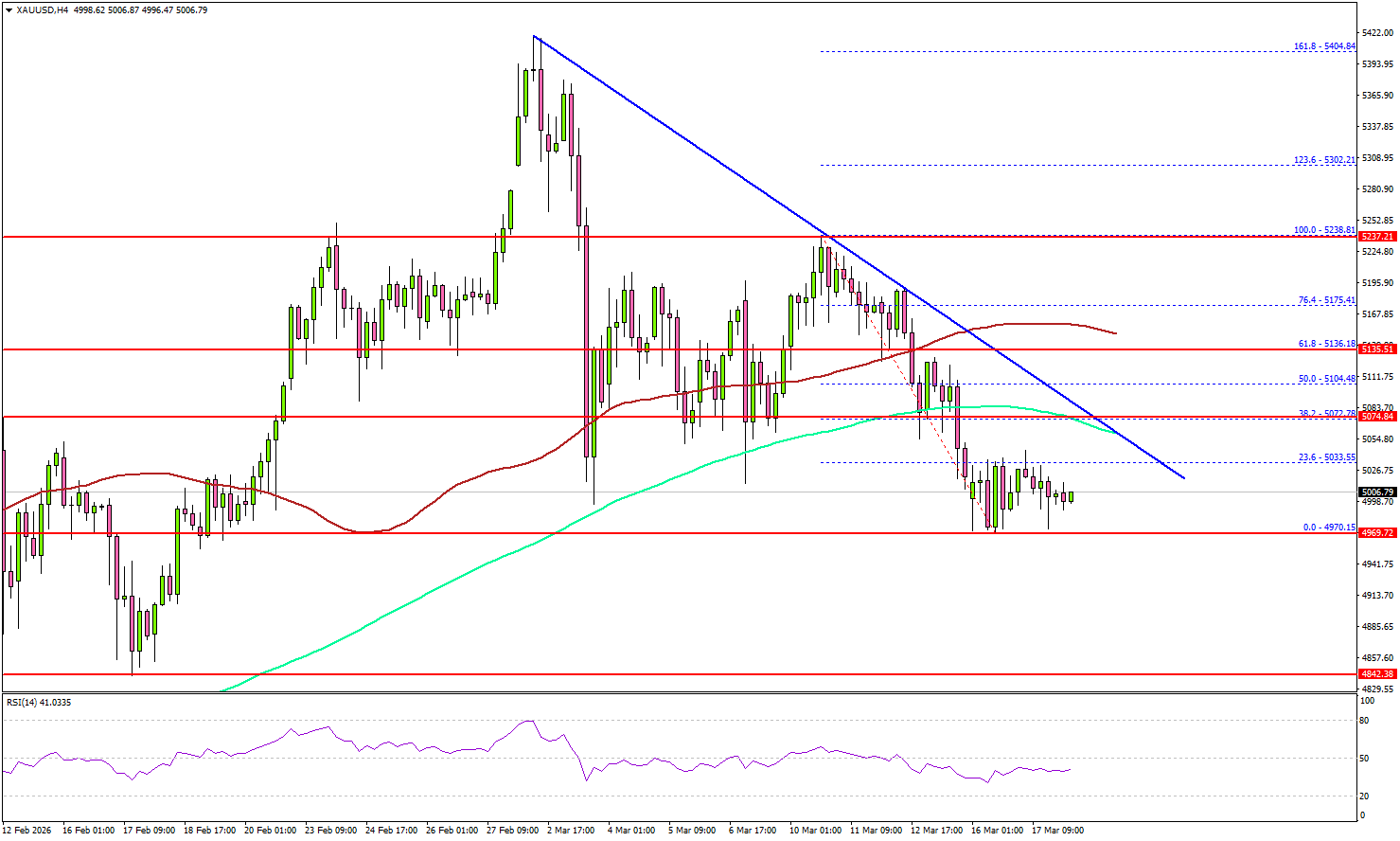

Gold Price Technical Analysis

Gold remained well bid above $4,970 against the US Dollar. The price climbed above $5,150 and $5,200 before it started a fresh decline.

The 4-hour chart of XAU/USD indicates that the price trimmed gains from $5,238 and traded below $5,150. There was a close below the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours).

The price traded as low as $4,970 and is currently consolidating losses. There is also a major bearish trend line forming with resistance at $5,075.

On the upside, immediate resistance is $5,075 and the trend line. The next major resistance sits near $5,100. A clear move above $5,100 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $5,135 and the 61.8% Fib retracement level of the downward move from the $5,238 swing high to the $4,970 low.

The main target for the bulls could be $5,165 and the 100 Simple Moving Average (red, 4 hours), above which the price could test $5,200. If there is another decline, Gold might find bids near the $5,000 level. The first major support sits at $4,970, below which the price might slide to $4,920.

The main support sits at $4,880. Any more losses might call for a test of $4,840 or even $4,820 in the coming days.

Looking at WTI Crude Oil, the price rallied over 10% amid the ongoing Iran war before the bears took a stand near the $102 level.

Economic Releases to Watch Today

- US Producer Price Index for Feb 2026 (MoM) – Forecast +0.3%, versus +0.5% previous.

- US Producer Price Index for Feb 2026 (YoY) – Forecast +2.9%, versus +2.9% previous.

- BoE Interest Rate Decision - Forecast 3.75%, versus 3.75% previous.

Japan trade data highlights diversification, shift away from China and U.S.

Japan’s trade data for February revealed a mixed but resilient picture, with exports rising 4.2% yoy to JPY 9,572B, comfortably above expectations. Imports also strengthened, up 10.2% yoy to JPY 9,514B, resulting in a trade surplus of JPY 57.3B. While overall export growth remained solid, the underlying composition points to a significant realignment in demand.

Shipments to China declined -10.9% yoy. Exports to the U.S. fell -8%, driven in part by a sharp -14.8% drop in auto exports.

In contrast, exports to other regions showed strong momentum. Hong Kong saw a surge of 32.3%. Southeast Asia recorded a 5.1% increase, with the regional bloc overtaking China as Japan’s second-largest export destination.

Western Europe also provided support, with shipments rising 17.5% on strong demand from Germany and the U.K.

The data suggests Japan’s exporters are increasingly diversifying away from traditional markets, a shift that may help cushion the impact of global economic fragmentation.

Technical Levels for Major FX Pairs Ahead of FOMC

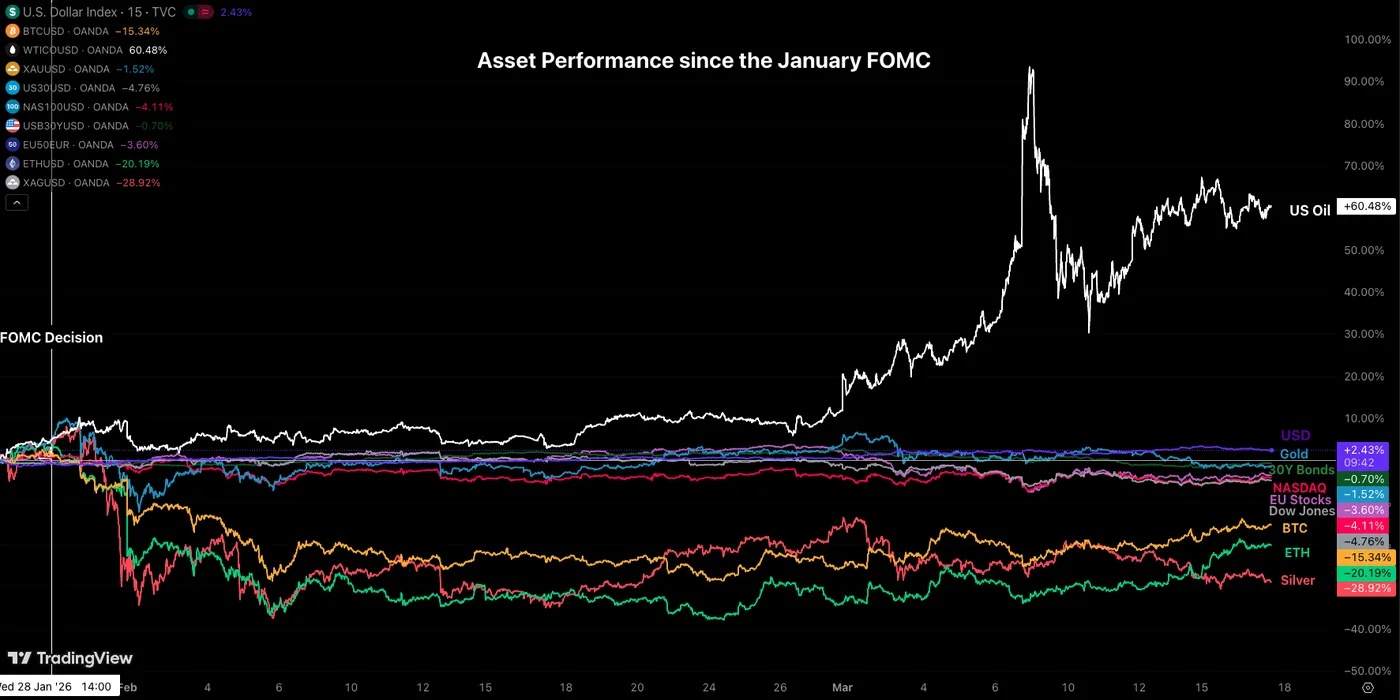

It has been what felt like a few years since the previous FOMC, with what resembles a totally different Market since.

Since January 28, Oil is up close to 60%, Silver is down 25%, previously indestructible US Indexes have eased between 3% to 5%, and the World is now looking very different.

Asset Performance since the January FOMC – March 17, 2026. Source: TradingView

But what is probably the most overlooked Market development remains the US Dollar, aka Petrodollar that reached 10 months highs last Friday, as record bearish positioning led to swift position closures; hence rebounds.

The global Reserve Currency takes the upper hand when it comes down to a squeeze in Oil prices, with countries around the globe forced to hedge, and trade in US Dollars for ever-more expensive Barrels of Crude.

This phenomenon also got magnified by the swift pricing out of Fed Cuts, going from 65 bps pre-conflict to the current ~20 bps.

We will dive into an intraday chart outlook for all Major FX Currency pairs and provide trading levels for the upcoming FOMC event, as traders are anxiously awaiting for the Fed's own economic projections and impacts from the conflict.

All FX Majors Charts with the key levels in play for the March FOMC

NZD/USD 4H Chart and technical levels

NZD/USD 4H Chart, March 17, 2026, Source: TradingView

FOMC Trading Levels for NZD/USD:

Resistance Levels

- 4H 50-period MA 0.58780

- 0.5885 to 0.59 Momentum Pivot

- 0.5930 to 0.5950 (+/- 70 pips) Pivotal Resistance

- March Resistance 0.60 to 0.60150

- July 2025 Resistance 0.6060 to 0.6070

Support Levels

- 0.5850 December High Pivotal Support

- 0.5770 to 0.5790 Mini-Support

- Main Support 0.5720 to 0.5750

USD/JPY 4H Chart and technical levels

USD/JPY 4H Chart, March 17, 2026, Source: TradingView

FOMC Trading Levels for USD/JPY:

Resistance Levels

- 158.50 to 159.50 2026 Major resistance

- 159.75 2026 Highs

- April 2024 160.00 to 160.40 Major Resistance

Support Levels

- 4H 50-period MA 158.63

- Dec highs Major Pivot 157.40 to 157.65

- 156.00 Pivotal Support

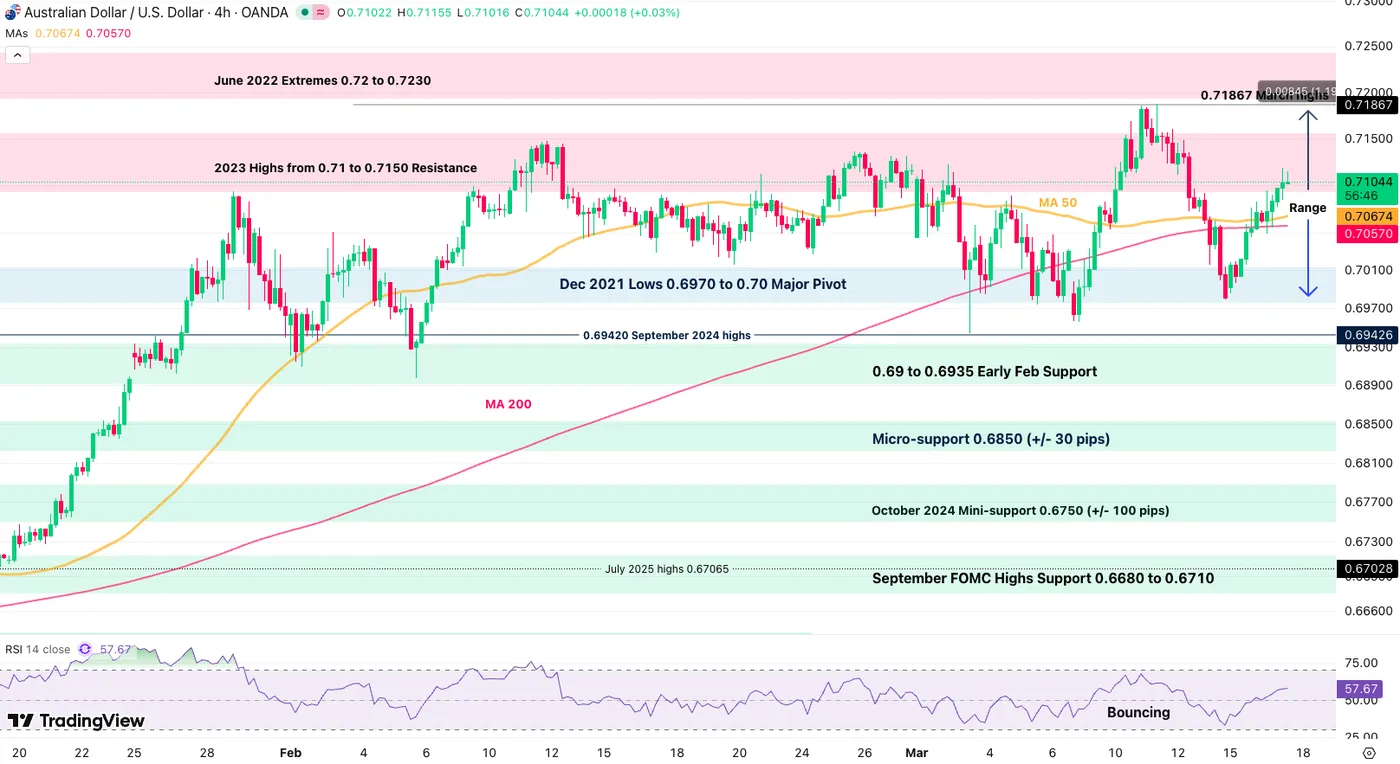

AUD/USD 4H Chart and technical levels

AUD/USD 4H Chart, March 17, 2026, Source: TradingView

FOMC Trading Levels for AUD/USD:

Resistance levels

- 0.71867 2026 Highs

- 2023 Highs from 0.71 to 0.7150 Resistance

- June 2022 Extremes 0.72 to 0.7230

Support levels

- Dec 2021 Lows 0.6970 to 0.70 Major Pivot

- 0.69 to 0.6935 Early Feb Support

- Micro-support 0.6850 (+/- 30 pips)

- October 2024 Minor support 0.6750 (+/- 100 pips)

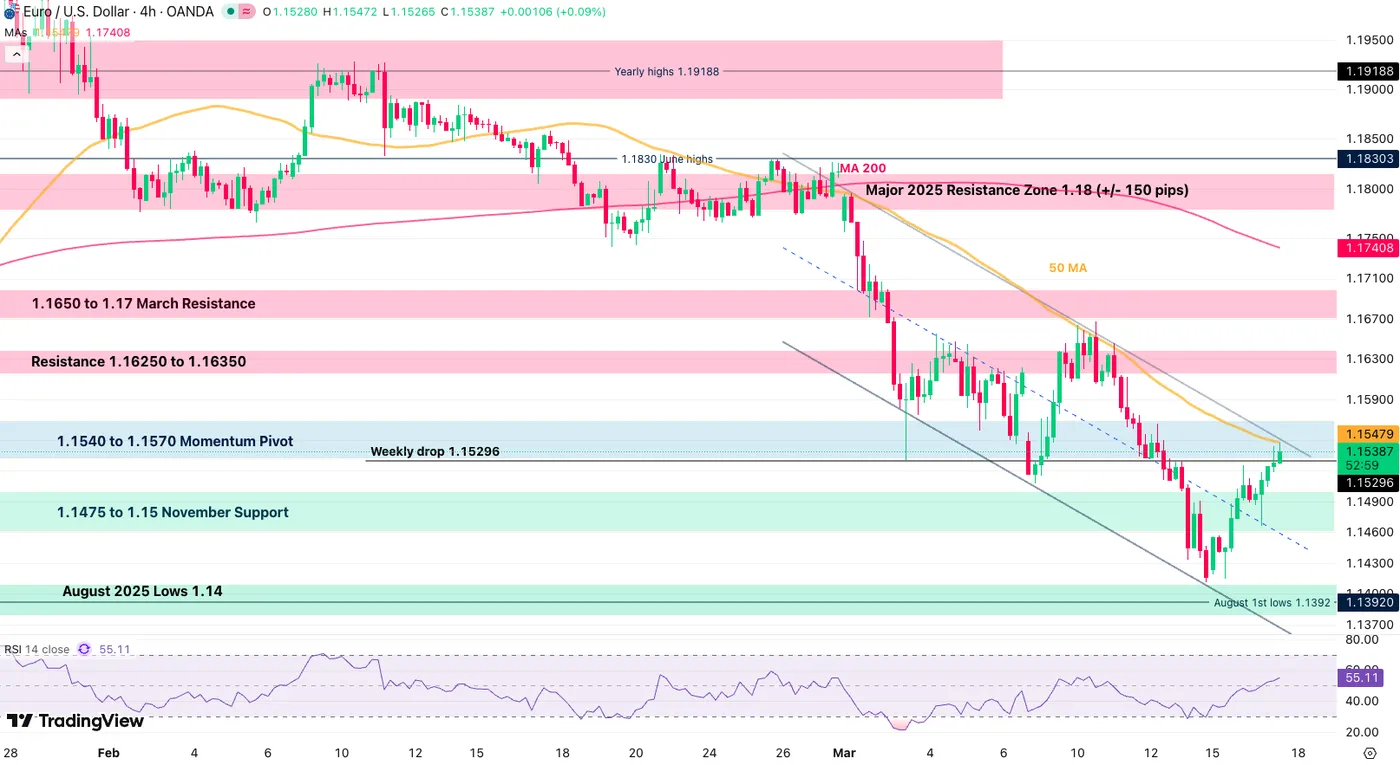

EUR/USD 4H Chart and trading levels

EUR/USD 4H Chart, March 17, 2026, Source: TradingView

FOMC Levels to watch for EURUSD:

Resistance Levels:

- 1.1540 to 1.1570 Momentum Pivot (4H 50-MA and Channel top)

- Resistance 1.16250 to 1.16350

- 1.1650 to 1.17 March Resistance

Support Levels:

- 1.1475 to 1.15 November Support

- August 2025 Lows 1.14

- Channel lows 1.35670

USD/CHF 4H Chart and technical levels

USD/CHF 4H Chart, March 17, 2026, Source: TradingView

FOMC Levels to watch for USD/CHF:

Resistance Levels

- 0.7850 2025 lows Pivotal Resistance (Bullish Above – testing)

- Recent highs 0.79310

- 0.7950 Minor Resistance

- 0.80 Next resistance

Support Levels

- 4H 50-period MA 0.7827

- 0.7780 to 0.78 Momentum Pivot

- 0.77 to 0.7725 August 2011 Lows Support

- 0.76 Support zone July 2011

GBP/USD 4H Chart and trading levels – Reaching 2025 highs

GBP/USD 4H Chart, March 17, 2026, Source: TradingView

FOMC Levels to watch for GBPUSD:

Resistance Levels

- 50-period MA 1.33540 (immediate test)

- Key pivot 1.34 to 1.3440

- 4H 200-period MA 1.3508

- December Resistance 1.36

Support Levels

- Pivotal Support 1.33 - 1.3340

- 1.3120 December Support

- End 2025 Support at 1.30 Zone (+/- 300 pips)

USD/CAD 4H Chart and trading levels – Reaching 2025 highs

USD/CAD 4H Chart, March 17, 2026, Source: TradingView

Levels to watch for USD/CAD:

Resistance Levels

- 1.3750 Pivotal Resistance (Recent rejection)

- 1.37418 weekly highs

- 1.38 Handle Resistance +/- 150 pips

Support Levels

- 1.3630 to 1.3660 Mid-Range Pivot

- 1.3550 to 1.3570 Main 2025 Support

- 1.35 Key Psychological Support – Pre-2025 CAD weakening level

- 1.34 Next Main Support

Happy Saint-Patrick and Safe Trades as the FOMC approaches!

FOMC Meeting Preview: A ‘Hawkish Hold’ as Geopolitical Risk & Stagflation Fears Rise, Implications for DXY & Dow Jones

- The Federal Reserve is expected to deliver a "hawkish hold."

- The Summary of Economic Projections (SEP) is anticipated to show higher inflation forecasts and a risk that the one expected 2026 rate cut could be pushed into 2027.

- Market implications include an extended rally for the US Dollar Index (DXY) and a "risk triangle" for the Dow Jones Industrial Average due to elevated yields, margin squeeze from oil prices, and geopolitical uncertainty.

As the Federal Open Market Committee (FOMC) prepares to convene on March 18, 2026, the economic landscape has shifted from "normalization" to a complex "wait-and-see" puzzle.

Chair Jerome Powell now faces a dual-mandate nightmare: a cooling labor market clashing with a renewed energy-driven inflation shock after the conflict in the Middle East.

The Decision: Inflation vs labor market

Market consensus is overwhelmingly aligned: the Federal Reserve is expected to keep the federal funds rate unchanged at its current level. While the Fed entered 2026 with a dovish tilt, the escalating conflict in the Middle East has sent oil prices surging, complicating the path toward the 2% inflation target.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Recent data has been contradictory. A "train wreck" of a February jobs report, which saw payrolls fall by roughly 92,000 and unemployment climb to 4.4%, suggests the economy needs support.

However, with PCE inflation stuck near 3% and energy costs rising, the Fed cannot risk a premature cut that might unanchor inflation expectations.

The persistence of inflation is being driven by more than just energy. Food prices are expected to jump due to a surge in fertilizer costs related to the Middle East conflict, and manufactured goods are seeing "downstream" price increases.

Furthermore, inflation expectations, which had previously been well-anchored, have shown signs of an "uptick," providing the committee with a primary justification for pushing out rate cut expectations until 2027.

The Dot Plot: Shifting projections

The Summary of Economic Projections (SEP) will be the focal point for investors. While the December "dots" hinted at one rate cut in 2026, there is a distinct risk that this could be pushed into 2027.

Analysts suggest a "stagflationary" shift in the SEP:

- GDP: Likely revised marginally lower for 2026 following a weak Q4 2025.

- Inflation: Projections for 2026 and 2027 are expected to edge higher to reflect higher energy costs and stickier core components.

- Rate Path: The median dot may remain unchanged for now, but the "balance of risks" is tilting hawkish. The Fed may signal that while two cuts (potentially June and September) remain on the table, they are increasingly data-dependent.

The impact of Powell’s potential departure

The question around the Fed Chair position remains an intriguing one. Current Fed Chair Jerome Powell has indicated through his attorneys that he feels bound to remain on the Board of Governors for the duration of the investigation to defend the Fed’s independence.

Traditionally, Fed chairs resign from the board once their term as chair expires, but Powell’s decision to stay could prevent President Trump from "packing" the board with more dovish governors. This leadership vacuum creates a "lame duck" period where the market is uncertain about who will be setting interest rates by the summer of 2026.

The political pressure on the Fed is also mounting. President Donald Trump has publicly criticized Chair Powell and called for an emergency meeting to slash rates.

This external pressure, combined with the legal challenges facing the chair, threatens to undermine the market’s perception of the Federal Reserve as an independent, data-driven institution.

For professional investors, this means that every policy decision must now be weighed against the potential for political interference or leadership turnover.

Market Implications – US dollar index

The US Dollar Index (DXY) has found renewed support in recent weeks, and a "hawkish hold" from the Fed could extend this rally. The "safe-haven" appeal of the Dollar is being bolstered by Middle East tensions, while tighter financial conditions are acting as a shield for American consumers against rising oil prices.

Furthermore, a policy divergence is emerging. While markets are flirting with the idea of rate hikes from the ECB and BoE to combat energy-driven inflation, the Fed’s ability to remain "higher for longer" compared to its peers should maintain the Dollar’s yield advantage.

If Powell emphasizes the need to keep rates restrictive until the energy supply uncertainty persists, the DXY could break toward the 106.00 level.

US Dollar Index (DXY) Chart, March 17, 2026

Source: TradingView.Com (click image to enlarge).

Implications for the Dow Jones

For the Dow Jones Industrial Average, the March meeting presents a "risk triangle" involving yields, oil prices, and geopolitical headlines.

Growth Concerns: Lower GDP revisions and a softening labor market are headwinds for industrial and consumer discretionary stocks.

Margin Squeeze: Rising energy costs increase input prices for major Dow components, potentially squeezing corporate earnings.

Interest Rates: If the SEP removes the prospect of near-term easing, the "higher-for-longer" narrative could trigger a pullback in equities as discount rates remain elevated.

Historically, the Dow dislikes uncertainty. A clear signal that the Fed is "holding steady" rather than reacting aggressively to the oil spike might provide a relief rally, but any hint of a potential rate hike—a tail risk mentioned by some hawkish governors would likely trigger a sharp sell-off.

The "Governance Discount": Market participants are becoming worried about political friction in Washington. Specifically, public disagreements between the White House and the Federal Reserve make people feel the central bank might lose its independence. This makes the dollar seem like a riskier place to keep money.

Dow Jones Daily Chart, March 17, 2025

Source: TradingView.Com (click image to enlarge).

Outlook: Powell’s Toughest Balancing Act

Chair Powell’s press conference will likely emphasize that the Fed is "not under pressure to make quick changes." By acknowledging the two-sided risks of the energy shock, inflationary on one hand, growth-dampening on the other, the Fed will seek to maintain a neutral stance.

For market participants, the takeaway is clear: the era of predictable, synchronized rate cuts has ended. The March 18 meeting will likely confirm that while the Fed's bias remains toward eventual easing, the "geopolitical tax" of the Iran conflict has significantly raised the bar for the next move.

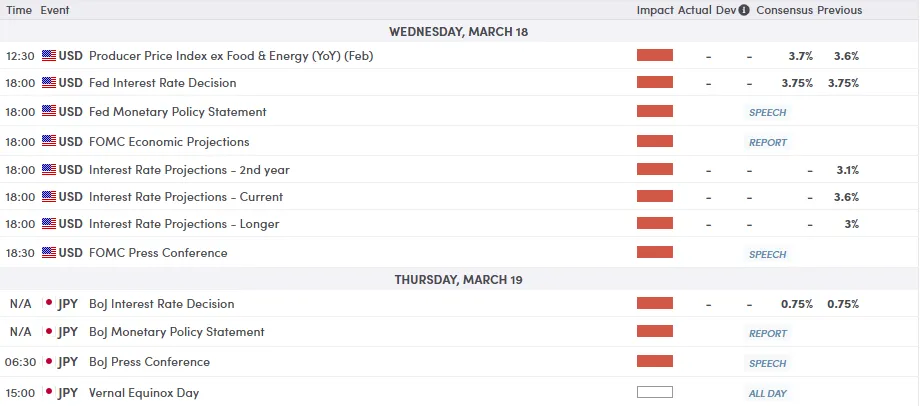

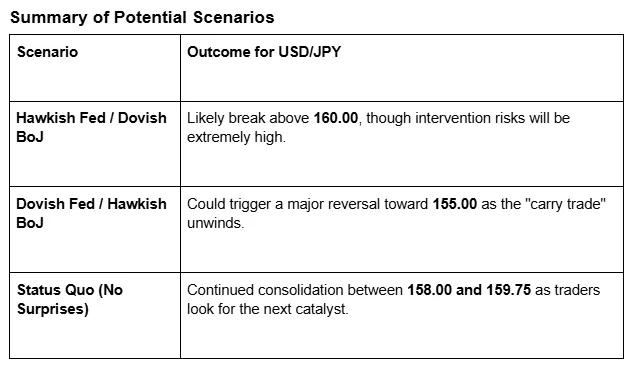

USD/JPY Conundrum: Intervention Risk Looms as Central Banks Meet (Fed-BoJ Double-Header)

- The USD/JPY pair is trading around 158.90, facing a high risk of FX intervention by the Japanese Ministry of Finance as it nears the 160.00 level.

- The week is dominated by a "central bank double-header," with the Federal Reserve meeting on Wednesday and the Bank of Japan meeting on Thursday.

- Check out the possible scenario matrix i have put together. What would a BoJ and Fed hawkish tilt mean?

USD/JPY is caught in a real conundrum at present and continues to edge lower ahead of a crucial pair of central bank meetings. The pair trades at 158.90 right now as the 160.00 handle still remains elusive.

The question that is also keeping markets on edge with USD/JPY is the potential for FX intervention as both the FED and BoJ would like to see USD/JPY lower. For different reasons of course but this appears to be the case.

Looking at the longer term bullish trend which still remains intact, it has been largely supported by the gap between US and Japanese bond yields. This remains a key factor that will play a role moving forward.

While the USD is currently overbought, buyers remain in control as long as the Fed stays hawkish and the BoJ remains relatively loose.

With these more longer term factors playing out, focus will shift back to the now. The rest of this week will be key and could be the deciding factor in whether FX intervention by the Japanese Ministry of Finance will support the Yen.

What to watch for the rest of the week

The week ahead is dominated by a "central bank double-header" that will likely determine the next major trend for USD/JPY.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar.

The Federal Reserve (Wednesday, March 18)

The Decision: The Fed is widely expected to hold interest rates steady at 3.75%.

The Impact: The real movement will come from the "Dot Plot" (projections for future rate cuts). If the Fed signals fewer cuts for 2026 due to sticky inflation (currently around 3.1%), the US Dollar could surge, potentially testing the 160.00 level against the Yen

The Bank of Japan (Thursday, March 19)

The Decision: The BoJ is forecast to keep its policy rate at 0.75%.

The Impact: Markets will look for the BoJ’s assessment of rising energy costs. If the BoJ sounds concerned that high oil prices are hurting the economy, they may delay further rate hikes, which would weaken the Yen. However, any hint of a "hawkish" shift to combat inflation could trigger a sharp pullback in USD/JPY.

Below I have compiled my own matrix for potential scenarios depending on how the Central Bank meetings turns out. Obviously this is not a given and it is just my personal opinion, as high volatility is likely a given especially if we trade near the 160.00 level ahead of either meeting.

Created by Zain Vawda

USD/JPY Daily Chart, March 18, 2026

Source: TradingView (click to enlarge)

Head and Shoulders in WTI! Is the rally over for Crude Oil? Stock Markets Mixed ahead of FOMC

Welcome to a more unusual Market update to show what could be a significant development for Markets for periods ahead.

WTI Crude Oil is forming a Head & Shoulders ahead of the FOMC meeting, a first bearish pattern since the beginning of the War.

WTI Oil 2H Chart. March 17, 2026 – Source: TradingView

It sure is a risky, counter-trend, and counter-Market view, but here are the elements that could point towards the end of a WTI Rally.

First and foremost, advancements in the War:

Most of the key figures of the Iranian Islamic Regime have been eliminated throughout the first three weeks of the conflict, leaving a snake without its head for the authoritarian regime.

Overnight, Ari Larijani, the right-hand of the Ayatollah, along with Basij Forces Commander Soleimani, was eliminated in strikes.

These two figures were exercising heavy influence over the IRGC army for the former and the Political police for the latter.

This could prove to be a turning point in the ongoing US-Iran-Israel War.

The two-country coalition is now expressing more concrete plans to move further towards the securitization of the Strait of Hormuz.

If even Al Jazeera is saying that the US-Israel operation is working, the War could really avoid dragging out for long – this fundamental turn should ease pressure on the Crude Market.

While supply issues remain, particularly for Asian nations, less uncertainty often translates to easier Market conditions ahead.

Oil won't just flash back to the $55 lows from the beginning of the year, but less pressure on the head will help soothe Participants and inflation expectations.

Second, technical elements:

WTI Oil gapped higher to $101.30 at the weekly Open, which could have added further momentum to an already tense Market.

But the selling seen in the previous session formed a Head & Shoulders pattern. It is a strong sign of trend exhaustion, as bulls attempted to break previous highs but failed twice, also forming a lower high at the same time (overnight spike to $99).

The measured move target would hint at $85 oil in the short run. More advancements to the conflict would be required to sustain a more persistent correction in the commodity.

The pattern is invalidated if bulls close above $99.04 (overnight highs).

Keep a close eye on the 2H 50-period MA ($95.19), which is acting as short-term support. Breaking it could trigger the selloff.

Technical Levels for WTI

Resistance Levels

- 99.04 Overnight highs (H&S Void above)

- $98 to $100 Resistance

- $106 to $108 June 2022 Resistance

- War highs $116 to $120

Support Levels

- Immediate Support 2H 50-MA $95.17 (bearish below)

- H&S Neckline $92.64

- $85 Head & Shoulders Target

- 2025 Highs Key Support $78 to $80

- $69 to $70 Main Support

- 2025 lows $55.00

Stock Markets are sending Mixed signs

Current picture for the Stock Market (12:03 A.M. ET) – Source: TradingView – March 17, 2026

The Stock Market is all over the place today.

After the overnight failed spike in Oil, Stock Indexes opened well but have failed to sustain momentum and are now correcting again.

Participants will be awaiting further clarity from tomorrow's Fed Meeting – The Summary of Economic Projections will be released, providing at least more clarity on what to expect from the Fed in 2026.

An FX and Fundamental preview for the event will be landing this afternoon.

Markets will be all eyes and ears to listen to what Jerome Powell has to say during one of his final press conferences tomorrow at 14:30.

Dow Jones 1H Chart and Trading Levels

Dow Jones (CFD) 1H Chart – March 17, 2026 – Source: TradingView

The Dow Jones rejected the upper bound of its descending channel, opening the way for a more mixed price action ahead – 47,000 is the level to watch for the FOMC (Bullish if close above, bearish if close below).

Expect slow trading all the way towards tomorrow's 14:00 Decision.

Dow Jones technical levels for trading:

Resistance Levels

- Morning highs 47,429

- Pivotal Resistance 47,400 to 47,600

- Key Resistance at 48,000 (bull above)

- 48,400 to 48,500 mini-resistance

Support Levels

Key Pivot 47,000

- Current War lows Mini-Support 46,300 and past day Double Bottom (bearish below)

- 46,000 +/- 100 pts November Support

- August highs 45,715

- 45,000 psychological level (Main Support on higher timeframe)

Safe Trades and keep a close eye on the US-Iran developments!

Gold Continues to Pressure Strong $5000 Support

Gold price remains at the back foot on Tuesday and continues to pressure key $5000 support zone (recent range floor / psychological / top of thin ascending daily cloud) after Monday’s attack failed to register sustained break lower.

Broader bulls remain on hold with the price holding around the mid-point of $5598/$4402 corrective pullback, as global uncertainty keeps the metal underpinned, but dollar became more popular due to growing threats of fresh inflation rise over escalating Middle East crisis and oil shock on disruption of supply through Hormuz strait.

The yellow metal is likely to hold in prolonged range trading but expected to keep bullish bias, with main economic event this week being FOMC policy decision.

The Fed is widely expected to stay on hold at Wednesday’s meeting, but policymakers will continue to closely monitor developments.

I don’t expect significant impact from the Fed meeting (if decision remains within expectations) and remain focused on $5000 support.

Near term structure would weaken on firm break here and bring in focus targets at $4910/00 (50% retracement of $4402/$5419 recovery leg / 55DMA / round-figure) and $4841 (Feb 17 higher low) in extension. Bearishly aligned daily studies (negative momentum / Tenkan / Kijun-sen bear-cross) support scenario.

Conversely, ability to hold above $5000 would keep slight bullish bias, though bounce above minimum $5100 would be needed to neutralize immediate downside threats.

Res: 5038; 5100; 5124; 5179

Sup: 4967; 4940; 4900; 4841

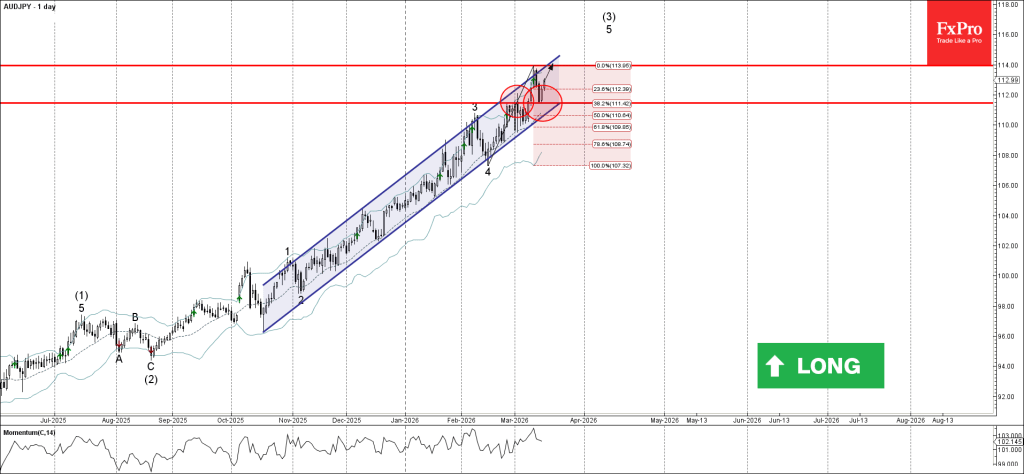

AUDJPY Wave Analysis

AUDJPY: ⬆️ Buy

- AUDJPY reversed from support area

- Likely to rise to resistance level 114.00

AUDJPY recently reversed from the support area between the support level 111.45 (former resistance from February), 20-day moving average and the 38.2% Fibonacci correction of the upward impulse from February.

The upward reversal from this support zone continues the active impulse waves 3 and (5).

Given the strong daily uptrend, AUDJPY can be expected to rise to the next resistance level 114.00 (which reversed the pair at the start of March).

Eco Data 3/18/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q4 | -5.98B | -4.85B | -8.37B | -8.36B |

| 23:30 | AUD | Westpac Leading Index M/M Feb | -0.10% | -0.04% | 0.00% | |

| 23:50 | JPY | Trade Balance (JPY) Feb | -0.37T | -0.61T | 0.46T | 0.50T |

| 08:00 | CHF | SECO Economic Forecasts | ||||

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 1.90% | 1.90% | 1.90% | |

| 10:00 | EUR | Eurozone Core CPI Y/Y Feb F | 2.40% | 2.40% | 2.40% | |

| 12:30 | USD | PPI M/M Feb | 0.70% | 0.30% | 0.50% | |

| 12:30 | USD | PPI Y/Y Feb | 3.40% | 2.90% | 2.90% | |

| 12:30 | USD | PPI Core M/M Feb | 0.50% | 0.30% | 0.80% | |

| 12:30 | USD | PPI Core Y/Y Feb | 3.90% | 3.70% | 3.60% | |

| 13:45 | CAD | BoC Interest Rate Decision | 2.25% | 2.25% | 2.25% | |

| 14:00 | USD | Factory Orders M/M Jan | 0.10% | 0.40% | -0.70% | |

| 14:30 | USD | Crude Oil Inventories (Mar 13) | 6.2M | -1.5M | 3.8M | |

| 18:00 | USD | Fed Interest Rate Decision | 3.75% | 3.75% | 3.75% | |

| 18:30 | USD | FOMC Press Conference |

| 21:45 | NZD |

| Current Account (NZD) Q4 | |

| Actual | -5.98B |

| Consensus | -4.85B |

| Previous | -8.37B |

| Revised | -8.36B |

| 23:30 | AUD |

| Westpac Leading Index M/M Feb | |

| Actual | -0.10% |

| Consensus | |

| Previous | -0.04% |

| Revised | 0.00% |

| 23:50 | JPY |

| Trade Balance (JPY) Feb | |

| Actual | -0.37T |

| Consensus | -0.61T |

| Previous | 0.46T |

| Revised | 0.50T |

| 08:00 | CHF |

| SECO Economic Forecasts | |

| Actual | |

| Consensus | |

| Previous | |

| 10:00 | EUR |

| Eurozone CPI Y/Y Feb F | |

| Actual | 1.90% |

| Consensus | 1.90% |

| Previous | 1.90% |

| 10:00 | EUR |

| Eurozone Core CPI Y/Y Feb F | |

| Actual | 2.40% |

| Consensus | 2.40% |

| Previous | 2.40% |

| 12:30 | USD |

| PPI M/M Feb | |

| Actual | 0.70% |

| Consensus | 0.30% |

| Previous | 0.50% |

| 12:30 | USD |

| PPI Y/Y Feb | |

| Actual | 3.40% |

| Consensus | 2.90% |

| Previous | 2.90% |

| 12:30 | USD |

| PPI Core M/M Feb | |

| Actual | 0.50% |

| Consensus | 0.30% |

| Previous | 0.80% |

| 12:30 | USD |

| PPI Core Y/Y Feb | |

| Actual | 3.90% |

| Consensus | 3.70% |

| Previous | 3.60% |

| 13:45 | CAD |

| BoC Interest Rate Decision | |

| Actual | 2.25% |

| Consensus | 2.25% |

| Previous | 2.25% |

| 14:00 | USD |

| Factory Orders M/M Jan | |

| Actual | 0.10% |

| Consensus | 0.40% |

| Previous | -0.70% |

| 14:30 | USD |

| Crude Oil Inventories (Mar 13) | |

| Actual | 6.2M |

| Consensus | -1.5M |

| Previous | 3.8M |

| 18:00 | USD |

| Fed Interest Rate Decision | |

| Actual | 3.75% |

| Consensus | 3.75% |

| Previous | 3.75% |

| 18:30 | USD |

| FOMC Press Conference | |

| Actual | |

| Consensus | |

| Previous | |

Sunset Market Commentary

Markets

Tomorrow’s FOMC meeting has been somewhat overlooked recently. The US central bank started 2026 on the back of three consecutive 25 bps rate cuts as downside employment risks warranted pre-emptive action on the notion that monetary policy could move from restrictive to neutral given falling upside inflation risks and strengthening confidence in the inflation outlook. At the start of the year, the Fed shifted to a wait-and-see mode as the labour market showed signs of stabilization. The equilibrium is precarious as a shrinking labour supply (immigration crackdown) balances the unemployment rate against relatively weak job growth, but it’s an equilibrium still. This allowed the Fed to switch the needle back to (goods) inflation which has been on the rise since US President Trump’s protectionist trade agenda got installed. The Fed’s preferred core PCE deflator accelerated from a 2.6% Y/Y low last year in April to 3.1% in January (highest since March 2024). These developments even urged uber-dove and Trump-disciple Miran into acknowledging that he would raise his end-of-year projection for the Fed funds rate from a 2-2.25% low in the dot plot to 2.5%-2.75% which would ceteris paribus still be the low point by the way. In the December dot plot, the median forecast projected room for one additional 25 bps rate cut over the course of 2026 and another one in 2027.

7 out of 19 Fed members in December already flagged a preference to hold rates steady over 2026. Minutes of the January FOMC meeting showed that several participants would’ve supported two-sided language on the rate path, putting the door open fore a rate hike if necessary. They also cautioned that easing policy further in the context of elevated inflation readings could be misinterpreted as implying diminished commitment to the 2% inflation objective. The start of the US-Israeli war against Iran adds to upside inflation risks in first instance through the energy channel. US diesel retail prices today hit $5/gallon for the first time since December 2022 compared to half of that price ahead of the war. Our in-house nowcast shows that, if petrol prices ($4.33 currently) join diesel in surpassing this psychological mark, PCE and CPI inflation would rise to 3.8% and 4% respectively by April. This compares with the latest prints of 2.8% (PCE, January) and 2.4% (CPI, February). That scenario also raises the risk of secondary effects on top of those stemming from tariff/goods inflation. In this context, it is very unlikely that the policy statement, the quarterly projections or Fed Chair Powell’s press conference will still pave the way for a rate cut this year. At the end of February, US money markets discounted 2.5 rate cuts by December with the policy rate bottoming out around 2.75%-3% next year. Now, Fed funds futures only discount one Fed rate cut this year which would most likely be the final one than this cycle but might be pushed further in time. That leaves more room for repositioning in bear flattening fashion especially as we don’t exclude inflation hawks to put rate hikes in their forecasts. Such hawkish outcome would add to overall USD strength since the beginning of March, denting risk sentiment.

News & Views

The Swiss National Bank barely, if any, intervened in FX markets in the final quarter of last year, data from its annual report revealed today. The central bank over the course of 2025 bought FX worth CHF 5.2bn but earlier data showed that the tally already stood at CHF 5.18bn after the first nine months of last year. The bulk occurred in Q2, after US president Trump unveiling his tariff plan sparked haven flows to the Swiss franc. The Iran war that erupted early March did the same, luring SNB officials from the shadows to signal their willingness to intervene in the market, if needed. The strong franc has always been a key focus for the SNB since it dampens imported inflation, especially at a time where it is already at the low end of the 0-2% target. The central bank is meeting on Thursday with EUR/CHF just inches away from the 0.90 record low (barring the 2015 episode) seen in early March.

The EU’s foreign policy chief Kaja Kallas has pushed back against a call by Belgian PM De Wever to normalize (trade) ties with Russia and regain access to cheap Russian energy. In an exclusive interview with Reuters, Kallas said she doesn’t see the appetite De Wever sees in other EU leaders to do so, adding that “if we go back to business as usual, we will have more of this, more wars.” Since the Ukraine war, Dutch TTF gas futures have settled at structurally higher levels than before. The Middle East conflict pushed prices to the highest since February 2025.