Sample Category Title

EUR/JPY Weekly Outlook

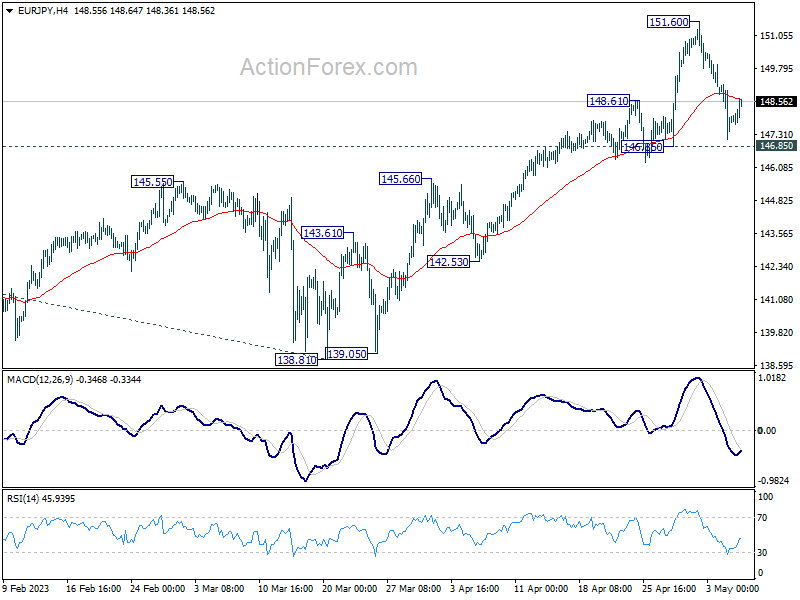

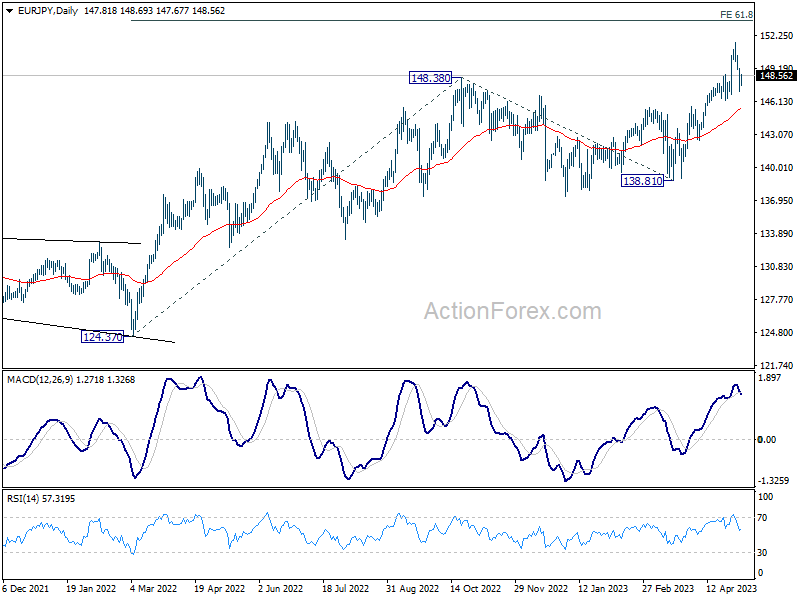

EUR/JPY's pull back from 151.60 extended lower last week, but recovered ahead of 146.85 support. Initial bias stays neutral this week first, and outlook stays bullish. On the upside, break of 151.60 will resume larger up trend to 153.64 projection level. Nevertheless, firm break of 146.85 will confirm short term topping and turn bias to the downside for deeper pull back.

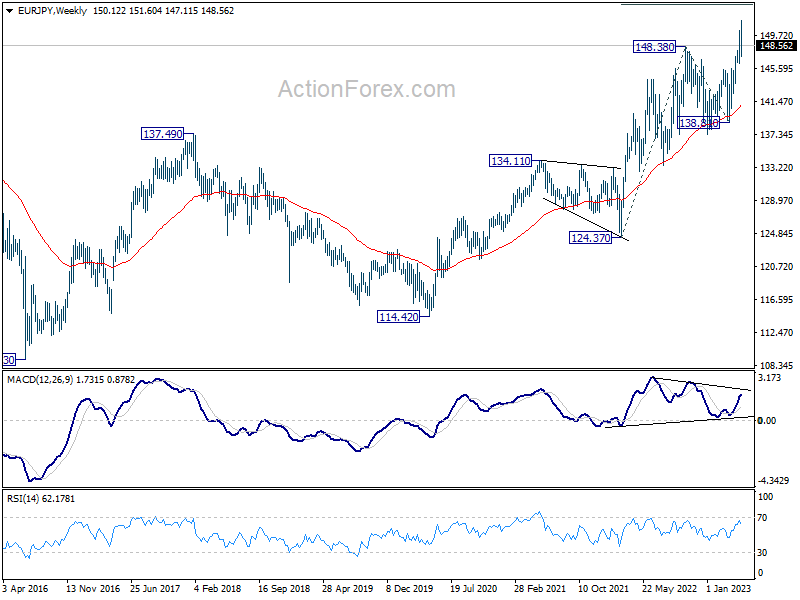

In the bigger picture, current development indicates that rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 138.81 support holds, even in case of deep pull back.

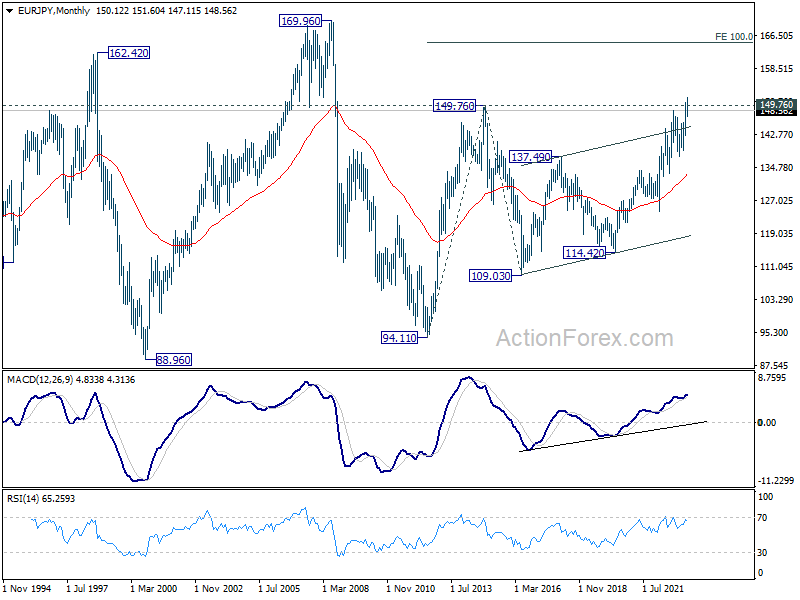

In the long term picture, break of 149.76 (2014 high) argues that whole up trend form 94.11 (2012 low) is resuming. Sustained trading above 149.76 will pave the way to 100% projection of 94.11 to 149.76 from 109.03 at 164.68, which is close to 169.96 (2008 high).

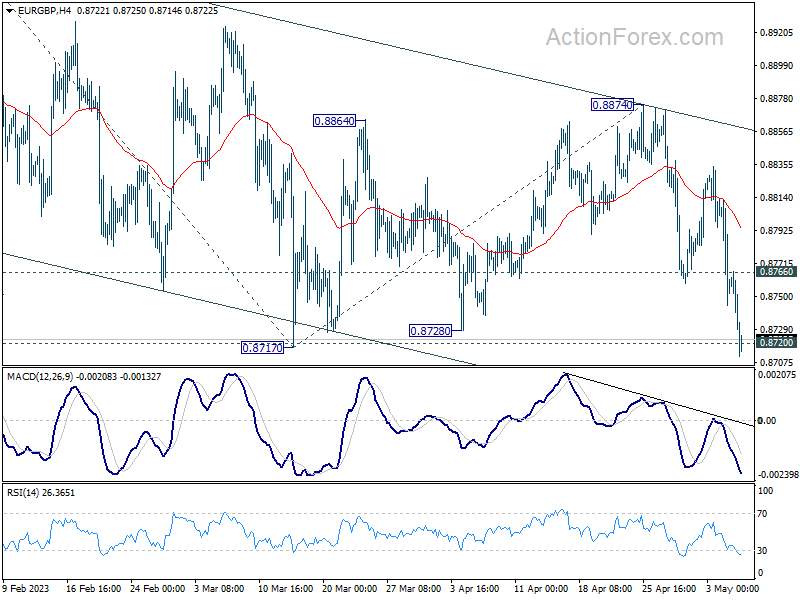

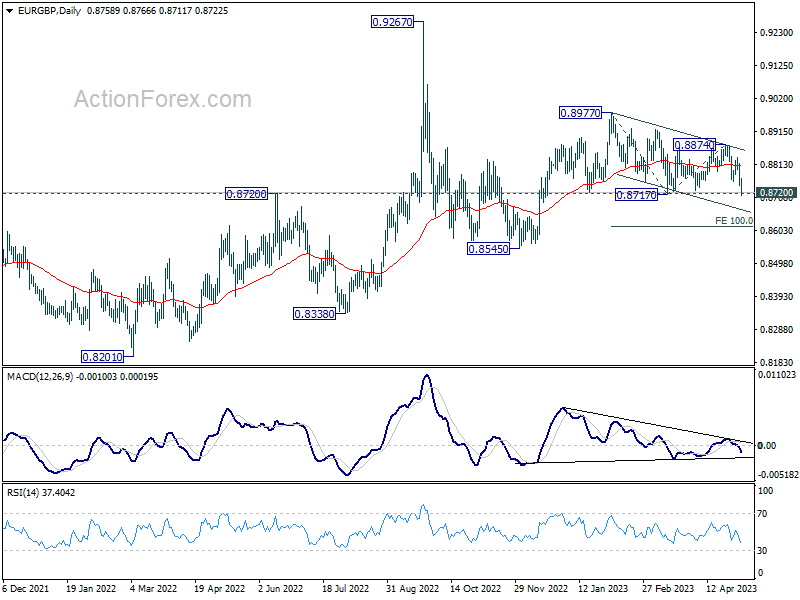

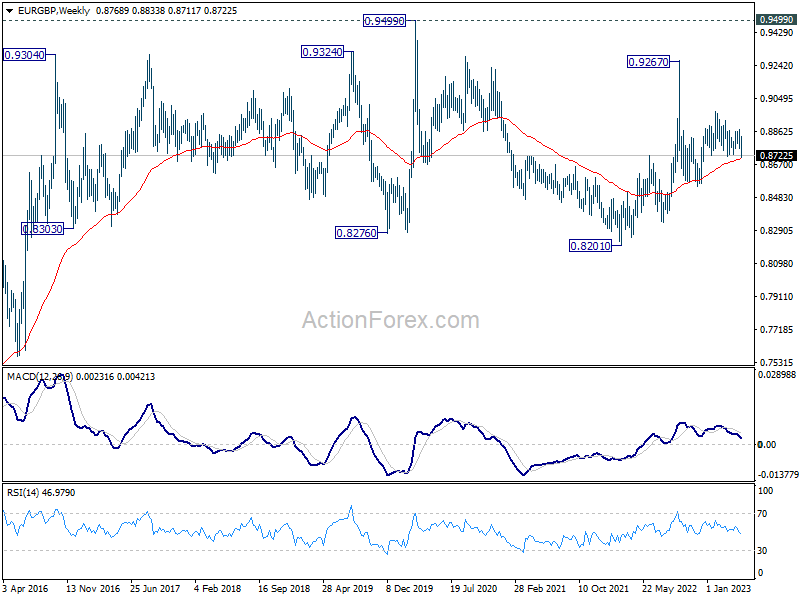

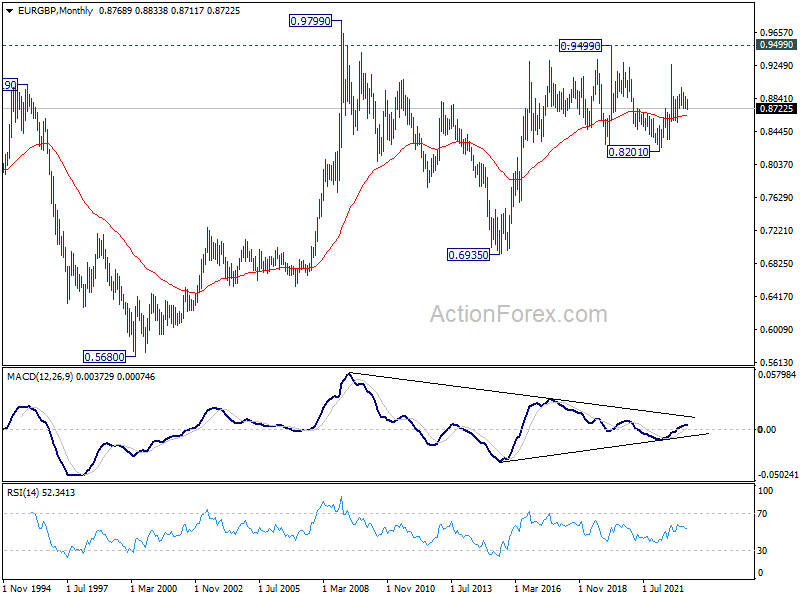

EUR/GBP Weekly Outlook

EUR/GBP's break of 0.8717 support indicates that the choppy decline from from 0.8977 is resuming. Initial bias is now on the downside this week. Deeper fall would be seen to 100% projection of 0.8977 to 0.8717 from 0.8874 at 0.8614. On the upside, above 0.8766 minor resistance will turn intraday bias neutral first.

In the bigger picture, outlook remains rather mixed for now, except that price actions from 0.9267 (2022 high) are part of the long term range pattern from 0.9499 (2020 high). With 0.8720 support intact, rise from 0.8545 is in favor to continue through 0.8977. However, firm break of 0.8720 will argue that such rebound has completed, and open up deeper fall through this support level.

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to extend at a later stage, to 0.9799 (2009 high).

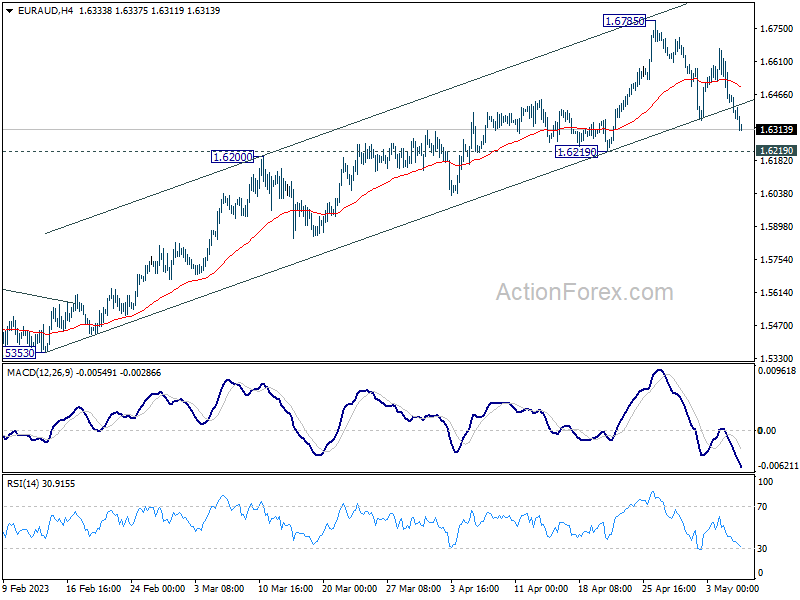

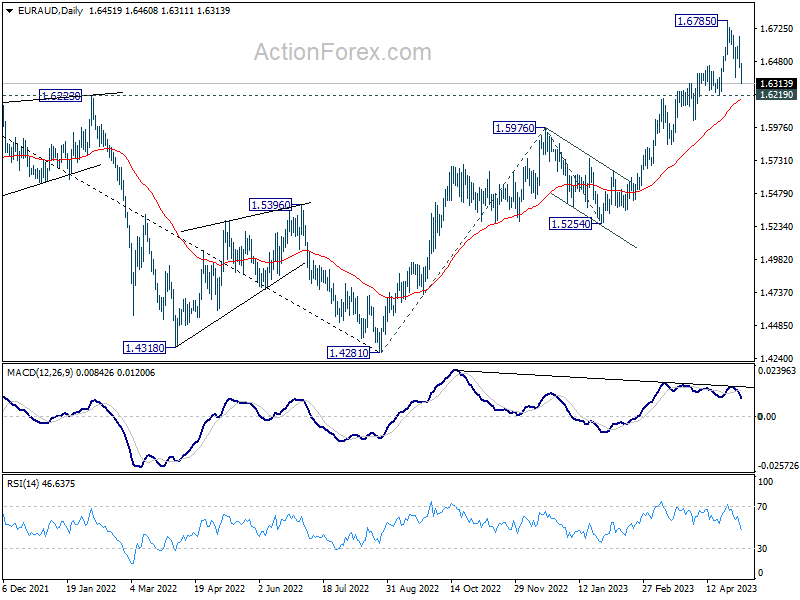

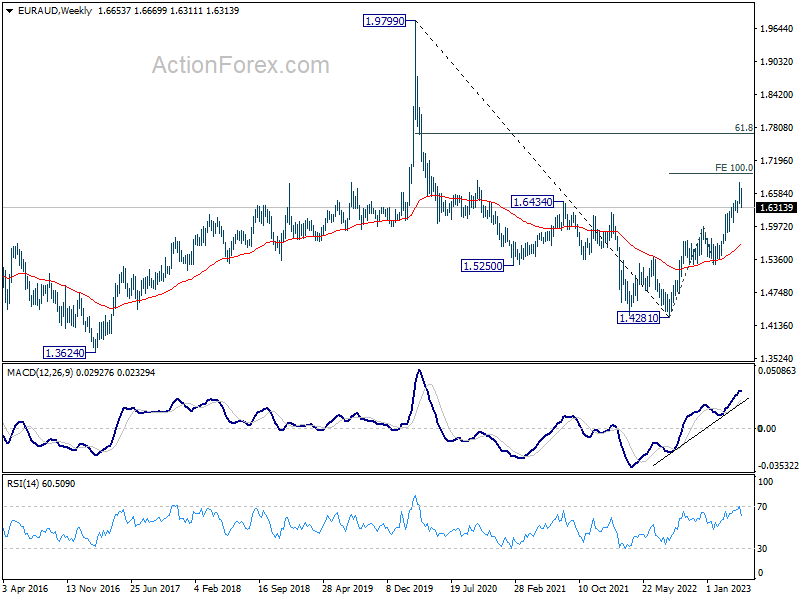

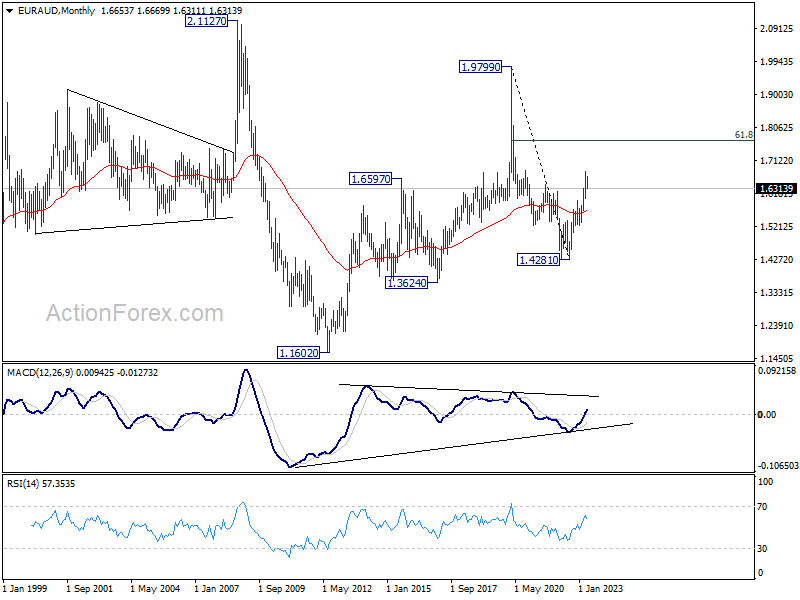

EUR/AUD Weekly Outlook

EUR/AUD's pull back from 1.6785 extended lower last week but stayed above 1.6219 support. Initial bias remains neutral first and further rally is in favor. On the upside, break of 1.6785 will resume larger up trend to 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949. However, considering bearish divergence condition in D MACD, decisive break of 1.6219 will argue that it's already in correction to whole up trend from 1.4281. Deeper decline would then be seen towards 1.5254/5976 support zone instead.

In the bigger picture, whole down trend from 1.9799 (2020 high) should have completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement of 1.9799 to 1.4281 at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). Attention will be paid on the structure on the current rally to make an assessment later.

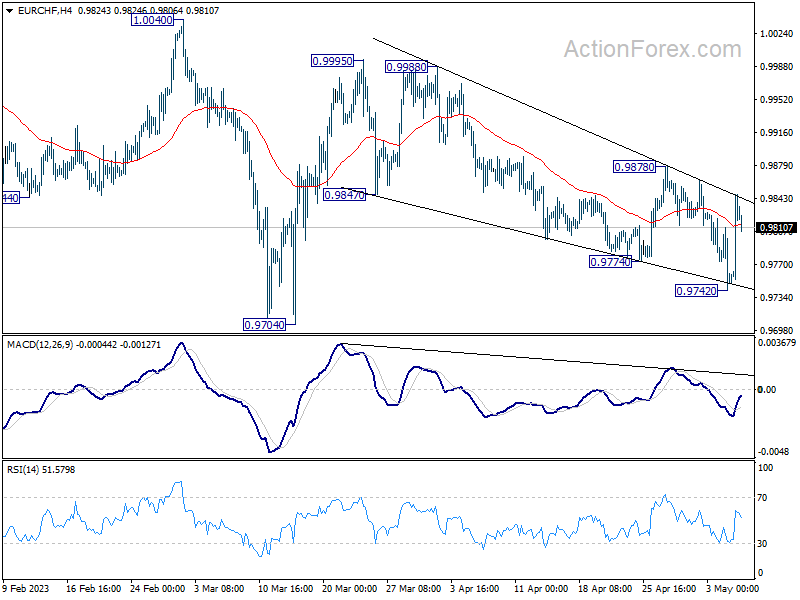

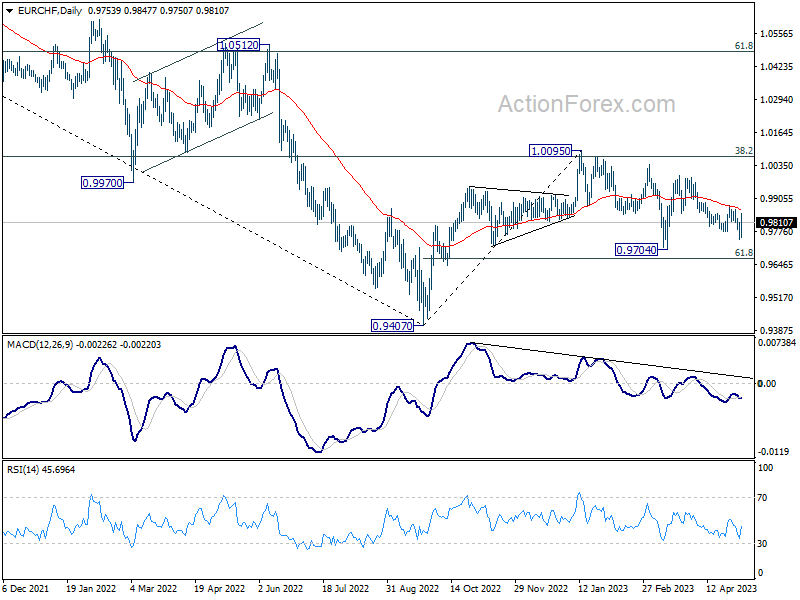

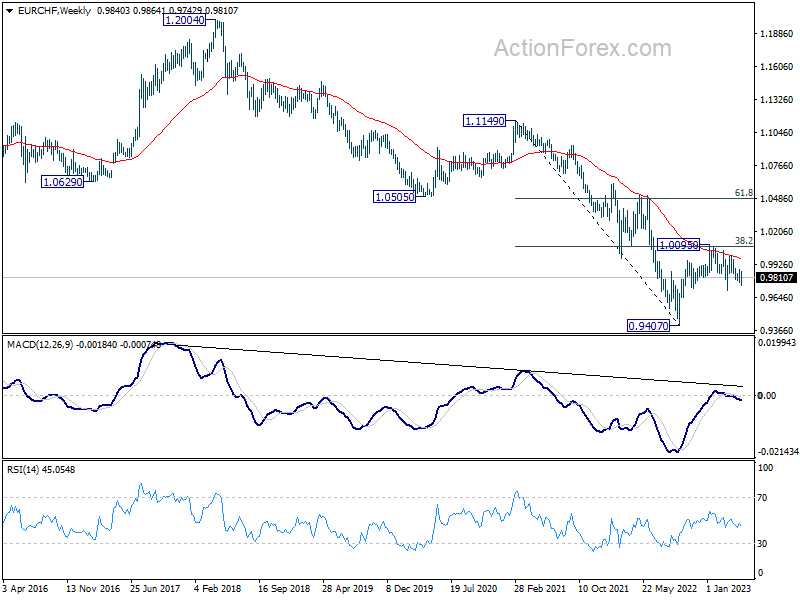

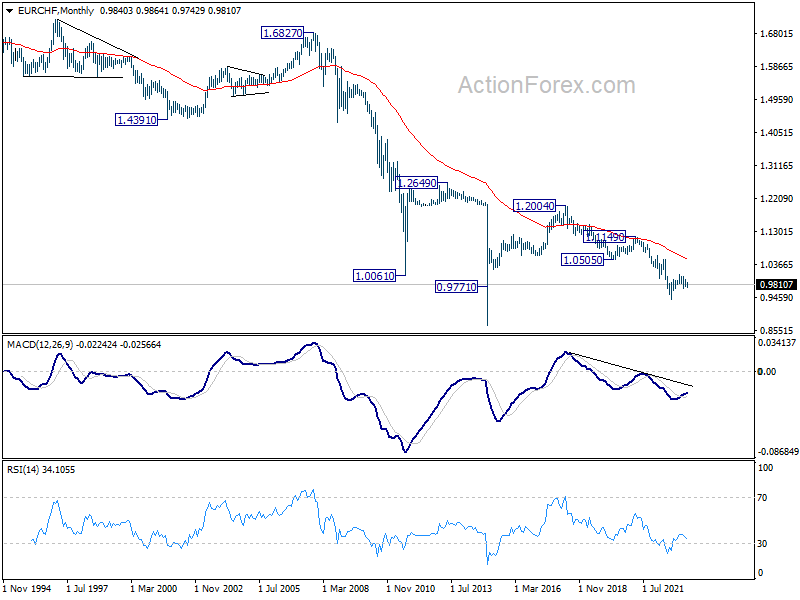

EUR/CHF Weekly Outlook

EUR/CHF extended the decline from 0.9995 last week but quickly rebounded. Initial bias remains neutral this week first and outlook is unchanged. That is fall from 0.9995 is a correction to rise from 0.9704 only. Break of 0.9878 resistance will indicate that such correction has completed and target 0.9995. Firm break there should confirm that larger corrective decline from 1.0095 has completed at 0.9704 too.

In the bigger picture, prior rejection by 55 W EMA (now at 0.9971) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0515) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Summary 5/8 – 5/12

Monday, May 8, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | BoJ Meeting Minutes | ||

| 01:30 | AUD | NAB Business Conditions Apr | 16 | |

| 01:30 | AUD | NAB Business Confidence Apr | -1 | |

| 01:30 | AUD | Building Permits M/M Mar | 3.00% | 4.00% |

| 06:00 | EUR | Germany Industrial Production M/M Mar | -1.60% | 2.00% |

| 08:30 | EUR | Eurozone Sentix Investor Confidence May | -7.9 | -8.7 |

| 14:00 | USD | Wholesale Inventories Mar F | 0.10% | 0.10% |

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | 1.00% | 1.10% |

| 23:30 | JPY | Overall Household Spending Y/Y Mar | 0.40% | 1.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | BoJ Meeting Minutes | |

| Forecast: | Previous: | ||

| 01:30 | AUD | NAB Business Conditions Apr | |

| Forecast: | Previous: 16 | ||

| 01:30 | AUD | NAB Business Confidence Apr | |

| Forecast: | Previous: -1 | ||

| 01:30 | AUD | Building Permits M/M Mar | |

| Forecast: 3.00% | Previous: 4.00% | ||

| 06:00 | EUR | Germany Industrial Production M/M Mar | |

| Forecast: -1.60% | Previous: 2.00% | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence May | |

| Forecast: -7.9 | Previous: -8.7 | ||

| 14:00 | USD | Wholesale Inventories Mar F | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | |

| Forecast: 1.00% | Previous: 1.10% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Mar | |

| Forecast: 0.40% | Previous: 1.60% | ||

Tuesday, May 9, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 03:00 | CNY | Trade Balance (USD) Apr | 69.0B | 88.2B |

| 06:45 | EUR | France Trade Balance (EUR) Mar | -9.5B | -9.9B |

| 10:00 | USD | NFIB Business Optimism Index Apr | 89.6 | 90.1 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 03:00 | CNY | Trade Balance (USD) Apr | |

| Forecast: 69.0B | Previous: 88.2B | ||

| 06:45 | EUR | France Trade Balance (EUR) Mar | |

| Forecast: -9.5B | Previous: -9.9B | ||

| 10:00 | USD | NFIB Business Optimism Index Apr | |

| Forecast: 89.6 | Previous: 90.1 | ||

Wednesday, May 10, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Mar P | 97.9% | 98.0% |

| 06:00 | EUR | Germany CPI M/M Apr F | 0.40% | 0.40% |

| 06:00 | EUR | Germany CPI Y/Y Apr F | 7.20% | 7.20% |

| 08:00 | EUR | Italy Industrial Output M/M Mar | 0.20% | -0.20% |

| 12:30 | CAD | Building Permits M/M Mar | 2.30% | 8.60% |

| 12:30 | USD | CPI M/M Apr | 0.40% | 0.10% |

| 12:30 | USD | CPI Y/Y Apr | 5.00% | 5.00% |

| 12:30 | USD | CPI Core M/M Apr | 0.30% | 0.40% |

| 12:30 | USD | CPI Core Y/Y Apr | 5.80% | 5.60% |

| 14:30 | USD | Crude Oil Inventories | -1.3M | |

| 23:01 | GBP | RICS Housing Price Balance Apr | -38% | -43% |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 23:50 | JPY | Bank Lending Y/Y Apr | 2.90% | 3.00% |

| 23:50 | JPY | Current Account (JPY) Mar | 1.32T | 1.09T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Mar P | |

| Forecast: 97.9% | Previous: 98.0% | ||

| 06:00 | EUR | Germany CPI M/M Apr F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 06:00 | EUR | Germany CPI Y/Y Apr F | |

| Forecast: 7.20% | Previous: 7.20% | ||

| 08:00 | EUR | Italy Industrial Output M/M Mar | |

| Forecast: 0.20% | Previous: -0.20% | ||

| 12:30 | CAD | Building Permits M/M Mar | |

| Forecast: 2.30% | Previous: 8.60% | ||

| 12:30 | USD | CPI M/M Apr | |

| Forecast: 0.40% | Previous: 0.10% | ||

| 12:30 | USD | CPI Y/Y Apr | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 12:30 | USD | CPI Core M/M Apr | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | CPI Core Y/Y Apr | |

| Forecast: 5.80% | Previous: 5.60% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -1.3M | ||

| 23:01 | GBP | RICS Housing Price Balance Apr | |

| Forecast: -38% | Previous: -43% | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Bank Lending Y/Y Apr | |

| Forecast: 2.90% | Previous: 3.00% | ||

| 23:50 | JPY | Current Account (JPY) Mar | |

| Forecast: 1.32T | Previous: 1.09T | ||

Thursday, May 11, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations May | 4.60% | |

| 01:30 | CNY | CPI Y/Y Apr | 0.30% | 0.70% |

| 01:30 | CNY | PPI Y/Y Apr | -3.20% | -2.50% |

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 54.1 | 53.3 |

| 11:00 | GBP | BoE Interest Rate Decision | 4.50% | 4.25% |

| 11:00 | GBP | MPC Official Bank Rate Votes | 7--0--2 | 7--0--2 |

| 12:30 | USD | PPI M/M Apr | 0.30% | -0.50% |

| 12:30 | USD | PPI Y/Y Apr | 1.40% | 2.70% |

| 12:30 | USD | PPI Core M/M Apr | 0.30% | -0.10% |

| 12:30 | USD | PPI Core Y/Y Apr | 2.70% | 3.40% |

| 12:30 | USD | Initial Jobless Claims (May 5) | 245K | 242K |

| 14:30 | USD | Natural Gas Storage | 54B | |

| 22:30 | NZD | Business NZ PMI Apr | 48.1 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | 2.70% | 2.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations May | |

| Forecast: | Previous: 4.60% | ||

| 01:30 | CNY | CPI Y/Y Apr | |

| Forecast: 0.30% | Previous: 0.70% | ||

| 01:30 | CNY | PPI Y/Y Apr | |

| Forecast: -3.20% | Previous: -2.50% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Apr | |

| Forecast: 54.1 | Previous: 53.3 | ||

| 11:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.25% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 7--0--2 | Previous: 7--0--2 | ||

| 12:30 | USD | PPI M/M Apr | |

| Forecast: 0.30% | Previous: -0.50% | ||

| 12:30 | USD | PPI Y/Y Apr | |

| Forecast: 1.40% | Previous: 2.70% | ||

| 12:30 | USD | PPI Core M/M Apr | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 12:30 | USD | PPI Core Y/Y Apr | |

| Forecast: 2.70% | Previous: 3.40% | ||

| 12:30 | USD | Initial Jobless Claims (May 5) | |

| Forecast: 245K | Previous: 242K | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 54B | ||

| 22:30 | NZD | Business NZ PMI Apr | |

| Forecast: | Previous: 48.1 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | |

| Forecast: 2.70% | Previous: 2.60% | ||

Friday, May 12, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | 3.30% | |

| 06:00 | GBP | GDP Q/Q Q1 P | 0.10% | 0.10% |

| 06:00 | GBP | GDP M/M Mar | 0.00% | 0.00% |

| 06:00 | GBP | Industrial Production M/M Mar | -0.10% | -0.20% |

| 06:00 | GBP | Industrial Production Y/Y Mar | -3.70% | -3.10% |

| 06:00 | GBP | Manufacturing Production M/M Mar | -0.10% | 0.00% |

| 06:00 | GBP | Manufacturing Production Y/Y Mar | -3.80% | -2.40% |

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | -17.5B | -17.5B |

| 12:30 | USD | Import Price Index M/M Apr | 0.30% | -0.60% |

| 14:00 | USD | Michigan Consumer Sentiment Index May P | 63.00 | 63.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | |

| Forecast: | Previous: 3.30% | ||

| 06:00 | GBP | GDP Q/Q Q1 P | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 06:00 | GBP | GDP M/M Mar | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 06:00 | GBP | Industrial Production M/M Mar | |

| Forecast: -0.10% | Previous: -0.20% | ||

| 06:00 | GBP | Industrial Production Y/Y Mar | |

| Forecast: -3.70% | Previous: -3.10% | ||

| 06:00 | GBP | Manufacturing Production M/M Mar | |

| Forecast: -0.10% | Previous: 0.00% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Mar | |

| Forecast: -3.80% | Previous: -2.40% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | |

| Forecast: -17.5B | Previous: -17.5B | ||

| 12:30 | USD | Import Price Index M/M Apr | |

| Forecast: 0.30% | Previous: -0.60% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index May P | |

| Forecast: 63.00 | Previous: 63.5 | ||

Weekly Economic & Financial Commentary: Global Central Banks Still Active

Summary

United States: Rock Solid Labor Market Keeps the Fed in a Hard Place

- In April, employers added 253K jobs and the unemployment rate fell to 3.4%. During the same month, the ISM services index edged up to 51.9, while the ISM manufacturing index improved to 47.1. In March, the count of job openings declined to 9.6 million, while construction spending rose 0.3%. Nonfarm productivity declined 2.7% in Q1 as unit labor costs jumped 6.3%.

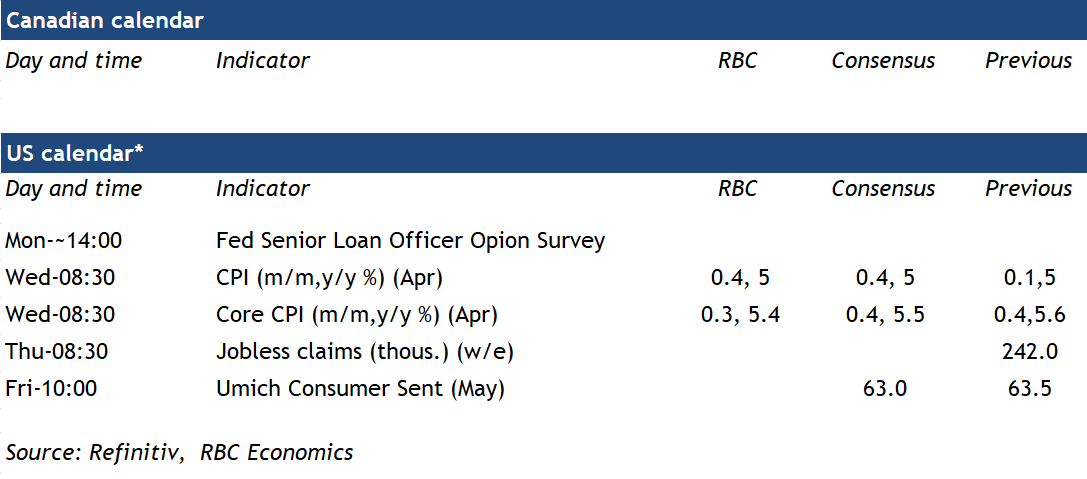

- Next week: NFIB (Tue), CPI (Wed), Consumer Sentiment (Fri)

International: Global Central Banks Still Active

- In addition to the Fed's rate hike, several international central banks were active this week. The European Central Bank raised its policy rate 25 bps to 3.25%, and signaled further tightening to come. Norway's central bank also raised its policy rate 25 bps to 3.25% and indicated rates would be raised further, while the Reserve Bank of Australia surprised market participants with a 25 bps rate increase to 3.85%.

- Next week: Mexico CPI (Tue), Bank of England Policy Decision (Thu), U.K. GDP (Fri)

Interest Rate Watch: The Fed Hikes Again

- As widely expected, the FOMC elected to raise its target range for the federal funds rate by 25 bps on Wednesday to 5.00%–5.25%. This may very well be the last hike of the current tightening cycle. The FOMC did not pre-commit to another rate hike on June 14, and the next action will depend on how the economy evolves from here.

Topic of the Week: The Looming Debt Ceiling X Date Draws Closer

- On Monday, Treasury Secretary Janet Yellen gave guidance that the Treasury could be unable to meet all of the government's obligations as soon as early June due to the debt ceiling constraint. The Treasury bill market suggests investors have taken notice of the political standoff over the nation's debt ceiling.

The Weekly Bottom Line: Fed Lifts Policy Rate to a 16-year High

U.S. Highlights

- The Federal Reserve hiked the policy rate 25 basis points this week, lifting it to a 16-year high of 5.00-5.25%. Changes in FOMC statement hinted at the potential for a pause, though Chair Powell stated that such a decision had not been made.

- The banking stress continues to fester, with this week marking the failure of another bank (First Republic).

- Though still slowing on a trend basis, hiring ticked up in April, with the economy adding 253k jobs. That was above market expectations for a gain of 180k, but downward revisions to the prior months tempered the optimism.

Canadian Highlights

- Oil prices slid this week on growth concerns, pressuring equities lower. However, we think that oil prices will ultimately rise as the year wears on.

- This week’s data flow skewed positive, highlighted by a jobs report where headline employment growth was healthy. However, job markets didn’t tighten further, as labour force growth was also robust.

- The jobs report reinforced our view that the Bank of Canada will likely keep interest rates unchanged this year, as it showed that healthy job gains can manifest without materially tighter conditions.

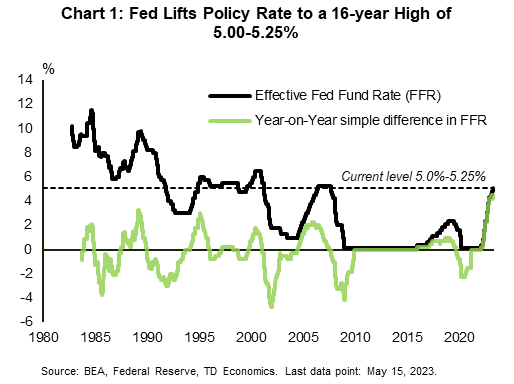

U.S. - Fed Lifts Policy Rate to a 16-year High

The Fed followed through with its highly anticipated decision to hike the policy rate by 25 basis points (bps) this week. This lifted the fed funds rate to 5.00-5.25% – the highest level in 16 years – in what has been a historically aggressive hiking cycle (Chart 1). Changes in the FOMC statement hinted at the potential for a pause, so this could very well be the last hike of this cycle. But, stating this explicitly would not serve the Fed well at this point. In the press conference, Chair Powell tried to keep his options open, stating bluntly that a decision on a pause had not been made.

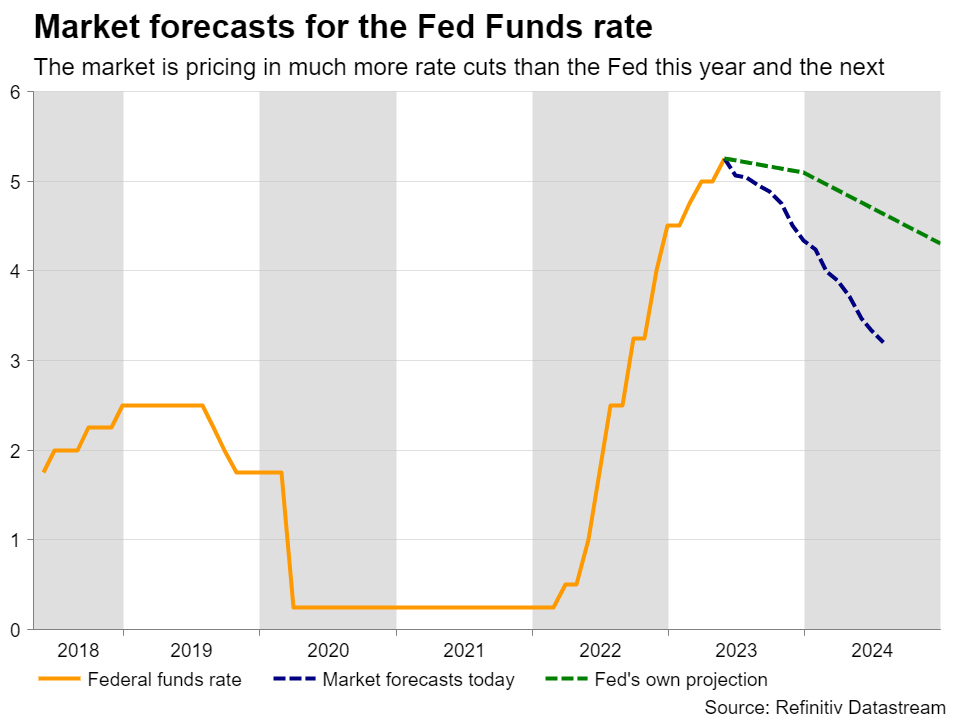

The Fed’s communication is at odds with market expectations. Markets are dismissing the possibility of further rate hikes and are instead signaling that after a brief pause the Fed will begin cutting rates. Market odds as tracked by the CME Group point to 75 bps in cuts over the last few months of the year. Asked about this divergence, Powell pushed back against the notion of soon-to-come cuts. In his words, the reasoning is that the Fed sees inflation coming down “not so quickly”, and that if that outlook proves to be broadly correct then “it would not be appropriate to cut rates”.

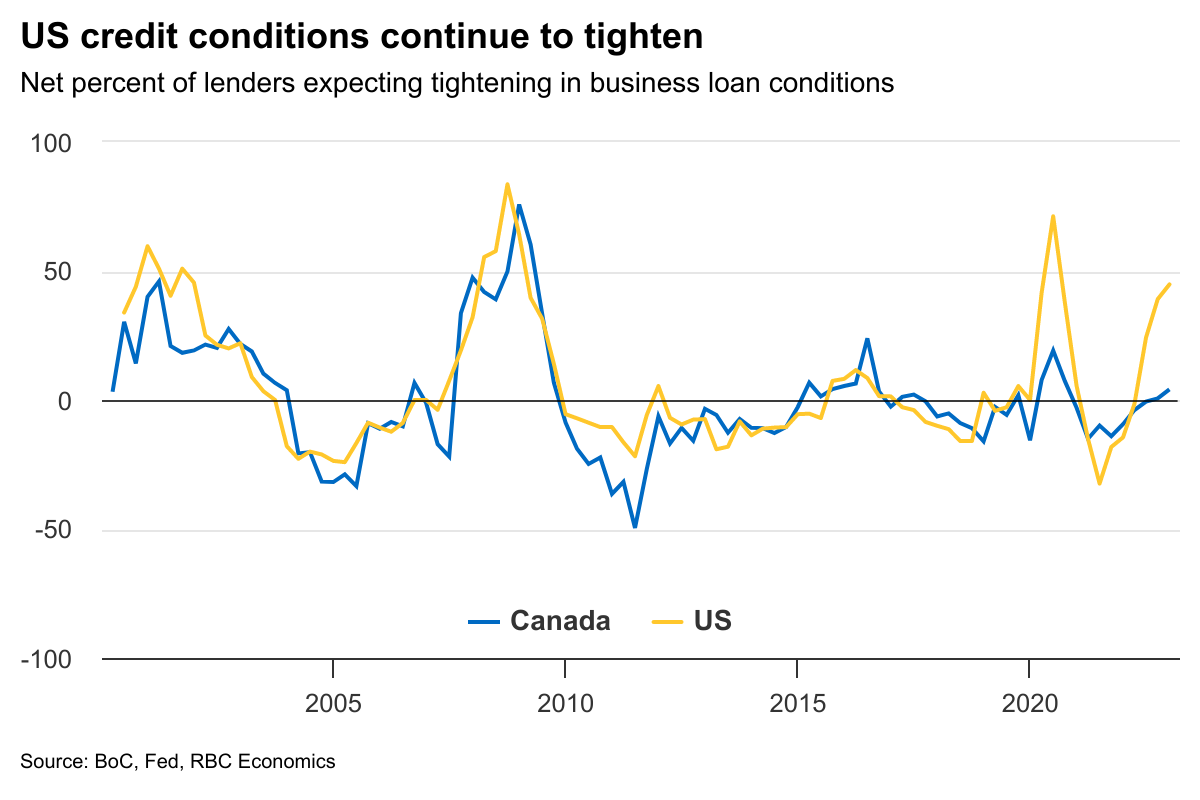

Fed Chair Powell noted that upcoming policy rate decisions would ultimately be data-dependent, mentioning the usual suspects (i.e., inflation and labor market metrics), while also putting a focus on credit conditions. Tighter credit conditions ultimately serve a similar purpose to rate hikes when it comes to cooling economic growth and inflation. This is something that the Fed considers in setting monetary policy, especially in light of the recent banking stress, with this week marking the failure of another regional bank. Powell had access to the Senior Loan Officer Opinion Survey (SLOOS), due to be released publicly on Monday, and noted that it would show a tightening in credit conditions among small and medium sized banks.

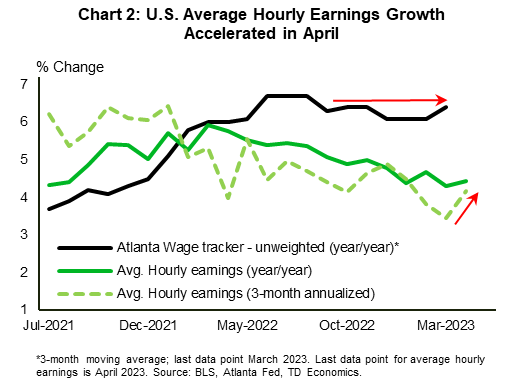

Factoring in the banking stress and tighter credit conditions suggests that the Fed has done enough, but labor market resilience continues. On the one hand, the pace of job creation continues to trend down on a three-month moving average basis. On the other hand, it’s hard to discount the strength in the April jobs report. The economy added 253k jobs last month – well above expectations for 180k. Gains were concentrated in service sectors (+197k). The labor force participation rate held flat at post-pandemic high of 62.6%, while the unemployment rate ticked down to 3.4%, matching January’s multi-decade low. Amidst the ongoing tightness in the labor market, growth in average hourly earnings accelerated both on a year-on-year and month-on-month basis, while other wage measures also point to some resilience (Chart 2).

Should the strength seen in April extend in the months ahead, it could push the Fed to hike a bit more. However, other labor market indicators – such as job openings, which are trending down, and initial jobless claims, which continue to trend up – are not in tune with this view. All told, the upcoming data will continue to bear careful watching, with next week’s CPI report next under the magnifying glass.

Canada – Canada's Goldilocks Jobs Market

In a week that was chock full of U.S. developments, Canadian markets largely took their cues from south of the border. Pessimism reigned for much of the week, as investors fretted over the economic outlook, on-going turmoil in the U.S. banking sector, and unsettling news that the so-called "x-date" on the U.S. debt ceiling could be fast approaching. At one point, the Canadian 10-year bond yield had fallen about 30 bps from its Monday high. However, much of this gloom was undone at the end of the week by a pair of solid job reports in the U.S. and Canada. This shift in sentiment wasn't enough to pull WTI higher, as it slid about 7% this week (as of writing). However, we see it rising through the rest of the year, supported by Chinese economic growth.

As for the Canadian economic outlook, this week's data reinforced the narrative that near-term resilience is in the cards, despite some indications that activity could be easing. On the negative side, the Canadian manufacturing PMI indicated only modest growth in April, and forward-looking indicators were soft. In addition, import volumes fell again in March, suggesting flagging domestic demand.

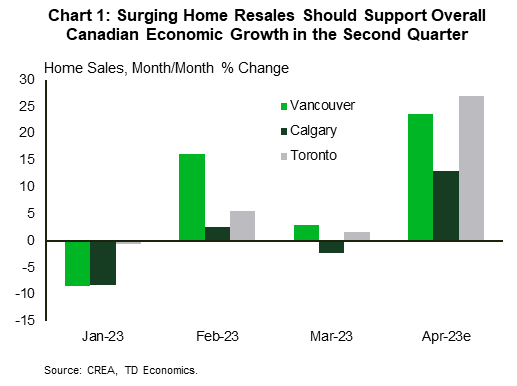

On the other hand, housing data from local boards released during the week pointed to surging home sales in April (Chart 1). This result was supported by lower interest rates, solid job markets and the jolt to buyer psychology sent from a central bank that's currently on pause. Furthermore, the rapid run up in interest rates had pushed sales to levels far below any reasonable long-run trend – given fundamentals (like household income) – and so some recovery to trend is likely to continue.

However, what's most germane for the outlook is the fact that Canada's jobs market continues to be firm. This morning's employment report showed that 41k net new positions were added last month and that solid growth was recorded in highly cyclical industries. Hours worked even managed to climb 0.2% m/m, despite job gains being driven by part-time work. It also helped that the federal worker's strike fell outside of the survey week. Notably, the strike ended this week and while it should weigh on GDP growth in April, a bounce back in May will likely follow.

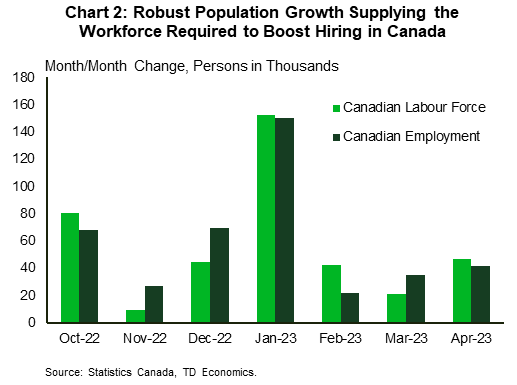

Strikingly, what would have been considered a very robust headline employment in the past didn't flow through to a materially tighter job market. Indeed, the unemployment rate was unchanged and wage growth (while remaining robust) decelerated slightly during the month. This speaks to yet another solid gain in Canada's labour force (Chart 2) which, in turn, is being driven by robust population growth.

In terms of the outlook for interest rates, the jobs report makes us more confident in our view that the Bank of Canada will keep its policy rate unchanged this year. On the one hand, the positive indications for growth flowing from the report argue against the notion of rate cuts. On the other, the fact that healthy job growth didn't result in a tighter labour market likely discourages any lean towards tighter policy.

U.S. Inflation Continues to Slow as Credit Risks Build

Next week’s April U.S. inflation report is expected to show headline inflation unchanged at 5%, matching the annual rate in March. This would be the first time that the U.S. inflation rate didn’t post a decline since peaking in June 2022. But the underlying details should be more encouraging. A 3% monthly increase in gasoline prices (on a seasonally adjust basis) likely pushed April energy prices up slightly, to -4.5% on a year-over-year basis. But with oil prices running well below year-ago levels, energy prices should continue to lose steam. And though food inflation is still high, it likely slowed again in April. We expect this measure to slip to ~8% from a year ago.

Outside of food and energy products, “core” CPI growth also likely slowed. We expect this measure to fall to 5.4% from 5.6% in March on a year-over-year basis or increase 0.3% from March. That would mark the smallest month-over-month increase since November. Higher rent prices have been driving the majority of core price growth in recent months, as earlier hikes feed through to the consumer price index. But that surge has probably run its course. Measures of current market rent inflation peaked more than a year ago.

Inflation is still a concern for Federal Reserve officials, and U.S. price pressures, while easing, have been sticky. But there is a growing list of signs that economic momentum is slowing under the surface and higher interest rates are cutting into household purchasing power. Employment is still rising, but job openings are down. Lower quit rates and slowing wage growth suggest workers aren’t as confident in labour markets as they once were. And credit markets have tightened as the list of U.S. regional banks struggling to calm investor worries continues to grow. The Senior Loan Officer Opinion Survey—on tap next week—should provide an update on lending practices in the U.S., where tighter standards and weaker demand for commercial and industrial (C&I) and consumer loans are expected to have continued.

Week ahead data watch

Week Ahead – US CPI Data Eyed While BoE Seeks to Get Inflation Back Below 10%

US

The labor market is showing signs of resilience, but now the focus shifts back to inflation, with a close eye staying on the banking space. The banking system does not look ‘sound and resilient’ as more banks come under stress. US regulators will eventually be forced to act as the banking crisis worsens and that could mean the further unwinding of more banks.

The April inflation report is expected to show that the disinflation process is starting to lose momentum, which could delay some Fed rate cut bets. Headline inflation is expected to remain stuck at 5.0%, which is the slowest pace in almost 2 years. The month-over-month reading is expected to rise from 0.1% to 0.4%. Core inflation might only slow a bit, but that should start to fall more quickly in the coming months as the housing lag will better reflect softening rent and home prices.

President Biden will also meet with four top congressional leaders on May 9th to discuss the budget which will definitely impact debt ceiling negotiations.

Peak earnings are behind us but we still get some important results. Corporate updates for the week: Bayer, Credit Agricole, Devon Energy, Duke Energy, Engie, Honda Motor, PayPal Holdings, Saudi Arabian Oil, SoftBank, Toyota Motor, Walt Disney, and Westpac Banking.

Eurozone

It’s all looking a bit quiet for the euro area next week with the few data releases we do have being tier three and therefore not particularly impactful. The ECB slowed its tightening cycle in May but further hikes are likely over the next few meetings with markets pricing in another one or two before the end of the year.

UK

The Bank of England may be convinced that inflation is about to fall sharply but I doubt it will be brave enough to pause the tightening cycle while inflation is still above 10%. A 25 basis point hike is priced in for Thursday, after which markets expect one more to follow before then easing next year. GDP data then follows on Friday and is expected to show the economy growing marginally again which is probably the best we can hope for over the coming quarters.

Russia

Inflation data will be in focus next week as the CBR looks for evidence of price pressures easing on a sustainable basis which will allow for further rate cuts in the future. But it is being cautious and has signaled that rate cuts are neither guaranteed or even necessarily on the horizon. The CBR releases its monetary policy report on Thursday which may shed further light on the path for interest rates.

South Africa

There are a few notable economic releases next week but mostly tier-two or three data. Manufacturing production on Thursday is one standout, while business confidence on Wednesday could also be of interest.

Turkey

There’s just over a week to go until the election so there may not be a huge amount of interest in what the economic data has to say, despite there being some interesting releases. Ultimately, the outcome of the election is what will dictate future interest rate moves and the path of travel for the economy, not whether unemployment can fall below 10%. Can President Erdogan cling to power after such a turbulent few years?

Switzerland

There are no noteworthy events over the next week.

China

Consensus estimates expect the balance of trade for April, released on Tuesday to show a decline to US$74.3 billion from $88.19 billion in March with exports growth decline to 8% year-on-year in April from 14.8% printed in March while zero growth in imports growth after it contracted by -1.4% year-on-year in March, its 6th consecutive month of negative growth.

Credit growth data will be on the radar where new yuan loans are expected to decline to CNY 3.10 trillion in April from CNY 3.89 trillion in March, a slight dip in outstanding loan growth is being forecasted at 11.6% year-on-year in April from the 11.8% in March, its fastest pace of increase since October 2021. In addition, the M2 money supply is expected to dip slightly as well to 12.6% year-on-year in April from 12.7% in March.

Next up on Thursday, key inflation data is the focus where the consumer inflation rate for April is expected to come in at a slight increase to 0.9% year-on-year from 0.7% in March, its lowest reading since September 2021. Meanwhile, the slump in producer prices is expected to slow down slightly to -2.1% year-on-year in April from -2.5% in March, its 6th consecutive month of production deflation and steepest contraction since June 2020. If such forecasts turn out as expected, inflationary pressures in China are way below an average gauge of inflation rate among emerging and developed countries which suggests that China’s central bank, the PBoC, has more leeway to conduct accommodating monetary policy.

India

The key data to focus will be on industrial production and CPI out on Friday. Growth in industrial production is forecasted to shrink to 3.2% year-on-year in March from 5.6% in February.

Meanwhile, consumer price inflation for April is expected to ease further to 5.50% year-on-year from 5.66% in March, its lowest since December 2021; below RBI’s upper tolerance limit of 6%.

Australia

On Monday, data on building permit growth for March is forecast to show a decline to 2.6% month-on-month from 4.0% in February.

The Westpac Consumer Confidence Index for May out on Tuesday is forecasted to decline to 82.1 (-4.3% month-on-month) from 85.8 in April.

New Zealand

The key data to focus on will be food inflation for April out on Thursday where it is expected to ease to 11.4% year-on-year after the biggest increase of 12.1% in March since September 1989.

To round up the week, the manufacturing PMI for April out on Friday is forecasted to decelerate further to 47.0 from 48.1 in March.

Japan

A couple of key releases to take note of; household spending for March out on Tuesday where it is expected to show a slowdown in growth to 0.4% year-on-year from 1.6% in February while expanding 1.5% month-on-month in March from a contraction of -2.4% printed in February.

On Thursday, market participants will be able to have some clues on the thinking of BoJ officials via the release of its Summary of Opinions from the most recent April monetary policy meeting where it maintained its dovish stance despite upgrading its inflation forecasts for FY 2023 and 2024.

Lastly, the current account surplus for March is forecasted to expand to JPY 2,947.3 billion from JPY 2,197.2 billion, and growth in bank lending is expected to be almost unchanged at 2.9% year-on-year in April versus 3% in March.

Singapore

No key data.

Economic Calendar

Saturday, May 6

Economic Events

- German Chancellor Scholz is in Kenya

- Taliban’s top diplomat, Amir Khan Muttaqi to discuss extending Belt and Road initiative in Afghanistan with Chinese counterpart Qin Gang in Pakistan

Sunday, May 7

Economic Data/Events

- China data expected this week includes forex reserves, Money Supply, Trade Balance, New yuan loans, Aggregate financing

- Japan PM Kishida to visit South Korea

Monday, May 8

Economic Data/Events

- US wholesale inventories

- Australia building approvals

- Chile copper exports, CPI, trade

- Germany industrial production

- Taiwan trade

- UK bank holiday honoring coronation of Charles III

- Meeting on Indo-Pacific trade pact in Singapore

- ECB Chief Economist Lane speaks at Forum New Economy conference in Berlin

- Riksbank Deputy Governor Floden speaks on competition and inflation

Tuesday, May 9

Economic Data/Events

- Australia consumer confidence

- China aggregate financing, trade, money supply, new yuan loans

- France trade

- Japan household spending

- Mexico international reserves, CPI

- President Joe Biden to meet with congressional leaders on the debt limit.

- Victory Day in Russia as war rages in Ukraine

- French finance minister Le Maire, Bank of France Governor Villeroy, ESMA director Cazenave, and EU climate chief Frans Timmermans speak at Bloomberg Future of Finance Conference in Paris

- ECB Governing Council member Rehn speaks at the Bank of Finland event on digital euro

- ECB Chief Economist Lane participates in a panel at the IMF event ‘Europe’s Balancing Act: Taming inflation without a recession’

- Riksbank issues minutes of April monetary policy meeting

- Riksbank Deputy Governor Floden speaks on monetary policy

Wednesday, May 10

Economic Data/Events

- US Apr CPI M/M: 0.4%e v 0.1% prior; Y/Y: 5.0%e v 5.0% prior; CPI ex Food & Energy M/M: 0.3%e v 0.4% prior; Y/Y: 5.4%e v 5.6% prior

- Poland rate decision: Expected to keep the base rate steady at 6.75%

- Germany CPI

- Italy industrial production

- New Zealand home sales

- Poland rate decision

- South Korea jobless rate

- Hungary CPI

- Turkey industrial production

- NATO defense chiefs meet in Brussels

- Italy’s Istat monthly economic note

- Sweden Riksbank Deputy Governor Bunge speaks on economic development

- ECB Governing Council member Centeno makes closing remarks at a conference in Lisbon on “Digital Financial Literacy: a Strategy for Portugal”

Thursday, May 11

Economic Data/Events

- US PPI, initial jobless claims

- BOE rate decision: Expected to raise rates by 25bps to 4.50%

- China PPI, CPI

- New Zealand food prices

- Peru rate decision

- Philippines GDP

- South Africa manufacturing production

- Turkey current account

- UK industrial production, GDP

- G7 Finance minister and central bank governors meet in Japan

- BOJ releases Summary of Opinions from April monetary policy meeting

- Sweden Riksbank’s Floden speaks on monetary policy

- German Finance Minister Lindner begins a five-day trip to Japan and China

Friday, May 12

Economic Data/Events

- US University of Michigan consumer sentiment and inflation expectations

- France CPI

- India industrial production, CPI

- Japan M2 money stock

- Mexico industrial production

- New Zealand PMI

- Norway GDP

- Russia CPI

- Spain CPI

- Fed’s Jefferson and Bullard participate in a panel discussion on monetary policy at Stanford University

- EU foreign ministers meet in Stockholm

- President Biden hosts Spanish Prime Minister Sánchez at the White House

- Sweden Riksbank Deputy Governor Jansson speaks

- Bank of England Chief Economist Pill speaks

- Bank of Canada issues Senior Loan Officer Survey

Sovereign Rating Updates

- Denmark (Fitch)

- Italy (Fitch)

- Sweden (Fitch)

- European Union (DBRS)

- Luxembourg (DBRS)

Week Ahead – BoE Takes the Central Bank Torch, US CPI Data Also in Focus

Following the FOMC and ECB decisions last week, the central bank torch will now be passed to the BoE, which will deliver its decision on Thursday. A 25bps hike is mostly priced in, so the spotlight will fall on clues and hints on how officials are planning to move forward. The US CPIs will also attract special attention as investors are trying to figure out whether the Fed will pause or hike once more in June.

Will the BoE hint at more hikes?

At its latest meeting in March, the BoE raised interest rates by 25 basis points, marking the 11th consecutive hike for this Bank. However, officials played down the surprise surge in inflation during February and maintained a careful view regarding their future course of action, saying that further tightening would be required if there is evidence of more persistent price pressures.

Since then, data showed that inflation slowed by less than expected, with the headline year-over-year rate staying fractionally above 10%, which is allowing investors to price in around 60bps worth of additional rate increases until the end of this year. For this gathering, they are assigning a nearly 85% chance for another quarter-point hike, with the remaining 15% pointing to no action.

Therefore, a 25bps hike by itself is unlikely to shake the pound. Any market reaction may come from the statement, the minutes and/or the updated economic projections. Back in February, the Bank projected that CPI inflation would end the first quarter at 9.7% and slow to 3.0% in 12 months. So, revising higher, or even maintaining that same path may allow investors to continue pricing more hikes, even if officials repeat the same cautious guidance.

With the Fed expected to cut rates by around 75bps by the end of the year, the path of least resistance for pound/dollar will likely remain to the upside, even if a reiteration of the prior guidance results in a small setback. What could distort the outlook may be a larger-than-expected slowdown in the first estimate of the UK GDP for Q1, which is scheduled to be released on Friday, alongside the nation’s trade data for March.

Will the US CPI numbers spark speculation for a June hike?

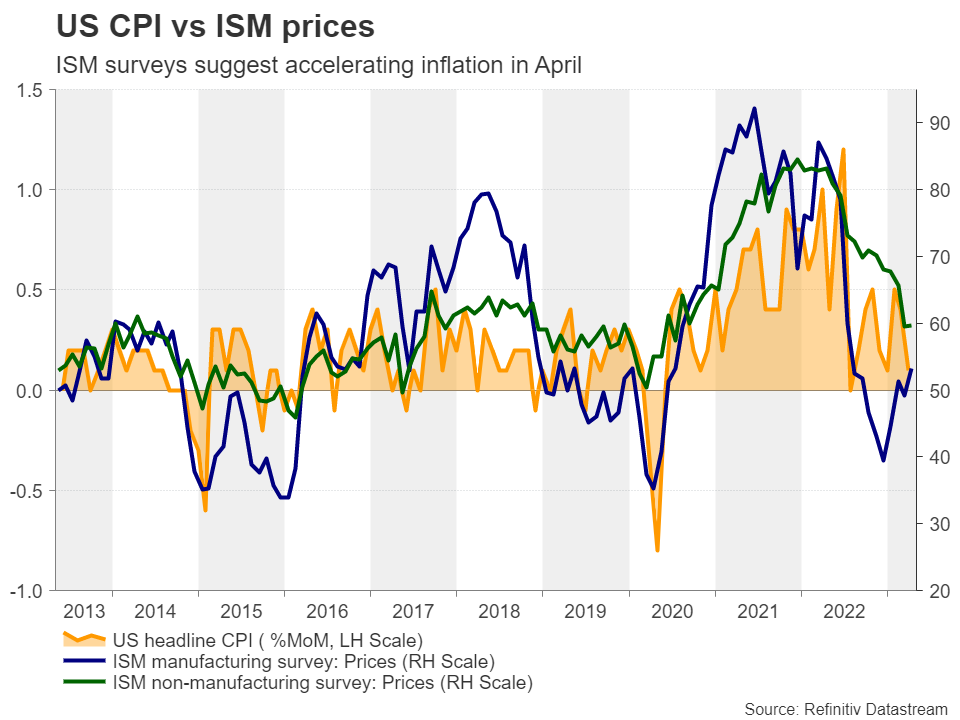

In the US, the highlight will probably be the US CPI numbers for April, due out on Wednesday. The headline rate is forecast to have rebounded to 5.2% y/y from 5.0%, while the core one is expected to have held steady at 5.6% y/y, more or less confirming the ISM and S&P global PMI surveys, which showed that output prices accelerated during the month.

However, such results are unlikely to spark strong speculation about a potential Fed hike in June. After all, the PMI reports were available ahead of Wednesday’s FOMC decision, and yet, even after Powell refused to close the door to a June hike, investors are still pricing in a 90% probability for no action, with the remaining 10% pointing to a quarter-point cut. They are also expecting more than 75bps worth of rate reductions towards the end of the year.

For the pricing to change and start indicating a decent probability for another hike in June, a strong upside surprise may be needed. That could add fuel to the dollar’s engines, but calling for a bullish reversal may still be premature. For a full-scale reversal to start being examined, inflation must continue to accelerate, data may need to reveal that the US economy is in a better shape than many are anticipating, and the Fed might need to prove market expectations wrong, either by raising rates in June or by keeping them untouched through and beyond summer.

China trade data and BoJ Summary of Opinions also on tap

Flying to Asia, China’s trade data, due out on Tuesday, may attract some attention from aussie and kiwi traders, as the world’s second largest economy is the main trading partner of both Australia and New Zealand. Following this week’s disappointing PMIs, weak trade data could corroborate the idea that after the post-reopening boost, the engines of the Chinese economy are now struggling to gather momentum. China’s CPI and PPI numbers are coming out on Thursday.

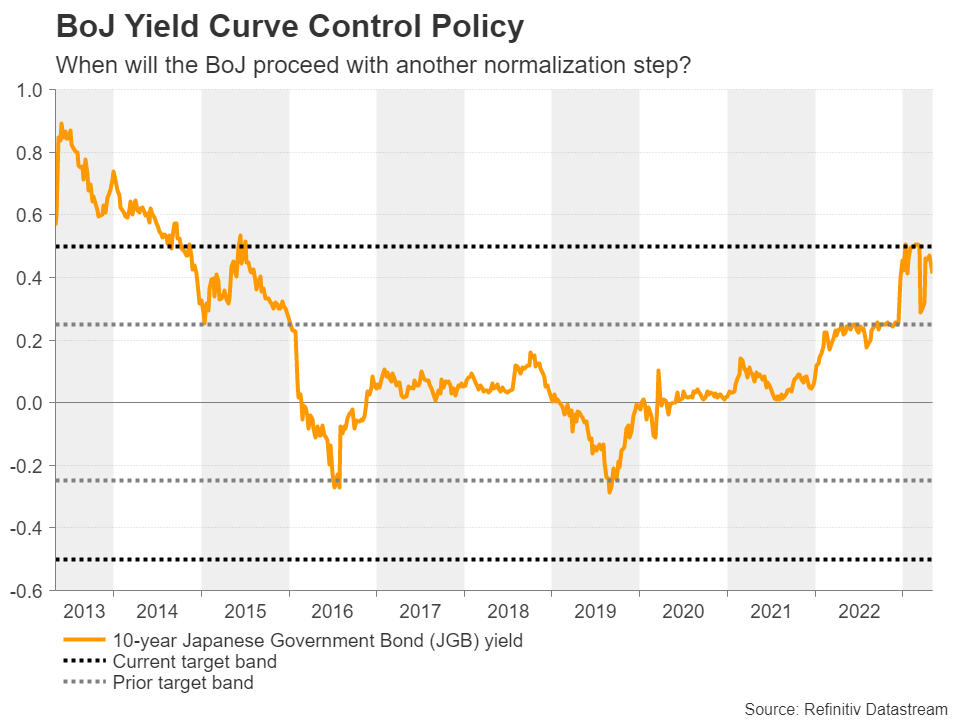

Regarding Japan and the yen, traders could pay some attention to the BoJ’s Summary of Opinions, as this would be the summary concerning the first gathering under Kazuo Ueda’s leadership. At that meeting, officials decided to keep their policy settings unchanged, and although they removed the pledge to keep interest at “current or lower levels”, they decided to conduct a monetary policy review with a planned time frame of around one and a half years.

The yen tumbled at the time of the announcement as the review’s time frame may have raised some speculation that the Bank is unlikely to proceed with any changes during that period. However, with no clear clues on when the Bank may proceed another normalization step, traders may dig into the summary to see whether there is still a chance for that to happen before the end of the year.