Sample Category Title

Dollar Rallies on Strong Non-Farm Payroll Data, Can It Keep the Momentum?

Dollar jumps in early US session as lifted by a set of strong non-farm payroll data. But it remains to be seen if buying could sustain. Still, Canadian Dollar looks even stronger for its own robust employment data too. For now, Swiss Franc is the worst performer for the day, very much thanks to the reversal in cross against Euro. Yen is the second worst, followed by Euro. The Looking is the strongest one, followed by Aussie. Let's see if the greenback to reclaim more of the ground lost earlier in the week.

Technically, USD/CHF is heading back to 0.8993 resistance quickly. Decisive break there will be a signal of near term bullish reversal, on bullish convergence condition in daily MACD, ahead of 0.8756 long term support (2020 low). That, if realized, could be an early sign of turn around in Dollar in general. In particular, Both EUR/USD and GBP/USD could follow with deeper pull back.

In Europe, at the time of writing, FTSE is up 0.48%. DAX is up 0.73%. CAC is up 0.66%. Germany 10-year yield is up 0.0105 at 2.295. Earlier in Asia, Japan was still on holiday. Hong Kong HSI rose 0.50%. China Shanghai SSE dropped -0.48%. Singapore Strait Times dropped -0.08%.

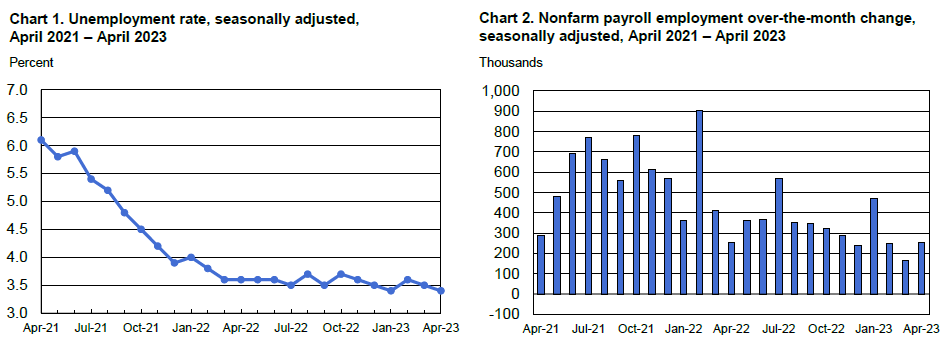

US NFP grew 253k, unemployment rate down to 3.4%, avg hour earnings up 0.5% mom

US non-farm payroll employment grew 253k in April, well above expectation of 181k. However, prior month's growth figure was revised sharply down from 236k to 165k. That compared to the average monthly growth of 290k over the prior 6 months.

Unemployment rate dropped from 3.5% to 3.4%, below expectation of staying unchanged at 3.5%. Overall, unemployment rate has ranged from 3.4% to 3.7% since March 2022. Labor force participation rate was unchanged at 62.6%. Employment-population ratio was also unchanged at 60.4%.

Average hourly earnings grew strongly by 0.5% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings have increased by 4.4%.

Also released, Canada employment grew 41k or 0.2% mom in April, well above expectation of 21.6k. Part-time employment increased by 48k while full-time employment held steady. Unemployment rate was unchanged at 5.0%, holding steady at this level since December 2022. Unemployment rate was also near record low of 4.9% made in June and July 2022. On a year-over-year basis, average hourly wages rose 5.2%.

ECB SPF downgrades 2023 headline inflation forecasts, upgrades core

In ECB Survey of Professional Forecasters for Q2 2023, respondents downgraded their expectations for headline HICP inflation in 2023 downward. The lower headline inflation expectations are primarily attributed to expectations of reduced energy price inflation, particularly for natural gas. Headline inflation expectations for 2023, 2024, and 2025 are now at 5.6%, 2.6%, and 2.2%, respectively, compared to Q1 forecasts of 5.9%, 2.7%, and 2.1%.

On the other hand, expectations for HICP inflation excluding food and energy in 2023 were revised upward, primarily results from recent data outturns and higher wage growth forecasts. Core inflation projections are at 4.9% in 2023, 2.8% in 2024, and 2.3% in 2025, comparing to prior forecasts of 4.4%, 2.8% and 2.3% respectively.

Real GDP growth is now projected at 1.2% in 2023, 1.6% in 2024, and 1.4% in 2025, compared to prior forecasts of 1.4%, 1.7%, and 1.4%.

Eurozone retail sales contracted -1.2% mom in Mar, EU down -1.1% mom

Eurozone retail sales volume contracted -1.2% mom in March, much worse than expectation of -0.2% mom. The volume of retail trade decreased by -1.4% mom for food, drinks and tobacco and by -1.1% mom for non-food products, while it increased by 1.6% mom for automotive fuels.

EU retail sales declined by -1.1% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in Latvia (-2.7%), Germany and Poland (both -2.4%) and Luxembourg (-1.9%). The highest increases were observed in Romania (+2.9%), Portugal (+2.3%) and Ireland (+1.0%).

Swiss CPI slowed to 2.6% yoy in Apr, core CPI unchanged at 2.2% yoy

Swiss CPI slowed from 2.9% yoy to 2.6% yoy in April, below expectation of 2.8% yoy. Core CPI (excluding fresh and seasonal products, energy and fuel) was unchanged at 2.2% yoy. Domestic prices edged down from 2.7% yoy to 2.6% yoy. Imported prices plunged from from 3.8% yoy to 2.4% yoy.

For the month, CPI was unchanged at 0.0% mom. Core CPI rose 0.2% mom. Domestic prices rose 0.2% while imported prices rose 0.2% mom.

RBA SoMP: Faster inflation slowdown in 2023, but not after

In the quarterly Statement on Monetary Policy, RBA reiterated that "some further tightening of monetary policy may be required" to ensure that inflation returns to target in a "reasonable timeframe". But that will depend upon "how the economy and inflation evolve."

The new economic projections show both headline and trimmed mean inflation slowing more rapidly in 2023. However, both measures are only expected to reach the top of target range by mid-2025. Additionally, the central bank downgraded its GDP growth forecasts for 2023 and predicts a higher unemployment rate. The evolving economic landscape will be key in determining the RBA's future policy moves.

Year-average GDP growth forecast:

- 2023 at 1.75% (revised down from 2.25%).

- 2024 at 1.50% (unchanged).

Unemployment rate forecast:

- Dec 2023 at 4.00% (revised up from 3.75%).

- Dec 2024 at 4.50% (revised up from 4.25%).

Headline CPI forecast:

- Dec 2023 at 4.50% (revised down from 4.75%).

- Dec 2024 at 3.25% (unchanged).

- Jun 2025 at 3.00% (unchanged).

Trimmed mean CPI forecast:

- Dec 2023 at 4.00% (revised down from 4.25%).

- Dec 2024 at 3.00% (unchanged).

- Jun 2025 at 3.00% (unchanged).

China Caixin PMI services dropped to 56.4, remains to be seen if rebound sustainable

China's Caixin PMI Services dropped to 56.4 in April, down from 57.8 in March and slightly below the expected 56.5. According to Caixin, the sector experienced slower yet still sharp increases in activity and new work, while input cost inflation accelerated to a one-year high. Employment growth slowed and backlogs continued to build, with the PMI Composite index falling from 54.5 to 53.6.

Wang Zhe, Senior Economist at Caixin Insight Group said: "In April, the services sector kept up momentum, while manufacturing activity turned comparatively sluggish and became a drag on economic growth. It remains to be seen if the economic rebound is sustainable after a short-term release of pent-up demand, with a number of indicators flagging that the recovery has yet to find a stable footing."

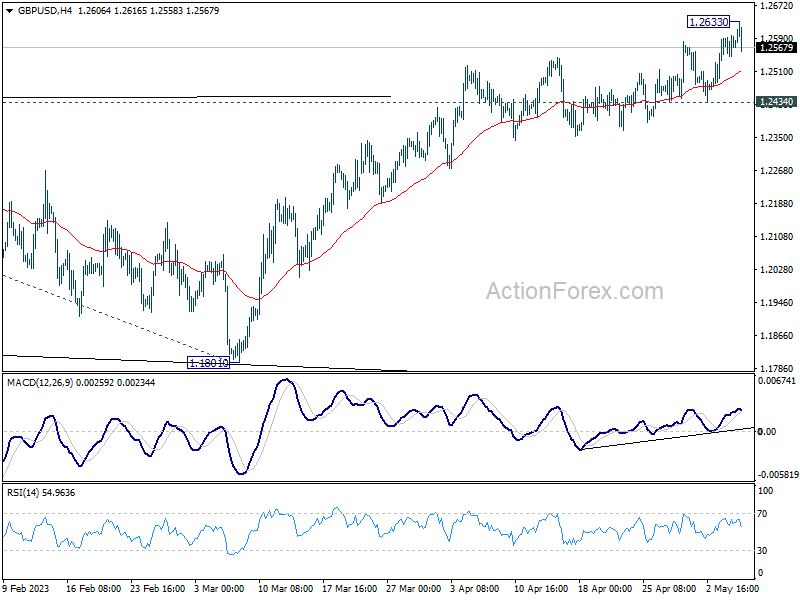

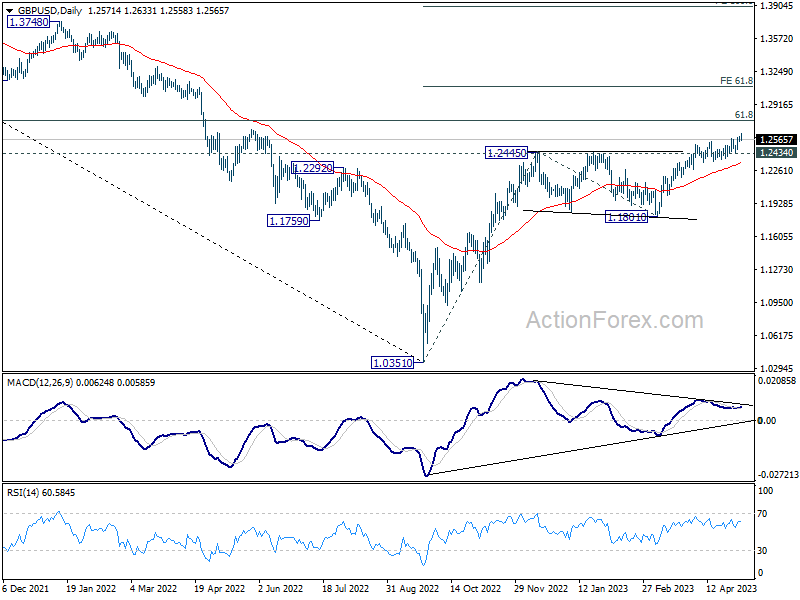

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2548; (P) 1.2573; (R1) 1.2598; More...

GBP/USD retreats notably after hitting 1.2633 and intraday bias is turned neutral first. Some consolidations could be seen but near term outlook will stay bullish as long as 1.2434 support holds. Break of 1.2633 will resume recent up trend to 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Monetary Policy Statement | ||||

| 01:45 | CNY | Caixin Services PMI Apr | 56.4 | 56.5 | 57.8 | |

| 05:45 | CHF | Unemployment Rate Apr | 1.90% | 1.90% | 1.90% | |

| 06:00 | EUR | Germany Factory Orders M/M Mar | -10.70% | -2.00% | 4.80% | |

| 06:30 | CHF | CPI M/M Apr | 0.00% | 0.20% | 0.20% | |

| 06:30 | CHF | CPI Y/Y Apr | 2.60% | 2.80% | 2.90% | |

| 06:45 | EUR | France Industrial Output M/M Mar | -1.10% | -0.30% | 1.20% | 1.40% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Apr | 732B | 743B | ||

| 08:00 | EUR | Italy Retail Sales M/M Mar | 0.00% | 0.00% | -0.10% | |

| 08:30 | GBP | Construction PMI Apr | 51.1 | 51.1 | 50.7 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | -1.20% | -0.20% | -0.80% | |

| 12:30 | USD | Nonfarm Payrolls Apr | 253K | 181K | 236K | 165K |

| 12:30 | USD | Unemployment Rate Apr | 3.40% | 3.50% | 3.50% | |

| 12:30 | USD | Average Hourly Earnings M/M Apr | 0.50% | 0.30% | 0.30% | |

| 12:30 | CAD | Net Change in Employment Apr | 41.4K | 21.6K | 34.7K | |

| 12:30 | CAD | Unemployment Rate Apr | 5.00% | 5.10% | 5.00% |

US NFP grew 253k, unemployment rate down to 3.4%, avg hour earnings up 0.5% mom

US non-farm payroll employment grew 253k in April, well above expectation of 181k. However, prior month's growth figure was revised sharply down from 236k to 165k. That compared to the average monthly growth of 290k over the prior 6 months.

Unemployment rate dropped from 3.5% to 3.4%, below expectation of staying unchanged at 3.5%. Overall, unemployment rate has ranged from 3.4% to 3.7% since March 2022. Labor force participation rate was unchanged at 62.6%. Employment-population ratio was also unchanged at 60.4%.

Average hourly earnings grew strongly by 0.5% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings have increased by 4.4%.

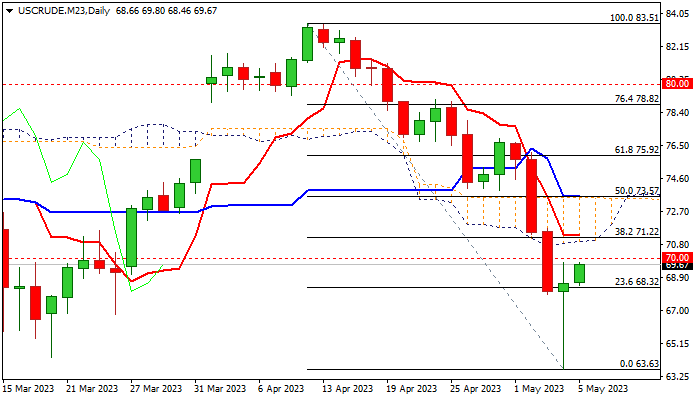

WTI Oil: Recovery from New Multi-Month Low Likely to be Limited as Negative Fundamentals weigh

WTI contract is holding in recovery mode for the second straight day, following a dramatic fall this week, which hit the lowest since Dec 2021 before bouncing.

Oil was down over 15% before regaining ground, pressured by growing fears about US recession and turbulence in banking sector, as well as weaker than expected China’s manufacturing data which add to the risk of weaker demand from world’s largest oil importer.

Quick rebound which left a daily candle with very long tail on Thursday, points to strong bids at the zone of former multi-month low at $64.34 (Mar 20).

Recovery is likely to mark a price adjustment and offer better selling levels as the picture on daily chart is firmly bearish and warn of fresh weakness on persisting negative fundamentals.

Correction is still holding below psychological $ 70 resistance, break of which may spark further upside as next week’s daily cloud twist could be magnetic.

Extended upticks should be capped by strong barriers at $71.06/33 zone (daily cloud base / Fibo 38.2% of $83.51/$63.63 daily Tenkan-sen) to mark a healthy correction before bears regain control.

Firm break of recent lows ($64.34/$63.63) to challenge immediate supports at $62.42 and $61.79 (Dec/Aug 2021 troughs) and risk acceleration towards $53.87 (Fibo 61.8% of $6.32/$130.48) if fundamental picture worsens.

Only break above $73.57 (daily Kijun-sen / 50% retracement of $83.51/$63.63) would sideline downside risk and generate reversal signal.

Res: 70.00; 71.06; 71.33; 73.57.

Sup: 68.32; 67.94; 66.81; 64.34.

ECB SPF downgrades 2023 headline inflation forecasts, upgrades core

In ECB Survey of Professional Forecasters for Q2 2023, respondents downgraded their expectations for headline HICP inflation in 2023 downward. The lower headline inflation expectations are primarily attributed to expectations of reduced energy price inflation, particularly for natural gas. Headline inflation expectations for 2023, 2024, and 2025 are now at 5.6%, 2.6%, and 2.2%, respectively, compared to Q1 forecasts of 5.9%, 2.7%, and 2.1%.

On the other hand, expectations for HICP inflation excluding food and energy in 2023 were revised upward, primarily results from recent data outturns and higher wage growth forecasts. Core inflation projections are at 4.9% in 2023, 2.8% in 2024, and 2.3% in 2025, comparing to prior forecasts of 4.4%, 2.8% and 2.3% respectively.

Real GDP growth is now projected at 1.2% in 2023, 1.6% in 2024, and 1.4% in 2025, compared to prior forecasts of 1.4%, 1.7%, and 1.4%.

USD/CAD Extends Slide ahead of Job Reports

- Canada’s employment change expected to slow

- US nonfarm payrolls projected to fall to 179,000

- Canadian dollar rallies for third straight day

The Canadian dollar continues to rally today and has climbed 120 points since Tuesday. Earlier in the day, USD/CAD touched a low of 1.3490, its lowest level since April 21st.

Canadian employment change expected to ease

The markets will be treated to key employment numbers on both sides of the border later today. Canada is expected to have added 20,000 new jobs in April, following 34,700 in March. This would be the lowest reading in four months and would be a clear sign that the labour market is weakening as interest rate hikes make their effect felt on the economy.

In the US, nonfarm payrolls for April could move the dial on the US dollar ahead of the weekend. The markets are braced for a drop to 179,000, following 236,000 in March. There is a growing feeling that the labour market, which is been surprisingly resilient to relentless rate hikes, is showing cracks. Unemployment claims jumped to 242,000, up from a downwardly revised 229,000 and above the consensus of 240,000. Business optimism remains weak and that could translate into less hiring. If nonfarm payrolls fall to 180,000 or less, I would expect to see the US dollar lose ground, on expectations that the Fed may ease policy.

The Fed’s rate hike of 25 basis points this week may have been the end of the current rate-hike cycle, in which the Fed has raised rates 10 consecutive times. Fed Chair Powell hinted that the Fed could pause rates as soon as June, although he reminded his listeners that the battle against inflation was far from over and didn’t close the door on further hikes. The markets are betting on a pause in June, with a probability of 99%, according to the CME Group.

Powell said that given the inflation outlook, rate cuts were not on the table. The markets don’t buy it and have priced in a rate cut at around 50% in July and a whopping 88% in September, according to the CME Group.

USD/CAD Technical

- USD/CAD tested support at 1.3492 earlier. Next, there is support at 1.3435

- 1.3580 and 1.3637 are the next resistance lines

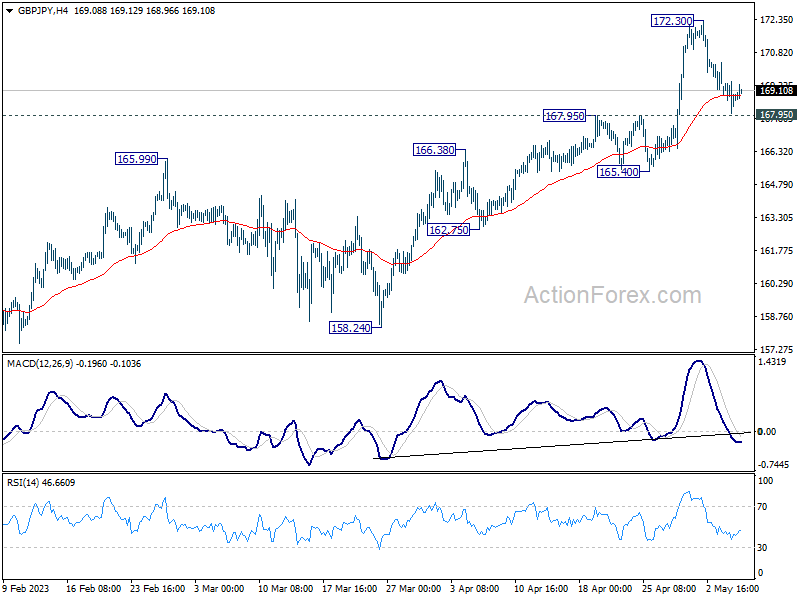

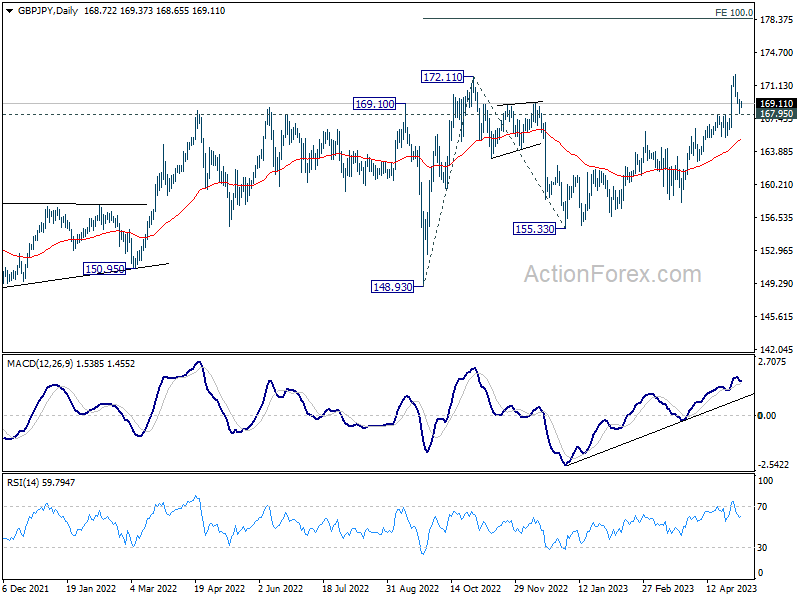

GBP/JPY Daily Outlook

Daily Pivots: (S1) 168.07; (P) 168.81; (R1) 169.55; More...

Intraday bias in GBP/JPY stays neutral for the moment. Downside of retreat should be contained by 167.95 resistance turned support to bring another rally. On the upside, break of 172.30 will resume larger up trend to 100% projection of 148.93 to 172.11 from 155.33 at 178.51. Nevertheless, firm break of 167.95 should confirm short term topping, and turn bias back to the downside for deeper pull back to 165.40 support instead.

In the bigger picture, based on current momentum, up trend from 123.94 (2020 low) is likely ready to resume. Next target is 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. This will now remain the favored case as long as 165.40 support holds, in case of retreat.

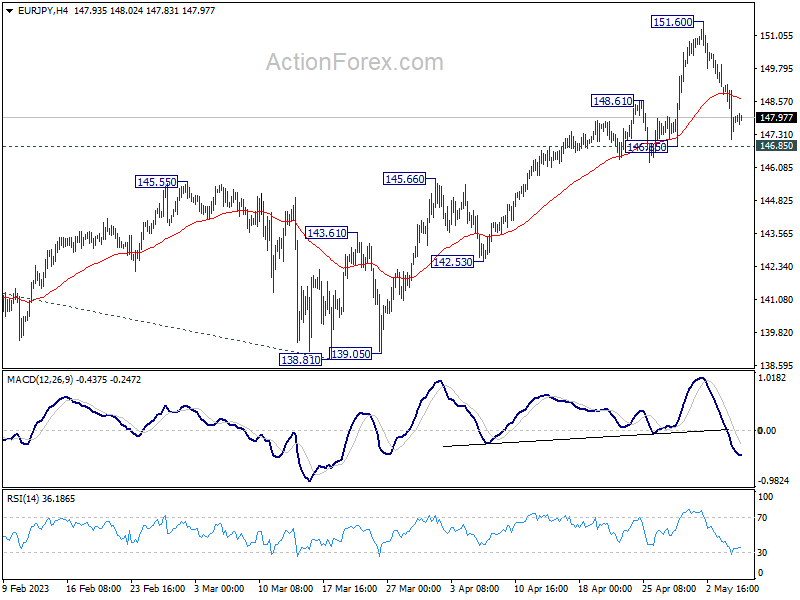

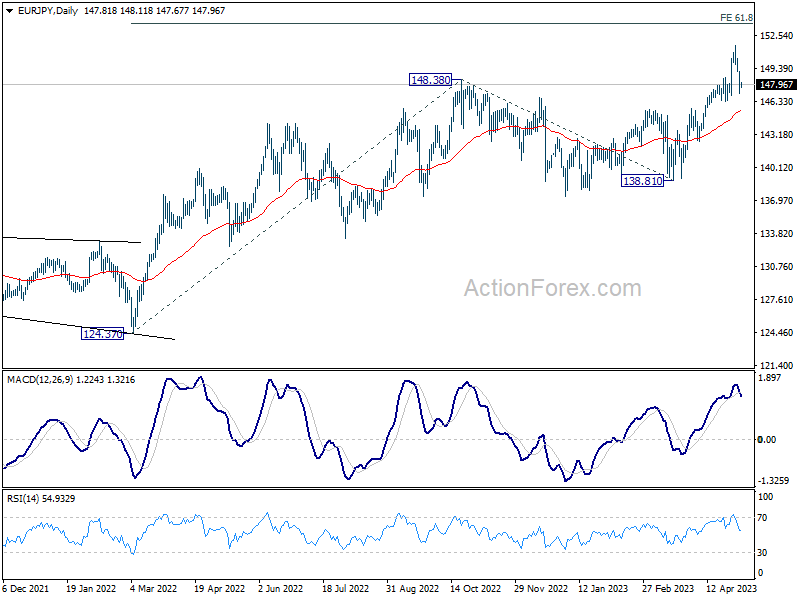

EUR/JPY Daily Outlook

Daily Pivots: (S1) 146.94; (P) 148.07; (R1) 149.02; More....

EUR/JPY's retreat from 151.60 extended lower but it's holding above 146.85 support. Intraday bias remains neutral and outlook stays bullish. On the upside, break of 151.60 will resume larger up trend to 153.64 projection level. Nevertheless, firm break of 146.85 will confirm short term topping and turn bias to the downside for deeper pull back.

In the bigger picture, current development indicates that rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 138.81 support holds, even in case of deep pull back.

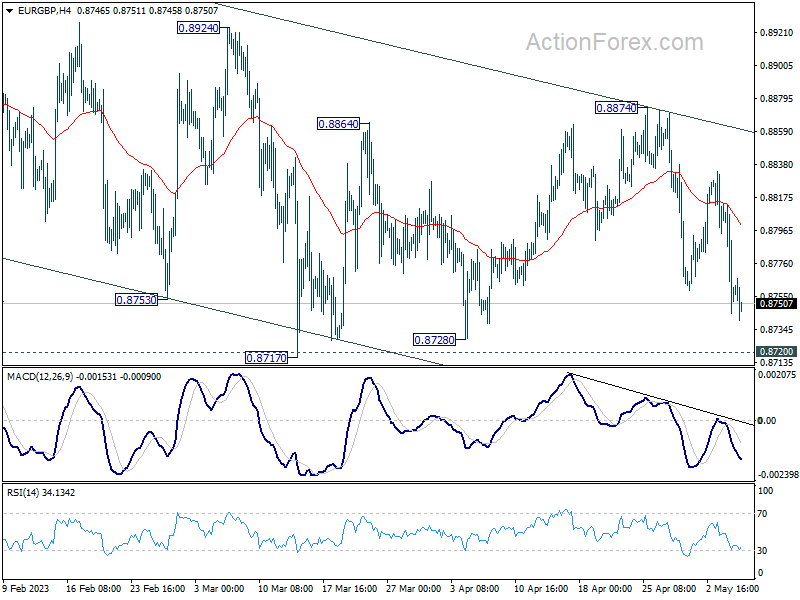

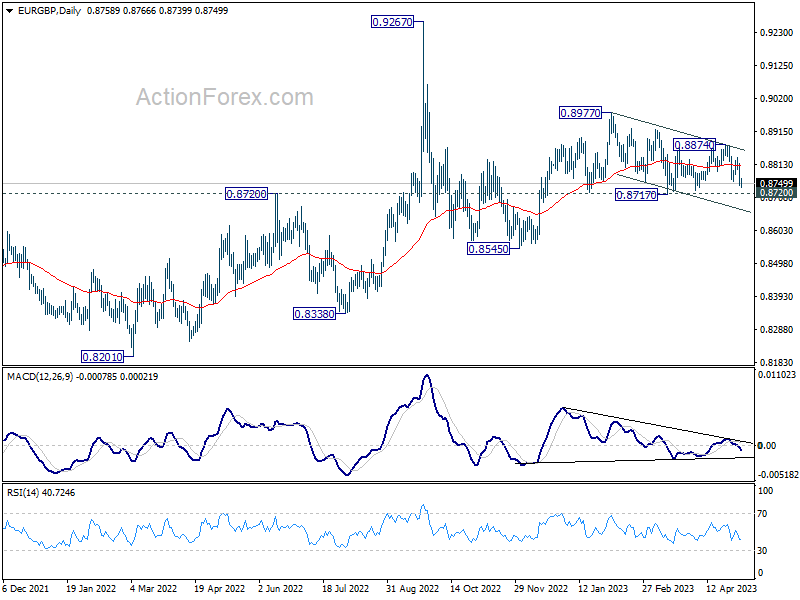

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8733; (P) 0.8773; (R1) 0.8801; More...

Intraday bias in EUR/GBP remains neutral as range trading continues, and outlook is mixed. On the downside, decisive break of 0.8717 support will resume whole choppy decline from 0.8977. On the upside, break of 0.8874 will resume the rebound from 0.8717 instead.

In the bigger picture, outlook remains rather mixed for now, except that price actions from 0.9267 (2022 high) are part of the long term range pattern from 0.9499 (2020 high). With 0.8720 support intact, rise from 0.8545 is in favor to continue through 0.8977. However, firm break of 0.8720 will argue that such rebound has completed, and open up deeper fall through this support level.

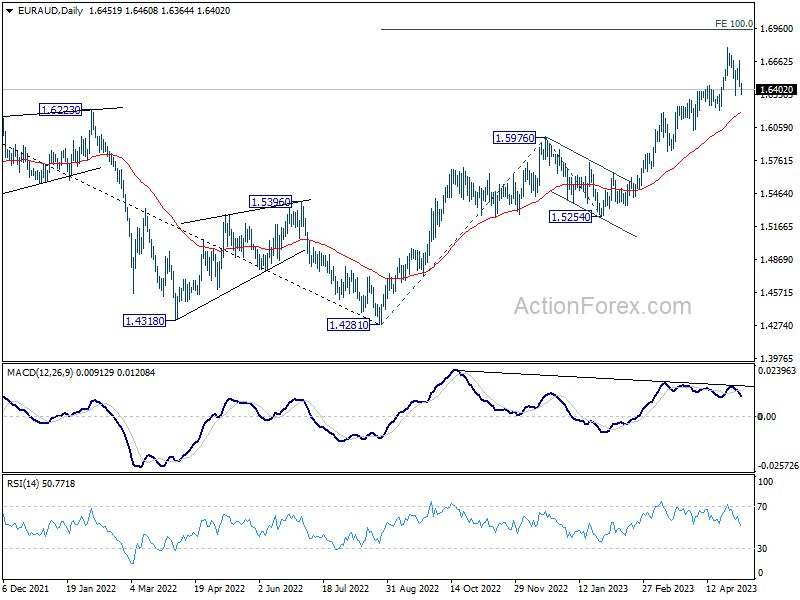

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6368; (P) 1.6518; (R1) 1.6603; More...

EUR/AUD is staying in consolidation from 1.6785 and intraday bias remains neutral for the moment. As long as 1.6219 support holds, further rally is expected. On the upside, break of 1.6785 will resume larger up trend to 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949. However, firm break of 1.6219 will argue that larger correction is on the way.

In the bigger picture, the solid break of 1.6434 resistance argues that whole down trend from 1.9799 (2020 high) has completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement of 1.9799 to 1.4281 at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

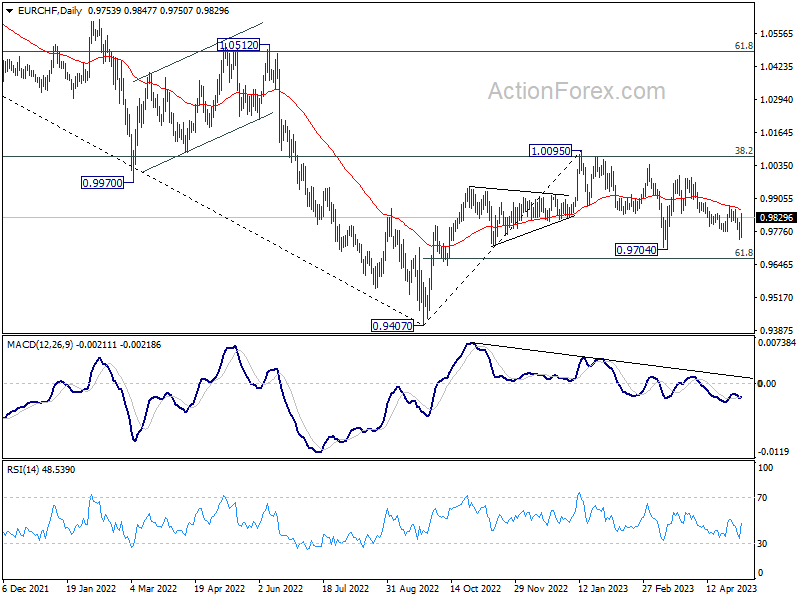

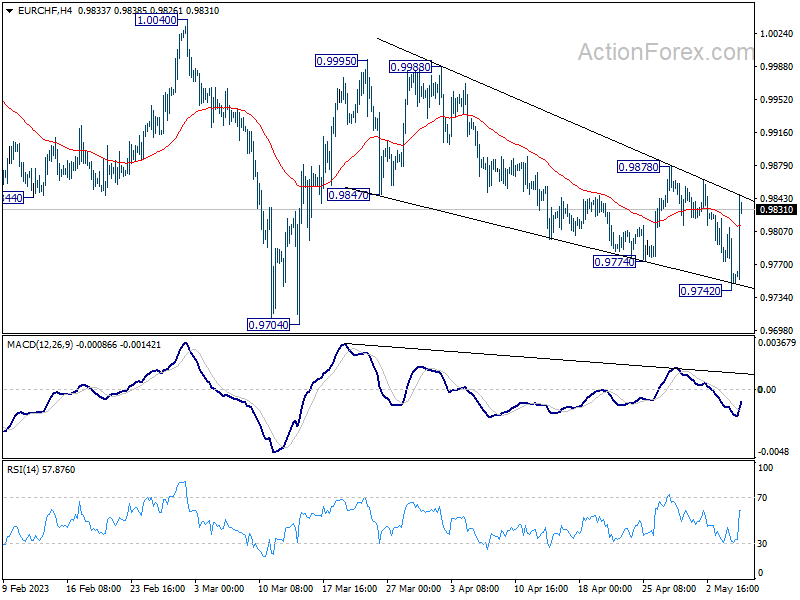

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9730; (P) 0.9772; (R1) 0.9798; More...

EUR/CHF rebounded strongly after dipping to 0.9742 and intraday bias is turned neutral first. On the upside, break of 0.9878 will indicate short term bottoming, and turn bias back to the upside. Also, outlook is unchanged that whole correction from 1.0095 has completed at 0.9704. Sustained trading 55 D EMA (now at 0.9864) will affirm this bullish case, and target 0.9995 resistance next.

In the bigger picture, prior rejection by 55 W EMA (now at 0.9972) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).