Sample Category Title

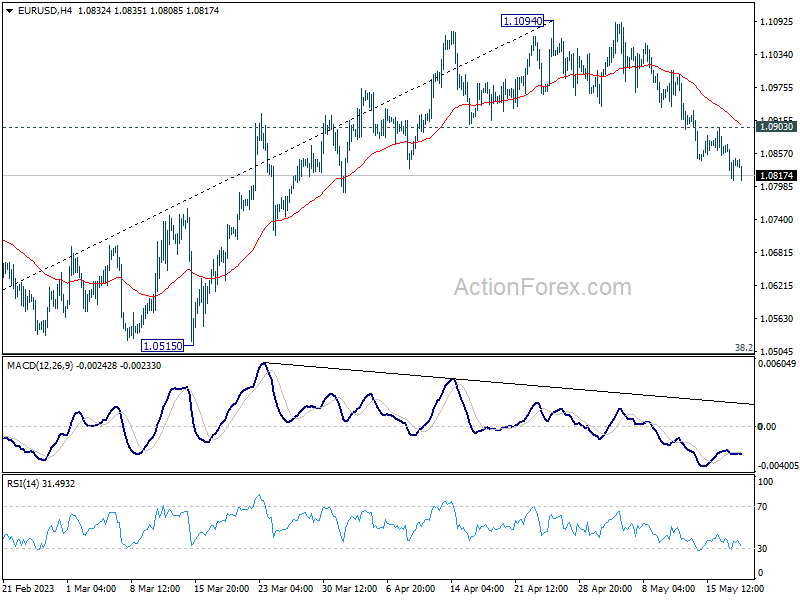

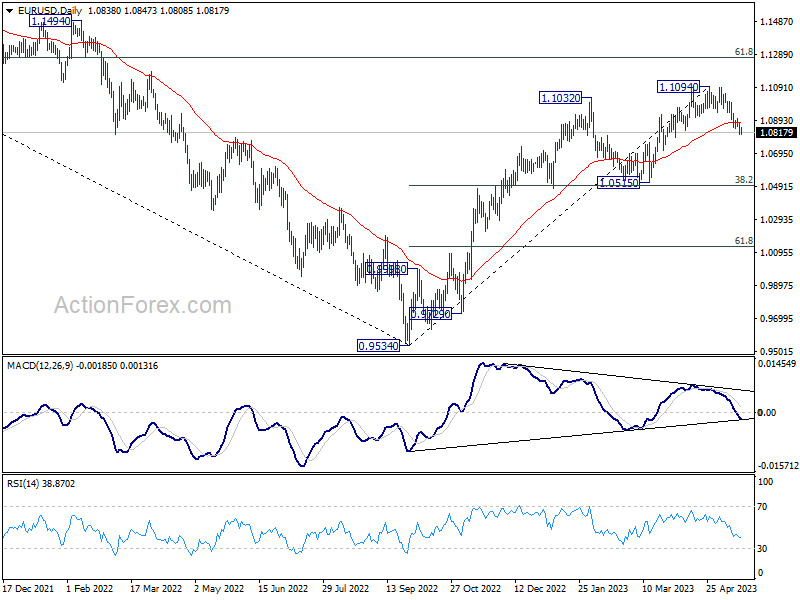

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0808; (P) 1.0841; (R1) 1.0872; More...

Intraday bias in EUR/USD remains on the downside as fall from 1.1094 short term top is in progress. Current decline is seen as correcting whole up trend from 0.9534. Deeper fall would be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, above 1.0903 minor resistance will turn intraday bias neutral first.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

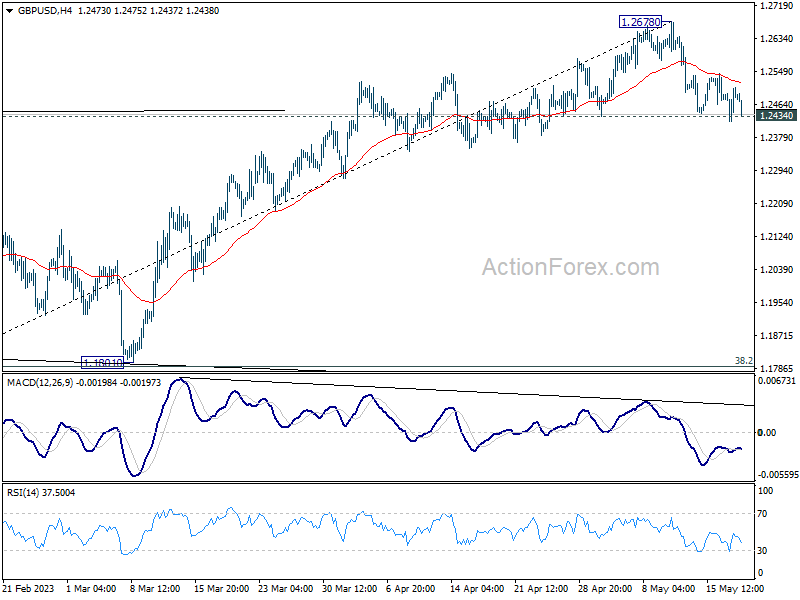

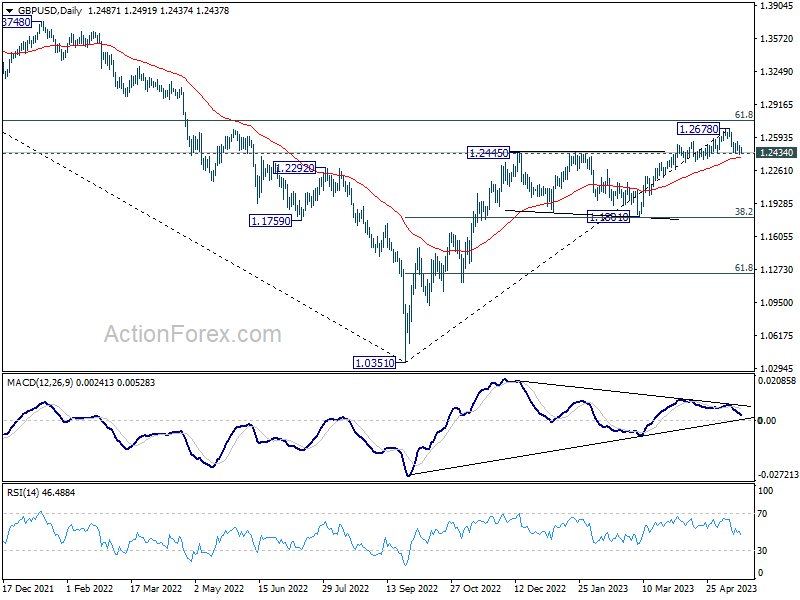

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2436; (P) 1.2473; (R1) 1.2524; More...

Intraday bias in GBP/USD remains neutral at this point. On the downside, firm break of 1.2434 will confirm short term topping at 1.2678, on bearish divergence condition in 4H MACD. Intraday bias will be back on the downside for 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789), as correction to whole up trend from 1.0351. On the upside, however, break of 1.2678 will resume larger up trend from 1.0351 instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

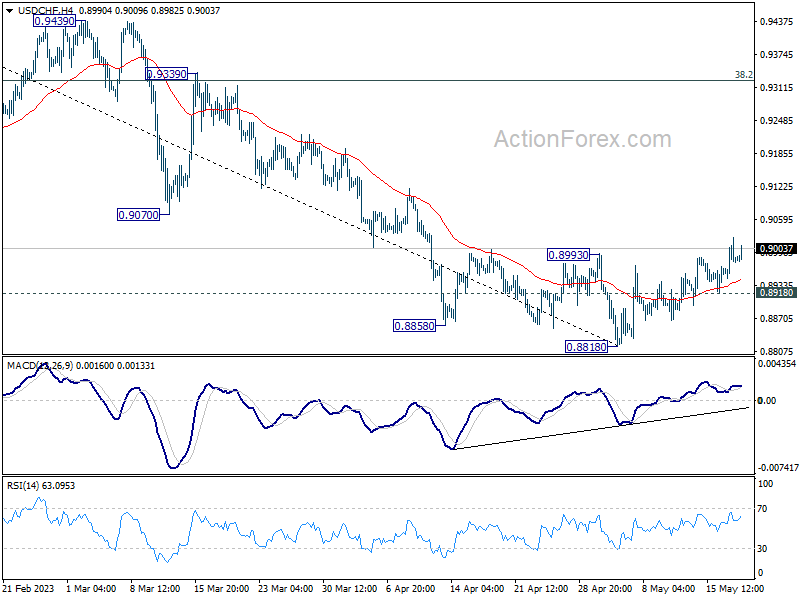

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8947; (P) 0.8987; (R1) 0.9024; More...

Intraday bias in USD/CHF stays on the upside at this point. Rise from 0.8818 short term bottom is at least corrective whole down trend from 1.0146. Sustained break of 55 D EMA (now at 0.9042) will confirm this case and target 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, below 0.8918 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

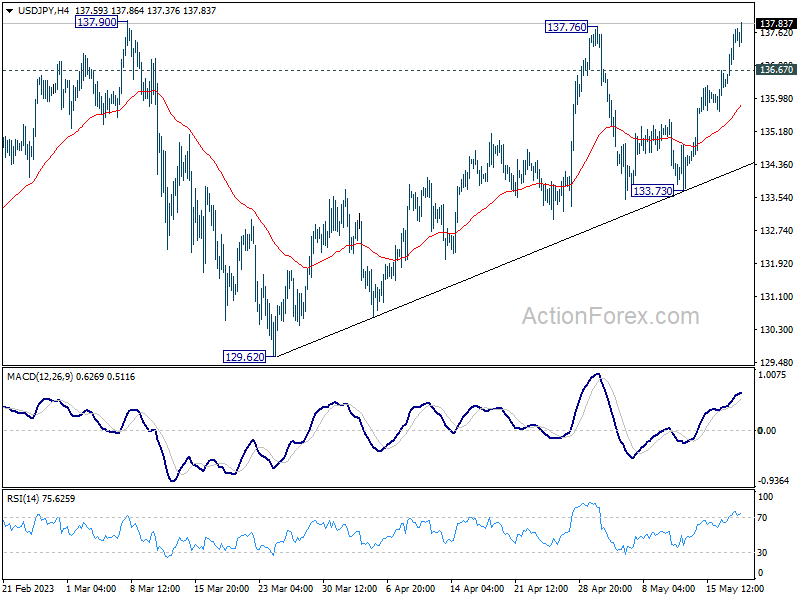

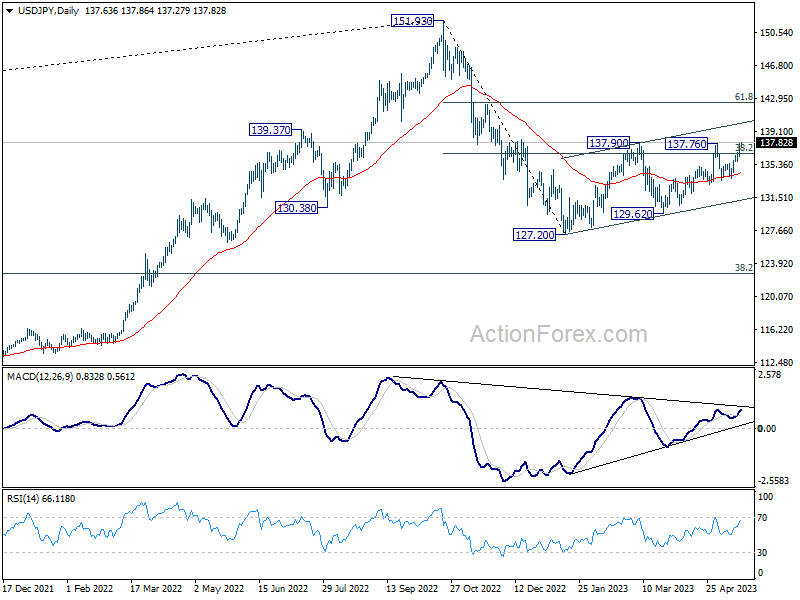

USD/JPY Daily Outlook

Daily Pivots: (S1) 136.78; (P) 137.24; (R1) 138.18; More...

Intraday bias in USD/JPY remains on the upside at this point. Decisive break of 137.76/90 resistance zone will resume whole rebound from 127.20. Next target is 142.48 fibonacci level. On the downside, below 136.67 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rise to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

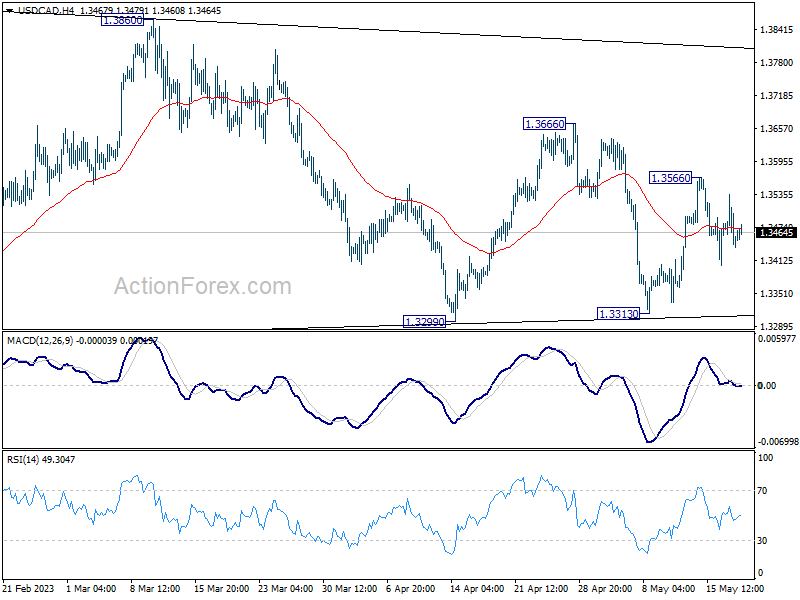

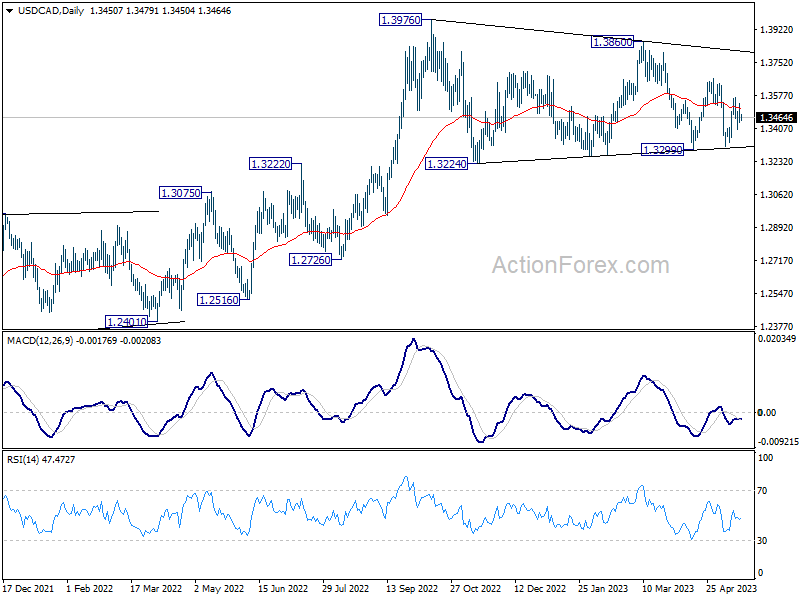

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3416; (P) 1.3476; (R1) 1.3515; More....

Outlook in USD/CHF remains unchanged as range trading continues. Intraday bias stays neutral for the moment. Overall, the pair is seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

In the bigger picture, as long as 55 W EMA (now at 1.3321) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

As Dollar Attempts a Comeback, Are Markets Wrong About Fed?

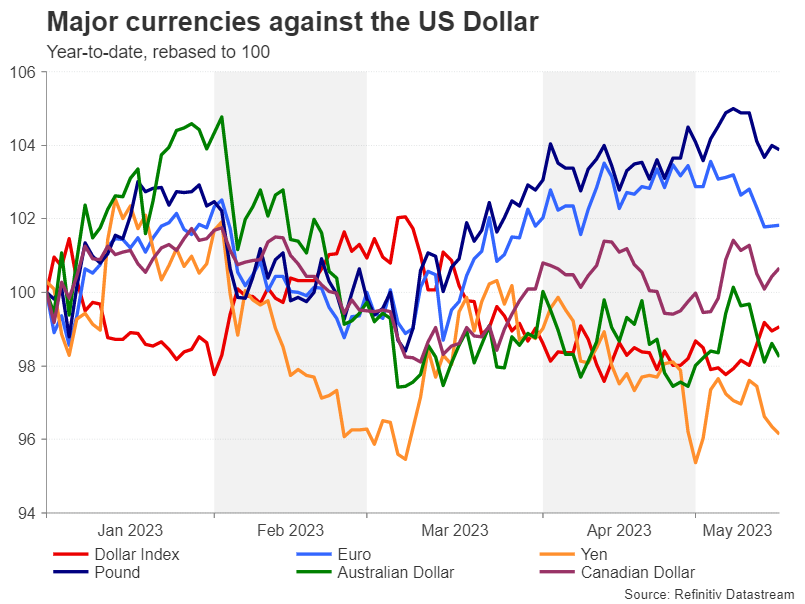

The US dollar is showing signs of life again, notching up its best week since September of last year and reaching a five-week high against the euro. From a technical perspective, the dollar index – a gauge measuring the US currency against a basket of six peers – has a few more hurdles to climb before it can claim to have emerged from its bearish phase, while from a fundamentals standpoint, the Federal Reserve is getting closer to hitting the pause button on its rate hiking cycle. So, is this latest bounce a false signal or are the groundworks being laid for a trend reversal?

The elusive Fed pivot

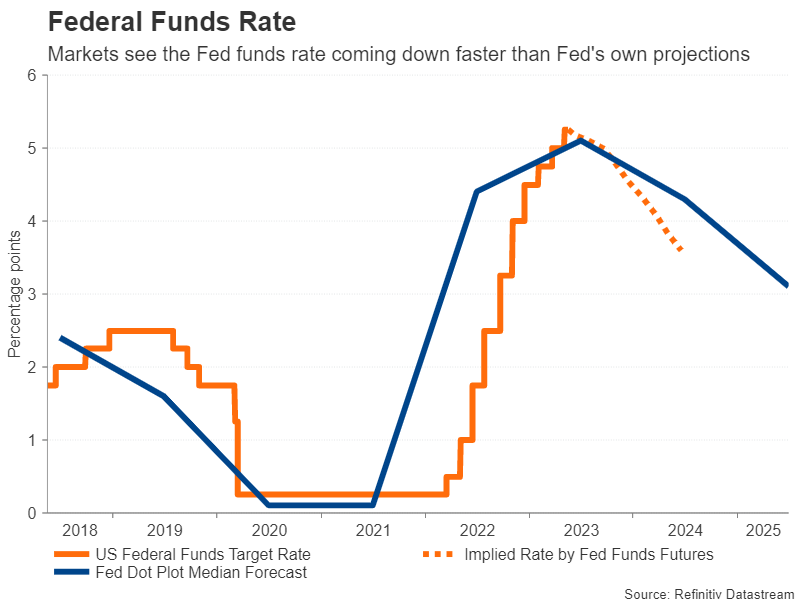

Markets started betting on a Fed pause long before policymakers even hinted that they were approaching the end of their tightening cycle. Speculation about the timing of a Fed pivot dominated the market theme in late 2022 and has reached fever pitch in 2023. Some might argue that the Fed has already pivoted, having downshifted twice to smaller increment rate hikes. The next step therefore might well be the long-awaited pause.

The biggest clue to wrapping up the rate increases came at the May policy decision when the clause “The Committee anticipates that some additional policy firming may be appropriate” was removed from the FOMC statement. However, this wasn’t quite the pause signal that impatient traders had been hoping for. Whilst opening one door, Chair Jerome Powell refused to shut another, keeping both a hike and pause options firmly on the table.

The message from other policymakers had similarly been that the Fed is entirely data dependent. But in the last few days, things started to take an interesting twist.

A hawkish pause may not be what markets asked for

Several policymakers decided to raise the stakes by expressing their dissatisfaction at the slow progress in core inflation coming down. Fed governors Michelle Bowman and Philip Jefferson, who has been nominated by President Biden to become the next Vice Chair, were among those casting doubt on the prospect of an imminent end to the tightening process. But others, like the Atlanta Fed’s Raphael Bostic, flagged an inclination to pause.

The problem for the dollar is that although it has gained some ground from the renewed hawkish tone, Fed fund futures have barely responded. Investors are currently pricing in a slightly less than 20% probability of a 25-bps rate rise at the June meeting and expect the Fed to deliver at least two cuts of the same size by December.

Such misalignments between the market view and the Fed’s rarely ends well and investors should be worried. Even if the Fed does pause in June, one thing is clear – policymakers will be doing so with a bias to tighten again should inflation remain sticky. This then almost certainly rules out a rate reduction this year. So why are investors convinced that the Fed will cut rates?

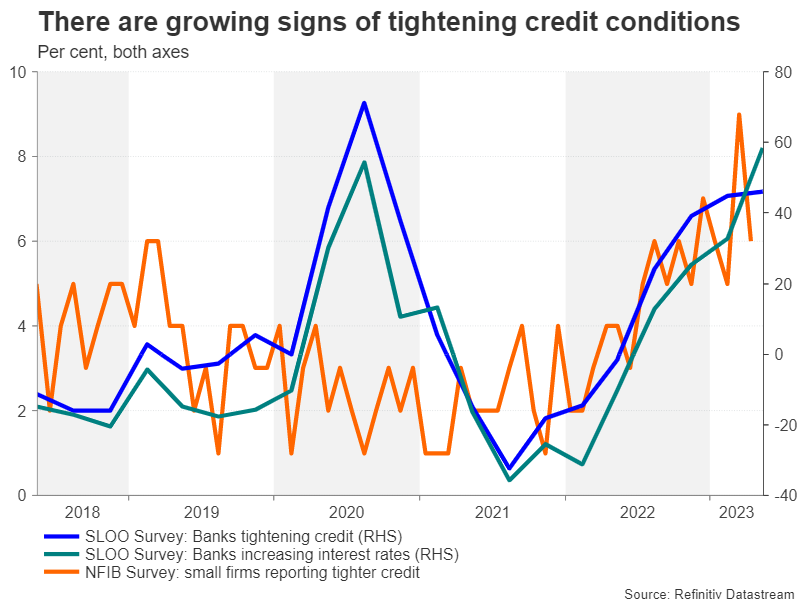

Is the US headed for a credit crunch?

Markets initially started to price in a lower Fed funds rate over fears that the central bank will overtighten and induce a recession. But more recently, it is concerns about America’s fragile banking system that is driving those fears rather than overtightening. There is some evidence to suggest that credit conditions have tightened significantly following the turmoil in March that led to the failure of several regional banks.

With the Fed far from being ready to switch away from restrictive policy, investors are anticipating the worst. There is one notable flaw to this reasoning as it assumes that the Fed will start slashing rates as soon as the US economy hits recession regardless of whether or not inflation has fallen fast enough by then. Yet, all the indications are that Powell is willing to sacrifice short-term pain to get inflation back to the Fed’s 2% goal as quickly as possible.

Safe haven boost

This also doesn’t explain why dollar bulls have been reawakened. Although it is true that the dollar has been attracting support lately from a mixed run of data, which have been inconclusive when it comes to how fast the economy, and the labour market specifically, is cooling, the main factor pushing it higher has been safe-haven flows.

Fresh concerns about China’s post-pandemic recovery and a real possibility of a recession in Germany have alarmed investors in recent days, while the ongoing stalemate over a bi-partisan deal in the US Congress to raise the debt ceiling has also contributed to the increased risk aversion over the past week.

But none of these are solid foundations for a bullish reversal in the dollar, hence, it is too early to draw any conclusions, even as the dollar index is flirting with its 50-day moving average.

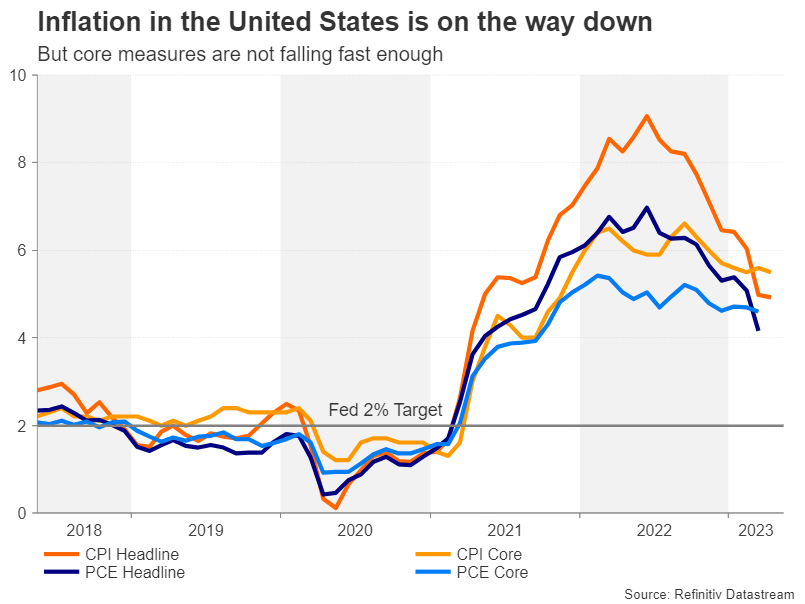

The problem of sticky inflation

Much of the dollar’s slide this year had been based on expectations of a transatlantic divergence in monetary policy, with the European Central Bank and Bank of England raising rates into the summer and the Fed’s May hike being the last.

But investors have seemingly gotten carried away by the improving inflation picture. As impressive as the drop in America’s headline CPI rate has been, underlying inflation remains elevated. The decline in both the CPI and PCE core measures appears to have stalled, and this hasn’t gone unnoticed at the Fed. There is also the continued resilience of the jobs market that the Fed just can’t get its head around.

Policymakers will want to see a lot more progress on both fronts before they can even start thinking about cutting rates. The question now is, what’s it going to take for traders to reassess their rate cut bets, or is it the Fed that will have to align its dot plot with the market-implied path?

The Fed vs the markets

After all, the risk of a credit crunch has not completely dissipated and it may take months for the fallout from the banking crisis to fully unravel, in which case, rate cuts would not be so implausible. Unfortunately, the scenario where the Fed isn’t forced to lower rates isn’t particularly appealing either.

Whereas at the start of the tightening campaign, it was the markets telling the Fed that the price hikes were not transitory, the tables have turned and it is investors who now seem to be ignoring the danger that high inflation is proving to be a lot stickier than anticipated.

If core inflation stays stubbornly high over the next few months, there would be nothing stopping the Fed from resuming its rate increases even after a pause, raising the prospect of a prolonged period of stagflation.

US dollar: more downside than upside?

For the dollar, given that the Fed has already been more aggressive than other central banks, some limited upside is probably the best that the bulls can hope for in the event that a credit squeeze does not materialize and the Fed is able to keep rates higher for longer. Such an outcome could see the dollar index revisiting the highs from March right before the banking episode to test its 200-day moving average.

However, the scale of any downside moves may be a little more difficult to predict. As things stand, the uncertainty around the outlook for the global economy and Fed policy is putting a floor under the greenback. But should some of the clouds start to lift and the monetary divergence paths become clearer, with the Fed pivoting before the ECB and the Bank of Japan only just starting to tighten policy, the dollar could suffer more substantial losses.

But even then, the road to all the way down to the January 2021 trough is a very long stretch for the dollar index. The 61.8% Fibonacci retracement of the uptrend that began from this low and ended at a two-decade high in September 2022 may be a more realistic target for the bears.

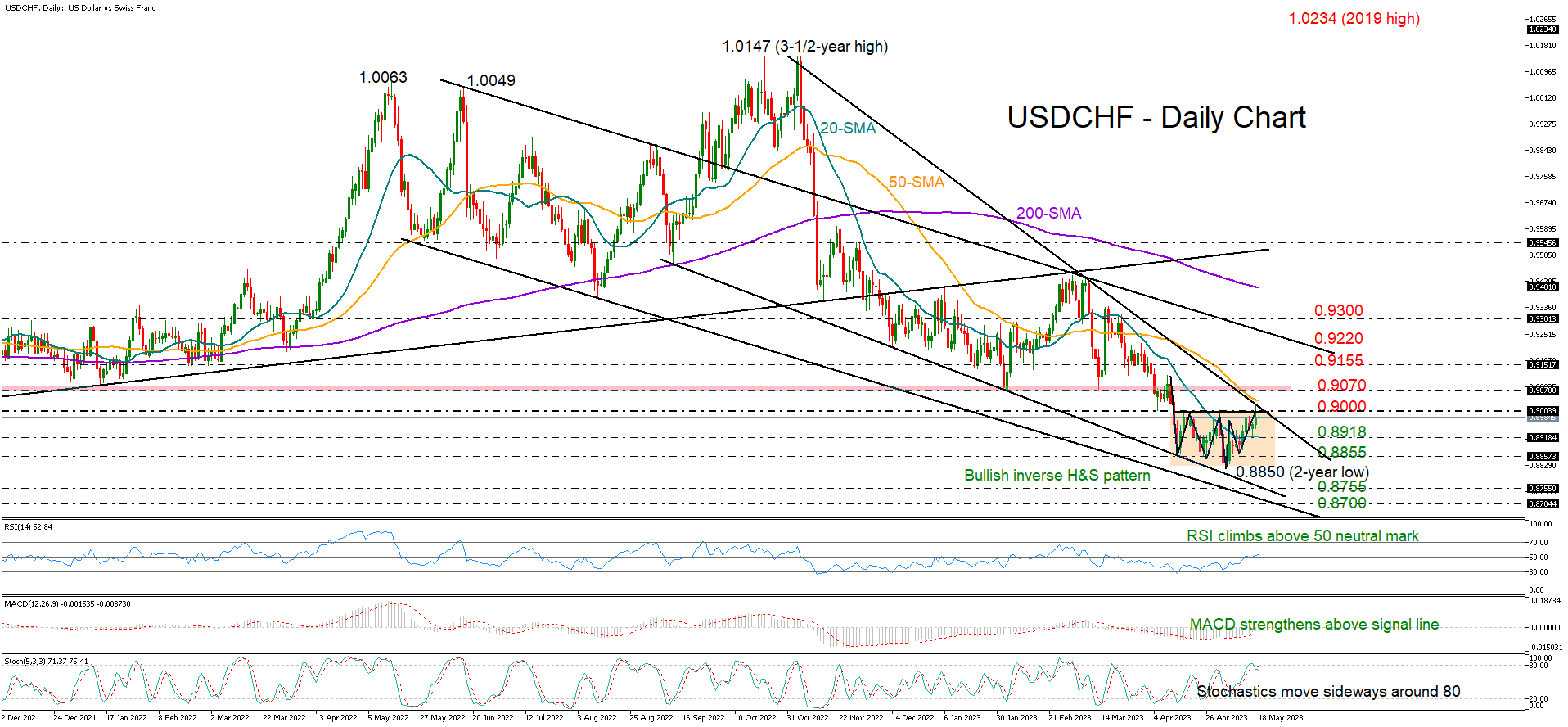

Is the Downtrend Over for USDCHF?

USDCHF has been building a base in the form of an inverse head and shoulders (H&S) pattern around a two-year low of 0.8850 over the past month, boosting hopes for a bullish trend reversal.

Traders are currently waiting to see whether the pair will find enough buyers to confirm the bullish structure above the 0.9000 neckline, and more importantly, mark a new higher high above the crucial 2023 constraining zone of 0.9070. Notably, the descending trendline, which connects the highs from November 2022, is located in the same area.

The RSI and the MACD are sending encouraging signals, with the former stretching its uptrend above its 50 neutral mark and the latter strengthening above its red signal line and towards the positive region. Yet, the Stochastic oscillator is warning that a continuation of the consolidation phase or a downside correction cannot be ruled out as the indicator flatlines near its 80 overbought level.

In the positive scenario, where the price closes above 0.9070, the next obstacle could emerge around 0.9155. Not far above, the resistance line drawn from June’s 2022 peak could be more demanding, around 0.9200. If the price successfully breaches that bar, the spotlight will turn to the 0.9300 psychological mark. Then, the pair will attempt to upgrade the medium-term outlook above the 200-day simple moving average (SMA) at 0.9400 and the March high of 0.9439.

Alternatively, a pullback below 0.9000 could initially halt near the 20-day SMA at 0.8918. If not, the bears will attempt to re-activate the downtrend below the 0.8855-0.8850 region with scope to reach the support line from September at 0.8755. Slightly lower, the longer-term descending line from May could be another ideal area for a pivot.

In a nutshell, USDCHF seems to have set the ground for a positive trend reversal, though only a sustainable recovery above 0.9070 would verify the case.

WTI Tries to Gain Foothold

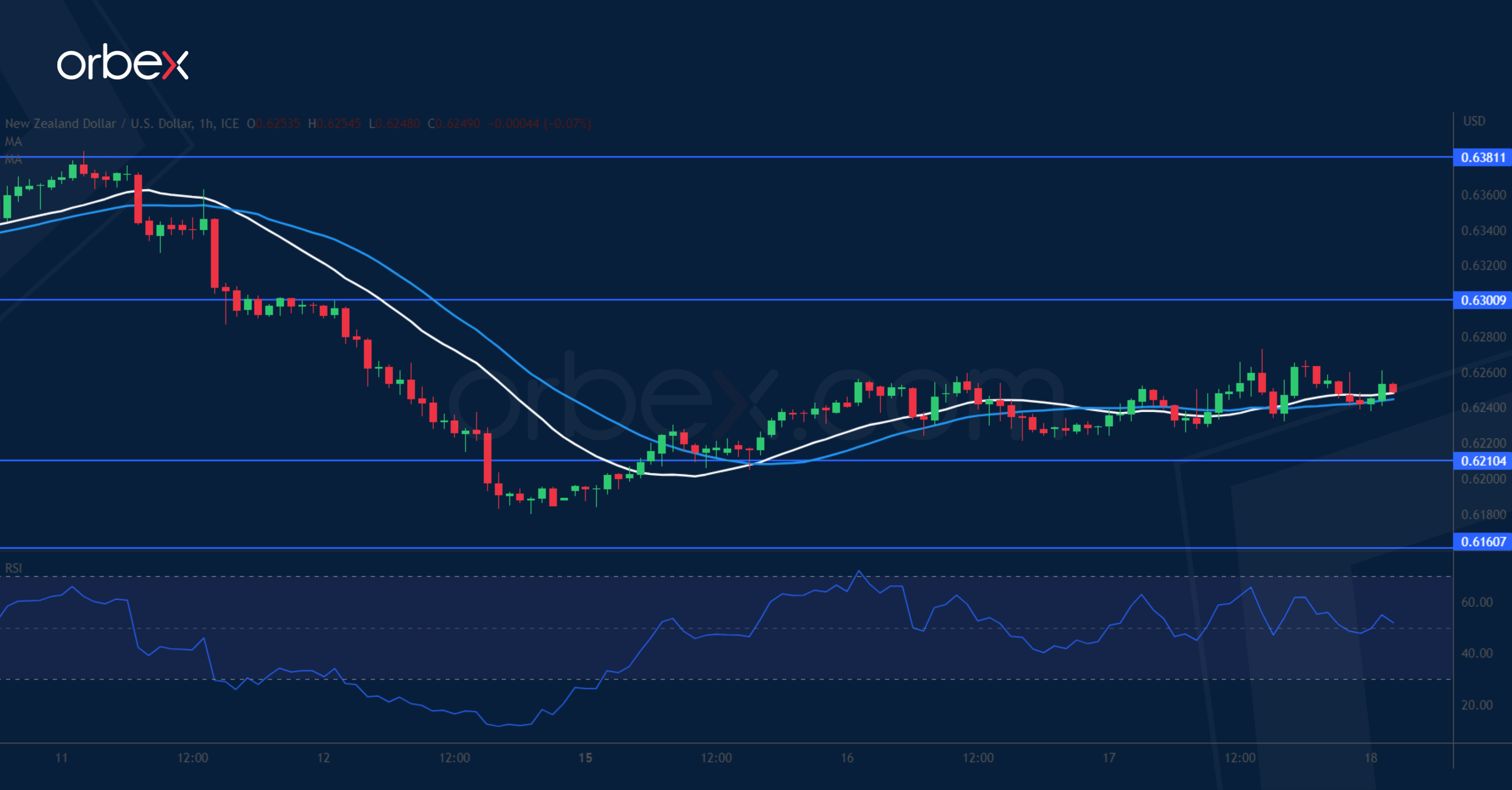

NZD/USD attempts to rebound

The New Zealand dollar grinds higher thanks to an uptick in the market’s risk appetite. The kiwi has retraced most of the recent gains from its late April rally. The RSI’s deeply oversold condition attracted some bargain hunting bids but these early buyers will need to consolidate their gains and clear 0.6300 before they could hope for a sustained recovery. 0.6210 is the first layer of defence in case of further hesitation. The demand zone 0.6120-0.6160 is important in keeping the rebound valid in the medium-term.

US Oil tests resistance

WTI rallied after the IEA expressed optimism about demand in the second half of the year. While a bearish MA cross on the daily chart suggests a lingering selling pressure, the price seems to have found a floor at 69.40 and is testing the previous swing high of 73.40. A bullish breakout would prompt sellers to take some chips off the table, reducing the pressure. Then 76.00 along the 30-day SMA is a major hurdle to lift before a recovery would materialise. On the downside, the daily double bottom at 66.00 is a critical support.

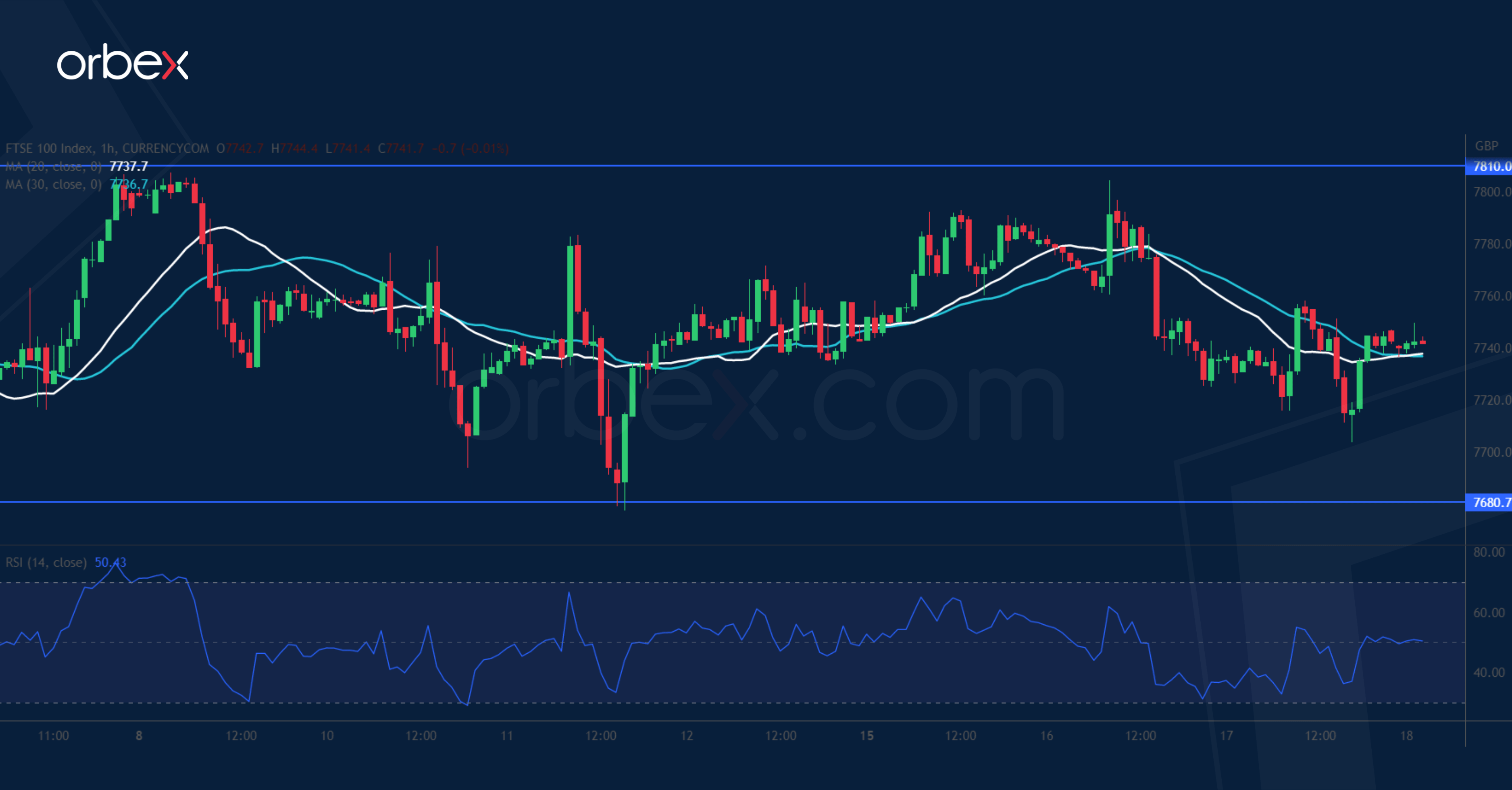

UK 100 struggles for support

The FTSE 100 edges lower as downbeat reports from blue-chip companies dent sentiment. The index is still in a correction mode after hitting resistance at 7930. The sideways action shows the bulls’ struggle to contain the pullback and their inability to lift offers around the support-turned-resistance of 7810 reveals strong selling interests from fresh sellers and trapped buyers. 7680 is the current support and 7630 is where the bulls would draw a line in the sand, as a breakout would trigger a sell-off towards 7500.

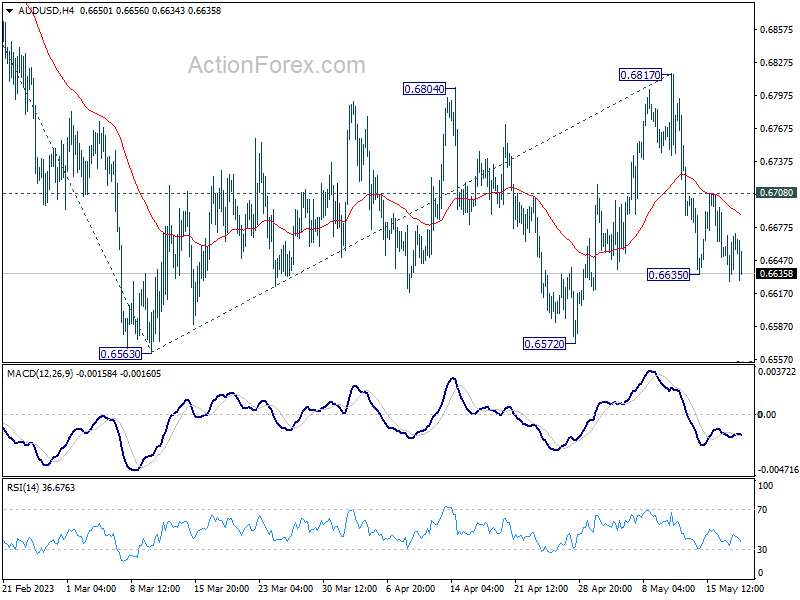

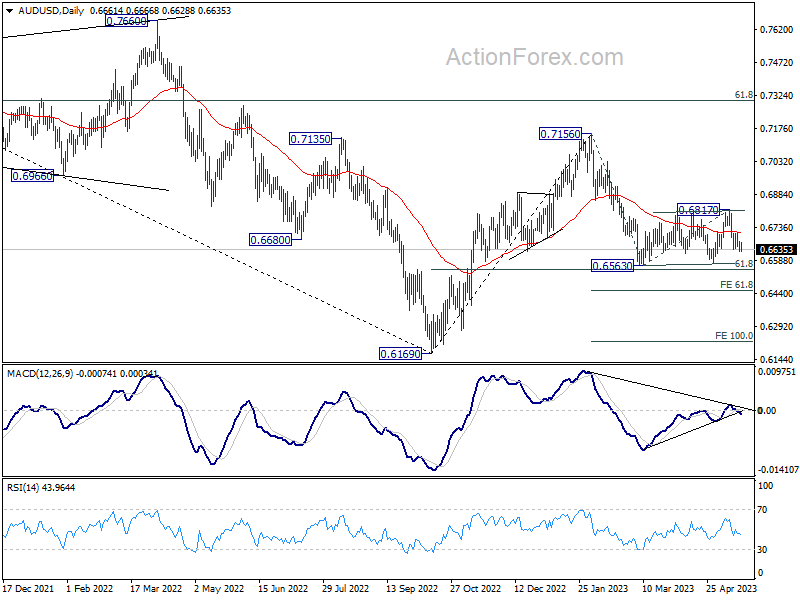

AUD/USD Daily Report

Daily Pivots: (S1) 0.6634; (P) 0.6654; (R1) 0.6678; More...

AUD/USD's fall resumed after brief recovery and intraday bias is back on the downside for retesting 0.6563 low. As noted before, consolidation pattern from 0.6563 could have completed with three waves to 0.6817.Decisive break of 0.6563 will resume larger decline from 0.7156 to 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. On the upside, above 0.6708 minor resistance will turn intraday bias neutral again first.

In the bigger picture, the failure to break through 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Firm break of 61.8% retracement of 0.6169 to 0.7156 at 0.6546 will raise the chance of long term down trend resumption through 0.6169 low. This will now be the favored case as long as 0.6817 resistance holds.

Dollar Holds Strong Despite Risk Market Rally: Debt Ceiling Negotiations Offer a Glimmer of Hope

Market sentiment received a significant boost following upbeat news about US debt ceiling negotiations, and yet, Dollar remains resilient, showcasing an impressive strength. US President Joe Biden, following a meeting with Republican House Speaker Kevin McCarthy, presented an air of optimism as discussions continue. "Now we have a structure to find a way to come to a conclusion," said McCarthy, adding "I think at the end of the day we do not have a debt default. I think we finally got the president to agree to negotiate." Biden shared this confidence, stating, "I'm confident that we'll get the agreement on the budget, that America will not default."

Stocks in the US closed the day in a broad rally, with NASDAQ's performance standing out as the index managed to close above 38.2% retracement of 16212.22 to 10088.82 at 12436.48. This significant bullish development forecasts further rallies as long the 12209.57 support level holds. The index should now aims for 13181.08 cluster resistance, 50% retracement at 13157.41. The burning question is whether Dollar could keep pace with the risk-on trend reflected in the stock market, or revert back to an inverse relationship.

Shifting focus back to the currency markets, Yen retains its position as the week's weakest performer, dragged down by ongoing rallies in US and European benchmark yields. In addition, strong Nikkei index performance seems to amplify Yen's inverse movement. Swiss Franc and Euro are also trailing in performance. Meanwhile, Kiwi and Loonie are faring well, but Aussie is being hampered by disappointing job data. Dollar, on the other hand, is extending its gains against Euro, Swiss Franc, and Yen, while remaining within range against Aussie, Loonie, and Sterling.

In Asia, Nikkei rose 1.60%. Japan 10-year JGB yield rose 0.0207 to 0.390. At the time of writing, Hong Kong HSI is up 0.41%. China Shanghai SSE is up 0.40%. Singapore Strait Times is up 0.40%. Overnight, DOW rose 1.24%. S&P 500 rose 1.19%. NASDAQ rose 1.28%. 10-year yield rose 0.032 to 3.581.

Australia employment down -4.3k in Apr, unemployment rate up to 3.7%

Australia employment contracted -4.3k in April, much worse than expectation of 25k growth. Full time job decreased -27.1k while part-time jobs rose 22.8k. Unemployment rate rose from 3.5% to 3.7%, above expectation of being unchanged at 3.5%. Participation rate dropped -0.1% to 66.7%. Employment-to-population ratio fell -0.2% to 64.2%. Monthly hours worked rose 2.6% mom or 49m hours.

Bjorn Jarvis, ABS head of labour statistics, said: "The small fall in employment followed an average monthly increase of around 39,000 people during the first quarter of this year." Meanwhile, both employment-to-population ratio and participation rate "were still well above pre-COVID-19 pandemic levels and close to their historical highs in 2022".

Japan's exports grow at slowest pace since Feb 2021 despite setting record high for Apr

Japan's exports grew by a modest 2.6% yoy to JPY 8288B in April. Although this represented the lowest growth in exports since February 2021, it still marked the largest export figure for April on record.

A closer examination of the data reveals a shift in trading dynamics. Exports to China fell by -2.9% yoy, marking the fifth consecutive month of decline. The decrease was driven by downturns in shipments of cars, car parts, and steel. Similarly, exports to Asia overall declined by -6.6% yoy, continuing a contraction trend for the fourth month in a row.

However, things looked rosier elsewhere. Exports to the US and EU showed robust growth, rising by 10.5% yoy and 11.7% yoy respectively. This uptick was led by a rebound in exports of cars and car parts, which have seen easing supply constraints.

Contrasting with export trends, imports fell by -2.3% yoy to JPY 8721B, the first annual decline witnessed in 27 months. This decrease was largely attributed to a slump in imports of crude oil and liquefied natural gas. Consequently, Japan recorded a trade deficit of JPY -432B for the 21st month running.

In seasonally adjusted term, the situation presents a slightly different picture. Exports rose by 2.5% mom to JPY 8259B, while imports inched up by 0.1% mom to JPY 9276B. In light of this, trade deficit narrowed to JPY -1017B.

Looking ahead

Canada new housing price index will be released in European session. US will release jobless claims, Philly Fed survey and existing home sales.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6634; (P) 0.6654; (R1) 0.6678; More...

AUD/USD's fall resumed after brief recovery and intraday bias is back on the downside for retesting 0.6563 low. As noted before, consolidation pattern from 0.6563 could have completed with three waves to 0.6817.Decisive break of 0.6563 will resume larger decline from 0.7156 to 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. On the upside, above 0.6708 minor resistance will turn intraday bias neutral again first.

In the bigger picture, the failure to break through 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Firm break of 61.8% retracement of 0.6169 to 0.7156 at 0.6546 will raise the chance of long term down trend resumption through 0.6169 low. This will now be the favored case as long as 0.6817 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q1 | 0.20% | 0.50% | 0.50% | |

| 22:45 | NZD | PPI Output Q/Q Q1 | 0.30% | 0.80% | 0.90% | |

| 23:50 | JPY | Trade Balance (JPY) Apr | 0.80% | -1.08T | -1.21T | |

| 01:30 | AUD | Employment Change Apr | -4.3K | 25K | 53K | 61.1K |

| 01:30 | AUD | Unemployment Rate Apr | 3.70% | 3.50% | 3.50% | |

| 12:30 | CAD | New Housing Price Index M/M Apr | -0.10% | 0.00% | ||

| 12:30 | USD | Initial Jobless Claims (May 12) | 260K | 264K | ||

| 12:30 | USD | Philadelphia Fed Survey May | -20 | -31.3 | ||

| 14:00 | USD | Existing Home Sales Apr | 4.35M | 4.44M | ||

| 14:30 | USD | Natural Gas Storage | 109B | 78B |