Sample Category Title

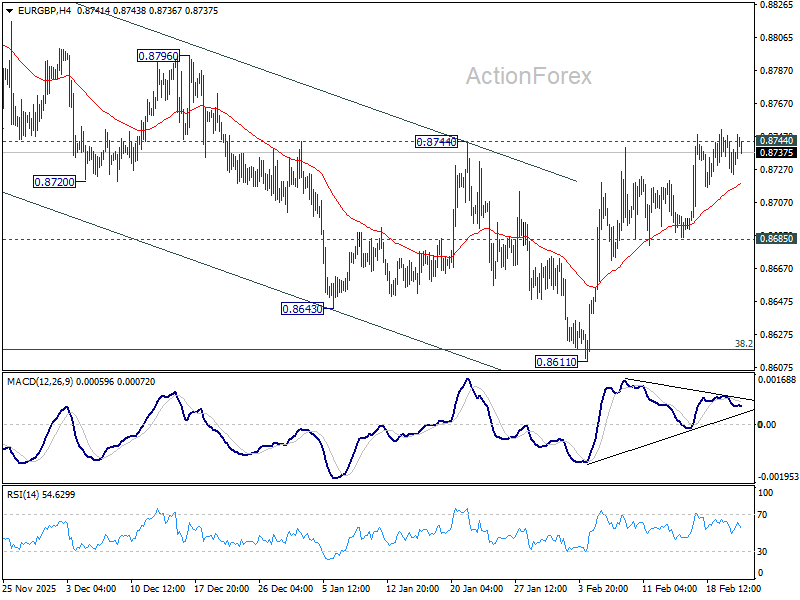

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8727; (P) 0.8738; (R1) 0.8751; More…

Intraday bias in EUR/GBP stays neutral with focus on 0.8744 resistance. Decisive break there should confirm that fall from 0.8863 has completed as a correction at 0.8661. Further rise should then be seen back to retest 0.8663 high. On the downside, break of 0.8685 support will turn bias back to the downside for 0.8611. Sustained break of 38.2% retracement of 0.8221 to 0.8663 at 0.8618 will carry larger bearish implications and turn outlook bearish.

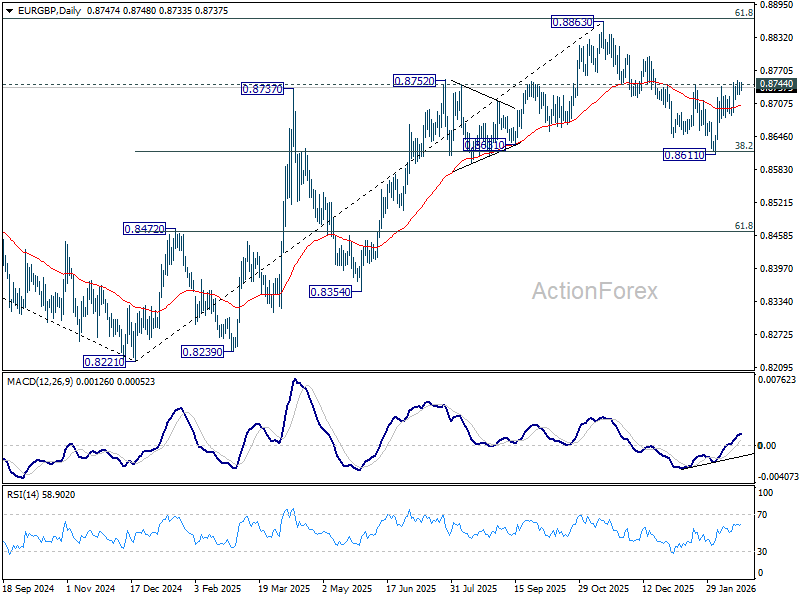

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8636) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

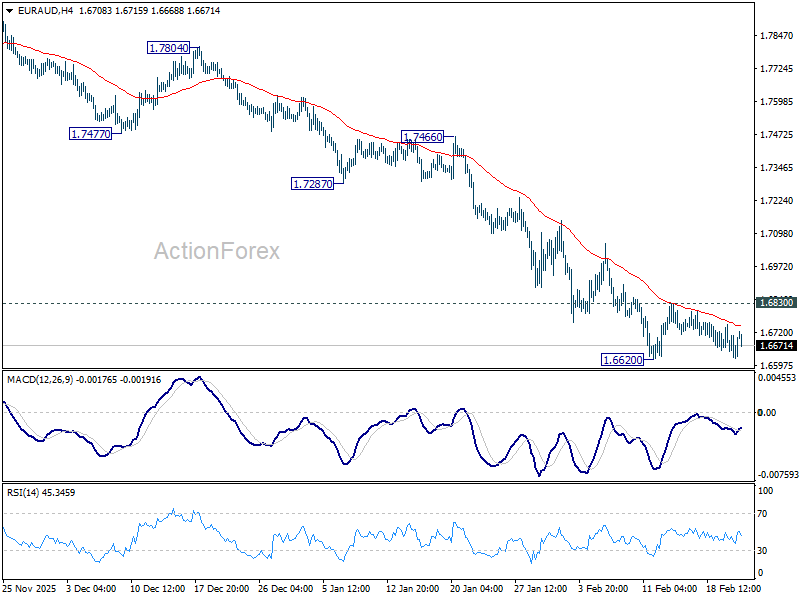

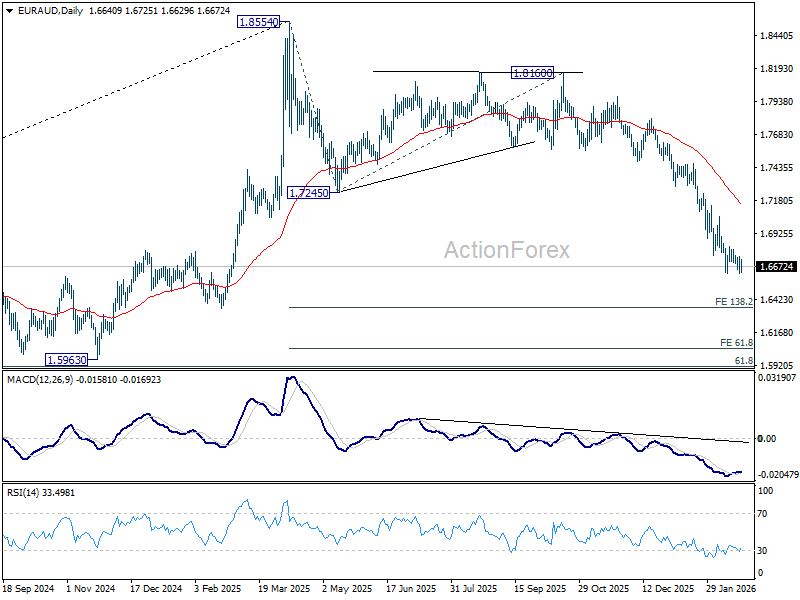

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6588; (P) 1.6672; (R1) 1.6716; More...

Range trading continues in EUR/AUD above 1.6620 and intraday bias remains neutral. Further decline is expected with 1.6830 resistance intact. On the downside, decisive break of 1.6620 will resume the larger decline from 1.8554 to 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351 next. However, firm break of 1.6830 resistance will indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

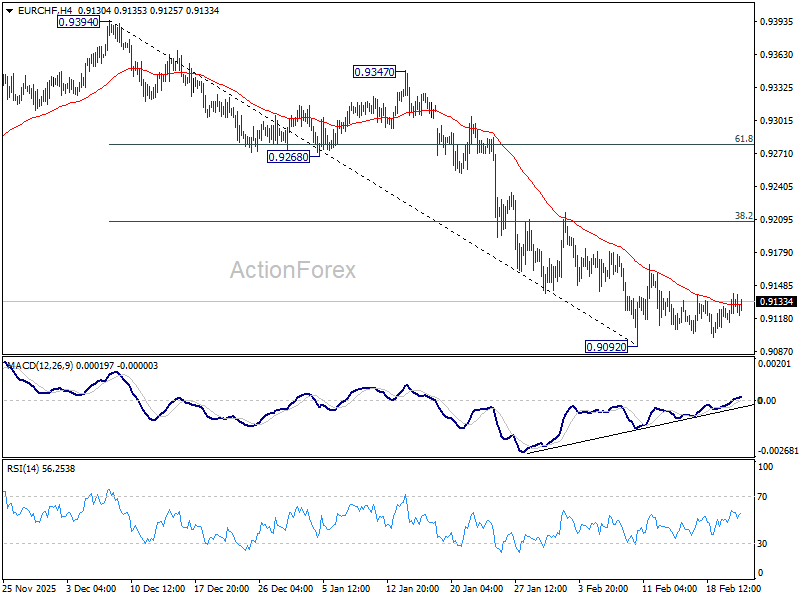

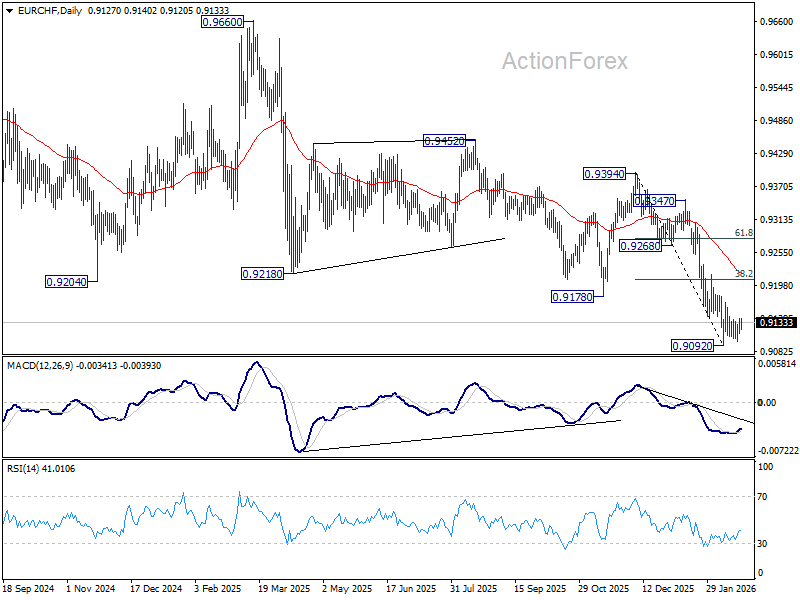

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9124; (P) 0.9133; (R1) 0.9151; More....

Intraday bias in EUR/CHF remains neutral and consolidations continues above 0.9092. Stronger rebound might be seen but upside should be limited by 38.2% retracement of 0.9394 to 0.9092 at 0.9207. On the downside, firm break of 0.9092 will resume larger down trend.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9326) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

Sell “America” Reemerges After Trump’s Tariff Defiance – USD/JPY, Gold, Hang Seng Index Intraday Outlook

Key takeaways

- Tariff escalation despite court setback: President Trump rejected the Supreme Court’s ruling against his 10% baseline tariffs and moved to lift them to 15% under Section 122 of the 1974 Trade Act, raising fresh policy uncertainty and reviving the “Sell America” narrative.

- Risk-off market reaction: The US dollar weakened, S&P 500 and Nasdaq futures fell, while gold rallied as investors sought safe havens amid renewed trade tensions and legal uncertainty over tariff policy.

- Diverging technical setups: USD/JPY remains bearish below 154.65/154.95, gold is testing key $5,170 resistance with breakout risk, and the Hang Seng Index shows short-term bullish momentum above 26,615 support.

US President Trump has refused to back down on his global tariffs policy after the US Supreme Court ruled against his use of his reciprocal tariffs enacted last year under the International Emergency Economic Powers Act (IEEPA), in turn, deemed the global baseline tariff rate of 10% as illegal.

Trump called the Supreme Court verdict “unpatriotic” and vowed to press on the current White House’s aggressive trade policy stance to circumvent the Supreme Court’s ruling by imposing an increase in the global reciprocal tariff to 15% from 10% with immediate effect via a social media post on Saturday, 21 February.

Trump is applying the new baseline tariff under Section 122 of the 1974 Trade Act, which allows the president to impose tariffs for 150 days without congressional approval. Beyond the 150 days, securing congressional approval is likely to prove challenging for the White House because Democrats and several Republicans have opposed elements of Trump’s trade policy.

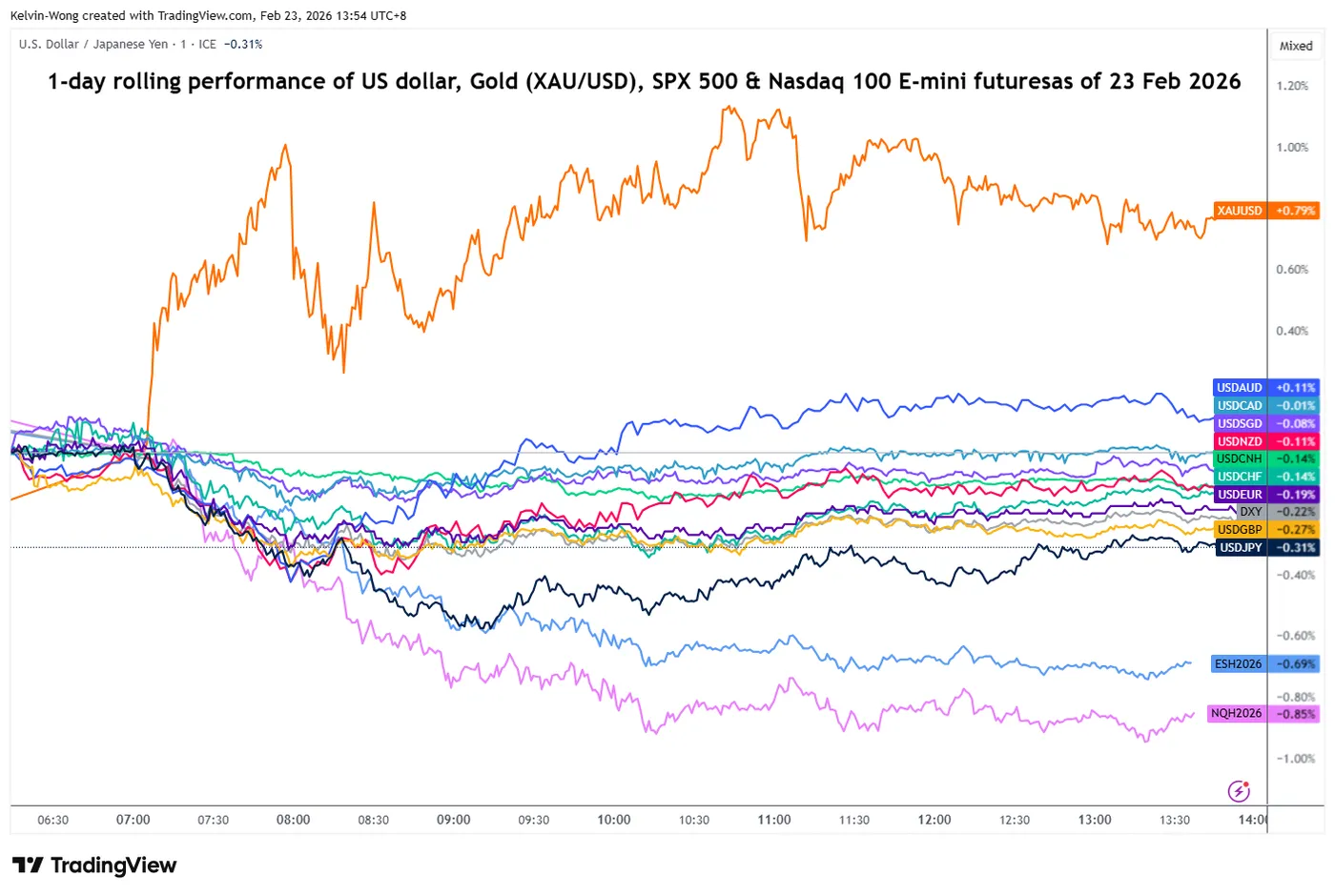

The latest cloud of uncertainty over the US tariff policy has triggered another bout of the “Sell America” narrative, where the US dollar weakened further in today’s Asia session (US Dollar Index shed -0.2%), S&P 500, and Nasdaq 100 e-mini futures dropped by 0.7% and 0.9% respectively. Gold (XAU/USD) jumped by 0.8% (see Fig. 1) at the time of writing.

Fig. 1: 1-day rolling performances of the US dollar, Gold (XAU/USD), SPX 500 & Nasdaq 100 E-mini futures as of 23 Feb 2026 (Source: TradingView)

Let’s dissect the short-term trajectory of USD/JPY, Gold (XAU/USD), and Hang Seng Index.

USD/JPY – Reintegrate below 20-day and 50-day moving averages

Fig. 2: USD/JPY minor trend as of 23 Feb 2026 (Source: TradingView)

Bearish bias below 154.65/154.95 short-term pivotal resistance, and a break below 153.83 key near-term support opens scope for further potential weakness to expose the next intermediate support of 152.65/152.20 (see Fig. 2).

However, a clearance and an hourly close above 154.95 invalidates the bearish tone for a squeeze up towards the next intermediate resistances at 155.66 and 156.36.

Gold (XAU/USD) – Squeezed up to probe $5,170 key short-term resistance

Fig. 3: Gold (XAU/USD) minor trend as of 23 Feb 2026 (Source: TradingView)

Gold (XAU/USD) ended last Friday, 20 February, US session with a daily return of 2.2% and extends its gains further in today’s Asia session with an intraday rally of almost 1% to test a key short-term resistance at $5,160 (also the 61.8% Fibonacci retracement of the prior minor down move from 29 January 2026 all-time high to 2 February 2026 low) (see Fig. 3).

The hourly RSI momentum indicator has started to inch downwards from its overbought reading of 82. Mixed elements, neutral between $5,170 and $4,960 (also close to the 20-day moving average).

Only a clearance and hourly close above $5,170 ignites a potential bullish move towards $5,448 and $5,606 (current all-time high).

On the flipside, failure to hold at $4,960 sees another round of choppy sideways downward drift towards the range supports of $4,842 and $4,703 (also the 50-day moving average).

Hang Seng Index – Short-term minor bullish momentum breakout

Fig. 4: Hong Kong 33 CFD index minor trend as of 23 Feb 2026 (Source: TradingView)

The price actions of the Hong Kong 33 CFD index (a proxy of the Hang Seng Index futures) have cleared above its 20-day moving average, which has acted as a near-term resistance since 12 February 2026 (see Fig. 4).

In addition, its hourly RSI momentum indicator has staged a bullish breakout above its former descending resistance at around the 50 level, which suggests a potential revival of short-term bullish momentum.

Bullish bias above 26,615 key short-term pivotal support for a potential push up to test 27,228 intermediate resistance follow by the 27,500 major resistance.

On the other hand, a break and an hourly close below 26,615 negates the bullish tone for a potential drift down to retest the minor range support of 26,285 (in place since 20 January 2026).

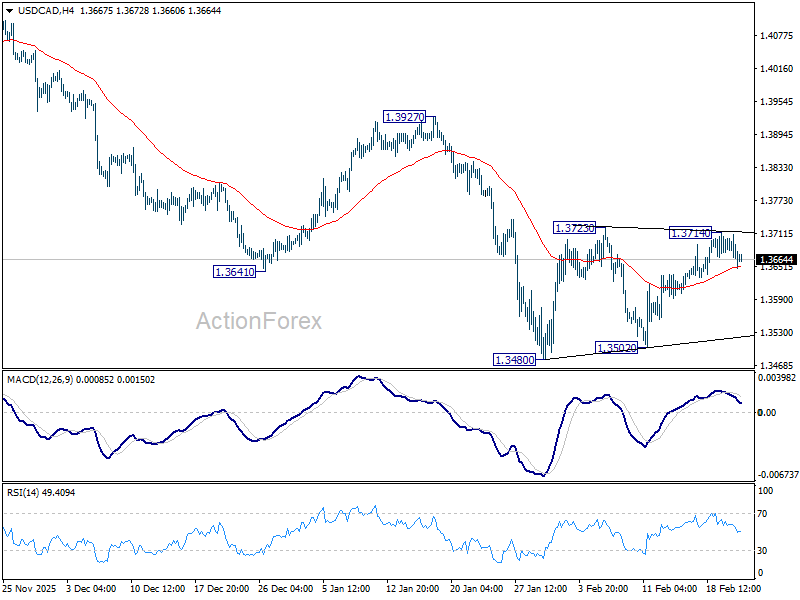

USD/CAD Analysis Following Changes in US Tariff Policy

Currency markets opened on Monday with the US dollar under pressure, as traders assessed weekend developments related to US tariff policy. According to Reuters:

- → On Friday, the Supreme Court ruled that President Trump’s sweeping tariffs exceeded his authority.

- → In response, the US president criticised the court and introduced a blanket 15% import levy. Trump also insisted that higher-tariff agreements with trade partners should remain in force.

Against this backdrop, USD/CAD slipped below the 1.3660 level today. This comes despite the upward move observed since 11 February (marked by purple lines), which developed after Canadian inflation slowed from 2.7% to 2.4%. The weaker inflation data weighed on the Canadian dollar, as markets began pricing in the possibility of future interest rate cuts by the Bank of Canada.

Technical Analysis of the USD/CAD Chart

When analysing USD/CAD on 29 January (with the market trading near the psychological 1.3500 level), we:

- → highlighted the presence of a long-term descending channel;

- → noted that price was close to its lower boundary, which could act as support;

- → considered a rebound scenario.

Since then, USD/CAD has formed two bullish reversals near the 1.3500 area. However, on both occasions bullish momentum appeared to fade around 1.3700.

The current price action resembles a rounding top pattern, suggesting that sellers may soon attempt to regain control and push towards the lower purple boundary in an effort to resume the broader long-term downtrend.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3663; (P) 1.3687; (R1) 1.3705; More...

Intraday bias in USD/CAD stays neutral at this point. Consolidations from 1.3480 and stronger rebound might be seen. But upside should be limited by 55 D EMA (now at 1.3738) to complete the pattern. On the downside, below 1..3502 will bring retest of 1.3480 low. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

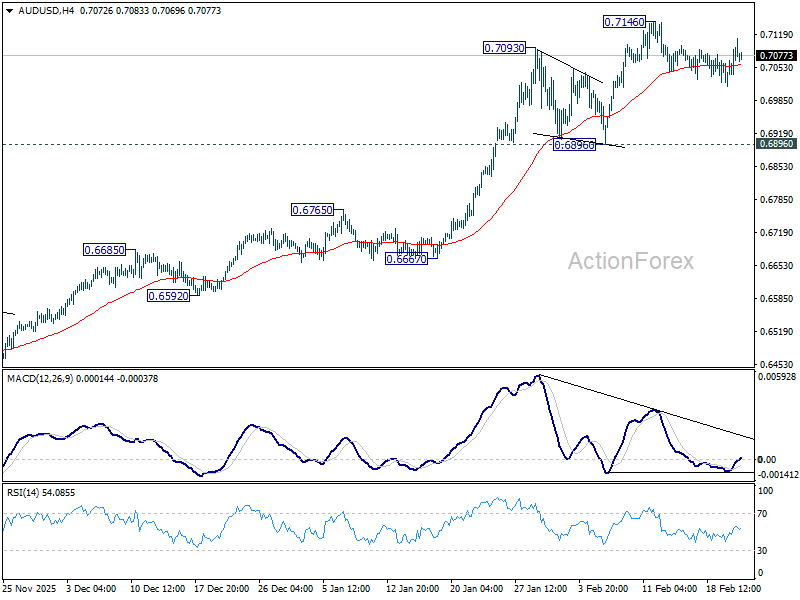

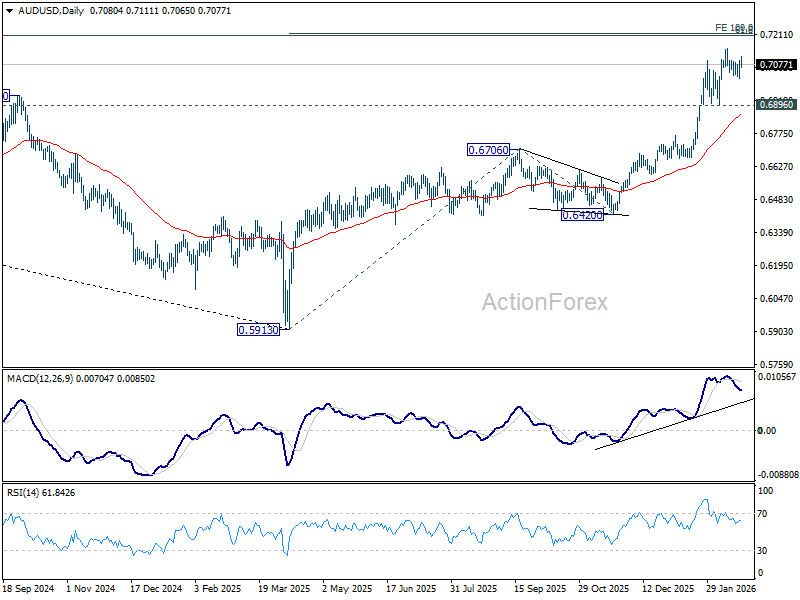

AUD/USD Daily Report

Daily Pivots: (S1) 0.7035; (P) 0.7065; (R1) 0.7114; More...

Intraday bias in AUD/USD remains neutral and more consolidations could be seen below 0.7146. Deeper retreat cannot be ruled out, but downside should be contained above 0.6896 support. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

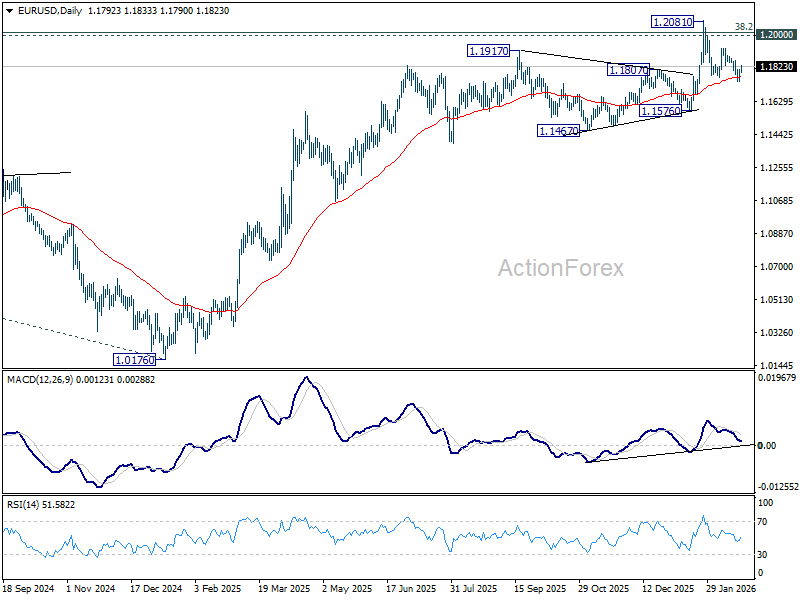

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1747; (P) 1.1778; (R1) 1.1811; More….

Intraday bias in EUR/USD stays neutral at this point. Risk will remain on the downside as long as 1.1928 resistance holds. Below 1.1740 will target 1.1576 support next. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

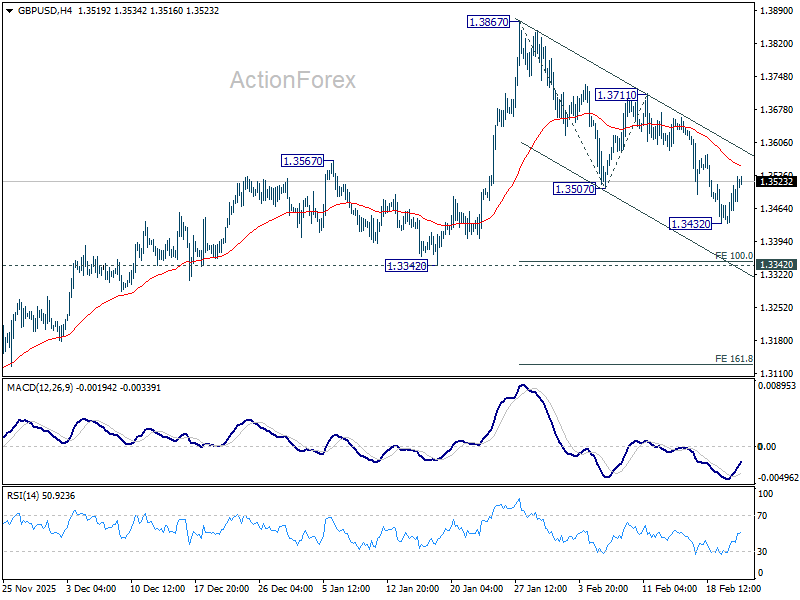

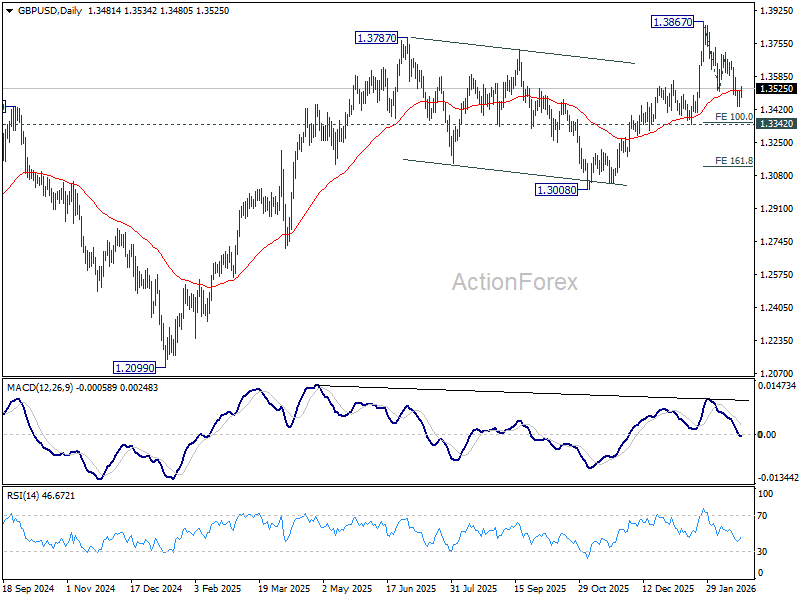

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3438; (P) 1.3476; (R1) 1.3518; More...

Intraday bias in GBP/USD remains neutral for the moment. For now, fall from 1.3867 is seen as correcting the whole rise from 1.2099. Risk will stay on the downside as long as 1.3711 resistance holds. Below 1.3432 will target 1.3342 support first. Firm break there will solidify this case, and target 161.8% projection of 1.3867 to 1.3507 from 1.3711 at 1.3129.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

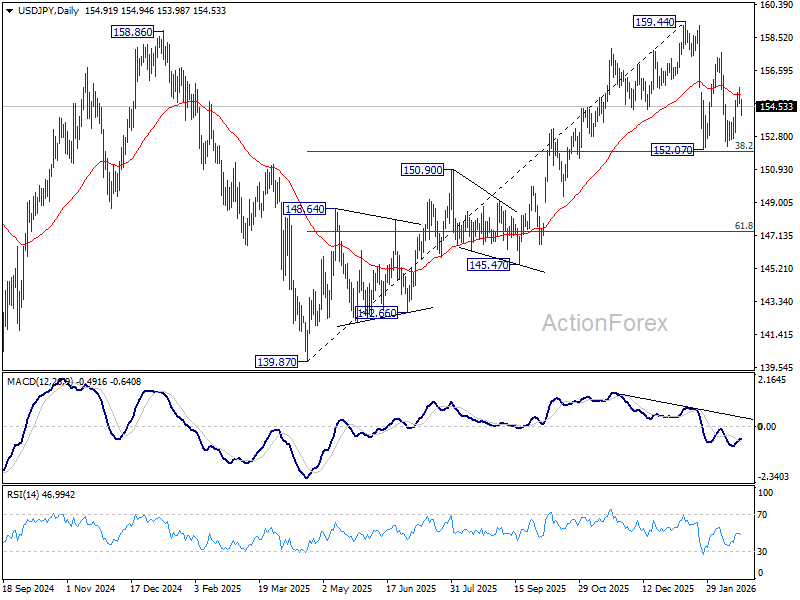

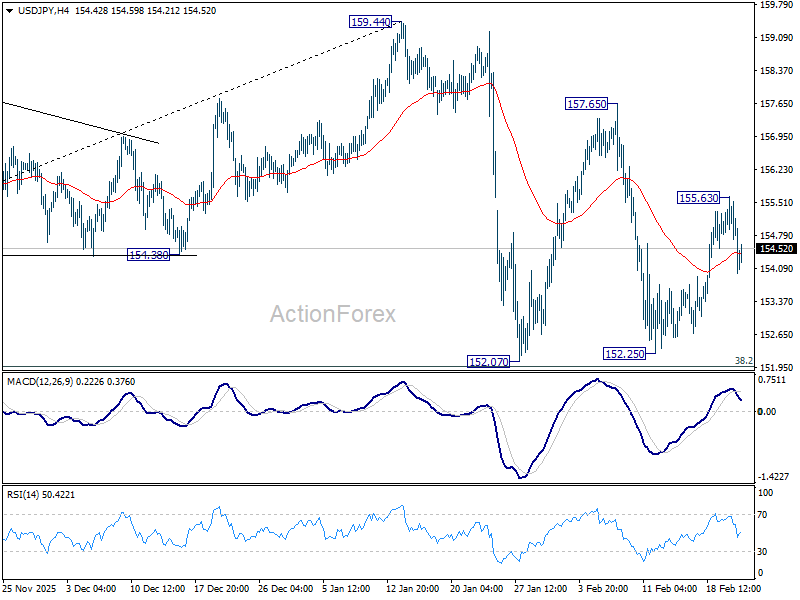

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.65; (P) 155.14; (R1) 155.57; More...

Intraday bias stays neutral at this point. On the upside, above 155.63 will resume the rally from 152.25 and target 157.65 first. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also rise from 139.87 is expected to resume through 159.44 at a later stage.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.