Sample Category Title

What Lies Ahead for the Crypto Market?

Here's the latest scoop: Paul Tudor Jones, the billionaire hedge fund manager, seems concerned about Bitcoin's appeal. He believes the growing unfriendly regulatory landscape in the United States makes Bitcoin less attractive. Additionally, the prospect of lower inflation and its impact on Bitcoin's price has got him a bit worried too. In a recent interview, Jones shared his thoughts on Bitcoin and the US economic scenario, painting a rather pessimistic picture. He mentioned how Bitcoin and Gold had lost some of their bullish charm as the whole "inflation hedge" narrative seems to be losing steam. But wait, there's more! The US government's tough stance on cryptocurrencies has also caught Jones' attention. The increased skepticism and scrutiny from regulatory bodies have made the crypto industry a hot topic. Despite his concerns, Jones still holds on to a small amount of Bitcoin in his investment portfolio. He believes that Bitcoin's finite supply, which humans can't manipulate, sets it apart from other assets. So, while he may have reservations, he's sticking with them. Let's see how these factors might impact Bitcoin's future!

US Dollar - H4 Timeframe

The US Dollar recovered spontaneously last week in response to the release of the CPI news. The resultant bullish movement broke out of a triangle pattern and is approaching a major supply zone on the Daily timeframe. My expectation based on this is that we should see a rejection from the supply zone that could push prices back to the trendline of the triangle pattern.

Analyst’s Expectations:

- Direction: Bearish

- Target: 102.420

- Invalidation: 103.550

BTCUSD - H4 Timeframe

The strength of the US Dollar, coupled with the unfriendly sanctions in the United States, as previously mentioned in the introduction, has impacted the price action on the BTCUSD chart: the bearish price action on the chart, as seen above, is proof. However, the price is currently approaching a key area of support. It is expected to rebound off that area based on the projection of an impending US Dollar's impending weakness, as discussed earlier.

Analyst’s Expectations:

- Direction: Bullish

- Target: $27961.46

- Invalidation: $25394.90

ETHUSD - Daily Timeframe

The overlap of the trendline support and the 100-Day moving average is a key confluence supporting a bullish reaction. The moving averages on the Daily timeframe of the ETHUSD chart are also arrayed in ascending order, another confirmation of a bullish trend. Correlating the technical analysis of Ethereum with the forecast from the US Dollar, I have reason to expect a bullish reaction from the highlighted pivot zone.

Analyst’s Expectations:

- Direction: Bullish

- Target: $1886.84

- Invalidation: $1724.66

XRPUSD - Daily Timeframe

XRPUSD seems to have already commenced its bullish reaction from the support area, originating from the overlap of the trendline support and the 200-Day moving average. Similar to what we saw on the ETHUSD chart, the moving averages on Ripple are also arrayed in ascending order - another indication of likely bullish price action. My conclusion on this is that we will see some continuation of the bullish movement until the price hits the pivot zone I have highlighted.

Analyst’s Expectations:

- Direction: Bullish

- Target: $1889.51

- Invalidation: $1707.62

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

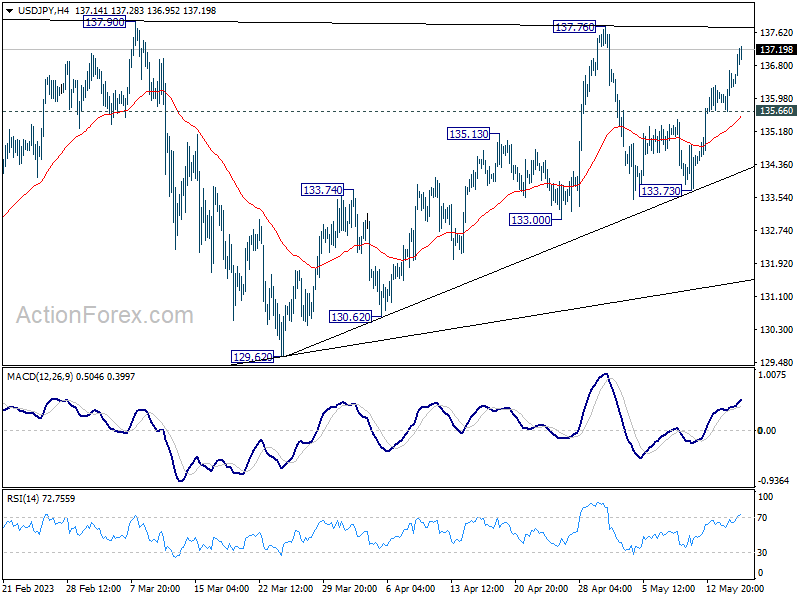

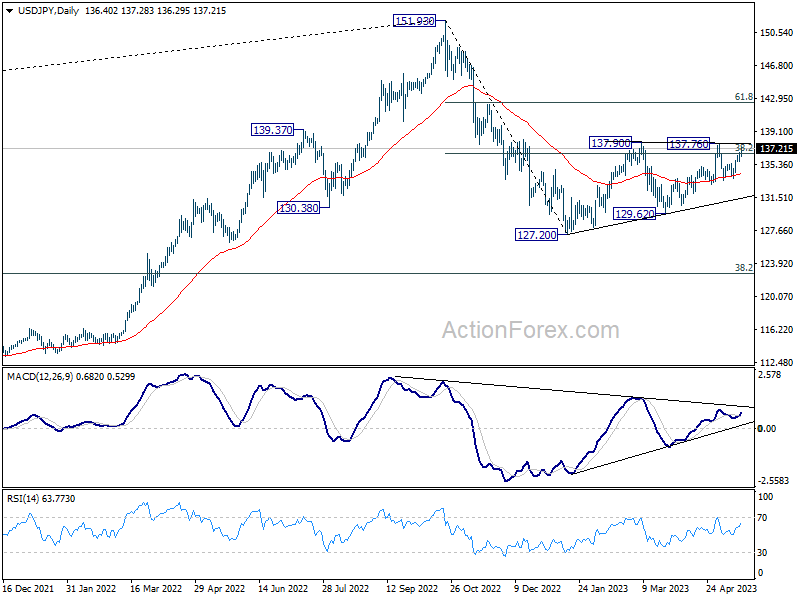

USD/JPY – Japan’s GDP Improves But Yen Slips

- USD/JPY climbs above 137

- Japan’s GDP surprises to the upside

- JP Morgan expects Fed to trim rates

The Japanese yen is on a four-day losing streak and is in negative territory on Wednesday. In the North American session, the yen is trading at 137.39, up 0.74% on the day.

Japan’s GDP beats estimate

Japan’s GDP in the first quarter was higher than expected. The economy grew by 1.6% y/y, after a 0.1% decline in Q4 2022 and easily beat the estimate of 0.7%. On a quarterly basis, GDP expanded by 0.4%, up from 0.0% in Q4 and above the estimate of 0.1%.

One key driver behind the spurt in growth was personal consumption, as demand continues to rise now that the country has reopened. The services sector remains strong but manufacturing continues to struggle. On a sour note, exports fell 4.2% in Q4, as demand for semiconductors and automobiles declined.

The uptick in growth means that sustainable inflation could stay above 2%, and that could prod the Bank of Japan to take steps toward normalization, such as adjusting its yield curve control (YCC) policy. The BoJ has said it would consider tightening policy if inflation is sustainable above 2%, but any shifts in policy are likely to be small, especially if the yen remains weak. The BoJ announced it would conduct a policy review which could take a year or more, and I would not expect the BoJ to raise rates before 2024.

Federal Reserve members continued to remind listeners that more rate hikes are possible if inflation stays high. The Fed has also tried to dampen expectations of rate cuts in the second half of the year. The markets are listening somewhat, as the odds of a rate cut this year have fallen. JP Morgan came out in support of rate cuts on Tuesday, saying that “the market is right to be penciling in cuts”, as inflation remains too high and the US was likely headed for a recession.

USD/JPY Technical

- USD/JPY is testing resistance at 137.08. Above, the next resistance line is 138.42

- There is support at 136.26 and 135.08

Sunset Market Commentary

Markets

A summer lull is the well-known phenomenon of a short period of calm in which little happens. Afterwards, business picks up again. Lesser known is the spring lull. In case you wondered, we’re in the middle of it. Core bonds are trading rangebound and stock markets cede some ground after testing important resilience levels earlier this year. The dollar manages to regain momentum as the relative yield spread (US/GE 2y) is correcting back in the greenback’s favour. EUR/USD fell to the lowest level since early April around 1.0820. The 100d simple moving average provides support as it did in March. EUR/GBP follows EUR/USD south with the pair remaining below support lost last week around 0.8720. BoE governor Bailey spoke at the Global Annual Conference of the British Chambers of Commerce, but his speech lacked guidance for June. “While we expect CPI inflation to fall quite sharply as energy costs begin to ease, albeit at a somewhat slower pace than projected in February given the near-term outlook for food prices, the outlook for inflation further out is more uncertain and depends on the extent of persistence in wage and price setting.” The UK central bank is firmly in data dependence mode. Bailey specifically mentioned trends in wages, job vacancies and core inflation.

The current spring lull bridges the period between May policy meetings by ECB/Fed and first relevant datapoints for the June updates. A 25 bps ECB rate hike and a conditional Fed pause are the benchmarks against which they’ll be checked. Next week’s EMU PMI’s are the amuse-bouche ahead of EMU inflation and US payrolls thereafter. Simultaneously with the eco pause, regional US banking shares are recovering from the lows as they gradually see some new deposit inflows. Everybody’s talking about the US debt ceiling debate with X-date (default date) early June, but apart from US T-bills and US CDS levels, there’s no sign of stress. Markets probably aren’t worrying until we’re effectively days/hours away from a default. All of this combined creates the low volatility spring lull we’re currently in.

News & Views

The deal under which Russia allows Ukraine safe grain export from its Black Sea ports lapses on Thursday. The UN and Turkey brokered the deal in July last year for an initial 120 days in a bid to prevent a global food crisis from escalating. The deal was extended in November for another 120 days and then for 60 days back in March, helping corn prices ease from multiyear highs of >$800/bushel mid-2022 to $571 currently. Russia had threatened to quit the deal as restrictions on payments, logistics and insurance posed a barrier to shipments, even as Russian exports of food and fertilizer are not subject to Western sanctions. Bloomberg, citing Turkish officials, in the meantime reported that the deal is set to be extended anyway. An official announcement should follow later today.

Hungary’s foreign minister Szijarto said it will block a further €500 million tranche of European financial assistance to Ukraine for now, adding that it is also reluctant to back further sanctions against Russia. One of the reasons underpinning the decision was Ukraine’s move to add Hungary’s largest lender to its list of international war sponsors and as such risk harming the lender’s reputation. As long as this is the case, Hungary “can’t support decisions requiring new economic and financial sacrifice on the part of the European Union and its member states”. The Hungarian forint lost ground after Szijarto ‘s comments with EUR/HUF bouncing of critical support just below 370 to 371.3 currently. Investors fear it will further complicate the disbursement of billions of EU funds to Hungary – which are officially blocked over a rule of law dispute. But the country’s stance vs Ukraine (aid) has often been to the dismay of the EU which has previously used the blocked resources as a leverage in the discussions.

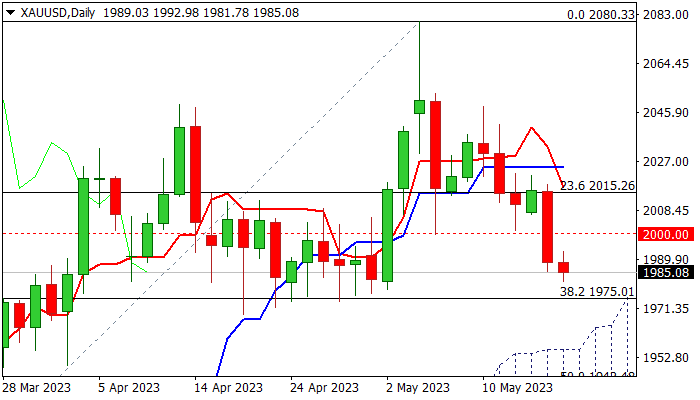

XAU/USD: Bears Firmed on Loss of $2000 But Face Significant Supports at $1975/55

Gold price remains at the back foot on Wednesday and hit new two-week low, in extension of Tuesday’s 1.3% fall which also registered a daily close below psychological $2000 level for the first time since May 1.

The metal came under increased pressure on the latest hawkish comments from Fed officials, who played down prospects for rate cuts this year, but pointed to central bank’s super strong stance in fighting high inflation.

This revived expectations for another rate hike, against still high percentage forecast that the Fed is about to pause its tightening cycle, as signaled after the last policy meeting, deflating the non-interest bearing metal.

Daily chart structure weakened on break of $2000 handle, daily Tenkan-sen crossed below Kijun-sen, 14-d momentum is at the border line and the action is weighed by Tuesday’s large bearish candle, but stochastic is oversold.

However, fresh bears still face strong supports at $1975 (higher base/Fibo 38.2% of $1804/$2080) and $1955 (top of rising daily Ichimoku cloud which underpins the action) where strong headwinds should be anticipated, and bears are unlikely to break them on first attempt.

Near-term bias is expected to remain with bulls while the action stays above $1975, though the downside would remain vulnerable while $2000 caps.

Bounce and close above $2000, as minimum requirement for initial reversal signal, would improve near-term picture, however verification of the signal will still require acceleration above daily Kijun-sen ($2024).

Res: 1992; 2000; 2015; 2024.

Sup: 1975; 1969; 1955; 1942.

US: Housing Starts Rose and Permits Fell in April

Housing starts rose by 2.2% month-on-month (m/m) in April to 1.40 million (annualized) units, in-line with consensus expectations. Revisions to the three prior months were negative, subtracting roughly 39k units from the previous reported tallies.

Starts in the single-family segment rose by 1.6% m/m (or 13k units) after falling by 0.2% in March. Multi-family starts also ticked up, rising by 3.2% m/m (or 17k units) after seeing a sharp decline in the previous month.

Residential permits fell in April by 1.5% m/m to 1.42 million units. The decline was led by a strong reduction in multi-family permitting which fell for a second consecutive month. Meanwhile, single-family permits rose for a third consecutive month in April, ticking up by 3.1% m/m.

Among the four Census regions, housing starts fell in the Northeast (-23.4% m/m) and the South (-6.3% m/m). The West and Midwest regions each recorded sizeable monthly gains of 34.6% m/m and 32.6% m/m, respectively.

Key Implications

Homebuilding activity was mixed in April, with starts picking up in both the single-family and multi-family segments, while permitting activity fell for a second month on multi-family weakness. However, single-family permitting activity has seen a solid rebound to start 2023 after contracting for most of last year. While there are some signs of positivity in this report, starts and permits each remain roughly 20% below year-ago levels.

The National Association of Home Builders' Housing Market Index – a measure of homebuilder sentiment in the single-family market – rose for a fifth consecutive month in May to its highest level since July 2022. Homebuilders have become increasingly optimistic about the outlook for residential construction as the past few years of excess demand has drained the housing market of supply. In addition, with mortgage rates remaining near a 15-year high, many potential sellers cannot afford to re-enter the market, which has kept the stock of existing homes for sale low. With new homes now making up roughly one-third of all sales, residential construction is expected to continue to play a large role in returning affordability to the U.S. housing market.

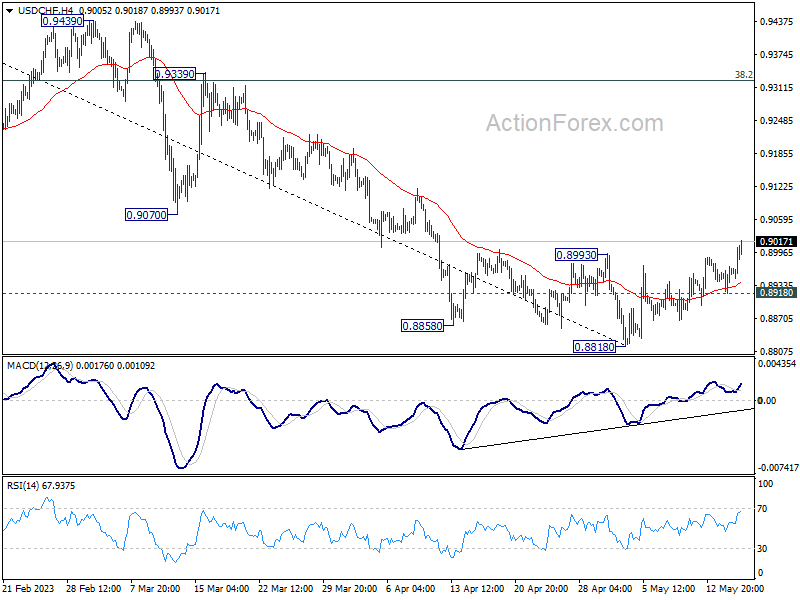

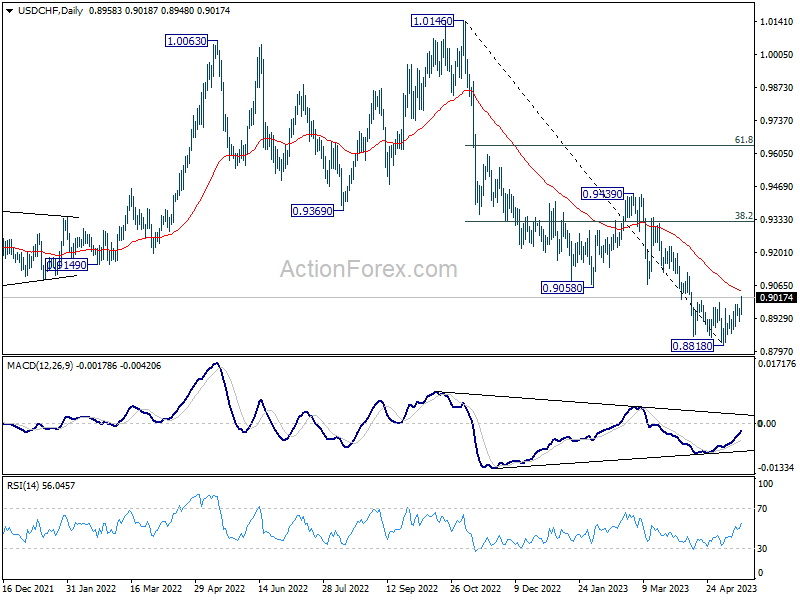

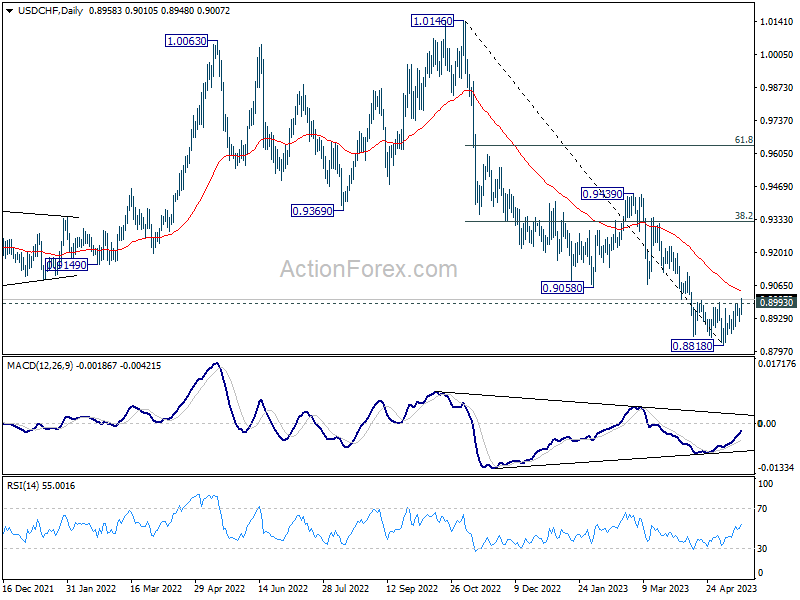

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8932; (P) 0.8951; (R1) 0.8983; More...

USD/CHF's break of 0.8993 resistance confirms short term bottoming at 0.8818, ahead of 0.8756 long term support. Intraday bias is back on the upside for 55 D EMA (now at 0.9045). Sustained break there should confirm that it's at least correcting whole down trend from 1.0146. Further rally would be seen to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, below 0.8918 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 135.82; (P) 136.26; (R1) 136.82; More...

Intraday bias in USD/JPY remains on the upside for the moment. Decisive break of 137.76/90 resistance zone will resume whole rebound from 127.20. Next target is 142.48 fibonacci level. On the downside, below 135.60 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rise to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

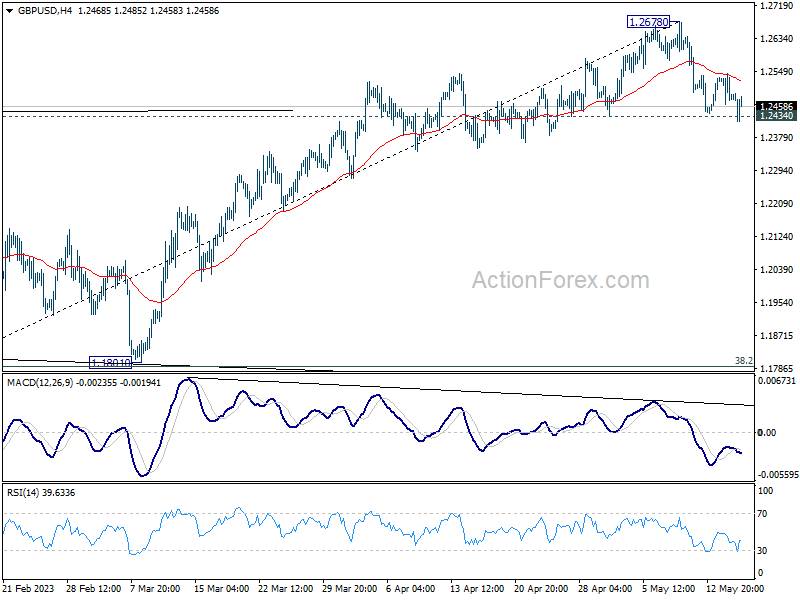

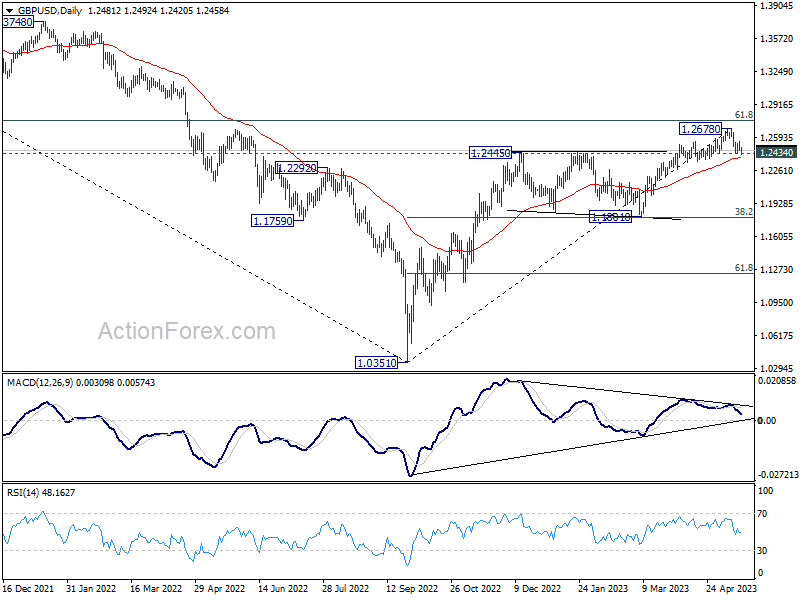

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2452; (P) 1.2499; (R1) 1.2532; More...

GBP/USD recovered after brief breach of 1.2434 support and intraday bias stays neutral first. On the downside, firm break of 1.2434 will confirm short term topping at 1.2678, on bearish divergence condition in 4H MACD. Intraday bias will be back on the downside for 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789), as correction to whole up trend from 1.0351. On the upside, however, break of 1.2678 will resume larger up trend from 1.0351 instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

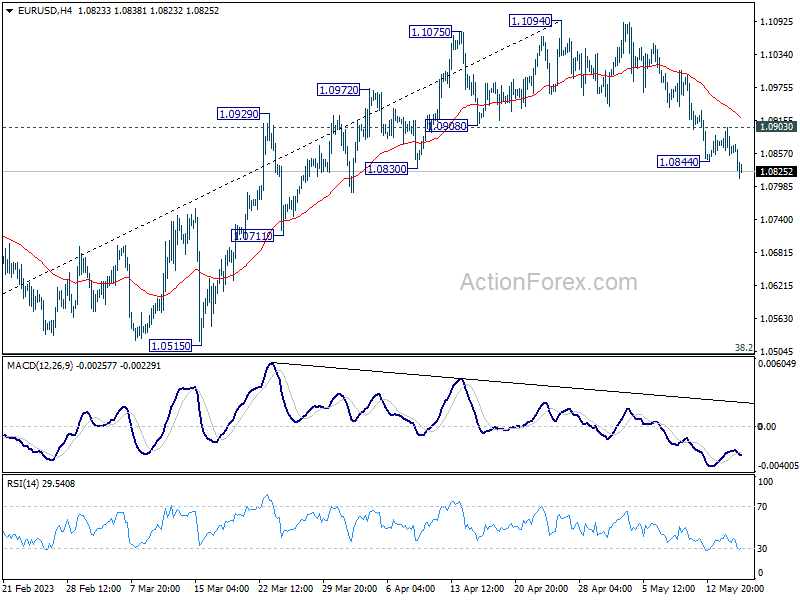

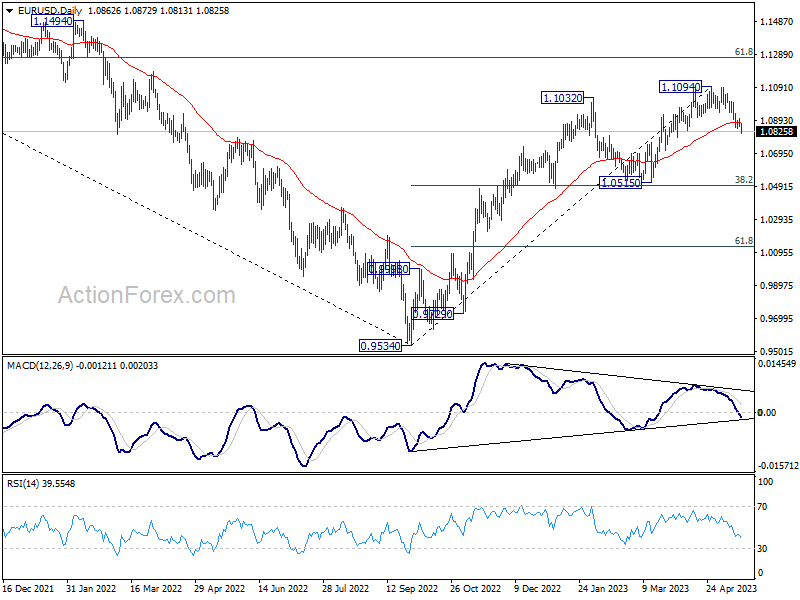

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0844; (P) 1.0874; (R1) 1.0894; More...

EUR/USD's fall from 1.1094 short term top resumed after brief consolidations. Intraday bias is back on the downside. Current fall is seen as correcting whole up trend from 0.9534. Deeper decline would be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, above 1.0903 minor resistance will turn intraday bias neutral first.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Dollar Extending Rally Against Euro and Swiss Franc, Sentiment Flip-Flops

Market sentiment continue to flip-flop on flowing headlines regarding US debt ceiling negotiations. But then, it should be remembered that it's not done until it's done. So uncertainties and volatility still lie ahead. Yen is the consistent one extending its near term decline. Commodity currencies are rebounding with Sterling. But the more important development is in Dollar's rally extension against Euro and Swiss France.

Technically, USD/CHF's break of 0.8993 resistance today now argues that rebound from 0.8818 might at least correcting whole fall from 1.0146. This is supported by bullish convergence condition in D MACD. Next focus is the resistance zone between 55 D EMA (now at 0.9044) and 0.9058 support turned resistance. Sustained break there will affirm this case and bring further rally to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. Meanwhile, to aid the rally, EUR/CHF better takes out 0.9780 minor resistance too.

In Europe, at the time of writing, FTSE is down -0.05%. DAX is up 0.49%. CAC is up 0.15%. Germany 10-year yield is down -0.0424. Earlier in Asia, Nikkei rose 0.84%. Hong Kong HSI dropped -2.09%. China Shanghai SSE dropped -0.21%. Singapore Strait Times dropped -1.25%. Japan 10-year JGB yield dropped -0.0264 to 0.369.

BoE Bailey: Will adjust rate further if inflation pressures persist

BoE Governor Andrew Bailey pledged in a speech, "I can assure you that the MPC will adjust Bank Rate as necessary to return inflation to target sustainably in the medium term, in line with its remit."

"If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required," he added.

In the baseline modal projection of May Report, which is conditional on a market-implied path for interest to peak at 4.75% in Q4, inflation will fall materially below the 2% target in the medium term."

However, he noted, "risks to inflation are skewed significantly to the upside", primarily reflecting the possibility of more persistence in domestic wage and price setting. Also, the "unwinding of second-round effects may take longer than it did for them to emerge".

This "asymmetry" was not made as part of the baseline modal projection. Instead, "we think of this as a material upside risk to the inflation outlook over the medium term."

Eurozone CPI finalized at 7% yoy in Apr, CPI core at 5.6% yoy

Eurozone CPI was finalized at 7.0% yoy in April, up from March's 6.9% yoy. The highest contribution to came from food, alcohol & tobacco (+2.75%), followed by services (+2.21%), non-energy industrial goods (+1.62%) and energy (+0.38%). CPI core (excluding energy, food, alcohol & tobacco) was finalized at 5.6% yoy, down from prior month's 5.7% yoy.

EU CPI was finalized at 8.1% yoy. The lowest annual rates were registered in Luxembourg (2.7%), Belgium (3.3%) and Spain (3.8%). The highest annual rates were recorded in Hungary (24.5%), Latvia (15.0%) and Czechia (14.3%). Compared with March, annual inflation fell in twenty-two Member States and rose in five.

Japan's economy bounced back in Q1, up 1.6% annualized, 0.4% qoq

Japan's economy delivered a robust performance in Q1, expanding at annualized rate of 1.6%, which significantly surpassed expectation of 0.7%. This marks the first expansion in three quarters, thanks to a potent combination of strong private consumption and a rebound in inbound tourism.

In terms of real GDP, adjusted for inflation, there was an increase of 0.4% qoq, beating the forecast growth of 0.1% qoq. The positive data signals a welcome resurgence in Japan's economy, signaling a potential turn-around after short period of technical recession.

Looking into the details, private consumption for the quarter rose by 0.6%, driven by robust demand for cars and durable goods. Concurrently, consumers boosted spending on services such as dining out, culminating in the fourth consecutive quarterly gain. Meanwhile, capital spending rose by 0.9%, aided by increased car-related investments and marking the first increase in two quarters.

However, not all sectors exhibited positive trends. Exports took a hit, declining by -4.2% due to a slump in shipments of cars and machinery used for chip production. Imports also fell by 2-.3%. Public investment remained largely flat.

Australia wage growth accelerated to 0.8% in Q1, highest in over a decade

Australia wage price index posted 0.8% qoq increase in Q1 2023, slightly short of expected 0.9% rise. Despite this, annual wage growth accelerated to 3.7%, marking the highest level since Q3 2012. This uptick is attributable to a combination of factors, including low unemployment, tight labour market, and high inflation.

Private sector emerged as the primary engine of growth, with wages climbing 0.8% over Q1 and experiencing an annual rise of 3.8%. According to Leigh Merrington, ABS's acting head of prices statistics, several private sector industries witnessed an annual wage growth exceeding 4%, with the remaining industries all recording an annual growth above 3%.

In the public sector, the highest quarterly (0.9%) and annual (3.0%) wage growth in a decade was reported. Increase in public sector wages is attributed to outcomes from enterprise agreement bargaining, regular scheduled rises, and higher wage caps.

Merrington further highlighted wage outcomes for Q1 2023, stating, "There was a continued lift in the share of jobs receiving wage rises of between 4 and 6 per cent, which is the highest share since 2009. The share of jobs with a wage rise of 2 per cent or less has fallen from over 50 per cent in mid-2021 to less than 20 per cent."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0844; (P) 1.0874; (R1) 1.0894; More...

EUR/USD's fall from 1.1094 short term top resumed after brief consolidations. Intraday bias is back on the downside. Current fall is seen as correcting whole up trend from 0.9534. Deeper decline would be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, above 1.0903 minor resistance will turn intraday bias neutral first.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Annualized Q1 P | 0.40% | 0.20% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | 2.00% | 2.00% | 1.20% | |

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.80% | 0.90% | 0.80% | |

| 04:30 | JPY | Industrial Production M/M Mar F | 1.10% | 0.80% | 0.80% | |

| 08:00 | EUR | Italy Trade Balance (EUR) Mar | 7.54B | 2.50B | 2.11B | |

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 7.00% | 7.00% | 7.00% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr F | 5.60% | 5.60% | 5.60% | |

| 12:30 | USD | Housing Starts Apr | 1.42M | 1.40M | 1.42M | 1.43M |

| 12:30 | USD | Building Permits Apr | 1.42M | 1.44M | 1.43M | 1.37M |

| 14:30 | USD | Crude Oil Inventories | -1.5M | 3.0M |