Sample Category Title

US Import Prices Show Fight Against Inflation Not Over

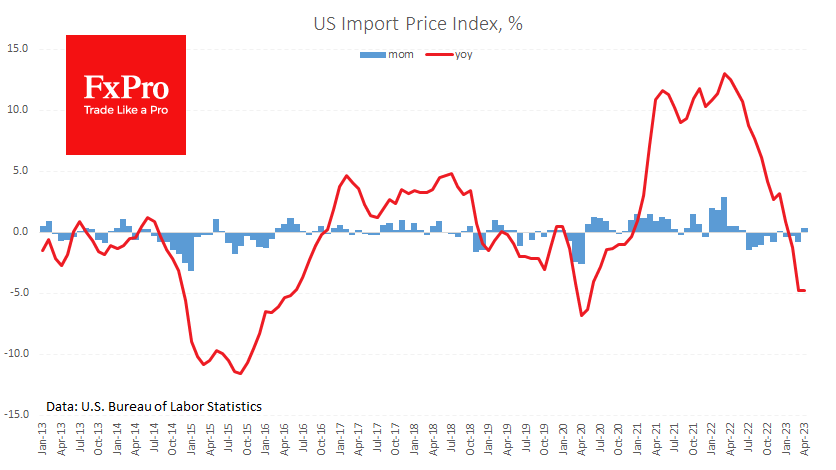

The US import price index came in much better than expected, with a decline of 4.8% y/y in April against expectations of -6.3% y/y. Last month the index rose by 0.4%, the biggest increase since May 2022.

The US is a huge importer, so this index’s development will significantly impact CPI inflation in the coming months. This index’s annual rate of increase began to fall sharply from April last year. It takes another three months for PPI to start declining and CPI to record a peak.

Perhaps imported inflation is the first early signal of how brutal the fight against inflation will be in the coming months. Investors and traders should remember that the Fed’s target is 2%. Inflation has slowed from 9.1% to 4.9%, but monthly price growth must still be on track.

In short, the consumer and import price indices released this week support the idea that the fight against inflation in the US is not over and that a prolonged pause (our main scenario) and another hike may be needed before a long rate plateau.

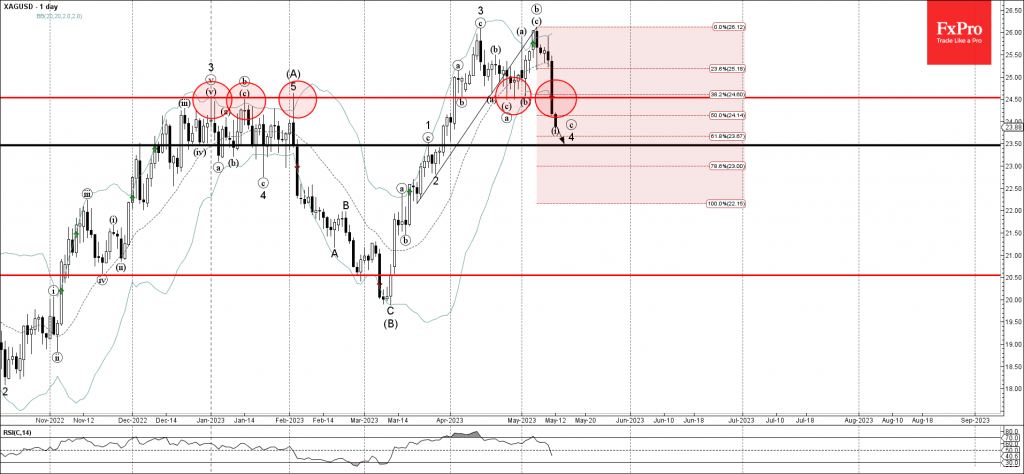

Silver Wave Analysis

- Silver under bearish pressure

- Likely to fall to support level 23.50

Silver under the bearish pressure after the price broke the pivotal support level 24.5 (former strong resistance from January and February) intersecting with the 38.2 Fibonacci correction of the earlier upward impulse from March.

The breakout of the support level 24.5 accelerated the active impulse wave (c) which belongs to the ABC correction 4 from the start of April.

Given the widespread bearish sentiment seen across the precious markets, Silver can be expected to fall toward the next support level 23.50.

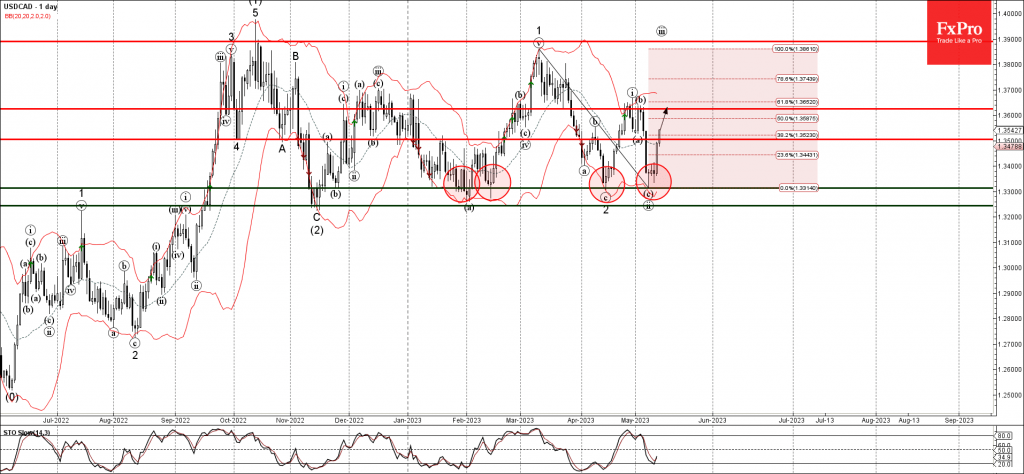

USDCAD Wave Analysis

- USDCAD broke resistance level 1.3500

- Likely to rise to resistance level 1.3625

USDCAD currency pair under the bullish pressure after the earlier breakout of the resistance level 1.3500 intersecting with the 38.2 Fibonacci correction of the previous downward impulse from March.

The breakout of the resistance level 1.3500 accelerated the active short-term upward impulse wave (iii).

Given the strongly bullish USD sentiment, USDCAD can be expected to rise toward the next resistance level 1.3625.

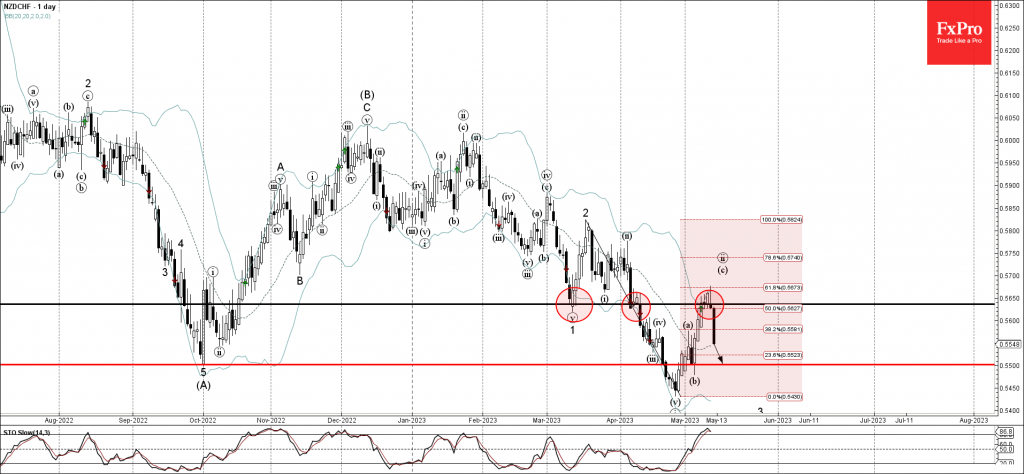

NZDCHF Wave Analysis

- NZDCHF reversed from resistance level 0.5635

- Likely to fall to support level 0.5500

NZDCHF currency pair recently reversed down from the key resistance level 0.5635 (former strong support from the start of March), intersecting with the upper daily Bollinger Band.

The downward reversal from the resistance level 0.5635 created the daily candlesticks reversal pattern Shooting Star.

Given the strong daily downtrend, NZDCHF can be expected to fall toward the next support level 0.5500.

Weekly Focus – Inflation Battle Not Done as BoE Follows Suit

In the absence of any bad news from the US banking sector, markets started the week off in a calm manner with yields edging higher. The US CPI print was markets' key focus point this week, and it printed very close to consensus, with core CPI unchanged at 0.4% mom, still way too high. On balance, it was to the soft side, though, as service inflation eased somewhat indicating beginning signs of easing price pressures in the part of the economy, which is running particularly hot. It triggered a move lower in US yields, most notably in the front-end and the market pricing of 3x25bp of rate cuts in the second half of the year further consolidated. Safe haven currencies have been the winners this week, amid uncertainty regarding the US regional banking sector and the US debt ceiling. EUR/USD has traded back below 1.10 and JPY has also seen some tailwinds.

In the US, news on credit conditions showed tightening lending growth and weaker demand for commercial loans but for the right reasons. Overall, the credit tightening was clearly not as worrying as the market had expected and feared. Initial jobless claims surprised to the upside, rising to the highest level since 2021, providing further evidence of a cooling labour market. That said, the labour market remains very tight and we continue to think this pricing is overdone.

China does not have a problem with high inflation, and April CPI printed even lower than consensus at 0.1%. The print triggered a decline in metal prices with copper trading at four-month lows on worries over the strength of the economic recovery. On the positive side, this paves the way for continued policy stimulus and we could see a rate cut from the People's Bank of China soon, which would boost Chinese demand and perhaps the struggling global manufacturing sector in the wake of that. South Korean export figures for the first 10 days of May were down 10% yoy, with semiconductor shipments particularly plummeting, which indicates manufacturing weakness continuing in May.

In Europe, Bank of England hiked by 25bp and left the door open for another hike in June due to a continued high wage and inflation pressure. We have pencilled in another 25bp hike in June in our expectations, marking the peak bank rate at 4.75%. In Germany, hard data confirmed the headwinds to the manufacturing sector following an otherwise promising start to the year, as industrial production declined 3.4% in March.

With major central bank meetings and April inflation figures just behind us, next week will be quieter on the data front. Retail sales will be interesting, not least in China, as the consumer is set to drive the recovery.

The following week, euro area PMIs will be scrutinised for clues on whether the service sector continues to be the key driver for euro area growth and inflation. In the US, April leading indicators were broadly quite upbeat, and it is going to be interesting to see if the strength will be reflected in the hard data as well, and if it has continued into May.

US Retail Sales Climb to Top of Investors’ Agenda

After Wednesday’s US inflation numbers added credence to the view that the Fed may be forced to cut interest rates later this year, the next focal data set may be the US retail sales for April, due to be released on Tuesday. Industrial production for March, as well as some housing data for the month of April are also in next week’s calendar. Will all these releases help alleviate worries over a potential recession? How will they affect Fed policy expectations and how may the dollar respond?

Fed cut bets remain firmly on the table

Despite not closing the door to a June hike when they last met, Fed officials watered down their forward guidance, noting that whether further hikes are needed will largely depend on incoming data. This allowed market participants to place bets that the Committee will step to the sidelines when it meets next.

On top of that, Wednesday’s inflation data revealed that the headline CPI rate ticked down to 4.9% year-over-year from 5.0%, with the core measure holding steady at 5.5% y/y, which combined with the jump in initial jobless claims to a one-and-a-half-year high added to investors’ stubborn view that the Fed may be forced to push the cut button after the summer, despite policymakers repeatedly saying that no cuts are warranted for this year.

Retail sales expected to rebound

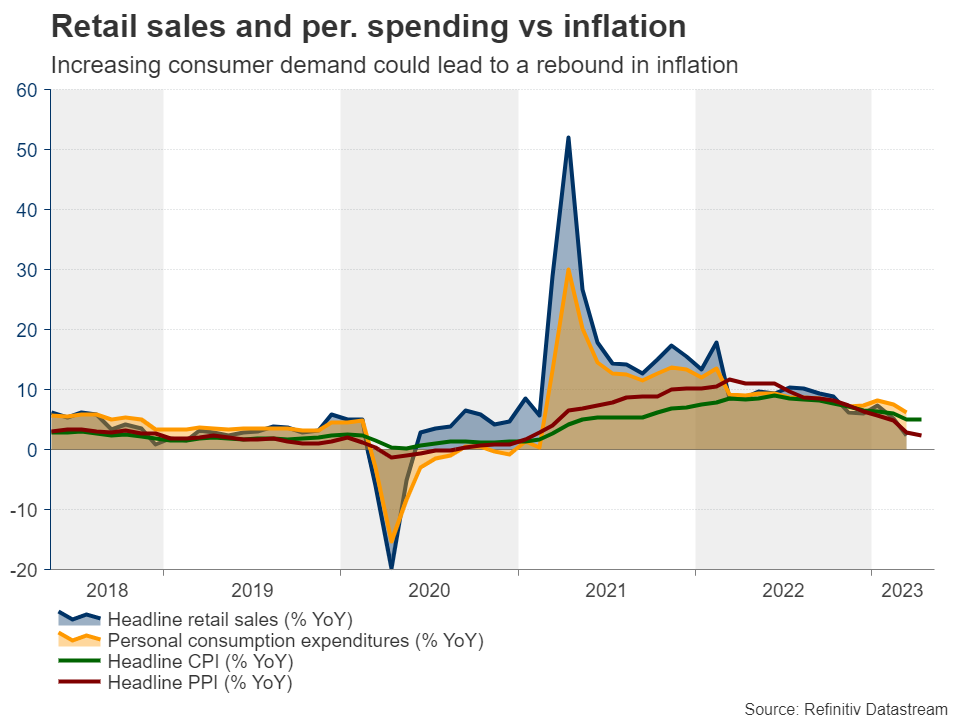

Now, the next highlight may be the US retail sales for April. Expectations are for both the headline and core month-over-month rates to have rebounded to 0.7% and 0.5% respectively from -0.6% and -0.4%.

Following the overall healthy jobs report for the month and the Fed’s loan survey that eased fears of a credit crunch, a rebound in retail sales could somewhat reduce recession concerns and allow market participants to scale back some basis points worth of rate reductions. What’s more, improving consumer demand could lead to a rebound in consumer prices in the months to come and lower interest rates may not be the recipe should this happen.

Housing market shows signs of stabilization

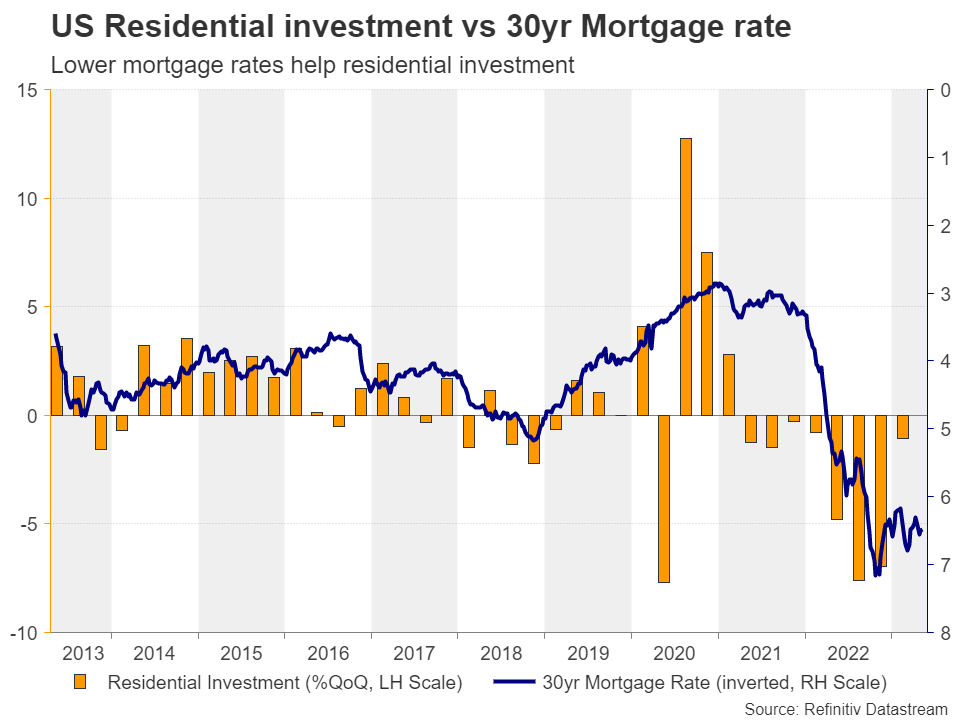

Housing data may be closely watched too by those trying to assess the health of the US economy. On Wednesday, building permits are expected to have fractionally increased and housing starts to have slightly declined, while on Thursday, existing home sales are seen declining 2% month-on-month.

The Fed’s aggressive tightening has pushed the housing market into recession, with residential investment contracting for eight quarters in a row but lately, there have been some signs of stabilization, perhaps as mortgage rates have come off their highs. Thus, further improvement could revive optimism but also add to expectations that inflation may prove stickier than previously thought.

Yield curve remains inverted

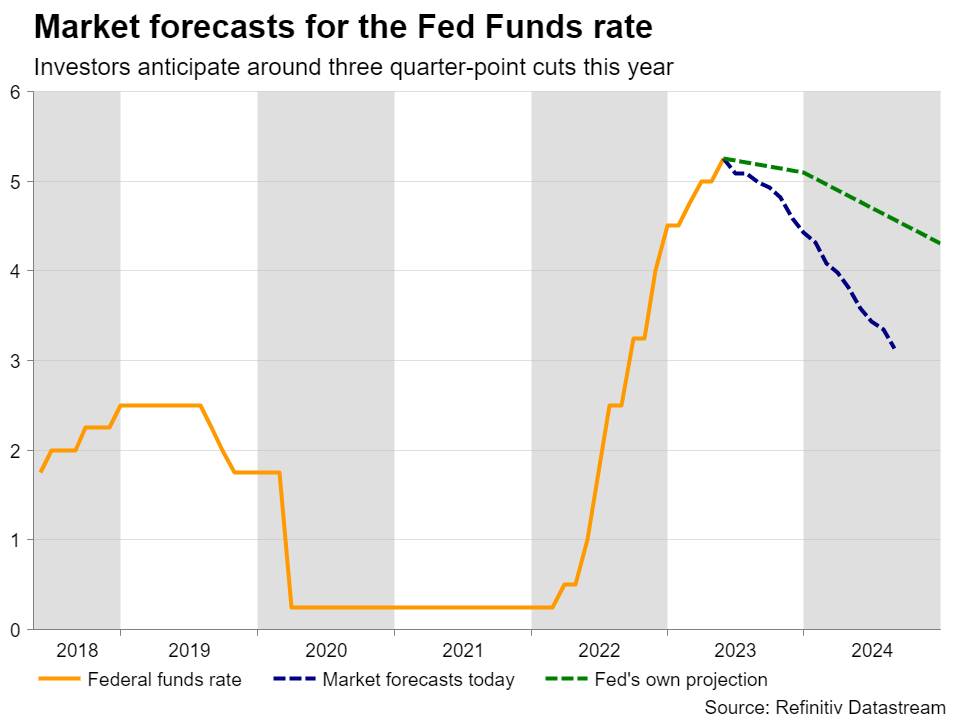

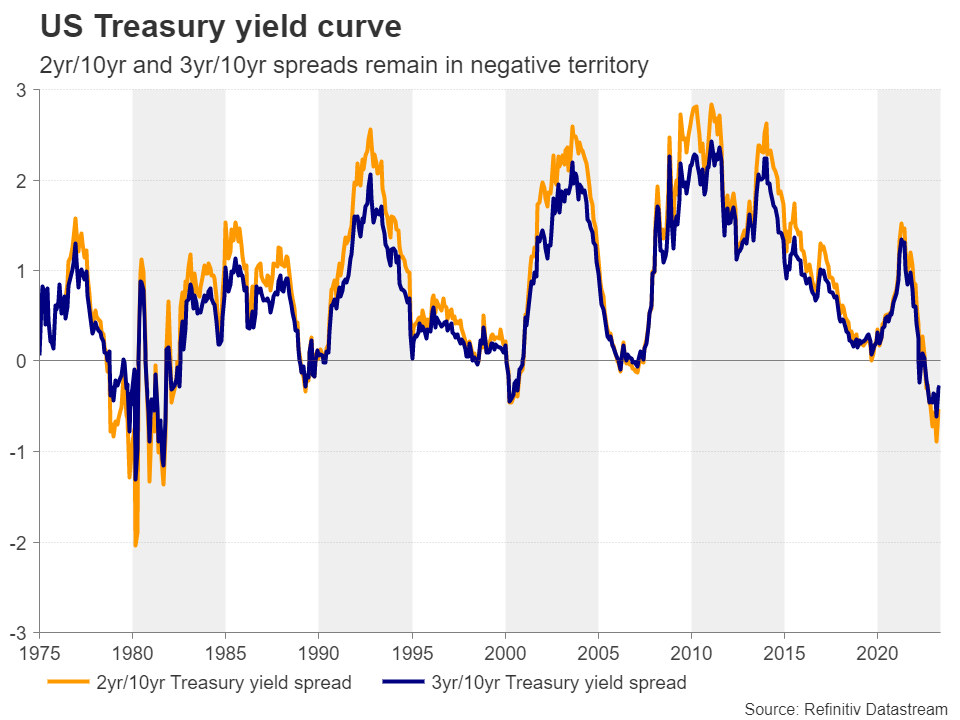

Although rebounding from their lowest levels since 1981, the 2yr/10yr and 3yr/10yr Treasury yield spreads remain in negative territory, pointing to a still-inverted yield curve. This and the bets of around 75bps worth of rate cuts by December suggest that investors are still concerned about the performance of the economy and just a week’s releases may not be enough to dispel their worries. The stalemate in the US Congress over the debt ceiling may be one of the reasons that they are holding back, as a government shutdown may well have adverse effects on the economy.

Dollar could gain, but reversal remains premature

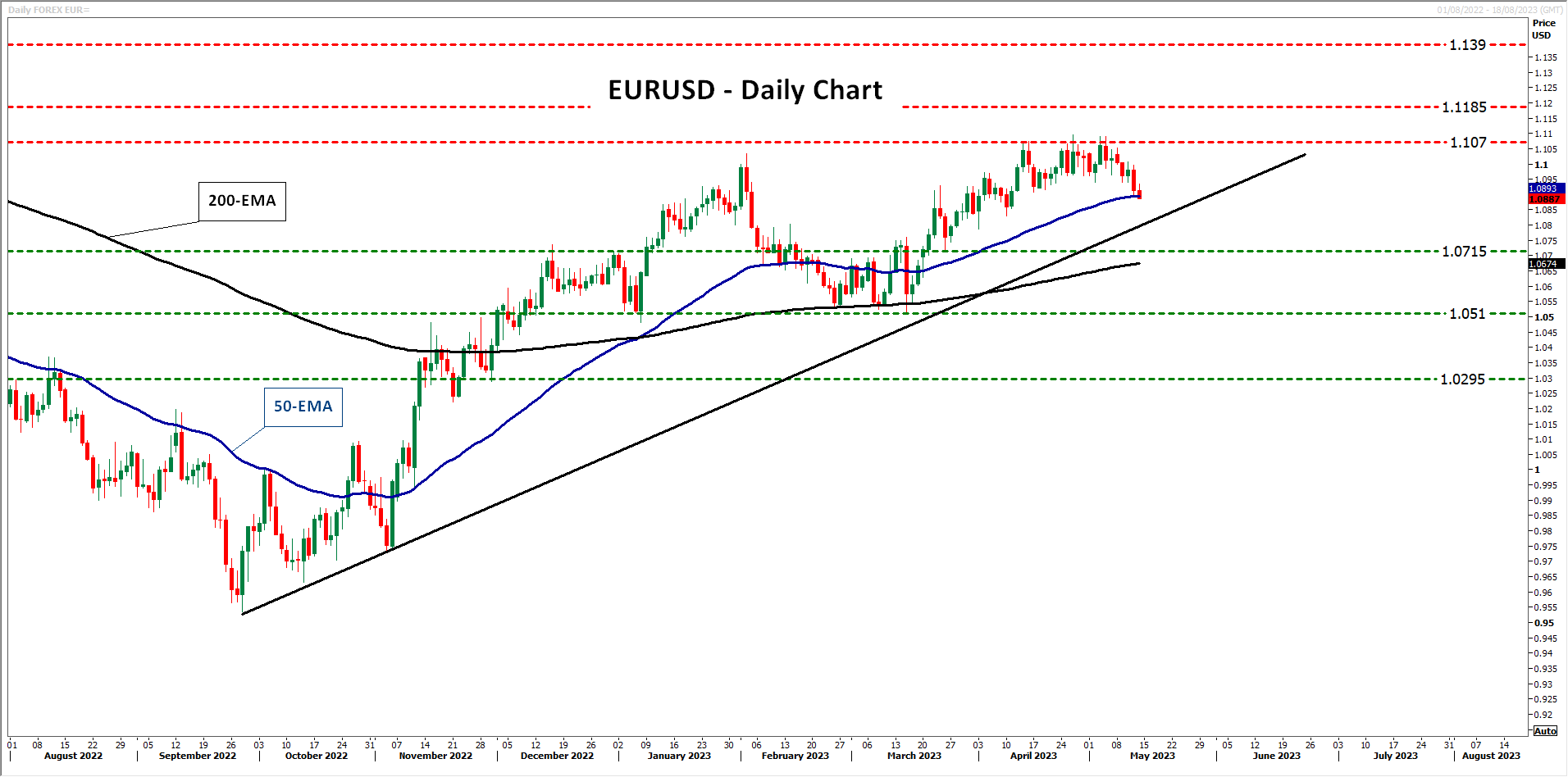

Therefore, even if the dollar strengthens next week, it will still be premature to call for a bullish reversal. Should the market reduce its expected Fed rate cuts to 50bps from 75bps, there will still be divergence between the ECB and the Fed, as the former is expected to deliver nearly another 50bps worth of rate hikes. Thus, the euro/dollar uptrend may stay intact for a while longer.

The latest retreat continues for a while longer, but the bulls may be tempted to re-enter the battlefield from near the uptrend line drawn from the low of September 28. A potential rebound from there may challenge the too-hard-to-break barrier of 1.1070. A breach of that ceiling may be needed to signal a trend continuation, with the next stop perhaps being the peak of March 31, 2022, at 1.1185.

For the outlook to turn bearish, a break below 1.0715 may be required. The price would be below the aforementioned uptrend line and may travel towards the 1.0510 area, which offered strong support in late February and early March this year.

Chinese Data on Radar Amid Worries of a Faltering Economic Recovery

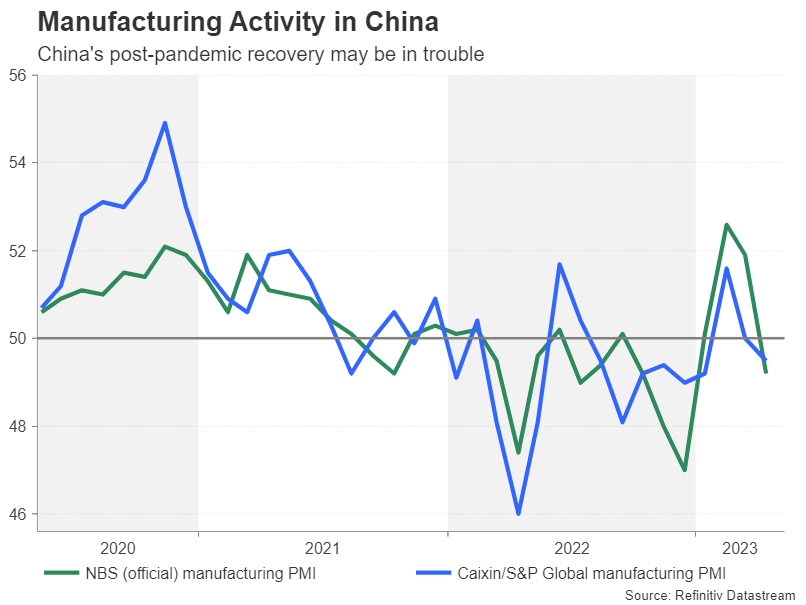

The next batch of economic indicators out of China are due on Tuesday (02:00 GMT) and after some dismal numbers recently, all eyes will be on the industrial output and retail sales releases for April. Fears have been running high lately that the post-pandemic recovery in China is stuttering as the country transitions from a high-growth to sustainable-growth economy. The concerns have added to broader recession risks globally, weighing on market sentiment. Thus, any positive surprises could buoy risk appetite.

Where did the recovery go?

China’s economy made a solid comeback in the first three months of the year following the removal of all Covid curbs back in December. However, the upbeat GDP print was greeted with some scepticism as investors were unconvinced whether there were enough drivers other than the reopening effect to maintain momentum beyond the first quarter. Those persisting concerns appear to be materializing as the data available to date for April is far from encouraging.

It all started with the manufacturing PMIs, as both the government’s and the Caixin/S&P Global surveys indicated that the sector contracted in April. Trade data for the month seemed to support the deteriorating trend. Export growth moderated in April, while imports plunged by 7.9% y/y, declining for a second straight month amid lower demand for commodities such as oil, copper and iron ore.

Most recently, inflation figures showed factory gate prices fell deeper into deflationary territory in April, suggesting that demand for industrial and manufactured goods is weakening rather than improving. Consumer prices were also subdued, with the annual increase in CPI slowing to just 0.1%.

An April bounce might be misleading

But there may be better news on the way from the next set of figures, based on the forecasts that is. Year-on-year growth in fixed asset investment likely quickened slightly to 5.2% between January and April. In the first quarter, much of the investment was driven by government spending so investors will want to see evidence of private investment picking up.

Industrial output made a modest rebound in Q1 and was up 3.9% y/y in March. It is expected to have surged by 10.1% in April. The recovery in consumer spending has been much stronger and retail sales are forecast to have jumped by 20.1%, accelerating from a 10.6% increase in March.

Unfortunately, as spectacular as both these forecasts are, there’s good reason to be cautious as the numbers are being skewed from a dip in April last year due to the lockdowns. It might therefore be difficult to draw too many conclusions about the state of the recovery in April. Yet, with markets going through a jittery phase amid the heightened fears of a global recession, any surprises could spark some volatility in equity markets, particularly in Asia, as well as for the risk-sensitive Australian dollar.

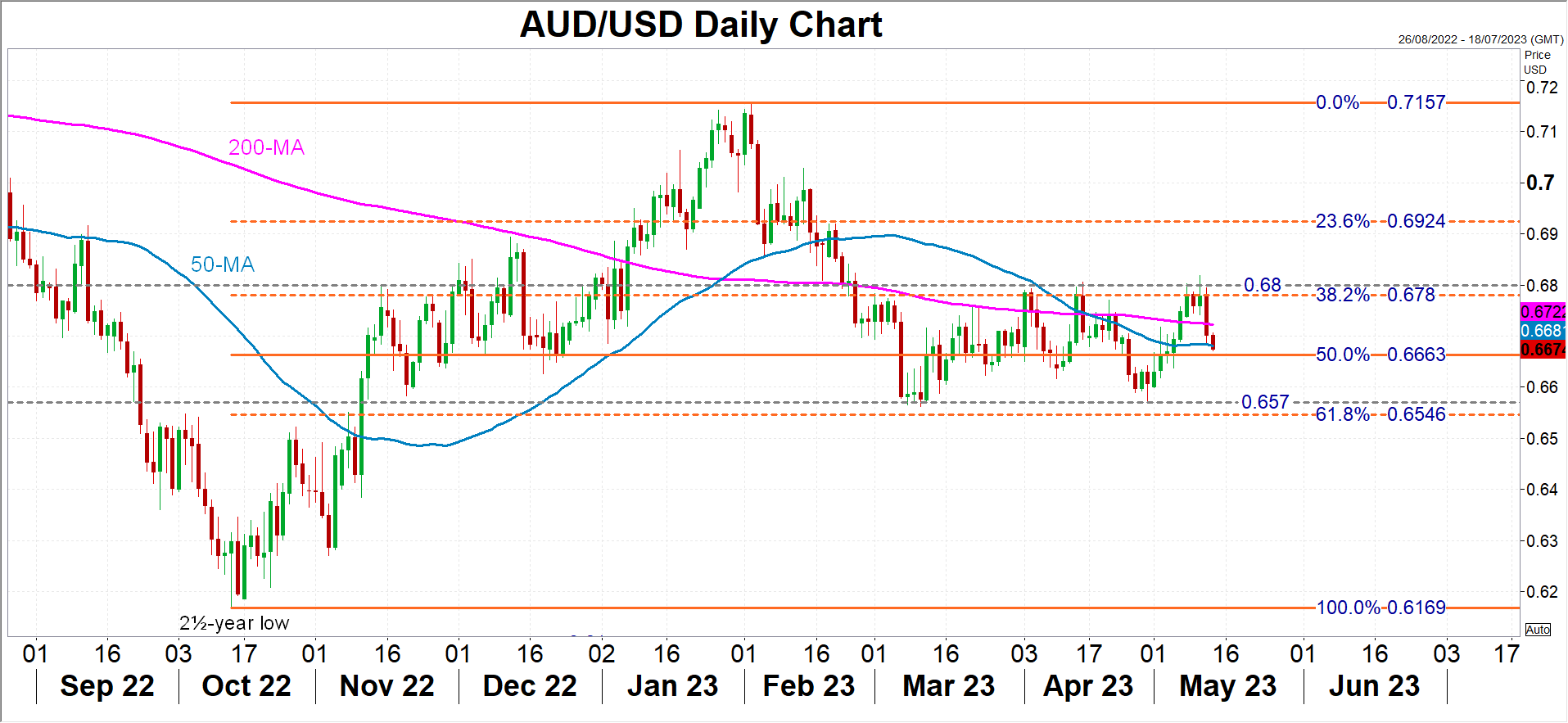

Rangebound aussie is looking for a breakout

The aussie has been finding it tough to crack the $0.68 handle and it’s by no means certain that stronger-than-expected data out of China on Tuesday would be enough to achieve an upside break.

On the other hand, with any disappointing numbers not only hurting the aussie for domestic reasons – as China is Australia’s biggest export market – but also boosting the US dollar for its safe-haven attributes, the pair could re-test the current range floor at around $0.6570 in the negative scenario.

Government is under pressure to do more

Looking at credit growth, financial instructions gave out fewer loans in April despite being under pressure from authorities to lend more, in another sign of a weak start to Q2. This could just be a natural drop after the massive expansion in credit in the first few months of 2023, but that won’t allay much worries about a slowdown. Although the People’s Bank of China (PBOC) has been injecting plenty of liquidity into the financial system, it has been reluctant to use other tools such as cutting interest rates.

The government as well has been treading carefully when it comes to stimulating the economy so as not to risk inflating the country’s already high debt-to-GDP ratio. Unless Beijing steps up with its promised structural reforms, it may be hard for investors to get too optimistic about the outlook.

Week Ahead – Focus on US Retail Sales as Debt Ceiling Drama Rumbles On

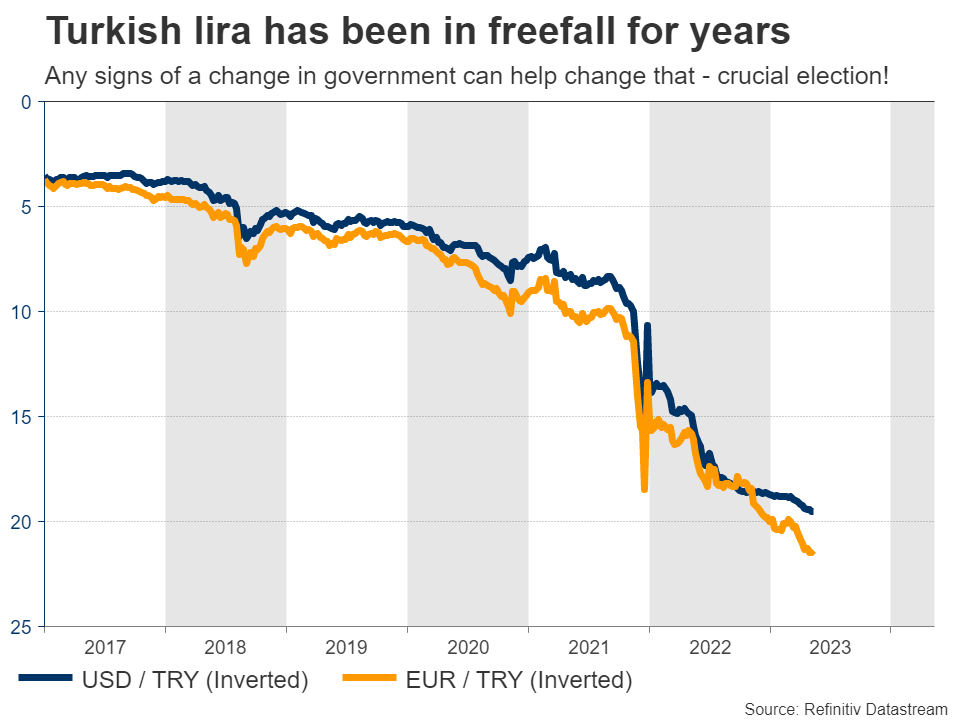

With no central bank decisions on the menu next week, investors will turn to data releases. Top of the list is the US retail sales report, which will help shape expectations about the Fed’s rate path, driving the dollar accordingly. There is also an onslaught of economic data from most major economies to keep traders busy, alongside an election in Turkey and the ongoing drama around the US debt ceiling.

Can the dollar shake off the blues?

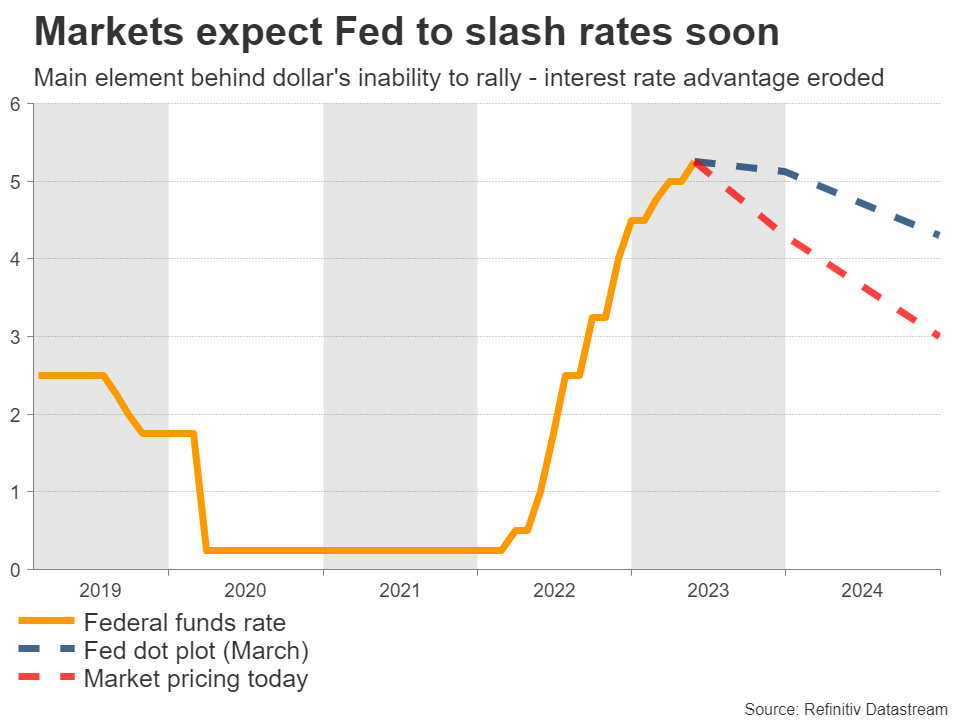

It’s been a rough year for the dollar so far. Despite mounting signs that the US economy has regained momentum, the greenback has been trading ‘heavy’, struggling to sustain any upward momentum. Most rallies get rejected quickly, even if they are backed up by stronger data.

Behind this sluggishness lies speculation that the Fed is about to start cutting interest rates soon. Markets expect the Fed to slash rates three times later this year in 25bps increments, starting in September. This is striking considering that core inflation seems sticky around 5.5%, way above its target.

Traders seem to be betting that the problems in the banking system will override inflation concerns, forcing the Fed to reduce borrowing costs in order to avoid a domino of bank failures, even if that means tolerating a period of higher inflation.

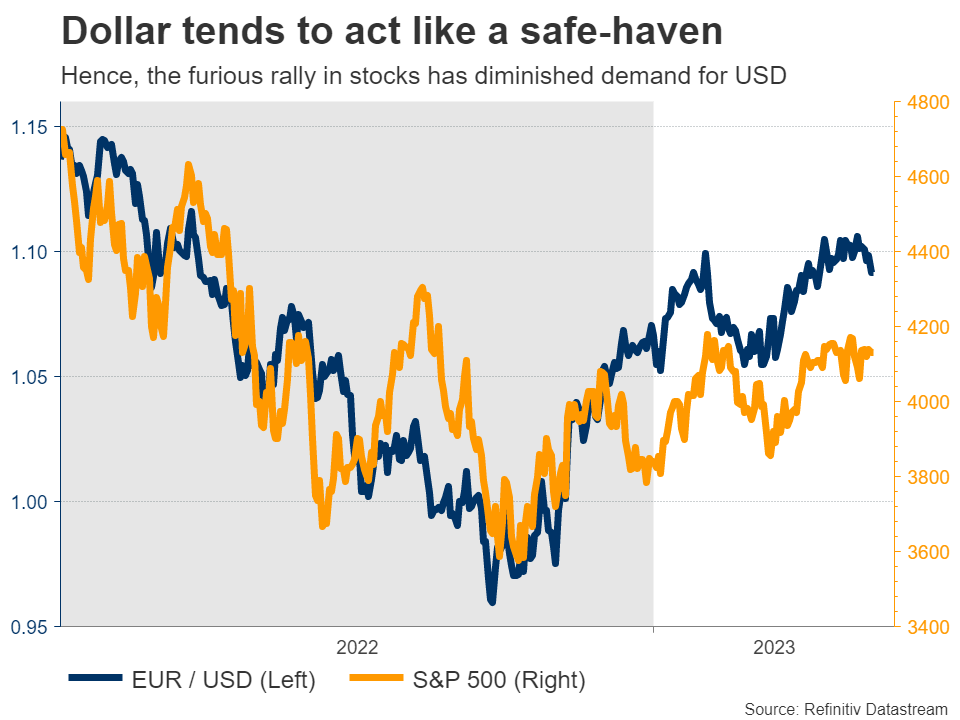

Another problem for the dollar has been the rally in stocks. Since the greenback often acts like a haven asset, the optimistic tone in markets has limited demand for the reserve currency. The charts tell the same story - the dollar index topped in late September, right before the stock market bottomed.

In other words, the dollar’s yield advantage has been eroded because of rate-cut bets, and its safe-haven qualities are not very popular right now. Therefore, for the greenback to start ‘working’ again, it might need an equity selloff that fuels demand for protection or a stream of encouraging data that dispels speculation of imminent rate cuts.

This puts extra emphasis on US retail sales out on Tuesday, which will reveal how consumers are holding up. Forecasts point to a 0.7% monthly increase in April, a rebound following a decline of similar size last month. This notion is supported by an increase in Visa’s US Spending Momentum Index, yet similar card data from Bank of America point to a spending rise of just 0.3% in April, presenting some downside risks.

Meanwhile, debt ceiling negotiations will continue. The Treasury Secretary has warned the US could face default by early June without a deal, although in reality, it is likely closer to July. Outside of short-term Treasury yields and credit default swaps, markets haven’t cared much about this standoff so far, but that might change as the X-date draws closer.

China and Japan await key data

Crossing into China, the ball will get rolling on Tuesday with retail sales, industrial production, and fixed asset investment - all for April. Investors will be looking at whether the reopening momentum has started to fade, as recent business surveys suggested.

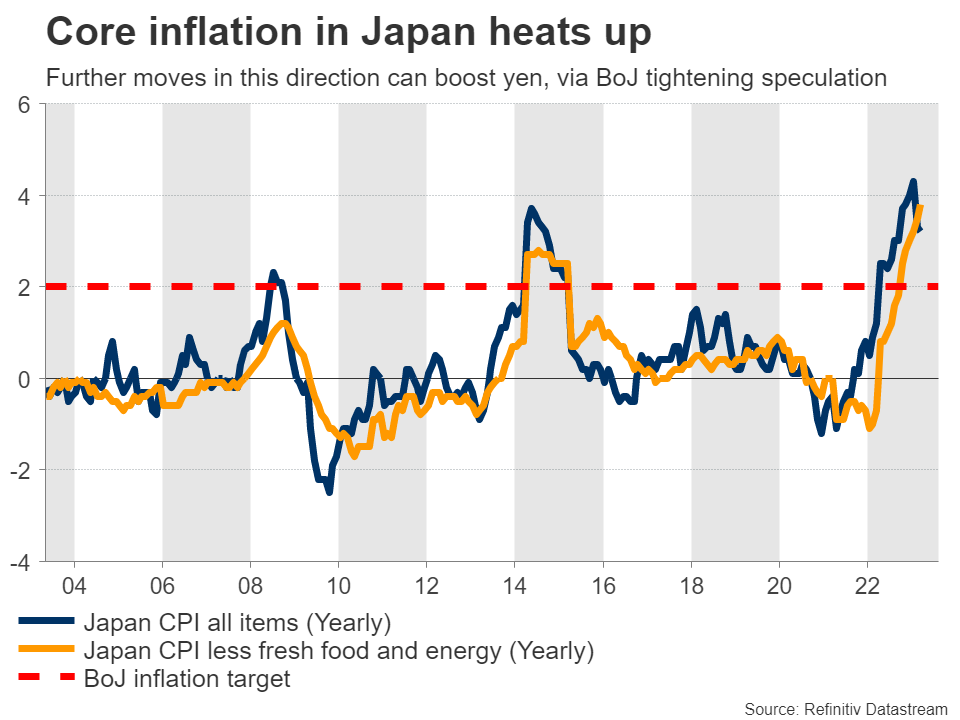

Over in Japan, things will heat up with GDP growth data for Q1 on Wednesday, ahead of the latest round of inflation stats on Friday. The Japanese economy is expected to have grown again entering 2023, albeit just barely.

On the inflation front, inflationary pressures probably continued to heat up in April, mirroring the forward-looking Tokyo CPIs. That would be pleasant news for the Bank of Japan, possibly fueling speculation for policy tightening in the future, perhaps this summer already.

The BoJ’s reluctance to tighten policy has devastated the yen, so any hints that this might change can help the currency regain strength. Governor Ueda has signaled he’s open to tightening, provided that inflation is persistent. For the yen, the dream scenario would be for the BoJ to start tightening right as other central banks stop, during a period of turbulence in global markets.

Risk-linked currencies eyed, Turkey goes to elections

Turning to currencies with strong links to risk sentiment, the British pound will be in the spotlight Tuesday with the release of jobs data for March. The Bank of England disappointed traders this week by not providing any strong clues about future action, so markets are pricing the rate decision next month almost like a coin toss.

In Australia, there’s a barrage of releases starting on Tuesday with the minutes of the latest RBA meeting, where the central bank unexpectedly raised interest rates. The wage price index for Q1 will follow Wednesday, ahead of jobs numbers for April on Thursday.

Over in Canada, the latest inflation stats are out Tuesday, ahead of retail sales on Friday. Market pricing suggests the Bank of Canada is done raising rates, so anything that challenges this perception could inject more volatility into the Canadian dollar, which has been shaken around lately by massive swings in oil prices.

Finally in Turkey, the nation will elect its next parliament and president on Sunday. President Erdogan is lagging behind his main rival Kilicdaroglu, although neither candidate is expected to secure 50% of the votes, which means there will probably be a second round in two weeks.

A strong showing by Kilicdaroglu could help the Turkish lira to appreciate, perhaps with a large gap at the open on Monday, on expectations that a new government will restore orthodox economic policies and allow the central bank to raise interest rates in order to fight runaway inflation.

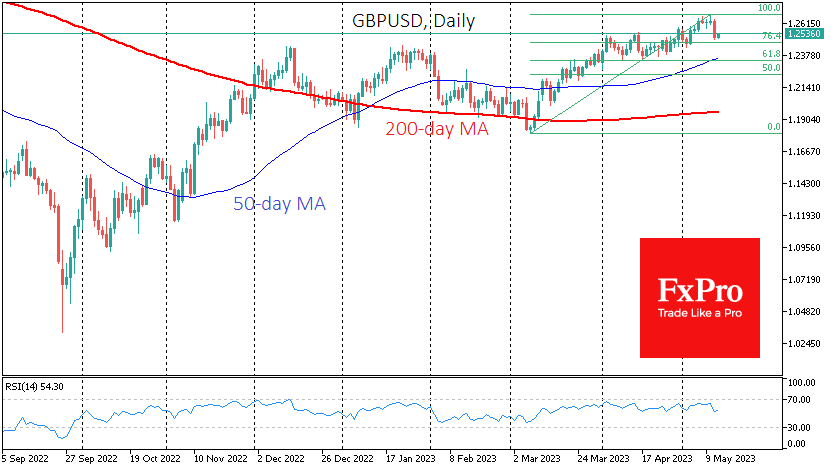

Pound Corrects March-May Rally But Has Not Completed It

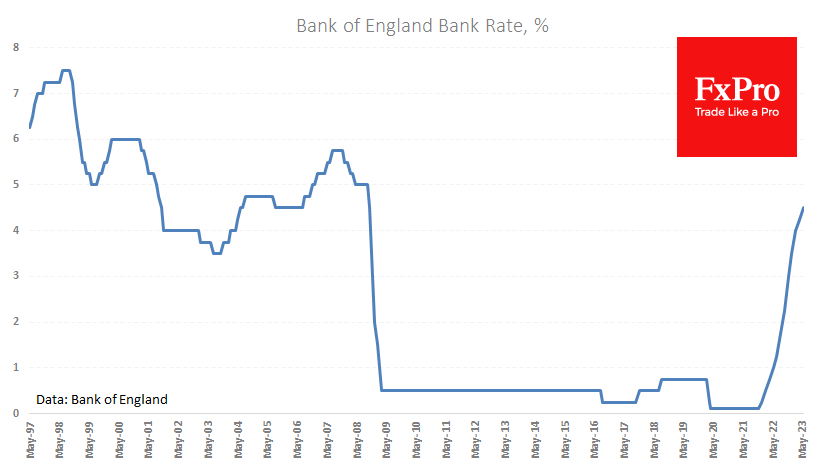

The Bank of England raised its key interest rate by 25 points to 4.5% on Thursday, marking the twelfth consecutive policy tightening. Two of the nine members have voted to keep rates on hold in the last four meetings.

The accompanying commentary left the door open for a further hike and a pause. Arguing in favour of further tightening is the more resilient inflation in the UK, forcing the central bank to raise its rate forecasts regularly. On the other hand, the central bank has done a considerable amount of work so far, and it will take some time for the hikes already made to have their full effect on the economy.

You could say that the Bank of England is trying to go in the same direction as the Fed by stopping rate hikes. A similar signal from the Bank of England could be stronger than the Fed. But the nominal interest rate level in the UK is now lower than in the US when historically the opposite is true.

The reaction of sterling has been interesting. The initial rise of a third of a per cent was wiped out by a triple-digit fall before the end of the day, taking GBPUSD back to 1.25. The market players continued to pocket profits after the Pound’s rally since early March, recalling the adage ‘sell in May and go away’. A retracement of the GBPUSD could occur around 1.2350, a 61.8% retracement of the March-May rally, local support from April and the 50-day moving average.

It is also worth noting that the Bank of England is now benefiting from the appreciation of its currency against its main rivals, as rising import prices significantly contribute to inflationary pressures. As such, we expect the Bank of England to adopt more hawkish rhetoric than the Fed in the coming months, which will support the GBPUSD to rise to the 1.30 area after the correction of the recent rally with a pullback to 1.2350.

Sunset Market Commentary

Markets

UK markets apparently needed some time to let yesterday’s Bank of England meeting outcome sink in. Another 25 bps rate hike was accompanied by similar hawkish guidance that more could follow should inflation be more persistent. Bank of England Chief Economist Pill today already stressed that upside inflation risks remain. Despite an higher implied policy rate path and significantly lower energy prices, the BoE’s preferred model delivered upward revisions to February’s inflation forecasts. Average double digit inflation in Q1, a more resilient economy and the tight labour market are the key reasons. Q1 GDP data printed in line with forecasts this morning at 0.1% Q/Q with details showing flat consumption and investment growth (+1.3%Q/Q) compensating for a decline in government spending (-2.5% Q/Q) and net exports (-0.9% Q/Q). UK Gilts underperformed, reversing yesterday’s move. UK yields add 4.6 bps (2-yr) to 6.9 bps (30-yr) at the time of writing. EUR/GBP this week fell below 0.8719 support to set a new YTD low at 0.8661. An attempt to regain the lost support at 0.8719 failed for now with the pair currently changing hands around 0.87. A weekly close below improves the short term picture for sterling. Next week’s eco data releases (labour market data) could make or break the current GBP-comeback. Sterling holds pace with the dollar resulting in a 1.25 status quo for GBP/USD, holding just above the upward trendline in place since mid-March. One implication is an extension of the topping out pattern in EUR/USD with the pair trading below 1.09 for the first time in a month. The eco calendar didn’t contain EMU figures, but we retain comments by German Bundesbank chief Nagel on the sidelines of the G-7 meeting for finance ministers and central bankers in Japan. He said that ECB tightening might even be required after Summer. That’s at odds with current money market pricing of maximum two additional 25 bps rate hikes in June and July. Voting Fed member Bowman offered some hawkish counterweight by leaving the door open for more rate hikes despite last week’s pause signal. In her view, recent inflation and employment reports have not provided consistent evidence that inflation is on a downward trend. German Bunds today marginally underperform US Treasuries, but it doesn’t help the single currency. German yields add up to 3 bps at the moment with US yields only 1 bp higher. Main stock markets record small gains. Next week’s calendar is light when it comes to eco data (apart from US retail sales) while an avalanche of central bankers on both sides of the Atlantic sheds his/her view on future monetary policy. The US political deadlock on raising the debt ceiling will get more traction with default date (somewhere early June) rapidly approaching. The health of US regional banks remains uncertain as well.

News & Views

Norwegian mainland GDP rose 0.2% q/q in the first three months of the year. Growth was slightly more than the 0.1% consensus estimate, in part thanks to a solid March output rebound (0.5% m/m). But it comes with a downward revision of the 2022Q4 figure (0.6% vs 0.8%). Private consumption weighed (-5.1% q/q) as it normalized from a 5.6% surge in the previous quarter. A rise in (net) exports and government expenditures offered some counterbalance. Today’s numbers are also better than the 0.1% contraction forecasted by Norway’s central bank and follows the stronger-than-expected CPI numbers published earlier this week. The Norges Bank raised rates last week by 25 bps to 3.25%. The final 25 bps rate hike project for June (to 3.5%) looks too conservative, especially against the background of ongoing and historical Norwegian krone weakness (EUR/NOK today trades around 11.63). Money markets expect a policy rate of at least 4%.

G7 finance leaders during their three-day meeting in Japan discussed the need to make supply chains more resilient by reducing over-reliance on China, German finance minister Lindner said today. He added that building partnerships with low- and middle-income countries through investment and aid. In countering the rise of China though, parties are less aligned. The US is pushing for stronger steps, including targeted controls in investment but Japan and German are skeptical to the idea. The members also stressed the need for the US to resolve the debt ceiling impasse and discussed the health of the global financial system and measures to avert another digital bank run. The G7 summit concludes this Saturday and is followed by a G7 country leader reunion next week.