Sample Category Title

Sunset Market Commentary

Markets

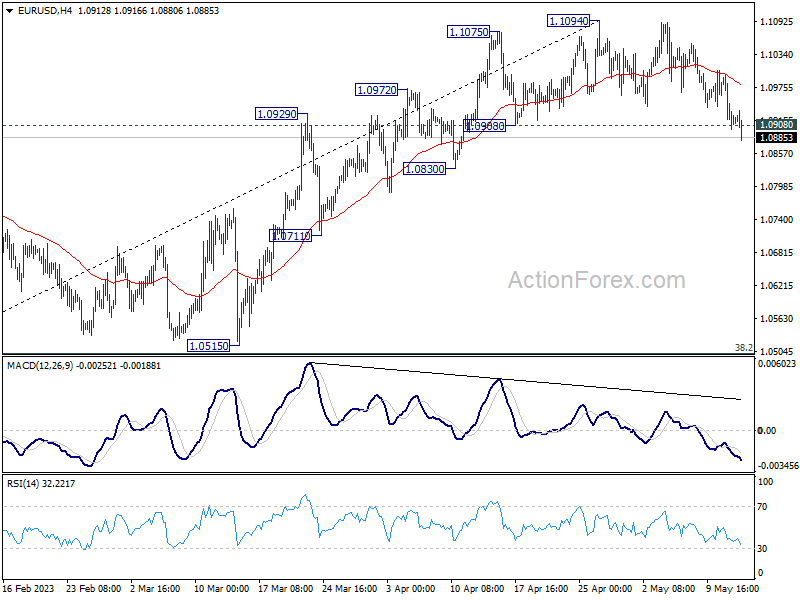

UK markets apparently needed some time to let yesterday’s Bank of England meeting outcome sink in. Another 25 bps rate hike was accompanied by similar hawkish guidance that more could follow should inflation be more persistent. Bank of England Chief Economist Pill today already stressed that upside inflation risks remain. Despite an higher implied policy rate path and significantly lower energy prices, the BoE’s preferred model delivered upward revisions to February’s inflation forecasts. Average double digit inflation in Q1, a more resilient economy and the tight labour market are the key reasons. Q1 GDP data printed in line with forecasts this morning at 0.1% Q/Q with details showing flat consumption and investment growth (+1.3%Q/Q) compensating for a decline in government spending (-2.5% Q/Q) and net exports (-0.9% Q/Q). UK Gilts underperformed, reversing yesterday’s move. UK yields add 4.6 bps (2-yr) to 6.9 bps (30-yr) at the time of writing. EUR/GBP this week fell below 0.8719 support to set a new YTD low at 0.8661. An attempt to regain the lost support at 0.8719 failed for now with the pair currently changing hands around 0.87. A weekly close below improves the short term picture for sterling. Next week’s eco data releases (labour market data) could make or break the current GBP-comeback. Sterling holds pace with the dollar resulting in a 1.25 status quo for GBP/USD, holding just above the upward trendline in place since mid-March. One implication is an extension of the topping out pattern in EUR/USD with the pair trading below 1.09 for the first time in a month. The eco calendar didn’t contain EMU figures, but we retain comments by German Bundesbank chief Nagel on the sidelines of the G-7 meeting for finance ministers and central bankers in Japan. He said that ECB tightening might even be required after Summer. That’s at odds with current money market pricing of maximum two additional 25 bps rate hikes in June and July. Voting Fed member Bowman offered some hawkish counterweight by leaving the door open for more rate hikes despite last week’s pause signal. In her view, recent inflation and employment reports have not provided consistent evidence that inflation is on a downward trend. German Bunds today marginally underperform US Treasuries, but it doesn’t help the single currency. German yields add up to 3 bps at the moment with US yields only 1 bp higher. Main stock markets record small gains. Next week’s calendar is light when it comes to eco data (apart from US retail sales) while an avalanche of central bankers on both sides of the Atlantic sheds his/her view on future monetary policy. The US political deadlock on raising the debt ceiling will get more traction with default date (somewhere early June) rapidly approaching. The health of US regional banks remains uncertain as well.

News & Views

Norwegian mainland GDP rose 0.2% q/q in the first three months of the year. Growth was slightly more than the 0.1% consensus estimate, in part thanks to a solid March output rebound (0.5% m/m). But it comes with a downward revision of the 2022Q4 figure (0.6% vs 0.8%). Private consumption weighed (-5.1% q/q) as it normalized from a 5.6% surge in the previous quarter. A rise in (net) exports and government expenditures offered some counterbalance. Today’s numbers are also better than the 0.1% contraction forecasted by Norway’s central bank and follows the stronger-than-expected CPI numbers published earlier this week. The Norges Bank raised rates last week by 25 bps to 3.25%. The final 25 bps rate hike project for June (to 3.5%) looks too conservative, especially against the background of ongoing and historical Norwegian krone weakness (EUR/NOK today trades around 11.63). Money markets expect a policy rate of at least 4%.

G7 finance leaders during their three-day meeting in Japan discussed the need to make supply chains more resilient by reducing over-reliance on China, German finance minister Lindner said today. He added that building partnerships with low- and middle-income countries through investment and aid. In countering the rise of China though, parties are less aligned. The US is pushing for stronger steps, including targeted controls in investment but Japan and German are skeptical to the idea. The members also stressed the need for the US to resolve the debt ceiling impasse and discussed the health of the global financial system and measures to avert another digital bank run. The G7 summit concludes this Saturday and is followed by a G7 country leader reunion next week.

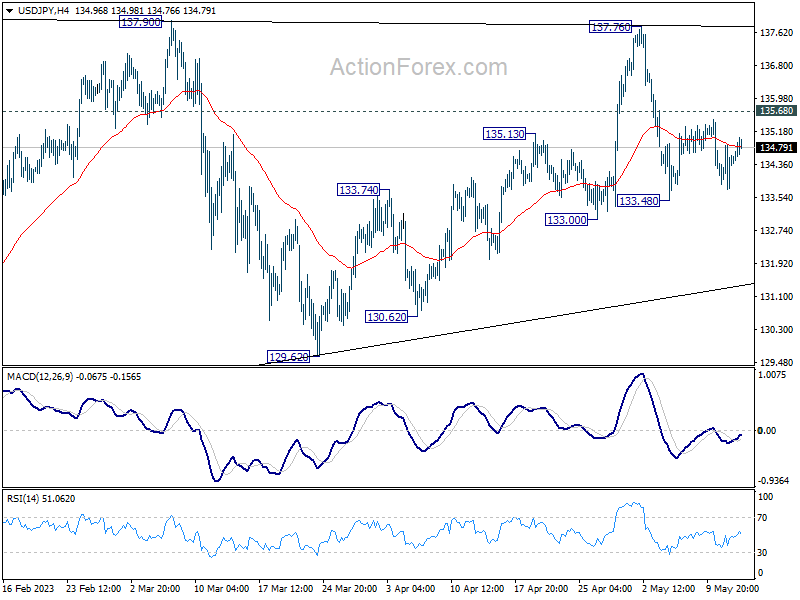

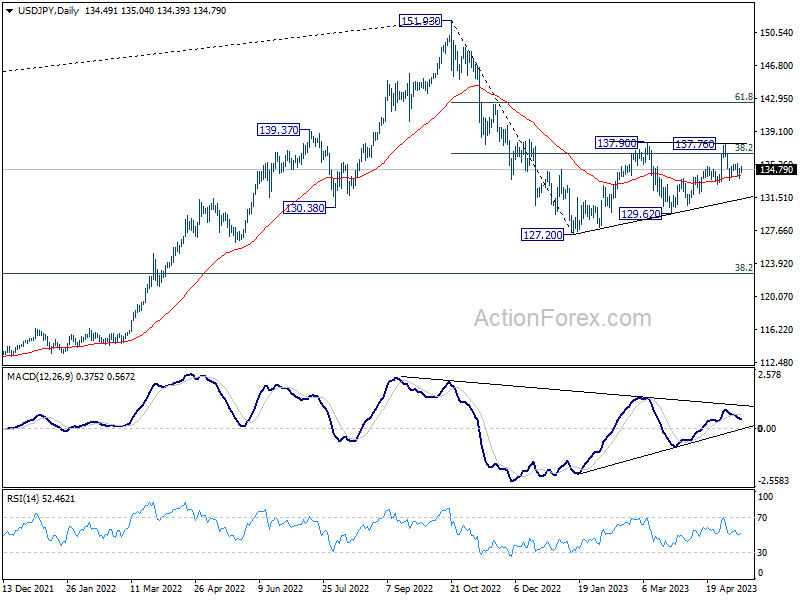

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 133.93; (P) 134.39; (R1) 135.02; More...

Outlook in USD/JPY remains neutral for the moment. Further decline is in favor with 135.68 resistance intact. Fall from 137.76 is seen as the third leg of the pattern from 137.90. Below 133.48 will target 133.00 first, break will target 129.62 support. Still, as long as 129.62 holds, larger rebound from 127.20 is still in favor to resume at a later stage. On the upside, above 135.68 minor resistance will turn bias back to the upside for 137.76/90 instead.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rebound to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8900; (P) 0.8929; (R1) 0.8972; More...

Intraday bias in USD/CHF remains neutral at this point. While down trend from 1.0146 could still extend lower, strong support should be seen from 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support, to bring rebound, at least on first attempt. On the upside, break of 0.8993 resistance will indicate short term bottoming, on bullish convergence condition in 4H MACD, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.9054) and possibly above.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

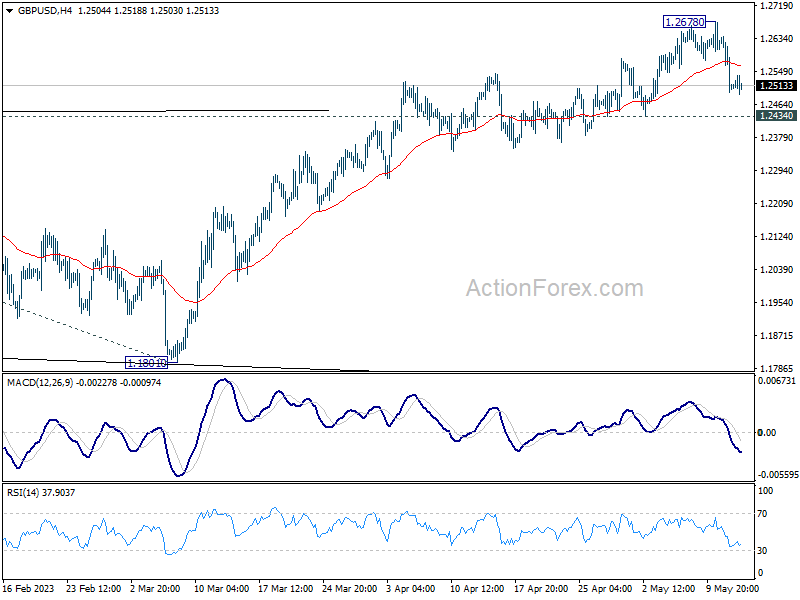

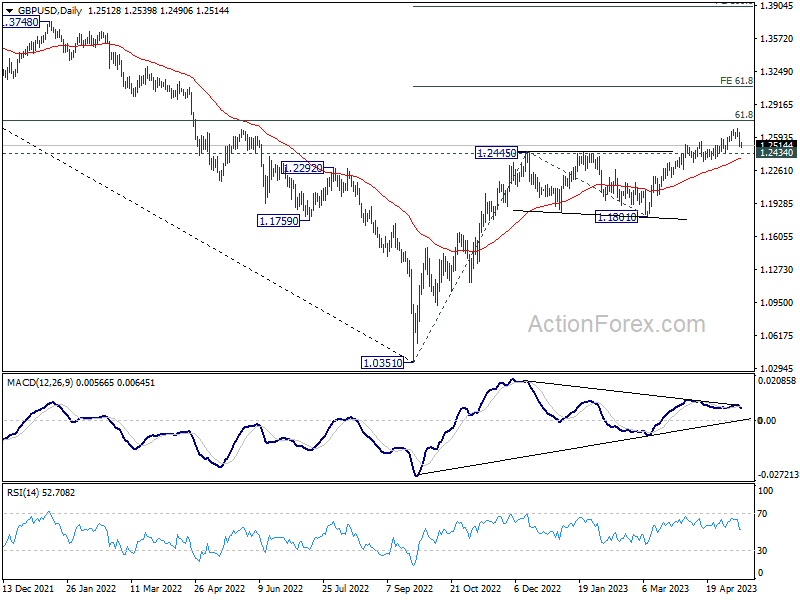

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2459; (P) 1.2550; (R1) 1.2603; More...

GBP/USD is staying above 1.2434 support and intraday bias remains neutral. Further rise is still mildly in favor. On the upside, break of 1.2678 will resume larger up trend to 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, decisive break of 1.2434 will confirm short term topping, and turn bias back to the downside for deeper fall.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0878; (P) 1.0938; (R1) 1.0976; More...

EUR/USD's break of 1.0908 support indicates short term topping at 1.1094. Intraday bias is back on the downside. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.0881) will pave the way back to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498, as a correction to whole up trend from 0.9534.

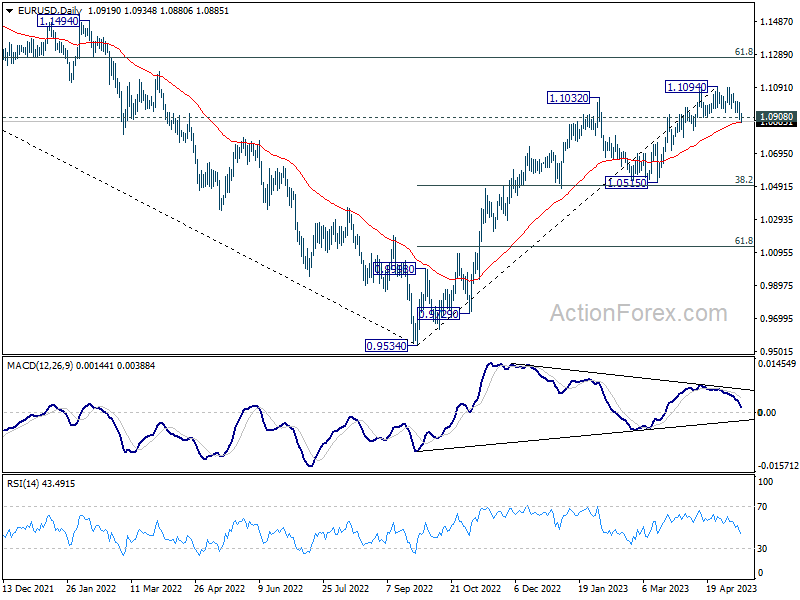

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Dollar Strengthens Amid Rise in Import Prices; Euro Breaks Near Term Support

Dollar is capitalizing on its recent rebound in early US sessions, bolstered by data that showed a 0.4% month-on-month rise in import prices for April – marking the first increase since late 2022. This resurgence places the Greenback on track to be this week's top performer, trailed by Japanese Yen and Swiss Franc. This picture hints at a subtle risk-off sentiment, despite its most apparent manifestation being in commodities market.

Conversely, Sterling remains weak after the surprising contraction in the country's monthly GDP for The Australian and New Zealand Dollars are faring even worse, struggling amidst the broader market dynamics.

Euro is also displaying softness, succumbing to fresh selling pressure against Dollar. From a technical perspective, break of 1.0908 support level in EUR/USD suggests that deeper correction is now underway. Given bearish divergence condition in Daily MACD, sustained trading below the 55 D EMA could trigger steeper selloff towards 1.0515 cluster support, in what could be a correction to the entire rise from 0.9534.

In Europe, at the time of writing, FTSE is up 0.20%. DAX is up 0.45%. CAC is up 0.47%. Germany 10-year yield is up 0.261 at 2.250. Earlier in Asia, Nikkei rose 0.90%. Hong Kong HSI dropped -0.59%. China Shanghai SSE dropped -1.12%. Singapore Strait Times dropped -0.65%. Japan 10-year JGB yield dropped -0.0031 to 0.389.

Fed Bowman suggests potential for further monetary tightening

Fed Governor Michelle Bowman highlighted concerns over persistently high inflation and a tight labor market. In a speech, she suggested the need for additional monetary policy tightening should these conditions persist.

She stated, "The most recent CPI and employment reports have not provided consistent evidence that inflation is on a downward path, and I will continue to closely monitor the incoming data as I consider the appropriate stance of monetary policy going into our June meeting."

She emphasized the necessity of a "sufficiently restrictive" policy stance to curtail inflation over time, especially if inflation remains elevated and the labor market continues to be tight.

She further added, "I also expect that our policy rate will need to remain sufficiently restrictive for some time to bring inflation down and create conditions that will support a sustainably strong labor market."

Despite her clear inclination towards policy tightening, Governor Bowman was careful to stress the uncertainty of economic outlook and the adaptability of Fed's policy actions.

"Of course, the economic outlook is uncertain and our policy actions are not on a preset course," she concluded, indicating Fed's readiness to adjust its approach as necessary in response to evolving economic conditions.

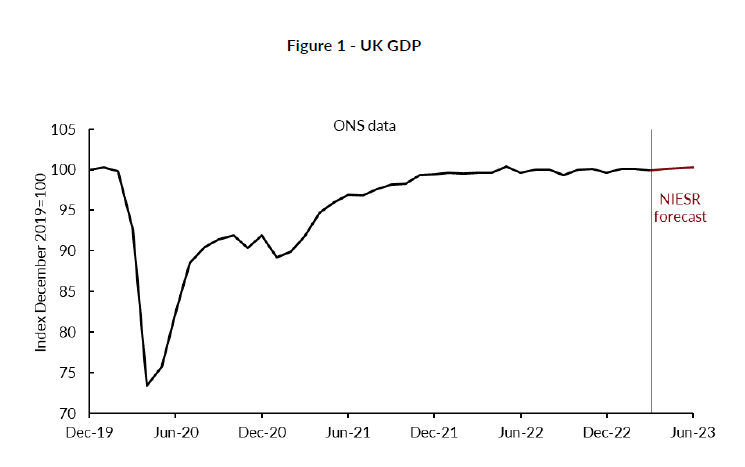

UK GDP contracted -0.3% mom in March; services main contributor to decline

UK GDP saw a contraction of -0.3% mom in March, significantly underperforming against expectations of being flat. The contraction was primarily driven by the services sector, which slipped by -0.5% in the month, following an unrevised dip of 0.1% in February.

However, not all areas of the economy were in decline. Production output experienced its strongest monthly growth since May 2021, with a 0.7% increase in March, rebounding from a 0.1% fall in February. Similarly, construction sector showed modest growth of 0.2% in March, albeit much slower than February's robust 2.6% rise.

On a quarterly basis, GDP growth for Q1 met expectations at 0.1% qoq. In output terms, services sector eked out 0.1% growth over the quarter, fueled by advancements in information and communication, and administrative and support service activities. Construction sector also saw growth at 0.7%, while the production sector managed a marginal 0.1% increase, with a slightly better 0.5% growth in manufacturing.

Year-on-year, the implied GDP deflator for Q1 2023 rose by 6.3%, indicating a slowdown from the 7.3% seen in Q4 2022. This suggests a softening of inflationary pressures within the UK economy over this period.

NIESR forecasts UK GDP to bounce back by 0.3% in Apr

National Institute of Economic and Social Research (NIESR) forecasts a modest rebound in UK's monthly GDP in April with growth of 0.3%, largely driven by services sector. However, this is viewed as a modest increment rather than the robust 'jump-start' the UK economy may need. Paula Bejarano Carbo, Associate Economist at NIESR, highlighted the situation as "(welcome) low growth".

Meanwhile, the think tank significantly downgrades annual GDP outlook for 2023 to a mere 0.3%, a stark contrast to 4.1% achieved in 2022. This economic stagnation is attributed to persistently high inflation and interest rates, which continue to weigh heavily on household and corporate budgets, and is expected to suppress demand in the forthcoming months.

The forecast paints a paradoxical picture of the UK's economic future. While there is cautious optimism as it appears the worst of the energy price shock has passed and the country seems poised to avoid an imminent recession, the subdued outlook suggests that it will feel like a recession for many households. NIESR predicts an average fall in real personal disposable incomes of approximately 2% over the next three years, further pressuring households already grappling with the economic challenges.

New Zealand BNZ PMI rose to 49.1, but struggles continue

New Zealand's manufacturing sector is continuing to grapple with challenges as BusinessNZ Performance of Manufacturing Index edged up to 49.1 in April, from 48.1 in March, remaining below neutral 50.0 mark that separates expansion from contraction.

While the index ticked higher, five of the last seven months have seen contraction, indicating ongoing stress in the sector. In fact, the proportion of negative comments rose to 70.3% in April, compared with 63.2% in March and 60.2% in February. Manufacturers expressed concerns over price pressures, staffing issues, and lower demand, mirroring the broader economic challenges faced by the country.

Digging deeper into the data, we see that production rose from 43.4 to 47.0 and employment edged up from 47.3 to 47.8. New orders also improved, rising from 46.9 to 49.8, but these sub-indexes remained in contraction territory. Finished stocks increased from 48.5 to 52.5, while deliveries dropped from 53.9 to 51.5.

Catherine Beard, BusinessNZ's Director of Advocacy, commented on the tough conditions, noting the stresses and strains of the wider economy appear to be playing out in the manufacturing sector. She further added that despite the overall activity not straying too far into contraction, the sector seems unable to regain expansion mode, with key indicators of production and new orders failing to return positive results in April.

RBNZ survey sees notable decline in inflation expectations

According to RBNZ Q2 Survey of Expectations (Business), inflation expectations for the year ahead took a notable dip, marking the largest drop since June 2020. The one-year-ahead inflation expectation declined by -83 basis points, moving from 5.11% down to 4.28%.

Further into the future, expectations for inflation over a two-year period also demonstrated a decrease. The mean two-year-ahead inflation expectation fell by -51 basis points from 3.30% to 2.79%, placing it back within RBNZ's target band of 1-3% for the first time since December 2021. The survey also found that the spread of responses has narrowed compared to the previous quarter, with a lower quartile of 2.00% and an upper quartile of 3.00%.

The survey's respondents also projected changes in the Official Cash Rate. By the end of June 2023, the OCR is expected to rise to 5.47%, an increase of 58 basis points from the last quarter's mean estimate of 4.89%. However, expectations suggest the OCR will fall back to 4.84% by March 2024, down from the previous quarter's estimate of 5.00%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0878; (P) 1.0938; (R1) 1.0976; More...

EUR/USD's break of 1.0908 support indicates short term topping at 1.1094. Intraday bias is back on the downside. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.0881) will pave the way back to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498, as a correction to whole up trend from 0.9534.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Apr | 49.1 | 48.1 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | 2.50% | 2.70% | 2.60% | 2.50% |

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | 2.79% | 3.30% | ||

| 06:00 | GBP | GDP Q/Q Q1 P | 0.10% | 0.10% | 0.10% | |

| 06:00 | GBP | GDP M/M Mar | -0.30% | 0.00% | 0.00% | |

| 06:00 | GBP | Industrial Production M/M Mar | 0.70% | -0.10% | -0.20% | -0.10% |

| 06:00 | GBP | Industrial Production Y/Y Mar | -2.00% | -3.70% | -3.10% | -2.70% |

| 06:00 | GBP | Manufacturing Production M/M Mar | 0.70% | -0.10% | 0.00% | 0.10% |

| 06:00 | GBP | Manufacturing Production Y/Y Mar | -1.30% | -3.80% | -2.40% | -1.90% |

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | -16.4B | -17.5B | -17.5B | -16.6B |

| 12:30 | USD | Import Price Index M/M Apr | 0.40% | 0.30% | -0.60% | -0.80% |

| 14:00 | USD | Michigan Consumer Sentiment Index May P | 63 | 63.5 |

NIESR forecasts UK GDP to bounce back by 0.3% in Apr

National Institute of Economic and Social Research (NIESR) forecasts a modest rebound in UK's monthly GDP in April with growth of 0.3%, largely driven by services sector. However, this is viewed as a modest increment rather than the robust 'jump-start' the UK economy may need. Paula Bejarano Carbo, Associate Economist at NIESR, highlighted the situation as "(welcome) low growth".

Meanwhile, the think tank significantly downgrades annual GDP outlook for 2023 to a mere 0.3%, a stark contrast to 4.1% achieved in 2022. This economic stagnation is attributed to persistently high inflation and interest rates, which continue to weigh heavily on household and corporate budgets, and is expected to suppress demand in the forthcoming months.

The forecast paints a paradoxical picture of the UK's economic future. While there is cautious optimism as it appears the worst of the energy price shock has passed and the country seems poised to avoid an imminent recession, the subdued outlook suggests that it will feel like a recession for many households. NIESR predicts an average fall in real personal disposable incomes of approximately 2% over the next three years, further pressuring households already grappling with the economic challenges.

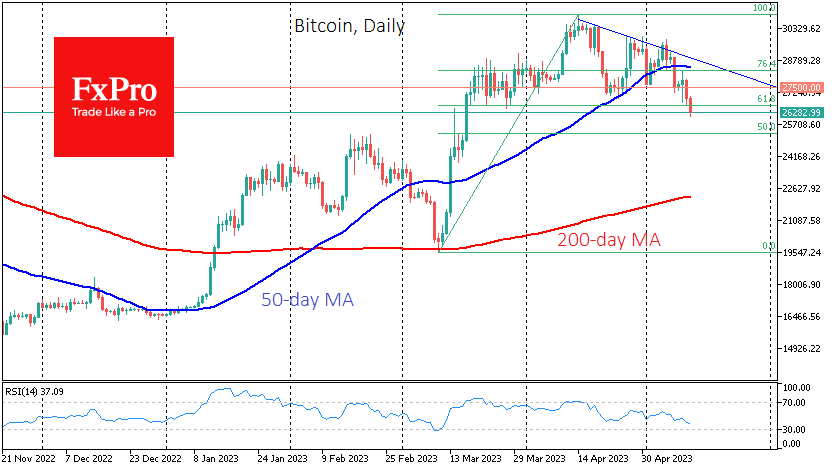

Bitcoin’s Fall Unlikely to Stop Above $25K

Market picture

The crypto market lost 3.2% over the past day, dragged down by the institutions’ favourite instruments: Bitcoin (-4.5%) and Ether (-4.3%). Other top altcoins range from -4% (Polygon) to 0% (XRP). The Cryptocurrency Fear and Greed Index fell to 49 (neutral), its lowest level in two months.

Bitcoin is trading at $26.3K, its lowest level since March 17, losing over 15% from its peak last month. The local technical pattern offers little reason for optimism. Bitcoin fell well below its 50-day moving average at the beginning of the week. By the end of Thursday, it was below $27.5K, the support line for the last two months. Friday’s early morning drop took BTCUSD below the 61.8% Fibonacci correction level from the rally off the March lows. In other words, we see more than just a correction of this latest growth impulse.

Bitcoin’s return to $25K looks like a real prospect in the coming days. The bears will have their work cut out for them here, as some oversold conditions will have built up by then. The $25K level is also significant that Bitcoin did not breach between the middle of last year and the middle of March. Now it has every chance of becoming an equally reliable support.

News background

Crypto assets could become a hedge against inflation, according to rating agency S&P Global. However, the history of the crypto market needs to be longer to prove this hypothesis.

The New York State legislature has begun considering a bill allowing dollar-pegged stablecoins to be used as a legal means of paying bail for defendants.

Former SEC official John Reed Stark has called on US financial regulators to ban crypto-related companies from offering Tether (USDT) stablecoins. According to him, the issuer of the USDT stablecoin could be the next domino to fall.

According to documents filed with the SEC, Franklin Templeton, which manages assets worth more than $1.4 trillion, plans to launch a second blockchain fund. The minimum investment in the fund will be $100K.

Circle, the issuer of the USDC stablecoin, has renounced US Treasury securities maturing after May 31 in case of a US default on government debt.

Elon Musk released a meme featuring NFTs from the Milady collection, which resulted in a 2600% increase in sales of anime tokens and hundreds of times price increase of the Milady Meme Coin.

Aussie Takes a Tumble, UoM Consumer Sentiment Next

- Australia’s inflation expectations higher than expected

- US inflation unlikely to sway Fed

- UoM consumer sentiment expected to ease

AUD/USD is down 0.19% today, trading at 0.6688.

Australia’s consumer inflation expectations rise

Australia’s consumer inflation expectations climbed to 5.0% in May, matching the estimate and above the April reading of 4.6%. This is not what the Reserve Bank of Australia wants to hear – if inflation expectations keep rising and become entrenched, it can manifest into higher inflation. The RBA surprised the markets with a 25-basis point hike earlier this month, as investors had expected a second straight pause. Another rate hike at the June meeting will not win the Bank any friends, with businesses and households straining under the weight of rising interest rates.

The US dollar flexed its muscles on Thursday as markets digested the US inflation report, posting strong gains against most of the majors. The Australian dollar took it on the chin, dropping 1.1%, its worst one-day performance since March.

US inflation remains sticky, as the deceleration process appears stalled. Headline CPI dropped from 5.0% to 4.9%, while the core rate ticked lower to 5.5%, down from 5.6%. The Fed pays more attention to the core rate and there’s no arguing that it remains much too high. This means that the Fed is unlikely to be considering any rate cuts, despite the markets mostly pricing in a cut in September.

Powell & Co. may be content to hold rates until inflation shows signs of falling more quickly, but in the meantime, the Fed remains somewhat hawkish. The inflation report wasn’t enough to sway the Fed’s stance, and the US dollar responded with sharp gains on Thursday.

The week wraps up with UoM Consumer Sentiment. Consumers haven’t been in the best of moods, which is to be expected, given rising interest rates and high inflation. The indicator fell to 63.5 in April and is expected to ease to 63.0 in May. If the release is weaker than expected, it will be another sign of cracks in the economy, and the US dollar could respond with losses. Conversely, a surprise to the upside would be bullish for the greenback.

AUD/USD Technical

- AUD/USD is putting pressure on support at 0.6665. Below, there is support at 0.6557

- 0.6756 and 0.6855 are the next resistance lines

GBP/USD Flat as UK GDP a Mixed Bag

- UK GDP remains steady at 1% in Q4

- BoE raises rates by 25 bp

- BoE revises upwards its growth, inflation forecasts

- UoM consumer sentiment expected to slow

GBP/USD is trading at 1.2517 in Europe, almost unchanged.

In the UK, GDP declined by 0.3% in March m/m, below the 0.1% estimate and the February reading of 0.0%. Still, the economy managed to gain 0.1% in the first quarter, unchanged from Q4 2022 and matching the estimate.

BoE raises rates by 25 bp, revises inflation, GDP forecasts

There was no surprise as the Bank of England raised rates by 25 basis points, bringing the cash rate to 4.50%, its highest since 2008. This marked the twelfth consecutive hike in the current rate-tightening cycle, underscoring the BoE’s pledge to curb hot inflation. Governor Bailey said after the rate announcement that Bank would “stay the course to make sure that inflation falls all the way back to the 2% target”.

Nobody is expecting that the road to 2% will be easy, with inflation currently in double digits. The BoE remains optimistic that inflation will fall rapidly during the year and will fall to 5% by the end of the year. In February, the BOE predicted 4% inflation by the end of the year. This seems like a tall order but is certainly possible if the rate hikes make themselves felt and cool the economy.

There have been constant concerns that the BoE’s aggressive rate policy would lead to a recession, and six months ago, the BoE had projected a recession. Bailey reversed course yesterday, saying that the drop in energy prices and stronger economic growth meant that GDP would expand by a weak 0.25% in 2023, versus the 0.5% contraction in the previous forecast.

In the US, the economy is showing signs of cooling and high interest rates are expected to dampen the robust labour market. Unemployment claims surprised on the upside on Thursday, rising from 245,000 to 264,000, well above the estimate of 242,000. This is just one weekly report, but it’s sure to raise speculation that the labour market is showing cracks.

The US wraps up the week with UoM Consumer Confidence, which is pointing to a rather sour US consumer. The indicator fell to 63.5 in April and is expected to ease to 63.0 in May. Weak consumer confidence can translate into a decrease in consumer spending, a key driver of economic growth.

GBP/USD Technical

- GBP/USD is putting pressure on support at 1.2495. The next support level is 1.2366

- 1.2573 and 1.2676 are the next resistance lines