Sample Category Title

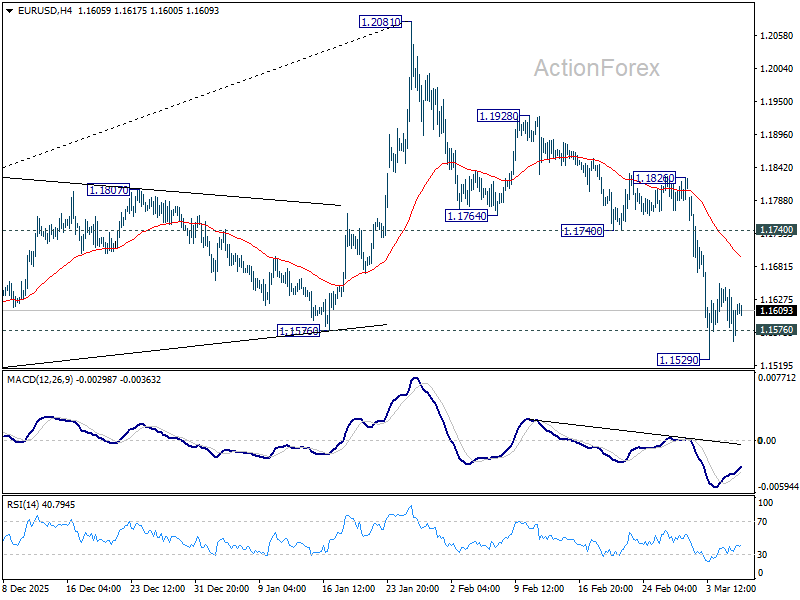

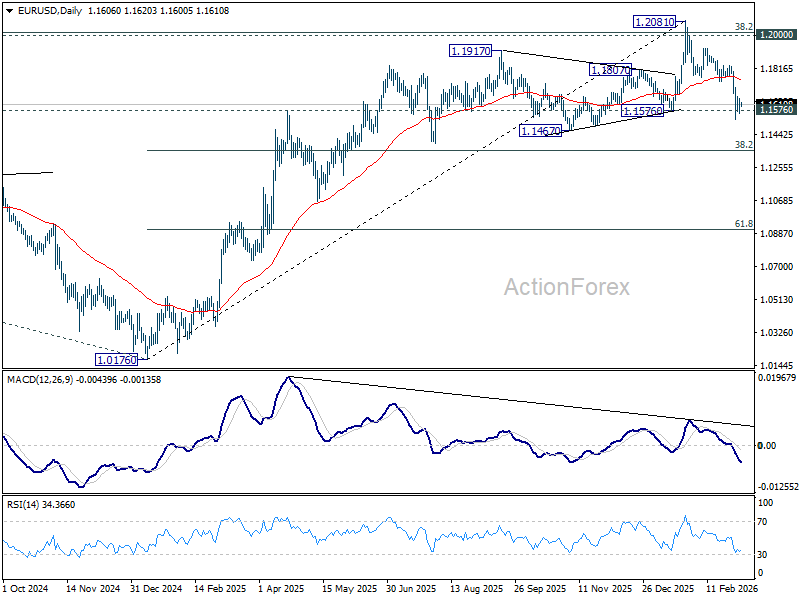

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1564; (P) 1.1605; (R1) 1.1652; More….

Intraday bias in EUR/USD remains neutral as consolidations continue above 1.1529 temporary low. On the downside, below 1.1529 will resume the fall from 1.2081. Sustained break of 1.1576 structural support would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. However, firm break of 1.1740 support turned resistance will revive near term bullishness, and bring stronger rebound back to retest 1.2081 high.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

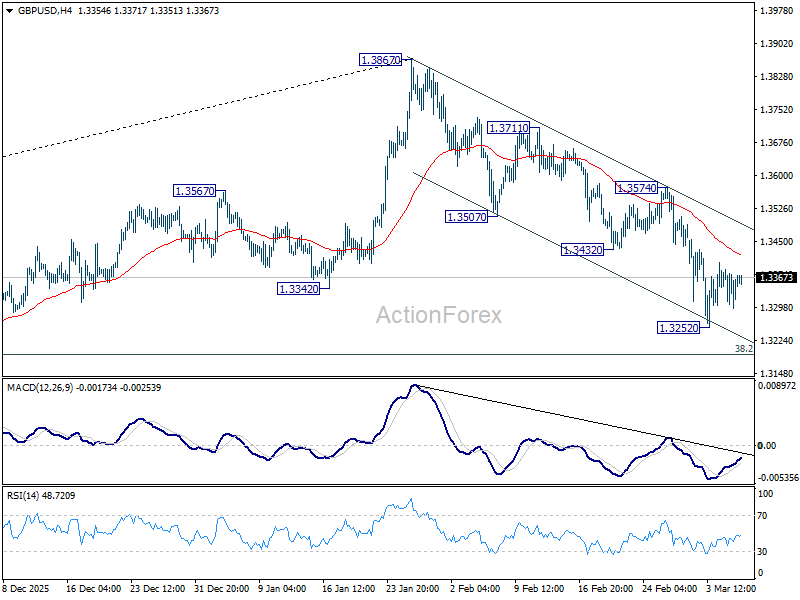

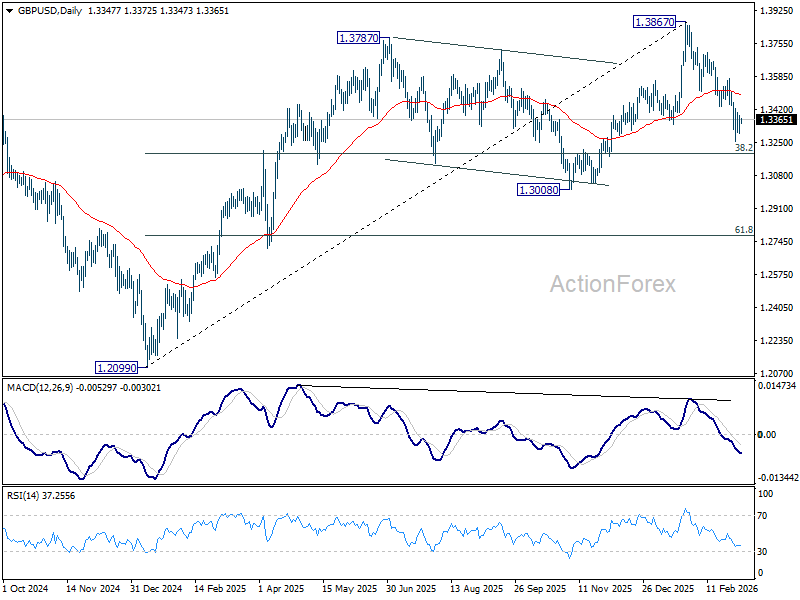

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3308; (P) 1.3347; (R1) 1.3397; More...

Intraday bias in GBP/USD remains neutral and more consolidations could be seen above 1.3252 temporary low. Fall from 1.3867 should at least be correcting the rise from 1.2009. Below 1.3252 will target 38.2% retracement of 1.2099 to 1.3867 at 1.3192. Sustained break there will pave the way to 1.3008 support. For now, risk will stay on the downside as long as 1.3574 resistance holds, in case of recovery.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

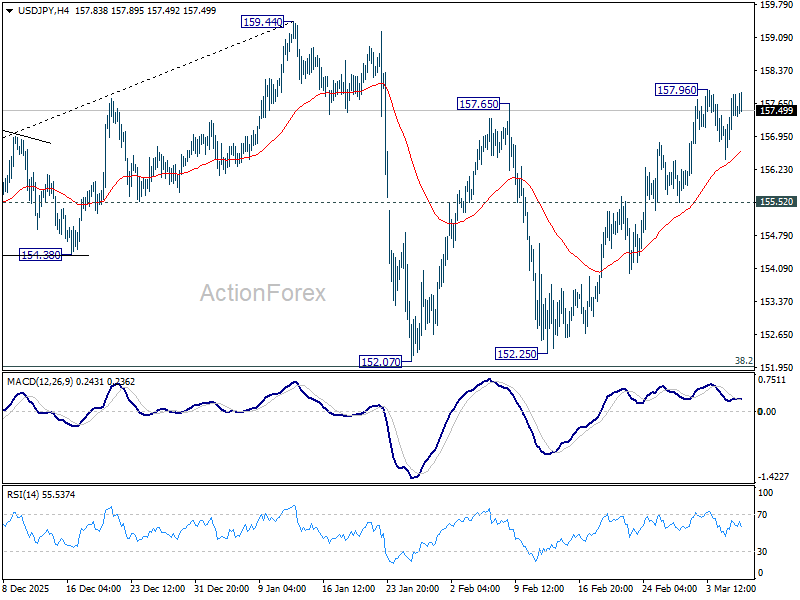

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.73; (P) 157.29; (R1) 158.12; More...

USD/JPY is staying in range below 157.96 temporary top and intraday bias remains neutral a this point. On the upside, above 157.96 will extend the rebound from 152.25 to retest 159.44 high. On the downside, though, break of 155.52 will bring deeper fall back to 152.07/152.25 support zone. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

Chart Alert: Why Japan’s Nikkei 225 Can Stage a Minor Recovery After Its 4-Day Plunge

Key takeaways

- Oil shock drove the sell-off: Since the start of the US–Iran War, Japan’s Nikkei 225 fell 6.1% in four days, underperforming global peers as Japan’s heavy reliance on imported oil heightens stagflation risks.

- Yield curve shift may support equities: A bull steepening of the Japanese government bond yield curve (10-yr minus 2-yr), partly driven by expectations of a less hawkish Bank of Japan, historically correlates with upside momentum in the Nikkei and may support a short-term rebound.

- Technical signals suggest a near-term bounce: The index has repeatedly held support around its 50-day moving average, with momentum indicators turning positive; a break above 56,530 could trigger a recovery toward 57,140–58,140, while a drop below 52,960 would invalidate the bullish scenario.

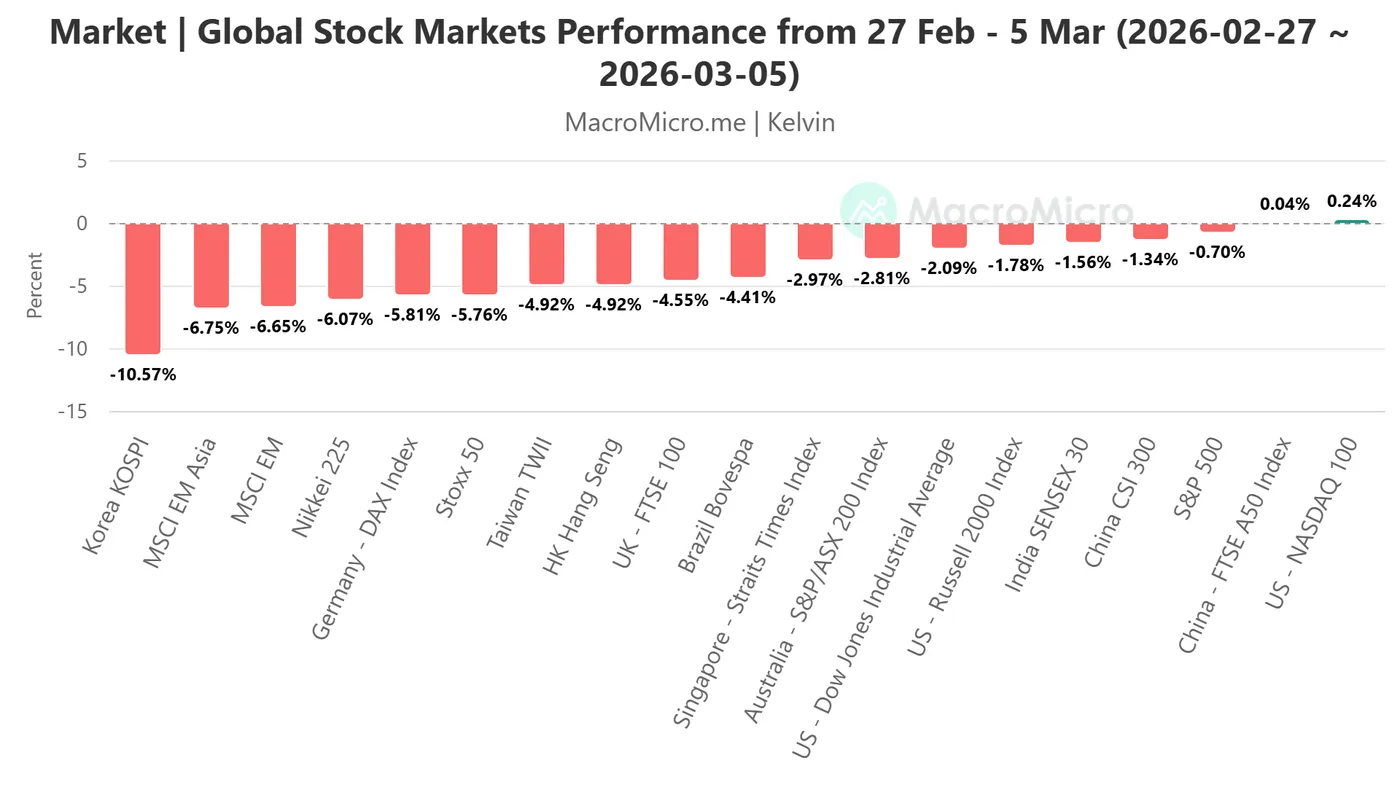

Since the start of the ongoing US-Iran war, Japan’s Nikkei 225 is one of the worst-performing key global benchmark stock indices due to being a major oil net importer, where the steep rally seen in oil prices in the past four days increases the odds of a negative feedback loop towards Japan’s economic growth prospects via the stagflation fear factor.

Japan’s Nikkei 225 is one of the worst-performing global benchmark stock indices

Fig. 1: Key global stock indices performances from 27 Feb 2026 to 5 Mar 2026 (Source: MacroMicro)

The Nikkei 225 staged a decline of 6.1% from last Friday, 27 February to Thursday, 5 March, underperforming other key Asia Pacific stock markets; Hong Kong’s Hang Seng Index (-4.9%), Singapore’s Straits Times Index (-3%), Australia’s ASX 200 (-2.8%), and China’s CSI 300 (-1.3%) (see Fig. 1).

Interestingly, the 4-day plunge of the Nikkei 225 is likely to stage a minor recovery at this juncture, supported by technical and intermarket factors.

Let’s dive deeper into these aspects.

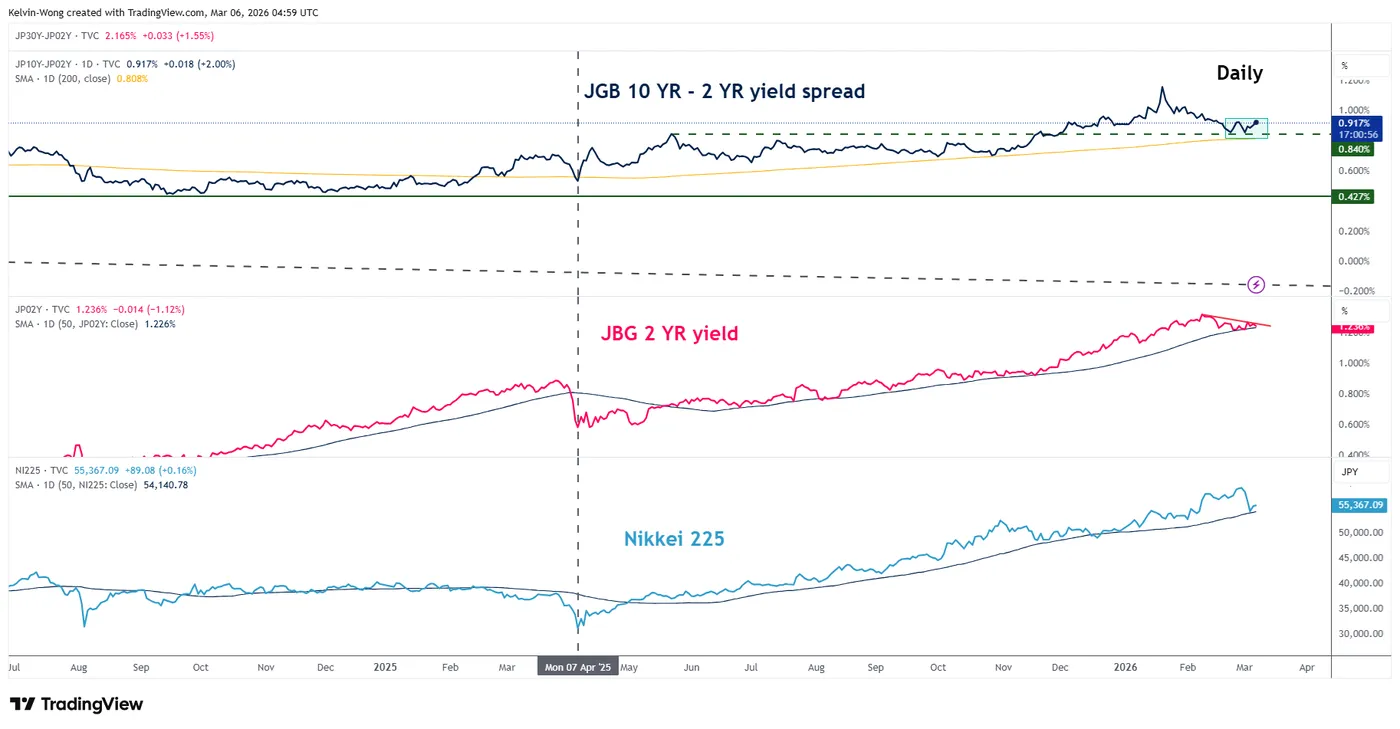

A lesser perceived hawkish BoJ triggers a bullish steepening of the JGB yield curve

Fig. 2: JGB yield curve (10-YR minus 2-YR) medium-term trend with Nikkei 225 as of 6 Mar 2026 (Source: TradingView)

Since the start of the ongoing major bullish trend phase of the Nikkei 225 from early April 2025, the upward trajectory of the Nikkei 225 has been supported and moved in a significant direct correlation with the steepening of the Japanese Government Bond (JGB) yield curve spread (10-year JGB yield minus 2-year JGB yield) (see Fig. 2).

As of 6 March 2026, the BoJ has conducted four interest rate hikes in its current tightening cycle, which began in 2024 as it exited from its ultra-easy monetary policy stance and negative interest rate environment.

The policy interest rate currently stands at 0.75%. Market participants polled by various media outlets expect the BoJ to continue its gradual interest rate hike policy by enacting 1 to 2 hikes in 2026 to bring the year-end target policy interest rate higher to 1.0%-1.25%.

The 2-year JGB yield is very sensitive to the latest monetary policy stance of the Bank of Japan (BoJ) as perceived by traders in the JGB market.

The 2-year JGB yield rocketed to a 30-year high of 1.31% on 9 February 2026 after the BoJ's last interest rate hike in December 2025, and Prime Minister Takaichi’s coalition party won a super majority in the lower house of Japan's parliament on 8 February 2026 snap election.

Since 9 February 2026, the 2-year JGB yield has softened by 7 basis points to trade at a current level of 1.24% at the time of writing and formed a “lower high” (see Fig. 2).

The current path of minor decline in the 2-year JGB, while still holding above its 50-day moving average, suggests that the BoJ may offer guidance to pause its interest rate hike cycle in the upcoming 19 March 2026’s monetary policy meeting due to the negative impact of higher oil prices arising from a prolonged US-Iran war.

A less hawkish expectation in BoJ’s future monetary policy stance can be implied by the recent rebound in the 10-year/2-year JGB yield curve spread, where a key support was tested at 0.84% (also its 200-day moving average) on Monday before it rebounded by 8 bps to trade at 0.92% at the time of writing (see Fig. 2).

Hence, a further bull steepening of the JGB yield curve (10-year minus 2-year) can translate into a minor recovery (at least in the first step after the 4-day plunge of the Nikkei 225 staged a retest on its 50-day moving average).

Let’s now look at the technical factors to determine Nikkei 225’s potential short-term trajectory (1 to 3 days).

Nikkei 225 – Bullish momentum at 50-day moving average

Fig. 3: Japan 225 minor trend as of 6 Mar 2026 (Source: TradingView)

The price actions of the Japan 225 CFD index (a proxy of the Nikkei 225 futures) have managed to find support at the 50-day moving thrice this week on three occasions; 3 March 2026, 4 March 2026, and 5 March 2026.

Watch the 54,100/52,960 key medium-term pivotal support, and a clearance above 56,530 increases the odds of a minor recovery to see the next intermediate resistances to come in at 57,140 (also the 20-day moving average) and 58,140, respectively (see Fig. 3).

On the flip side, a break with a daily close below 52,960 invalidates the recovery scenario to kickstart a medium-term downtrend phase (multi-week) to expose the next intermediate supports at 52,960 and 52,260 in the first step.

Key elements to support the bullish bias on the Nikkei 225

The recent rebound seen on the 54,100/52,960 key medium-term support zone also confluences with the major ascending channel support in place since the 7 April 2025 low.

The hourly RSI momentum indicator has staged a bullish breakout above its descending trendline resistance and jumped higher above the 50 level, a potential resurgence of minor bullish momentum condition.

Solid Labour Report May Put Growing Inflation Risks Even More in the Spotlight

Markets

One day. That’s all core bonds got in terms of reprieve. Bunds greatly underperformed Treasuries yesterday with huge offloading leading to net daily yield increases varying between +2.9 (30-yr) and +11.7 bps (5-yr) in a bear flattening move. Markets took aim at short-dated bonds amid rising expectations for ECB rate hikes. The market implied probability shot up to 65% (75% even, at some point) for a first move by end this year. This compares with a 55% chance end last week, before the Iran war erupted, for a rate cut. ECB meeting minutes released yesterday suggested that the central bank is ready to respond in both ways. That came amid a slew of warnings from the likes of de Guindos (ECB VP), Rehn (Finland) and Nagel (Germany) that a prolonged war in Iran may push up inflation (expectations). ECB policymakers have learned from the Ukraine war in 2022. Back then they wrote off the energy-led price spike as transitory. That may have been the case in the bygone era of a structurally low inflation. But things have changed. Oil prices meanwhile whipsawed on questionable headlines stating that Iran was ready to give up its highly enriched uranium stockpile and the Iranian commander of the ground forces saying that closing the Strait of Hormuz is not something they “believe in”. This morning, however, reports of a near-total halt of shipping traffic in the key oil artery for global supplies. Everything suggests oil prices to remain at elevated levels so long missiles are crossing Middle East air. It makes the US government contemplate to take action in the futures market to keep prices contained. Brent topped the $85 barrier yesterday and this morning for the first time since mid-2024. Dutch TTF gas futures pared initial 12% gains to 4% (>€50/Mwh). A looming energy crunch after the European economy barely recovered from the one in 2022 dents the appeal of regional assets. Stock markets tumbled 1.5% (EuroStoxx50). The euro lost territory, but losses could have been bigger. EUR/USD hovered around 1.16+ levels.

US yields trended higher but lacked European speed. The curve shifted 1.8-4.5 bps higher with the belly of the curve underperforming wings. Today’s payrolls have the potential to extend this week’s recovery. Fed Bowman said yesterday the labour market is showing additional evidence of stabilizing, indicating she favours the current rates status quo. There’s a long list of other Fed policymakers ready to air their thoughts before the quiet period kicks in this weekend. A solid labour market report may put the growing inflation risks even more in the spotlight, away from downside employment risks. Rate cuts could be pushed further out in time with markets for all of 2026 no longer pricing in two full rate cuts since this week. Against this backdrop we hold a bullish bias for the US dollar going into the weekend.

News & Views

The US Office of Foreign Assets Control (OFAC) of the US Treasury Department delivered a temporary license/waver to allow Indian refiners to buy Russian oil. The license applies to transactions of Russian crude oil and oil products that were loaded on/before March 5 with an expiry data as of April 4. US Treasury Secretary Scott Bessent indicated that the measure should be considered as a short-term measure to ‘enable oil to keep flowing into the global market’. The US assesses that the transaction will not provide significant financial benefit to the Russian government. It only authorizes transactions involving oil already at sea. The move is seen as a marked change in policy as the US in the recent past forced India to decouple from Russian oil purchases due to the war in Ukraine.

In an interview with Bloomberg published this morning, policymaker Henryk Wnorowski indicated that the National Bank of Poland (NBP) will avoid rate cuts until the war in Iran ends. Wnorowksi now indicates that likelihood of the policy rate to reach the 3.25%/3.5% as decreased dramatically. The comments come as the NBP on Wednesday still cut the policy rate by 25 bps to 3.75% as new projections showed that inflation was seen holding near the 2.5% target over the horizon till 2028. Referring to this week’s rate cut, the NBP policymaker indicated that leaving the policy rate unchanged this week would have sent an additional worrying signal to financial markets as already suffered from uncertainty due to the war in the Middle East. Despite the rate cut on Wednesday, the Polish 2-y swap rate yesterday already gained another 7 bps (to 3.80%) after rising sharply earlier this week (3.55% close on Friday). After weakening from levels near EUR/PLN 4.2175 end last week, the zloty now hovers around EUR/PLN 4.2725.

US Jobs Had Better Be Strong

Global markets continued to sell off on Thursday as Middle East tensions showed no sign of easing. Oil prices extended their rise. At its peak, US crude flirted with $83pb, while Brent crude approached $85pb. Sovereign yields continued to trend higher as well, amid growing worries that rising oil prices could force major central banks to tighten policy to fight a likely – and potentially notable – impact on inflation.

Announcements of potential measures from the US government to tame the oil price rally helped pour some cold water on the surge. These measures include a possible release of strategic oil reserves, loosening fuel-blending requirements, issuing a general licence allowing Russian oil sales to India (uh huh!), or even US Treasury trading oil futures – the latter would be unprecedented.

Now, US trading of oil futures could help counter speculation, but many doubt that government selling of oil futures would sustainably cap prices because the physical market ultimately drives pricing. Benchmarks such as Brent crude and West Texas Intermediate crude oil are tied to real supply and demand, so if a conflict in the Middle East disrupts flows for a prolonged period – say weeks or months – especially through chokepoints like the Strait of Hormuz, refiners will still bid up physical barrels regardless of financial selling.

On top of that, the oil futures market is enormous and highly liquid on exchanges such as CME Group and Intercontinental Exchange, meaning government intervention could easily be absorbed unless it were extremely large. As such, there is a risk that traders would see such selling as temporary and buy the dip, limiting its impact on prices – a bit like USD/JPY interventions.

So unsurprisingly, oil is pushing higher again this morning and sovereign yields are rising, though Asian indices are rebounding slightly and US and European futures trade in the green after a harsh week that saw the MSCI World ex-US shed more than 5% at its worst since Monday, while US indices delivered a relatively muted reaction to the war headlines.

The US benefited from its energy producer status. The US dollar saw strong inflows as investors sold their European and Asian holdings – reversing the earlier rotation trade – and moved back into US dollar. The dollar has the advantage of naturally benefiting when energy prices rise, as most energy trade is denominated in dollars and rising energy prices increase the dollar demand, pushing its price higher.

This combination of rising energy prices, more hawkish central bank expectations, higher yields and weaker appetite for risk assets will likely remain in play as long as Middle East tensions have a lasting impact on oil and gas prices.

For central bank watchers, it means that inflation dynamics may regain the upper hand in the coming months. This shift matters particularly for Federal Reserve (Fed) watchers – so essentially all of us – because the Fed had recently shifted its focus toward protecting the labour market while tolerating inflation running meaningfully above its 2% target. US inflation has been relatively stable around the 3% mark. But if price pressures start to build and push inflation – already running stubbornly above target – even higher, the Fed could forget about the two rate cuts that were broadly priced in before the Middle East conflict escalated.

So today’s US jobs data would ideally come in strong to keep market sentiment as positive as possible heading into the weekend. Weak data would struggle to fuel dovish Fed expectations at a time when inflation risks are rising alongside energy prices. The US economy is expected to have added around 58K new nonfarm jobs, according to the Bloomberg consensus. Average hourly earnings are seen holding near 3.7% year-on-year – still somewhat elevated for inflation to comfortably return to the 2% target – while the unemployment rate is expected to remain around 4.3%.

Given rising inflation risks, stronger data could trigger a positive market reaction, while weaker-than-expected figures could fuel stagflation concerns – rising unemployment alongside persistent inflation – and weigh on US equities ahead of the weekly close.

Beyond the Middle East headlines, one of yesterday’s most demoralizing developments was news that the US government plans to introduce a licensing requirement for certain advanced chip exports, forcing foreign companies to seek US government approval before acquiring these chips. The aim is to control the spread of advanced AI technologies and maintain the US technological edge. While understandable in the current geopolitical environment, it is not great news for Nvidia and AMD, which initially sold off before recovering some losses.

Overall, this week has injected a large dose of geopolitical uncertainty into a market environment that was already unsettled by concerns about Big Tech’s heavy AI spending – increasingly financed by debt – fears that AI could disrupt many business models and jobs, and growing stress in private credit markets.

The immediate market reaction was to buy US dollars and reverse the rotation trade from the US into Europe and Asia. Gold – traditionally both a safe haven and an inflation hedge – showed a surprisingly muted reaction to the rise in Middle East tensions, while defense and energy stocks outperformed as mining stocks gave back some gains, and airline companies got hammered.

Looking ahead, Middle East developments will likely remain in the headlines, though the initial surprise factor will gradually fade, meaning the knee-jerk reaction to headlines may become less pronounced. However, oil and energy prices will remain key in shaping inflation expectations and therefore central bank policy expectations, which in turn will drive global risk appetite.

As for oil prices, many analysts warn that crude could move toward the $100pb level if the conflict deepens. That is certainly a possibility. But the key question is not only how high prices rise, but how long they stay elevated. The longer energy prices remain high, the tighter global financial conditions become – and the weaker the appetite for risk assets.

US Jobs Data Takes Focus Amid Middle East Unrest

In focus today

The most important release today is the US February jobs report. Early high frequency indicators, like jobless claims, ADP's weekly private sector employment estimate and Indeed Hiring Lab's daily online job postings have generally signalled improving labour market conditions into February. We still expect a modest slowdown in NFP growth to +70k from 130k in January and unemployment rate to remain steady at 4.3%.

In the euro area, the third estimate of Q4 2025 GDP is released including a breakdown of the national accounts and the ECB's preferred wage growth measure, compensation per employee. The wage data is the most important and we expect it to remain at 4.0% y/y.

In Germany, Sunday's state election in Baden‑Württemberg will be the first test this year for Friedrich Merz and his grand coalition. Home to around 11 million residents and one of Germany's most economically important regions, the state has been governed by the Greens since 2011. With the Minister‑President not standing for re‑election, the CDU's Manuel Hagel leads in recent polls, with the CDU on 28%, the Greens on 25% and AfD on 19%. The result will be a bellwether for voters' sentiment towards the grand coalition.

Economic and market news

What happened overnight

In India, the US granted a temporary 30-day waiver to purchase sanctioned Russian oil, aiming to alleviate supply disruptions stemming from the Middle East conflict. Treasury Secretary Bessent clarified that the waiver applies only to stranded transactions and thus is not expected to provide significant financial benefit to Moscow.

What happened yesterday

In the Middle East, the conflict ended its sixth day as Iran reportedly attacked Azerbaijan and targeted additional tankers in the Gulf, pushing Brent crude up 5% to 85.4 USD/bbl and European natural gas prices 6% higher to 50.2 EUR/MWh. President Trump claimed he must be involved in appointing Iran's next leader, dismissing the candidacy of Mojtaba Khamenei, who is expected to continue his father's policies. This position contrasts with the White House's statement that regime change is not the primary objective of the military campaign. Despite soaring energy costs, Trump told Reuters he has no plans to tap the Strategic Petroleum Reserve, stating: "If they rise, they rise".

In the US, weekly jobless claims remained steady at low levels, unchanged at 213k for the week ending 28 February. Continuing claims ticked slightly higher, but not meaningfully so. The February Challenger report showed that even though firms' hiring announcements remained subdued, layoff announcements declined sharply to 48.3k from January's 108k SA. This suggests that US firms are still not under pressure to cut labour costs with layoffs.

Flash Q4 productivity growth slowed to 2.8% q/q AR (Q3: 5.2%), reflecting the weaker-than-expected GDP print from earlier. This lifted unit labour cost growth to 2.8% q/q AR (Q3: -1.8%). In the big picture, US labour cost pressures have cooled to modest levels in a historical context.

In the euro area, ECB speakers were on the wires commenting on impact of war in the Middle East. Highlighting both that the inflation expectations are key, duration of the war matters, that risks are on inflation but also could weigh on economic growth. Schnabel is set to speak Friday at 18:00 CET, which could easily provide a firm hawkish push given the recent rise in energy prices.

In Sweden, February flash inflation came in close to forecast. CPIF ex energy (core) came in at 1.38% y/y (forecast: 1.41%), while CPIF (the Riksbank's target variable) registered at 1.71% y/y (forecast: 1.75%), and CPI at 0.48% y/y, just shy of our projection of 0.52%. Deviations stemmed from lower energy prices and core goods, while food prices exceeded expectations. This marks the first time Statistics Sweden has published preliminary figures at a detailed level, and the monthly development since January is close to our forecast. R

Japan's largest labour union group, Rengo, is targeting a 5.94% average wage hike this year, slightly below last year's demand (6.09%) but still robust. Last year the result ended at 5.25%. A strong outcome is crucial to prevent core inflation from falling below target and remains a key condition for further BoJ rate hikes. Initial results from major firm negotiations are expected in the coming weeks.

Equities: Global equities declined modestly yesterday, with the MSCI world down 0.2%. This came despite continued relatively large intraday swings. However, please note that on an aggregate level the moves throughout the week have remained contained.

It is also worth noting the internal market dynamics: both tech and consumer discretionary finished higher yesterday. Looking across the week since the outbreak of the conflict involving Iran,cyclicals have actually outperformed defensives, and the NASDAQ is also higher this week.

This is quite telling of how a large part of the market is interpreting the situation and reflects the starting point going into the escalation. As discussed in earlier morning comments, one of the most interesting observations this week is the number of reversal trades that have been taking place. This morning most Asian equity markets are trading higher, European futures are up and US futures are marginally higher.

FI and FX: There was a dramatic rise in European government bond yields and rates as well as US government bond yields yesterday as oil and gas prices continue to rise given the uncertainty about when the war in the Middle East will end. This morning, there has been some spillover effect to the Asian bond markets with a modest rise in Australian government bond yields etc. US Treasuries have risen only very modestly in Asian trading this morning.

Today, the US labour market report is released and if the report comes out to the strong side it will add to the pressure on bond yields and swap rates. We have seen a rise in both the VIX index and the Move index (equity and rates volatility) as well as credit spreads (such as ITRAX) but there have been modest moves in the Schatz ASW-spread, so we are still not seeing a significant risk-off move as we have seen in the past.

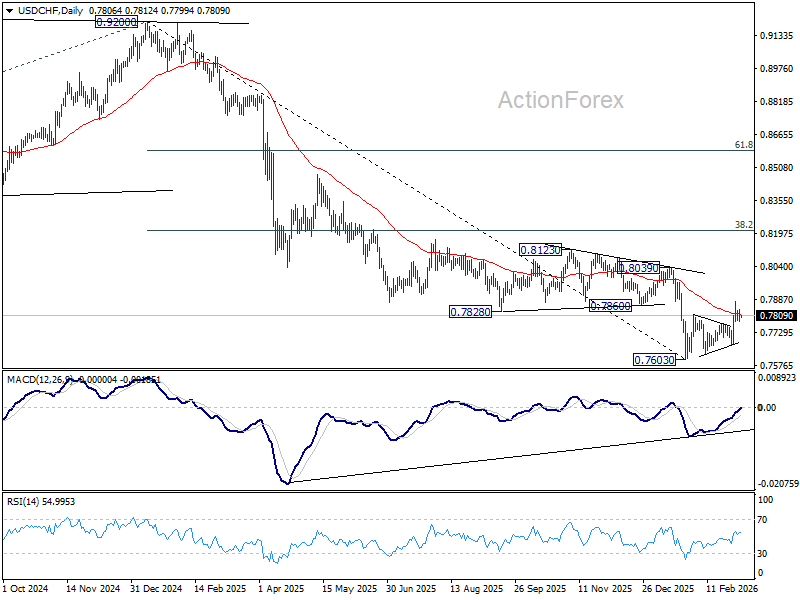

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7781; (P) 0.7810; (R1) 0.7838; More….

Intraday bias in USD/CHF remains neutral and more consolidations could be seen below 0.7877 temporary top first. Further rise is expected as long as 0.7671 support holds. Rebound from 0.7603 is seen as correcting the whole fall from 0.9022. Above 0.76877 will target 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213.

Markets Hold Breath for Crucial Payrolls, Oil Surges Dollar Holds Lead

The current market environment is the definition of a "powder keg" waiting for a spark, something that the February US Non-Farm Payroll report could be. While the Wednesday relief rally offered a temporary reprieve, the swift pullback in US stocks overnight suggests that bulls lack the conviction to fight against a darkening energy backdrop.

At the same time, WTI breaking 80 psychological level is not just a technical breakout; it is a fundamental alarm bell. With the Strait of Hormuz facing a de facto closure and the White House offering no timeline for a resolution, we are seeing a "war premium" being baked into every barrel.

Meanwhile, the U.S. decision to grant a 30-day waiver to India for Russian crude is a clear admission of vulnerability. By allowing "stranded" Russian oil to reach Indian refiners, Washington is attempting to cap global prices without formally backing down on sanctions. This "stopgap" measure highlights the desperation to keep the global economy from seizing up before the Middle East conflict finds a floor.

The significance of the US jobs data has been amplified by the geopolitical backdrop. With the Middle East conflict pushing oil prices higher and reviving inflation risks, a strong payrolls report could further reduce expectations for Fed rate cuts. Such a scenario would likely support higher Treasury yields and provide further strength to the Dollar.

For the week so far, Dollar remains the strongest performer among major currencies. Loonie follows closely behind, benefiting from rising oil prices, while Sterling holds third place. At the other end of the spectrum, Euro remains the weakest currency, reflecting concerns about Europe’s exposure to energy disruptions. Swiss Franc and Kiwi also lag, while the Aussie and Yen sit near the middle of the performance rankings.

In Asia, Nikkei closed up 0.57%. Hong Kong HSI is up 1.74%. China Shanghai SSE is up 0.32%. Singapore Strait Times is up 0.18%. Japan 10-year JGB yield rose 0.007 to 2.164. Overnight, DOW fell -1.61%. S&P 500 fell -0.56%. NASDAQ fell -0.26%. 10-year yield rose 0.066 to 4.146.

War shock amplifies NFP stakes, Dollar set for double-engine boost

Today’s US Non-Farm Payroll report has taken on unusual importance in a week dominated by geopolitical turmoil. The escalation of conflict in the Middle East has triggered a surge in oil prices and pushed US Treasury yields sharply higher, with the 10-year yield climbing above 4.14% overnight. Dollar has remained broadly firm as investors reassess inflation risks and monetary policy expectations.

Under normal circumstances, the monthly payroll report is already one of the most influential data releases for global markets. But this week’s geopolitical developments have amplified its significance. Skyrocketing energy costs has already threatened to keep headline inflation elevated for longer. Market expectations for Fed policy have shifted noticeably over the past few days.

Traders have started to abandon the view that the Fed could resume easing in June. Instead, September 2026 is increasingly seen as the earliest realistic timing for the next reduction. The shift does not stop there. Markets are now pricing only a single quarter-point cut for the entire year, a sharp downgrade from earlier expectations of multiple reductions as inflation gradually cooled.

With this backdrop, a strong NFP would almost certainly push the 10-year yield higher. That would also act as a powerful "double engine" for Dollar, with the rise in the 10-year yield providing the mechanical fuel for the greenback's ascent.

Economists expect payroll growth in the range of 58k to 65k jobs. The unemployment rate is forecast to hold steady at 4.3%, while average hourly earnings are expected to increase by around 0.3% to 0.4% mom.

Recent labor indicators point to a resilient, though not overheated, labor market. ADP private payrolls rose by 63k earlier this week, beating expectations The employment component of ISM Services climbed to 51.8. Since the service sector is the largest employer in the US, this expansionary reading points toward a stronger headline NFP.

At the same time, the latest JOLTS report showed job openings falling to 6.54 million, the lowest since 2020. But that's more of a little "crack" in the armor only.

Technically, 10-year yield's strong rebound this week and firm break of 4.106 resistance suggests that fall from 4.311 has completed at 3.956. The development kept 10-year yield within the converging triangle that started back in 4.629 (or 3.886). That is, medium term outlook is neutral, instead of being bearish.

Further rise is now in favor in the near term towards 4.311 resistance. But strong resistance is expected there to cap upside to continue range trading.

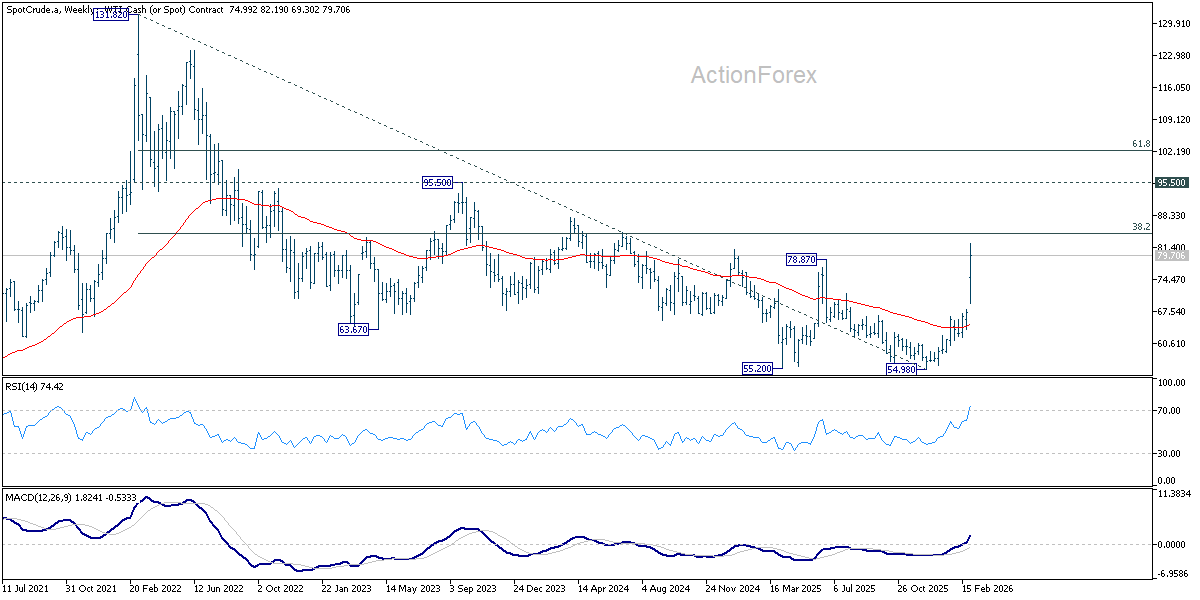

WTI Oil crosses 80 after White House timeline uncertainty, 84.3 now key

Crude oil has entered a new phase of the geopolitical crisis. WTI crude officially broke above the 80 per barrel level, marking both an important psychological milestone and its highest level since mid-2024. The move reflects a shift in market perception—from treating the Middle East conflict as a temporary geopolitical flare-up to pricing a more sustained disruption to global energy flows.

The latest "bullish nudge" came from comments of White House press secretary Karoline Leavitt, who said the Trump administration has no timeline for when commercial shipping through the Strait of Hormuz will be safe again. When asked about reopening the critical waterway, Leavitt declined to commit to any timeframe, saying the situation is still being “actively calculated” by both the Department of War and the Department of Energy.

For energy markets, the absence of a timeline was itself the message. Traders had been looking for signals that military operations were close to stabilizing the shipping route. Instead, the administration’s remarks suggested that the roughly 20 million barrels of oil that normally transit the Strait of Hormuz each day may remain effectively off the market for an extended period.

Equally important was the implication that restoring commercial shipping is not currently the immediate priority. Leavitt’s wording suggested that U.S. strategy may still be focused on degrading Iranian military infrastructure rather than quickly reopening the sea lanes for tankers. That interpretation reinforced fears that the disruption could persist longer than previously assumed.

Technically, the latest rally has also triggered an important chart development. WTI’s break above the key resistance level at 78.87 could confirm the completion of a medium-term double bottom pattern formed around the 55.20 and 54.98 lows. That structure suggests the multi-year downtrend from the 2022 peak at 131.82 may be reversing.

If that interpretation holds, attention now turns to the next major technical level of 38.2% retracement of 131.82 to 54.98 at 84.33. A decisive break above that level would strengthen the case that crude has entered a broader up trend rather than simply experiencing a war-driven spike.

That could trigger further upward acceleration to 95.50 structural resistance or even further to 61.8% retracement at 102.46.

Still, the rally remains sensitive to shifts in geopolitical expectations. A drop below 73.35 support level would signal stabilization in some form. Oil prices may then enter a consolidation phase while waiting for further developments in the conflict.

Fed’s Barkin: Inflation fight not over amid strong data and war risks

Richmond Fed President Thomas Barkin cautioned that the Fed need to reassess its policy risks as recent economic data and geopolitical developments complicate the inflation outlook. In remarks to Bloomberg Television overnight, Barkin highlighted that stronger job growth and persistently elevated inflation readings could challenge earlier assumptions about the trajectory of price pressures.

He noted that last year’s rate cuts were justified largely by concerns that the labor market was weakening while inflation risks were fading. However, :the data that's come in over the last couple months suggests it has moved in the other direction," he said.

At the same time, the ongoing conflict between the U.S. and Iran could further intensify inflation risks through higher energy prices. With recent run of stronger inflation readings, "that certainly puts pause to any conclusion that we're done fighting this," he emphasized.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7781; (P) 0.7810; (R1) 0.7838; More….

Intraday bias in USD/CHF remains neutral and more consolidations could be seen below 0.7877 temporary top first. Further rise is expected as long as 0.7671 support holds. Rebound from 0.7603 is seen as correcting the whole fall from 0.9022. Above 0.76877 will target 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213.

War shock amplifies NFP stakes, Dollar set for double-engine boost

Today’s US Non-Farm Payroll report has taken on unusual importance in a week dominated by geopolitical turmoil. The escalation of conflict in the Middle East has triggered a surge in oil prices and pushed US Treasury yields sharply higher, with the 10-year yield climbing above 4.14% overnight. Dollar has remained broadly firm as investors reassess inflation risks and monetary policy expectations.

Under normal circumstances, the monthly payroll report is already one of the most influential data releases for global markets. But this week’s geopolitical developments have amplified its significance. Skyrocketing energy costs has already threatened to keep headline inflation elevated for longer. Market expectations for Fed policy have shifted noticeably over the past few days.

Traders have started to abandon the view that the Fed could resume easing in June. Instead, September 2026 is increasingly seen as the earliest realistic timing for the next reduction. The shift does not stop there. Markets are now pricing only a single quarter-point cut for the entire year, a sharp downgrade from earlier expectations of multiple reductions as inflation gradually cooled.

With this backdrop, a strong NFP would almost certainly push the 10-year yield higher. That would also act as a powerful "double engine" for Dollar, with the rise in the 10-year yield providing the mechanical fuel for the greenback's ascent.

Economists expect payroll growth in the range of 58k to 65k jobs. The unemployment rate is forecast to hold steady at 4.3%, while average hourly earnings are expected to increase by around 0.3% to 0.4% mom.

Recent labor indicators point to a resilient, though not overheated, labor market. ADP private payrolls rose by 63k earlier this week, beating expectations The employment component of ISM Services climbed to 51.8. Since the service sector is the largest employer in the US, this expansionary reading points toward a stronger headline NFP.

At the same time, the latest JOLTS report showed job openings falling to 6.54 million, the lowest since 2020. But that's more of a little "crack" in the armor only.

Technically, 10-year yield's strong rebound this week and firm break of 4.106 resistance suggests that fall from 4.311 has completed at 3.956. The development kept 10-year yield within the converging triangle that started back in 4.629 (or 3.886). That is, medium term outlook is neutral, instead of being bearish.

Further rise is now in favor in the near term towards 4.311 resistance. But strong resistance is expected there to cap upside to continue range trading.