Sample Category Title

The Weekly Bottom Line: Oil’s Well… Until it Isn’t

Canadian Highlights

- Escalating conflict in the Middle East has sent oil prices parabolic. Major disruptions at the Strait of Hormuz leaves the near-term price outlook highly uncertain.

- Higher oil prices are a short-term boost for Canada’s energy sector and public revenues, but are already hitting consumers, with national gasoline prices up sharply on the week.

- The limited Canadian data this week was soft. Preliminary home sales data for February flatlined while Q4 productivity edged lower.

U.S. Highlights

- Global equity markets sold off this week, while energy prices pushed meaningfully higher following the United States and Israel’s strikes on Iran.

- Despite this week’s sharp move in oil prices, the impact to the U.S. economy remains relatively small, but that assumes the conflict is short-lived.

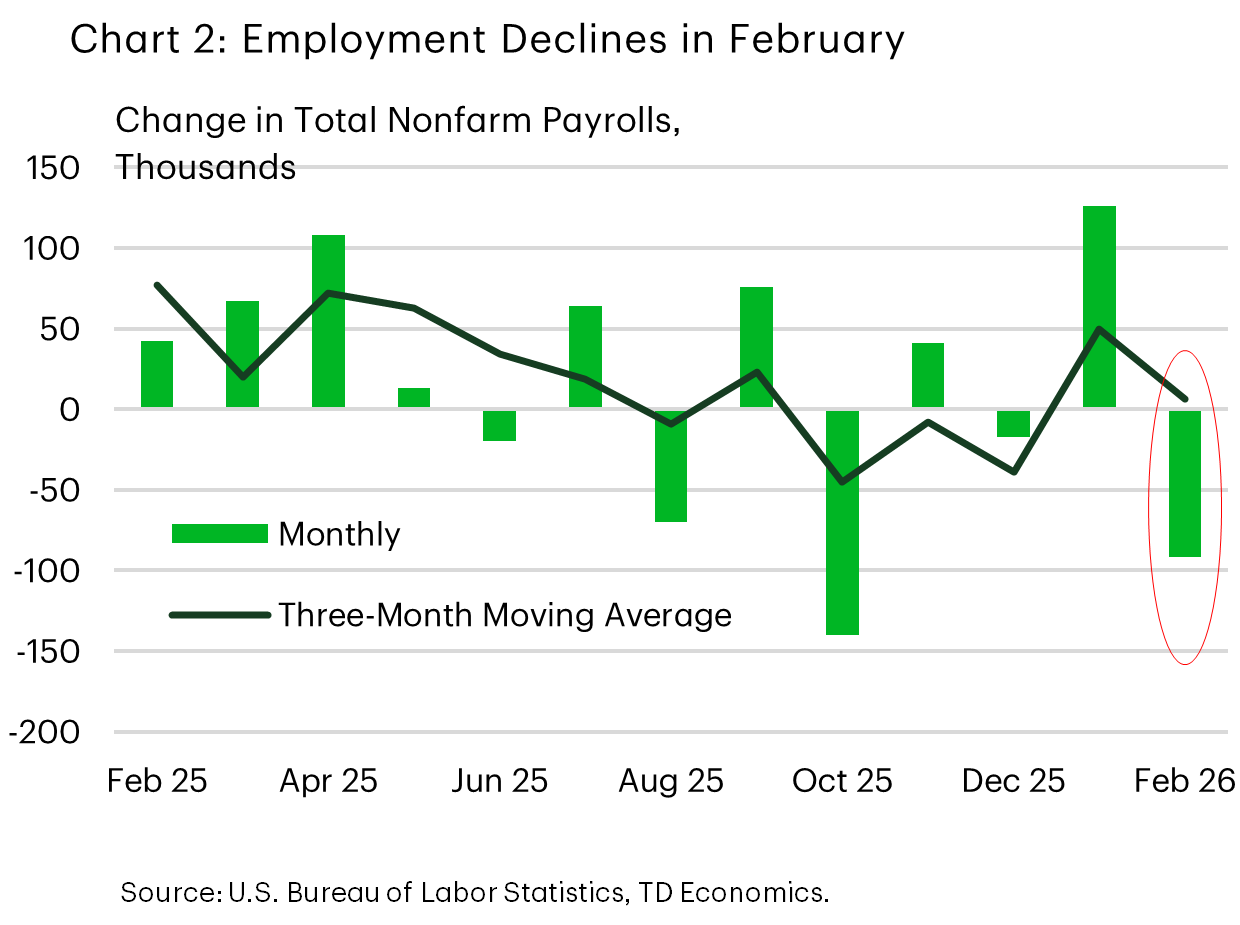

- The February employment report came in on the softer side, with hiring declining and the unemployment rate ticking higher.

Canada – Oil’s Well... Until it Isn’t

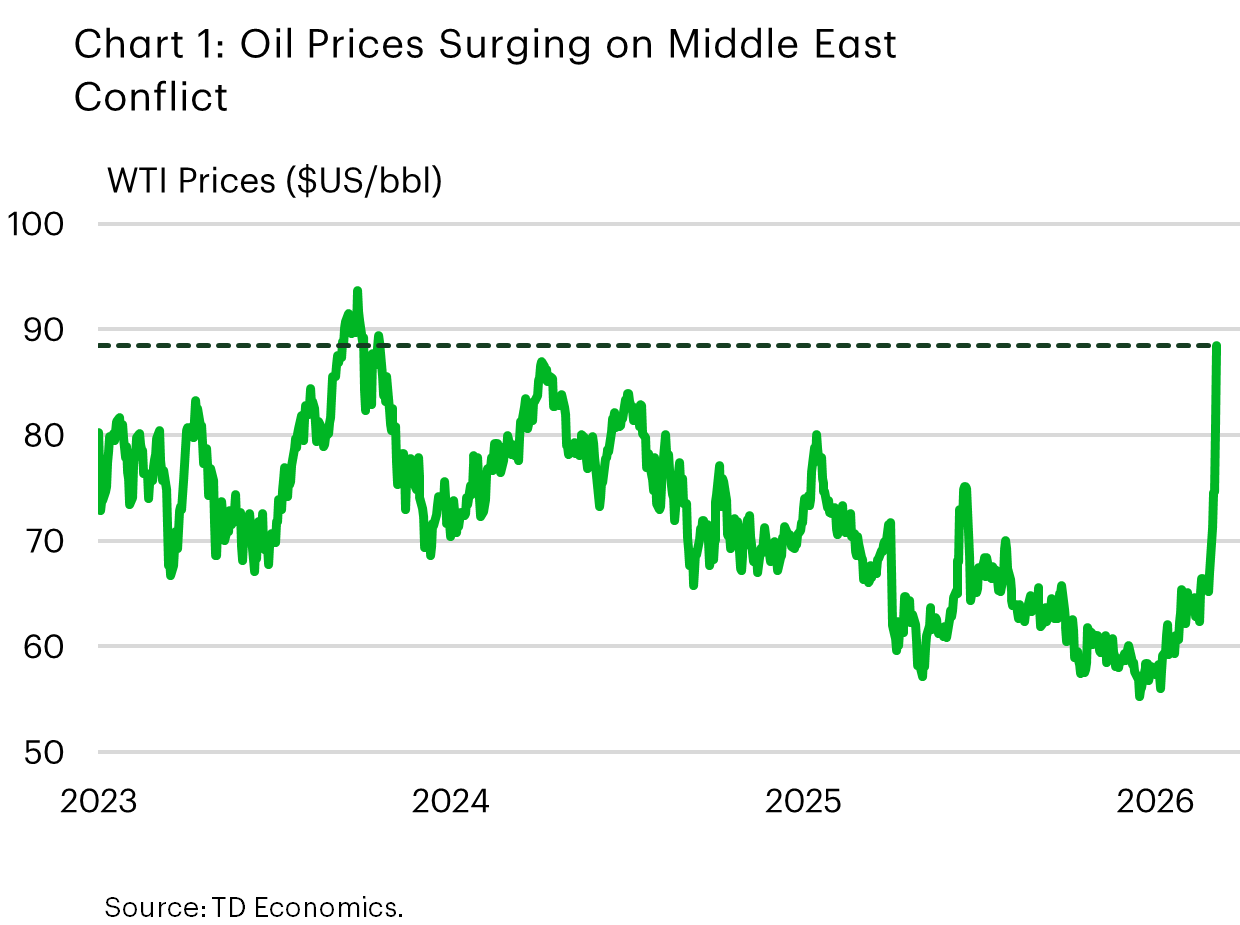

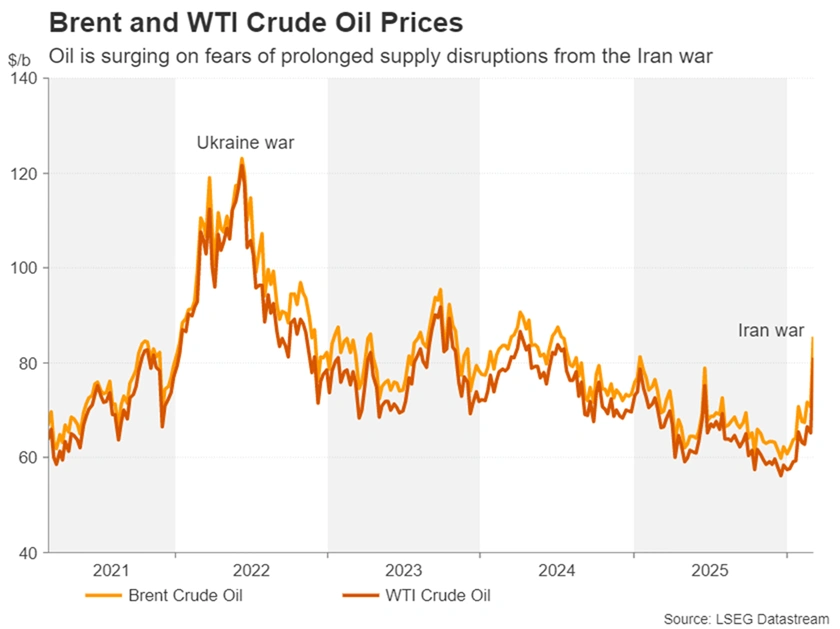

Escalating conflict in the Middle East dominated headlines this week. WTI oil prices surged an eye-watering 30% since last Friday to over $89/bbl – it’s highest level since late-2023, but changing by the minute (Chart 1). The key concern is the Strait of Hormuz, a choke point for 20% of global oil supply. At the time of writing, oil is not being transported through the Strait, and major Gulf producers are approaching storage limits, forcing them to make difficult decisions about near-term production. So far Iraq and Kuwait have started ratcheting back production, with Saudi Arabia and the UAE expected to start cutting soon.

Oil price forecasts are highly uncertain at this time. For now, we anticipate prices will stay elevated near current levels for the month of March, before very gradually easing in the months following. Risk premiums are assumed to stay high as the current episode is widely viewed as the most significant threat to Middle East energy supply in several years. A worst-case scenario could see prices breach $100/bbl should more oil supply go offline for longer and major infrastructure is damaged. We chart out some macroeconomic implications (here).

Canadian energy stocks caught a bid this week, though broader volatility pulled the TSX down 2%. Markets also began pricing higher inflation expectations into bonds, pushing 2 and 10-year Canada yields up around 20 basis points (bps) on the week. For Canada, rising oil prices are seen as a tailwind to energy producers’ revenues and government coffers. The downside is that Canadians are starting to see increased prices at the pumps. The national average price for gasoline has jumped 12 cents per litre (an almost 10% gain) this week, with further moves higher likely on the way.

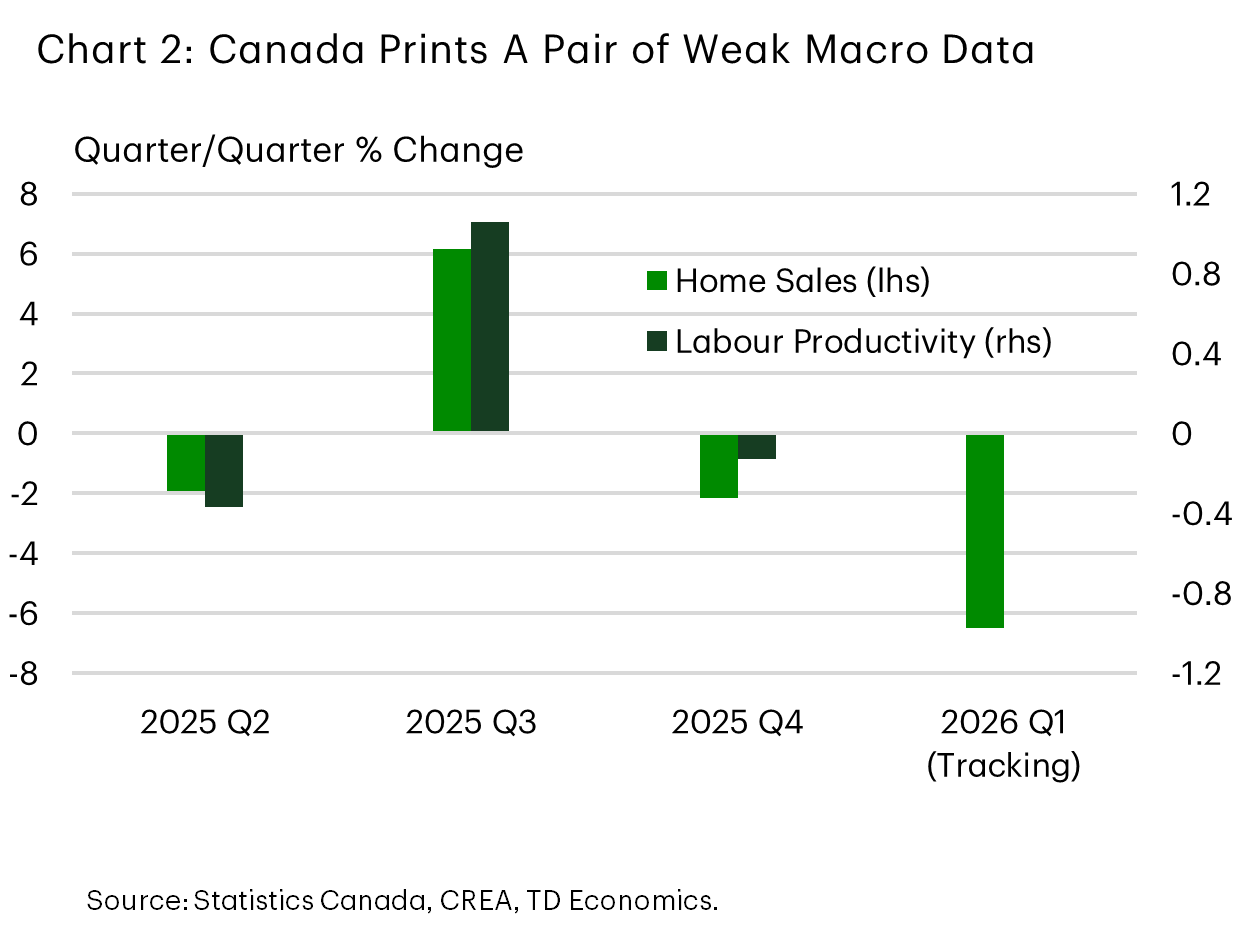

Outside of geopolitical events, Canadian data was light (Chart 2). A pulse check on Canadian housing markets via preliminary sales data for February showed a minimal bounce back in home sales after a dismal performance in January. Though sales gains edged higher in major B.C. and Quebec markets, a pullback in Toronto largely offset these gains. Elsewhere, Canadian productivity slipped in the fourth quarter, putting overall productivity growth in 2025 up a modest 1.1%. The data reinforces that Canada’s productivity problem is structural and will take time to see material improvements.

Meanwhile, Prime Minister Carney continued his quest to bolster trade relations with global trading partners. In a trip to India this week, Canada finalized a $2.6 billion uranium supply agreement, with product to be delivered between 2027-2035. Assuming shipments are evenly distributed through the trade deal horizon (~280 million/year), this would bump Canada’s total uranium shipments up by almost 10% annually. Nominally, the deal represents a very modest portion of Canada’s overall trade portfolio, but it is expected to have positive regional impacts for Saskatchewan, with Cameco serves as the principal supplier.

U.S. – Epic Fury Sends Shockwaves Through Financial Markets

The United States and Israel launched coordinated strikes on Iran over the weekend, prompting retaliatory counterattacks across other countries in the Middle East. On Monday, Iran announced that it would attack tanker ships passing through the Strait of Hormuz – a crucial choke point for 20% of global oil supply. Based on satellite imagery, shipping through the passage has effectively come to a halt. Energy prices pushed meaningfully higher this week, with WTI up roughly 33% (or $18per-barrel) and currently sits just north of $88 – its highest level since September 2023. U.S. equities were under pressure for most of the week, with February’s softer employment report adding further insult to injury on Friday. The S&P 500 looks to end the week down over 2%. Meanwhile, Treasury yields across the curve were about 20 basis points higher, as market participants pushed out the timing of expected rate cuts amid fears that higher oil prices will add further upward pressure to inflation.

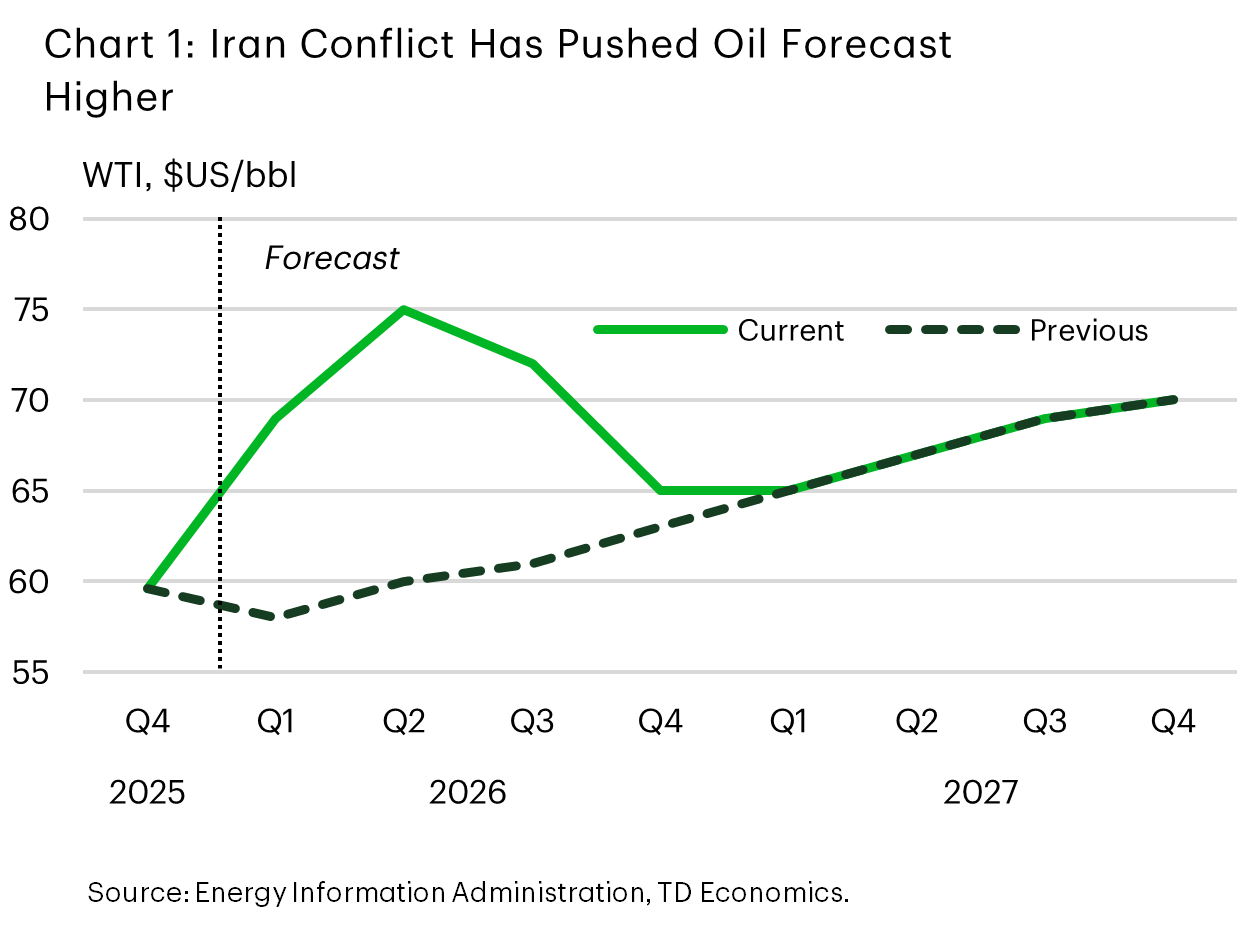

Despite the sharp move in oil prices, the impact to U.S. economy (so far) remains relatively small. In large part, that’s because the U.S. is now a small net exporter of oil, so energy shocks don’t pack the same punch that they used to. Case in point: we’ve marked-to-market our oil forecast, and the upgrade (shown in Chart 1) only shaves about a tenth of a percentage point from 2026 GDP growth – barely moving the needle considering our forecast of 2.7%.

But to say that uncertainty is elevated at the moment would be an understatement. President Trump and other administration senior officials have said this week that the conflict could drag on for at least another several weeks. This suggests further upside to oil prices over the near term, particularly if oil supplies were to remain choked off indefinitely.

From the Federal Reserve’s perspective, economic theory would tell us that policymakers should “look through” the energy shock given its supply driven nature. But because the jump in oil prices is coming atop already elevated inflationary pressures, Fed officials are likely to keep a close eye on inflation expectations. So far, market-based measures have remained well anchored, but there is a risk that they could start to drift higher, particularly if the conflict were to drag on.

The further upside risk to the inflation outlook comes at a time when market participants have started to question the labor market narrative. Nonfarm employment unexpectedly declined in February (Chart 2), while the unemployment rate ticked up to 4.4%. On the surface, the employment report looked very weak, but there were a few factors including a strike and potential weather-related impacts that contributed to at least some of last month’s pullback. We feel it’s still too early to upend our prior thinking of the labor market – but it certainly underscores that current conditions are far from perfect. At the moment, the greater threat to the Fed’s dual mandate is price stability. That is reflected in market participants having pushed out the timing of next rate cut until September and are only 80% priced for a second cut.

International Week Ahead—March 6, 2026

International Week Ahead

- Canada Labor Force Survey: Trade-Related Sectors Likely to Remain a Drag

- Canada Manufacturing Sales: Weak January Print After a Robust December Increase

- U.K. Monthly GDP: Strong Momentum to Start the Year

- Mexico CPI: Oil Price Shock Makes Banxico's Inflation Outlook More Challenging

- India CPI: RBI Now Firmly on Hold, Balance of Risk Shifts to Hikes

- Brazil CPI: Our Less Dovish BCB Outlook Slowly Being Priced into Financial Markets

- China Activity: Downside Risks to China GDP are Starting to Take Shape

G10

Canada Labor Force Survey • (3/13)

Trade-Related Sectors Likely to Remain a Drag

Canada’s labor market data for February is likely to show a modestly weakening job market, with pain concentrated in trade-centric sectors. For now, much of this has been felt in manufacturing, but is likely to spread to transportation. The Business Outlook Survey for Q4-2025 continues show weak hiring intentions and lack of labor shortages, consistent with falling job vacancies. We look for headline employment to come in at -10K and for the unemployment rate to tick higher, to 6.6%. The sharp decline in labor force participation in January is unlikely to be repeated. However, population growth has slowed markedly in recent months—falling from 3% in 2023/24 to 0.9% in 2024/25. This, along with the medium-term downtrend in labor force demographics on an aging population, implies a very low level of job growth (and even slight job loss) could keep the unemployment rate stable. As such, given these structural shifts, the Bank of Canada (BoC) is likely to pay closer attention to other indicators such as underlying job growth, vacancies, hiring intentions, wages, etc. to form a view on the health of the job market.

Canada Manufacturing Sales • (3/13)

Weak January Print After a Robust December Increase

We expect manufacturing sales to decline 3.3% month-over-month in January. The drop is likely to be driven by transportation equipment and machinery sectors, which in turn reflects the headwinds of trade-exposed industry. The January drop follows a robust December increase but still implies a weak trend in sales. The 3-month average month-over-month growth rate was -0.6% in December, well below the 12-month average -0.08%. We continue to think that the Bank of Canada (BoC) will lean dovishly given the domestic backdrop in our baseline. Higher oil prices, if sustained, change the outlook substantially by boosting both growth and inflation prospects. However, we think these levels need to be sustained for a month or two before a shift from in policy tone. The BoC's March meeting, on March 18, is likely too soon for it to make such an assessment.

U.K. Monthly GDP • (03/13)

Strong Momentum to Start the Year

We expect the UK’s January GDP print to come in strong at 0.3% month-over-month, up from December’s 0.1% and above consensus expectations (0.2%.) Growth will likely be broad-based across industrial, services and construction sectors, with economic activity indicators and January’s PMIs surveys both pointing to an encouraging start to the year. While services carries more weight on the economy, manufacturing activity also has been trending upward, adding to the positive impulse. However, policymakers’ concerns are heightened as they weigh the impact of the renewed conflict in the Middle East on growth and inflation. As an overall net exporter of oil and gas, the UK economy is exposed to higher energy prices, which if prolonged would act as a drag on activity. At this point, though, this is still not a prolonged conflict. As such, we maintain our view that the Bank of England (BoE) should continue cutting rates—whether that will be the case is another matter. We can see the BoE opting to hold at their March meeting as the language from policymakers has turned cautious over the past week.

EM

Mexico CPI • (3/9)

Oil Price Shock Makes Banxico's Inflation Outlook More Challenging

February inflation data will be an input into Banxico's assessment of monetary policy settings at its March meeting; however, the rise in oil prices due to events in the Middle East takes some of the steam out of the importance of next week's CPI release. In fairness, oil prices had ticked up before the conflict intensified. A 15% rise in oil prices pre-conflict was not immaterial, and policymakers expressed some concern, but not enough to push Banxico off its bias for lower interest rates. With Brent Crude now up ~35% year-to-date, upside risks to inflation are starting to take shape that policymakers may not be able to dismiss so easily. Elevated oil prices will feed directly into headline inflation, and based on the duration and intensity of the conflict, could potentially have second round effects that impact price formation more broadly. That dynamic may not be fully captured in next week's CPI data, leaving February CPI data a bit more backward-looking. Our view has been that local inflation trends are more complicated than Banxico's assessment of CPI, and at some point in the near future, Banxico will adopt a less optimistic stance that the CPI target will be hit in the coming quarters. The sharp rise in oil prices may be the catalyst for Banxico to shift its own inflation expectations. Our views on Mexico inflation led us to adopt a higher terminal rate forecast than markets were pricing pre-conflict, and we remain comfortable with an above-market pricing and consensus forecast given the events of the past week.

India CPI • (3/12)

RBI Now Firmly on Hold Although Balance of Risk Shifts to Hikes

India's economy is heavily exposed to events in the Middle East and the subsequent rise in oil prices, which also makes next week's CPI data less relevant than usual. One of the largest oil importers in the world, India could experience a notable rise in headline inflation come March with possible pass through to core inflation, depending on how long the oil spike and market volatility persists. The inflationary impact is a potential problem for India, but perhaps not as much of an issue at the moment, as price growth has been well below the Reserve Bank of India (RBI) CPI target for some time. With price growth below target, RBI policymakers may not be as quick to shift in a more hawkish direction on monetary policy. We would also note that government subsidies—despite India's public finance position being rather weak—could be enhanced to offset household affordability concerns from rising energy prices. Expanding subsidies raises its own challenges, but the combination of already subdued price pressures and fiscal offset could limit the inflationary impact and keep RBI policymakers on hold for now. A sustained rise in oil prices, however, likely prompts a more hawkish response from the RBI, especially if the rupee remains under pressure. For now, we forecast RBI policy rates to be left on hold, but the balance of risk has shifted toward rate hikes, as opposed to further rate cuts, given the upside risks to inflation and downside risks to the rupee.

Brazil CPI • (3/12)

Our Less Dovish BCB Outlook Slowly Being Priced into Financial Markets

Slightly different from Mexico and India, Brazil's February CPI will remain an influential data point for market participants and local policymakers. Brazilian Central Bank (BCB) policymakers have signaled that rate cuts are set to begin this month, but what is still unclear is the forcefulness of easing to start of the cycle. Next week's CPI data can offer insight into whether BCB policymakers choose to move quickly when removing monetary policy restriction or take a more gradual approach to lowering the Selic Rate. Worth noting, however, is how Middle East event risk is very much an input for the BCB too. To that point, late this week BCB monetary policy director and COPOM voter Nilton David signaled that the path for rates may change as a result of the conflict in the Middle East. Specifically David commented:

"The central bank can change course if the scenario changes. Our level of conviction extended only to the next meeting. There have been developments that we cannot ignore, and clearly they must be factored into our assessment."

We have been less dovish on the BCB than market pricing, calling for a more gradual 25 bps rate reduction at the March meeting, as opposed to a 50 bp cut markets are priced for. Consensus economists have also gravitated toward a 50 bp rate cut. We continue to feel comfortable, perhaps more comfortable, with our tempered start to the easing cycle forecast as oil prices pop higher, BRL is under pressure, looser fiscal policy is likely, and now after Monetary Policy Director David's comments. February CPI will not capture all the recent rise in oil prices, but will still matter, and should another above estimate inflation print, similar to what we saw with mid-month IPCA data hit, our view for a 25 bp cut would be reinforced.

China Activity • (3/15)

Downside Risks to China GDP Are Starting to Take Shape

February retail sales, industrial production and other activity data—which are the first hard data releases since the Lunar New Year period ended—will offer a pre-conflict glimpse into early 2026 economic momentum across China. We noted in recent publications how risks to China's near-term growth prospects had been tilted to the upside (despite the probability of "hard landing" risks rising); however, the near-term balance of risk for growth has become more two-sided as a result of the conflict with Iran. Should activity data align with underwhelming February manufacturing and non-manufacturing PMIs, the balance of risk could tilt more heavily to the downside. As of now, we forecast China's economy to grow 4.6% this year, which is notable given that our forecast represents a slower growth profile for China relative to last year, but also as China's official growth target was lowered to 4.5%–5.0% at the still-ongoing National People's Congress. The duration of the conflict in the Middle East will ultimately play a role in whether downside risks to growth become our new base case. For now, we have not made adjustments to our China economic outlook, and our GDP forecast is not only in the middle of the new official growth target, but in line with consensus estimates.

U.S. Weekly Economic & Financial Commentary

Summary

U.S. Week In Review

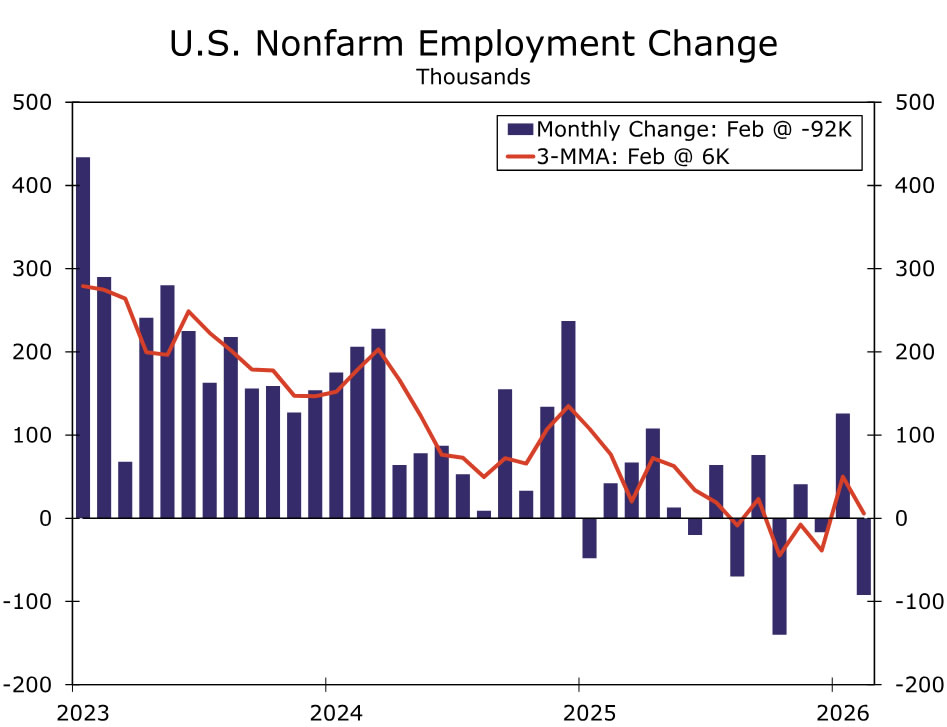

- The February jobs report was uniformly negative. Nonfarm payrolls slipped by 92K, labor force participation declined and the unemployment rate ticked up to 4.4%. Yet, increased productivity growth remains a green shoot amid increasingly apparent labor market deterioration. Control group retail sales also suggested that consumer spending remained buoyant in January.

U.S. Week Ahead

- Incoming inflation data are likely to confirm that price growth remains stubborn. We expect real disposable income growth to continue to run behind real consumption growth in January, underscoring that the wind at the household sector's back has weakened.

U.S. Week in Review

We published a note early this week detailing our thoughts on how the Iran conflict might influence the U.S. economy. Our best judgment is that the effects on domestic inflation are likely to be modest. However, much remains uncertain as brent crude futures currently trade at around $90 per barrel. Even if tail risks do materialize, for example, if the conflict lasts longer than expected or oil shipments cannot travel safely through the Strait of Hormuz, this global supply shock should not materially alter the Fed’s reaction function.

What is top of mind at the FOMC is the underlying stability of the labor market. This morning’s nonfarm payroll report was uniformly negative. The labor market shed 92K jobs in February, a significant downside miss compared to economist expectations. Payrolls over the prior two months were also revised down by a cumulative 69K, bringing the three-month average payroll gain to just 6K. Nearly every major industry shed headcount in February. Even health care & social assistance, this cycle’s mainstay driver of labor demand, experienced giveback. The household survey was similarly weak as the unemployment rate ticked up to 4.4% and the labor force participation slid by half a percentage point to 62.0% on revised population estimates.

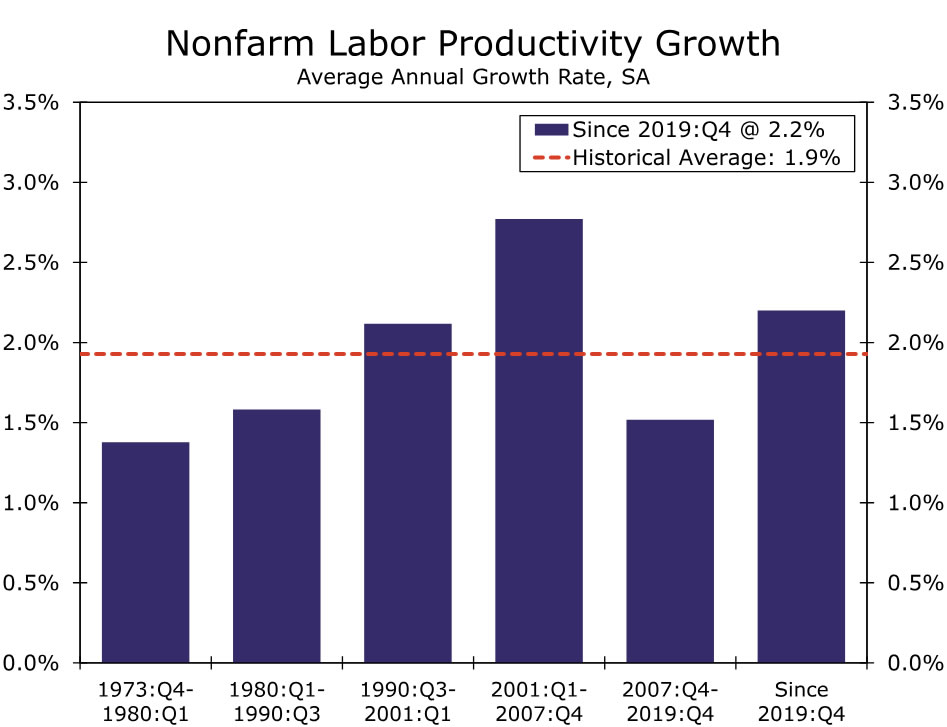

Increased productivity growth remains a green shoot amid increasingly apparent labor market deterioration. Nonfarm business productivity rose at an annualized 2.8% rate in Q4, surpassing economist expectations and adding to the above-average trend observed since the pandemic. Unit labor cost growth also accelerated over the quarter. But through the noise, the underlying trend in productivity-adjusted labor costs remains consistent with the Fed’s 2% inflation target.

Retail sales dipped 0.2% in January. Keep in mind that this week’s print was unusually lagged due to the government shutdown. The underlying details were also a bit stronger than the headline suggests. Stripping out weakness from gasoline stations and auto dealers, control group sales rose 0.4% accompanied by upward revisions to prior data. This does not necessarily mean that we expect consumers to go gangbusters over the next few months; poor winter weather and subdued credit card data point to another weak print in February. However, we do expect retail sales to show more material signs of life as larger tax refunds start to filter through in March.

The ISM indices painted a more resilient picture of economic activity. The February ISM Services index rocketed to its highest point in three and a half years, supported by a broad-based demand improvement across industries. Meanwhile, its manufacturing counterpart remained above 50 for the second straight month, marking the first two-month expansionary string since mid-2022. Firms across the board reported healthier new orders and production. Both sectors also reported growing backlogs to support future activity.

One potentially troubling development was a near-12-point jump in prices paid by manufacturers. Upon further inspection, this leap appears tied to steel and aluminum tariffs raising the cost of industry metals. Recall that the Section 232 tariffs on steel and aluminum have a firmer legal justification than the IEEPA tariffs recently rolled back by the Supreme Court. However, the ultimate transmission of higher metals costs to consumer prices is likely to be minimal.

U.S. Week Ahead

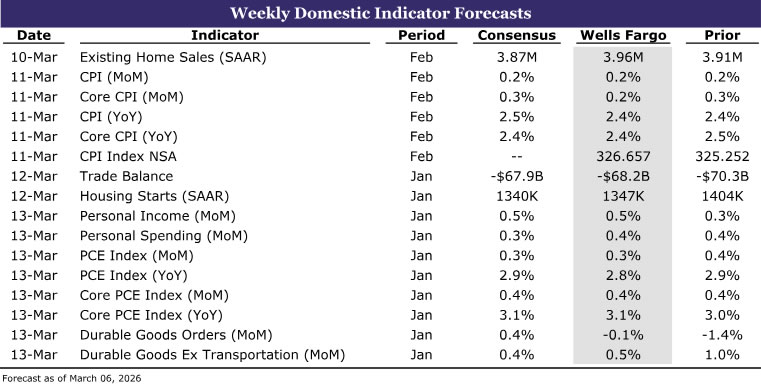

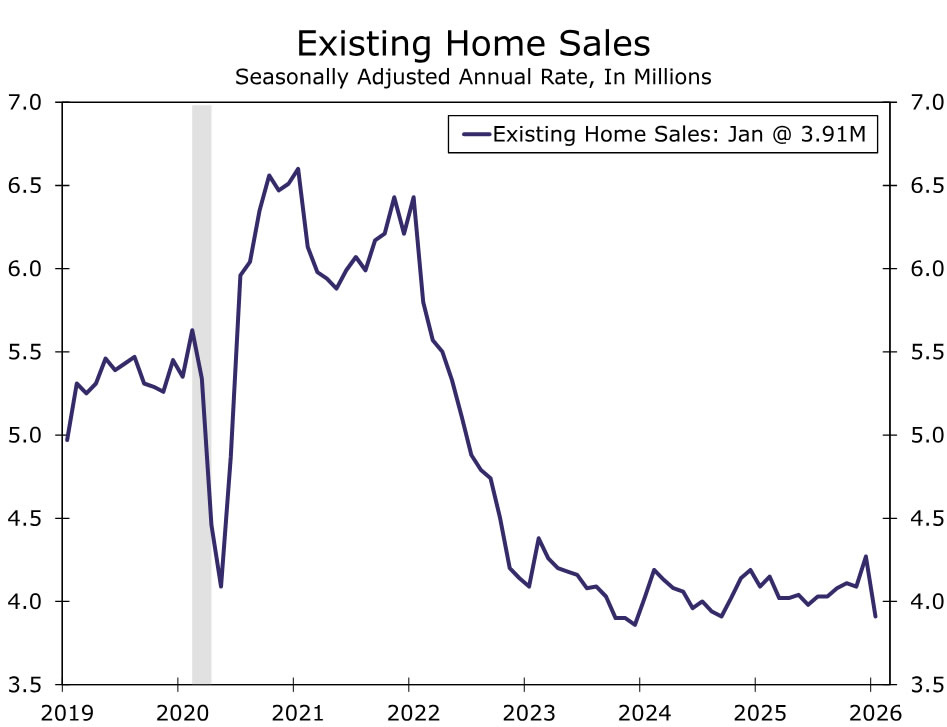

Monday • Existing Home Sales

Existing home sales likely regained some footing in February after a weather-related drop in January. We forecast resales strengthened to a 3.96 million-unit annualized pace. Marginally improved affordability and slightly better inventory conditions likely aided sales over the month, but there are numerous headwinds likely to restrain the housing market this year.

After briefly dipping below 6.0%, mortgage rates have moved up to 6.1% according to Mortgage News Daily. Looking ahead, home buyer financing costs are unlikely to fall further. Home price appreciation is also starting to pick up again after moderating over the past year. At the same time, household income growth is under pressure. Homeownership costs thus still consume over 40% of median income, illustrating that affordability conditions are far from favorable. We expect ongoing supply constraints and elevated borrowing costs to continue to weigh on activity, pointing to a gradual, rather than robust, recovery in existing home sales as 2026 unfolds.

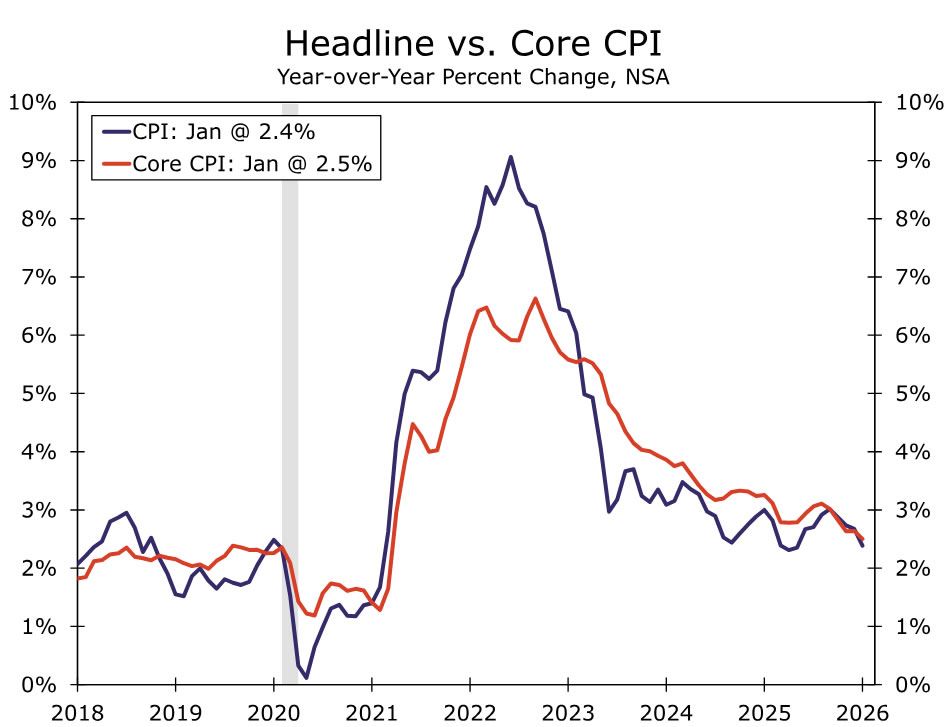

Tuesday • Consumer Price Index

February’s CPI report is likely to underscore that progress on disinflation is stalling out again. We expect the headline CPI rose 0.21% in February, a touch firmer than January. Energy is set to reassert upward pressure on overall prices, as oil and gasoline prices were already rising in February in anticipation of a conflict in the Middle East. Softer food inflation should offer a partial offset, with grocery prices due for a modest decline over the month.

Core CPI is expected to moderate to a 0.19% gain, led by some payback in services after outsized increases in travel and medical care in January. That said, core goods inflation likely firmed, reflecting higher used vehicle prices and ongoing tariff pass-through to consumers. Taken together, we forecast both the headline and core CPI rose 2.4% on a year-over-year basis in February. For more detail, see our February CPI Preview.

Friday • Personal Income and Spending

January’s personal income and spending report should continue to show a consumer that is holding up reasonably well despite persistent uncertainty and deteriorating confidence. We forecast personal income rose 0.5% in January, reflecting still-solid wage growth and annual adjustments to social security payments. Personal spending is expected to increase 0.4%, consistent with continued resilience in services outlays even as growth in discretionary outlays remains muted.

Beneath the headline, inflation remains uncomfortably stubborn. We expect real disposable income growth to continue to run behind real consumption growth in January, underscoring that the wind at the household sector's back has weakened. That said, favorable tax provisions from the One Big Beautiful Bill Act should provide a meaningful tailwind to household income this spring and help support consumption in the coming months.

Canada’s Jobs and Unemployment Rate Likely Ticked Higher in February

February’s Labour Force Survey for Canada next Friday, alongside January’s international merchandise trade report on Thursday will be in focus to assess whether the economy started 2026 on a solid footing.

We expect employment to increase by 10,000 in February, while the unemployment rate edges higher to 6.7% from 6.5% in January—reflecting a partial retracement in the labour force participation rate after an unusually large January decline.

The sharp drop in the unemployment rate in January (from 6.8% in December) came despite a 25,000 drop in jobs. The labour force posted a 119,000 drop—driven by further slowing in population growth, but also the largest drop in the labour force participation rate (-0.4 ppts) since a pandemic lockdown in January 2022.

The combination of falling employment and unemployment rate at the same time sounds unusual, but Labour Force Survey data is notoriously volatile and historically, it’s not so uncommon to see that dynamic in any one given month.

Since 2000, there have been 13 months were employment and the unemployment rate declined at the same time (about once every two years). Importantly, all of those came during periods of stable to improving labour markets, not during slowdowns.

Still, an unprecedented slowing in Canada’s population from caps on temporary resident arrivals means this combination could happen more often with a shrinking labour force lowering the pace of job growth needed to push unemployment lower.

The increase in the unemployment rate we expect in February would only partially reverse the prior decline, and leave a gradual downtrend from a recent peak of 7.1% in September intact.

Wage growth will also be closely watched for signs of continued easing in pay increases. Average hourly wage growth year-over-year has been declining, consistent with most survey results.

Easing trade in January

Canada’s January merchandise trade balance on Thursday is expected to show exports and imports slowed following stronger readings late last year.

Energy prices surged in January, which likely drove much of the movement in the trade balance given Canada’s role as a major energy exporter. At the same time, motor vehicle production appears to have softened early in the year, consistent with signals from Statistics Canada’s advance manufacturing indicators, although a jump in December production could see exports rising with a lag in January.

Data summary:

February U.S. inflation report due next week will provide additional context for North American price trends. We expect headline inflation to come in at 0.3% month-over-month, which will push the year-over-year rate slightly higher to 2.5%. Core inflation growth is expected to remain unchanged from the prior month at 2.5% year-over-year and 0.3% month-over-month.

Summary 3/9 – 3/10

Monday, Mar 9, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | 2.50% | 2.40% |

| 23:50 | JPY | Bank Lending Y/Y Feb | 4.40% | 4.50% |

| 23:50 | JPY | Current Account (JPY) Jan | 3.18T | 2.70T |

| 01:30 | CNY | CPI Y/Y Feb | 0.90% | 0.20% |

| 01:30 | CNY | PPI Y/Y Feb | -1.10% | -1.40% |

| 05:00 | JPY | Leading Economic Index Jan P | 113.2 | 111 |

| 05:00 | JPY | Eco Watchers Survey: Current Feb | 48.2 | 47.6 |

| 07:00 | EUR | Germany Industrial Production M/M Jan | 0.90% | -1.90% |

| 07:00 | EUR | Germany Factory Orders M/M Jan | -4.30% | 7.80% |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | -1.1 | 4.2 |

| 23:30 | JPY |

| Labor Cash Earnings Y/Y Jan | |

| Consensus | 2.50% |

| Previous | 2.40% |

| 23:50 | JPY |

| Bank Lending Y/Y Feb | |

| Consensus | 4.40% |

| Previous | 4.50% |

| 23:50 | JPY |

| Current Account (JPY) Jan | |

| Consensus | 3.18T |

| Previous | 2.70T |

| 01:30 | CNY |

| CPI Y/Y Feb | |

| Consensus | 0.90% |

| Previous | 0.20% |

| 01:30 | CNY |

| PPI Y/Y Feb | |

| Consensus | -1.10% |

| Previous | -1.40% |

| 05:00 | JPY |

| Leading Economic Index Jan P | |

| Consensus | 113.2 |

| Previous | 111 |

| 05:00 | JPY |

| Eco Watchers Survey: Current Feb | |

| Consensus | 48.2 |

| Previous | 47.6 |

| 07:00 | EUR |

| Germany Industrial Production M/M Jan | |

| Consensus | 0.90% |

| Previous | -1.90% |

| 07:00 | EUR |

| Germany Factory Orders M/M Jan | |

| Consensus | -4.30% |

| Previous | 7.80% |

| 09:30 | EUR |

| Eurozone Sentix Investor Confidence Mar | |

| Consensus | -1.1 |

| Previous | 4.2 |

Tuesday, Mar 10, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Mar | -2.60% | |

| 23:30 | JPY | Household Spending Y/Y Jan | 2.50% | -2.60% |

| 23:50 | JPY | GDP Q/Q Q4 F | 0.30% | 0.10% |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 3.40% | 3.40% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | 1.50% | 1.60% |

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Feb | 2.40% | 2.30% |

| 00:30 | AUD | NAB Business Confidence Feb | 3 | |

| 00:30 | AUD | NAB Business Conditions Feb | 7 | |

| 03:00 | CNY | Trade Balance (USD) Feb | 175.0B | 114.1B |

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | 25.30% | |

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | 15.2B | 17.1B |

| 10:00 | USD | NFIB Business Optimism Index Feb | 99.7 | 99.3 |

| 14:00 | USD | Existing Home Sales Feb | 3.90M | 3.91M |

| 23:30 | AUD |

| Westpac Consumer Confidence Mar | |

| Consensus | |

| Previous | -2.60% |

| 23:30 | JPY |

| Household Spending Y/Y Jan | |

| Consensus | 2.50% |

| Previous | -2.60% |

| 23:50 | JPY |

| GDP Q/Q Q4 F | |

| Consensus | 0.30% |

| Previous | 0.10% |

| 23:50 | JPY |

| GDP Deflator Y/Y Q4 F | |

| Consensus | 3.40% |

| Previous | 3.40% |

| 23:50 | JPY |

| Money Supply M2+CD Y/Y Feb | |

| Consensus | 1.50% |

| Previous | 1.60% |

| 00:01 | GBP |

| BRC Like-For-Like Retail Sales Y/Y Feb | |

| Consensus | 2.40% |

| Previous | 2.30% |

| 00:30 | AUD |

| NAB Business Confidence Feb | |

| Consensus | |

| Previous | 3 |

| 00:30 | AUD |

| NAB Business Conditions Feb | |

| Consensus | |

| Previous | 7 |

| 03:00 | CNY |

| Trade Balance (USD) Feb | |

| Consensus | 175.0B |

| Previous | 114.1B |

| 06:00 | JPY |

| Machine Tool Orders Y/Y Feb P | |

| Consensus | |

| Previous | 25.30% |

| 07:00 | EUR |

| Germany Trade Balance (EUR) Jan | |

| Consensus | 15.2B |

| Previous | 17.1B |

| 10:00 | USD |

| NFIB Business Optimism Index Feb | |

| Consensus | 99.7 |

| Previous | 99.3 |

| 14:00 | USD |

| Existing Home Sales Feb | |

| Consensus | 3.90M |

| Previous | 3.91M |

Wednesday, Mar 11, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Feb | 2.10% | 2.30% |

| 07:00 | EUR | Germany CPI M/M Feb F | 0.20% | 0.20% |

| 07:00 | EUR | Germany CPI Y/Y Feb F | 1.90% | 1.90% |

| 12:30 | USD | CPI M/M Feb | 0.20% | 0.20% |

| 12:30 | USD | CPI Y/Y Feb | 2.40% | 2.40% |

| 12:30 | USD | CPI Core M/M Feb | 0.20% | 0.30% |

| 12:30 | USD | CPI Core Y/Y Feb | 2.50% | 2.50% |

| 14:30 | USD | Crude Oil Inventories (Mar 6) | 2.8M | 3.5M |

| 23:50 | JPY |

| PPI Y/Y Feb | |

| Consensus | 2.10% |

| Previous | 2.30% |

| 07:00 | EUR |

| Germany CPI M/M Feb F | |

| Consensus | 0.20% |

| Previous | 0.20% |

| 07:00 | EUR |

| Germany CPI Y/Y Feb F | |

| Consensus | 1.90% |

| Previous | 1.90% |

| 12:30 | USD |

| CPI M/M Feb | |

| Consensus | 0.20% |

| Previous | 0.20% |

| 12:30 | USD |

| CPI Y/Y Feb | |

| Consensus | 2.40% |

| Previous | 2.40% |

| 12:30 | USD |

| CPI Core M/M Feb | |

| Consensus | 0.20% |

| Previous | 0.30% |

| 12:30 | USD |

| CPI Core Y/Y Feb | |

| Consensus | 2.50% |

| Previous | 2.50% |

| 14:30 | USD |

| Crude Oil Inventories (Mar 6) | |

| Consensus | 2.8M |

| Previous | 3.5M |

Thursday, Mar 12, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q4 | 2.70% | |

| 23:50 | JPY | BSI Large Manufacturing Q1 | 5.5 | 4.7 |

| 00:00 | AUD | Consumer Inflation Expectations Mar | 5% | |

| 00:01 | GBP | RICS Housing Price Balance Feb | -9% | -10% |

| 12:30 | CAD | Building Permits M/M Jan | -2.00% | 6.80% |

| 12:30 | CAD | Trade Balance (CAD) Jan | -1.0B | -1.3B |

| 12:30 | CAD | Wholesale Sales M/M Jan | -0.60% | 2.00% |

| 12:30 | USD | Initial Jobless Claims (Mar 6) | 215K | 213K |

| 12:30 | USD | Housing Starts Jan | 1.34M | 1.40M |

| 12:30 | USD | Building Permits Jan | 1.39M | 1.45M |

| 13:30 | USD | Trade Balance (USD) Jan | -67.8B | -70.3B |

| 14:30 | USD | Natural Gas Storage (Mar 6) | -42B | -132B |

| 21:45 | NZD |

| Manufacturing Sales Q4 | |

| Consensus | |

| Previous | 2.70% |

| 23:50 | JPY |

| BSI Large Manufacturing Q1 | |

| Consensus | 5.5 |

| Previous | 4.7 |

| 00:00 | AUD |

| Consumer Inflation Expectations Mar | |

| Consensus | |

| Previous | 5% |

| 00:01 | GBP |

| RICS Housing Price Balance Feb | |

| Consensus | -9% |

| Previous | -10% |

| 12:30 | CAD |

| Building Permits M/M Jan | |

| Consensus | -2.00% |

| Previous | 6.80% |

| 12:30 | CAD |

| Trade Balance (CAD) Jan | |

| Consensus | -1.0B |

| Previous | -1.3B |

| 12:30 | CAD |

| Wholesale Sales M/M Jan | |

| Consensus | -0.60% |

| Previous | 2.00% |

| 12:30 | USD |

| Initial Jobless Claims (Mar 6) | |

| Consensus | 215K |

| Previous | 213K |

| 12:30 | USD |

| Housing Starts Jan | |

| Consensus | 1.34M |

| Previous | 1.40M |

| 12:30 | USD |

| Building Permits Jan | |

| Consensus | 1.39M |

| Previous | 1.45M |

| 13:30 | USD |

| Trade Balance (USD) Jan | |

| Consensus | -67.8B |

| Previous | -70.3B |

| 14:30 | USD |

| Natural Gas Storage (Mar 6) | |

| Consensus | -42B |

| Previous | -132B |

Friday, Mar 13, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Feb | 55.2 | |

| 07:00 | GBP | GDP M/M Jan | 0.20% | 0.10% |

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -21.7B | -22.7B |

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | 0.70% | -1.40% |

| 12:30 | CAD | Net Change in Employment Feb | 10.0K | -24.8K |

| 12:30 | CAD | Unemployment Rate Feb | 6.60% | 6.50% |

| 12:30 | CAD | Manufacturingles M/M Jan | -3.30% | 0.60% |

| 12:30 | CAD | Capacity Utilization Q4 | 78.40% | 78.50% |

| 12:30 | USD | Personal Income M/M Jan | 0.50% | 0.30% |

| 12:30 | USD | Personal Spending M/M Jan | 0.30% | 0.40% |

| 12:30 | USD | PCE Price Index M/M Jan | 0.30% | 0.40% |

| 12:30 | USD | PCE Price Index Y/Y Jan | 2.90% | 2.90% |

| 12:30 | USD | Core PCE Price Index M/M Jan | 0.40% | 0.40% |

| 12:30 | USD | Core PCE Price Index Y/Y Jan | 3.10% | 3.00% |

| 12:30 | USD | GDP Annualized Q4 P | 1.40% | 1.40% |

| 12:30 | USD | GDP Price Index Q4 P | 3.60% | 3.70% |

| 12:30 | USD | Durable Goods Orders Jan | 1.10% | -1.40% |

| 12:30 | USD | Durable Goods Orders ex Transport Jan | 0.50% | 0.90% |

| 14:00 | USD | UoM Consumer Sentiment Mar P | 55 | 56.6 |

| 14:00 | USD | UoM 1-Yr Inflation Expectations Mar P | 3.40% |

| 21:30 | NZD |

| Business NZ PMI Feb | |

| Consensus | |

| Previous | 55.2 |

| 07:00 | GBP |

| GDP M/M Jan | |

| Consensus | 0.20% |

| Previous | 0.10% |

| 07:00 | GBP |

| Goods Trade Balance (GBP) Jan | |

| Consensus | -21.7B |

| Previous | -22.7B |

| 10:00 | EUR |

| Eurozone Industrial Production M/M Jan | |

| Consensus | 0.70% |

| Previous | -1.40% |

| 12:30 | CAD |

| Net Change in Employment Feb | |

| Consensus | 10.0K |

| Previous | -24.8K |

| 12:30 | CAD |

| Unemployment Rate Feb | |

| Consensus | 6.60% |

| Previous | 6.50% |

| 12:30 | CAD |

| Manufacturingles M/M Jan | |

| Consensus | -3.30% |

| Previous | 0.60% |

| 12:30 | CAD |

| Capacity Utilization Q4 | |

| Consensus | 78.40% |

| Previous | 78.50% |

| 12:30 | USD |

| Personal Income M/M Jan | |

| Consensus | 0.50% |

| Previous | 0.30% |

| 12:30 | USD |

| Personal Spending M/M Jan | |

| Consensus | 0.30% |

| Previous | 0.40% |

| 12:30 | USD |

| PCE Price Index M/M Jan | |

| Consensus | 0.30% |

| Previous | 0.40% |

| 12:30 | USD |

| PCE Price Index Y/Y Jan | |

| Consensus | 2.90% |

| Previous | 2.90% |

| 12:30 | USD |

| Core PCE Price Index M/M Jan | |

| Consensus | 0.40% |

| Previous | 0.40% |

| 12:30 | USD |

| Core PCE Price Index Y/Y Jan | |

| Consensus | 3.10% |

| Previous | 3.00% |

| 12:30 | USD |

| GDP Annualized Q4 P | |

| Consensus | 1.40% |

| Previous | 1.40% |

| 12:30 | USD |

| GDP Price Index Q4 P | |

| Consensus | 3.60% |

| Previous | 3.70% |

| 12:30 | USD |

| Durable Goods Orders Jan | |

| Consensus | 1.10% |

| Previous | -1.40% |

| 12:30 | USD |

| Durable Goods Orders ex Transport Jan | |

| Consensus | 0.50% |

| Previous | 0.90% |

| 14:00 | USD |

| UoM Consumer Sentiment Mar P | |

| Consensus | 55 |

| Previous | 56.6 |

| 14:00 | USD |

| UoM 1-Yr Inflation Expectations Mar P | |

| Consensus | |

| Previous | 3.40% |

Non-Farm Payrolls Large Miss and Oil Explodes Higher to $90 – A Stagflation Cocktail Ahead of Weekend Risk

This morning is sending a nasty look for Markets, as Oil continues to explode higher amid Middle East tensions. At the same time, US labor data keeps showing volatility, this time to the downside.

It is a dark day for risk assets, and the fundamentals aren't going to help – particularly with a miss in Retail Sales rubbing salt in the wound, it seems that prior bounces in US data could have been a seasonal effect of Holidays/New Year hiring and consumption. We could now be facing a hangover.

Morning US Data – MarketPulse Economic Calendar

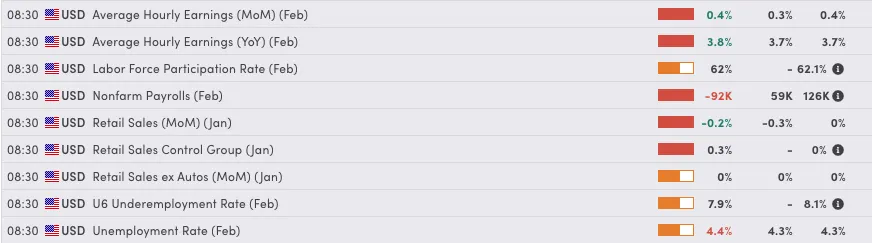

Non-Farm Payrolls just released at -92K vs +56K expected, a significant (-148K) miss!

Such a reversal in the data can't fail to raise questions about actual job displacement from new AI technologies and whether the Federal Reserve is really getting behind the curve.

The issue for the Central Bank is that inflation is certainly bouncing higher despite lower Retail Sales – so combine a weaker jobs Market, consumption, and elevated inflation, and conclusions about stagflation could be reached quickly – and with decent reasoning, too!

With Energy prices shooting higher throughout the week, it is certain that inflation expectations are not going to ease anytime soon – the only thing that could soothe them at this point is an actual pricing of slower consumption ahead, but that wouldn't fare well for the US economy.

Goods-producing, Private Education, and Services took the largest hit, with gains only seen in Financials and Wholesale Trades.

We will provide a quick outlook on the Market before diving into WTI (US) Oil Charts to get ready for what could be another volatile weekend.

A Nasty Market Picture

Stock and Energy Product Futures – Courtesy of Finviz

There goes risk-appetite, as a close to 10% rise in daily WTI prices will keep raising inflation expectations and that tends to coincide with major repricings in Equity markets

An in-depth Stock Market coming at the top of the morning.

Cryptos Are Not Getting Spared

Bitcoin 4H Chart – March 6, 2026 – Source: TradingView

Bitcoin and Cryptocurrencies are not sustaining the dampening Market mood.

Even Bonds, which could have thought to rebound in such a miss in Non-Farm Payrolls, are actually met with high pressure from the rise in Oil (and rising Inflation Expectations).

Only Metals Are Sustaining the Pressure

Gold 4H Chart – March 6, 2026 – Source: TradingView

Only Gold and Silver are rebounding, albeit a timid rebound for now – A Double bottom in Gold will be helping its prospects on the intraday.

Nonetheless, a larger picture double top could still have its effect, so Bulls will have to show real strength, volume and conviction!

WTI (US) Oil Wicks at $90, Explodes to October 2023 Highs!

WTI Daily Chart – March 6, 2026 – Source: TradingView

The last time we saw the $90 handle in WTI was in late 2023 – A scary picture, particularly considering that Oil was trading at $55 just about two months ago!!

The Commodity has now risen 30% since the beginning of the week and despite some slight easing, the squeeze doesn't seem to be stalling.

A more detailed analysis for Oil is coming up in the afternoon. For now, keep track on if the action remains above $86.

- If it closes here, pressure will remain high.

- Correcting below should point to a slight correction ($80 would be the next step).

Keep a close eye on sentiment and Middle East news.

Safe Trades!

Week Ahead – US Inflation Data to Offer Distraction Amid Iran War Fallout

- US CPI and PCE inflation reports both due as Fed cut bets scaled back.

- Geopolitical turmoil keeps investors on edge as energy prices spike.

- Canadian employment, UK GDP and Japanese data also on the agenda.

World grapples with new energy threat

Four years into the Ukraine war and still reeling from the ensuing shock to energy prices, major economies are facing the real threat of a fresh energy crisis, as the war in the Middle East roils markets. For the US economy, which is showing renewed signs of momentum and where inflation has been moderating only slowly, Fed rate-cut expectations had already been pared back before the war broke out.

Following the escalation, which has not only embroiled neighbouring countries, inflicting damage on their energy facilities or forcing their closure, but has also effectively shut the Strait of Hormuz to vessels, potentially disrupting about 20% of the world’s oil and gas supply.

All this cannot be good for the inflation outlook, as oil futures have soared by around 20% and European gas futures have skyrocketed by more than 50%. The United States is somewhat more immune to a direct energy shock from the Middle East turmoil, but the situation nonetheless creates a fresh headache for the Fed, which is unhappy about the slow progress of inflation returning to its 2% target.

Year-end rate-cut expectations have fallen to around 40 basis points from 60 bps a few weeks ago, while the next move is not fully priced in until September.

Spotlight on US inflation as Fed cut bets recede

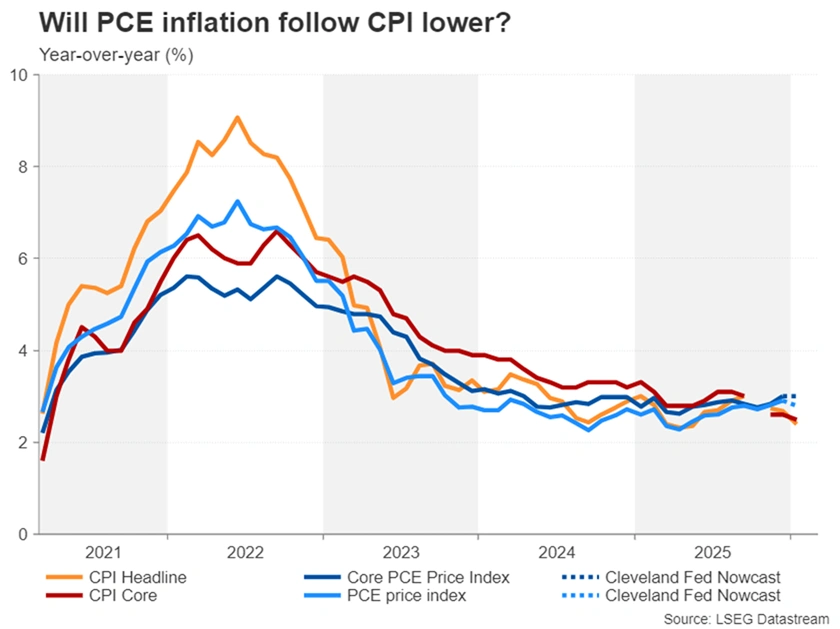

Next week’s data will be crucial in further shaping Fed easing expectations, as both the CPI (Wednesday) and PCE (Friday) reports are incoming. Although some policymakers appear comfortable with the idea of a long pause, less hawkish FOMC members could be persuaded to back a rate cut as early as June, if not sooner.

Headline CPI fell to 2.4% y/y in January, while the core rate moderated to 2.5%. Both are expected to have stayed unchanged in February. What might prove more market-moving, however, is the PCE data, as it’s watched more closely by the Fed, and unlike the CPI numbers, it remains stuck near 3.0%.

After edging up to 2.9% in December, headline PCE is estimated to have dropped to 2.8% in January according to the Cleveland Fed’s Nowcast model. But the more important core PCE price index is forecast to have held steady at 3.0%.

Whilst the PCE figures may not be as up to date as the CPI ones, any upside surprises during the current backdrop of elevated inflation risks could deal a further blow to Fed rate cut bets, increasing the US dollar’s short-term bullishness.

Investors will also be keeping an eye on the other releases included in the PCE report, namely, the personal income and consumption stats. Moreover, the week as a whole will be a data-heavy one, with a batch of housing market indicators on Tuesday and Thursday, as well as durable goods orders, the JOLTS job openings and the University of Michigan’s preliminary consumer sentiment survey, all due on Friday.

Yen loses out to Dollar and Franc

The Japanese yen has seen a mixed response to the major geopolitical flare-up, appreciating against most major currencies but falling against some, like the US dollar. Investors have favoured the dollar over other safe havens during the Iran crisis, even gold. The Swiss franc was also initially a strong beneficiary of safe-haven flows but it got knocked back when the Swiss National Bank issued a rate intervention warning.

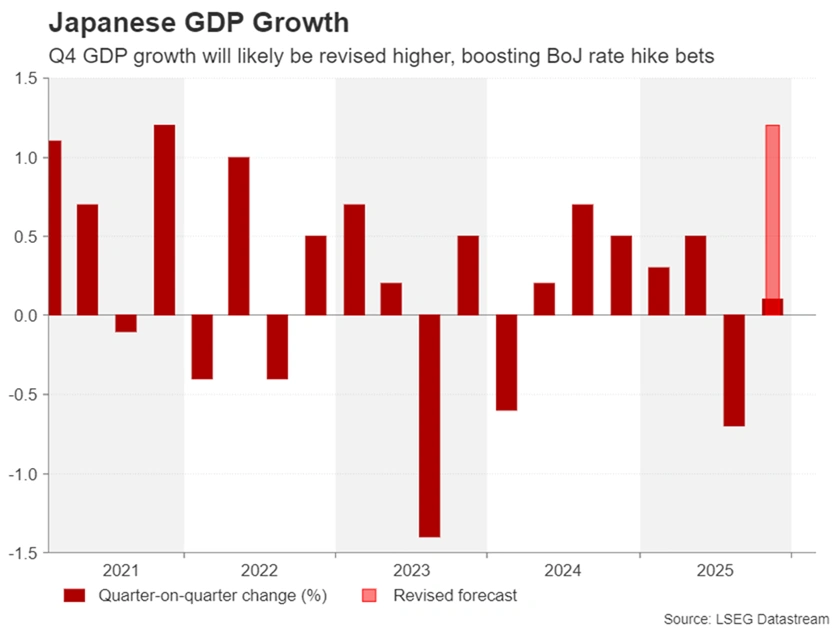

However, this doesn’t appear to have redirected any safety flows to the yen, as traders struggle to make sense of Bank of Japan communication, with the Middle East conflict complicating the policy direction even more, as it raises the prospect of stagflation. Governor Ueda remains uncommitted to a timeline for raising interest rates, while the government continues to question the need for further tightening.

Still, the BoJ has a history of catching markets off guard, and although investors see little chance of a hike before the June meeting, an earlier move cannot be ruled out, particularly if the wage and consumption data surprise to the upside.

Hence, next week’s releases on wage growth (Monday), household spending (Tuesday), revised GDP estimates (Tuesday) and corporate goods prices (Wednesday), will be monitored. A more imminent risk, though, for the yen, is a possible intervention by Japanese authorities, as the dollar hovers near the 158–160-yen intervention zone.

Pound subdued even as BoE rate cut priced out

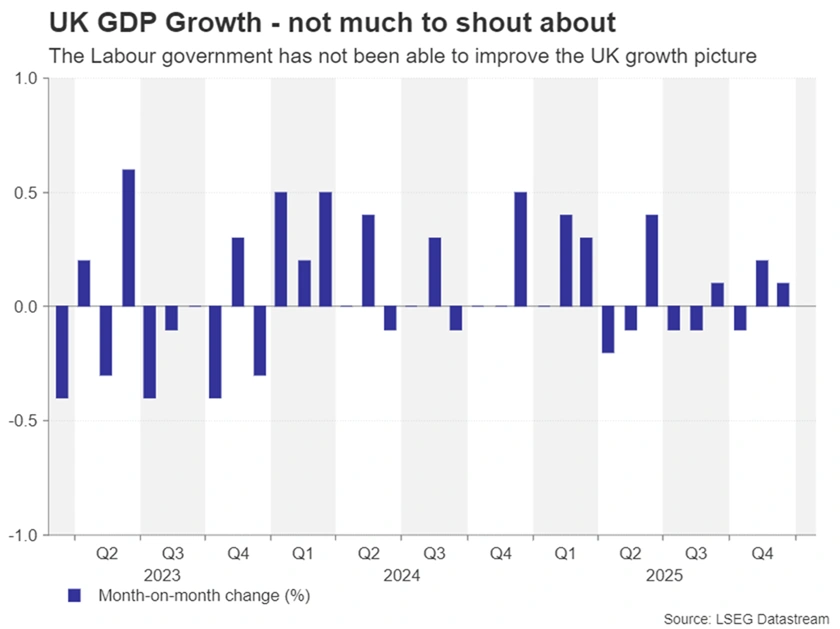

The UK economy has barely grown since last summer as the government’s tax increases on businesses and the uncertainty generated by Chancellor Rachel Reeves’ chaotic budget has hit hiring and investment. The sluggish performance has kept the Bank of England on an easing path even as inflation re-accelerated during 2025.

The BoE’s main concern is the upward trending unemployment rate, which hit a five-year high in December. Nevertheless, with inflation decelerating only slowly and at 3.0%, still well above the BoE’s 2.0% target, the current developments in the Middle East could easily blow any rate cut plans off course.

Investors have already sharply lowered their expectations of a 25-bps reduction at the next meeting to less than 15% from over 80% and simultaneously priced out a second 25-bps cut.

However, if the upcoming releases, all due on Friday, disappoint, easing expectations would likely be bolstered, adding to sterling’s woes amid a resurgent dollar. The slew of data will include monthly GDP readings for January, as well as industrial production and trade figures.

Loonie eyes jobs data amid Oil boost

In Canada, employment numbers will likely attract some attention on Friday for the Canadian dollar, which has been lifted from the jump in oil prices amid fears of a prolonged disruption to supply from Iran’s counter attacks to the US- and Israel-led strikes.

Canada’s labour market shed jobs in January so a rebound in February would add more fuel to the loonie’s engines against other currencies apart from the dollar. However, a weak jobs report could prompt a pullback.

On the whole, though, geopolitical events will likely remain in the driver’s seat for the loonie as the Bank of Canada is not expected to tweak its policy settings anytime soon.

Aussie rally loses steam, might find support in China data

The Australian dollar is headed for its first weekly loss in seven weeks against the greenback, as risk sentiment ebbs on the back of the Iran conflict. However, Australia also faces fresh tariff uncertainty following the US Supreme Court ruling that President Trump’s reciprocal levies were illegal. Australian exports to the US look set to be charged 15% duties instead of 10%.

Yet, the Reserve Bank of Australia is still expected to hike rates again later this year, especially if higher energy prices push up inflation. But in the short term, the aussie might need a boost from other sources, which may come in the form of Chinese indicators.

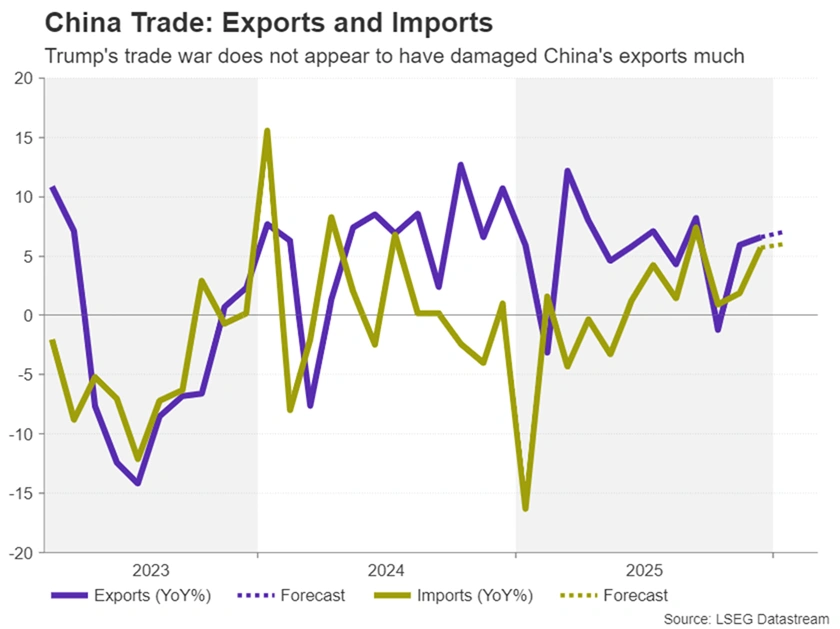

Trade data out on Tuesday will show whether or not the rise in exports to non-US countries continues to outstrip the decline in shipments to America in February. Moreover, China potentially stands to gain from the Supreme Court decision, with its effective tariff level falling from 20% to the new global rate of 15%.

A day earlier, the consumer and producer price indices for February will also be watched. Stronger-than-forecast readings could lend some support to the Aussie.

Weekly Focus – Modest Reaction to Large Conflict

Since Saturday, Israel and the US have been attacking Iran from the air with Iran firing back with missiles and drones against targets throughout the Middle East. Iran has also effectively closed ship traffic through the Strait of Hormuz which removes a significant share of seaborne oil, oil products and natural gas from the global market. Spot crude oil prices have increased close to 20% in USD terms, while European natural gas prices are up by more than 50%. Given the scale of the disruption, we see this price reaction as modest and also note that markets expect spot prices to decline again in coming months. The relatively modest reaction likely reflects that this is happening at a time when the global economy is relatively balanced as witnessed by the low and stable inflation and unemployment we are seeing in major economies and in contrast to the situation in 2021-2022.

Another reason for the relative calm in energy markets is likely that markets expect the war to be short, either because the US and Israel will reach their objectives or because they will choose to stop for political and economic reasons. This means that there is a risk of significant further price increases if the war lasts longer. The most important aspect to watch in this regard is likely to be the Hormuz Strait traffic. If that can be resumed, it will sharply reduce the disruption to energy markets, even if the conflict continues in other areas.

A similar risk applies to broader financial markets. There have been modest declines in equity prices especially in Europe, which unlike the US is a big net importer of oil and gas. Similarly, there has been a modest strengthening of USD. In bond markets, there has been noticeable increases in especially short-term yields as there appears to be fears that the ECB might hike interest rates in case of a more prolonged conflict and that the Federal Reserve could postpone or cancel the rate cuts expected this year. The argument is that high energy prices add to inflation. However, in the current macro environment we see it as more likely that central banks will take the textbook approach and not react to the supply chock, unless it starts to affect inflation expectations. Like in energy markets, we see a risk that the reaction becomes much more pronounced in financial markets in general if the conflict broadens or drags out.

In the euro area, inflation surprised to the upside at 1.9% y/y in February with a rebound in core inflation to 2.4% y/y. Unemployment declined to a record low 6.1% in January. Hence, the data is also slightly supportive of higher yields.

China has lowered its official economic growth target from 5% to a range of 4½-5% in line with previous signals. Higher growth in household consumption is stated as a top priority but there is little in the way of new policies to achieve this, and we see it as likely that exports and investments will have to continue to drive demand, not least because the housing market remains very weak.

The most important factor to watch in the coming week is the war and especially the Hormuz Strait traffic. However, we also get US CPI inflation for February which likely was lifted by energy prices also before the attack but with core inflation held down by housing rents.

Sunset Market Commentary

Markets

The daily barrage of war-related headlines produced a noteworthy one from a market perspective. The Qatari energy minister Saad al-Kaabi in the FT warned that all Gulf states will soon be forced to shut down production and that a return to normal could take weeks to months even if the war ended immediately. “Everybody that has not called for force majeure we expect will do so in the next few days that this continues”, Kaabi said, adding that if the war continues for weeks it will bring down economies with higher energy prices, shortages of some (petrochemical, fertilizer) products and a chain reaction of factories that cannot supply. QatarEnergy, the world’s biggest LNG company (20% of world production), declared force majeure earlier this week, triggering a bidding contest for whatever output that remains. Kaabi predicts crude prices to rise to $150 a barrel in two to three weeks if the Strait of Hormuz remains shut. Gas prices would rise to around €120/MWh. His comments spark another energy price burst with Brent closing in on the $90/b barrier (a weekly +23%) and Dutch TTF gas jumping to €52 (+62%). That’s pushing up ECB rate hike bets even further with a 25 bps move more than discounted by end-2026. 3M Euribor futures underwent a colossal 40 bps weekly repricing: money markets just one week ago mulled additional rate cuts. Front-end European yields today surge 8 bps, bringing the weekly tally to a stunning +33 bps. Gains for long-term maturities vary between +1.5 (30-yr) to +21 bps (10-yr). European stocks, fearing the economic impact from a new energy crisis after not even having fully recovered from the 2022 one, slip around 1%. The euro is under pressure with EUR/USD entering the payrolls release near the lowest sub 1.16 levels since end-November.

The February labour market report greatly missed the +55k expectations with employment dropping 92k and the two previous months revised downwardly by 69k. A strike in the health care sector weighed on employment but does little to alter the overall view of what is a soft report. The unemployment rate climbed to 4.4% from 4.3% even as the participation rate eased from 62.1% to 62%. Wages grew at a slightly faster-than-expected clip of 0.4% m/m and 3.8% y/y, remaining (well) above the pre-pandemic average. The payrolls cast doubt on the state of the labour market, which an increasing amount of Fed officials, including the dove Bowman just yesterday, said was showing signs of stabilizing after weakening. US yields swapped earlier 2-3 bps gains for similar-sized losses but simply cannot ignore the sharp energy price rise. With “Brent hits $90” headlines dropping as we write, Treasury yields get back positive, further fueled by President Trump stripping the market of any hopes for a short-term deal with Iran in a Truth Social post. Instead he’s demanding unconditional surrender. US yields rise up to 3 bps, German rates extend daily gains to 11 (!) bps. The dollar’s payrolls kneejerk reaction lower was muted and temporary. European stocks double earlier declines to 2% and Wall Street opens around 1.5% lower.

News & Views

Switzerland plans a temporary VAT increase of 0.8 ppts for ten years starting in 2028 to address a significantly worsened security environment. The measure is designed to raise about CHF 31bn, which will fund stronger military and civilian protection against hybrid threats, cyberattacks, long range strikes, and infrastructure vulnerabilities. All additional revenue will flow into a new defense procurement fund, which can temporarily take on up to CHF 6bn in debt to accelerate key purchases, with all debt to be repaid by the end of the ten year period. The Federal Council aims for a required national vote in summer 2027, enabling the VAT increase to take effect on 1 January 2028. The Swiss franc holds near strongest levels on record against the euro in the risk-off market climate (EUR/CHF 0.9050).

The food price index of the Food and Agriculture Organization of the United Nations in February posted the first rise in five months. The overall index rose 0.9% compared to January. Still, the overall index was 1.3% lower compared the same month last year. Increases in the sub-indices of cereals, meats and vegetable oils more than offset declines in the indices of dairy and sugar. Even so, in a broader perspective, the overall price index still was 1% lower Y/Y and 21.8 % Y/Y below the March 2022 peak. Focusing on cereal prices, the index rose 1.1% but was also still 3.5% below the year-ago level. Amongst others, wheat prices rose due to heightened seasonal factors in producer regions in Europe and the US. Logistical disruptions in the Russian Federation and continuing tensions in the Black Sea region also contributed to the increase. Vegetable oil price accelerated 3.3% M/M, reaching the highest level since June 2022, with prices for palm oil, soy and rapeseed all adding to a higher level of this sub-index.

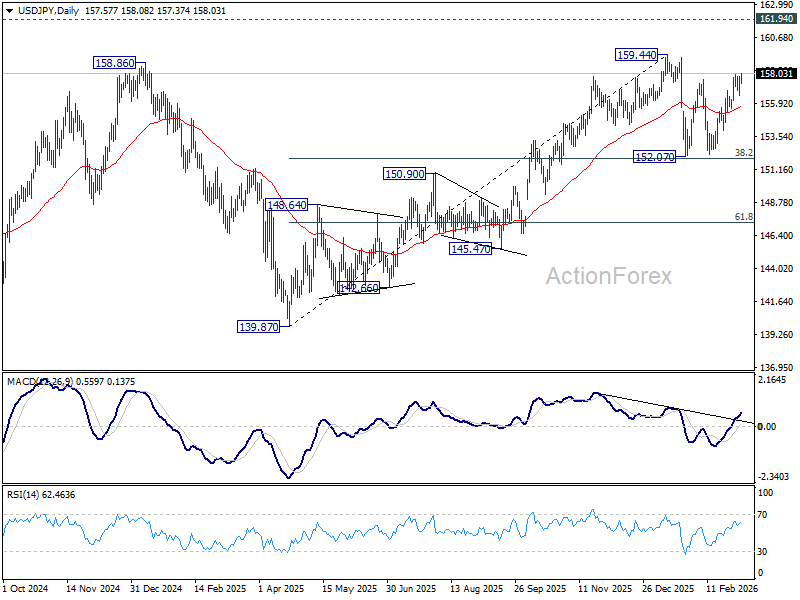

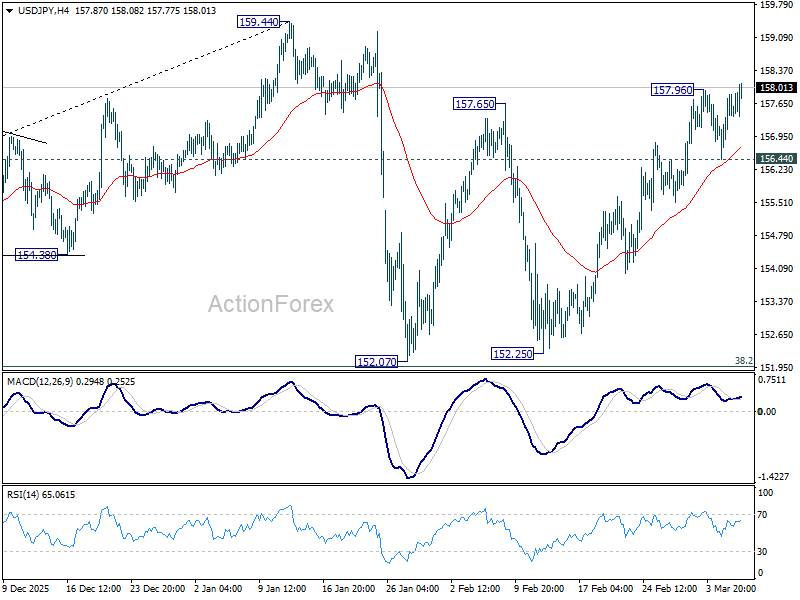

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.73; (P) 157.29; (R1) 158.12; More...

Intraday bias in USD/JPY is back on the upside with breach of 157.96 temporary top. Rise from 152.25 is resuming for retesting 159.44 high next. On the downside, below 156.44 support will turn bias neutral again first. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.