Sample Category Title

BoE Bailey: Will adjust rate further if inflation pressures persist

BoE Governor Andrew Bailey pledged in a speech, "I can assure you that the MPC will adjust Bank Rate as necessary to return inflation to target sustainably in the medium term, in line with its remit."

"If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required," he added.

In the baseline modal projection of May Report, which is conditional on a market-implied path for interest to peak at 4.75% in Q4, inflation will fall materially below the 2% target in the medium term."

However, he noted, "risks to inflation are skewed significantly to the upside", primarily reflecting the possibility of more persistence in domestic wage and price setting. Also, the "unwinding of second-round effects may take longer than it did for them to emerge".

This "asymmetry" was not made as part of the baseline modal projection. Instead, "we think of this as a material upside risk to the inflation outlook over the medium term."

What about the Dollar? Debt Default Hangs in the Balance as the US Tries to Garner Confidence

The US government is currently actively engaged in attempting to talk its way out of a potential default on its national debt as the ceiling which is imposed by US law is being reached to the extent that if something is not done, the country's government could run out of money in just two weeks' time.

The myriad of reports which now adorn the internet cover all manner of potential outcomes, including that the calculations have been done and that the US government has enough to cover its debt until and beyond June 1.

This mantra is not necessarily to be taken at face value, however, because debt talks are currently in progress at the White House, meaning that there is a potential need for the government to raise the debt ceiling, something that can be done by the US government periodically if needed.

There is no current consensus on exactly which way the outcome will go; whether the US will actually default on its debt, whether the debt is serviceable and it can carry on as it is, or whether the ceiling will be raised and the country will borrow more money.

However, if a default were to happen, what would happen to the US dollar?

It is, after all, the currency issued by the indebted government, which the Federal Reserve is the central bank for.

Firstly, and perhaps most obviously, the US Dollar could potentially depreciate as investors lose confidence in the country's ability to meet its financial obligations, leading to a possible rise in value by the British pound and the euro against the US dollar.

Yes, the US economy has now got its inflation under control at approximately 6% compared to the European side of the Atlantic's 11% in the West to 25% in some parts of Eastern Europe, but a debt default by a national government is a very serious matter as it is a mark of national insolvency.

The second possible outcome is that forex traders and investors may dump the Dollar and head toward some safe-haven currencies, such as the Swiss franc, in order to trade on a more even keel than a potentially volatile US dollar.

Thirdly, traders of physical commodities that are traditionally regarded as stores of value may ramp up their portfolios. Gold, silver, and consumable commodities such as crude oil may become interesting asset classes as demand for oil is being created via the OPEC countries' current slowdown of production, and precious metals are often used as stores of value at times of national currency volatility.

The fourth area in which the markets may be affected is currency volatility. Major currencies are often subject to minor movements due to their widespread use as de facto settlement currencies and the global dominance of the central banks that issue them as bastions of stability in the financial markets ecosystem.

However, a debt default by the United States would represent the insolvency of the world's benchmark economy; therefore, sharp fluctuations between the US Dollar and its major peers such as the Yen, Euro, Pound, and Swiss Franc may occur.

Lastly, disruption of the global financial markets could be a factor to consider. The wider commodities, equities, stock, and bond markets may be subject to traders and investors dumping toxic US stocks or bonds and realising their value quickly in order to avoid any possible uncertainty of future value in a world in which the United States is insolvent.

Of course, it may come to pass that a default does not happen. It also may come to pass that in order to avoid a default, the US borrows more money.

If that occurs, we all have to ask ourselves if that is really a way out or if it is just a way to become even more burdened and nationally insolvent without actually having it written down by debt insolvency administrators.

BTCUSD Remains Suppressed by 50-SMA

BTCUSD has been generating a structure of lower highs and lower lows after peaking at the 10-month high of 31,064 in mid-April. Even though the digital coin found its feet at the May bottom of 25,785 and attempted a rebound, it has been repeatedly held down by its 50-period simple moving average (SMA).

The momentum indicators currently suggest that near-term risks are tilted to the downside. Specifically, the RSI has flatlined beneath its 50-neutral mark, while the stochastic oscillator is descending sharply near the 20-oversold zone.

Should the 50-period SMA continue to cap the price’s upside, Bitcoin could decline towards 26,661, which is the 38.2% Fibonacci retracement of the 19,540-31,064 upleg. A break below that wall may set the stage for the May bottom of 25,785. Failing to halt there, the price might then challenge the 50.0% Fibo of 25,302.

Alternatively, bullish actions could propel the price towards the recent rejection region of 27,675. If that barricade fails, the spotlight may turn to the 23.6% Fibo of 28,344 before buyers attack the 30,000 psychological mark. Even higher, the 10-month peak of 31,064 could curb any upside moves.

Overall, BTCUSD has been stuck in a bearish pattern since mid-April, while its latest efforts for a recovery have been repelled multiple times by the 50-period SMA. Thus, a clear break above the 50-period SMA is needed to revive bulls’ hopes for a trend reversal.

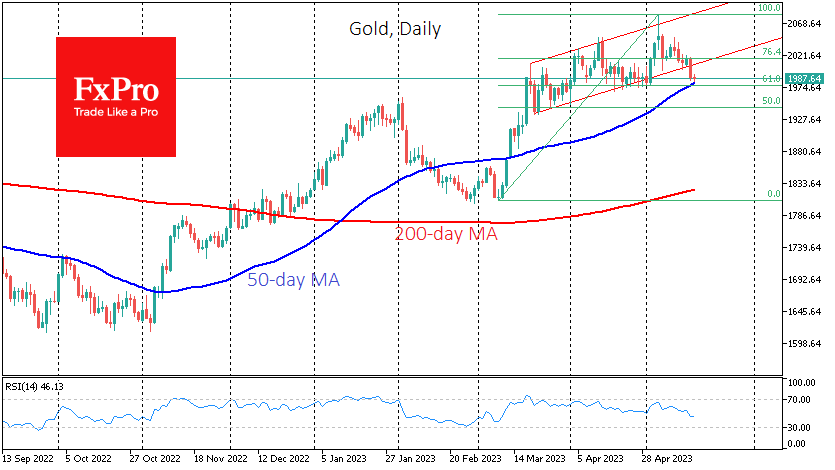

Will Gold Have Another Bearish Round?

Gold attempted to recover some lost ground earlier in the day, but its bullish efforts proved short-lived around 1,993 in the four-hour chart as the broken support trendline switched to resistance.

The focus has turned back to the key support region of 1,976, which overlaps with the 38.2% Fibonacci retracement of the 1,804-2,079 uptrend. Given the oversold signals coming from the RSI and the Stochastic oscillator, there is a potential for an upside correction or some consolidation near that level. If selling forces persist, the precious metal may seek shelter around February’s peak of 1,960. The 50% Fibonacci level of 1,945 could next protect the market from sellers reaching the crossroads of two key trendlines around 1,925.

On the upside, there are several obstacles which could ruin potential bullish actions. Above the 1,993 mark, the simple moving averages (SMAs) and the 23.6% Fibonacci level could immediately cap the price within the 2,005-2,015 territory. Notably, the short-term descending trendline is placed in the same territory. Then, the steeper support-turned-resistance trendline at 2,028 could be another hurdle, blocking the way towards the crucial 2,048 barrier. Beyond the latter point, all the attention will shift to the record high of 2,079.

All in all, gold is facing a discouraging situation, likely preparing for another bearish round following the pullback from 1,993. Yet, selling pressures might prove limited as the key floor of 1,976 is nearby.

Gold Cools Off After the Rally and Chooses a Path Forward

Gold had made impressive moves yesterday before active trading in New York. Still, comments from Fed officials, combined with the release of relatively strong industrial production data, pushed the price back almost $30 to $1990, where it remains at the time of writing.

The Fed’s Loretta Meister noted yesterday that US interest rates have not yet reached a level where the central bank could stop tightening, given the resilience of inflation. Influential Fed member John Williams noted that inflation is “gradually moving in the right direction” but remains “unacceptably high”.

In addition, the bond markets took a positive view of the outcome of the McCarthy-Biden meeting to discuss the debt ceiling, although no agreement was reached.

The market also reacted positively to the Fed’s report on industrial production growth of 0.5% in April, of which the manufacturing sector added 1%, much higher than expected.

As a result, the market is again pricing in more than a 20% chance of another rate hike in mid-June. These are far from extreme levels, as the probability has been above 30% since the second half of April. Nonetheless, this revision of expectations is creating some pull for the dollar. The dollar index has risen by 2% since last week, putting pressure on precious metals and cryptocurrencies.

As a result of yesterday’s fall, gold has broken out of the bullish range formed at the end of March. Gold is now close to the April lows from which it was then supported.

At the same time, gold is approaching its 50-day moving average, above which it rallied at the end of last year and confirmed in March. At just below $1970 is the 61.8% retracement level of the rally from the March lows to the early May highs.

From this perspective, a sharp pullback below $1980 would be an essential signal of a change in market sentiment, forcing a further drop to $1950 (the February high).

However, the fall below the $1980 scenario does not yet appear mainstream. The recent pullback has cleared the overbought conditions on the daily timeframes and opened the way to the upside.

The next advance could take gold to new highs if it finds some support. A technical target for the bulls could be the $2250 level, representing 161.8% of the last two-month rally. The 12-month target for the gold bugs seems to be an ambitious $2640.

Australian Dollar Calm after Wage Growth Accelerates

- Australia wage growth accelerates in Q1

- JP Morgan expects Fed to trim rates

The Australian dollar is steady on Wednesday. AUD/USD is trading at 0.6650 in Europe, down 0.06% on the day.

Australian wage growth rises

Australia’s wage price index jumped in the first quarter. Wage growth rose 3.7% y/y, following an upwardly revised 3.4% in Q4 2022 and above the estimate of 3.6%. On a quarterly basis, wages rose 0.8%, unchanged from Q4 and just below the estimate of 0.9%.

The RBA is determined to bring inflation back down to the 2% target, and 3.7% wage growth is simply too high for the central bank. This supports an argument for the RBA to lift rates at the June meeting (or later down the road). The markets have priced in a 100% probability of a pause in June, according to the ASX RBA Rate Tracker.

The RBA minutes from the May meeting noted that the decision to raise rates was a close one, but concerns about inflation becoming entrenched won out and the Bank hiked by 25 basis points. The minutes didn’t provide much guidance for future moves, with policy makers saying further rates might be required, depending on economic and inflation data.

The Federal Reserve trotted out some members earlier this week to reiterate that no rate cuts are coming, and market pricing for a rate cut before the end of the year have fallen. According to CME’s FedWatch, the odds of a cut in September are 52%, compared to 72% a week ago. Still, there is support for rate cuts. JP Morgan said on Tuesday that “the market is right to be penciling in cuts”, as inflation remains too high and the US was likely headed for a recession.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6699. This is followed by 0.6761

- 0.6579 and 0.6517 are providing support

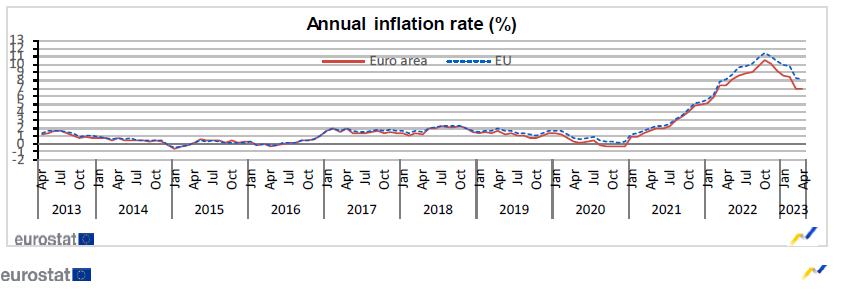

Eurozone CPI finalized at 7% yoy in Apr, CPI core at 5.6% yoy

Eurozone CPI was finalized at 7.0% yoy in April, up from March's 6.9% yoy. The highest contribution to came from food, alcohol & tobacco (+2.75%), followed by services (+2.21%), non-energy industrial goods (+1.62%) and energy (+0.38%). CPI core (excluding energy, food, alcohol & tobacco) was finalized at 5.6% yoy, down from prior month's 5.7% yoy.

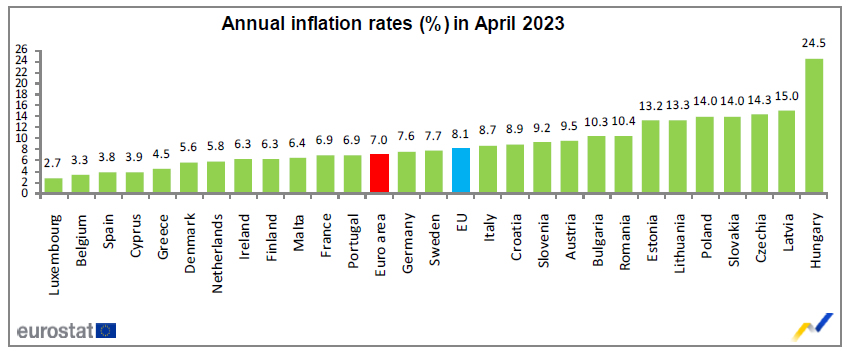

EU CPI was finalized at 8.1% yoy. The lowest annual rates were registered in Luxembourg (2.7%), Belgium (3.3%) and Spain (3.8%). The highest annual rates were recorded in Hungary (24.5%), Latvia (15.0%) and Czechia (14.3%). Compared with March, annual inflation fell in twenty-two Member States and rose in five.

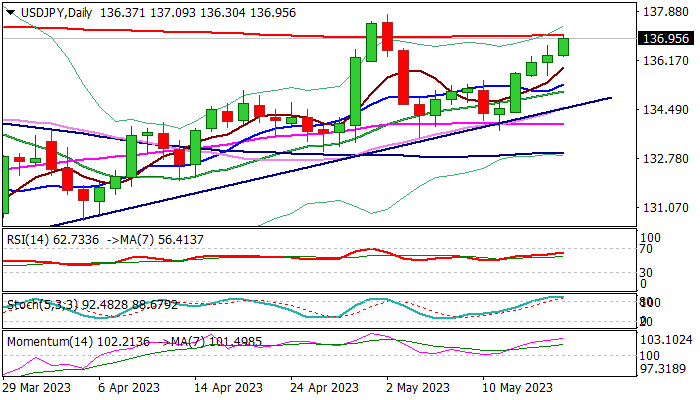

USD/JPY: Key Barriers in Focus But Consolidation Likely to Precede Attack

Strong bullish acceleration extends into fifth straight day and cracks 200DMA (137.05), with key barriers at 137.77 (May 2 top) and 137.90 (Mar 8) in focus.

Daily studies in full bullish setup support the action, along with last Thursday’s strong downside rejection at the trendline support/55DMA (which left a bear-trap) and subsequent rally on Friday (up 1%, the biggest daily gain since Apr 28).

Violation of 134.77/90 pivot would generate strong bullish signal for continuation of larger recovery rally from 127.22 (2023 low of Jan 16) and expose targets at 139.58 (50% retracement of 151.94/127.22) and 140.00 (psychological).

However, overbought conditions warn of headwinds which could keep the action on hold for consolidation/limited correction.

Extended dips should find ground above rising 10DMA (135.34) to keep bulls in play for fresh push higher.

Res: 137.54; 137.77; 137.90; 138.17.

Sup: 136.30; 135.93; 135.34; 134.89.

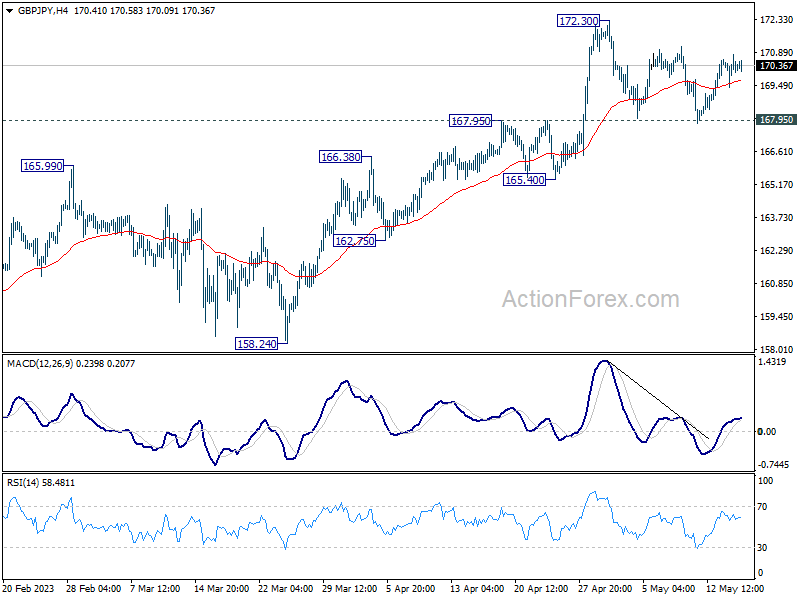

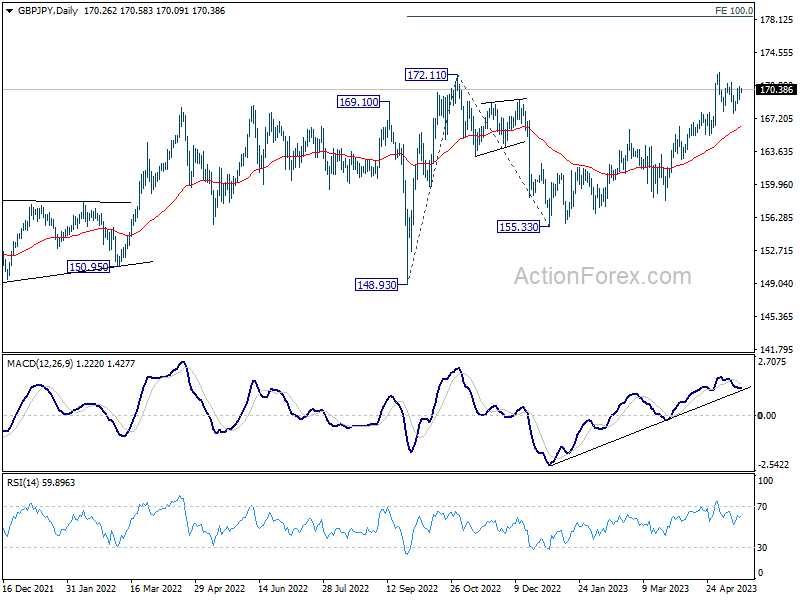

GBP/JPY Daily Outlook

Daily Pivots: (S1) 169.52; (P) 170.17; (R1) 170.94; More...

Intraday bias in GBP/JPY remains neutral first and outlook is unchanged. On the upside, break of 172.30 will resume larger up trend to 100% projection of 148.93 to 172.11 from 155.33 at 178.51. Nevertheless, firm break of 167.95 should confirm short term topping, and turn bias back to the downside for deeper pull back to 165.40 support and possible below instead.

In the bigger picture, focus stays on 172.11 resistance (2022 high). Decisive break there will resume whole up trend from 123.94 (2020 low). Next target will be 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. Nevertheless, firm break of 165.40 support will indicate rejection by 172.11 and extend the corrective pattern from there with another falling leg.

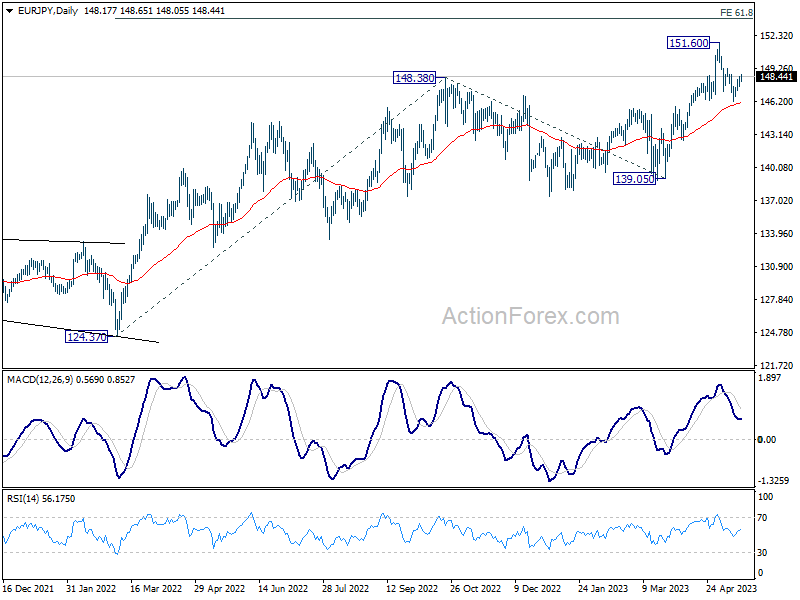

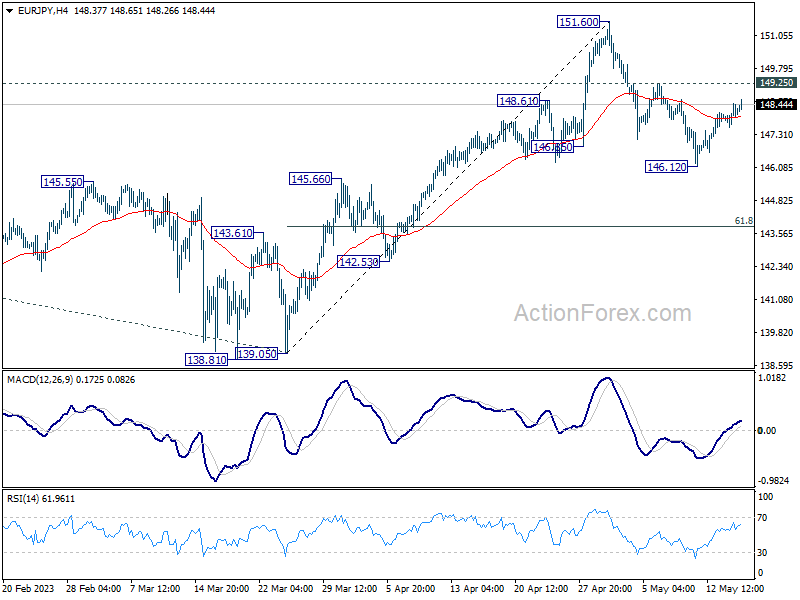

EUR/JPY Daily Outlook

Daily Pivots: (S1) 147.67; (P) 148.09; (R1) 148.56; More....

No change in EUR/JPY's outlook and intraday bias stays neutral. Further decline is in favor as long as 149.25 resistance holds. Sustained trading below 55 D EMA (now at 146.01) will bring deeper pull back to 61.8% retracement of 139.05 to 151.60 at 143.84. On the upside, though, firm break of 149.25 will turn bias back to the upside for retesting 151.60 high instead.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 139.05 support holds, even in case of deep pull back.