Sample Category Title

The Weekly Bottom Line: Housing Falls as the Fed Blackout Period Begins

U.S. Highlights

- China’s economy saw solid growth in the first quarter, with a strong rebound in consumption and exports after lockdowns were lifted at the end of last year.

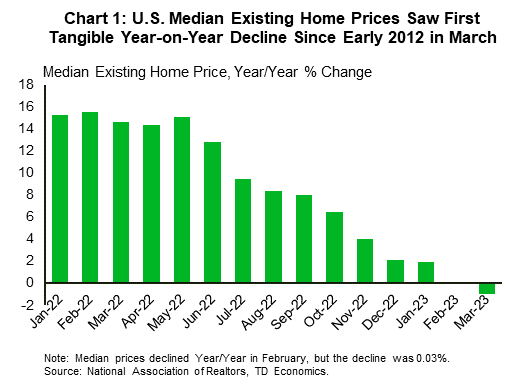

- U.S. existing home sales fell by 2.4% month-on-month (m/m) in March, falling from February’s revised 13.8% m/m uptick as past mortgage rate increases weighed on demand.

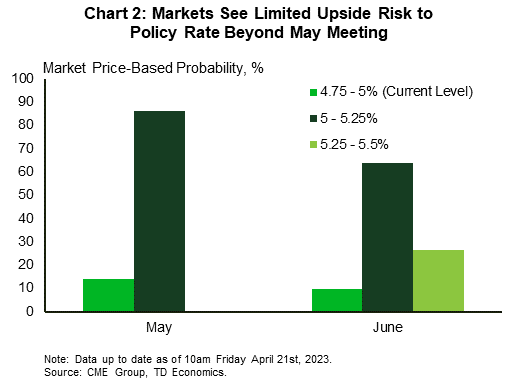

- FOMC members noted that they continue to monitor credit conditions, but many seem to be in favor of further policy tightening at the next meeting in May.

Canadian Highlights

- Canadian inflation continued to ease in March, coming in at 4.3% year-on-year, as energy prices weighed on the overall index.

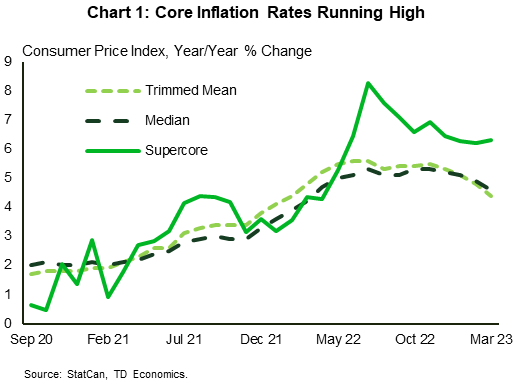

- Core inflation rates also fell, but to a lesser degree, as strength in the Canadian economy has led to an upturn in the cyclical components of inflation (supercore).

- Although today’s retail sales data showed that Canadians pared back on goods spending, our internal TD data revealed that this was more about consumers shifting to services rather than an outright pull back in spending.

U.S. - Housing Falls as the Fed Blackout Period Begins

As earnings season picked up pace this week, markets were closely attuned to the first quarter performance of U.S. companies. However, the net result on equity markets was muted, as results that were on aggregate moderately positive were partially overshadowed by the downbeat outlook for demand amid the expected economic slowdown later this year. As of the time of writing, the S&P 500 is down 0.5% on the week while the ten-year Treasury yield is up 5 basis-points (bps) to 3.57%.

On the global economic data front, we kicked off the week with first quarter Chinese GDP data, which grew by 4.5% from its year-ago level. The print was better than expected, as pent-up demand from consumers powered growth. China’s economic rebound is expected to be short-lived as consumer exuberance fades and structural headwinds continue to weigh on the economy in the back half of the year.

In the U.S. we had a housing-centric week for economic data, with updates on both existing home sales and residential construction. Data released on Thursday showed that existing home sales fell by 2.4% month-on-month (m/m) in March, pulling back from February’s revised 13.8% m/m increase. Month-to-month changes have been mirroring the volatility seen in mortgage rates (with a lag) as elevated prices have increased the reliance of buyers on financing conditions. While median home prices declined for a second consecutive month relative to year-ago levels (Chart 1), the seasonally adjusted change between February and March was slightly positive. Prices have been held up in part due to low inventory levels. However, new home construction is picking up, with single-family housing starts recovering for a second consecutive month in March, after eleven straight months of declines.

With the Federal Reserve’s pre-meeting blackout period starting on Saturday, we won’t hear from any FOMC members again until Chair Powell’s press conference on May 3rd. Luckily, we heard from ten Fed officials this week, six of whom are voting members. Most of the speakers noted that they were continuing to monitor credit conditions for signs of further stress. The Fed’s regional monitoring in April’s Beige Book stating that “several Districts noted that banks tightened lending standards amid increased uncertainty and concerns about liquidity”. Although this may aid the Fed in tightening credit conditions, as noted by Chicago Fed President Goolsbee this week, most members seemed to agree that further policy tightening would be required to sustainably return inflation to the Fed’s 2% target. As of the time of writing, markets are expecting the Fed to hike by 25bps in May, and then hold in June (Chart 2).

Next week we’ll get a first look at first quarter U.S. GDP and March PCE inflation, both of which are expected to show signs of cooling. Our forecast calls for activity to continue to slow through the remainder of 2023. This should help ease inflation pressures, enabling the Fed to keep the funds rate at 5.25% for the rest of the year.

Canada – It's a Bird, It's a Plane, It's Supercore!

March's inflation data was under the microscope this week, and it continued its steady deceleration. The headline Consumer Price Index (CPI) was up 4.3% year-on-year (y/y), a significant drop from its reading of 5.2% y/y in February and its peak of 8.1% y/y last June. This trend is likely to continue. We expect that inflation is on course to flirt with the 3% upper bound of the Bank of Canada's (BoC's) target range this summer.

So far, headline inflation has cooled largely due to an easing in supply chain bottlenecks and steep decline in commodity prices over the last eight months. As a result, goods inflation has fallen to 3.6% y/y (down from 11.2% in June 2022), while energy inflation has turned negative, at -6.9% y/y. Energy prices are expected to continue to weigh on goods inflation over the next few months. This is the main reason why we are confident that inflation is likely to slow to a 3% pace in short order.

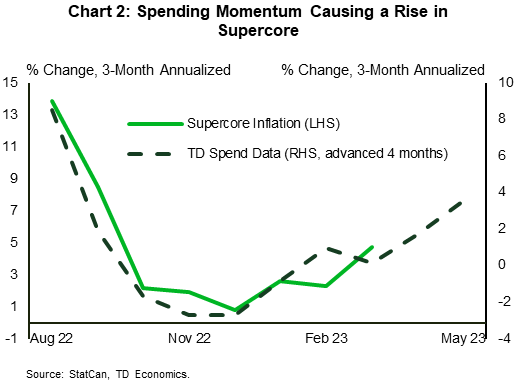

However, the BoC has stated it won't be happy with 3% inflation. It wants to finish the job and get to 2%. Central bankers typically look at core inflation measures as a guidepost to underlying inflation pressures, since things like food and energy can be volatile. Core inflation has come down, but at a much slower pace than headline inflation. The BoC's preferred metrics, trimmed mean and median inflation, came in slightly higher than headline CPI, at 4.4% y/y and 4.6% y/y, respectively. The story is more concerning when we look at our index of 'supercore' inflation (cyclical inflation in services), which posted a 6.3% y/y print (Chart 1)! If these core metrics don't start to fall decisively, the BoC will be hard pressed to stabilize inflation at its 2% goal.

Core inflation rates have failed to move lower because consumer spending has seen a revival recently. Labour markets have continued to expand at an average pace of 62 thousand new jobs every month (4 times the trend pace) and governments are supporting peoples' incomes through debt financed transfers. No wonder our internal TD credit/debit card data have shown that total spending has been on the rise. Spending on services has fueled this growth – rising more than 4% month-on-month (m/m) in February, as Canadians shifted away from spending on goods. In that sense, today's retail sales data confirmed what we already knew, as retail spending (goods) fell 0.2% m/m in February. As we show in Chart 2, total spending in Canada is surging (Chart 2). And given that consumer demand is the main driver of cyclical inflation, we expect that supercore inflation will keep rising over the coming months.

The BoC is likely concerned about this. Although it has seen a cooling in interest rate sensitive parts of the economy like housing – as evidenced by the 11% drop in housing starts released this week – the cyclical thrust in other areas has intensified. This is likely why Governor Macklem has been reenforcing the message that rates will need to stay higher for longer. Or rather, rates will stay high for as long as it takes for renewed momentum to fizzle out.

Weekly Economic & Financial Commentary: Give Thought to the Pause

Summary

United States: A Downturn Is Still in the Cards

- Data released this week support our expectations for a recession in the second half of the year. The LEI continued to flash contraction as early signs of labor market weakening are starting to emerge. Meanwhile, a batch of housing data confirmed that a full-fledged housing market recovery is still far off.

- Next week: Durable Goods (Wed), GDP (Thu), Personal Income & Spending (Fri)

International: Global Growth Prospects Continue to Improve

- Early this week, China reported Q1-2023 GDP data, a widely anticipated data release. Q1 data offered markets an opportunity to gauge how China's economy performed after authorities lifted Zero-COVID policies around the end of last year. The key takeaway was that China's economy performed better than expected, growing 2.2% on a quarterly basis and 4.5% on a year-over-year basis.

- Next week: Central Bank of Turkey (Thu), Eurozone GDP (Fri), Bank of Japan (Fri)

Interest Rate Watch: Give Thought to the Pause

- The fastest pace of policy tightening since the early 1980s is winding down. Our forecast anticipates one more quarter-point rate hike at the upcoming FOMC meeting on May 3, after which we suspect the Fed will remain on hold until the fourth quarter. Had we not encountered a banking crisis, a few more rate increases might have been in the offing. However, the recent difficulties in the financial sector diminish the need for further hikes beyond May, in our view.

Credit Market Insights: Fed's Beige Book Brings Some Color to Recent Financial Turmoil

- On Wednesday, the latest edition of the Federal Reserve’s Beige Book was released, covering the month of March and through early April. The previous Beige Book was published in early March but quickly became stale following the failures of Silicon Valley Bank and Signature Bank. The latest read covers the period following recent financial turmoil and the fallout it has caused.

Week Ahead – Spotlight on BoJ’s Ueda as First Meeting Looms; US and Eurozone Data Eyed Too

The Bank of Japan will hold its first policy meeting under the stewardship of Kazuo Ueda next week, although it’s looking unlikely that he will kick things off with a bang. The focus may therefore quickly shift to GDP numbers out of the United States and Eurozone where both economies are expected to have dodged a recession, while the all-important PCE inflation report will be one of the final pieces of the rate puzzle before the Fed’s May decision.

Ueda to play it safe at his first meeting

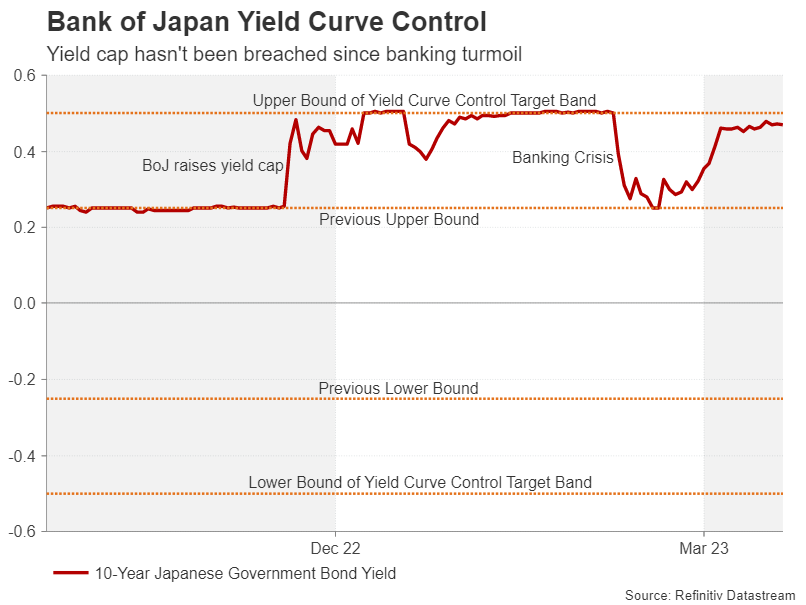

The banking crisis may have been a blessing in disguise for the Bank of Japan as the turmoil sent Japanese government bond (JGB) yields diving, taking the pressure off policymakers to make any imminent tweaks to their controversial yield curve control policy. The 10-year yield, which the BoJ aims to keep below 0.50%, has not breached this cap since the crisis first unfolded.

However, most market participants see it as only a matter of time before the Bank makes further adjustments to rein in its ultra-accommodative policies even though inflation now appears to be on the way down. If as expected, Ueda delivers no surprises in his inaugural meeting on Friday and keeps all of the BoJ’s monetary policy settings unchanged, investors will be hunting for clues about the timing of any possible tweak.

Ueda has so far not strayed too far from his predecessor’s stance, signalling that he wants to see stronger wage growth before altering the policy course. However, his tone on achieving this goal has been somewhat more optimistic and he may use his first post-meeting press conference to lay the groundwork for eventually phasing out yield curve control.

The Bank will also be publishing an updated set of quarterly projections, thus, the forecast on inflation will also guide the markets on where policy might be headed. In addition, there’s a barrage of Japanese economic indicators on the agenda too, the majority of which are due on Thursday and will include April CPI figures for Tokyo, preliminary industrial production readings, as well as retail sales and jobs stats.

The yen may not necessarily react much to the data but should Ueda hint at some kind of a change later in the year, the currency is likely to gain versus its peers.

Eurozone GDP probably rebounded mildly in Q1

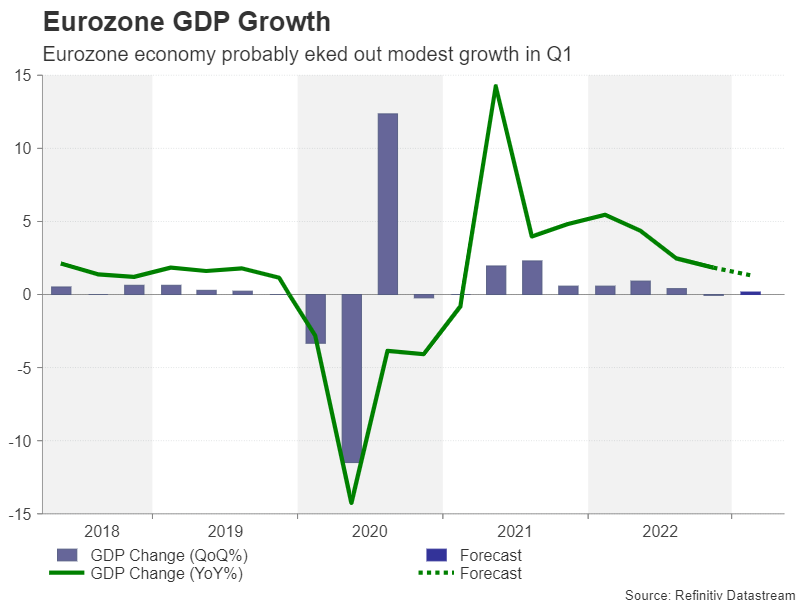

The Eurozone economy grinded to a halt at the end of last year, but it’s expected to have eked out modest growth in the first three months of 2023. Lower fuel prices and a relatively mild winter that didn’t leave households completely out of pocket likely helped the euro area avoid a recession, at least for now. The flash GDP estimates out on Friday are forecast to show GDP rising by 0.2% over the quarter.

That’s not exactly cause for a huge celebration, but the outlook has improved dramatically from a few months ago, or even more recently when there was a real threat of the bank collapses in the US and Switzerland having a domino effect on Eurozone banks.

A notable miss in the GDP print might make the European Central Bank more hesitant about hiking rates by 50 basis points at its May meeting, whereas a bigger rebound would probably remove any doubts about going big.

However, ECB policymakers will also be monitoring the flash CPI figures out of Germany and France due the same day. The Eurozone-wide numbers will be released a few days later but Friday’s sneak peek still has the capacity to move the markets as a 50-bps move is only 30% priced in.

Should those odds creep up, the euro could climb higher as it fights to make a clear break above the $1.10 level.

PCE inflation to lead data-packed week in the US

Fed officials will be staying mum over the coming week as they enter the blackout period ahead of the May 2-3 policy meeting. However, there’s plenty on the US economic agenda that should provide some last-minute guidance as to what to expect from the Fed.

Starting things off is the consumer confidence index for April on Tuesday along with March new home sales. Durable goods orders will follow on Wednesday, but the first top tier release will land on Thursday with the advance estimate of Q1 GDP.

The American economy is expected to have expanded by an annualized pace of 2.0% over the period, which would imply that a recession is not imminent. Pending home sales are also due the same day.

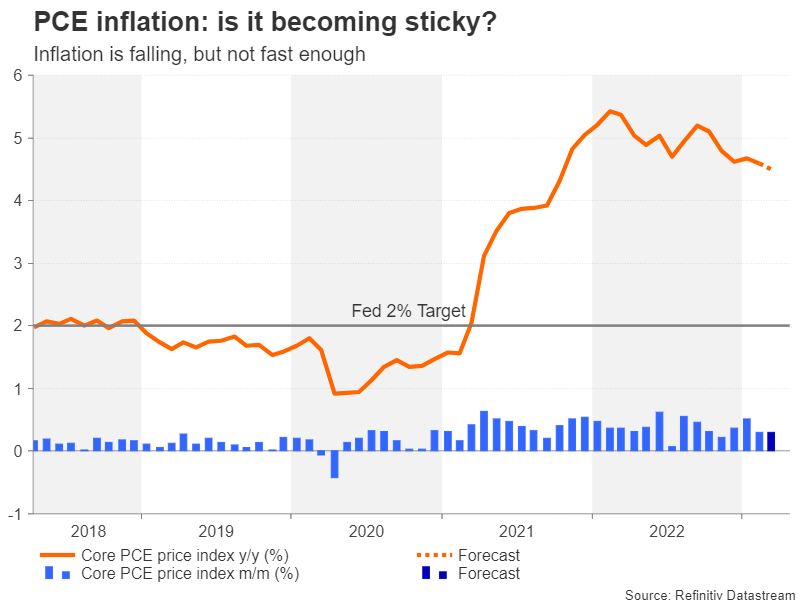

The second highlight will be Friday’s personal income and outlays report that contains the all-important core PCE price index as well as consumption figures. Other data on Friday will include quarterly wages and the Chicago PMI.

Although the Fed’s favourite price gauge has moderated significantly from its high of 5.4% in 2022, the downward progress has slowed in recent months. The core PCE price index is forecast to have edged down slightly to 4.5% y/y in March.

It is almost certain that the Fed will hike rates by 25 bps in March, but a bigger increment is highly unlikely. Nevertheless, a hotter-than-expected reading would reduce the chances of the Fed pausing in May, especially if the incoming data is overall positive.

The bigger question is whether the US dollar can enjoy a meaningful boost from a stronger set of numbers. Investors remain convinced the Fed will begin cutting rates in the second half of 2023 while other key central banks potentially remain on a hiking path.

So the data alone may not do much in tempering those dovish bets and the dollar may struggle to attract much upside unless Fed Chair Powell does a more convincing job of ratcheting up his hawkish rhetoric.

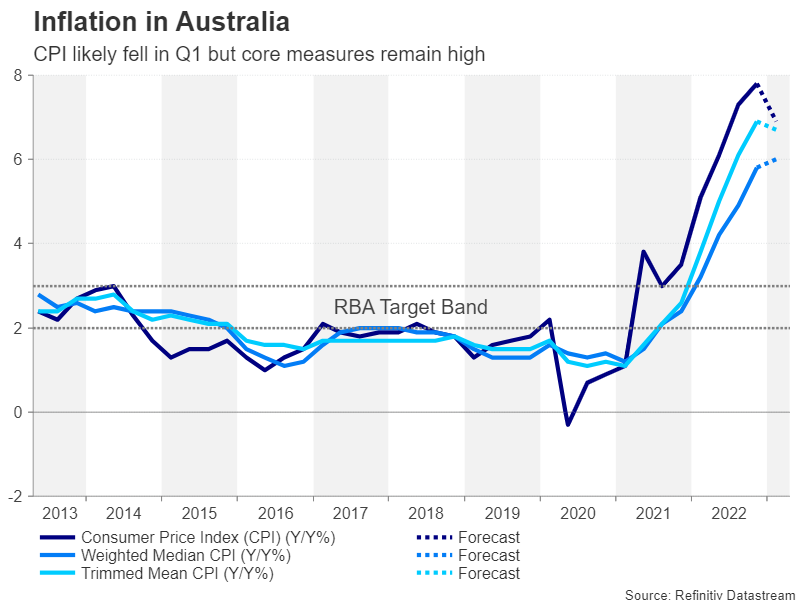

Inflation on tap in Australia

The Australian dollar regained some bullish impetus from the Reserve Bank of Australia’s latest meeting minutes that revealed that the decision to pause rate hikes was a close call. However, Wednesday’s CPI report might see some of those revived hawkish bets being wound back as inflation likely eased in the fourth quarter of 2022.

The headline rate of CPI reached a three-decade high of 7.8% at the end of 2022 but is expected to have fallen back to 6.9% in the first quarter of 2022. The March print is also due and investors will be watching to see if CPI continued to decline after the sharp drops in January and February, as well as keeping an eye on the core measures, which are only published quarterly.

If the latest price gauges reinforce the picture of subsiding inflationary pressures, the aussie might slip back against its US counterpart.

Letting the Euro Area Data Speak for Itself

With the market counting down the days to the first week of May, next week’s data releases will probably give us the strongest indication about the forthcoming ECB decision. Inflation and GDP figures set the scene for an exciting week especially as euro/dollar is trying to remain in the vicinity of 1.10.

CPI is the key for the May ECB meeting

At the March meeting the ECB announced its new data-dependent strategy. It essentially moved from the “hike-as-fast-as-possible” doctrine to a more mainstream central bank strategy. With the next meeting coming on May 4, next week's data is extremely crucial. ECB member and Dutch central bank chief Knot was quite explicit in his comment earlier this week that April inflation will determine the size of the May hike. While Knot is a known hawk, it appears that the hawks could potentially push for a stronger rate hike than the current market-anticipated move of 25bps.

While one could justify this inherent hawkishness on the fact that the ECB has the Bundesbank mentality imprinted in its DNA, it is worth considering that the inflation situation in the nearby UK might be also affecting the ECB's stance. The more hawkish members are determined to avoid high inflation becoming an everyday concern affecting long-term consumer perceptions.

Another drop in the German CPI?

On Friday, April 28 we will get the usual release of the CPI figures for the key German states with the preliminary national print coming after midday. This is the key number by far for market sentiment. During 2022, inflation releases produced the strongest post-announcement volatility. The German CPI has been on a gentle downward trend, with the April figure expected to record another small dip to 7.2% year-on-year change. This is clearly elevated and not an easy reading for the hawks, but they can take some solace from the latest German PPI number showing a significant deceleration in the year-on-year print. On the other hand, a strong show at the German CPI would clearly open the floodgates with the immediate response being an increased possibility of a 50 bps move at the May meeting.

GDP figures might prove an unpleasant reading

Friday will commence with the preliminary GDP figures from the biggest euro area countries and the eurozone aggregate for the first quarter of 2023. Market eyes will understandably be on the German print with the consensus pointing to another negative quarter-on-quarter figure, but an improvement compared to the fourth quarter of 2022 print of -0.4% quarterly change. A second consecutive negative GDP quarter will allow for pompous headlines that Germany is officially in recession.

Semantics aside, the magnitude of the slowdown will be the key topic of discussion at the ECB halls. The IMF penciled in a -0.1% annual figure for 2023 in its April Outlook update, a view shared by the German IFO institution, and hence a weaker print at Friday’s figure will potentially open Pandora's box with more pessimistic views spreading quickly in the newswires.

Strong start of the week with the IFO survey

The week, though, will start on an equally high note as the German IFO survey for April will be published on Monday morning. One cannot fail to notice the impressive improvement in this survey since October 2022, but it is also true that the outright level of the Expectations component remains very low compared to its long-term average. The average of the IFO survey for the first quarter of 2023 is pointing to a downside risk in the current GDP forecast.

Similarly, the market is expecting a drop in the April IFO figures, which will not be a good discussion point for ECB hawks pushing for a 50 bps rate move in two weeks, especially as Friday's Manufacturing PMI release surprised on the downside.

Euro/pound in waiting mode

Euro/pound has been on an upward path since March 2022 lows, but it has obviously not been a one-way street. The recent range-trading activity has caused a build-up of key resistance and support points around the 0.8800 level. In addition, a right-angled triangle is trying to dictate market reaction.

With the momentum indicators confirming this delicate balance, next week’s data will most likely give the necessary push to market participants to make the first move. Euro bulls appear to have an easier path higher, at least until the 0.8902 area. On the other hand, euro bears will face considerable support at the 0.8794-0.8815 area defined by multiple SMAs and historical peaks.

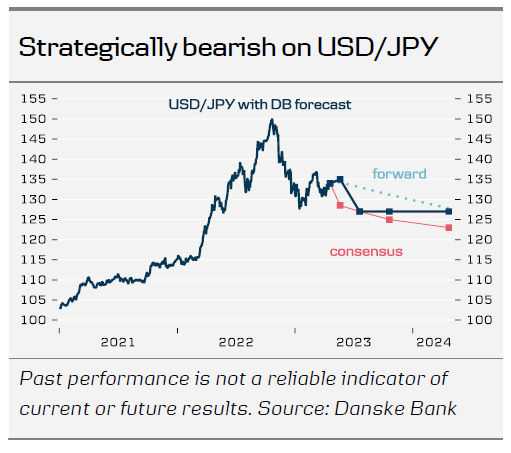

Bank of Japan Preview: Risk of Tightening Too Soon Still Dominates

- We do not expect any changes to monetary policy on the new Governor Ueda's first monetary policy meeting on 28 April.

- Inflationary pressures seem persistent, especially fuelled by stronger-thanexpected wage growth, which could pave the way for the BoJ to at least tweak the Yield Curve Control (YCC) on either the June or the July meeting.

- We remain bearish on USD/JPY on a strategic horizon and expect the cross towards 127 in 3M.

Calling the timing of BoJ backtracking from its YCC is a difficult task. If the BoJ starts guiding the market by indicating a steeper JGB-curve, investors will immediately dump their bond holdings, and BoJ will be forced to throw in the towel. Thus, we should not expect any clues from the BoJ and we do not read too much into Governor Ueda's message to maintain monetary stimulus.

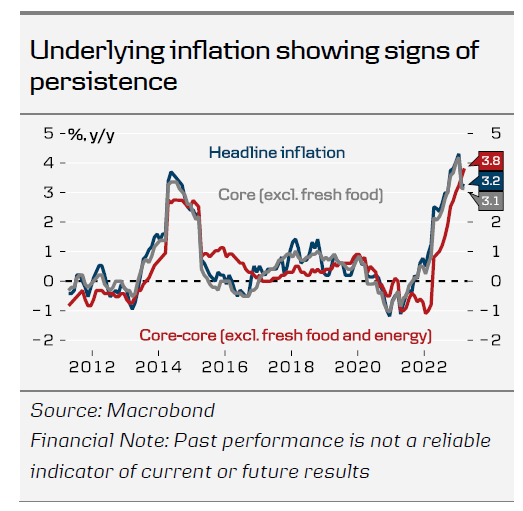

Recent CPI prints show more broad-based price pressures in Japan. Even though headline inflation fell slightly to 3.2% y/y in March, down from 3.3% in February, the core-core measure, which excludes fresh food and energy and more interesting for the BoJ, increased to 3.8% y/y in March, up from 3.5% in February, suggesting underlying price pressures are increasingly becoming more persistent. Latest figures for wage growth indicate increases well above consensus for the fiscal year of 2023. Currently the figures suggest 3.5% y/y broad nominal wage hikes, which is substantially above consensus and above the 3.0% the BoJ states is needed to obtain 2% inflation sustainably.

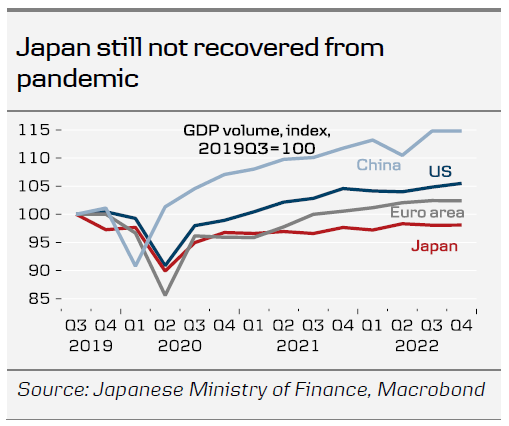

When discussing BoJ entering tightening mode, it is also important to remember that Japan, as opposed to the other big global economies, actually still has not recovered from the pandemic. Although improving, domestic private demand remains subdued due to VAThike, COVID-related lockdowns and higher inflation. Following decades with deflation, it remains a significant risk that tightening too soon sends the economy back in to deflation or low-inflation mode, before a sustainable price-wage dynamic is achieved. We think the BoJ will wait for confirmation of broad wage increases before it tightens policy. It is a fine balancing act, though, and we believe the BoJ will ultimately see the current situation as a good opportunity to finally loosen the grip on the yield curve and back away from a policy, which is highly distorting markets. However, we also know, there is no consensus on the policy board on the urgency to back off YCC.

We expect a cautious approach from the BoJ and see it slowly widening the tolerance band around the 0% 10-year JGB yield target at either the June or the July meeting. We think tweaks are more likely than an outright abandonment of the YCC – it could e.g. be by widening the YCC band from +/- 50bp to +/- 100bp.

We remain strategically bearish on USD/JPY; although we acknowledge there could be topside risk to the cross in the near-term on a relatively hawkish Fed and dovish BoJ. On the strategic horizon, our models suggest the cross is fundamentally overvalued, and together with monetary tightening from the BoJ, we forecast the cross lower at 127 in 3M.

Weekly Focus – PMIs Continue to Show a Two-Speed Economy

Financial markets lacked clear direction this week, although negative sentiment strengthened towards Friday. The recovery in equity markets stalled, while bond yields turned lower. EUR/USD continues to hover near 1.10, but in our latest FX Forecast Update, 19 April, we still see the cross turning lower in H2. April Flash PMIs continued to show a picture of a two-speed economy, with euro area manufacturing index remaining on contractionary territory, but with services sector driving the composite index to a 11-month high (54.4). We think the ECB is more concerned about the latter due to the close link to wage dynamics, and continue to look for a 50bp hike in the May meeting.

Chinese GDP growth surprised to the upside in Q1 at 2.2% q/q. Positively, the recovery was driven by stronger consumer sentiment, illustrated by retail sales rising 10.6% y/y in March. Getting the private consumption engine started is essential for making the recovery more sustained, rather than just stimulus-driven. The release creates some upside risks for our Chinse GDP growth forecast of 5.5% this year.

The political situation around the US debt ceiling remains tense, and the lower-than-expected tax revenues around the April 'Tax Day' this week could suggest that the time for coming up with a resolution is running short. The 'X-date', when the US Treasury will not be able to cover its expenses anymore due to the debt ceiling, could come as early as June. Meanwhile, House Speaker McCarthy presented a proposal for the spending cuts republicans demand in return for supporting a USD 1.5 trillion raise to debt ceiling this week. The proposal did not receive a warm welcome from the senate democrats, with the Majority Leader Schumer saying it has 'no chance of moving forward in senate'. Read our thoughts from Research US - X-date looms closer as 'Tax Day' disappoints, 20 April.

Japanese inflation came out largely in line with expectations. Consumer prices excl. fresh food rose by 3.1% y/y in March, but excluding energy as well, inflation continued to accelerate to 3.8% y/y - the fastest since 1980s. Next week, we do not expect Bank of Japan to make changes to their monetary policy in the meeting ending on Friday, even if we think BoJ is still moving towards loosening the grip on the yield curve. BoJ likely wants confirmation on broad based wage hikes before they move at the June or July meeting.

We expect Rikbank to hike rates by 50bp, read more in the Nordic section below.

On the data front, Q1 flash GDP figures will be released from the euro area and the US. In the euro area, we look for a decline of -0.1% as a strong rebound in private consumption is not yet in sight. We also get Ifo (Monday) and EU Commission sentiment indicator (Thursday), which will give more insights how the economy started into Q2. German CPI figures on Friday will also be watched closely by the market, especially for signs of moderating underlying inflation pressures ahead of ECB's May meeting.

US GDP likely continued its modest recovery in Q1, supported by brisk consumer spending especially in the first two months of the quarter. We look for +0.8% q/q AR, although risks are likely to the upside given that the economy still appears resilient to the banking sector uncertainty, which began in March.

Cliff Notes: RBA Review Received as China’s Economic Strength Shines Bright

Key insights from the week that was.

Monetary policy remained centre stage across the world this week, but particularly in Australia as the RBA Review and April Board meeting minutes were released.

The April RBA meeting minutes highlight the Board’s preference for optionality. As detailed by Chief Economist Bill Evans, the “case for an increase is much stronger than was the case for the April meeting”, with the Board members noting: “the forecasts produced by the staff in February had inflation returning to target range only by mid-2025 and that it would be inconsistent with the Board’s mandate for it to tolerate a slower return to target”; these “forecasts were conditioned on monetary policy being tightened a little further”. The Board also raised some new risks, in particular: that the current strength in population growth “could put significant pressure on Australia’s existing capital stock, especially housing, which would in turn manifest in higher consumer prices”; and there was “increased risk of larger wage increases in parts of the economy, including the public sector”. Also critical to the decision in May will be next week’s Q1 CPI report. Westpac remains of the view that, while moderating, another high annual inflation print in Q1 warrants one further 25bp hike in May to 3.85% after which the cash rate will be left on hold until early-2024 to quell lingering risks.

Subsequent to the minutes, the Government commissioned RBA Review was publicly released and commented on by RBA Governor Lowe. ‘An RBA fit for the Future’ “analyses the RBA’s performance over the past 30 years and makes recommendations on the monetary policy framework, governance, leadership and culture of the RBA”. Many of the recommendations are significant, albeit with the detail and timing still to be worked through. Chief Economist Bill Evans’ note discusses the implications for policy setting.

Ahead of Australia’s Q1 CPI next week, New Zealand’s latest update (pleasingly) disappointed market and RBNZ expectations for a second-consecutive quarter, printing at 1.2%, 6.7%yr (from 7.2%yr at December). Individual items showed considerable volatility. But measures of underlying momentum steadied or eased back in Q1. Our NZ economics team remains of the view that inflation won’t be back below 3.0%yr until the second half of 2024. The RBNZ is therefore seen hiking by 25bps at the May meeting to a cycle peak of 5.50% to be held until mid-2024.

Of the data from further afield, China’s Q1 GDP release and associated partial data was most significant. At 2.2%, the Q1 gain was strong but broadly in line with expectations. However, Q4 2022’s outcome was revised up from 0.0% to 0.6%, seeing the annual rate at 4.5%yr at March 2023 versus the market’s expectation of 4.0%. We remain of the view that GDP growth will continue to outperform during 2023, coming in above 6.0%yr – a rate materially above authorities’ guidance and current market estimates. The primary support for this view from the March data round is the building strength in consumer spending, year-to-date retail sales growth jumping from 3.5%yr in February to 5.8%yr in March. Although property investment disappointed, likely as a result of the limited pipeline of work to be done on existing projects, residential property sales created confidence in the outlook for 2023 and beyond, year-to-date growth accelerating from 3.5%yr in February to 7.1%yr in March. That new home prices look to have based and are now rising points to further near-term momentum in activity, particularly given the robust health of household wealth and income. In our view, the momentum apparent in China’s domestic economy along with their exposure to Asia will well and truly offset the negative influence of weakening developed-world demand, setting China apart from other major economies in 2023 and beyond.

Turning to the US, data has been light this week and concentrated on housing. Starts and permits remained volatile in March as they were caught between tight financial conditions and a lack of new housing supply. Existing home sales meanwhile disappointed falling 2.4%, although it remains unclear whether demand or supply is the prime influence.

Arguably of greatest significance for US monetary policy however was the release of the latest Beige Book, covering conditions across the 12 Federal Reserve districts. Broadly this update suggests the US economy is stagnating and that labour market slack is building, weighing on wage growth and easing risks related to inflation. Also critical for policy into 2024, “Several Districts noted that banks tightened lending standards amid increased uncertainty and concerns about liquidity”.

Together with the sanguine inflation data received last week, these observations point to little need for further action by the FOMC to tame inflation. The economy arguably instead needs an extended period of stable contractionary policy to allow remaining inflation risks to abate and consumer expectations to reset without heightened fears over economic activity. However, we also need to be aware of the mindset of FOMC members, many of whom continue to reference a need for a further marginal increase in the policy rate, which the market is taking to mean another 25bp hike at or before the June meeting. Whereas FOMC members argue policy will then remain on hold for a lengthy period, the market has approximately 75bps of rate cuts priced by January 2024. This view speaks to the downside risks that are building for activity given the already contractionary stance of monetary policy and the tightening of financial conditions occurring through the US banking system.

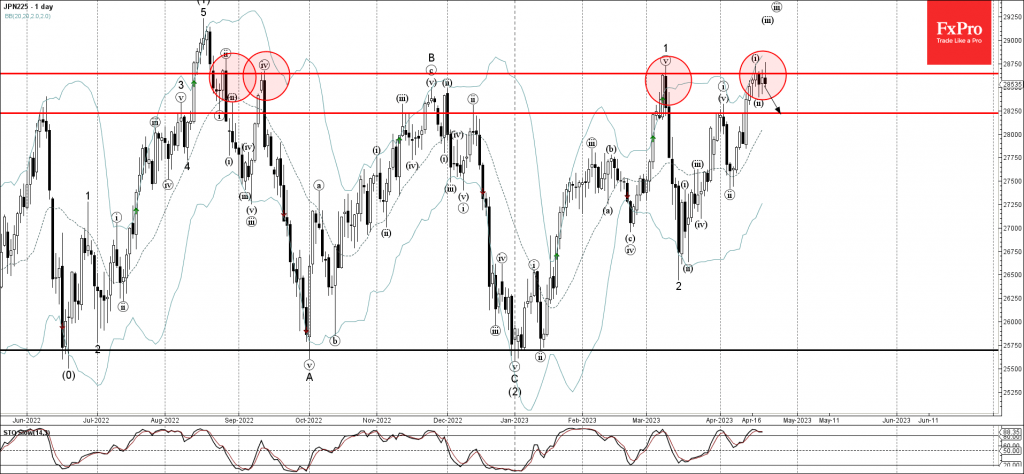

Nikkei 225 Wave Analysis

- Nikkei 225 reversed from resistance level 28645.00

- Likely to fall to support level 28250.00

Nikkei 225 index recently reversed down from the long-term resistance level 28645.00 (which has been steadily reversing the price from August of 2021).

The resistance level 28645.00 was strengthened by the upper daily Bollinger Band.

Given the strength of the resistance level 28645.00 and the overbought daily Stochastic, Nikkei 225 index can be expected to fall further toward the next support level 28250.00.

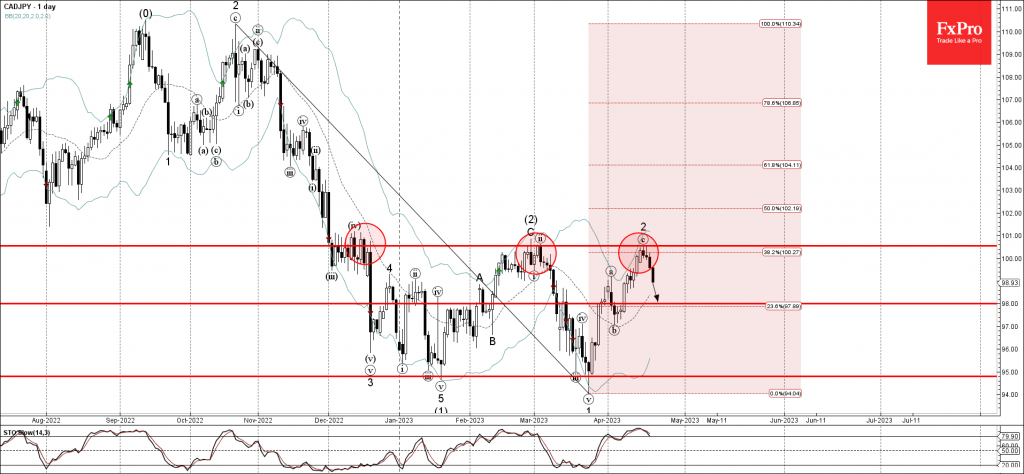

CADJPY Wave Analysis

- CADJPY reversed from resistance level 100.50

- Likely to fall to support level 98.00

CADJPY currency pair recently reversed down from the pivotal resistance level 100.50 (which has been reversing the price from the middle of December) coinciding with the upper daily Bollinger Band and the 38.2% Fibonacci correction of the downward impulse from October.

The downward reversal from the resistance level 100.50 stopped the previous minor ABC correction 2.

Given the strong daily downtrend, CADJPY can be expected to fall further toward the next support level 98.00.

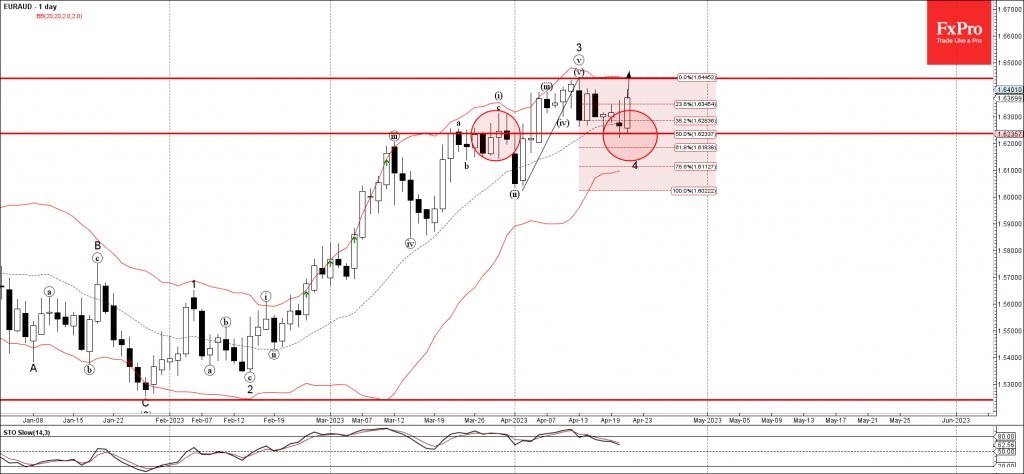

EURAUD Wave Analysis

- EURAUD reversed from support level 1.6235

- Likely to rise to resistance level 1.

EURAUD currency pair recently reversed up from the support level 1.6235 (former resistance from March) coinciding with the 20-day moving average and the 50% Fibonacci correction of the upward impulse from March.

The upward reversal from the support level 1.6235 created the weekly Japanese candlesticks reversal pattern Morning Star.

Given the clear daily uptrend, EURAUD can be expected to rise further toward the next resistance level 1.6440 (top of the previous impulse wave 3).