Sample Category Title

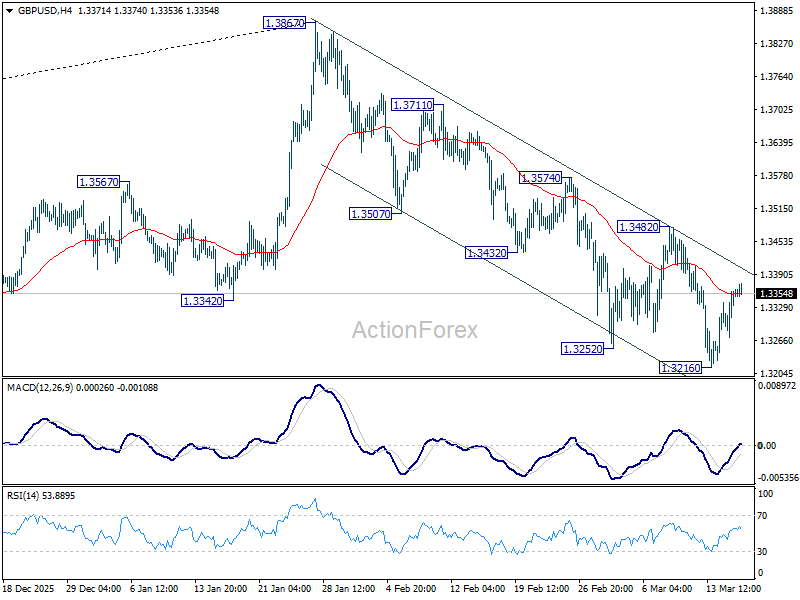

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3298; (P) 1.3332; (R1) 1.3390; More...

Intraday bias in GBP/USD stays neutral at this point. Consolidations from 1.3216 could extend further. But risk will stay on the downside as long as 1.3482 resistance holds. Below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. Firm break there will carry larger bearish implication and target 1.2524 fibonacci level.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

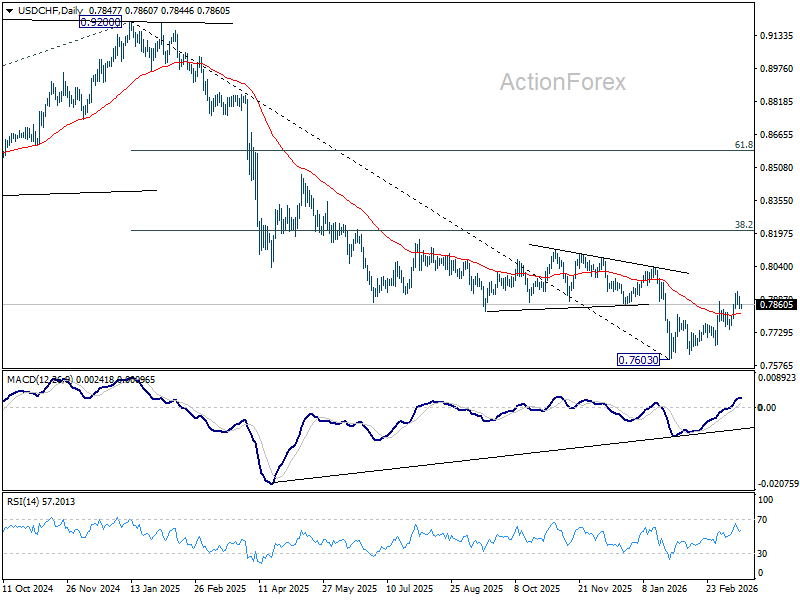

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7853; (P) 0.7888; (R1) 0.7913; More….

Intraday bias in USD/CHF remains neutral and more consolidations could be seen below 0.7921. Further rally is still expected as long as 0.7746 support holds. Rise from 0.7603 is seen as correcting whole down trend from 0.9200. Break of 0.7921 will target 38.2% retracement of 0.9200 to 0.7603 at 0.8213.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8091) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

Risk Probably for Fed Guidance to be Still More Hawkish

Markets

There was little ‘real’ market relevant news from the conflict in the Middle East, yesterday. There was hardly any progress on ideas/strategies to secure a passage through the Strait of Hormuz. Visibility on how and when the conflict might end also remains close to non-existent. With higher energy prices the major economic fall-out, markets now might move to a position where oil prices in the vicinity of $100-105 p/b are somewhat of a short-term anchor point/new normal which is more or less priced in. In technical trading yields US yields didn’t show any clear directional trend with yields changing between +0.25 bps (2-y) and -2.6 bps (30-y). German yields at the same time ceded between 1.9 bps (2-y) and -4.2 bps (30-y). The reaction function of bond markets currently is far from unequivocal, but given market sensitivity to inflation risk premia and to a lesser extent, fiscal risk premia, a bull flattening of the curve currently probably should be seen as a sign of tentative easing of market stress. In this context, it coincided with modest equity gains for the second consecutive day (S&P +0.25% ; Eurostoxx 50 +0.53%). In the same move, the dollar corrected slightly further (DXY from 99.87 to 99.58; EUR/USD from 1.1505 to 1.1540, USD/JPY marginally lower at 159).

The starting point today is similar when looking at the situation in the Middle East. (Brent) oil ($100.8), US yields and the dollar (DXY 99.45, USD/JPY 158.75) are easing a bit further. Asian equities are recovering (Nikkei +2.77%). In the absence of ‘new news’ from the Middle East the focus later today might turn to the Fed policy decision, new quarterly projections (dots) and the assessment from Fed Chair Powell at the press conference. Of course, any Fed scenario thinking also remains highly conditional on event risk/energy price scenarios. Even so, recent developments (higher oil prices potentially pushing PCE/CPI inflation to the 3.5%+ area) might cause at least some governors to abstain from guidance on future interest rate cuts. In the December dots, 7 out of 19 Fed members already indicated interest rates staying unchanged throughout 2026. So not that much is need for tipping this balance to an unchanged median dot. US money markets still discount one additional Fed rate cut by year end (compared to 2.5 cuts before the start of the war). The risk probably is for Fed guidance to be still more hawkish compared to current market pricing, suggesting room for some further bear flattening. Such an outcome would add to overall USD strength since the beginning of March, potentially denting risk sentiment.

News & Views

February trade data published by the Japanese Ministry of Finance this morning showed export (value) rising by 4.2% Y/Y (from +16.8% in January). A significant increase of export to the EU (+14% Y/Y) offset declines to the US (-8% Y/Y) and China (-10.9% Y/Y). Towards the US, tariffs especially weighed on car shipments. When it comes to China, the timing of Lunar NY might have distorted the data. Japanese imports (value) increased by 10.2% Y/Y (from -2.6% Y/Y in January) with especially import growth from Asia (+16.2% Y/Y) and China (+33.3% Y/Y) increasing rapidly. Imports from the EU were down 2% Y/Y. On a seasonally adjusted basis, the trade balance swung from an exceptional JPY 499.1bn surplus in January to a JPY 374.2bn deficit in February.

New Zealand consumer confidence has taken a knock in Q1, albeit only a small one at this stage. The Westpac-McDermott Miller index fell from 95.5 to 94.7 with levels below 100 indicating that there are more households pessimistic about economic conditions than optimistic. Surveys were conducted during the first two weeks of March. Improving domestic conditions (improving financial positions thanks to continued strength in export commodity prices like dairy and a large drop in borrowing costs) have been over taken by more worrying global events. The outbreak of war in the Middle East sent local fuel costs already sharply higher with spillover to other costs like airfares. The longer the conflict continues, the larger the resulting disruptions to economic activity and pressure on households' finance will be.

Up and Down

On Tuesday, crude oil pushed higher as Middle East tensions escalated following reports of the killing of senior Iranian figure Ali Larijani. Experts suggested this could prompt Iran to intensify attacks on Gulf countries.

This morning, oil is sharply down on news that Iraq signed a deal to resume oil exports via Turkey, bypassing the Strait of Hormuz, while Saudi Arabia is also rerouting exports toward the Red Sea. The region is reorganizing, preparing for the possibility of a prolonged conflict. Restoring oil exports fully will take time, and we may soon see physical-market shortages — likely keeping oil prices under upward pressure. Yet, as flows adapt to alternative routes, the initial surge in oil prices seen at the start of the war could ease.

This matters for global economies already pressured by higher energy costs and rising hawkish central bank expectations.

Yesterday, the Reserve Bank of Australia (RBA) raised rates for the second consecutive month to counter inflationary pressures exacerbated by the Middle East conflict.

Today, the Federal Reserve (Fed) is expected to hold rates steady while revising growth and inflation projections. Recent data show US price pressures had been building even before the latest spike in oil prices, suggesting challenging months ahead. The Fed will need to decide whether to look through these pressures, assuming they are short-lived, or act by signaling no rate cuts in the foreseeable future.

The US Dollar is weaker this morning against major currencies, pulled down by the sharp fall in oil prices. The EURUSD consolidates gains above 1.15, while the USDJPY retreats from the problematic 160 level. On the index front, the Nikkei is up over 1%, Kospi rallies almost 5%, and US and European futures point to an encouraging start.

Oil prices remain the common denominator for global risk appetite: the lower and more sustainable, the better. Yet, the lack of a near-term resolution will keep oil markets volatile. The longer uncertainty lasts, the bigger the impact on physical availability and the harder it will be to bring prices back to pre-war levels.

Rising energy prices are not the only inflationary risk — they are the major one, affecting everything from agricultural and industrial goods to transportation and services. There are also US tariffs, and AI competing with local communities for resources such as electricity — and, in some regions, water — further threatening price pressures.

Inside tech, the memory chip shortage — aggravated by high and growing AI demand — has pushed the industry into a deep crunch since last year, a shortage that SK Hynix expects to persist over the next four years. This will likely push electronics prices higher and squeeze margins for producers, including PC, smartphone, car, appliance and TV manufacturers.

Earnings from Micron Technology are due today after the bell, and expectations are sky-high. Analysts forecast revenue of around $19 billion — more than double year-on-year — and EPS in the $8.5–$9 range, a more than fivefold increase versus last year. The surge is driven by AI-related memory chip demand, with tight supply continuing to push prices and margins. The key question is whether results can beat already elevated expectations and support further gains, after the stock hit a fresh ATH above $462 per share yesterday.

China is where the AI action is heating up, particularly with OpenClaw, an open-source agent framework capable of executing tasks rather than just answering questions. This shift from AI assistants to agentic AI — highlighted by Nvidia CEO Jensen Huang earlier this week — has triggered a race among Chinese tech giants. Alibaba is integrating agent tools into enterprise platforms, while Tencent is embedding them across WeChat and its cloud ecosystem. AI agents drive cloud demand, enhance platform stickiness, and create new enterprise revenue streams. Investors are reacting fast: MiniMax, a smaller Chinese AI player with its own OpenClaw-based agent, surged more than 20% in Hong Kong today.

In the US, Google and Meta Platforms are also investing heavily in agentic AI. Meta trades more than 20% below its August ATH, with a PE near 21, while Google is down 15% with a PE above 33. A deeper pullback will attract bargain-seekers, but investors must look past the massive investment plans increasingly relying on debt.

Fed to Wait and See and Energy Shock Clouds Economic Outlook

In focus today

- Focus remains on the Middle East, particularly on Iran's response to Israel killing its top security chief and the potential repercussions for global energy markets.

- The main event will be the FOMC meeting tonight. We and markets expect no monetary policy changes. Markets are still pricing in one more rate cut later in the year, while we call for two. US February PPI data will be released in the afternoon ahead of the rate decision.

- In the afternoon, focus turns to the Bank of Canada meeting at 14:45 CET - where we, in line with consensus, expect the policy rate to remain on hold at 2.25%. Note that this is an interim meeting without a new Monetary Policy Report, so focus will be on the tone of forward guidance.

- We also receive final February inflation data for the eurozone ahead of ECB's policy rate decision tomorrow. Inflation figures are expected to confirm flash estimates.

Economic and market news

What happened yesterday

In the conflict in the Middle East, the Israeli military (IDF) killed Iran's top security chief, Ali Larijani, a key figure in Iran's political and military establishment, along with Gholamreza Soleimani, leader of the Basij militia within the IRGC. In response, Iran launched missile strikes on Tel Aviv overnight. Mojtaba Khamenei reiterated that he rejects proposals for reducing tensions or agreeing to a ceasefire, declaring that peace would not be pursued until the US and Israel "accept defeat and pay compensation".

The political pressure on Trump intensifies as Joe Kent, the director of the US National Counterterrorism Centre, resigned in protest of the Iran war. Trump stated on Tuesday that the US will end its military operation in Iran "in the near future" but emphasised that withdrawal is not yet imminent.

In the Oil market, the biggest news overnight was a deal between Iraq and the Kurds to reroute some oil via pipeline through the Kurdish region and further to Turkey. On the margin, it will relieve a little of the pressure on the oil market and Iraqi economy. The oil price was fairly steady overnight just above USD100/bbl.

In Germany, the ZEW index surprised in March with the assessment of the current situation rising in contrast to consensus estimates while expectations for future growth fell much more than expected. The assessment of the current situation increased to -62.9 (cons: -68.0, prev.: -65.9) and expectations declined to -0.5 (cons: 39.2, prev.: 58.3). The decline in expectations was historically large and of similar magnitude as the decline last year after Liberation Day and in the first months of Covid. The decline in growth expectations highlights the dilemma that the ECB faces of lower growth expectations amid higher prices.

Equities: Equities moved higher again yesterday, with a familiar intra-day pattern: sentiment improved through the European and US cash sessions. On the surface, price action pointed to stronger risk appetite, equities higher, cyclicals outperforming defensives, min vol underperforming and VIX drifting lower.

However, the cross-asset signal remains more nuanced. Oil prices did not decline yesterday, which breaks the typical geopolitical "risk-on = lower oil" relationship.

This suggests that markets are not pricing a full de-escalation scenario. Instead, investors appear to be gradually adapting to a prolonged conflict backdrop, supported by increasing evidence that oil supply, while constrained, continues to flow out of the Middle East.

Within equities, the US session in particular saw a more pronounced cyclical rotation. Notably, consumer cyclicals have started to recover after massively underperforming the last 6 months. This morning, the positive tone continues across Asia, led by South Korea (+5% at the time of writing). US and European futures are also higher. Importantly, oil is declining this morning, providing an additional tailwind for risk assets compared to the previous session.

FI and FX: EUR/USD shifted back above 1.15 yesterday amid declining UST yields and cautiously recovering risk sentiment. We do not expect tonight's FOMC meeting to be a game changer for EUR/USD, as the Fed remains in a comfortable position to just wait-and-see how the war in Iran evolves. Before that, we expect the BoC to stay on hold. The CAD remains resilient among G10 currencies against the USD, supported by Canada's net-energy exporter status. However, risk-off sentiment and broader USD strength have kept USD/CAD rangebound between 1.36-1.37. Yesterday, our tactical trade to face recent NOK strength hit its stop, and we stay on the sidelines for now in Norway, awaiting the central bank meetings and the Regional Network survey tomorrow.

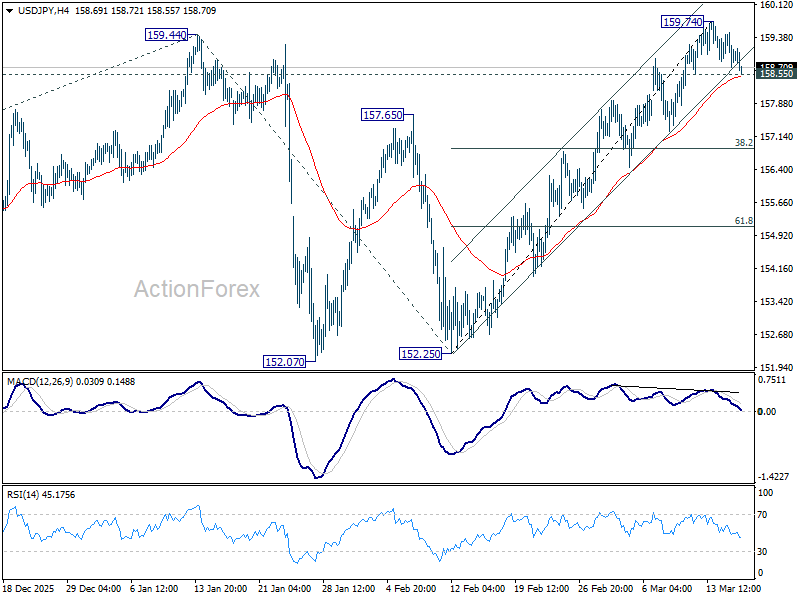

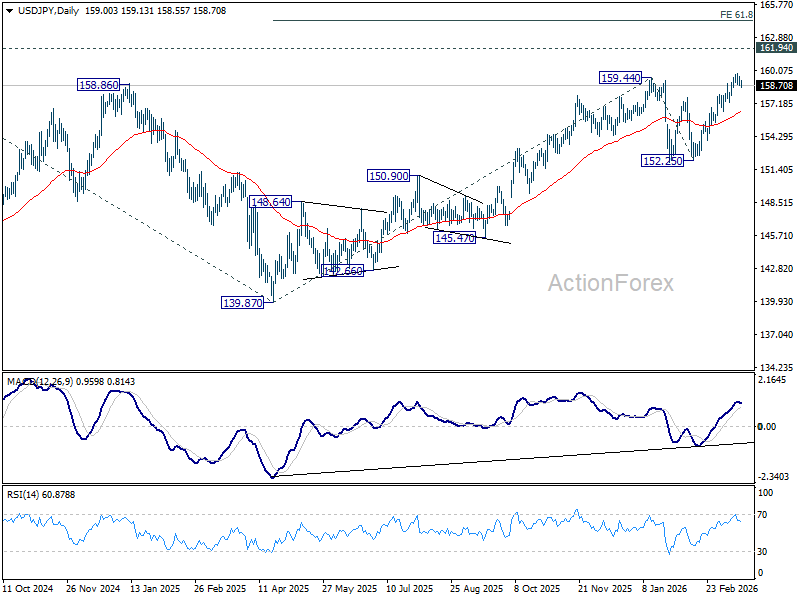

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.65; (P) 159.07; (R1) 159.43; More...

Intraday bias in USD/JPY remains neutral for the moment. Considering bearish divergence condition in 4H MACD, break of 158.55 should indicate short term topping. Intraday bias will then be back on the downside for 38.2% retracement of 152.25 to 159.74 at 156.87. Nevertheless, strong bounce from current level, followed by break of 159.74, will target a retest of 161.94. Firm break there will confirm larger up trend resumption and target 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

Markets Steady as War Fatigue Sets In, Focus Shifts to Fed and Global Central Banks

Markets were steady in Asian session today, with equities posting modest gains led by Japan, as investors showed signs of “war fatigue” amid the ongoing Middle East conflict. Despite continued escalation between Iran, Israel and the U.S., price action across major asset classes has become increasingly muted, suggesting that geopolitical risks are not the dominant driver of near-term market moves, at least for now.

The latest developments saw Iran intensify attacks on Israel and U.S. assets in the region, following Israel’s killing of Iran’s security chief Ali Larijani, head of the Supreme National Security Council. While such escalation would typically trigger strong risk-off reactions, markets have largely absorbed the news without significant disruption.

This muted response is most visible in oil markets. After briefly surging above the 100 level earlier in the week, WTI crude has now retreated back toward the 92 handle. The inability to sustain gains signals that the “geopolitical risk premium” is fading, as traders increasingly view the conflict as a prolonged but contained disruption rather than an immediate threat to global supply.

As attention shifts away from geopolitics, central banks are moving back to the forefront. Today’s Bank of Canada decision serves as the opening act for a highly concentrated policy week, with Federal Reserve, Bank of Japan, Swiss National Bank, Bank of England and European Central Bank all set to announce decisions tomorrow.

In currency markets, Dollar is showing signs of weakness for the week so far. A key driver appears to be growing skepticism around expectations for a “hawkish hold” from the Fed. Traders are beginning to question whether policymakers will deliver a sufficiently strong signal to justify current market positioning.

This shift reflects a broader uncertainty surrounding Fed policy. With officials in blackout period and no direct guidance on how they assess the recent oil-driven inflation risks, markets are left navigating a “valuation vacuum.”

Meanwhile, Loonie is also under pressure ahead of the BoC decision. Canada faces a markedly different macro backdrop compared to other major economies, with cooling inflation and weakening labor market offsetting the impact of higher oil prices. This raises the risk that the BoC may lean dovish even as global inflation risks rise.

In contrast, Aussie continues to outperform following this week’s RBA rate hike and Governor Michele Bullock’s clear message that the board remains united on the direction of policy. This clarity has reinforced expectations for further tightening.

Kiwi is also benefiting from the improved tone in risk sentiment, while European majors and Yen are trading in the middle of the pack. Overall, major currency pairs and crosses remain largely range-bound, reflecting the market’s reluctance to take strong directional bets ahead of key policy decisions.

In Asia, Nikkei rose 2.77%. Hong Kong HSI is up 0.85%. China Shanghai SSE is up 0.17%. Singapore Strait Times is up 1.39%. Japan 10-year JGB yield is down -0.048 at 2.215. Overnight, DOW rose 0.10%. S&P 500 rose 0.25%. NASDAQ rose 0.47%. 10-year yield fell -0.018 to 4.202.

“Hawkish hold” may disappoint as Fed avoids committing either way

A “hawkish hold” is priced in—but the Fed may deliver something more neutral. If so, markets could be caught off guard, opening the door to a sharp repricing in Dollar and global assets. Read more.

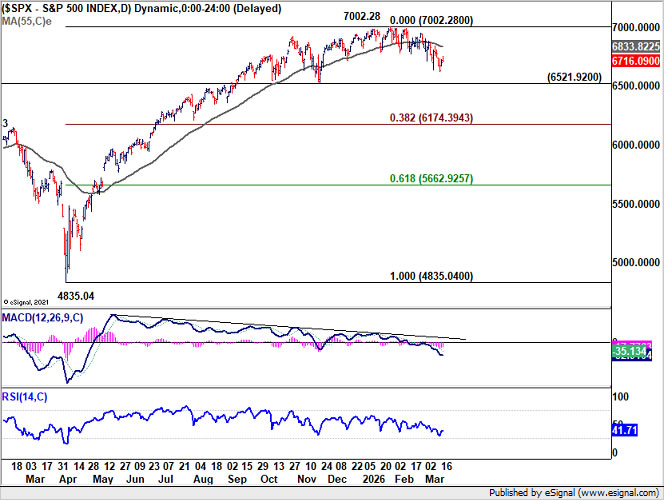

Fed boost or bull trap? S&P 500 rebound to faces resistance at 55-Day EMA

A Fed-driven bounce in S&P 500 may prove temporary, with the index still in a downtrend and facing key resistance at the 55-day EMA. A break below 6521 support would confirm a deeper correction toward 6174 and could support renewed Dollar strength. Read more.

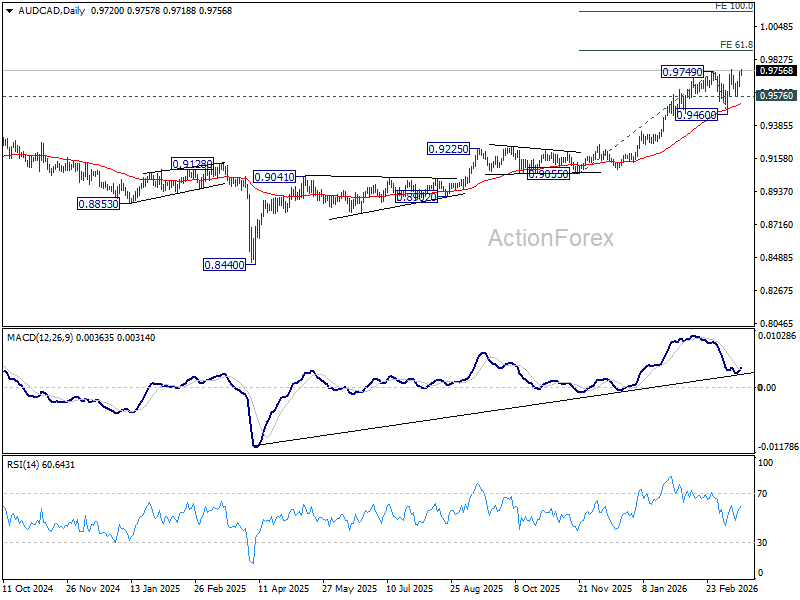

AUD/CAD targets 0.9889 as BoC dovish risk supports breakout setup

AUD/CAD is building upside momentum as markets brace for a potentially dovish BoC hold, with cooling inflation and weak jobs data offsetting oil-driven price pressures. A sustained break above 0.9749 would pave the way toward 0.9889 while 0.9576 support holds. Read more.

Japan trade data highlights diversification, shift away from China and U.S.

Japan’s exports rose 4.2% yoy in February, beating forecasts despite sharp declines in shipments to China and the U.S. Strong demand from Southeast Asia and Europe helped offset weakness, signaling a shift in trade dynamics. Read more.

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.65; (P) 159.07; (R1) 159.43; More...

Intraday bias in USD/JPY remains neutral for the moment. Considering bearish divergence condition in 4H MACD, break of 158.55 should indicate short term topping. Intraday bias will then be back on the downside for 38.2% retracement of 152.25 to 159.74 at 156.87. Nevertheless, strong bounce from current level, followed by break of 159.74, will target a retest of 161.94. Firm break there will confirm larger up trend resumption and target 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

AUD/CAD targets 0.9889 as BoC dovish risk supports breakout setup

AUD/CAD moved higher this week as markets increasingly positioned for a divergence in policy outlook between the RBA and the BoC. Attention now turns to the BoC decision today, where rates are expected to remain unchanged at 2.25% for the third consecutive meeting. Notably, this level already sits at the lower bound of the Bank’s estimated neutral range of 2.25%–3.25%, meaning any rate cut would push policy into accommodative territory. Any dovish guidance today could drive the next upleg in AUD/CAD.

At first glance, the surge in oil prices would argue for a more cautious or even hawkish stance from the BoC, given the inflationary impulse. However, Canada’s domestic backdrop tells a different story. February CPI slowed to 1.8% yoy, below the 2% target. Core measures such as CPI common also eased notably from 2.7% to 2.4%, suggesting underlying inflation pressures are already moderating.

At the same time, the labor market is flashing clearer warning signs. Employment dropped by -84k in February, with losses concentrated in full-time jobs, pointing to weakening demand conditions. Combined with ongoing pressure from U.S. tariffs, the economy faces a dual hit from softer growth and external uncertainty.

This creates a policy dilemma where oil-driven inflation is offset by deteriorating domestic fundamentals. As a result, Governor Tiff Macklem is more likely to emphasize growth risks than inflation concerns. More importantly, any signal that the BoC is prepared to return to easing later this year, i.e. a “dovish hold”, would weigh on the Canadian Dollar.

Technically, AUD/CAD is attempting to resume its uptrend from 0.8440 (2025 low). Sustained trading above 0.9749 resistance would open the way toward 61.8% projection of 0.9055 to 0.9749 from 0.9460 at 0.9889 quickly. As long as 0.9576 support holds, the near-term outlook remains bullish, with policy divergence continuing to provide the fundamental backing for further upside.

Fed boost or bull trap? S&P 500 rebound to faces resistance at 55-Day EMA

Equity markets may initially react positively if the Federal Reserve delivers a more neutral hold than expected, as outlined in our Fed analysis. A softer tone could ease rate concerns and lift risk sentiment in the short term. However, the sustainability of any such rebound remains highly uncertain given the underlying technical structure.

Technically, S&P 500 has been spiraling lower since peaking at 7,002.28 record in January. Any rebound triggered by the Fed is likely to face strong resistance at the 55 D EMA (now at 6833.82). As long as price action remains capped below this level, rallies should be viewed as temporary recovery only.

The key level to watch on the downside is 6,521.92. A firm break of this structural support would confirm that the index has formed a medium-term top at 7,002.28, on persistent bearish divergence in D MACD. S&P 500 should then be already in correction to the whole rise from 4835.04 (2025 low).

The next target comes in at 38.2% retracement of 4,835.04 to 7,002.28 at 6,174.39. A move toward this level would likely coincide with renewed Dollar strength, as equity weakness feeds back into broader risk sentiment across global markets.

“Hawkish hold” may disappoint as Fed avoids committing either way

The Federal Reserve is widely expected to leave interest rates unchanged at 3.50–3.75% today, with little room for surprise on the decision itself. Instead, markets are focused squarely on the message. While many participants are bracing for a “hawkish hold,” that expectation may prove too simplistic for a Fed facing growing risks on both sides of its mandate.

At the core of the policy challenge is a renewed stagflationary threat. The surge in oil prices following the escalation of conflict in the Middle East is likely to push headline inflation higher in the near term. This has prompted concerns that the Fed may need to keep policy tighter for longer, or even consider further hikes if inflation proves persistent.

However, policymakers are unlikely to view the energy shock as a sufficient reason to turn decisively hawkish. There is a strong argument within the Fed that oil-driven inflation is more likely to be transitory than structural. With interest rates already in a “sufficiently restrictive” range, officials may believe current policy is adequate to prevent a 1970s-style wage-price spiral from taking hold.

On the other side of the mandate, the labor market is showing clearer signs of strain. February’s nonfarm payrolls report delivered a sharp -92,000 contraction, while the unemployment rate rose to 4.4%. Although some of the weakness can be attributed to temporary factors, underlying softness in sectors such as manufacturing and information is becoming more apparent.

Beyond cyclical weakness, structural risks are also emerging. The acceleration of AI adoption is raising concerns about job displacement across certain industries. These developments make it difficult for the Fed to justify any premature tightening, even in the face of higher inflation.

Against this backdrop, the Fed’s most likely strategy is to push back against market pricing for near-term rate cuts while stopping short of signaling any renewed tightening cycle. In other words, policymakers will aim to anchor expectations in both directions without committing to either path.

This balancing act is further shaped by leadership dynamics. Chair Jerome Powell is in the final weeks of his term, with his tenure ending on May 15. With a transition on the horizon, Powell has little incentive to introduce major policy shifts. Instead, his priority is likely to be maintaining stability and handing over a coherent framework to his successor.

The dot plot will be a key focal point. Increased dispersion is likely, reflecting divergent views within the Committee. Some participants may nudge their projections higher, signaling vigilance on inflation, while others may maintain or even lower their expected rate path in response to labor market risks.

Such divergence typically results in a relatively stable median projection, allowing the Fed to project firmness without committing to a more aggressive stance. This outcome may fall short of market expectations for a clearly hawkish signal, particularly if investors are positioned for a stronger pushback against easing bets.

In this context, the risk is that a “balanced” outcome is interpreted as less hawkish than anticipated. For markets, that could translate into renewed pressure on the Dollar and a continuation of range-bound trading, as investors reassess the path of policy in an environment defined more by uncertainty than conviction.