Sample Category Title

RBA Hopes for Stronger Data to Avoid “Policy Mistake” Discussion

With the market still digesting the recent central banks’ announcements, the focus in Australia now shifts to incoming economic data. Next week will give us more information on the consumer sector, with the RBA hoping that these data releases justify its recent surprise rate hike. In the meantime, the aussie would clearly love another push, especially as most of the gains recorded after the May 2 move have evaporated.

RBA probably feels better after various rate hikes globally

The RBA managed to pull a surprise at its most recent meeting by announcing a 25 bps rate hike and keeping the door open for further rate moves. This action was partly a reversal of the April meeting, but in our book, there was sufficient justification for this announcement. The rate hikes that ensued by both the Fed and ECB, and the hawkish commentary from the latter, are bound to have lifted the spirits in the RBA halls.

In the meantime, the statement of Monetary Policy published early on Friday, May 5 gave a bit more insight into the RBA’s decision. The updated forecasts point to inflation at 3%; the upper boundary set by the RBA, in 2025 and thus justifying the recent rate announcement. The market should probably pay more attention to this publication as the overall tone is not conducive to a stop in the rate hiking cycle.

As we are getting close to the peak of the current hiking cycle, central banks are afraid of repeating the famous “rate hike mistake” by Trichet et al in 2008. Therefore, incoming data remain extremely important for the monetary policy outlook, especially as we are clearly entering a critical phase with the market pricing in rate cuts for the key central banks over the next 12-15 months. In the case of the RBA, the market assigns a 40% change for another 25 bps rate increase by August, but then expects almost 53 bps of rate cuts by May 2024.

The consumer sector in the spotlight

The monthly Consumer inflation expectations will be released on Friday, May 12 with the market looking for a small acceleration. This indicator has actually been on an aggressive downwards path since June 2022, but remains elevated at a 4.6% year-on-year change. This recent drop has been captured by the Westpac consumer confidence survey jumping last month to the highest level since October 2020. Another strong set of consumer-related data would offer some early confirmation about the appropriateness of the recent RBA rate hike.

Housing data and business survey kick off the week

The week though starts on an equally high note. The building permits print for March is unlikely to be an easy reading for the RBA as this indicator is flirting with the multi-decade low print recorded in May 2022. The housing sector is the black spot globally, especially in regions like the euro area where the floating rate mortgages dominate the housing market.

Also on Monday, we get another business survey. The NAB business confidence survey has been stabilizing lately in negative territory, but the Business Conditions subcomponent is portraying a more positive picture. This move could be the result of some initial impact from the Chinese reopening, but it is evident that both the market and regional central banks were clearly expecting a stronger impact on their export volumes from China.

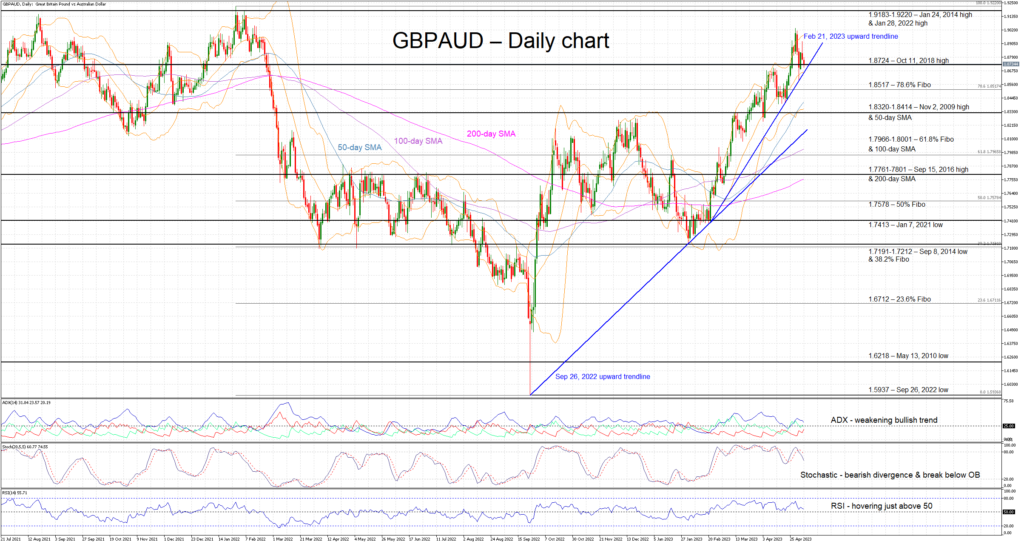

GBPAUD retreating from 15-month high

The aussie has had an interesting week following the RBA surprise announcement on Tuesday, May 2. The GBPAUD pair managed to retreat from the 15-month high, but it has come up against the February 21, 2023 upward sloping trendline. The recent upleg since mid-February has been very aggressive and hence a more sizeable pullback could be on the cards. A positive set of data releases could infuse some confidence into the aussie bears and help them stage a move towards the 1.8517 area.

On the other hand, a combination of weak economic figures and the growing expectations for another rate hike by the BoE on Thursday, 11 May could open the door for a retest of the April highs, and potentially a more convincing move towards the 1.90 area.

Bank of England Preview – 25 and Priming the Markets for a Pause

- We expect the Bank of England (BoE) to hike the Bank Rate by 25bp.

- We expect this to mark the peak in the Bank Rate of 4.50% as the BoE is set to signal a pause in the hiking cycle.

- EUR/GBP is set to remain rather unchanged but move slightly higher during the press conference on dovish remarks.

BoE call. We expect the Bank of England (BoE) to hike the Bank Rate (key policy rate) by 25bp on 11 May bringing it to 4.50%. This is in line with markets expectations.

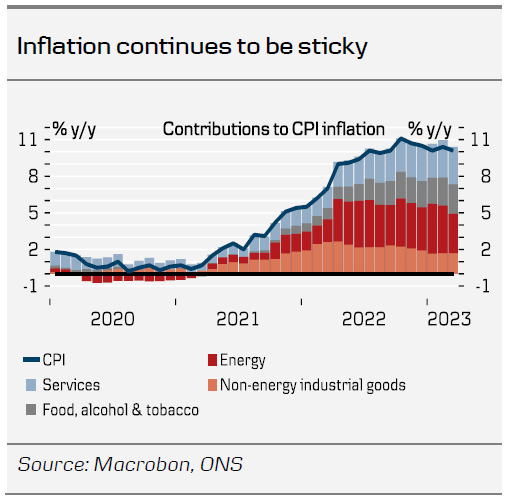

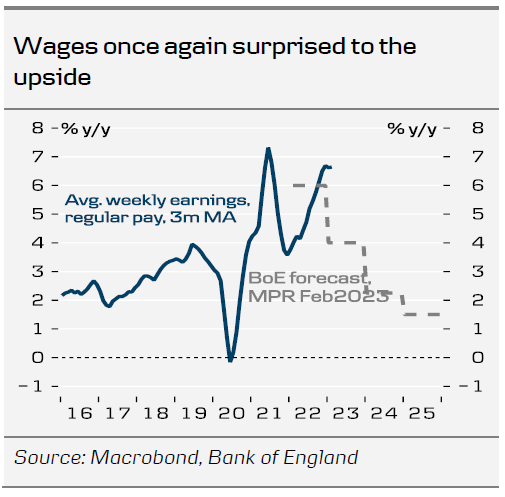

Since the last monetary policy decision in March, both wage growth and inflation releases have surprised to the upside. The latest labour market report showed a slightly higher unemployment rate at 3.8% (up from 3.7%), but unfilled vacancies remained markedly above pre-pandemic levels. However, wage growth excluding bonuses surprised largely to the upside at 6.6% (consensus: 6.2%) with wage growth levelling off in the private sector but continues to accelerate in the public sector. The MPC have expressed the importance of wage growth and hence this supports the view of another 25bp hike.

BoE's forecast of 9.2% from the February report as well as the consensus view. The contribution from the services sector remained unchanged at 3.07%. Hence, the inflation remains stickier than expected but with the large drop in shipping prices, lower agricultural commodity prices and the slowing rate of producer prices all points to lower goods inflation from here we believe this will drag the inflation lower despite the stickier services inflation. The latest BoE's monthly Decision Maker Panel survey showed that inflation expectations continued the trend lower seen over the recent months. Combined with core inflation, this remains a key release for the MPC in order to determine persistency of inflation pressures.

All in all, we expect this to be the final hike from the BoE but note that the BoE most likely will repeat the message that they will tighten further if there is evidence of further persistence in inflation. Hence, their approach remains increasingly data dependent. Markets pricing has increased the previous months to a peak rate of 4.8%, up from 4.5% at the end of March. At the same time, markets seems to see the probability for rate cuts this year as lower than previously. We expect no rate cuts until 2024.

Growth outlook. The UK economy seems to narrowly avoid a negative GDP growth in Q1 as well as the February print showed +0.1% on a 3M/3M basis at same time as the data from January was revised higher. PMI data also suggest a pick up in the activity with the composite index reached a 12 month high in April. The recession outcome that in October last year felt as a done deal for the UK economy is now on the course to be avoided.

FX. In our base case of a 25bp hike, we expect EUR/GBP to remain rather unchanged on the release but move slightly higher during the press conference. In its statement we expect the BoE to prime markets for a pause in the hiking cycle as the central banks want to fully evaluate the effect from previous Bank Rate increases. Overall, we regard the relative central bank outlook to be a positive for EUR/GBP but with other factors acting as a headwind, we increasingly see a case for continued range trading in the cross.

Sunset Market Commentary

Markets

Subsequent waves of investor uncertainty on the health of smaller/regional US banks this week unsettled the market dynamics, often overshadowing the impact of key economic data releases or even high profile central bank policy decisions, even from the likes of the Fed and the ECB. Another blip during the US session yesterday triggered a new safe haven run on core bonds. German/EMU yields closed at intraday lows while US yields rebounded later as panic subside again, laying the groundwork for a comeback in EMU yields this morning. First ECB speakers after yesterday’s ECB policy meeting (Villeroy, Simkus, Muller) joined Lagarde’s narrative that even as the ECB slowed the pace of rate hikes from 50 to 25 bps, additional steps should be expected at upcoming meetings. German yields rebound 7-8 bps this morning, with the focus shifting to the US April payrolls. The report showed little signs of a cooling in the US labour market. The economy in April added 253k jobs (vs 185k expected), admittedly with a cumulative 2-month downward revision of 149K. However other details of the report were also strong. AHE jumped 0.5% M/M (to 4.4%) vs 0.3% expected. The unemployment rate (based on the household data) declined from 3.5% to 3.4% (3.6% expected). The participation rate stabilized at 62.6% as employment according to this survey rose modestly combined with a small decline in the labour force. At least for now, there is no additional interference from financial stability issues. US yields are rising 8 bps (2-y) and 5 bps (30-y). Expectations on Fed interest rate cuts eased a bit post the report. Still, the market discounts about 75 bps of rate cuts by the December meeting. German yields add 9-10 bps across the curve with the short end outperforming (+6 bps). Good eco news this times is also seen as good for equities, with Eurostoxx50 rebounding 0.8%. US indices open with gains of about 1.0%. Easing fears on an imminent (US) recession, also support a bottoming process (Brent) oil, rebounding to $75 p/b compared to a correction low just north $ 71 p/b earlier this week.

After nearing (DXY) or outright testing (EUR/USD) key support levels yesterday, the dollar gained some further traction, but gains are far from impressive. DXY trades at 101.65 (from 101.34). EUR/USD eased to 1.098. Still the technical picture for the greenback hasn’t improved in any profound way. Even the gain in USD/JPY remains disappointing (134.80, with the week top still at 137.77). Despite higher core yields most smaller currencies perform well (EUR/SEK 11.22 from 11.286, EUR/NOK 11.65 from 11.8). This also applies to the CE currencies (EUR/CZK 23.40, EUR/HUF 372, EUR/PLN 4.575).

News & Views

The FAO Food Price Index by the UN showed a slight rebound in April (+0.6%) – the first increases since March 2022 – led by a steep increase in the sugar price index (+17.6%), along with an upturn in the meat price index (+1.3%), while the cereals (-1.7%), dairy (-1.7%) and vegetable oil price index (-1.3%) continued to drop. The Sugar Price Index rose for a third consecutive month to the highest level since October 2011. The increase was mostly related to heightened concerns over tighter global availabilities for India and China, along with lower-than-earlier-expected outputs in Thailand and the EU. The Cereal Price Index is down 19.8% Y/Y. A decline of in world prices of all major grains outweighed an increase in rice prices month on month. International wheat prices declined to their lowest level since July 2021.

Canadian payrolls beat market consensus. Employment grew by 41.4k in April (vs 20k expected). Details were more mixed with part time employment completely responsible for job gains (+47.6). Full time occupations dropped by 6.2k. The unemployment rate and participation rate both stabilized at respectively 5% and 65.6%. Interestingly, hourly wages for full time FTE rose by 5.2% Y/Y (vs 4.8% Y/Y). The loonie holds on to its daily gains against the dollar even as the greenback profits from strong US payrolls. CAD strength on today’s data has much to do with relatively hawkish comments by BoC governor Macklem yesterday who suggested that more work had to be done even as the BoC paused its tightening cycle since January. USD/CAD fell from 1.354 to 1.3475. First support remains far at 1.3302. Canadian swap yields rise around 10 bps across the curve today.

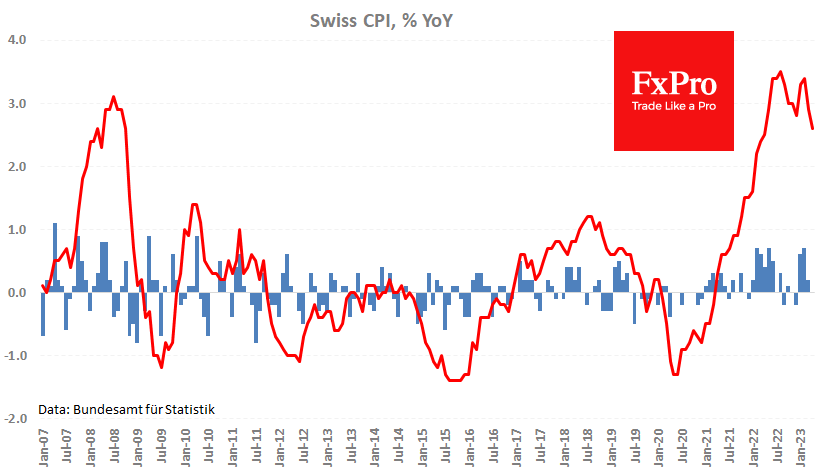

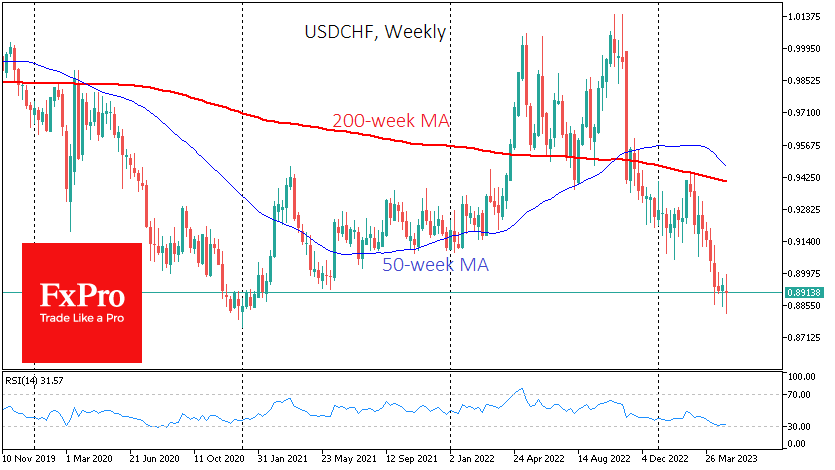

Swiss Franc is Losing Ground Due to Low Inflation

The Swiss franc declined, losing about 1% to 0.8920 after a fresh batch of macroeconomic data. The unemployment rate remains at 1.9%, a historic low. But at the same time, inflation is surprising, falling short of forecasts.

The consumer price index was virtually unchanged over the past month, and the annual inflation rate fell from 2.9% to 2.6%, while economists, on average, expected growth of 0.2% m/m and 2.8% y/y, respectively. The current inflation rate is the lowest in the last 11 months and very close to the SNB target.

The latter fact has spurred speculation that the country’s central bank will refrain from further tightening policy after raising rates by 225 points in the current monetary cycle. However, the head of SNB Jordan is in a hurry to moderate these expectations, not ruling out further rate hikes.

Switzerland’s significantly lower inflation is mainly due to the performance of the franc, which is now close to the same levels from which it began its decline against the dollar in early 2021. For comparison, the EURUSD is now 10% lower; at the worst point, it exceeded 22%.

The franc’s strengthening accelerated in March, apparently due to the problems of US banks, which caused steady demand for safe havens such as Switzerland. However, having slipped below 0.8900, USDCHF was close to the levels from which the SNB turned the pair to growth over the past 11 years.

It is hard to believe that this time the exchange rate will be reversed again by the intervention of the Central Bank since this would contradict the primary policy course. But over the years, support has been formed in this area, which will take a lot of work to pass.

US: Job Growth Surprised to the Upside in April, But Prior Months See Sizeable Downward Revisions

The U.S. economy added 253k jobs in April, well above the consensus forecast of 180k. Revisions to the two months prior were significant, subtracting 149k from the previously reported figures. Hiring over the last three-months averaged 222k, a meaningful stepdown from the 295k registered in March.

Employment gains on the service side (+197k) were concentrated in healthcare (+64k), professional & business services (+43k) and leisure & hospitality (+31k). Goods producing industries (+33k) added jobs on the month, with both construction (+15k) and manufacturing (+11k) chipping in with modest gains. Hiring across the public sector moderated, but still added 23k jobs.

In the household survey, civilian employment rose by a modest +139k, while the labor force shrank by 43k, resulting in the unemployment rate falling by 0.1%-pts to 3.4%. The participation rate held steady at 62.6%.

Average hourly earnings were up 0.5% month-on-month (m/m) – accelerating from March's gain of 0.3% m/m. Both the 12 and 3-month (annualized) moved higher, rising to 4.4% and 4.2%, respectively.

Key Implications

Job growth accelerated in April, but there were certainly some indications in the report suggesting that the labor market is softening. Revisions to the two prior months were significantly lower, which after smoothing through the monthly noise, the three-month moving average shows the pace of hiring has continued to decelerate. Moreover, the breadth of hiring – while having ticked higher in April – remains well below year ago levels.

The uptick in average hourly earnings comes as little surprise. We have been saying that the recent downward drift in average hourly earnings is likely more to do with the fact that this measure doesn't adjust for compositional shifts in the labor force. This distinction has been particularly key in recent months where leisure & hospitality– one of the lowest paying industries – has accounted for an outsized share of recent job creation. But with its contribution having significantly receded last month, we were bound to some acceleration in wage growth.

Taking this morning's report in conjunction with other recent labor market metrics (e.g., rising jobless claims, downward trend in job openings, and the uptick in layoffs) there are certainly some early signs of softening in the labor market. However, it's unclear if things are progressing fast enough. The FOMC has left the door open to another rate hike in June, and they may need to follow through on that if we don't see a more meaningful cooling in labor market conditions over the next few months. Let's see what next week's inflation report brings!

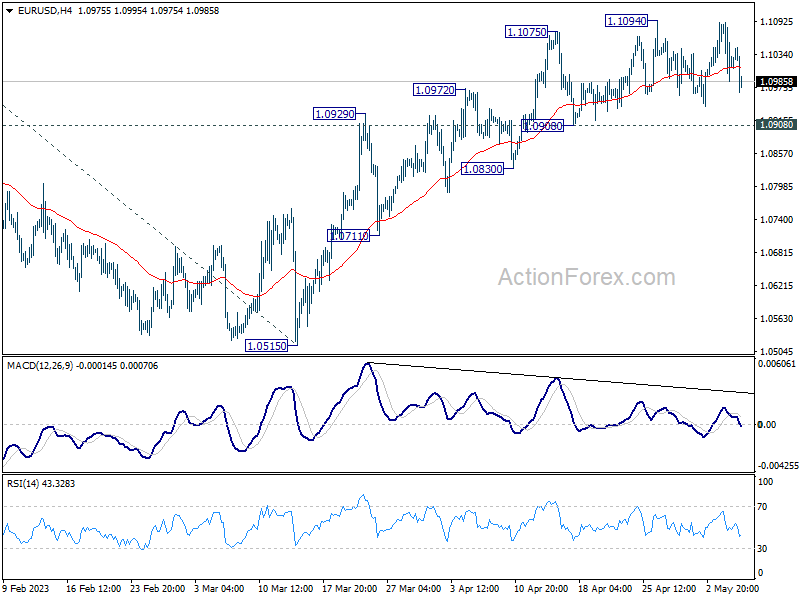

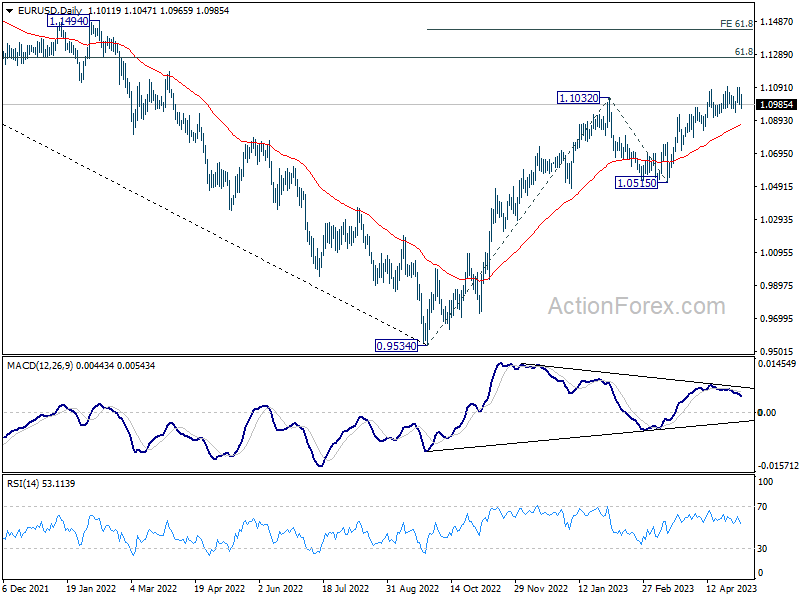

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0968; (P) 1.1030; (R1) 1.1073; More...

EUR/USD drops notably again today but stays in range of 1.0908/1094. Intraday bias remains neutral at this point. Outlook stays bullish as long as 1.0908 support holds. Further rally remains in favor for now. On the upside, firm break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441 However, considering bearish divergence condition in 4H MACD, break of 1.0908 support will indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

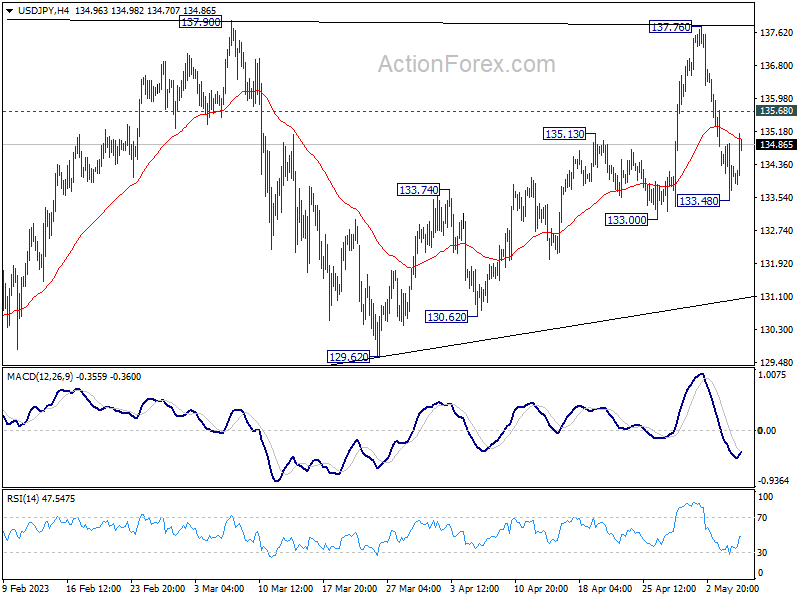

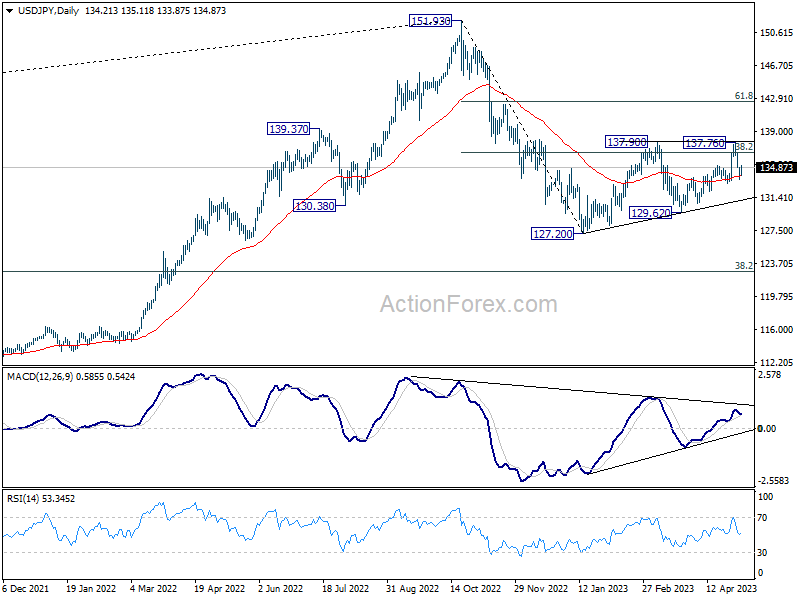

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 133.56; (P) 134.22; (R1) 134.94; More...

Intraday bias in USD/JPY is turned neutral first with current recovery. Fall from 137.76 is seen as the third leg of the pattern from 137.90. Below 133.48 will target 133.00 first, break will target 129.62 support. But still, as long as 129.62 holds, larger rebound from 127.20 is still in favor to resume at a later stage. On the upside, above 135.68 minor resistance will turn bias back to the upside for 137.76/90 instead.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 31.8% retracement of 151.93 to 127.20 at 136.34 will bring stronger rebound to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

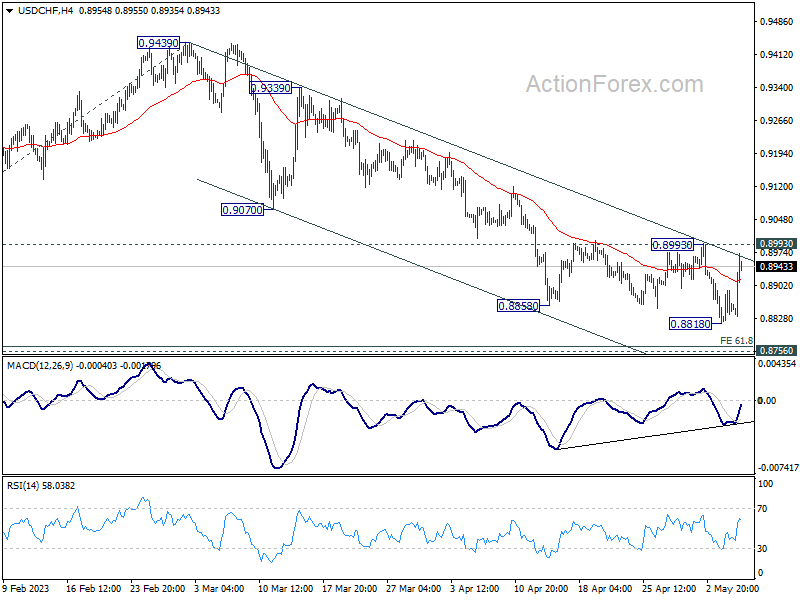

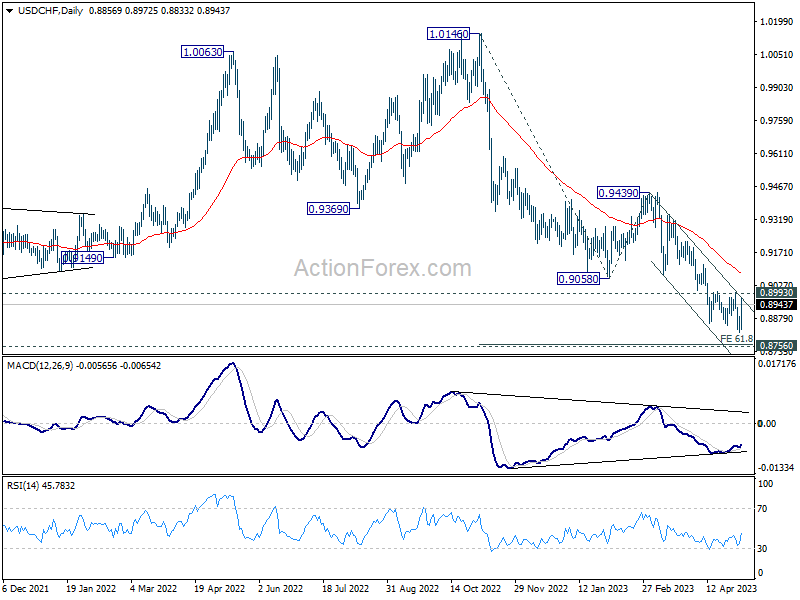

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8823; (P) 0.8857; (R1) 0.8894; More...

Intraday bias in USD/CHF is turned neutral with today's strong rebound. At this point, down trend from 1.0146 could still extend lower with 0.8993 resistance intact. However, strong support should be seen from 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support, to bring rebound, at least on first attempt. On the upside, break of 0.8993 resistance will indicate short term bottoming, on bullish convergence condition in 4H MACD, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

Canada’s Labour Market Surges Again

The Canadian labour market added 41.4k positions in April, with full-time employment down 6.2k and part-time employment up 47.6k.

The unemployment rate held steady at 5.0% and the participation rate held at 65.6%.

Employment was up in highly cyclical industries: wholesale/retail trade (+24k), transportation/warehousing (+17k), and information, culture and recreation (+16k). A decline was seen in business, building and other support services (-14k), but this was just an offset from last month's big gain.

Lastly, total hours worked were up 0.2% month-on-month and wages were up 5.2% year-on-year (vs 5.3% in March).

Key Implications

Once again, the Canadian jobs market surprises to the upside. Over the last seven months, employment has risen 412k, three times the trend pace over the 2010 to 2019 time period. This has been driven by rapid population growth, which has surged by a million people in the last year. The supply of workers has been boosted, enabling firms to put a big dent in the number of job vacancies.

The BoC won't change its policy stance based on this report. The inflow of new Canadians is changing the calculus on what a standard jobs report looks like. The fact that the unemployment rate has been stable means that we may have reached a new steady state. This means that the 'surprise' employment report isn't adding the same labour market tightness as it would have in the past. Plus, the BoC can always focus on the lack of breath in sector hiring and the fact that this print was driven by part-time employment, with full-time employment going negative. All told, the BoC's position on the sidelines is probably more stable following today's release.

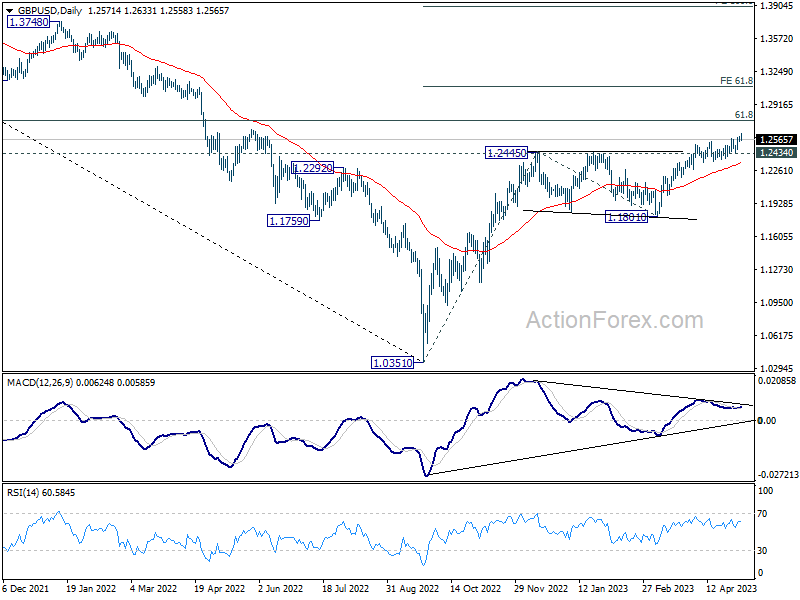

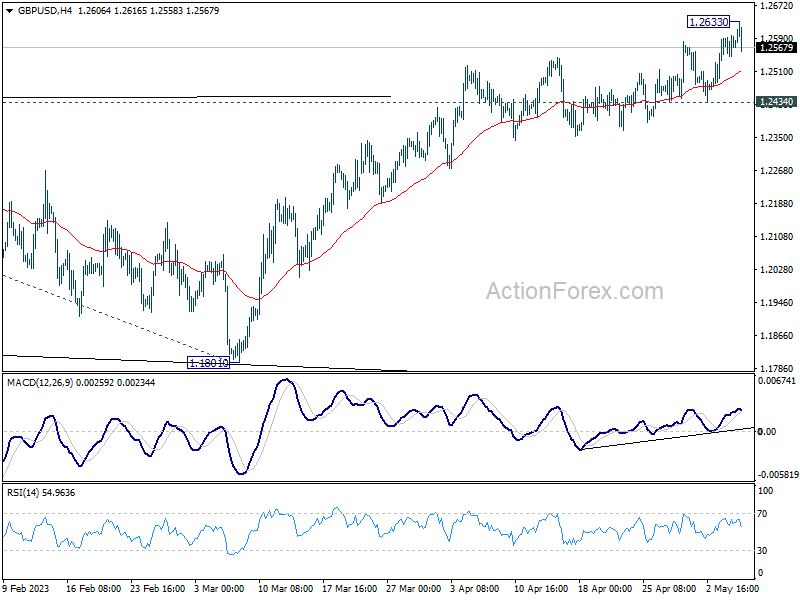

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2548; (P) 1.2573; (R1) 1.2598; More...

GBP/USD retreats notably after hitting 1.2633 and intraday bias is turned neutral first. Some consolidations could be seen but near term outlook will stay bullish as long as 1.2434 support holds. Break of 1.2633 will resume recent up trend to 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.