Sample Category Title

Swiss growth outlook cut as energy shock and strong Franc weigh on economy

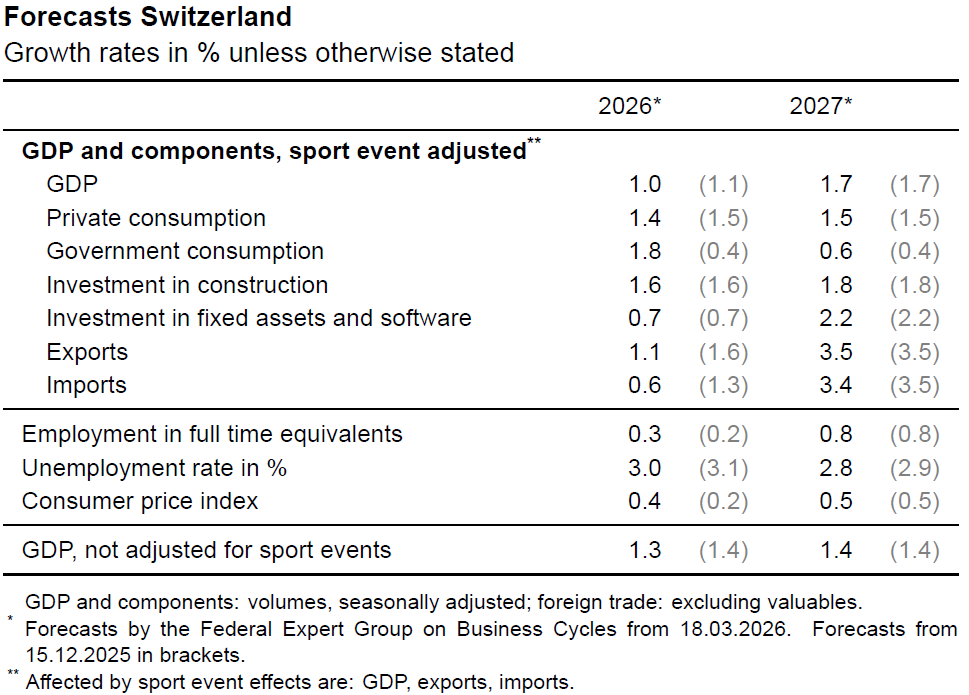

Switzerland’s economic outlook has been revised slightly lower as the fallout from the Middle East conflict continues to ripple through global markets. The Federal Government Expert Group on Business Cycles now expects GDP growth of 1.0% in 2026, down from the previous 1.1% forecast, reflecting below-average expansion. Growth is still projected to recover to 1.7% in 2027, but the near-term outlook has clearly softened amid rising uncertainty.

The key driver behind the downgrade is the sharp increase in energy prices since late February. Higher oil prices are not only lifting inflation expectations globally but also weighing on consumption and business sentiment. In Switzerland, inflation is now expected to come in slightly higher at 0.4% in 2026, compared to the earlier estimate of 0.2%.

At the same time, Switzerland’s export sector continues to face headwinds from subdued global demand and the strength of the Swiss Franc. These factors are dampening investment activity and limiting growth momentum in exposed industries.

Looking ahead, conditions are expected to improve gradually in 2027 as global demand recovers, particularly in Europe, with Germany’s stabilization likely to provide some support. However, the near-term outlook remains constrained by external risks and currency strength.

Gold Back in Focus as Markets React to Geopolitics

The market is fixated on the threat of accelerating inflation driven by high energy prices. As a result, central banks are expected to adopt a tighter monetary policy, keeping rates at high levels or even raising them. This has a positive impact on fiat currencies and strips gold of its key feature as a store of value amid currency debasement. It is no surprise that the precious metal, which had got off to a strong start, has been losing out to Bitcoin and the US dollar since the start of the armed conflict in the Middle East.

Although gold is generally regarded as a safe-haven asset, in the early stages of financial market turmoil, investors often choose to flee to liquidity. They favour fiat currencies and are far more willing to buy US dollar-nominated short-term treasuries.

Gold prices usually recover only if market shocks worsen, fears of recession or stagflation rise, and central banks start adding liquidity. Bank of America believes that the markets are still underestimating the scale of the potential consequences of geopolitical tension. They are fixated on the threat of accelerating inflation and are not considering a global economic downturn. Therefore, the longer the conflict between the US, Israel and Iran lasts, the better it is for the precious metal.

UBS Global Wealth Management notes that gold serves as a hedge against currency devaluation, rising budget deficits and recession. All of these could result from a geopolitical shock. The firm therefore maintains its bullish outlook on gold. In its view, the precious metal could rise to the $5,900-$6,200 range before the end of this year.

However, gold must first weather the storm of numerous central bank meetings. The RBA has already raised its cash rate to 4.15%. Investors now expect ‘hawkish’ rhetoric from the rest. The ECB and the Bank of Japan are ready to tackle inflation, and the futures market expects them to tighten monetary policy. The Fed and the Bank of England are most likely to talk about prolonged pauses in their cycles.

Thus, gold appears to be a win-win option. It will gain if the conflict in the Middle East drags on, and will not lose if it ends. Investors just need to be patient for a little while.

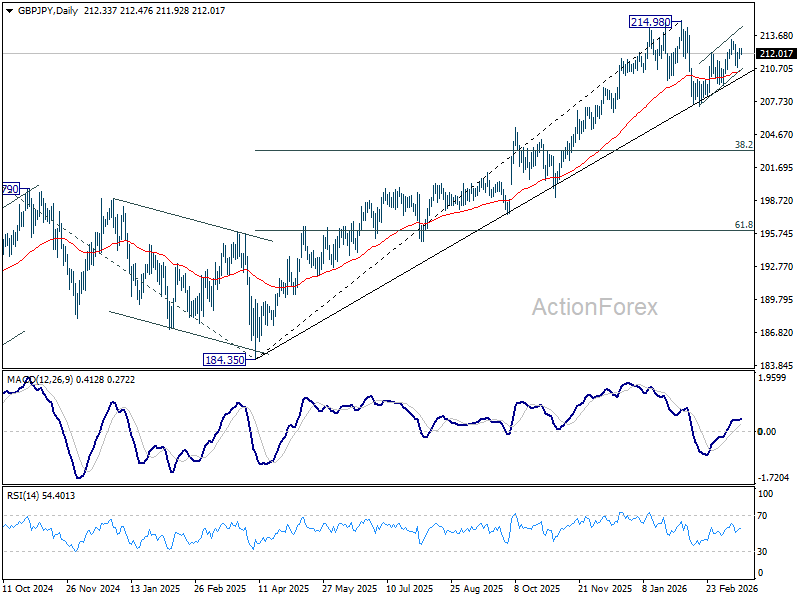

GBP/JPY Daily Outlook

Daily Pivots: (S1) 211.83; (P) 212.16; (R1) 212.71; More...

Intraday bias in GBP/JPY stays neutral first. Outlook is unchanged that rebound from 207.20 could have completed with three waves up to 213.28. Below 210.78 will target 209.15 support first. Firm break there will solidify this case and target 207.20 next. On the upside, however, above 213.28 will target a retest on 214.98 high instead.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.08) holds, even in case of another deep pullback.

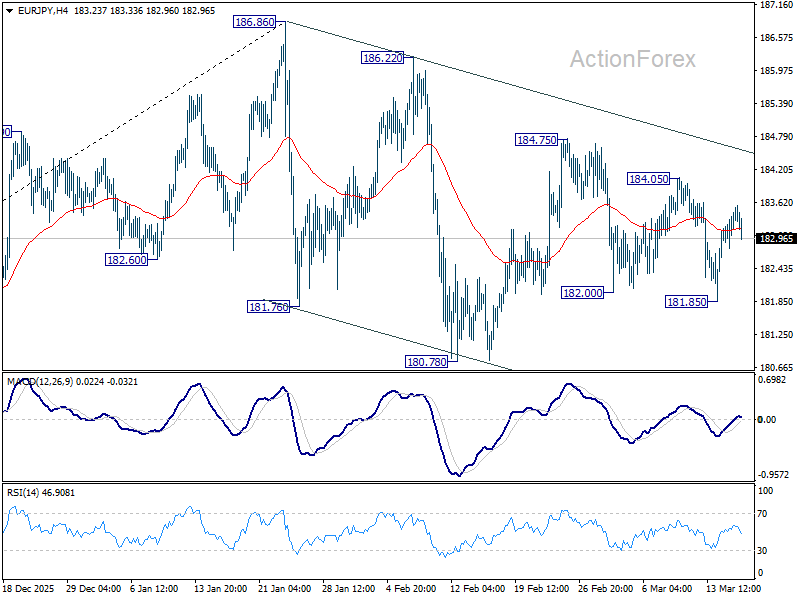

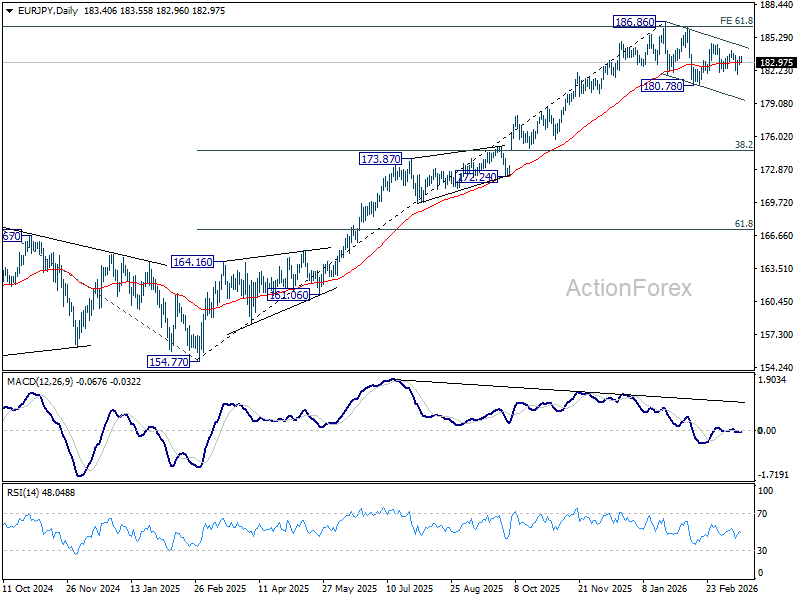

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.02; (P) 183.30; (R1) 183.77; More...

Intraday bias in EUR/JPY stays neutral for the moment. On the downside, below 181.85 will target 180.78 support. Decisive break there will indicate that fall from 186.86 is already correcting whole up rise from 154.77, and solidify the near term bearish outlook. On the upside, above 184.75 will resume the rebound from 180.78 to retest 186.86 high.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.29) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

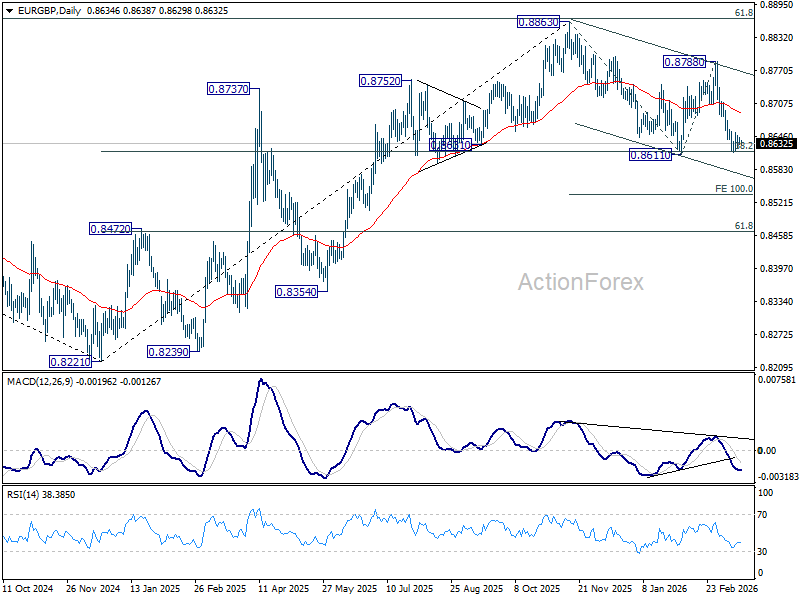

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8633; (P) 0.8640; (R1) 0.8649; More…

Intraday bias in EUR/GBP remains neutral and more range trading could be seen. Further decline is expected as long as 55 D EMA (now at 0.8688) holds. Firm break of 0.8611 will resume the whole fall from 0.8863 to 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

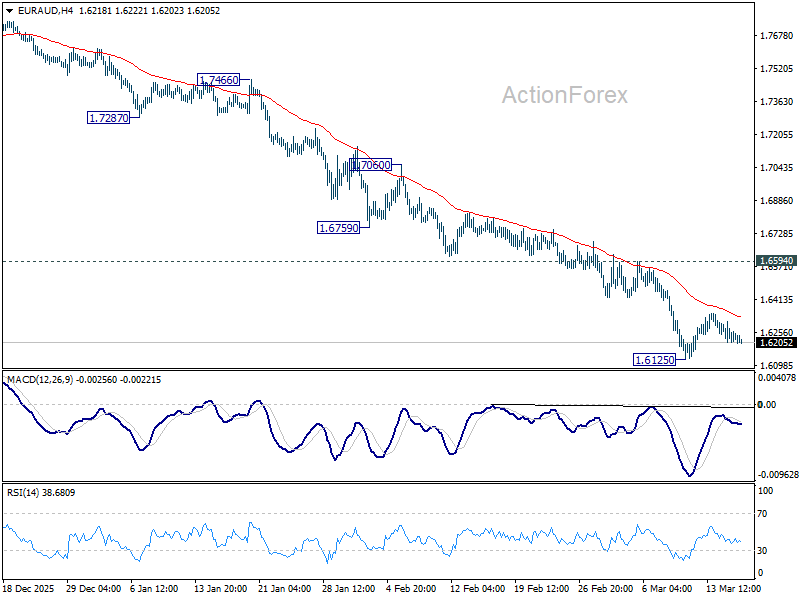

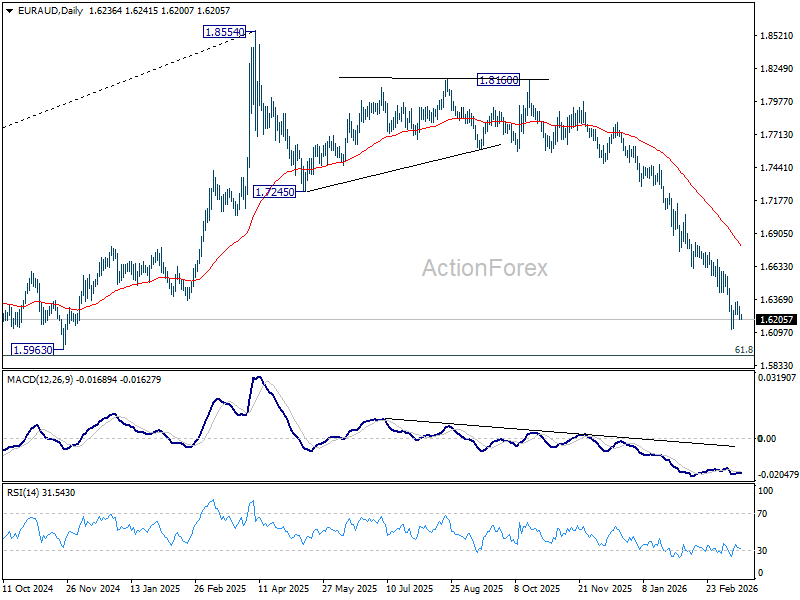

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6198; (P) 1.6255; (R1) 1.6301; More...

Intraday bias in EUR/AUD stays neutral for the moment as range trading continues. Further decline is expected with 1.6594 resistance intact. Firm break of 1.6125 will resume the fall from 1.8554 to 1.5913 fibonacci level next. Nevertheless, break of 1.6594 will indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7238) holds, even in case of strong rebound.

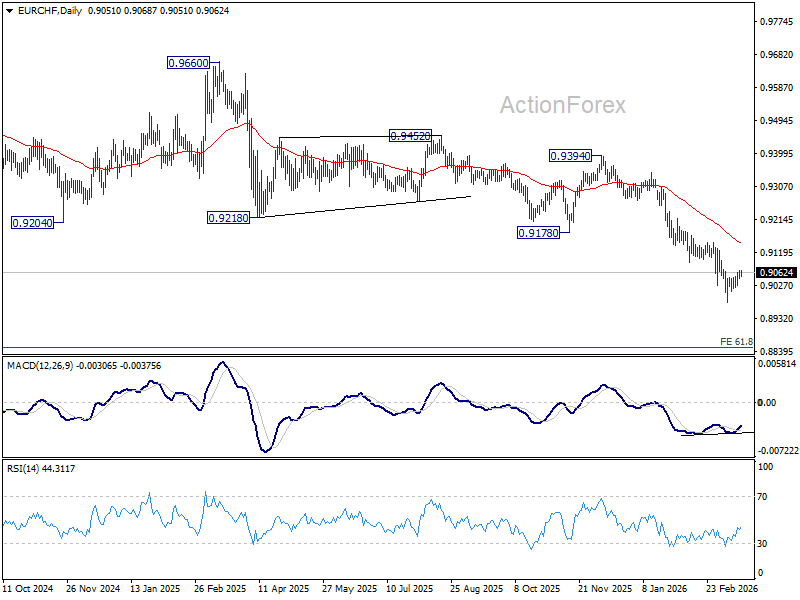

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9046; (P) 0.9059; (R1) 0.9071; More....

Intraday bias in EUR/CHF stays neutral. While recovery from 0.8979 might extend, further decline is expected with 0.9092 support turned resistance intact. On the downside, firm break of 0.8979 will resume larger down trend. However, break of 0.9092 will bring stronger rebound to 0.9149 resistance instead.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

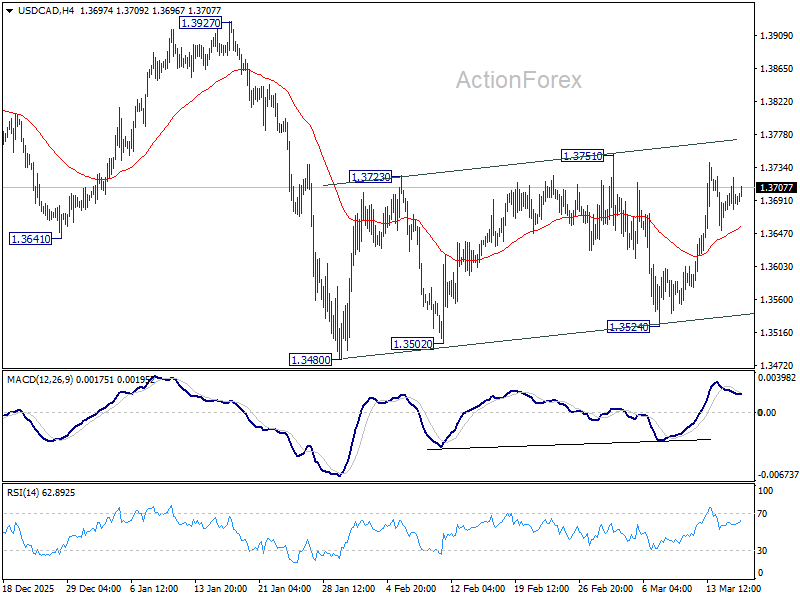

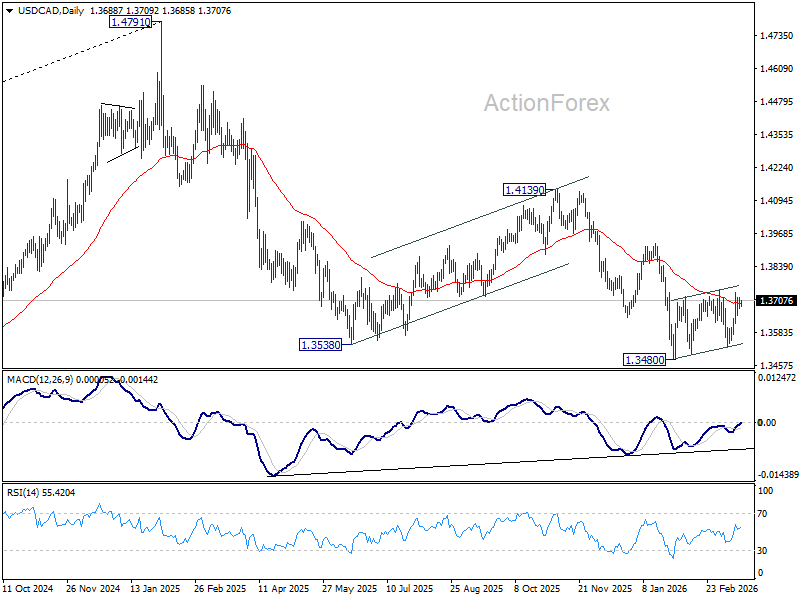

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3673; (P) 1.3698; (R1) 1.3716; More...

Intraday bias in USD/CAD stays neutral as range trading continues. On the upside, firm break of 1.3751 resistance will suggest that stronger rebound is underway, and target 1.3927 resistance first. Meanwhile, break of 1.3524 support will bring resumption of whole down trend from 1.4791.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

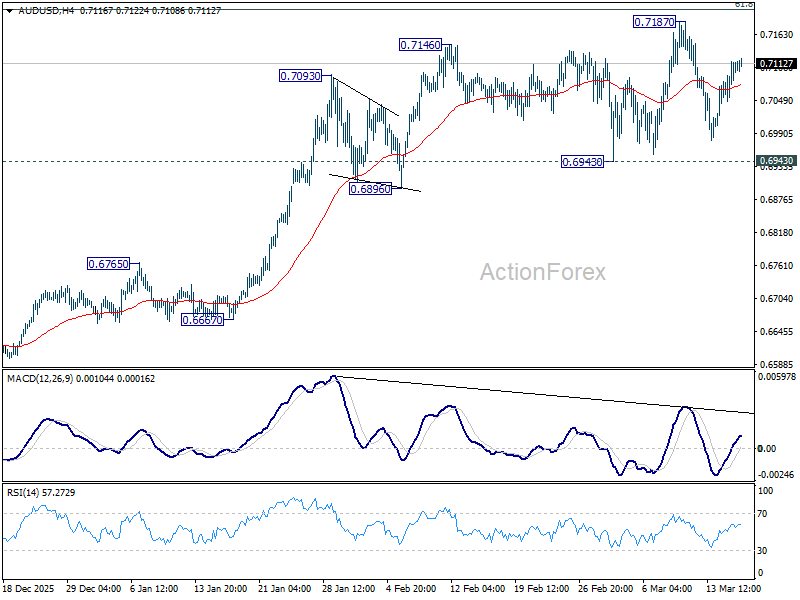

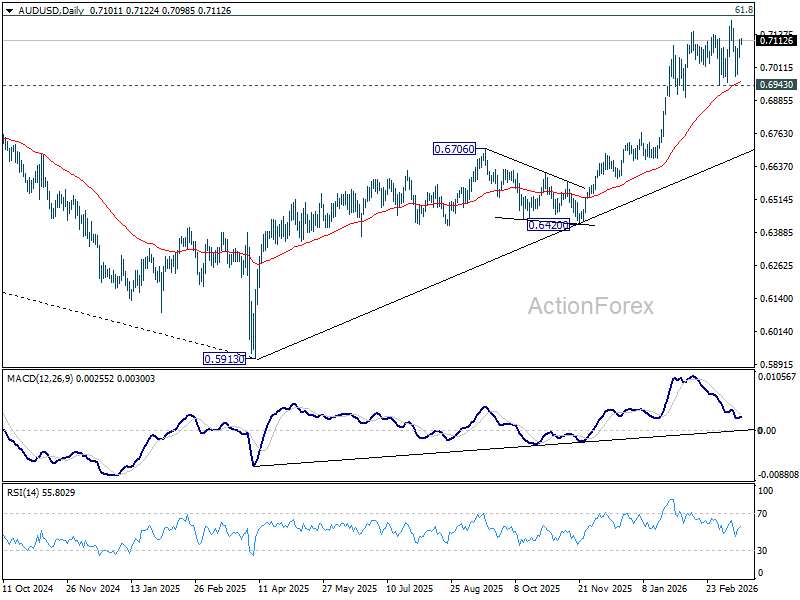

AUD/USD Daily Report

Daily Pivots: (S1) 0.7063; (P) 0.7091; (R1) 0.7133; More...

Intraday bias in AUD/USD stays neutral at this point as sideway trading continues. With 0.6943 support intact, further rally is still expected. On the upside, firm break of 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 could prompt upside acceleration to 161.8% projection at 0.7703. However, firm break of 0.6943 will indicate that a larger scale correction is already underway.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1518; (R1) 1.1570; More….

EUR/USD is extending consolidations from 1.1408 and intraday bias remains neutral. Further decline is expected as long as 1.1666 resistance holds. Below 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Firm break there will target 61.8% projection at 1.0904 next.

In the bigger picture, the break of 55 W EMA (now at 1.1495) confirms rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. In either case, deeper fall is now expected to long term channel support (now at 1.0528. Risk will stay on the downside as long as 1.2081 holds, in case of recovery.