Sample Category Title

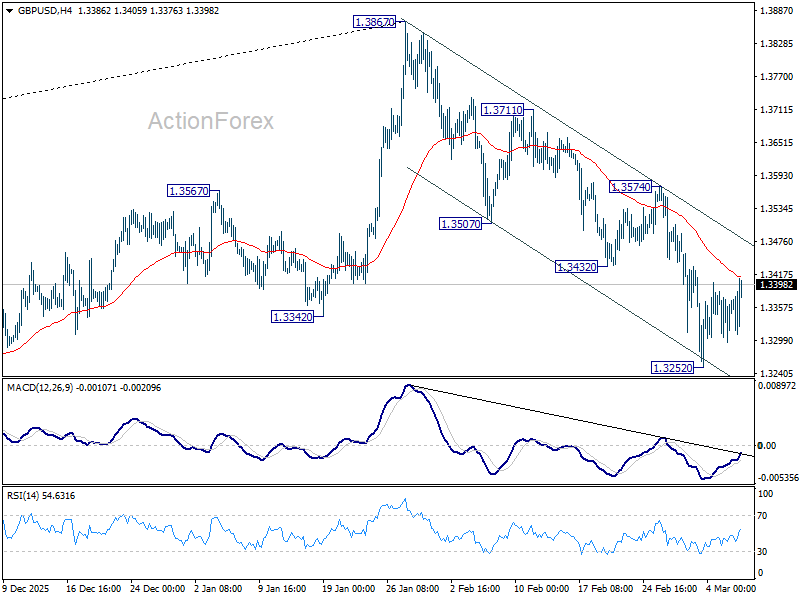

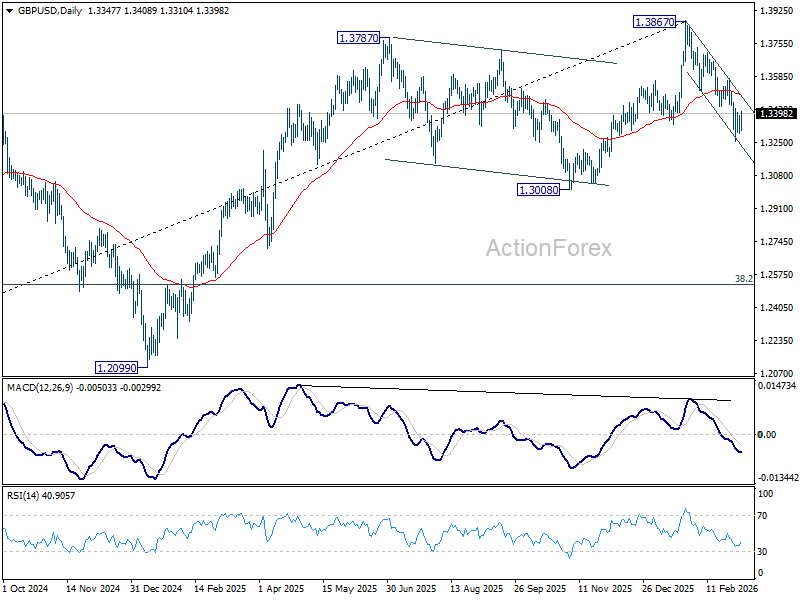

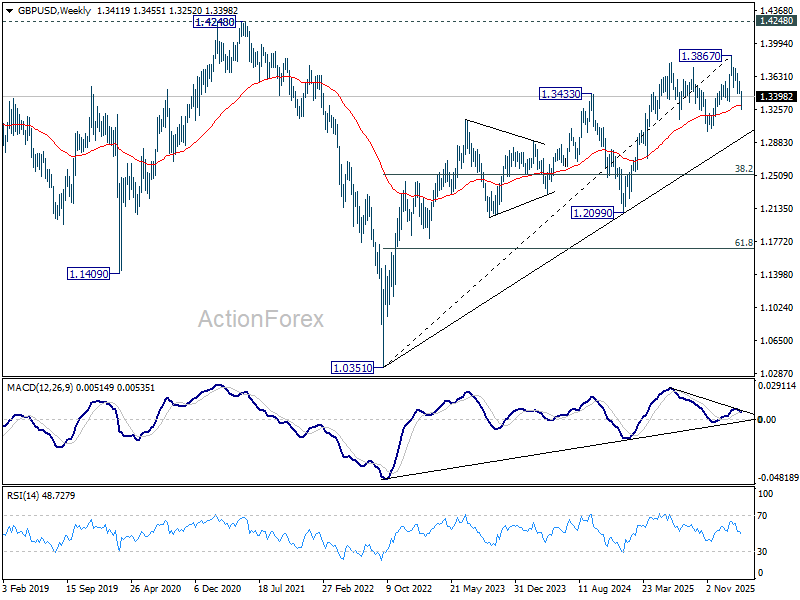

GBP/USD Weekly Outlook

GBP/USD fell to 1.3252 last week but recovered since then. Initial bias remains neutral this week first. Risk will stay on the downside as long as 1.3574 resistance holds, in case of stronger rebound. On the downside, below 1.3252 will extend the fall from 1.3867 to 1.3008 structural support. Decisive break there will carry larger bearish implications.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least corrective the whole rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.0351 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

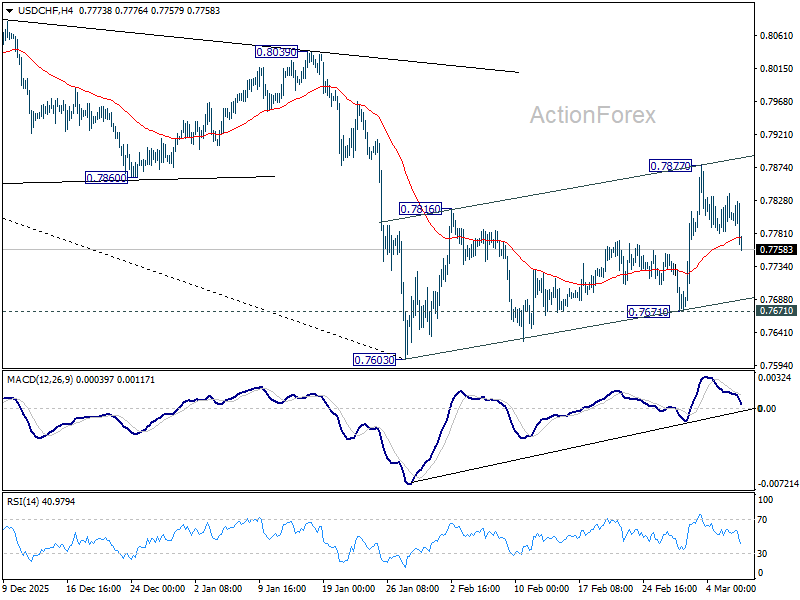

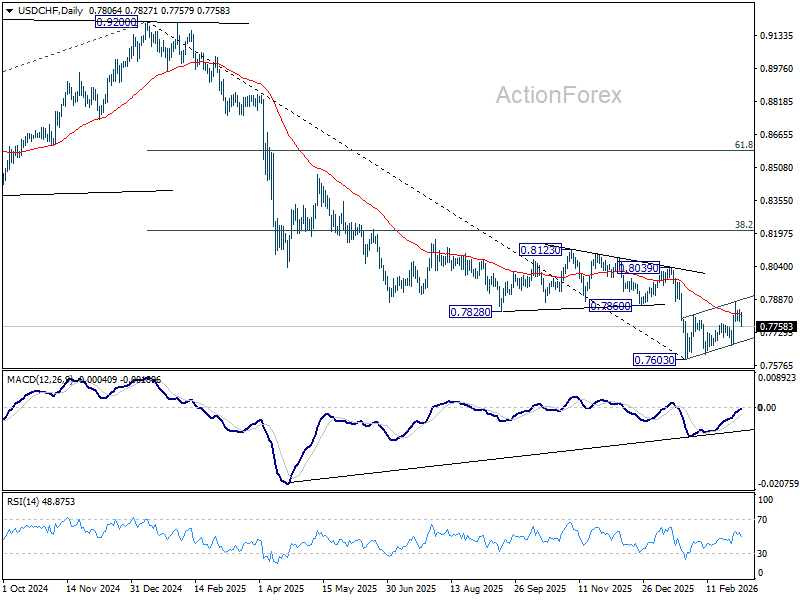

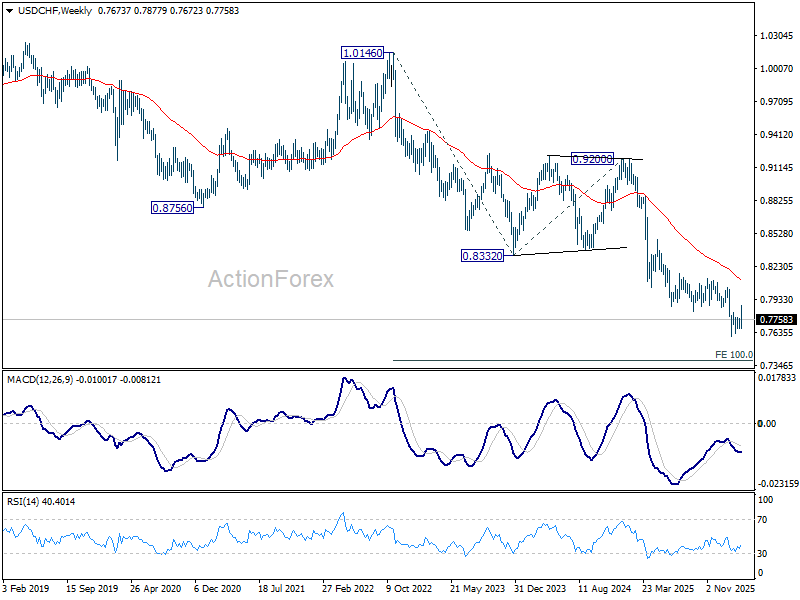

USD/CHF Weekly Outlook

USD/CHF rebounded further to 0.7877 last week but failed to sustain above 55 D EMA (now at 0.7817) and retreated. Initial bias remains neutral this week first. On the downside, break of 0.7671 support will revive near term bearishness and bring retest of 0.7603 low. Decisive break there will resume larger down trend. On the upside, though, break of 0.7877 will bring stronger rally to 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213. However, break of 0.7603 will resume the down trend to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

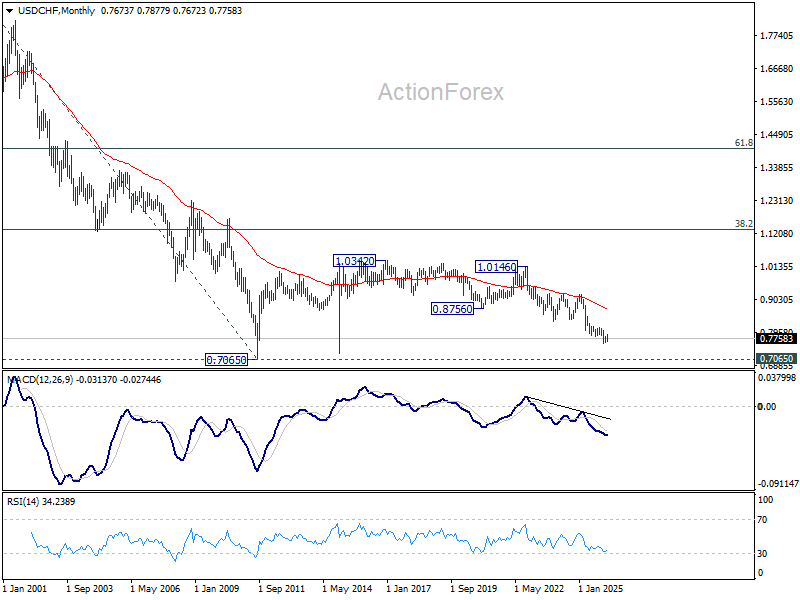

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

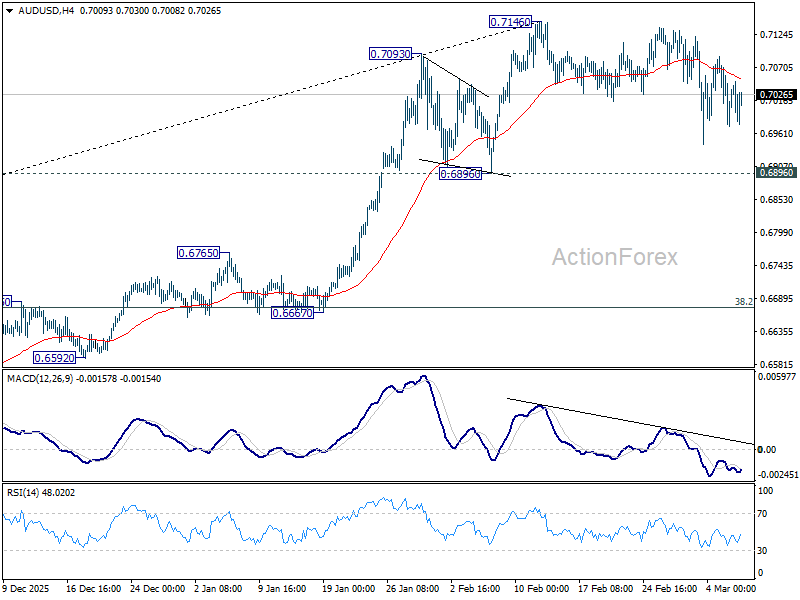

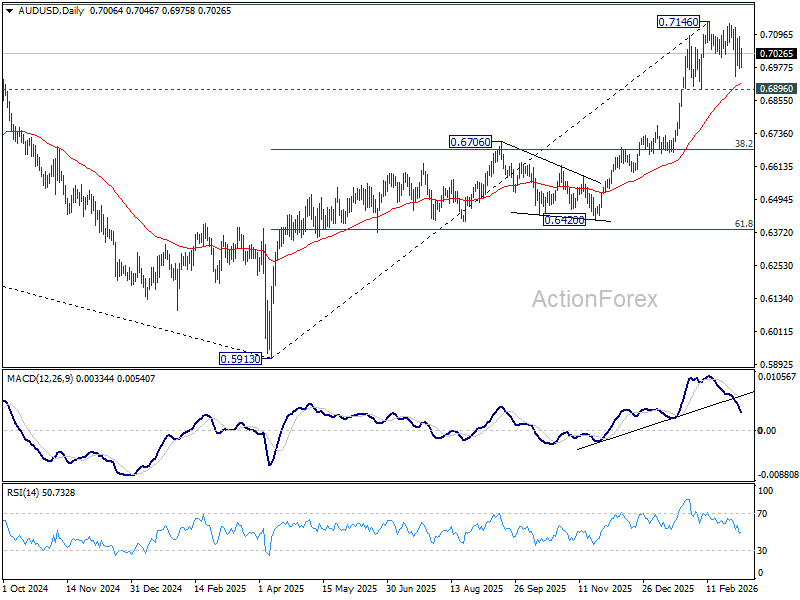

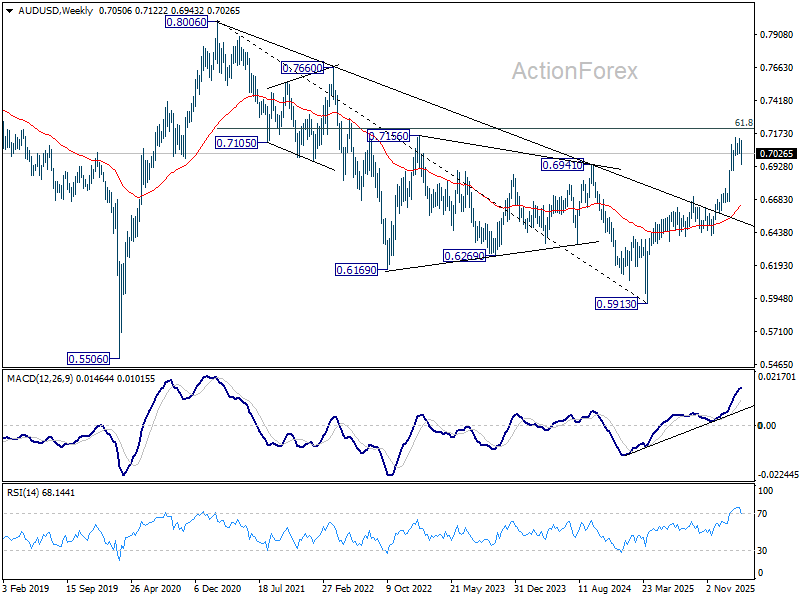

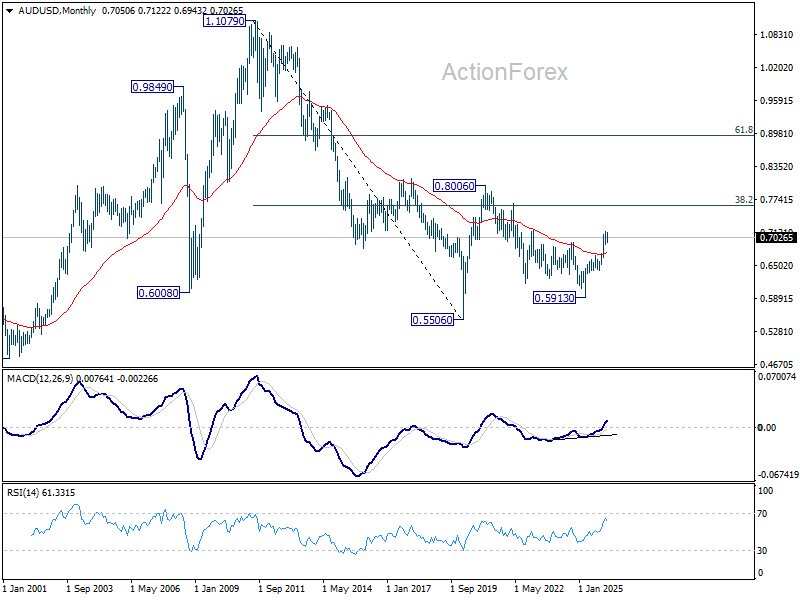

AUD/USD Weekly Report

Despite the intra-week dip, AUD/USD is still holding in range of 0.6896/7146. Initial bias remains neutral this week first. While more consolidations would be seen, outlook stays bullish with 0.6896 support intact. On the upside, break of 0.7146 will resume larger up trend to 0.7206 fibonacci level. However, firm break of 0.6896 will indicate that a larger scale correction is underway, and target 38.2% retracement of 0.5913 to 0.7146 at 0.6675.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above.

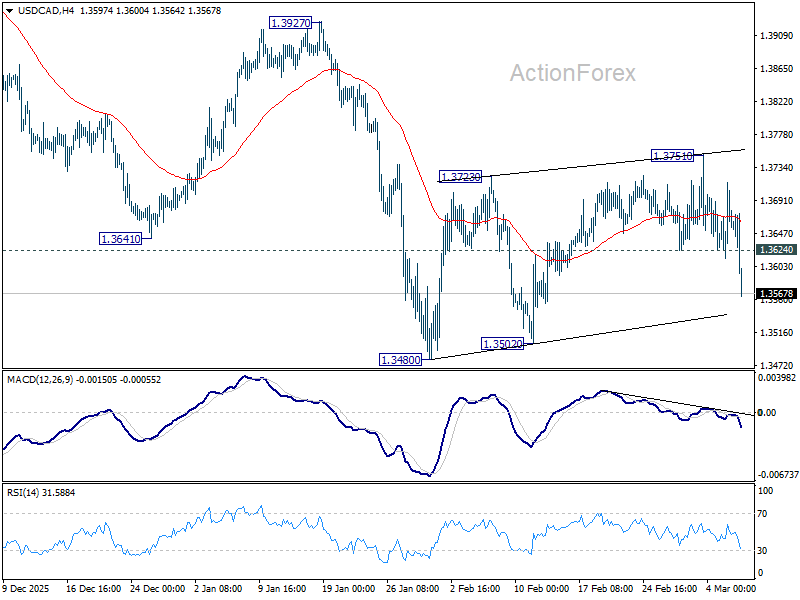

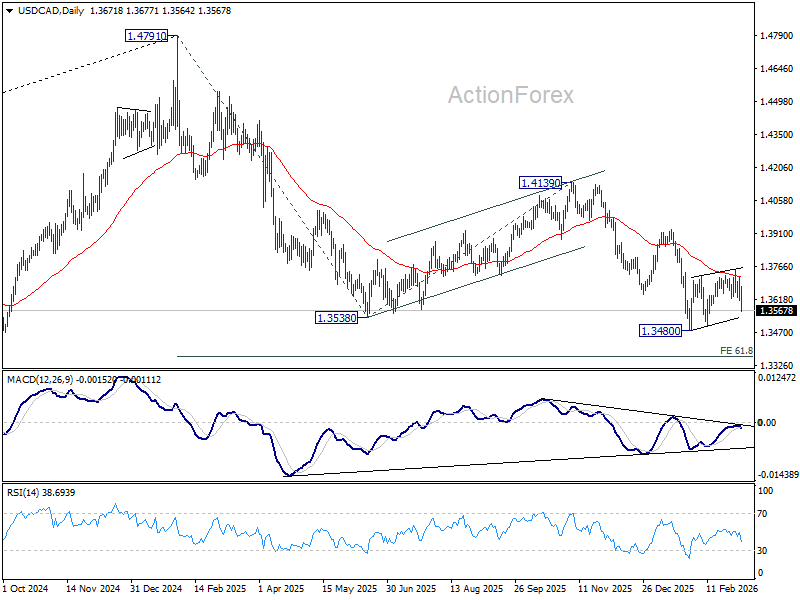

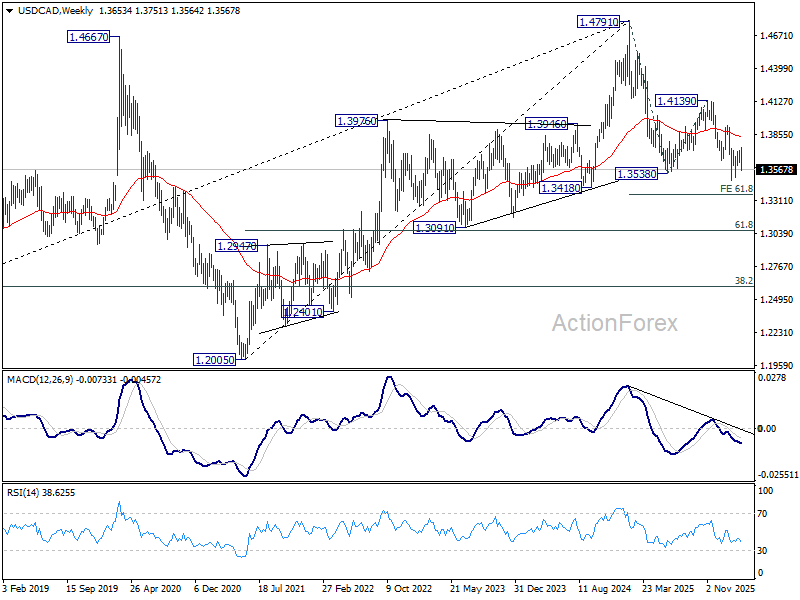

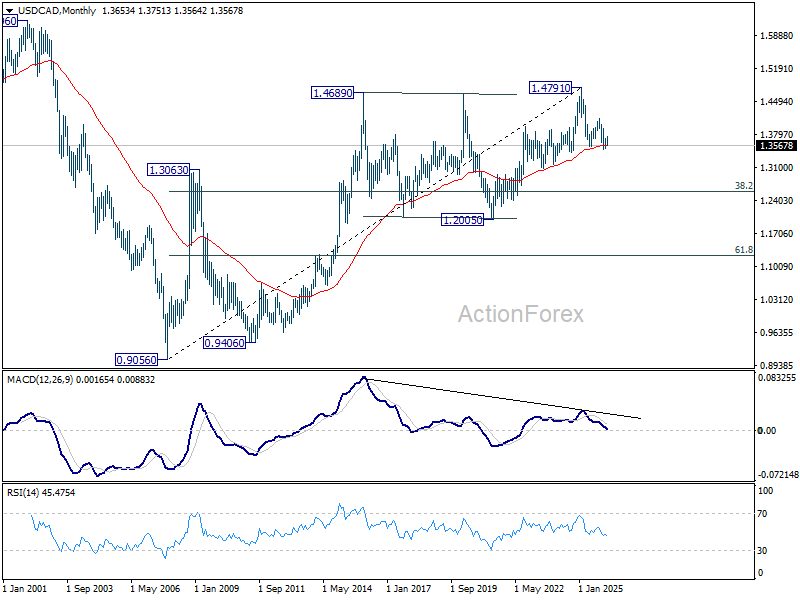

USD/CAD Weekly Outlook

USD/CAD's late decline last week suggests that consolidation pattern from 1.3480 has completed with three waves up to 1.3751, after hitting 55 D EMA (now at 1.3714). Initial bias is back on the downside this week for retesting 1.3480 low first. Firm break there will confirm resumption of whole fall from 1.4791, and target 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. For now, near term outlook will remain bearish as long as 1.3751 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

In the long term picture, rising 55 M EMA (now at 1.3569) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

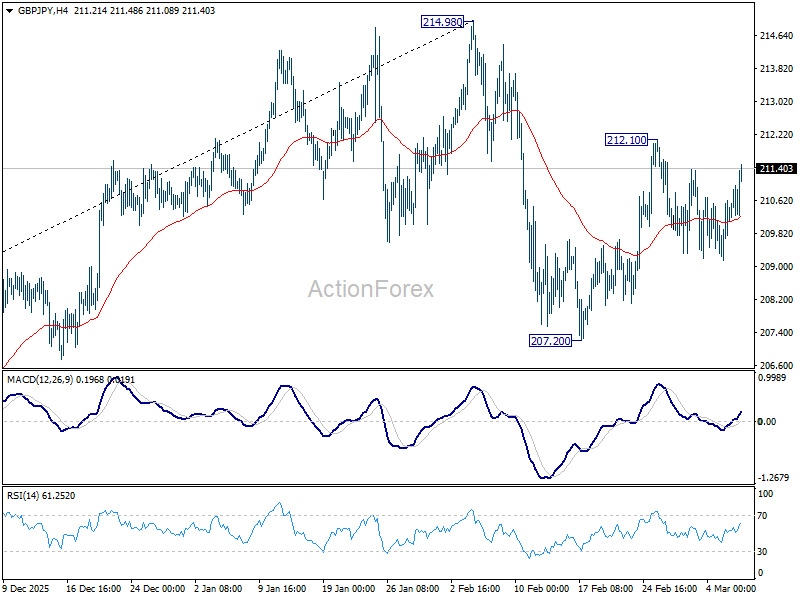

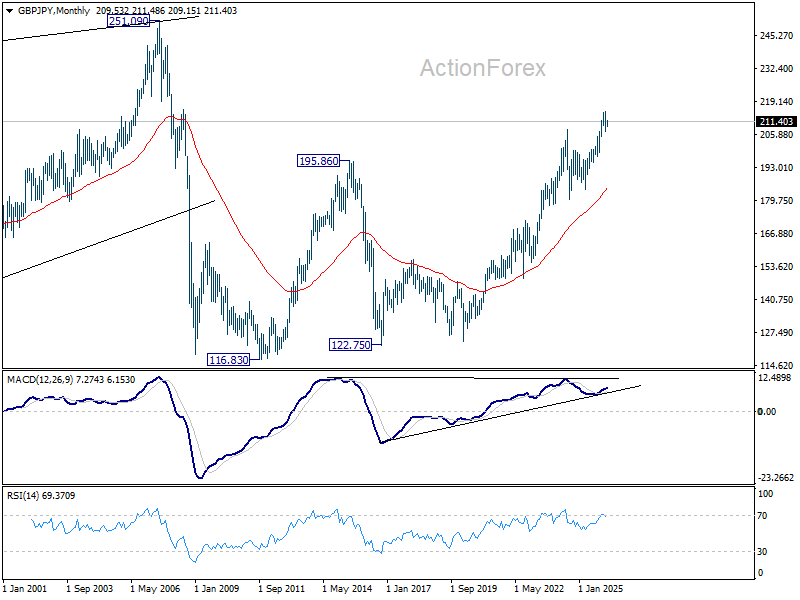

GBP/JPY Weekly Outlook

GBP/JPY gyrated in tight range below 212.10 temporary top last week. Initial bias remains neutral this week first. Overall, price actions from 214.98 are seen as a corrective pattern that could extend further. On the upside, break of 212.10 will resume the rebound from 207.20 to retest 214.98 high. On the downside, though, break of 207.20 will resume the fall from 214.98, to correct whole rally from 184.35.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 201.84) holds, even in case of another deep pullback.

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 184.02) holds.

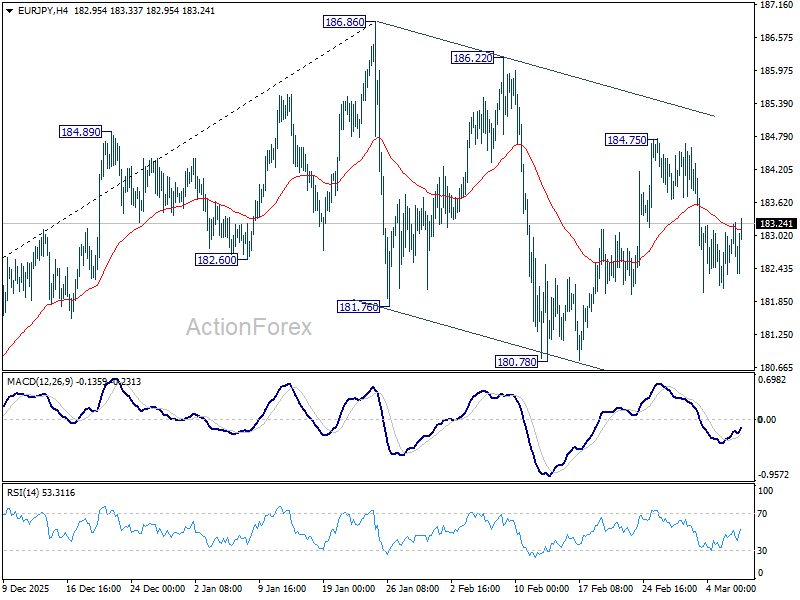

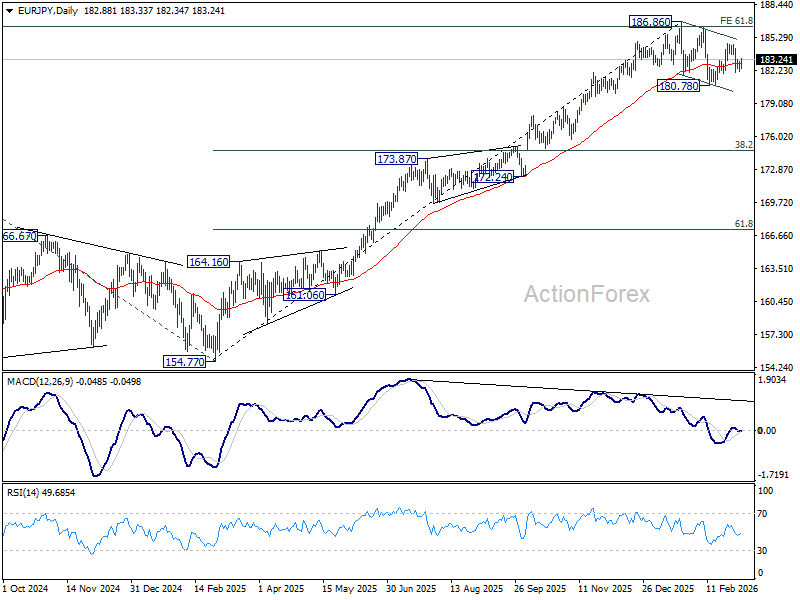

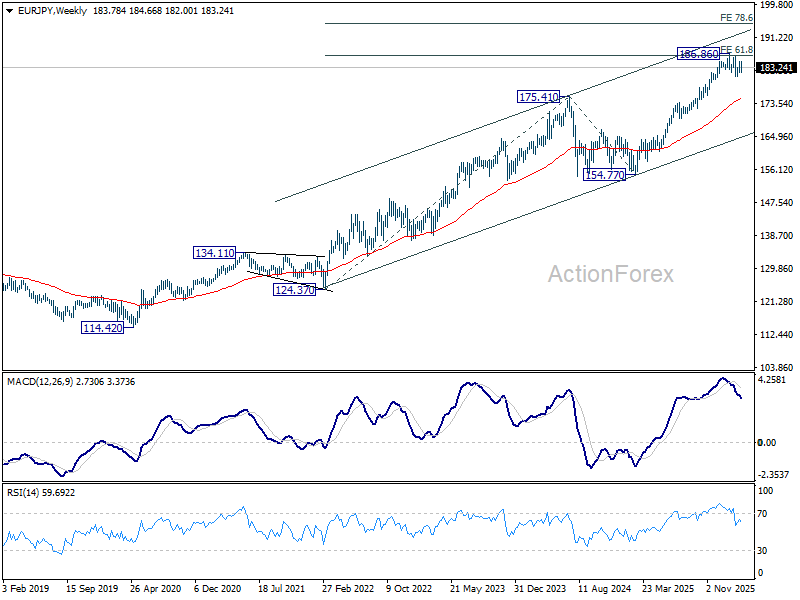

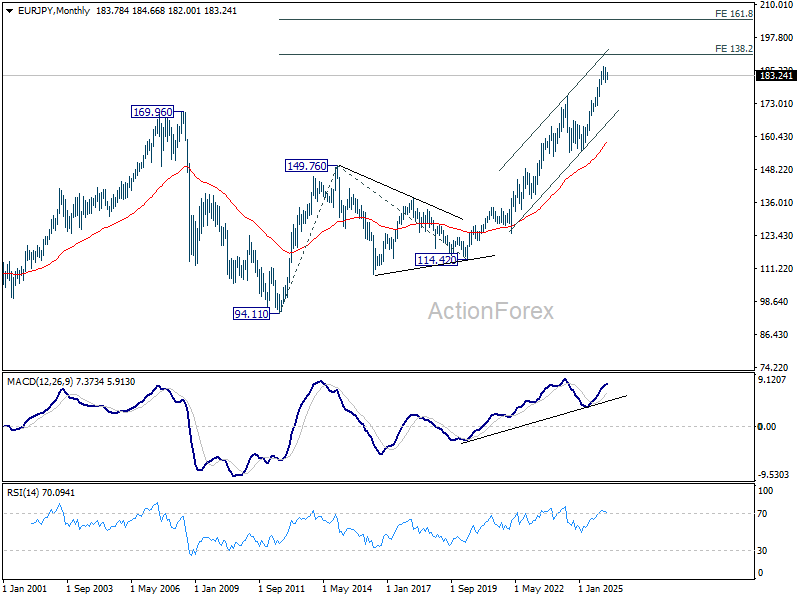

EUR/JPY Weekly Outlook

EUR/JPY dipped notably last week but stayed in range of 180.78/184.75. Initial bias remains neutral this week first. On the downside, firm break of 180.78 support will indicate that fall from 186.86 is already correcting whole up rise from 154.77. Deeper fall should then be seen to 38.2% retracement of 154.77 to 186.86 at 174.60. For now, near term outlook is neutral at best as long as 186.86 holds, or until there is sign of upward acceleration.

In the bigger picture, a medium term top should be in place at 186.86 and some more consolidations could be seen. Nevertheless, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

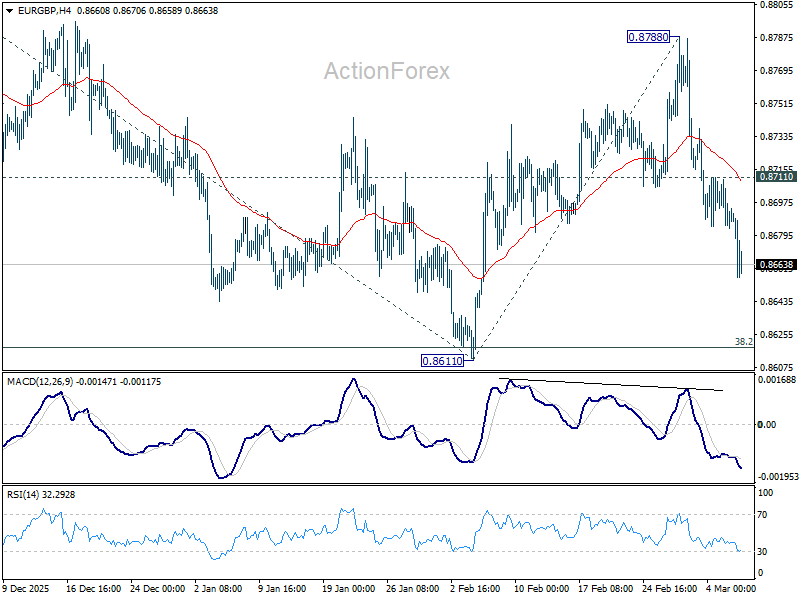

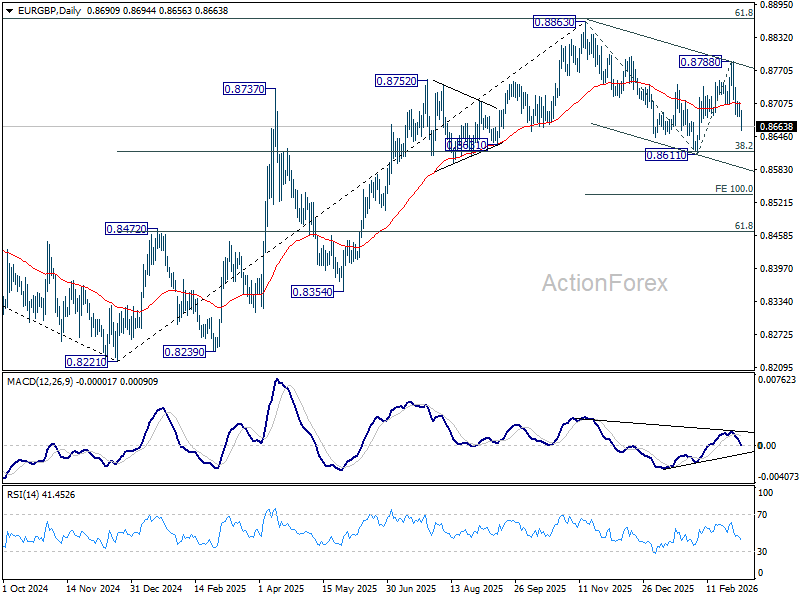

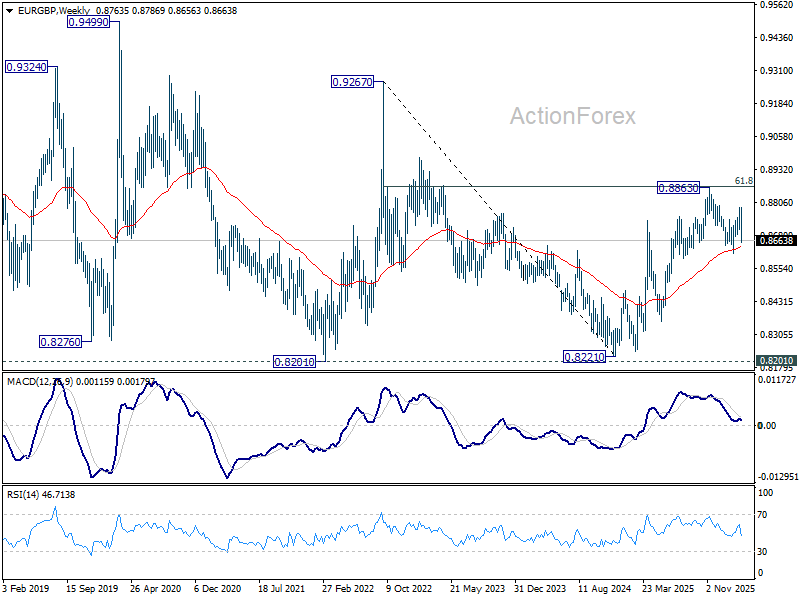

EUR/GBP Weekly Outlook

EUR/GBP's extended decline last week suggests that rebound from 0.8611 has already completed at 0.8788. Initial bias stays on the downside this week for retesting 0.8611 first. Firm break there will resume the whole fall from 0.8863. Next target is 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536. On the upside, above 0.8711 minor resistance will turn intraday bias neutral again first.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

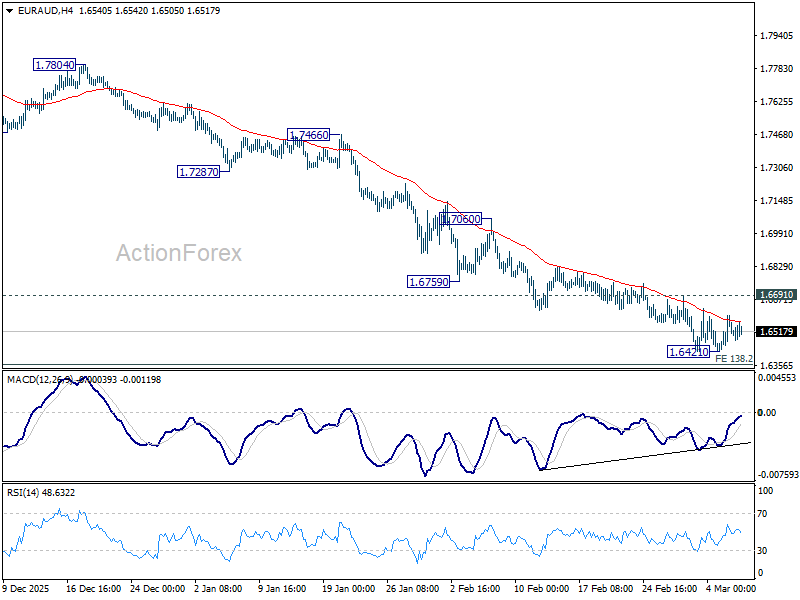

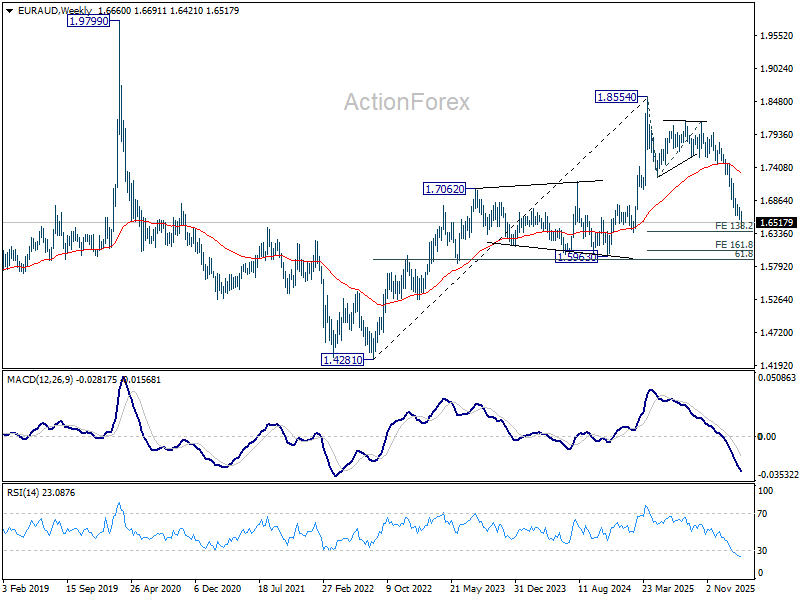

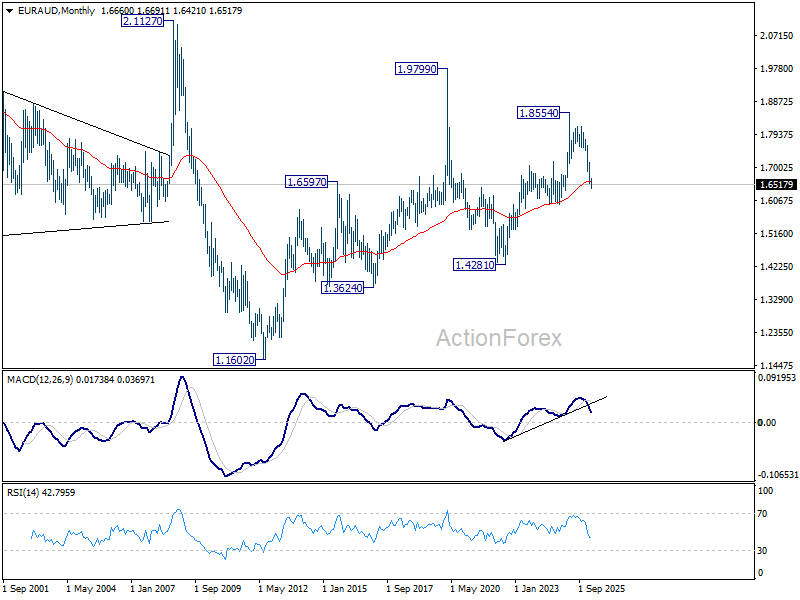

EUR/AUD Weekly Outlook

EUR/AUD edged lower to 1.6421 last week but recovered. Initial bias remains neutral this week first. On the downside, sustained break of 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351 will extend larger down trend to 161.8% projection at 1.6042 next. However, considering bullish convergence condition in 4H MACD, firm break of 1.6691 resistance will indicate short term bottoming. Intraday bias will be back on the upside for stronger rebound towards 55 D EMA (now at 1.6979).

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Current development argue that it has already completed at 1.8554. Sustained trading below 55 M EMA (now at 1.6603) will confirm this bearish case, and pave the way back towards 1.4281.

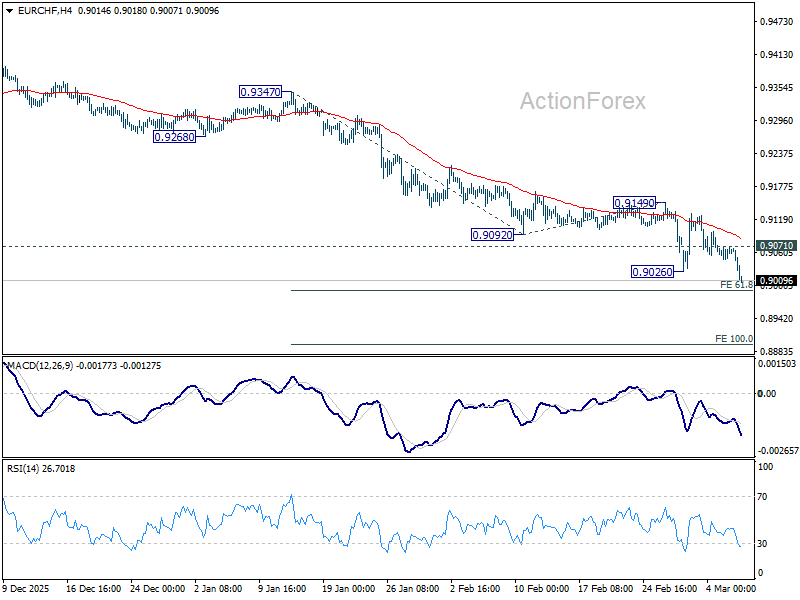

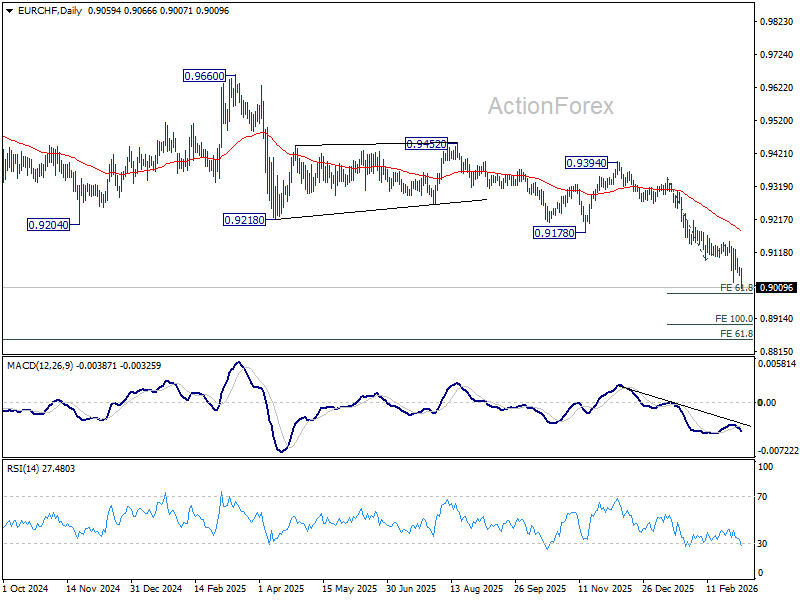

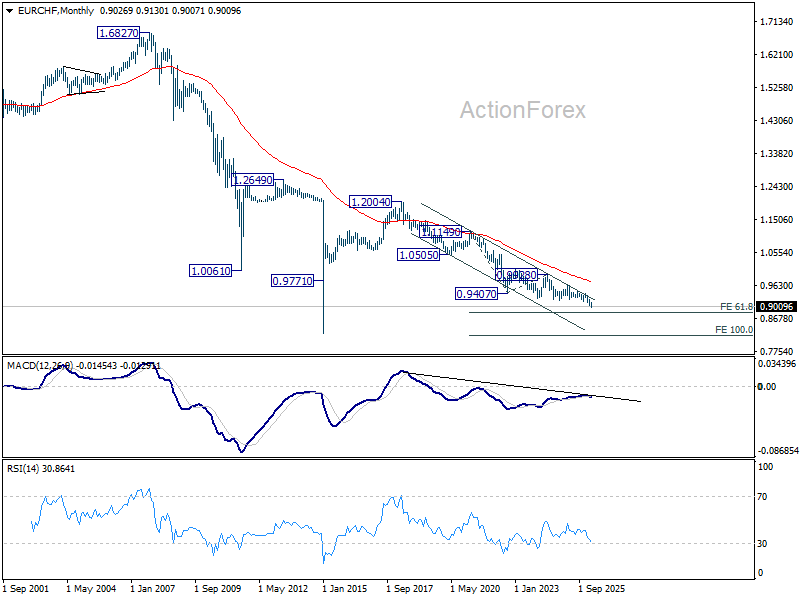

EUR/CHF Weekly Outlook

The brief initial recovery in EUR/CHF didn't last long as down trend resumed towards the end of the week by breaking through 0.9026 temporary low. Initial bias is back on the downside this week for 61.8% projection of 0.9347 to 0.9092 from 0.9149 at 0.8991. Firm break there will pave the way to 100% projection at 0.8894. ON the upside, above 0.9071 resistance will turn intraday bias neutral again first. But outlook will remain bearish as long as 0.9149 resistance holds.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

In the long term picture, EUR/CHF is also holding well inside long term falling trend channel. Down trend from 1.2004 (2018 high) is still in progress. Outlook will continue to stay bearish as long as falling 55 M EMA (now at 0.9739) holds.

Markets Weekly Outlook – Geopolitics Overpower Fundamentals: The $150 Oil Warning and Rate Cut

Week in review

- Escalating Middle East conflict and disruptions in the Strait of Hormuz have pushed Brent crude to $90 a barrel, raising fears of oil hitting $150.

- A surprising contraction in the US labor market (unexpected job losses in February and unemployment at 4.4%) has increased the chance of a June or July interest rate cut by the Fed.

- US markets show more resilience, supported by the tech sector and net oil exporter status, while Europe faces a potential "stagflationary shock" due to its vulnerability to energy price spikes

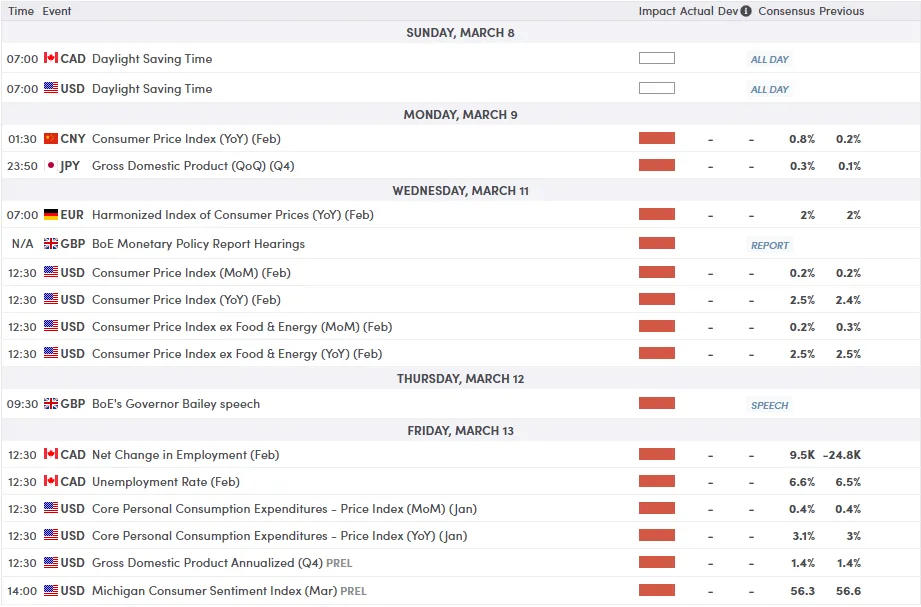

- The week ahead is dominated by geopolitics, but major economic releases include US CPI and Core PCE for insights into inflation's "stickiness," and a significant upward revision expected for Japan's Q4 2025 GDP.

Wall Street’s primary indexes tumbled on Friday, led by a sharp decline in the Dow to a three-month low as the market grappled with escalating conflict in the Middle East and a surprising contraction in the US labor market.

Data revealed the economy unexpectedly lost jobs in February,exacerbated by healthcare strikes and severe winter weather pushing the unemployment rate up to 4.4%.

This combination of geopolitical tension and economic cooling has shifted market expectations; traders have now priced in a roughly 50% chance of a June interest rate cut, while some analysts suggest the Fed’s dual mandate to balance inflation and employment could pull the first cut forward to July.

The volatility is being fueled by a dramatic spike in energy prices, with Brent crude hitting $90 a barrel following disruptions in the Strait of Hormuz. As shipping halts and analysts warn that oil could reach $150 a barrel if Gulf exports are fully suspended, airline stocks have plummeted nearly 13% this week.

Qatar’s recent warnings regarding prolonged delivery delays for natural gas have only added to the "stagflation" fears, a situation where growth slows while prices rise.

Despite the downturn, US markets have shown more resilience than their global counterparts, buoyed by a strong tech sector and the nation's status as a net oil exporter.

In contrast, European markets suffered their worst week in nearly a year, with the STOXX 600 hitting a two-month low. Because Europe is more vulnerable to energy price shocks, major exchanges in Frankfurt, Paris, and Madrid recorded historic weekly losses as investors braced for a potential stagflationary environment across the continent.

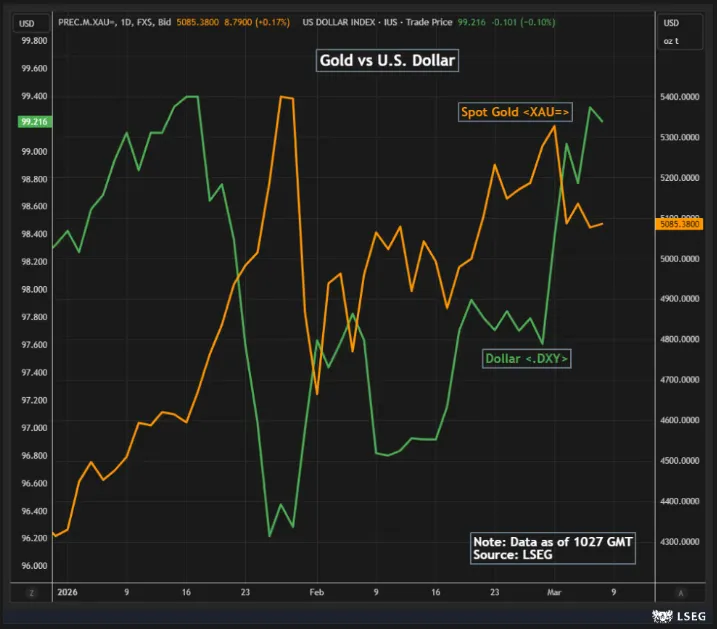

Gold prices edged higher on Friday as escalating tensions in the Middle East sparked a wave of safe-haven buying.

Spot gold rose 0.3% to $5,090.16 per ounce, while US gold futures for April delivery climbed 0.4% to $5,099.50. Despite these daily gains, the metal remained on track for a 3.5% weekly decline, effectively snapping a four-week winning streak.

This downward pressure stemmed from persistent inflation worries and a volatile dollar, both of which have dampened investor expectations for imminent interest rate cuts.

Source: LSEG

The broader commodities market showed a stark contrast, as crude oil prices surged toward their most significant weekly gain since the 2022 invasion of Ukraine.

Spot WTI oil was up around 34% at the time of writing.

While gold benefited slightly from its status as a refuge during geopolitical instability, the reality of "higher-for-longer" interest rates continues to weigh on bullion's appeal compared to yield-bearing assets.

The Week Ahead

Global markets enter the second week of March 2026 under the shadow of a rapidly escalating Middle East conflict. With a US-led campaign against Iran entering its second week and shipping through the Strait of Hormuz at a standstill, the "2022 Energy Shock" is no longer just a historical reference, it is the primary lens through which investors are viewing the week ahead.

The Macro Theme: Geopolitics Overpowers Fundamentals

While the economic calendar is packed with heavy hitters like US CPI and UK GDP, their influence may be dampened by the "high-risk zone" of current geopolitics.

- Energy Prices as the Barometer: Brent crude has already surged toward $85/bbl. Analysts warn that a breach of $100/bbl would be a "psychological milestone" that could trigger a deeper sell-off in risk assets.

- 2022 vs. 2026: There does appear to be a critical difference from the 2022 shock: the labor market is now much cooler. Unlike 2022, when workers could chase higher pay to offset energy costs, the current cooling trend (highlighted by a weak February US jobs report) means consumers have less of a buffer.

United States: The Inflation-Rate Cut Tug-of-War

The spotlight is firmly on the US Consumer Price Index (CPI) due Wednesday and Core PCE on Friday.

The Dilemma: Markets are looking for signs of how "sticky" inflation remains before the full impact of the current energy spike is even recorded. A surprise upside in CPI would likely force markets to price out the two Fed rate cuts currently expected for 2026.

Consumer Sentiment: Friday’s University of Michigan survey will be the first real-time look at how the "energy shock" and tariff fears are sapping household confidence.

Asia: China’s "Two Sessions" and Japan’s GDP Revision

Asia remains at the forefront of the supply chain disruption, with a specific focus on the closing of China’s National People’s Congress.

- China (Monday/Tuesday): February CPI and PPI data will be released. Analysts expect a bounce in CPI to ~1.0% due to Lunar New Year spending, though this may be viewed as a "noise" rather than a trend. Trade data (Tuesday) will be scrutinized for the resilience of external demand.

- Japan (Tuesday): Expect a significant upward revision to Q4 2025 GDP (from 0.1% to 0.3% QoQ) following strong capital spending and winter bonuses. This could keep the Bank of Japan on its path toward normalization despite global turmoil.

Europe & UK: Looking for Signs of Life

The Eurozone is navigating a "stagflationary shock" where energy deficits punish the Euro, though narrowing interest rate differentials against the USD are providing some support.

- Germany (Monday/Wednesday): Industrial Production and final Inflation data will show if the "fledgling recovery" in manufacturing can withstand the new energy spike.

United Kingdom (Friday): Monthly GDP and industrial output for January will be released. Markets are looking for a pickup in growth to confirm the encouraging signals seen in recent PMI surveys.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the week - WTI Oil

From a technical standpoint, WTI has just posted a massive bullish engulfing candle which has completely invalidated the previous multi-year downtrend, thrusting WTI from the mid-$60s to over $90.00 in a matter of days.

The move as is largely the case was driven by the geopolitical and fundamental dynamics around Oil prices. However, it is important to note that were thechnical signs that Oil was in a consolidation phase with a breakout growing ever-more likley.

Nobody however envisioned a 30% + price spike in the space of a week.

Where does price go to from here?

This will of course depend on the course the war in the Middle East takes.

Further refinery attacks by Iran or any escalation on that front and we could open the new week already above the $100/barrel mark.

Alternatively, if tensions do begin to ease, Oil prices may fall quite quickly.

The price is currently testing the $90.05 level. If the momentum continues, the next major psychological and technical targets are $93.96 and the multi-year high at $100.00.

In the event of a "cool-off," the previous resistance at $80.19 and the 200-day SMA ($75.41) now serve as the primary floor.

There is a significant liquidity gap between $70 and $85. In normal market conditions, these gaps tend to fill, but in "war-premium" markets, they can remain open for weeks.

WTI Oil Weekly Chart, March 6, 2026

Source:TradingView.Com (click to enlarge)