Sample Category Title

Japan Inflation: Higher Than Expected But Slowing

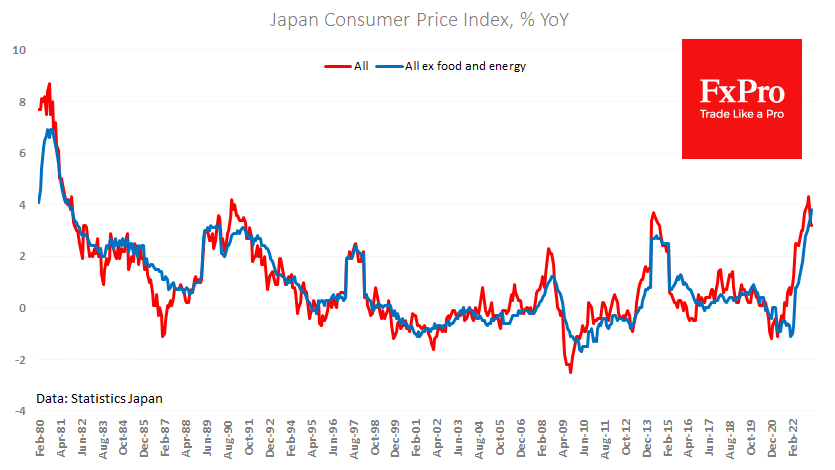

Consumer price inflation in Japan is in no hurry to slow down. In March, prices rose 3.2% y/y, compared with 3.3% in February and an expected 2.6%.

The core price index excludes food and energy but has not yet peaked, reaching 3.8% y/y from 3.5% the previous month. The last time core inflation was this high in Japan was in 1981. Worse, this index has risen by 0.6% in just one month without any visible slowdown, as we see in most developed countries.

However, the situation calls for patience rather than immediate intervention. The Corporate Goods Price index slowed to 7.2% YoY in March, down from 8.3% in February and a peak of 10.6% in December. We will see the Corporate Service Price Index next Tuesday, but the February pace was 1.8%, well within the inflation target.

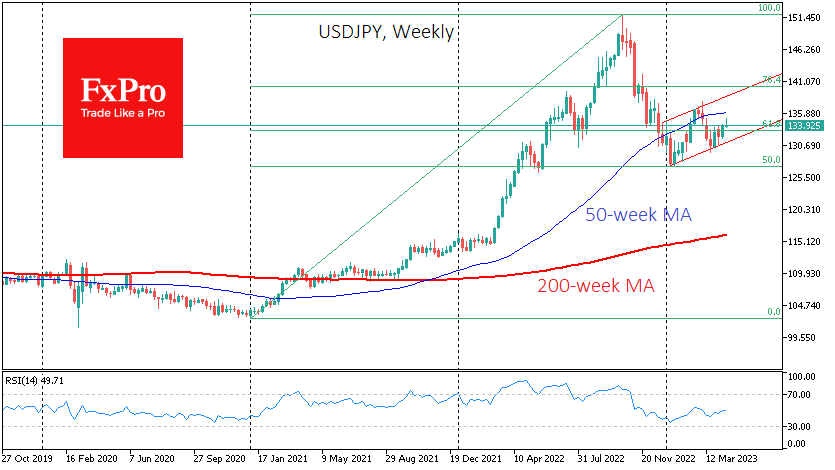

For forex traders, higher-than-expected inflation is often a reason to buy currencies (in our case, sell USDJPY). However, with the overall growth rate in consumer and producer prices have peaked without active intervention from the BoJ, we should not expect the central bank to warm to raising interest rates now.

This interest rate differential between Japan and the rest of the world is working against the Yen.

From October 2022 to January 2023, the USDJPY gave back 50% of its rally from January 2021. Since then, the pair has returned to the upside. And we expect this moderate uptrend to prevail until interest rate cuts begin in the US and Europe.

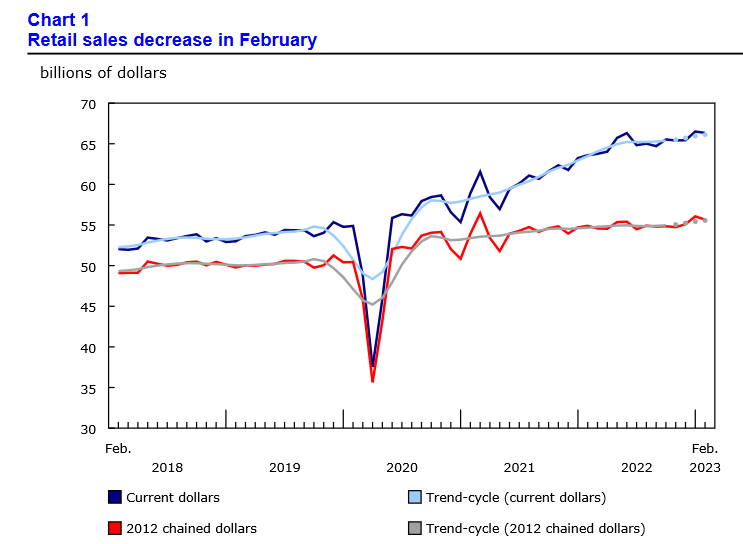

Canada: Retail Sales Post a Moderate Decline in February

Retail sales fell by 0.2% month-on-month (m/m) in February – a shallower decline than 0.6% loss reported by the Statistics Canada's advanced estimate. January's print remained unrevised at a 1.4% gain.

Adjusting for the impact of inflation, the decline in volume of sales was even more pronounced at 0.7% m/m.

The decline in today's headline reading was largely driven by receipts at gasoline stations, which lost 5.0% m/m due to prices at the pump. In volume terms, sales at gasoline stations decreased 4.9% m/m – reversing three months of gains .

Offsetting some of these losses, sales at motor vehicle and parts dealers rose for the seventh month in a row, up 0.9% m/m. That is a step down from a 3.0% gain in January.

Excluding sales of autos and gasoline, core retail sales were 0.1% m/m higher in February.

- The gain in core sales was led by higher sales at clothing & accessories stores (+4.4% m/m), followed by strong performance at health & personal care (+1.1% m/m) and furniture & home furnishings stores (+1.1 % m/m). Sales at electronics and appliance stores (+1.3% m/m) and building material, garden equipment & supplies dealers (+0.2% m/m) were also positive.

- Meanwhile, miscellaneous store retailers (-2.3% m/m), general merchandise retailers (-1.6% m/m), food and beverage stores (-0.2% m/m) and sporting goods, hobby items, musical instruments and books stores (-0.2% m/m) were the biggest underperformers.

- E-commerce sales, which are not included in the headline tally, were up a whopping 7.8% on the month in February.

- Statistics Canada's advanced estimate for March indicates a 1.4% m/m decline. In contrast, our internal card spending data (which excludes auto sales and tilts toward housing-related categories) points to a moderate increase in retail sales.

Key Implications

The decline in retail sales has been expected as the boost from one-time government transfers, such as daycare subsidies and several one-off provincial inflation relief programs, continues to wane. One category that stands out is auto sales, which have been supported by relatively strong pent-up demand. But even here, growth is slowing as higher borrowing costs worsen affordability, especially as mortgage costs continue to creep higher.

Looking one month ahead, Statistics Canada expects a more pronounced decline in retail trade in March. The recent Survey of Consumer Expectations for the first quarter of 2023 suggests that consumers are expecting to spend less on discretionary items. That said, our internal high-frequency data points to a moderate gain in total spending in March and that puts our tracking for consumer spending slightly above 4% (annualized) in Q1 2023.

Sunset Market Commentary

Markets

The EMU composite PMI for April rose from 53.7 to 54.4, indicating that growth momentum in the region improved further at the start of the second quarter. However, growth has become increasingly unbalanced. The headline manufacturing PMI unexpectedly declined from 47.3 to 45.5. The services headline measures improved further from 55 to 56.6. According to S&P global, the outperformance of the services sector relative to manufacturing was the widest since early 2009. Overall orders growth improved, but this also masked a decline in manufacturing being more than counterbalanced by rise in services orders. Employment growth slowed in manufacturing but accelerated to the fastest pace since 2007 for services. Similar narrative for price trends as manufacturing input costs declined while services costs continued to raise sharply. Average prices charged for goods and services continued to rise at a pace above the long-term average. The reaction on European interest rate markets initially was remarkably moderate. European yields swapped a minor decline for a small daily rise. Even so, the ongoing rise in EMU services costs (wages) and final prices for consumers suggests persistent core inflation. The internal debate within the ECB MPC is ongoing with April CPI data and the ECB lending survey to published early May providing key data evidence. That said, we consider the current pricing of a 30% chance of a 50 bps hike rather than a 25 bps a steps being an ‘underpricing’. US bonds outperformed Europe going into the release of the US PMI’s. However, the US manufacturing PMI (50.4 from 49.2) as well as the services gauge (53.7 from 52.6) surprised on the upside. The impact of the ‘financial instability’ in March apparently stays limited for now. US yields after the releases try to erase negative daily prints (2-3-bps higher). German yields still take the lead gaining 4/5 bps. Equities again show no clear trend today. The Eurostoxx 50 trades marginally higher (0.2%). US indices also opened mixed/little changed. The break lower of the oil price slowed after two days of sharp losses (Bent $81.50/b).

On FX markets, EUR/USD after a brief dip early in Europe, currently trades little changed (at 1.096). DXY (101.7) lost a few ticks in a daily perspective. The yen outperformed going into the US PMI but currently rebounds to 134.3.(from 133.6 earlier today). This morning’s softer than expected UK retail sales were the trigger from quite a striking underperformance of sterling. EUR/GBP rallied from the 0.882 area to currently trade near 0.8855. UK PMI’s brought a similar message as was the case in EMU (manufacturing easing from 47.9 to 46.6, services gaining from 52.9 to 54.9). The report initially didn’t change the intraday dynamics.

News & Views

French finance minister Le Maire said the electricity price caps will remain in place beyond 2023, arguing that power prices haven’t normalized yet. The cap will likely be phased out over a two-year period by 2025. Prices soared in the wake of the Russian invasion, as did those for natural gas. But because the latter have lowered significantly in recent months, Le Maire said it will remove gas price caps at the end of 2023. Dutch TTF gas futures today trade below €41/MWh, around the lowest since July 2021.

China’s central bank hinted that it may start to gradually withdraw some of the stimulus measures introduced during the pandemic. Zou Lan, head of the monetary policy department said that most of the structural tools introduced were temporary in nature and will fade out as the economy begins recovering and credit demand picks up. These structural tools include relending programs and target specific areas of the economy. They were increasingly relied on to deliver economic stimulus rather than the blunt conventional measures such as the PBOC’s one-year policy loans and the reserve requirement ratio. The rates of the loans offered by the central bank often carried interest rates at around 1.75%, lower than the one-year policy rate of currently 2.75%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0940; (P) 1.0965; (R1) 1.0996; More...

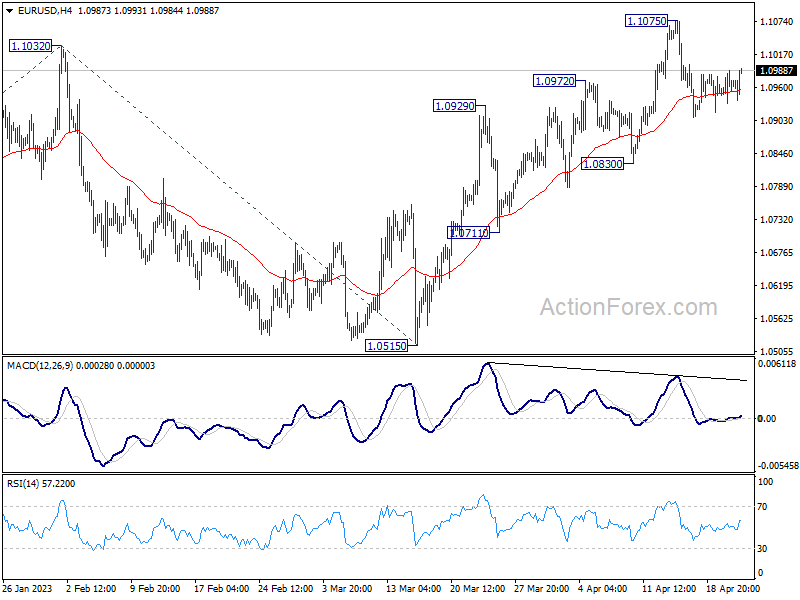

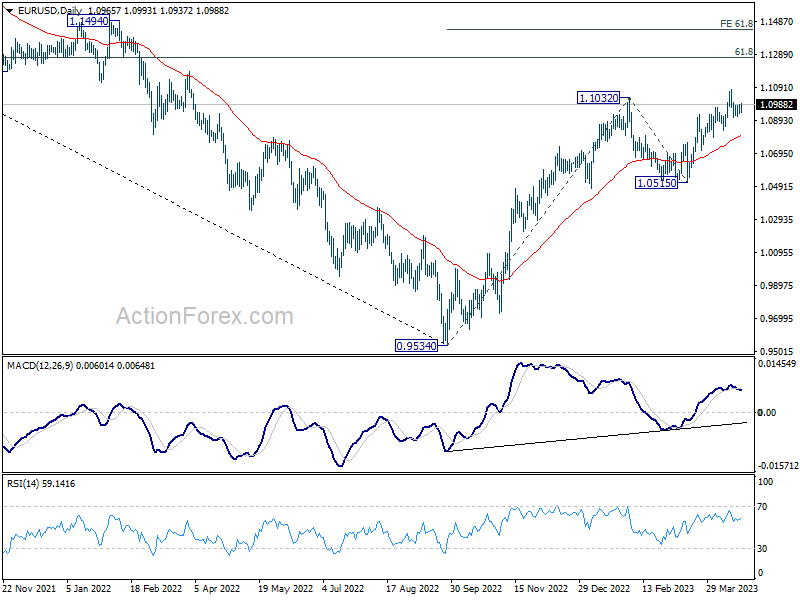

EUR/USD is staying in sideway trading below 1.1075 and intraday bias remains neutral. Outlook remains bullish with 1.0830 support intact. On the upside, break of 1.1075 will will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. However, firm break of 1.0830 will confirm short term topping and bring deeper decline to 1.0711 support instead.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

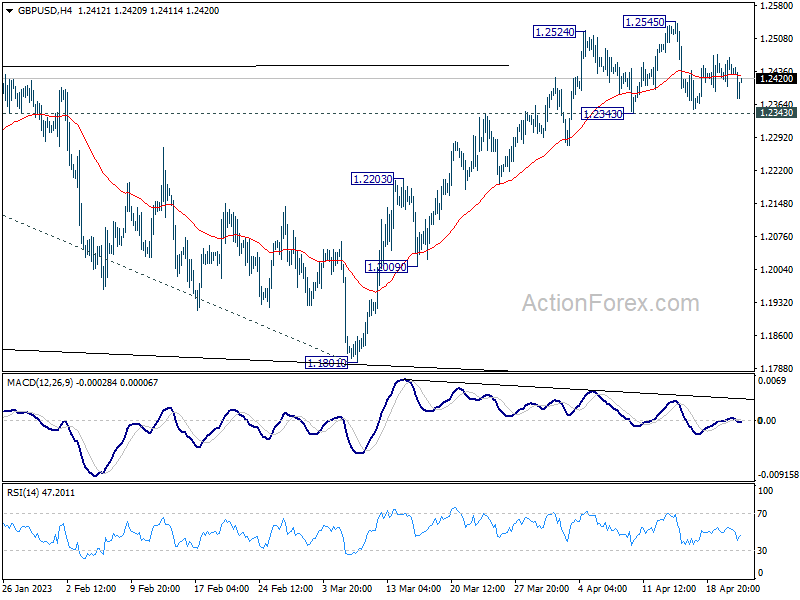

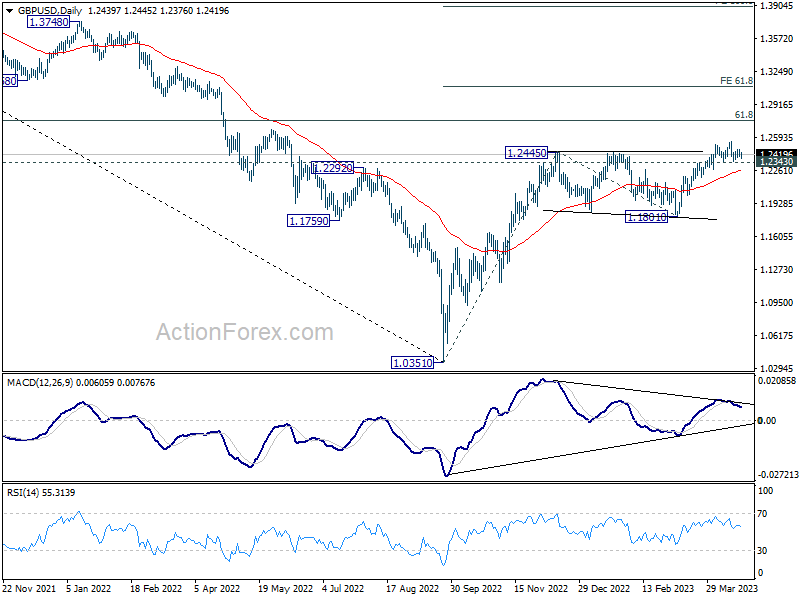

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2409; (P) 1.2439; (R1) 1.2472; More...

Intraday bias in GBP/USD remains neutral as sideway trading continues below 1.2545. Another rise is in favor with 1.2343 support intact. On the upside, above 1.2545 will target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, considering bearish divergence condition in 4H MACD, firm break of 1.2343 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

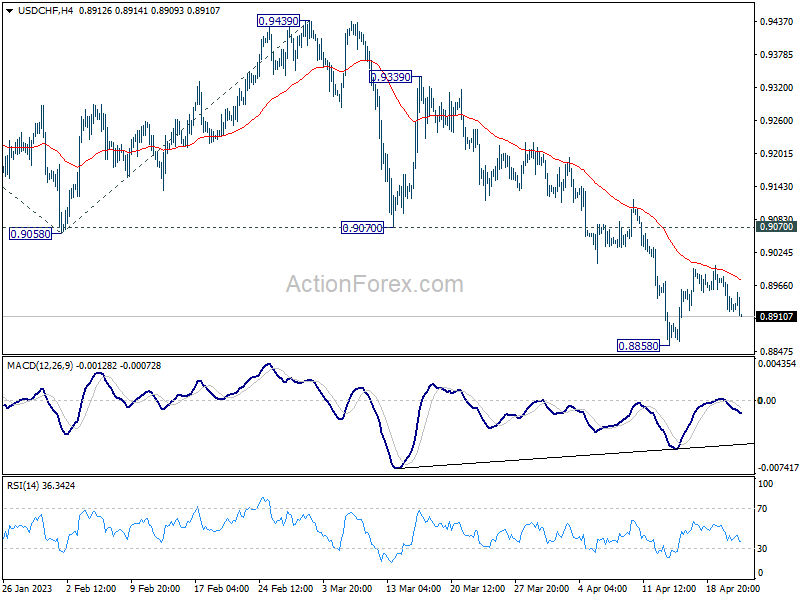

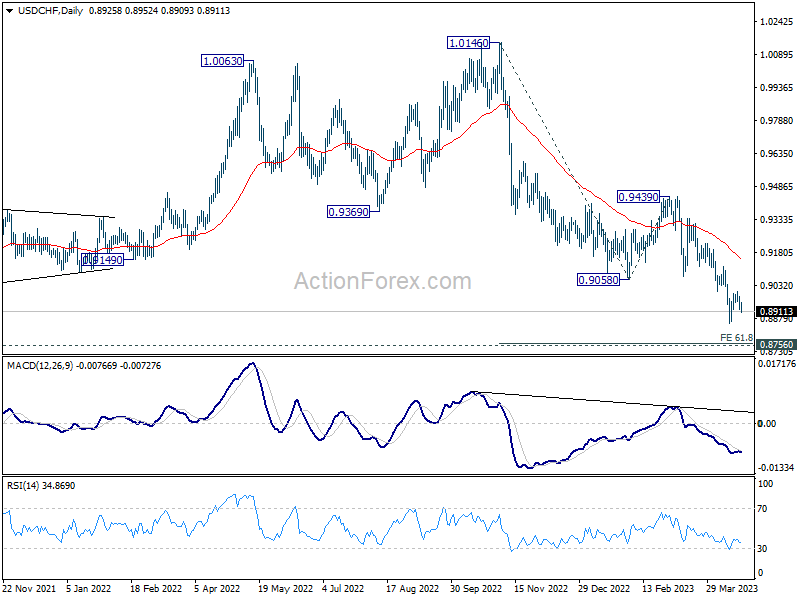

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8900; (P) 0.8944; (R1) 0.8967; More...

No change in USD/CHF's outlook as it's still bounded in range above 0.8858. Intraday bias stays neutral for the moment. Another decline cannot be ruled out with 0.9070 support turned resistance intact. On the downside, below 0.8858 will resume the down trend from 1.0146 to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt. On the upside, break of 0.9070 support turned resistance will confirm short term bottoming and turn bias back to the upside.

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

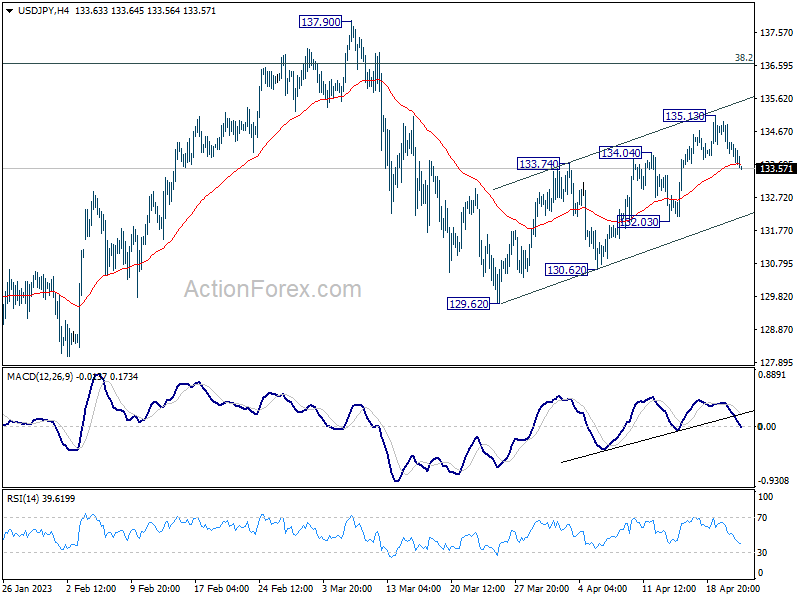

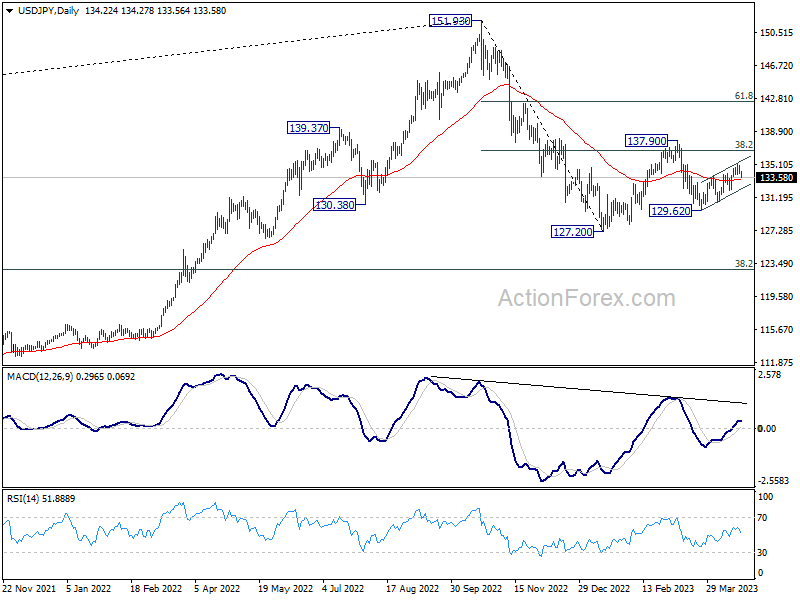

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 133.85; (P) 134.41; (R1) 134.82; More...

USD/JPY's retreat from 135.13 extends lower today but stays above 132.03 support. Outlook is unchanged and intraday bias remains neutral first. Another rally will remain in favor as long as 132.03 support holds. On the upside, break of 135.13 will resume the choppy rebound from 129.62 towards 137.90 resistance next.

In the bigger picture, corrective pattern from 127.20 might be extending. But after all, down trend from 151.93 is expected to resume at a later stage. Break of 127.20 will resume this down trend and target 61.8% projection of 151.93 to 127.20 from 137.90 at 122.61. This will now be the favored case as long as 137.90 resistance holds.

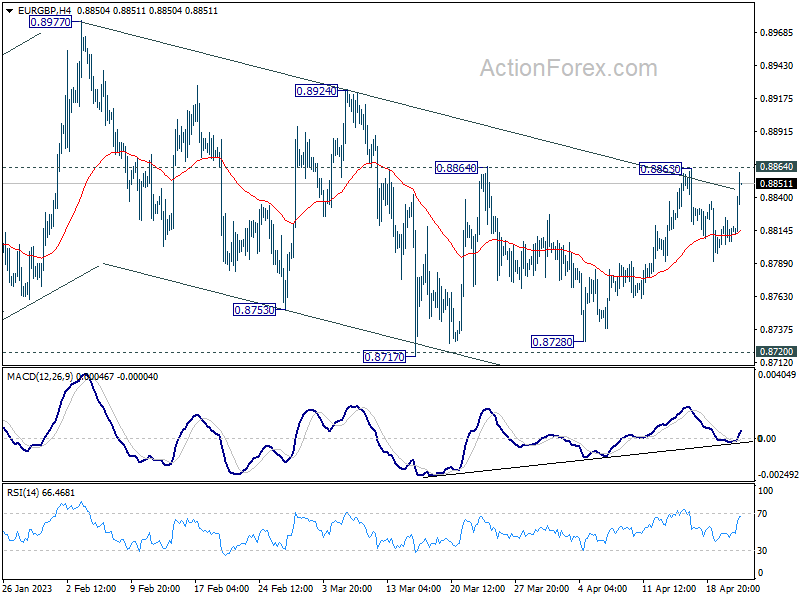

Yen Extending Rally While Euro and Swiss Franc Stay Firm

Japanese Yen is extending its rally in the early US session holding on to its gains and emerging as the second strongest currency for the week, just behind Swiss Franc. Despite persistently above-target inflation data, it remains unlikely that BoJ will make a shift in monetary policy next week. Additionally, the lack of volatility in 10-year JGB yield suggests traders are not betting on any changes to yield curve control. However, it's worth noting that BoJ has a history of surprising the markets, and traders should remain cautious.

Elsewhere in the currency markets, Euro is firmer after PMI data indicated a two-tracked economy gaining momentum, led by the services sector. Swiss Franc is also strong alongside Euro, but British pound lags behind after mixed data. Commodity currencies are the week's worst performers, with a few hours remaining to determine the weakest. Dollar is currently mixed but appears vulnerable against both Euro and Swiss Franc.

Technically, EUR/GBP is worth a watch before weekly close. Decisive break of 0.8864 resistance should clear the near term outlook and indicate that corrective fall from 0.8977 has completed. Strong rally should be seen to 0.8924. Firm break there will likely resume whole rally from 0.8545 through 0.8977.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is down -0.12%. CAC is down -0.01%. Germany 10-year yield is up 0.0198 at 2.466. Earlier in Asia, Nikkei dropped -0.33%. Hong Kong HSI dropped -1.57%. China Shanghai SSE dropped -1.95%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield dropped -0.0081 to 0.462.

Canada retail sales down -0.2% mom in Feb, smaller than expected

Canada retail sales contracted -0.2% mom to CAD 66.3B in February, better than expectation of -0.6% mom. Sales decreased in 4 of 9 subsectors, representing 48.0% of retail trade. The decrease was led by lower sales at gasoline stations and fuel vendors (-5.0%) and general merchandise retailers (-1.6%).

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—increased 0.1% mom.

In volume terms, retail sales decreased -0.7% mom in February.

Advance estimate suggests that sales decreased another -1.4% mom in March.

ECB Officials Highlight Persistent Core Inflation, Emphasize Data-Dependent Approach

ECB Vice President Luis de Guindos recently highlighted the persistence of core inflation, stating that it may be more persistent than markets anticipated. He emphasized that "core inflation remains very sticky," and while he believes it will eventually come down, the starting point is very high.

De Guindos also stressed that ECB will continue to communicate monetary policy on a meeting-by-meeting basis, with a data-dependent approach, rather than shifting to a forward-guidance strategy for several months. He added, "I believe that the current approach will be maintained for a few months until the evolution of inflation and the effects of our measures become clearer."

In a separate statement, ECB Governing Council member Ignazio Visco echoed de Guindos' concerns regarding stubborn core inflation. He emphasized the need for caution when setting policy, recommending that decisions be made on a meeting-by-meeting basis.

ECB Rehn: No reason to abandon restrictive policy prematurely

ECB Governing Council member Olli Rehn emphasized the importance of maintaining a proactive, balanced policy in the current monetary policy landscape. According to Rehn, the central bank has moved into an area that restricts aggregate demand, and he argued against abandoning this stance prematurely.

Rehn stated, "In monetary policy, we have moved into an area that restricts aggregate demand, and there is no reason for us to abandon it or exit it prematurely." He added, "The path to sustainable growth is narrow, but it can be traversed with a proactive, balanced policy."

Rehn further explained that by adhering to this approach, "we can achieve our goals without causing unnecessary costs to the economy - also because now the central banks are independent and not subject to political pressure, as in the 1970s."

Eurozone PMIs: Unevenly distributed growth but same optimism

Eurozone PMI Manufacturing declined from 47.3 to 45.5 in April, hitting a 35-month low. On the other hand, PMI Services rose from 55.0 to 56.6, a 12-month high. PMI Composite rose from 53.7 to 54.4, an 11-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said: "The HCOB Purchasing Managers' Indices for the euro zone show a very friendly overall picture of an economy that continues to recover. However, a closer look reveals that growth is very unevenly distributed..."

"For the further, companies are rather positive not only in the services sector but also for the manufacturing sector. According to the companies surveyed, the reasons for this optimism include a diminishing fear of a resurgence of the energy crisis, supply chains that are functioning better again, and the expectation that inflation has passed its zenith. The latter is coupled with the hope that the ECB will pause its interest rate hikes soon."

Also released, Germany PMI Manufacturing fell from 44.7 to 44.0, a 35-month low. PMI Services rose from 53.7 to 55.7, a 12-month high. PMI Composite rose from 52.6 to 53.9, a 12-month high.

France PMI Manufacturing dropped from 47.3 to 45.5, a 35-month low. PMI Services rose from 53.9 to 56.3, an 11-month high. PMI Composite rose from 52.7 to 53.8, also an 11-month high.

UK PMI composite rose to 53.9, lopsided growth but gained momentum

UK PMI Manufacturing fell from 47.9 to 46.6 in April, a 4-month low. PMI Services jumped from 52.9 to 54.9, a 12-month high. PMI Composite rose from 52.2 to 53.9, also a 12-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"Flash PMI surveys signalled an acceleration of economic growth to the fastest for a year in April, building on a modest return to growth in the first quarter of the year.

"Growth is lopsided, however, with surging demand for services contrasting with an ongoing downturn in demand for goods. Even within the service sector, growth is dependent on consumers switching spending from goods to services and a revival of financial services activity, both of which are areas susceptible to the impact of higher interest rates and the ongoing cost of living squeeze. Business services and manufacturing are clearly struggling.

"However, for now the key takeaway is that the economy as a whole is not only showing encouraging resilience but has gained growth momentum heading into the second quarter, the latest PMI reading broadly indicative of GDP rising at a robust quarterly rate of 0.4%.

"Inflationary pressures have meanwhile continued to cool in manufacturing, but price pressures have picked up in services following the resurgence of demand.

"This combination of faster growth and elevated price pressures put a twelfth rate hike by the Bank of England an increasingly done deal when it next meets on 11th May, and will add to speculation that further hikes may be needed."

UK retail sales volume down -0.9% mom in Mar, value down -0.9% mom

In volume term, UK retail sales fell -0.9% mom in March, below expectation of -0.5% mom. Ex-fuel sales declined -1.0% mom, below expectation of -0.7% mom. For the year, retail sales was down -3.1% yoy while ex-fuel sales was down -3.2% yoy, versus expectation of -3.1% for both.

In value term, retail sales was down -0.9% mom and up 4.5% yoy. Ex-fuel sales was down -0.6% mom and up 6.0% yoy.

Australian PMIs reveal divergence between manufacturing and services, RBA rate hike likely in May

Australia's April PMI Manufacturing has dropped to a 35-month low at 48.1, down from 49.1, while PMI Services jumped to a 10-month high of 52.6, up from 48.6. The PMI Composite also reached a 10-month high at 52.2. The data reveals a growing divergence between the performance of Australia's manufacturing and service sectors.

Warren Hogan, Chief Economic Advisor at Judo Bank, said, "Manufacturing activity remains soft, a reflection of weaker demand for goods and a gradual slowdown in construction activity in Australia. The April flash results for the services sector have bounced strongly, bringing into question the broader economic slowdown."

Hogan dismissed the idea of a recession, stating that the results point to a lift in Australia's economic momentum through mid-2023. However, he noted that the risk to inflation is from excess demand in the economy, putting upward pressure on domestic prices in energy, housing, and labor markets.

With the RBA Board set to meet in early May, Hogan believes the April flash PMI, strong employment outcomes in March, and a resurgence in parts of the housing market all suggest that another 25bp rate hike in May is more likely than not, depending on the March quarter CPI to be released on April 26th.

Japan PMIs: Private sector expands driven by resurgent service economy

Japan's PMI Manufacturing in April slightly rose from 49.2 to 49.5, missing expectations of 49.9. PMI Services experienced a slight drop from 55.0 to 54.9, while PMI Composite fell from 52.9 to 52.5. Despite this, the country's private sector continued to expand solidly at the beginning of Q2, with the service economy's resurgence helping to offset the weak manufacturing sector performance.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said, "Inflows of total new business increased at the quickest pace for nearly a year-and-a-half as services companies registered a steep upturn in sales amid reports of stronger demand conditions and improved customer numbers." Fiddes also noted signs of cost pressures easing, with overall input costs rising to the weakest extent in 15 months in April.

Regarding the year-ahead outlook, optimism in the service sector hit a record high in April, but weakened among manufacturers. While service providers anticipate further improvements in demand and operating conditions as the impact of COVID-19 fades, some manufacturers expressed concerns over the economic outlook, rising costs, and component shortages.

Japan's CPI core unchanged at 3.1%, core-core at highest since 1981

Japan's CPI growth slowed from 3.3% yoy to 3.2% yoy, exceeding the expected 2.6% yoy increase. The CPI core (all items excluding food) remained unchanged at 3.1% yoy, in line with expectations. The CPI core-core (all items excluding food and energy) accelerated from 3.5% yoy to 3.8% yoy, surpassing the anticipated 3.4% yoy figure. This marks the 10th consecutive uptick and the highest level since December 1981.

New BOJ Governor Kazuo Ueda has recently committed to maintaining ultra-loose monetary policy. While no major changes to the bond yield control policy are expected at Ueda's first policy-setting meeting next week, the spreading inflation from energy to the broader economy may keep market expectations alive that BOJ could begin phasing out its massive stimulus later this year. However, this will depend on whether wages increase sustainably and support consumption.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 133.85; (P) 134.41; (R1) 134.82; More...

USD/JPY's retreat from 135.13 extends lower today but stays above 132.03 support. Outlook is unchanged and intraday bias remains neutral first. Another rally will remain in favor as long as 132.03 support holds. On the upside, break of 135.13 will resume the choppy rebound from 129.62 towards 137.90 resistance next.

In the bigger picture, corrective pattern from 127.20 might be extending. But after all, down trend from 151.93 is expected to resume at a later stage. Break of 127.20 will resume this down trend and target 61.8% projection of 151.93 to 127.20 from 137.90 at 122.61. This will now be the favored case as long as 137.90 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Apr P | 48.1 | 49.1 | ||

| 23:00 | AUD | Services PMI Apr P | 52.6 | 48.6 | ||

| 23:01 | GBP | GfK Consumer Confidence Apr | -30 | -35 | -36 | |

| 23:30 | JPY | National CPI Y/Y Mar | 3.20% | 2.60% | 3.30% | |

| 23:30 | JPY | National CPI Core Y/Y Mar | 3.10% | 3.10% | 3.10% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Mar | 3.80% | 3.40% | 3.50% | |

| 00:30 | JPY | Manufacturing PMI Apr P | 49.5 | 49.9 | 49.2 | |

| 00:30 | JPY | Services PMI Apr P | 54.9 | 55 | ||

| 06:00 | GBP | Retail Sales M/M Mar | -0.90% | -0.50% | 1.20% | 1.10% |

| 06:00 | GBP | Retail Sales Y/Y Mar | -3.10% | -3.10% | -3.50% | |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Mar | -1% | -0.70% | 1.50% | 1.40% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Mar | -3.20% | -3.10% | -3.30% | -3.00% |

| 07:15 | EUR | France Manufacturing PMI Apr P | 45.5 | 47.5 | 47.3 | |

| 07:15 | EUR | France Services PMI Apr P | 56.3 | 53.6 | 53.9 | |

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 44 | 45.6 | 44.7 | |

| 07:30 | EUR | Germany Services PMI Apr P | 55.7 | 53.5 | 53.7 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 45.5 | 48.2 | 47.3 | |

| 08:00 | EUR | Eurozone Services PMI Apr P | 56.6 | 54.6 | 55 | |

| 08:30 | GBP | Manufacturing PMI Apr P | 46.6 | 48.8 | 47.9 | |

| 08:30 | GBP | Services PMI Apr P | 54.9 | 52.9 | 52.9 | |

| 12:30 | CAD | Retail Sales M/M Feb | -0.20% | -0.60% | 1.40% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Feb | -0.70% | 0.00% | 0.90% | |

| 13:45 | USD | Manufacturing PMI Apr P | 49.2 | 49.2 | ||

| 13:45 | USD | Services PMI Apr P | 51.8 | 52.6 |

Canada retail sales down -0.2% mom in Feb, smaller than expected

Canada retail sales contracted -0.2% mom to CAD 66.3B in February, better than expectation of -0.6% mom. Sales decreased in 4 of 9 subsectors, representing 48.0% of retail trade. The decrease was led by lower sales at gasoline stations and fuel vendors (-5.0%) and general merchandise retailers (-1.6%).

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—increased 0.1% mom.

In volume terms, retail sales decreased -0.7% mom in February.

Advance estimate suggests that sales decreased another -1.4% mom in March.

ECB Rehn: No reason to abandon restrictive policy prematurely

ECB Governing Council member Olli Rehn emphasized the importance of maintaining a proactive, balanced policy in the current monetary policy landscape. According to Rehn, the central bank has moved into an area that restricts aggregate demand, and he argued against abandoning this stance prematurely.

Rehn stated, "In monetary policy, we have moved into an area that restricts aggregate demand, and there is no reason for us to abandon it or exit it prematurely." He added, "The path to sustainable growth is narrow, but it can be traversed with a proactive, balanced policy."

Rehn further explained that by adhering to this approach, "we can achieve our goals without causing unnecessary costs to the economy - also because now the central banks are independent and not subject to political pressure, as in the 1970s."