Sample Category Title

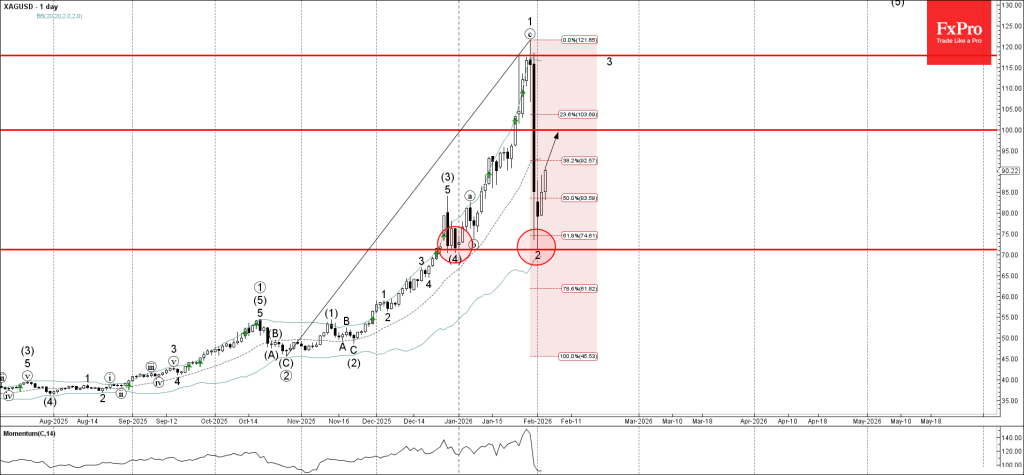

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver rising inside impulse wave 3

- Likely to test resistance level 100.00

Silver recently reversed up from the support zone between the support level 71.25 (which stopped wave (4) at the end of December), lower daily Bollinger Band and the 61.8% Fibonacci correction of the previous upward impulse from October.

The upward reversal from this support area created the daily Japanese candlesticks reversal patterns long-legged Doji, which stopped the previous sharp downward correction 2.

Given the overriding daily uptrend, Silver can be expected to rise toward the next round resistance level 100.00.

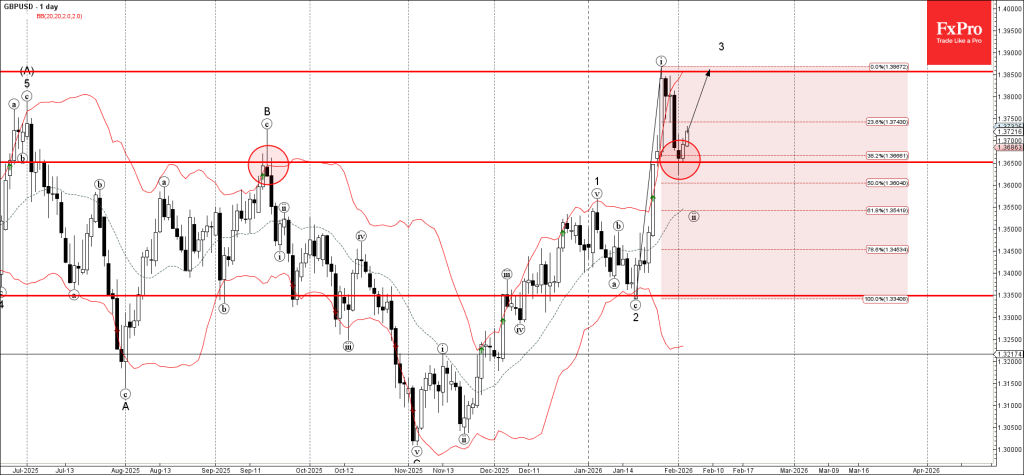

GBPUSD Wave Analysis

GBPUSD: ⬆️ Buy

- GBPUSD reversed from support area

- Likely to rise to resistance level 1.3850

GBPUSD currency pair recently reversed up from the support area located between the key support level 1.3650 (former resistance from September) and the 38.2% Fibonacci correction of the previous sharp upward impulse from January.

The upward reversal from this support area created the daily Japanese candlesticks reversal patterns Bullish Engulfing.

Given the bearish US dollar sentiment seen today, GBPUSD currency pair can be expected to rise toward the next resistance level 1.3850.

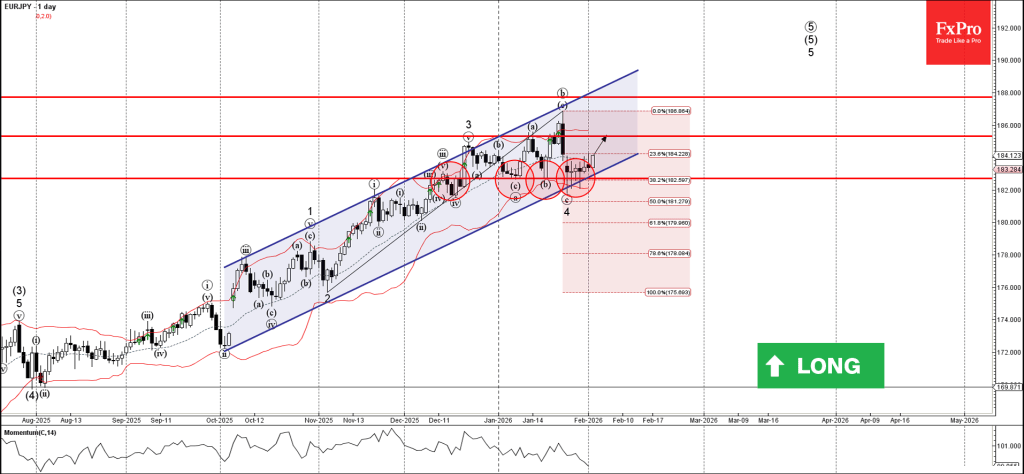

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY reversed from support area

- Likely to rise to resistance level 185.30

EURJPY currency pair recently reversed up from the support area located between the pivotal support level 182.70 (which has been reversing the pair from the start of this year) and the support trendline of the wide daily up channel from October.

The pair made multiple Japanese candlesticks reversal patterns Doji near the support level 182.70 – signalling the strength of this support level.

Given the strong daily uptrend, EURJPY currency pair can be expected to rise in the active impulse wave 5 toward the next resistance level 185.30.

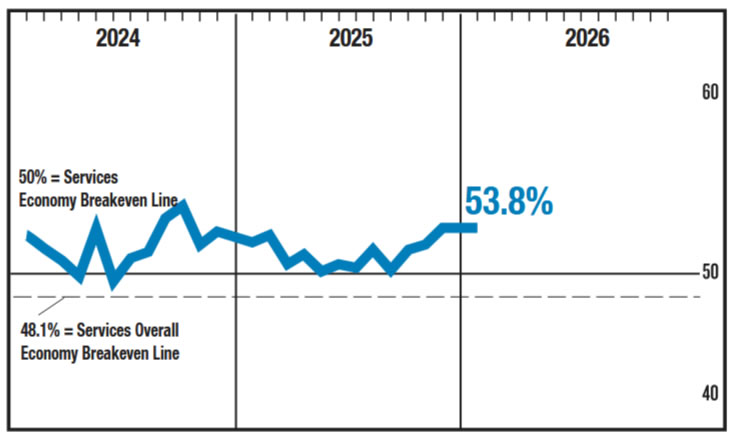

ISM Services Steady in January Despite Large Drop in Export Orders

The ISM Services index held steady in January at 53.8. This is the fourth consecutive month of expansion. Eleven industries out of 18 reported expansion, the same as last month.

The supplies delivery index moved deeper into in expansionary territory in January, marking the 14th consecutive month it has been in expansion. It increased 2.4 points to 54.2, indicating slower deliveries, which is expected when customer demand is increasing.

New Orders gave back some of its gains after a large increase last month, falling 3.4 points but remaining in expansionary territory at 53.1. The business activity posted its highest reading since October 2024, a sign of higher activity.

New export orders showed a large decline, falling to 45.0 from 54.2 in the month prior.

The prices index increased by 1.5 points to 65.1, indicating that price pressures are still prevalent. The employment index managed to remain in expansionary territory, falling to 50.3 from 51.7.

Key Implications

This report affirms that demand in the service sector remains reasonably strong, as we can see in the relatively strong performance of the new orders and business activity sub-indexes. The combination of expanding activity and slower supplier deliveries does raise the specter of price increases. We will get a more direct read on this in next week's CPI release, but the trend of steady employment growth, increasing demand, and increasing price pressures amplify the risk that rates take longer to come down again.

The biggest change in the details of this report is the outsized drop in the new export orders index, which plummeted 9.2 points into contractionary territory and to its lowest reading since March 2023. Respondents indicated that both tariffs and travel restrictions are significantly impacting export orders. Despite the large decrease in the index, only seven industries reported a decrease, meaning that this may not be the bottom for export orders if trade uncertainty continues. There is still the risk that this could spread to the other 11 industries, with the potential to further drag down service activity as a whole.

US ISM services unchanged at 53.8, points to 1.8% annualized GDP growth

US ISM Services PMI was unchanged at 53.8 in January, matching expectations and marking a second consecutive month at the highest level since October 2024. The steady headline reading points to continued resilience in the services sector, which remains a key pillar of overall economic momentum.

Beneath the surface, the details were mixed. Business activity strengthened notably, with the production index rising from 55.2 to 57.4. However, new orders eased back to 53.1 from 56.5. Employment index slipped closer to stagnation at 50.3, down from 51.7. Inflation signals firmed. The prices index climbed sharply from 65.1 to 66.6, highlighting renewed cost pressures in the services sector. Even so, all four major subcomponents remained in expansion territory for a second month.

Based on the historical relationship tracked by the Institute for Supply Management, the January PMI reading is consistent with roughly 1.8 percentage points of annualized real GDP growth.

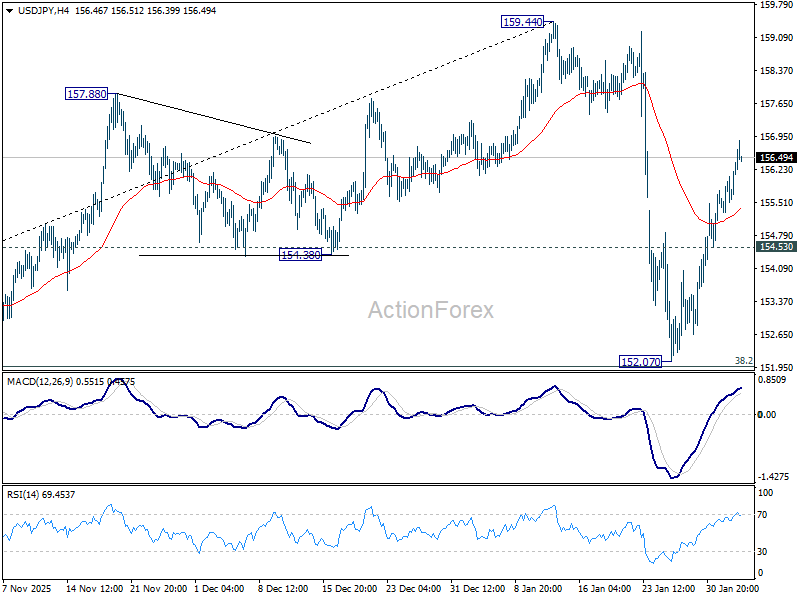

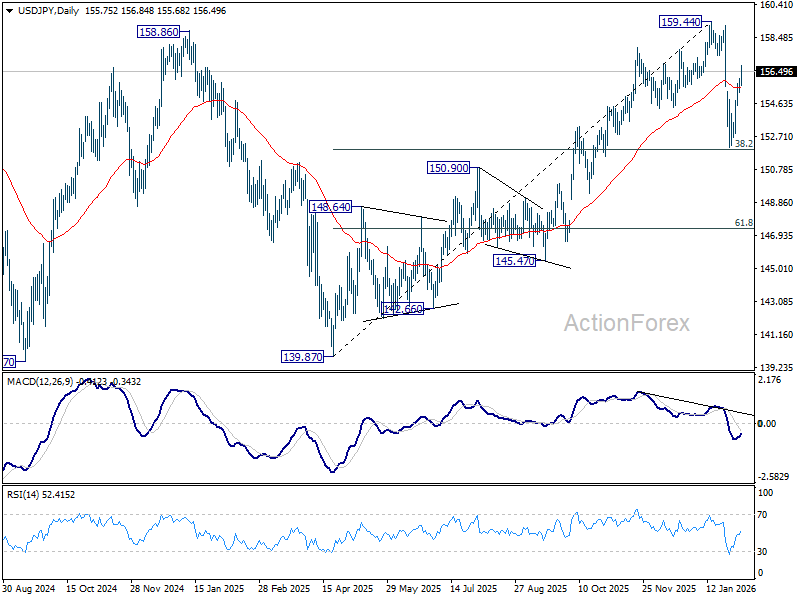

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.35; (P) 155.72; (R1) 156.13; More...

No change in USD/JPY's outlook and intraday bias stays on the upside. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Further rebound should be seen to retest 159.44 next. On the downside, below 154.53 minor support will turn intraday bias neutral first. Sustained break of 38.2% retracement of 139.87 to 159.44 at 151.96 will argue that it is reversing whole rise from 139.87.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.59) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

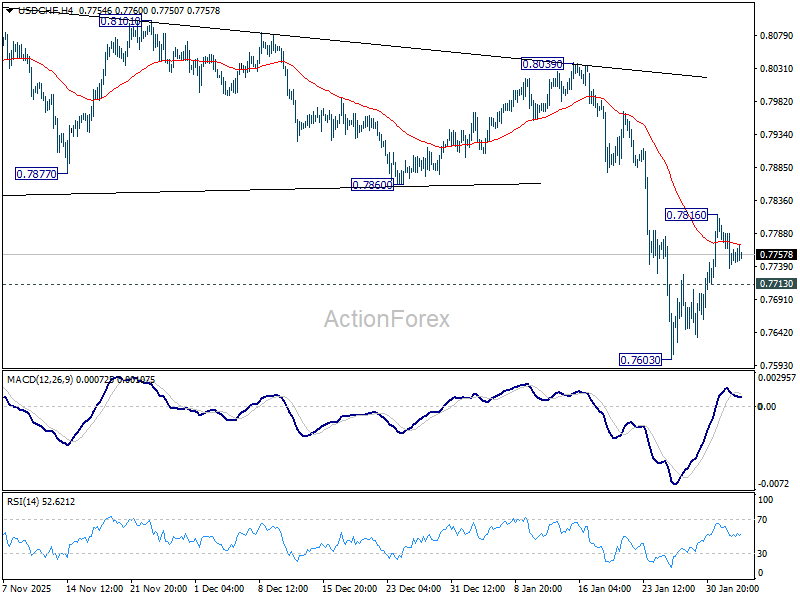

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7726; (P) 0.7765; (R1) 0.7791; More….

Intraday bias in USD/CHF stays neutral at this point. Above 0.7816 will resume the rebound from 0.7603 short term bottom to 55 D EMA (now at 0.7905). On the downside, below 0.7713 minor support will bring retest of 0.7603. Firm break there will resume larger down trend to 0.7382 projection level next.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8166) holds.

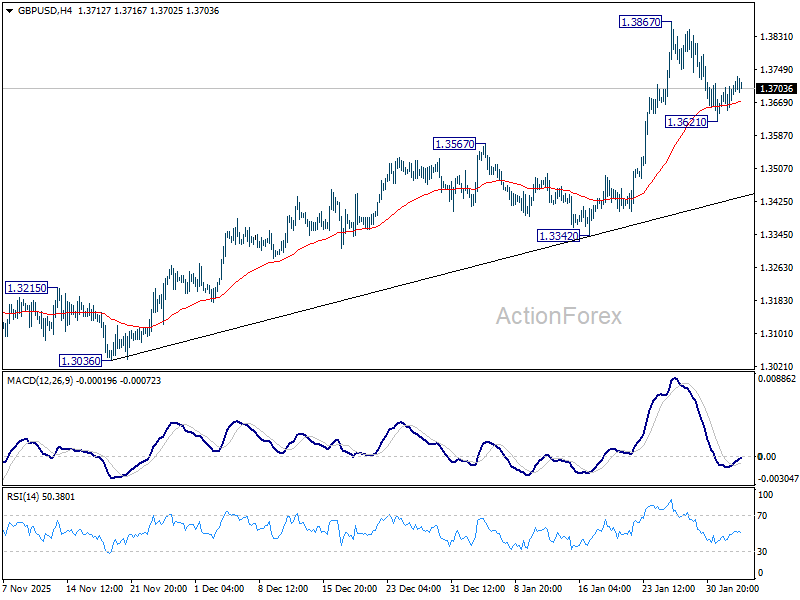

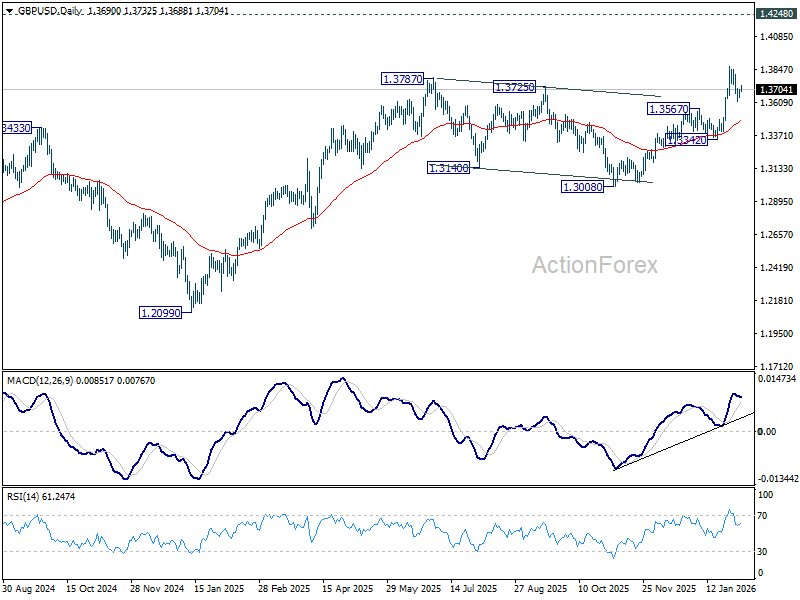

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3664; (P) 1.3686; (R1) 1.3720; More...

Intraday bias in GBP/USD remains neutral for the moment. Below 1.3621 will extend the pullback from 1.3867 short term top to 55 D EMA (now at 1.3471). On the upside, firm break of 1.3867 will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

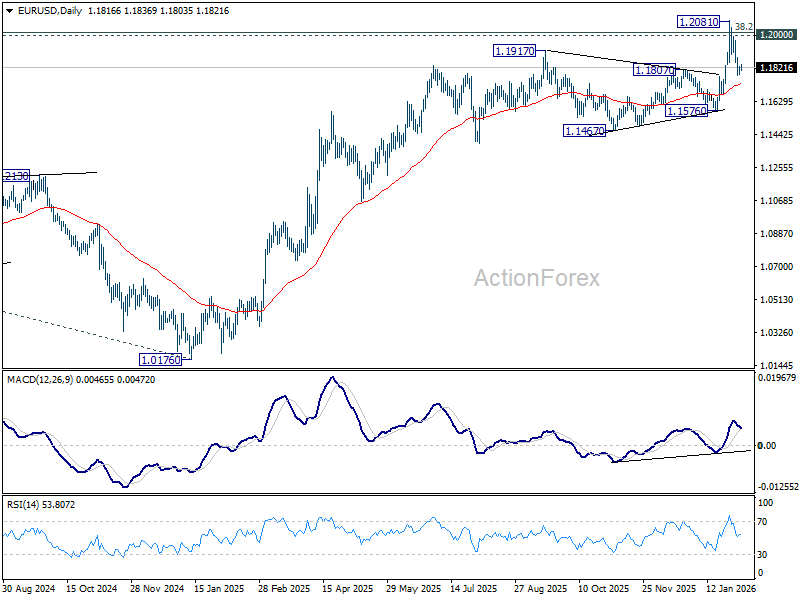

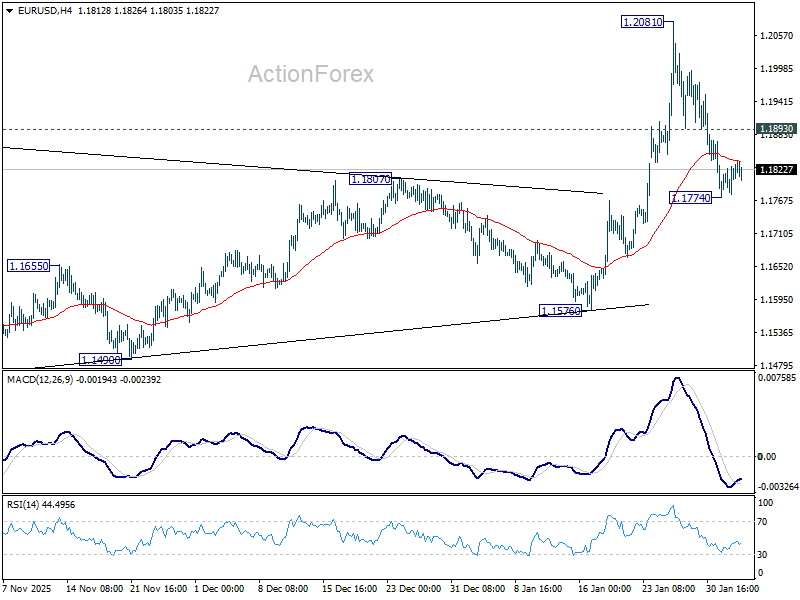

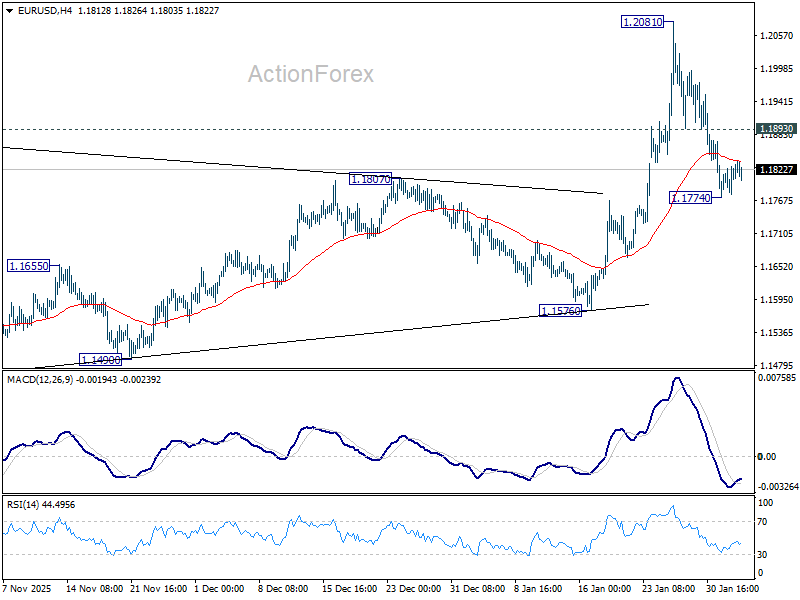

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1790; (P) 1.1809; (R1) 1.1839; More….

Intraday bias in EUR/USD remains neutral as it's bounded in right range above 1.1774. On the downside, below 1.1774 will extend the fall from 1.2081 short term top to 55 D EMA (now at 1.1724). Firm break there will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support. On the upside, above 1.1893 minor resistance will bring stronger rebound to retest 1.2081. Decisive break above 1.2 will carry larger bullish implications.

In the bigger picture, as long as 55 W EMA (now at 1.1458) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Euro Shrugs Off Soft Inflation, Dollar Steady after ADP Miss

Euro is trading steadily today despite inflation data coming in weaker than expected. The muted market reaction suggests investors are comfortable looking through near-term softness, focusing instead on the broader policy and inflation backdrop. Indeed, recent data point to inflation likely undershooting the ECB’s own forecasts in the near term. That said, medium-term inflation expectations remain well anchored, limiting pressure on policymakers to respond preemptively.

For now, the ECB can afford patience. With inflation expectations stable, a single downside surprise is unlikely to shift the policy stance, particularly given the Bank’s emphasis on medium-term dynamics rather than month-to-month volatility. Still, the price outlook is not without risk. Sustained renewal of Euro’s uptrend—especially if EUR/USD were to break and hold above the 1.20 level—could prompt reassessment, as currency strength would add a disinflationary impulse through import prices.

At the same time, services inflation remains sticky, as highlighted in today's PMI reports. Rising energy prices, coupled with a marked pickup in service-sector input costs and selling prices, could quickly reawaken inflation concerns if they persist.

Taken together, these cross-currents keep the bar for an ECB rate move high. Any rate move would require clearer evidence that inflation risks are either becoming entrenched or decisively fading, neither of which is yet the case. Looking further ahead, medium-term risks tilt mildly to the upside. Fiscal expansion in Germany later this year could provide additional demand support.

In the US, Dollar is also holding within tight ranges. The latest ADP report reinforced the “low hiring, low firing” narrative that has dominated recent labor market data. While hiring momentum is cooling, the adjustment is not yet feeding through to wage dynamics. Pay growth remains elevated, strengthening the argument for more hawkish members of the FOMC to remain patient for now.

Uncertainty lingers over the timing of the more comprehensive non-farm payrolls report, delayed by the brief government shutdown. With a funding deal already in place, markets hope the data will be released soon to provide clearer direction.

For the week so far, Aussie leads FX performance, followed by Sterling and Kiwi. Yen sits firmly at the bottom, trailed by Swiss Franc and Euro. Dollar and Loonie remain in the middle.

In Europe, at the time of writing, FTSE is up 1.22%. DAX is down -0.33%. CAC is up 0.87%. UK 10-year yield is down -0.001 at 4.526. Germany 10-year yield is down -0.019 at 2.875. Earlier in Asia, Nikkei fell -0.78%. Hong Kong HSI rose 0.05%. China Shanghai SSE rose 0.85%. Singapore Strait Times rose 0.43%. Japan 10-year JGB yield fell -0.009 to 2.251.

US ADP jobs grow only 22k, but wage pressures steady

US private employment rose by just 22k in January, according to the ADP report, well below expectations of 48k increase.

Job gains were concentrated in service-providing industries, which added 21k positions, while goods-producing sectors contributed just 1k. By firm size, medium-sized businesses drove employment growth with 41k new jobs, while large employers shed -18k positions and small establishments saw no net change, pointing to uneven demand for labor.

Wage growth, however, remained resilient. Pay for job-stayers rose 4.5% yoy, little changed from prior months. Job-changer wage growth slowed modestly from 6.6% yoy to 6.4%.

As Nela Richardson, chief economist at ADP, noted, job creation has slowed sharply over the past three years, but wage growth has remained stable—highlighting a labor market that is cooling through hiring rather than pay compression.

Eurozone CPI cools to 1.7% in January, core ticks down to 2.2%

Eurozone flash CPI slowed from 1.9% yoy to 1.7% in January, in line with expectations. Underlying pressures also moderated slightly. Core CPI, which strips out energy, food, alcohol, and tobacco, edged down from 2.3% to 2.2% yoy.

By component, services inflation remained the largest contributor but slowed to 3.2% from 3.4%. Food, alcohol, and tobacco inflation picked up from 2.5% to 2.7%. Non-energy industrial goods inched higher from 0.3% to 0.4%. Energy prices was a major drag, with annual inflation falling sharply from -1.9% to -4.1%.

Eurozone PMI services finalized at 51.6, cost pressures stay on ECB radar

Eurozone PMI Services was finalized at 51.6 in January, easing from December’s 52.4. PMI Composite edged lower to 51.3 from 51.5. The data still point to ongoing expansion, but momentum softened slightly at the start of the year.

At the country level, the picture was mixed but broadly supportive. Spain was the strongest performer with PMI Composite at 52.9, despite slipping to a seven-month low. Germany (52.1) and Italy (51.4) both posted modest improvements. France (49.1) stood out as the laggard, with activity remaining in contraction territory.

According to Cyrus de la Rubia of Hamburg Commercial Bank, service sector growth has been “decent” but far from comfortable, with weak new business growth and limited hiring highlighting the recovery’s vulnerability.

While headline inflation is close to the ECB’s 2% target, services inflation remains sticky. Rising energy prices linked to cold weather, alongside a marked pickup in service sector input costs and selling prices flagged by the PMI, could reawaken concerns.

UK PMI services finalized at 54.0, encouraging start to the year

UK PMI Services was finalized at 54.0 in January, surging from December’s 51.4 and marking the strongest reading since August 2025. PMI Composite also rose sharply to 53.7 from 51.4, the highest level since August 2024,.

According to Tim Moore of S&P Global Market Intelligence, the survey points to an “encouraging start” to the year after a sluggish end to 2025. Service sector output expanded at the fastest pace in five months, supported by improved investment sentiment and stronger inflows of new work. That said, Moore noted that consumer demand remains constrained by squeezed household incomes, while geopolitical risks continue to weigh on business spending decisions.

The recovery is therefore uneven. While business confidence improved to its highest level since October 2024, firms continued to cut staff at an accelerated pace as they sought to offset rising payroll costs. At the same time, a sharp increase in input prices fed through to the fastest rise in output charges in five months.

New Zealand jobs grow 0.5% in Q4, unemployment ticks to decade-high

New Zealand’s labor market delivered mixed signals in Q4. Employment rose 0.5% qoq, beating expectations for a 0.3% gain, pointing to continued job creation. Employment rate edged up to 66.7% from 66.6%, reinforcing the view that labor demand remains resilient.

At the same time, unemployment rate climbed to 5.4% from 5.3%, above expectations and the highest since the September 2015 quarter. The rise was accompanied by an increase in the labor force participation rate to 70.5% from 70.3%, suggesting that more people are entering or re-entering the job market, which is adding to slack even as hiring continues.

Wage pressures remained contained. The labor cost index rose 2.0% yoy, with private sector wages up 2.0% and public sector wages up 2.2%. The combination of steady employment growth, rising participation, and moderate wage inflation points to a labor market that is still cooling gradually.

Japan PMI composite finalized at 53.1, broadening growth at start of 2026

Japan’s PMI Services was finalized at 53.7 in January, up from December’s 51.6. PMI Composite rose to 53.1 from 51.1. The data point to a clear acceleration in private-sector activity at the start of 2026, with growth firmly back above expansionary levels.

According to Annabel Fiddes of S&P Global Market Intelligence, business activity rebounded at the fastest pace since May 2023. Services remained the primary growth engine, posting the strongest rise in activity in nearly a year, while manufacturing output also returned to growth for the first time since last June.

The surveys suggest the recovery is becoming more broad-based. Demand improved across both manufacturing and services simultaneously for the first time in more than two-and-a-half years, a notable shift after a prolonged period of uneven momentum. Employment was another bright spot, with firms adding staff across both sectors to expand capacity in response to stronger demand.

Cost pressures eased at the start of the year, with input prices rising at their slowest pace in almost two years. However, companies raised selling prices more aggressively, indicating efforts to rebuild margins.

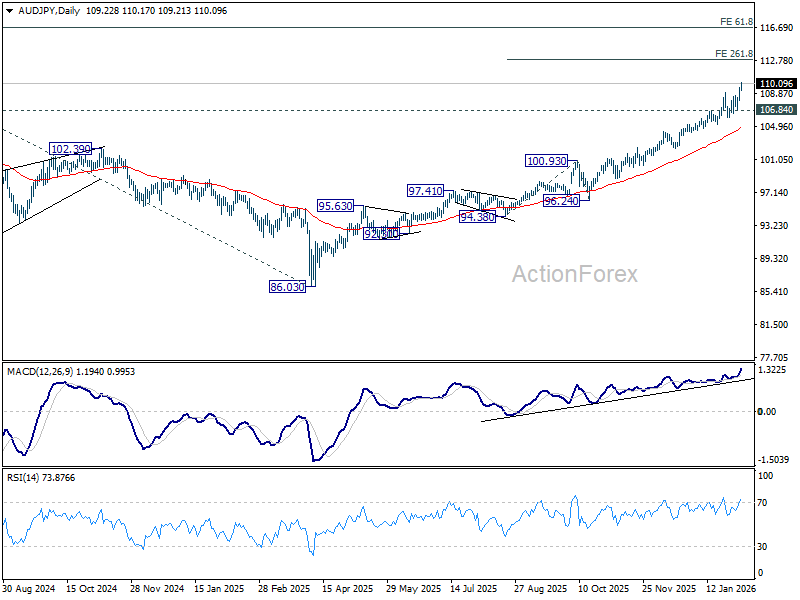

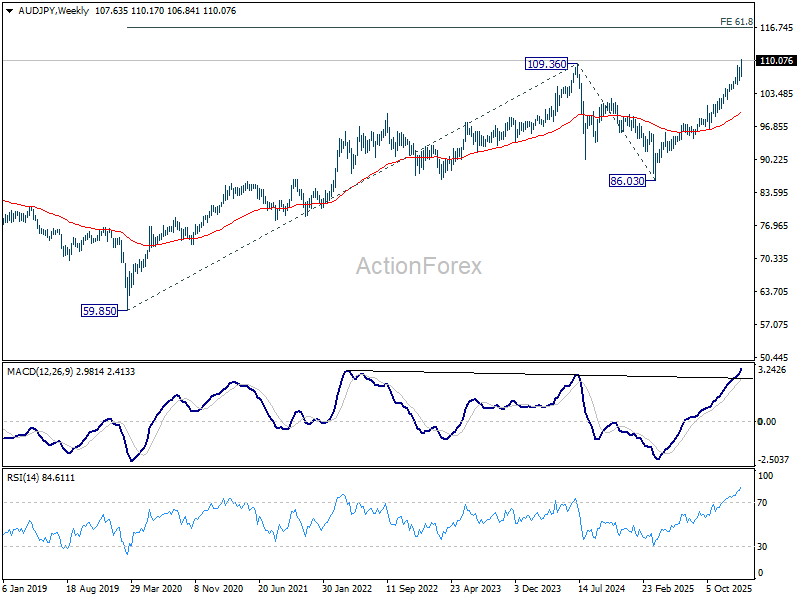

AUD/JPY re-accelerates to new record high, 113 and then 116 next targets

AUD/JPY surged to a fresh record high this week. The move reflects renewed strength in Aussie following a hawkish turn from the RBA, alongside renewed weakness in the Yen as intervention risks fade and election looms.

On the Australian side, the catalyst has been clear. The RBA became the first major central bank to reverse course from easing, responding to a resurgence in inflation that has been building since late last year. Policymakers highlighted stronger-than-expected consumption and a labor market that remains slightly tight, reinforcing that more policy restraint is needed.

Importantly, the RBA’s own forecasts assume interest rates rise further later this year. While officials have avoided pre-committing to a sequence of hikes, the projection alone has been enough to lift Aussie, particularly against low-yielding peers.

In contrast, Yen has come back under broad-based pressure. The perceived risk of intervention—especially coordinated action between Japan and the US—has receded markedly. Conflicting messages from Japanese officials on Yen weakness suggest authorities are not yet prepared to step in directly, at least not before USD/JPY approaches the 160 area again.

Political positioning has added another pressure to Yen. Some traders are positioning ahead of Sunday’s snap election, where the ruling Liberal Democratic Party could secure an outright majority on the back of strong approval for Prime Minister Sanae Takaichi. While her policy agenda raises longer-term fiscal concerns, a decisive win would also buoy domestic equities, reinforcing risk-on sentiment and keeping the Yen under pressure.

That combination of stronger Australian fundamentals and weaker Japanese currency support has proven potent. Even without a sharp change in global risk sentiment, domestic factors alone are sufficient to sustain AUD/JPY upside.

Technically, momentum has re-accelerated, with D MACD turning higher again. Near-term bias stays firmly bullish as long as 106.84 support holds. The next target sits at the 261.8% projection of 94.38 to 100.93 from 96.24 at 113.38.

Looking further out, the next major hurdle comes in at 61.8% projection of 59.85 (2020 low) to 109.36 (2024 high) from 86.03 (2025 low) at 116.62. Price action around that zone will be key in defining whether the current rally extends into a sustained long-term breakout or pauses after an extended run.

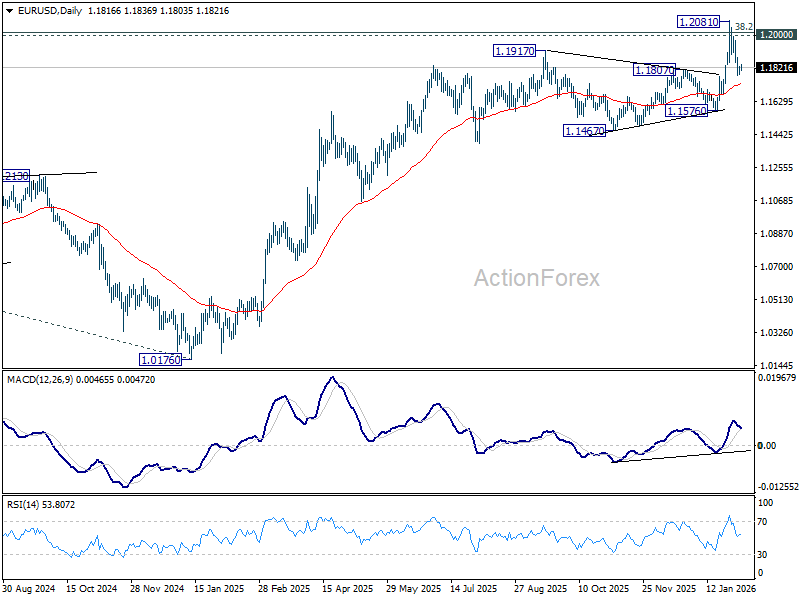

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1790; (P) 1.1809; (R1) 1.1839; More….

Intraday bias in EUR/USD remains neutral as it's bounded in right range above 1.1774. On the downside, below 1.1774 will extend the fall from 1.2081 short term top to 55 D EMA (now at 1.1724). Firm break there will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support. On the upside, above 1.1893 minor resistance will bring stronger rebound to retest 1.2081. Decisive break above 1.2 will carry larger bullish implications.

In the bigger picture, as long as 55 W EMA (now at 1.1458) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.