Sample Category Title

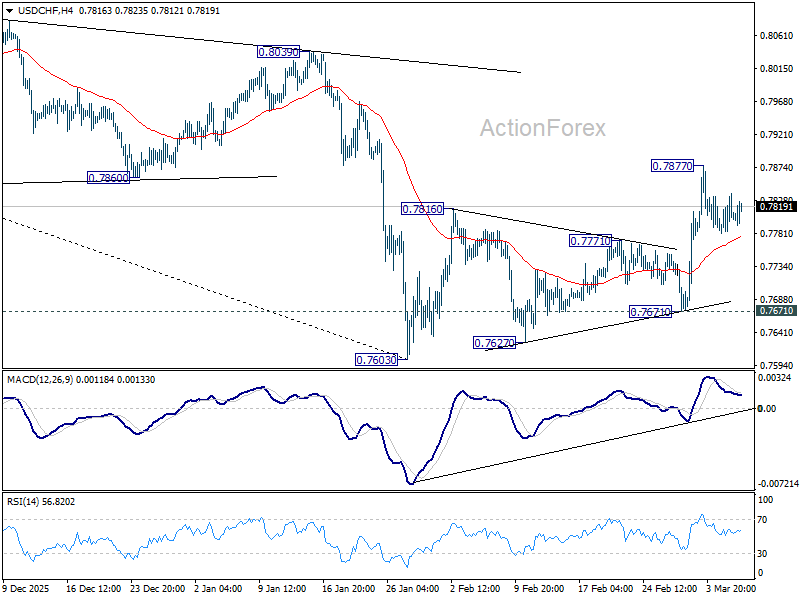

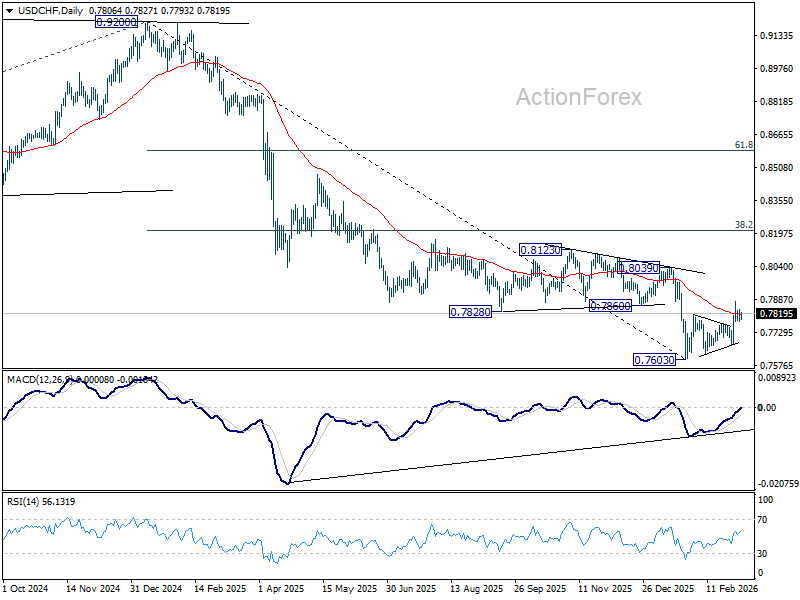

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7781; (P) 0.7810; (R1) 0.7838; More….

USD/CHF is still extending consolidations below 0.7877 and intraday bias stays neutral. Further rise is expected as long as 0.7671 support holds. Rebound from 0.7603 is seen as correcting the whole fall from 0.9022. Above 0.76877 will target 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213.

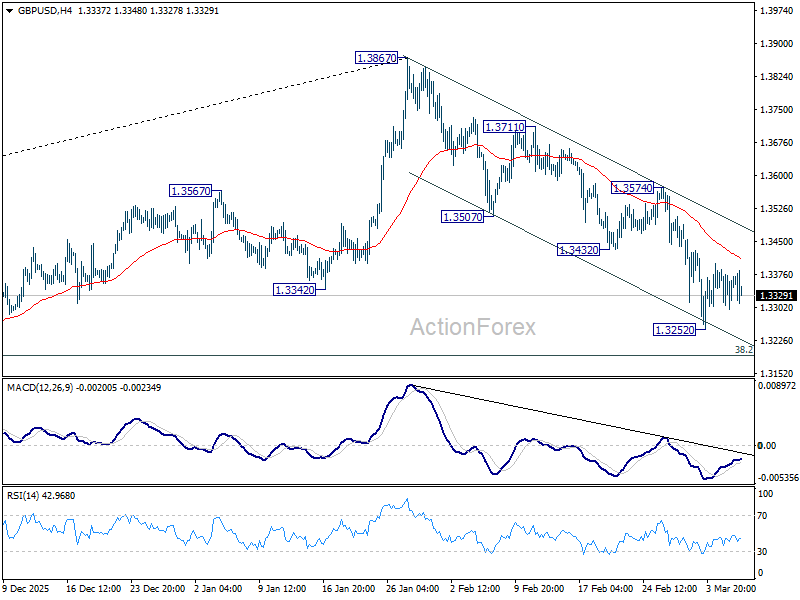

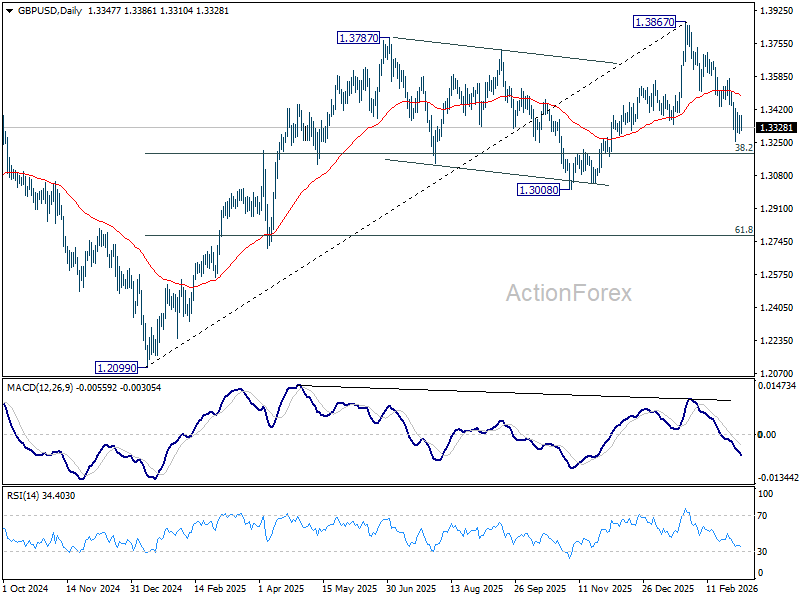

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3308; (P) 1.3347; (R1) 1.3397; More...

GBP/USD is still bounded in consolidations in tight range above 1.3252 and intraday bias remains neutral. Fall from 1.3867 should at least be correcting the rise from 1.2009. Below 1.3252 will target 38.2% retracement of 1.2099 to 1.3867 at 1.3192. Sustained break there will pave the way to 1.3008 support. For now, risk will stay on the downside as long as 1.3574 resistance holds, in case of recovery.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

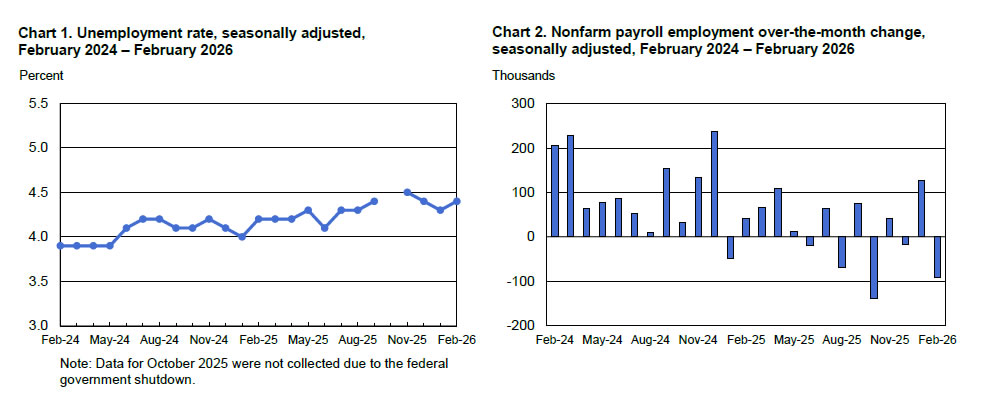

US: Employment Unexpectedly Declines in February and Unemployment Rate Tcks up to 4.4%

Nonfarm payrolls declined by 92k in February, well below the consensus forecast calling for a gain of 55k. Revisions to the two prior months subtracted a total of 69k from the previously reported figures, with the bulk of the revisions concentrated in December.

- Smoothing through the volatility, nonfarm payrolls have averaged just 6k per-month over the last three months, slightly below the prior twelve-month average of 24k.

Private payrolls fell by 86k, following a gain of 146k in January, with the bulk of the pullback coming from health care & social assistance (-18.6k after adding 116.4k in January). However, part of the reversal in health care (~37k) reflected a strike among offices of physicians. Job losses were also seen in weather-sensitive sectors like construction (-11k) and leisure & hospitality (-27k), though manufacturing (-12k), information (-11k) and professional & business services (-5k) also saw modest declines.

- Federal job cuts appear to be slowing, as the sector shed just 10k jobs last month, fewer than the 18k averaged over the prior three months.

In the household survey, an increase in the number of unemployed (+203k) offset stagnant growth in the labor force – pushing the unemployment rate up to 4.4%.

The household survey also included new population controls to better align with the Census Bureau estimates. The revisions were implemented as of January 2026, but the historical data prior to 2026 were left unchanged. Civilian population was revised lower by just 306k. But because the adjustment proportionally shifted the labor force, unemployment and employment levels, January's unemployment rate was kept unchanged at 4.3%.

Average hourly earnings (AHE) rose 0.4% month-on-month (m/m), matching January's gain. On a twelve-month basis, AHE ticked up to 3.8%.

Key Implications

A big miss on employment for February, with private payrolls recording its sharpest decline since December 2020. However, some of the pullback can be attributed to health care services, where job growth was impacted by an ongoing strike and comes on the heels of an unusually strong gain in January. Moreover, hiring activity was also notably weak in weather sensitive sectors, like construction and leisure & hospitality – suggesting last month's poor weather conditions may have helped to restrain hiring. And while the unemployment rate ticked higher, the broader U-6 measure, which includes individuals working part-time for economic reasons, fell to a seven-month low of 7.9%.

Bigger picture, this morning's release doesn't fundamentally alter our view on the labor market. From a policy perspective, the bigger threat to the Fed's dual mandate has shifted back to price stability. Core measures of inflation remain stubbornly elevated with this week's escalation of the Iran conflict adding further upside risk amid the spike in oil prices. Fed futures aren't fully pricing in the next rate cut until September and there are doubts about whether there will be a second this year – with a total of 44 basis points of easing priced by year-end.

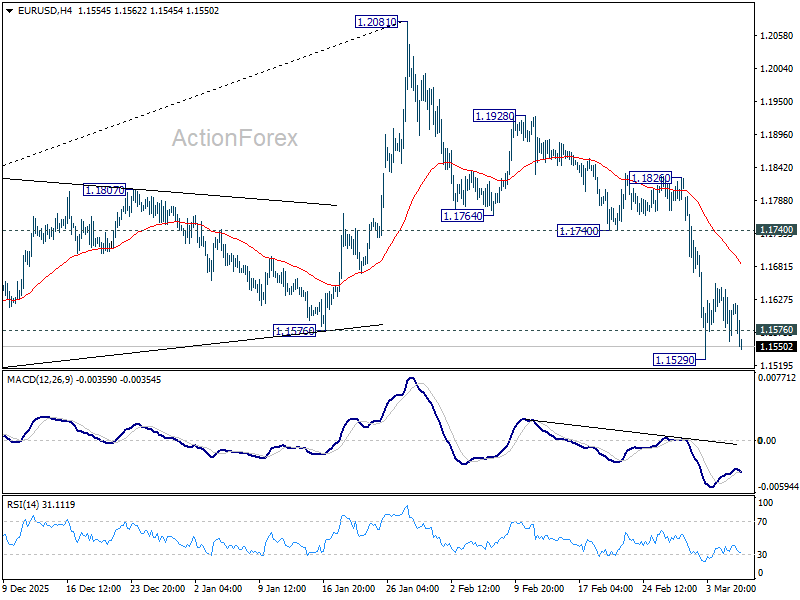

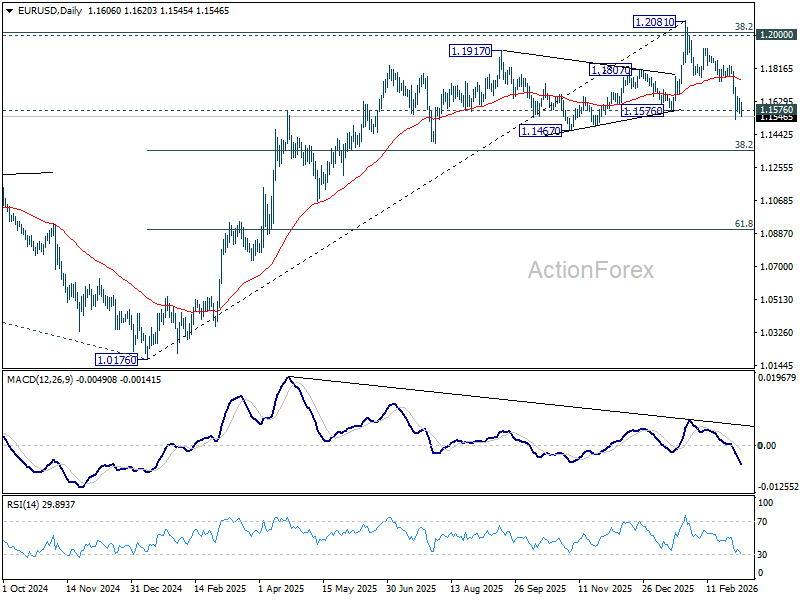

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1564; (P) 1.1605; (R1) 1.1652; More….

EUR/USD weakened notably today but stays above 1.1529 temporary low. Intraday bias stays neutral first. On the downside, below 1.1529 will resume the fall from 1.2081. Sustained break of 1.1576 structural support would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. In any case, risk will stay on the downside as long as 1.1740 support turned resistance holds.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Oil Shock Drowns Out Weak NFP, Risk Aversion Supports Dollar

Markets appeared largely unfazed by the shockingly weak US non-farm payroll report, as attention is already occupied by the explosive surge in oil prices. WTI crude has broken decisively above the 85 mark and continues to climb as the US session begins, turning energy markets into the dominant driver of global sentiment.

The weak payrolls report has shifted Fed expectations. The probability of the Fed holding rates at the current 3.50–3.75% range has fallen to around 50%, compared with roughly 67% just a day earlier. In effect, a 25-basis-point rate cut in the first half of the year has marginally returned to the table. However, the outlook remains highly dependent on how inflation evolves amid surging energy prices.

Surprisingly, Dollar has not weakened in response to the poor jobs report. Instead, the greenback is drawing support from risk aversion as equity markets come under pressure. DOW futures have fallen more than -1.2%, signaling a sharply weaker open for US equities and reinforcing safe-haven demand for the Dollar.

The real shock to markets is coming from the oil complex. WTI’s surge above 85 signals that markets are transitioning from geopolitical “risk-off” concerns to a more severe phase of structural panic. The effective blockade of the Strait of Hormuz provided the initial spark, but the latest comments from Qatar Energy Minister Saad al-Kaabi have dramatically intensified fears of a prolonged supply crisis.

Kaabi warned that Gulf energy exporters may soon declare force majeure, a move that would legally free them from their contractual delivery obligations. Such a scenario would mean that the world is no longer facing a temporary logistical disruption but rather a potential evaporation of Middle Eastern supply.

The minister’s remarks have also introduced a new psychological anchor for energy markets. By openly referencing the possibility of oil reaching 150 per barrel, Kaabi has effectively reset the upper bound of market expectations. Traders are increasingly beginning to price in the “chain reaction” he described.

That chain reaction could involve shortages of both crude oil and LNG feedstocks, forcing industrial shutdowns across Europe and Asia if supply disruptions persist. In that context, the recent surge above 85 is no longer seen as an extreme price level but rather an early stage of a potentially much larger move.

Even a rapid de-escalation in the Middle East may not immediately stabilize energy markets. With tanker traffic halted through the Strait of Hormuz, restoring supply chains could take weeks or even months after hostilities end.

In the currency markets, for the week so far, Loonie is the strongest performer, benefiting directly from rising oil prices, while the US Dollar holds second place as risk aversion lifts demand for safe assets. Sterling follows as the third-best performer. At the other end of the spectrum, Kiwi is the weakest currency this week, followed by Euro and Aussie. Swiss Franc are trading near the middle of the pack as markets grapple with the increasingly dominant energy shock narrative.

In Europe, at the time of writing, FTSE is down -1.28%. DAX is down -1.56%. CAC is down -1.39%. UK 10-year yield is up 0.174 at 4.655. Germany 10-year yield is up 0.029 at 2.874. Earlier in Asia, Nikkei rose 0.62%. Hong Kong HSI rose 1.72%. China Shanghai SSE rose 0.38%. Singapore Strait Times rose 0.03%. Japan 10-year JGB yield rose 0.009 to 2.166.

NFP misses big with -92k jobs, but wages hold up

US labor market data delivered a sharp downside surprise in February as non-farm payroll employment contracted by -92k, far below expectations for a 65k increase. The report marks a significant setback for the labor market outlook and contrasts with the relatively resilient signals from earlier indicators such as ADP and ISM employment data.

The details of the report were also weaker than expected. The unemployment rate rose from 4.3% to 4.4%, while the labor force participation rate slipped by -0.1 percentage point to 62.0%.

In addition, payroll revisions were notably negative, with December’s figure revised down by 65k to -17k and January trimmed slightly to 126k, further highlighting the softening momentum in hiring.

Despite the weakness in employment growth, wage pressures remained firm. Average hourly earnings rose by 0.4% mom, above expectations of 0.3%, while annual wage growth held at a solid 3.8%. The average workweek was unchanged at 34.3 hours.

Fed’s Waller downplays oil surge as temporary inflation shock

Fed Governor Christopher Waller signaled that the recent surge in oil prices tied to the Middle East conflict may not significantly alter the longer-term inflation outlook. Speaking to Bloomberg Television, Waller acknowledged that Americans will likely see a noticeable jump in gasoline prices in the near term, warning that drivers could be “a little shocked” when they see prices at the pump.

However, Waller emphasized that if the spike in energy prices unwinds within a few weeks or even a couple of months, "it's not going to be a big factor down the road."

From a policy perspective, Waller characterized the current oil shock as closer to a “one-off event” rather than a sustained inflation driver. He reiterated that the Fed focuses primarily on core inflation—which excludes volatile components such as energy and food—precisely because commodity prices can fluctuate sharply in response to temporary shocks without altering the underlying inflation trend.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1564; (P) 1.1605; (R1) 1.1652; More….

EUR/USD weakened notably today but stays above 1.1529 temporary low. Intraday bias stays neutral first. On the downside, below 1.1529 will resume the fall from 1.2081. Sustained break of 1.1576 structural support would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. In any case, risk will stay on the downside as long as 1.1740 support turned resistance holds.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Fed’s Waller downplays oil surge as temporary inflation shock

Fed Governor Christopher Waller signaled that the recent surge in oil prices tied to the Middle East conflict may not significantly alter the longer-term inflation outlook. Speaking to Bloomberg Television, Waller acknowledged that Americans will likely see a noticeable jump in gasoline prices in the near term, warning that drivers could be “a little shocked” when they see prices at the pump.

However, Waller emphasized that if the spike in energy prices unwinds within a few weeks or even a couple of months, "it's not going to be a big factor down the road."

From a policy perspective, Waller characterized the current oil shock as closer to a “one-off event” rather than a sustained inflation driver. He reiterated that the Fed focuses primarily on core inflation—which excludes volatile components such as energy and food—precisely because commodity prices can fluctuate sharply in response to temporary shocks without altering the underlying inflation trend.

NFP misses big with -92k jobs, but wages hold up

US labor market data delivered a sharp downside surprise in February as non-farm payroll employment contracted by -92k, far below expectations for a 65k increase. The report marks a significant setback for the labor market outlook and contrasts with the relatively resilient signals from earlier indicators such as ADP and ISM employment data.

The details of the report were also weaker than expected. The unemployment rate rose from 4.3% to 4.4%, while the labor force participation rate slipped by -0.1 percentage point to 62.0%.

In addition, payroll revisions were notably negative, with December’s figure revised down by 65k to -17k and January trimmed slightly to 126k, further highlighting the softening momentum in hiring.

Despite the weakness in employment growth, wage pressures remained firm. Average hourly earnings rose by 0.4% mom, above expectations of 0.3%, while annual wage growth held at a solid 3.8%. The average workweek was unchanged at 34.3 hours.

WTI: Crude Oil on Track for Biggest Weekly Gain in Four Years

WTI Oil price jumped above $86 per barrel on Friday, extending steep ascend into fifth straight day, on track for the biggest and steepest weekly gain since early 2022, when the war in Ukraine started.

Growing fears of stronger supply disruption due to closure of Hormuz strait and signals that war may extend until September, or more worrying latest comment from President Trump that there are no time limits for the duration of the war, are expected to continue to inflate oil prices.

On the other hand, Russian oil supply remains stable (US lifted some sanction for buying Russian oil) that may partially offset negative impact.

The latest market action and deteriorating conditions suggest that oil price can hit $100 per barrel, which is still away from spikes in 2022 ($130) and 2008 ($147).

Friday’s strong acceleration surged through round-figure $80 barrier and broke technical resistance at $85.53 (Fibo 76.4% of $95.00/$54.87, 2023/2025 downtrend), violation of which to open way towards Apr 2024 double-top ($87.61) and unmask $90 barrier.

Although the price action remains well supported by favorable fundamentals (key driver), we should expect some price adjustments as daily and weekly studies are strongly overbought and some traders are likely to collect profit profits at the end of the week.

However, dips are likely to be limited to keep larger bulls intact and provide better levels to re-enter strong bullish market.

Broken barriers at $80 (round-figure) and nearby $79.67 (Fibo 61.8% of $95.00/$54.87) reverted to supports which should ideally contain dips.

Res: 86.67; 87.61; 89.38; 90.00.

Sup: 84.90; 83.50; 81.80; 80.00.

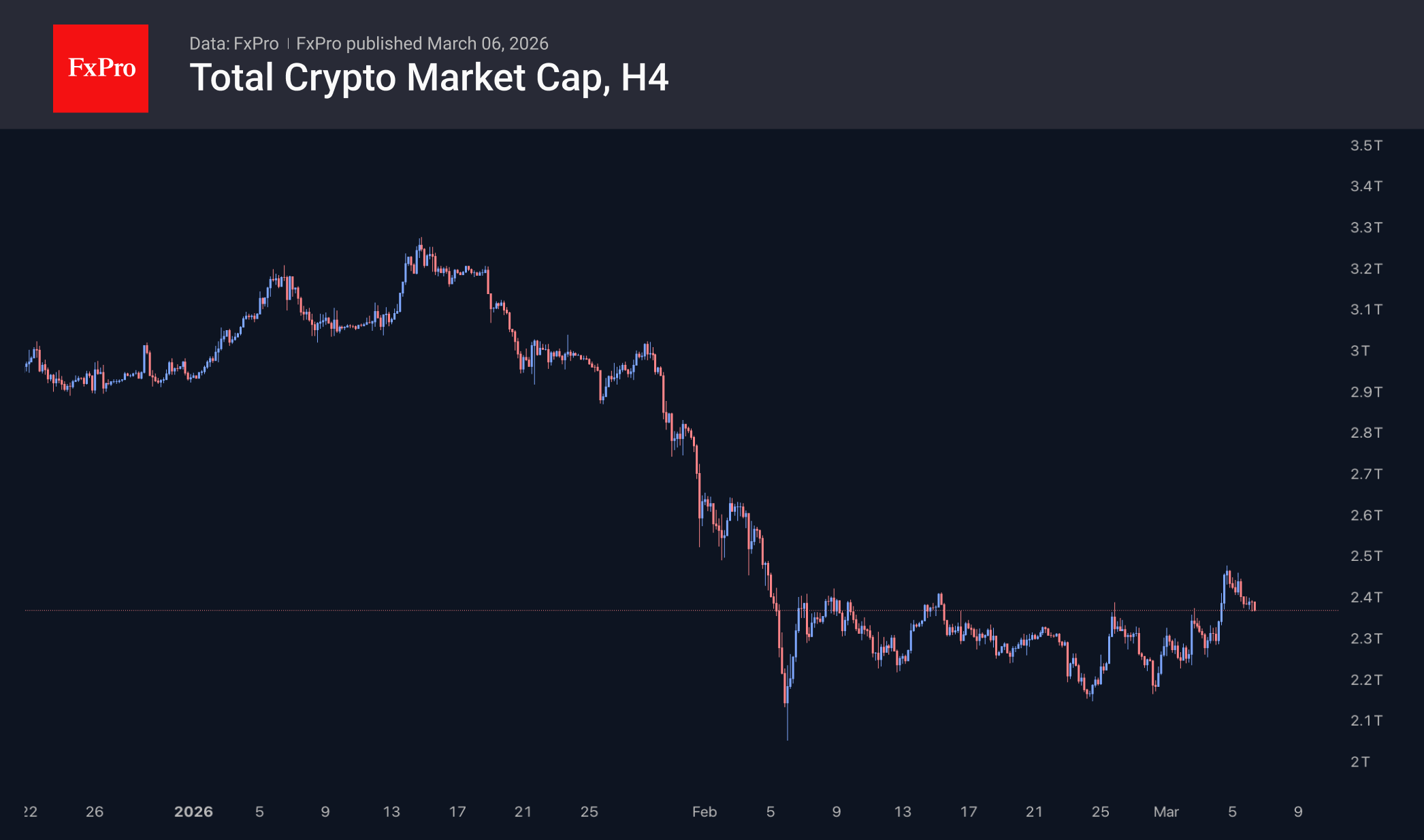

Ethereum Held Above Long-Term Uptrend

Market Overview

The crypto market cap has fallen by approximately 2% over the past 24 hours to $2.41 trillion. The market is cooling after a mid-week surge, consistent with the trend of large capital selling on the growth. The price jump is generating impressive speculative interest, allowing large players to carefully sell larger volumes over a long period without putting excessive pressure on the price.

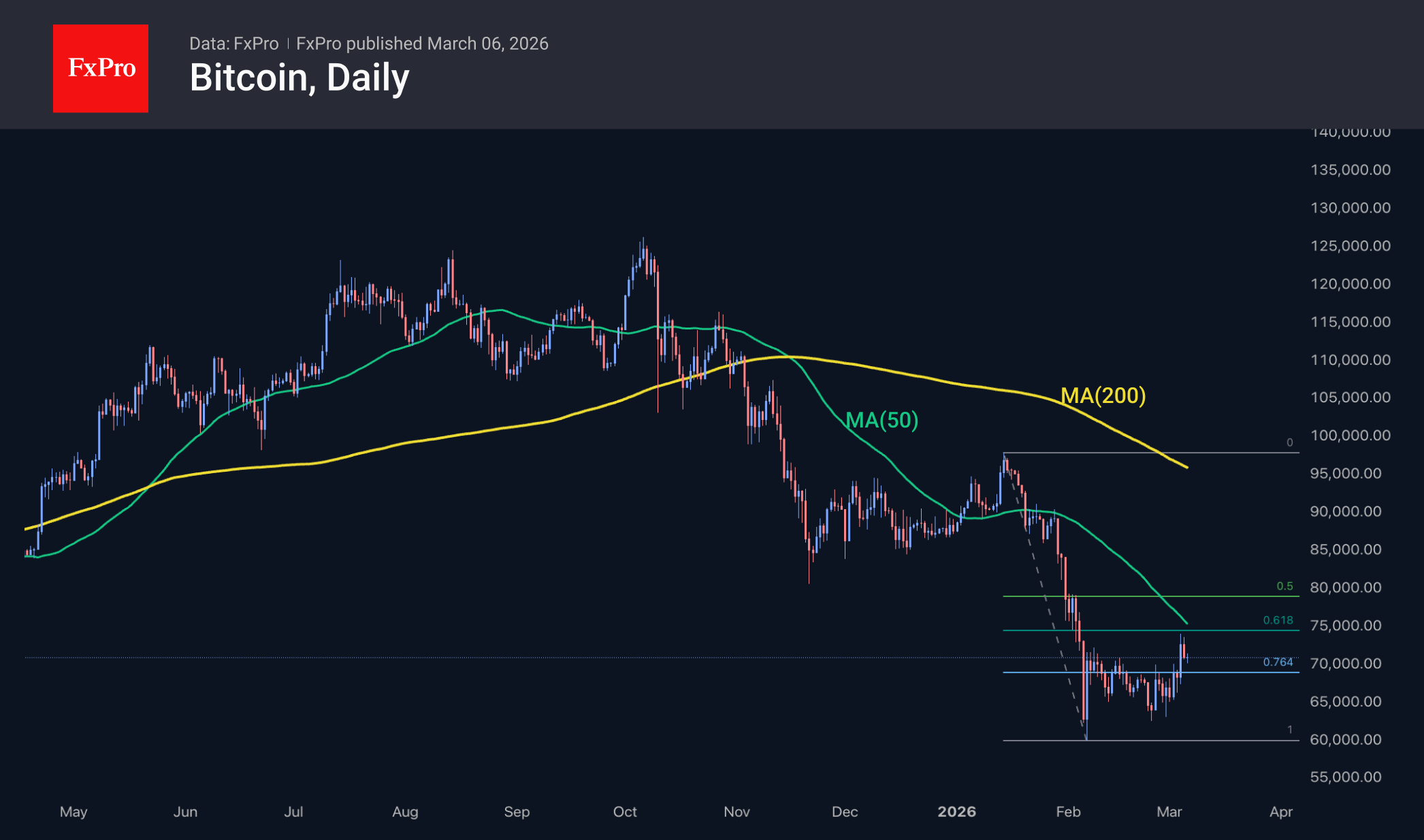

Bitcoin is cautiously retreating for the second day to $70.5K, having encountered resistance and exhausted its growth momentum from the liquidation of short positions a couple of days ago. Short-term obstacles to growth are the 50-day moving average and the 61.8% level of the decline from 14 January to 6 February. Bears are proving that they are in control, keeping Bitcoin within the correction range. In such conditions, there is a higher chance of movement towards the lower end of the range, which can be called typical behaviour for the end of the week in recent months.

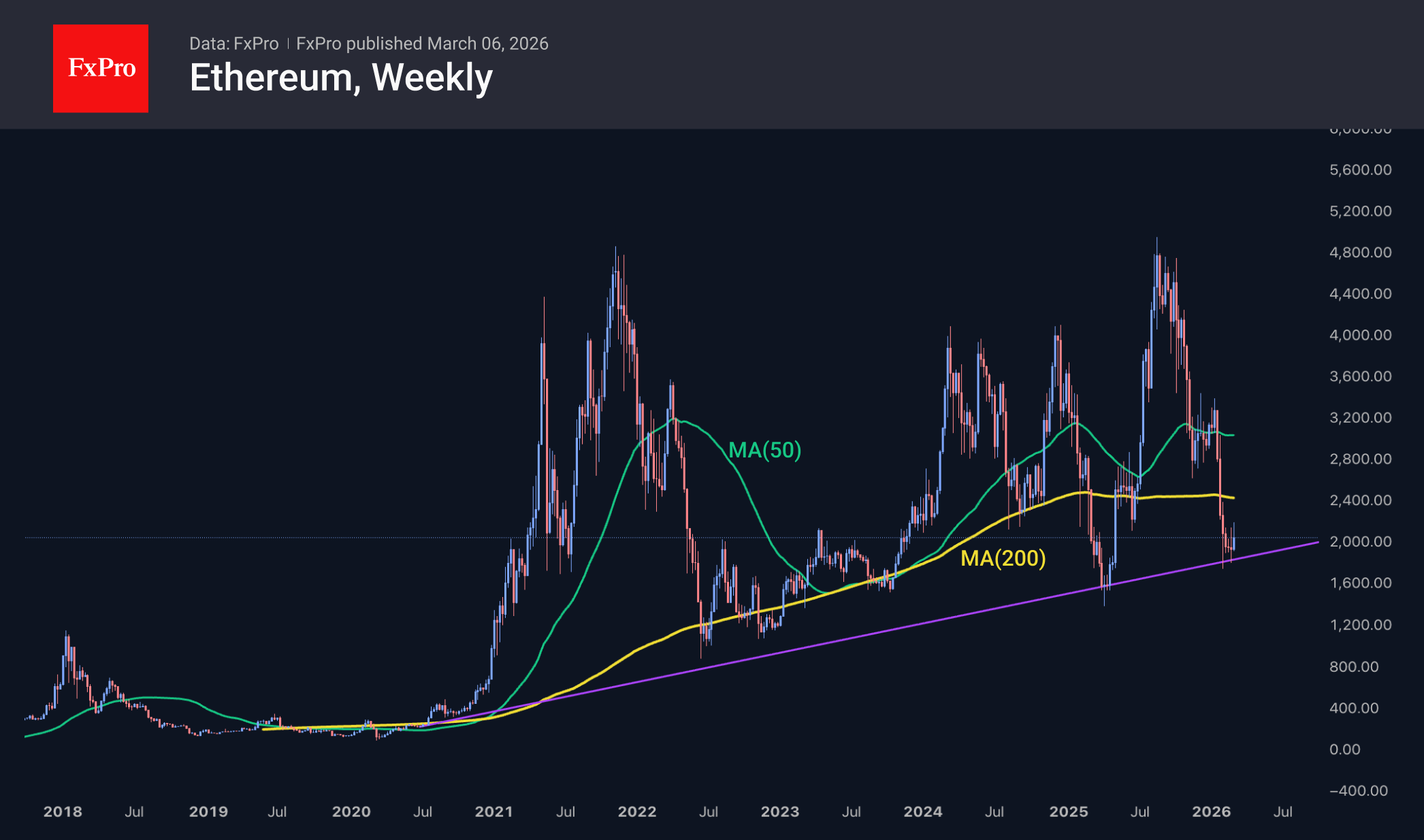

The start of March has been quite successful for Ethereum, with gains after six weeks of decline. Particularly encouraging is the ability of the second-largest cryptocurrency to rebound from the long-term support level of the uptrend and attempt to consolidate above $2,000. Our attention here is focused on the $2,500 area, where the 200-week moving average is located. Consolidation above this level promises to be a prelude to a sustained recovery.

News Background

Messari has recorded the return of retail investors to the market. Net inflows into stablecoins jumped 415% to $1.7 billion over the week. The number of daily transfers increased by almost 10%.

According to Glassnode, 43% of Bitcoin’s market supply is in the red. With the further recovery of BTC, investors may start to get rid of coins, which will limit the possible growth. Additional pressure comes from miners. Mining profitability has fallen to historic lows amid high electricity prices.

Mining companies have been liquidating coins over the past few months, and recent reports from major players suggest the trend may intensify, according to TheEnergyMag.

BitMEX co-founder Arthur Hayes called Bitcoin’s recent rise above $70,000 a ‘dead cat bounce’ that does not signal a shift from a bearish to a bullish trend. In his opinion, the price of the first cryptocurrency may go down again.

EUR/USD Under Pressure: Middle East Risks Outweigh All Else

EUR/USD is holding near 1.1620 on Friday, with the US dollar on track to gain approximately 1% by the end of the week. The dollar is benefiting from safe-haven demand amid the escalating conflict in the Middle East and rising crude oil prices.

The joint US-Israel military operation against Iran continues into its seventh day. Tehran has responded with a fresh wave of missile and drone strikes targeting Gulf countries.

US President Donald Trump also stated that he would like to be involved in selecting Iran's next leader. At the same time, he described the appointment of Mojtaba Khamenei – son of the late Supreme Leader – as unlikely.

Rising oil prices have heightened concerns over a new wave of global inflation, reinforcing expectations that the Federal Reserve may delay interest rate cuts. Markets now anticipate the first Fed rate cut no earlier than September or October, revised down from the previous July forecast.

This week, the dollar strengthened most notably against the euro, reflecting the European economy's heavy reliance on oil imports from the Middle East.

Technical Analysis

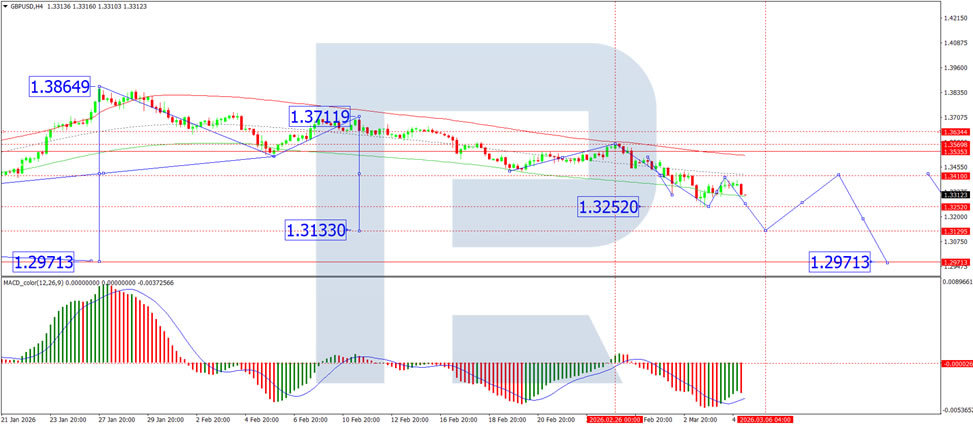

On the H4 chart, EUR/USD is forming a compact consolidation range around the 1.1600 level. The current structure suggests a high probability of a wave developing towards 1.1533, with scope to extend further to 1.1500.

A downside breakout from this range would open the door for the second half of the momentum to unfold, with targets at least around 1.1400. Technically, this scenario is confirmed by the MACD indicator, whose signal line is below zero and pointing strictly downwards, reflecting sustained bearish momentum.

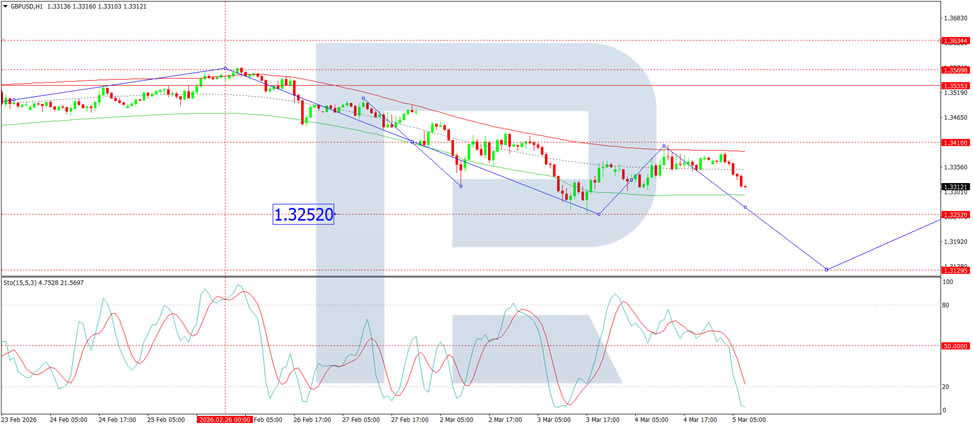

On the H1 chart, the market has completed a growth wave targeting 1.1620, followed by a decline to form a consolidation range around 1.1600. An upside breakout from this range could trigger another growth leg to 1.1660, potentially extending to 1.1675, after which the broader downward trend is likely to resume towards 1.1500.

A downside breakout from the range would activate a continuation wave towards 1.1500, which could mark the completion of the third wave in the broader downward trend. This scenario is confirmed by the Stochastic oscillator, whose signal line has turned away from 80, indicating a short-term downward swing towards the 20 level.

Conclusion

EUR/USD remains under significant pressure as geopolitical tensions in the Middle East drive safe-haven flows into the US dollar, while pushing oil prices higher and stoking inflation concerns. The combination of delayed Fed rate cut expectations and Europe's particular vulnerability to energy disruptions has exacerbated the euro's weakness. With technical indicators pointing firmly lower, further downside appears likely, though short-term consolidation around key levels may precede the next leg of the downtrend.