Sample Category Title

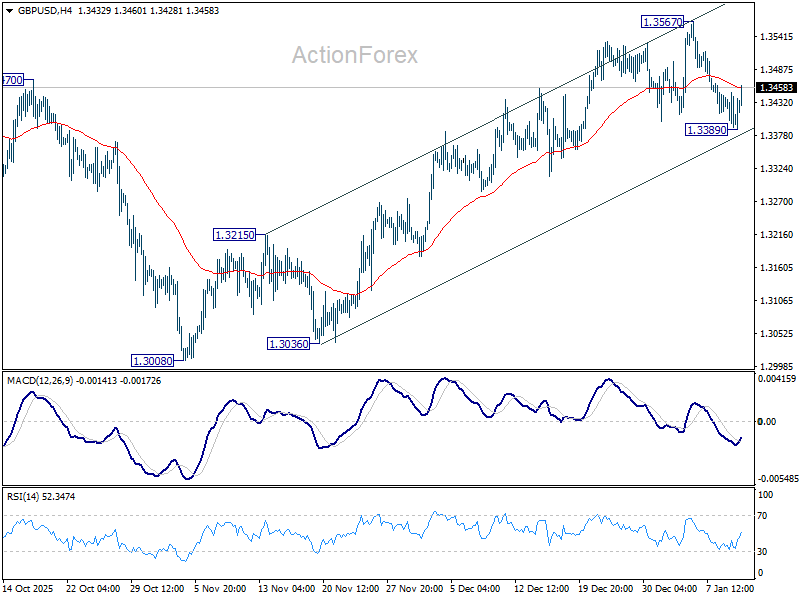

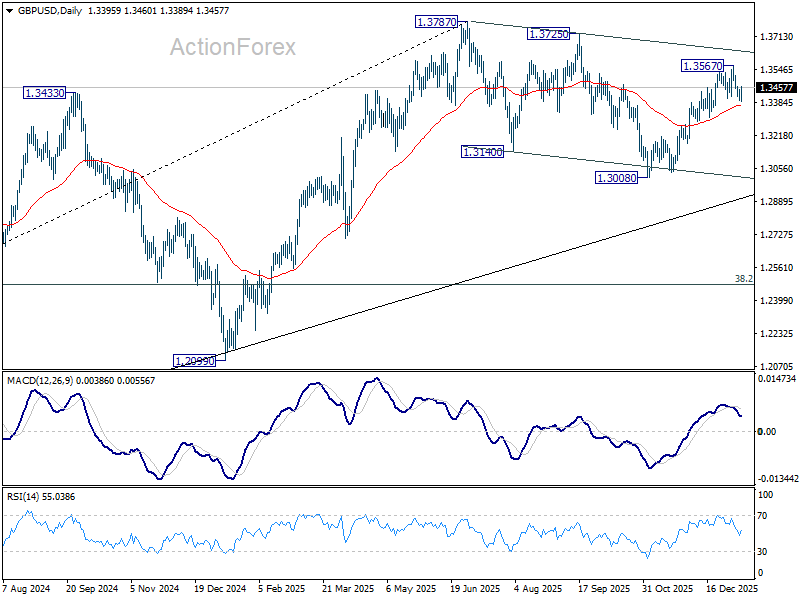

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3381; (P) 1.3416; (R1) 1.3439; More...

Intraday bias in GBP/USD is turned neutral first with current recovery. On the upside, break of 1.3567 will resume the rally from 1.3008 towards 1.3787 high. On the downside, break of 1.3389 will resume the fall from 1.3567. Sustained break of 55 D EMA (now at 1.3370) will argue that the decline is another falling leg in the corrective pattern from 1.3787. In this case, deeper fall should be seen back to 1.3008 support.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). Deeper decline could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.0351 to 1.3787 at 1.2474 to bring rebound. Break of 1.3787 for up trend resumption is expected at a later stage.

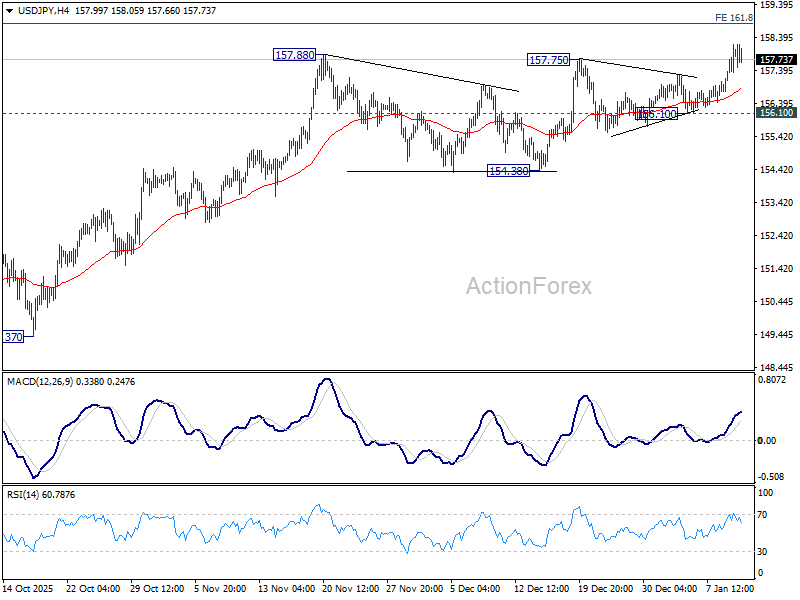

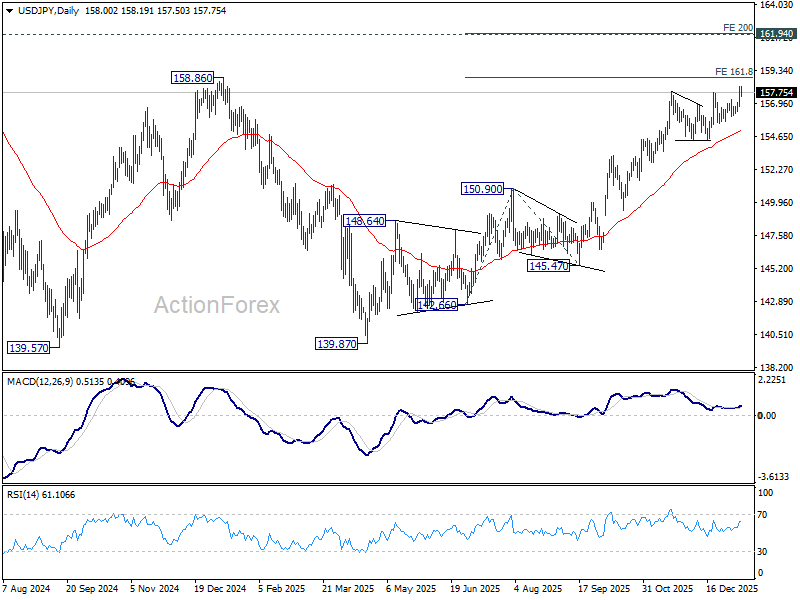

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.54; (P) 156.80; (R1) 157.15; More...

Intraday bias in USD/JPY remains on the upside at this point. Current rise from 139.87 should target 161.8% projection of 142.66 to 150.90 from 145.47 at 158.80. Firm break there will pave the way to 200% projection at 161.95, which is close to 161.94 high. For now, outlook will stay bullish as long as 156.10 support holds, in case of retreat.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

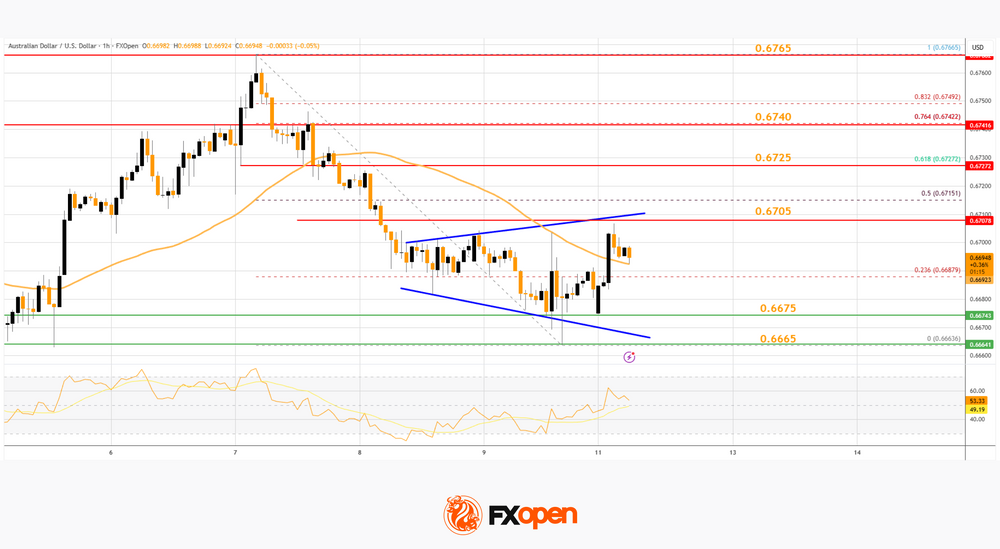

AUD/USD and NZD/USD Pull Back, Caution Creeps In

AUD/USD failed to stay in a positive zone and declined below 0.6700. NZD/USD is also moving lower and might extend losses below 0.5700.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar started a fresh decline from well above 0.6740 against the US Dollar.

- There is an expanding triangle forming with resistance at 0.6705 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD declined steadily from 0.5800 and traded below 0.5760.

- There is a key bearish trend line forming with resistance at 0.5750 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair struggled to clear 0.6765. The Aussie Dollar started a fresh decline below 0.6750 against the US Dollar.

The pair even settled below 0.6720 and the 50-hour simple moving average. There was a clear move below 0.6680. A low was formed at 0.6663, and the pair is now consolidating losses. There was a minor recovery wave above the 23.6% Fib retracement level of the downward move from the 0.6766 swing high to the 0.6663 low.

On the upside, immediate resistance is near an expanding triangle at 0.6705. The next major hurdle for the bulls could be near 0.6725 and the 61.8% Fib retracement.

The main selling point could be 0.6740, above which the price could rise toward 0.6765. Any more gains might send the pair toward 0.6800. A close above 0.6800 could start another steady increase in the near term. In the stated case, the next key resistance on the AUD/USD chart could be 0.6840.

On the downside, initial support is near 0.6675. The next area of interest might be 0.6665. If there is a downside break below 0.6665, the pair could extend its decline. The next target for the bears might be 0.6620. Any more losses might send the pair toward 0.6600.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair also followed a similar pattern and declined from the 0.5800 zone. The New Zealand Dollar gained bearish momentum and traded below 0.5770 against the US Dollar.

The pair settled below 0.5760 and the 50-hour simple moving average. Finally, it tested 0.5710 and is currently consolidating losses. There was a minor increase above the 23.6% Fib retracement level of the downward move from the 0.5810 swing high to the 0.5711 low.

If the pair recovers, it could face hurdles near 0.5750 and a key bearish trend line. The next major barrier is at 0.5760 since it coincides with the 50% Fib retracement.

If there is a move above 0.5760, the pair could rise toward 0.5770. Any more gains might open the doors for a move toward 0.5810 in the coming days. On the downside, immediate support on the NZD/USD chart is 0.5735.

The next major stop for the bears might be 0.5710. If there is a downside break below 0.5710, the pair could extend its decline toward 0.5665. The main target for the bears could be 0.5640.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Price Breaks Above $4,600 for the First Time

At the opening of Monday’s session on 12 January, gold (XAU/USD) gapped higher and briefly moved above the psychological $4,600 level, setting a new all-time high.

Bullish drivers:

→ Geopolitical tensions. Following developments in Venezuela, market attention has shifted to unrest in Iran and renewed discussion around the United States’ interest in Greenland, whether through purchase or other means.

→ Renewed friction between the White House and the Federal Reserve. Over the weekend, Jerome Powell stated that he had received threats of criminal prosecution, possibly linked to his stance on interest-rate cuts, which differs from President Trump’s view.

Technical Analysis of XAU/USD

Seven days ago, on 5 January, our analysis of the gold chart:

→ identified an ascending price channel;

→ highlighted the $4,400 level;

→ outlined a scenario in which the bullish trend could resume after a rebound from the lower boundary of the channel, with $4,400 acting as support.

That scenario has played out. As indicated by the arrow:

→ the market initially pulled back from the channel median;

→ however, as prices approached the $4,400 area, selling pressure faded, and a renewed wave of bullish sentiment pushed XAU/USD to a fresh record high.

Gold is now trading in the upper half of the active ascending channel, signalling overall demand dominance. The strong morning impulse has generated overbought signals on the RSI and increased the likelihood of a pullback. That said, any correction is likely to be limited, given:

→ potential support from the channel median and the $4,500–4,516 zone;

→ a highly tense and supportive fundamental backdrop.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

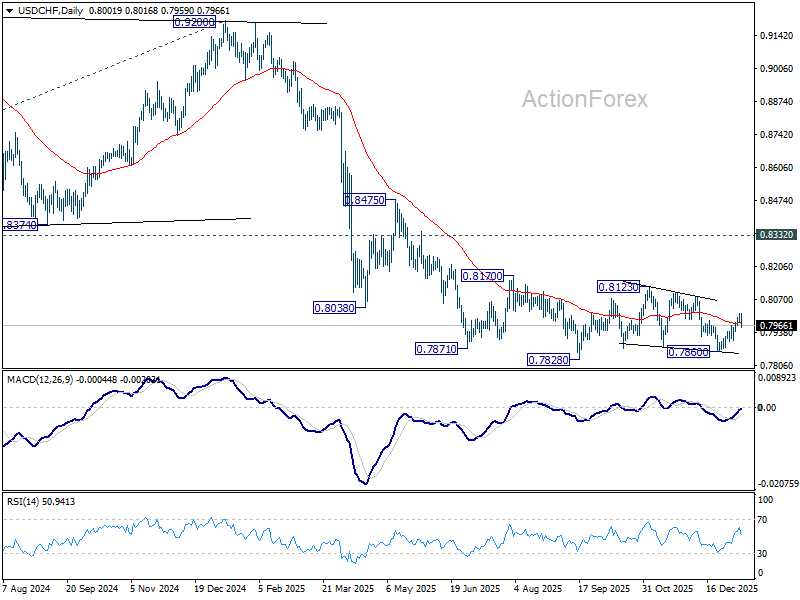

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7990; (P) 0.8004; (R1) 0.8026; More….

Intraday bias in USD/CHF is turned neutral with today's retreat and break of 0.7967 minor support. Overall outlook is unchanged that corrective pattern from 0.7828 low is extending. On the upside, above 0.8016 will target 08123 resistance next. Nevertheless, break of 0.7860 will bring retest of 0.7828, with odds of a break there to resume the larger down trend.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is in still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

Powell–Trump Clash Adds Risk Premium, But Calm Largely Holds for Now

News of a US criminal investigation into Fed Chair Jerome Powell dominated global financial headlines, injecting a fresh dose of political risk into markets. While the investigation itself was unsettling, the sharper jolt came from Powell’s unusually direct response, which framed the episode as part of a broader campaign to pressure the central bank.

In a formal statement posted on the Fed’s website, Powell warned that the threat of criminal charges was a consequence of “broader threats and ongoing pressure” by the administration. The language marked a rare and blunt escalation from a Fed chair typically careful to avoid political confrontation.

Powell went further, stating explicitly that “the threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the President.” Markets interpreted the remark as confirmation that tensions between the Fed and the Donald Trump administration have entered a more confrontational phase.

The clash unsettled markets, but reactions so far remain contained. Gold was the clear standout, surging to fresh record highs as investors sought protection against institutional risk and perceived threats to monetary policy independence. By contrast, moves elsewhere were more restrained. Dollar traded broadly lower, but the selloff lacked momentum. US equity futures dipped modestly, stopping well short of anything resembling disorderly risk-off conditions. Crucially, interest-rate expectations remain stable. Pricing for a March Fed rate cut is largely unchanged, with markets still assigning only around a 30% probability.

For now, investors appear reluctant to extrapolate political noise into imminent policy shifts. But that calm could prove fragile. If the standoff between Trump and Powell intensifies further, markets may be forced to reassess not just Fed independence, but the credibility of forward guidance itself. For now, however, investors are treating the episode as a risk premium adjustment rather than a regime shift.

Elsewhere, Yen continued to weaken, pressured by domestic political developments. Public broadcaster NHK reported that Japan’s ruling Liberal Democratic Party is preparing to dissolve the Lower House later this month, paving the way for a snap election likely in February. The move is seen as an attempt to capitalize on Prime Minister Sanae Takaichi’s strong approval ratings and stabilize the ruling coalition, including the Japan Innovation Party. Japan is on holiday today, leaving markets to assess whether the sharp jump in Nikkei futures will translate into a gap higher and follow-through momentum when trading resumes.

Overall, Dollar sits at the bottom of the performance table so far today, followed by Yen and then Loonie. Swiss Franc leads gains, with Euro and Kiwi close behind, while Aussie and Sterling are broadly in the middle of the pack.

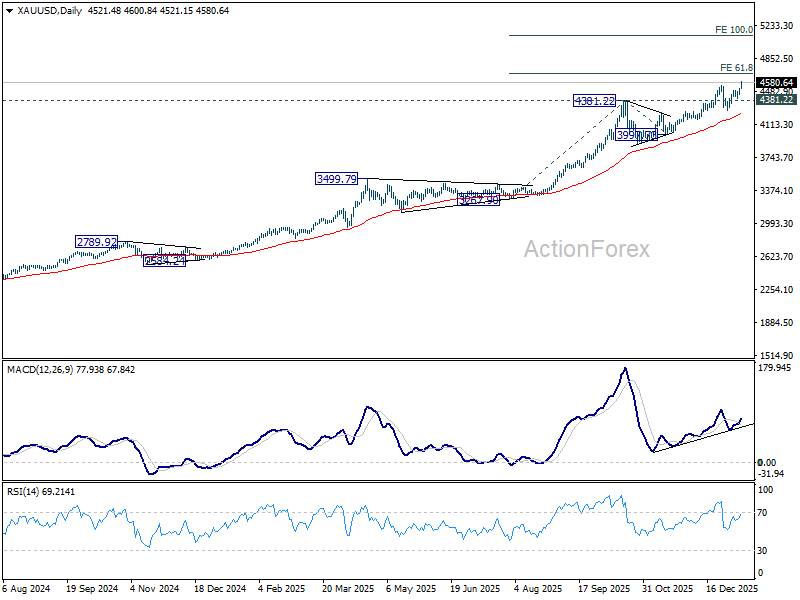

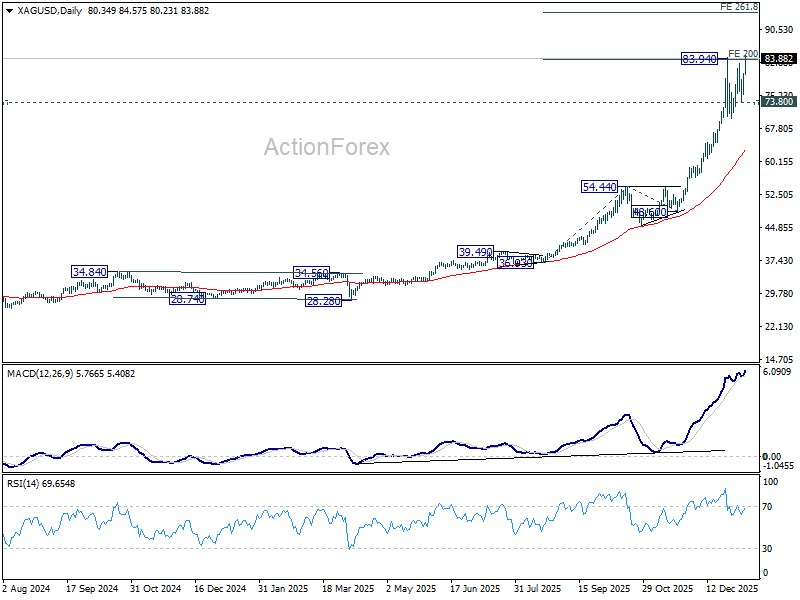

Powell investigation shock sparks Gold rush as 5,000 comes into view

Gold surged to a fresh record high, with Silver following close behind, as markets reassessed political risk around US monetary policy. The 4,685 projection firmly within reach for Gold, and break of which would pave the way to 5,000 psychological level and above.

Additionally, after a year of Silver leadership, momentum may now be shifting back toward Gold, a shift consistent with rising concern over institutional credibility rather than cyclical reflation.

The immediate catalyst came US prosecutors launched on Friday a criminal investigation into Fed Chair Jay Powell. The development jolted markets, reviving concerns that the central bank could face increasing political interference at a time when policy credibility remains critical.

The episode is widely seen as the latest salvo from the Donald Trump administration against the Fed. The central bank has been under sustained pressure to ease policy faster, even as policymakers remain wary of reigniting price pressures or undermining hard-won inflation progress.

Powell, in a statement released Sunday, confirmed that the Fed had received grand jury subpoenas and a threat of criminal indictment from the Justice Department. The matter relates to his testimony before Congress concerning a USD 2.5B renovation of the Fed’s headquarters, though Powell framed the move in a much broader political context.

He warned that the action should be seen against a backdrop of ongoing threats and pressure aimed at forcing lower interest rates and securing greater political control over monetary policy. He said bluntly, "this unprecedented action should be seen in the broader context of the administration’s threats and ongoing pressure".

Technically, Gold's up trend resumed and it's now on track to 61.8% projection of 3,267.90 to 4,381.22 from 3,997.73 at 4,685.76. Decisive break there will pave the way to 5,000 psychological level, and possible further to 100% projection at 5,111.05. Outlook will stay bullish as long as 4,381.22 resistance turned support holds, in case of retreat.

Silver is also trying to resume its long term up trend. Sustained trading above 83.94 resistance will pave the way to 261.8% projection of 36.93 to 54.44 from 48.50 at 94.34. Nevertheless, break of 73.80 will bring another pullback first.

US December CPI seen as speed bump, not a turning point for risk markets

December US inflation data dominates the macro calendar, as the broader week is filled mostly with second-tier releases. For markets, CPI is the key checkpoint for Fed policy expectations, though the bar for a disruptive surprise appears high.

November’s CPI print drew criticism from some economists, who argued that prolonged US government shutdown effects may have dampened the readings. Disruptions were seen as distorting seasonal patterns and muting underlying price pressures, leaving markets cautious about overinterpreting the softness.

Those distortions should fade in the December release. Consensus looks for headline CPI to hold steady at 2.7%, while core CPI is expected to tick higher from 2.6% to 2.7%. Such an outcome would offer little encouragement for earlier easing from the Fed. With core inflation still sticky, policymakers are likely to maintain their wait-and-see approach.

Markets pricing suggests just over a 70% chance of no change in March, with June shaping up as the earliest realistic opportunity for a cut, coinciding with updated economic projections that could give the Fed greater confidence.

Importantly, this outlook appears largely embedded in asset prices. As long as the data does not force a meaningful shift in the expected rate path. As a result, CPI may prove to be more of a clearing event than a catalyst. Absent a dramatic surprise, risk-on momentum could extend once uncertainty around the release passes, with investors comfortable holding positions aligned to mid-year easing.

In the UK, monthly GDP data is another focal point, with expectations for marginal growth of 0–0.1% in November. Activity had been weighed down by uncertainty ahead of the Autumn Budget, a drag that likely lingered, though consumer-facing sectors may have seen some support from pre-holiday demand and Black Friday promotions.

For the BoE, ongoing weakness in activity strengthens the case for further cuts, even if delivered cautiously. However, policymaker rhetoric continues to highlight internal divisions, leaving February finely balanced, while March remains the more probable window for the next move.

Here are some highlights for the week:

- Monday: Eurozone Sentix investor confidence:

- Tuesday: New Zealand NZIER business confidence; Australia Westpac consumer sentiment; US CPI.

- Wednesday: China trade balance; US retail sales, PPI, Fed's Beige Book.

- Thursday: Japan PPI; UK GDP; Eurozone industrial production, trade balance; Canada manufacturing sales, wholesale sales; US jobless claims, Empire state manufacturing; Philly Fed manufacturing, import prices.

- Friday: New Zealand BNZ manufacturing; US industrial production, NAHB housing index.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7990; (P) 0.8004; (R1) 0.8026; More….

Intraday bias in USD/CHF is turned neutral with today's retreat and break of 0.7967 minor support. Overall outlook is unchanged that corrective pattern from 0.7828 low is extending. On the upside, above 0.8016 will target 08123 resistance next. Nevertheless, break of 0.7860 will bring retest of 0.7828, with odds of a break there to resume the larger down trend.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is in still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

Fed Chair’s Forceful Reaction Marks a Clear Escalation in Fight on Central Bank Independency

Markets

Chances had already become quite slim and Friday’s US eco data rubberstamped markets’ feeling that the Fed has good reason to wait for clearer directional evidence that the economy is weakening and/or is inflation is moving decisively closer to target before further easing policy. Indeed, US December payrolls with monthly job growth at 50k (vs 70k expected) was no ‘grand cru’. However, with the unemployment rate easing from 4.5% to 4.4%, it only confirms the ‘low-hiring, low firing’ pattern that already reigns on the US labour market for quite some time. Average hourly earnings at 0.3% M/M and 3.8% Y/Y even were marginally higher than expected. Later in the session, consumer confidence of the University of Michigan also printed slightly stronger than expected (54 vs 52.9) with inflation expectations indicators (4.2% at 1-y and 3.4% for the 5 & 10-y sector) still printing uncomfortably high. Markets now have fully prices out an end January Fed rate cut. A next fine-tuning move now is only fully discounted for the June meeting. The US yield curve logically flattened with the 2-y adding 4.4 bps as the 30-y yield ceded 2.5 bps. German yields only changed 1 bps (at best). Markets on Friday also looked out at the opinion/ruling of the of the Supreme Court on the IEEPA US trade tariffs, but the judgment was delayed, maybe until this week. Equity markets at least could live with the Fed likely taking a balanced approach on further easing. US indices added between 0.48% (Dow) and 0.81 % (Nasdaq). The Eurostoxx 50 even remain on record path (+1.58%). The dollar retained its advantage over other majors. DXY closed a solid start to the new year at 99.13. EUR/USD dropped to close to week at 1.1637 (to be compared with a 1.1746 open on Jan 2).

The week after the payrolls usually brings some data poverty. US CPI data tomorrow and retail sales (Wed.) still are worth looking at but likely won’t change markets assessment on Fed policy. However, the lack of data drivers might be compensated for by multiple event risks that resurfaced or intensified during the weekend. Overnight, Fed Chair Powell said that the US central bank was served with grand jury subpoenas, related to Powell’s testimony and the renovations of the Fed headquarters. However, the Fed Chair clearly indicated that the move ‘should be seen in the broader context of the administration’s threats and ongoing pressure’. The Fed Chair’s forceful reaction marks a clear escalation in the fight on central bank independency. In a first reaction US risk premia understandably are rising. The 30-y US Treasury yield adds 3.5 bps. US equity futures are ceding 0.5%+. The dollar is falling prey to a reversal after recent gains. EUR/USD rebounds to the 1.167 area. Also keep an eye at other (geo)political event risk including to the US reaction on the tensions in Iran and the still pending ruling of the US Supreme Court on tariffs. Especially the fight on Fed independence will be highly debated on the financial newswires. In a first reaction it might put some further pressure on US assets, including the dollar. Still we are cautions to already draw firm, directional conclusions based on current ‘headlines’. The auction of US 3-y and 10-y paper this evening in this respect might be a good pointer of appetite for US assets as the Fed independency debate lingers.

News & Views

Rumours are swirling in Japan that PM Takaichi will call for snap elections. The co-leader of junior coalition party Ishin yesterday hinted at that when saying he felt “we have shifted to a new stage now” after talking with Takaichi. The biggest opposition party after the Sunday quote said they are now in election mode. Takaichi’s LDP under her predecessor Ishiba lost its majority in both houses of parliament. It now has a razor-thin one in the powerful lower house thanks to Ishin and the support of three independent lawmakers. Takaichi is polling high and is rumoured to announce the dissolution of the lower house as soon as January 23. Japanese markets are closed today in observance of Coming-of-age Day but it is expected that snap elections may lift (longer-term) bond yields through rising fiscal risk premia.

US President Trump is demanding credit-card companies to cap interest rates at 10%, drastically down of the 20%+ in recent years. Lenders argue that such rates are to compensate for the lack of collateral when borrowers default and warn the rates cap could result in reduced credit availability. Trump has set January 20 as a deadline for companies to comply, adding that they would be “in violation of the law” if they didn’t. POTUS’ move follows instructions last week for government-sponsored enterprises Fannie Mae and Freddie Mac to purchase $200bn in mortgage bonds, aimed at driving down mortgage rates.

Powell investigation shock sparks Gold rush as 5,000 comes into view

Gold surged to a fresh record high, with Silver following close behind, as markets reassessed political risk around US monetary policy. The 4,685 projection firmly within reach for Gold, and break of which would pave the way to 5,000 psychological level and above.

Additionally, after a year of Silver leadership, momentum may now be shifting back toward Gold, a shift consistent with rising concern over institutional credibility rather than cyclical reflation.

The immediate catalyst came US prosecutors launched on Friday a criminal investigation into Fed Chair Jay Powell. The development jolted markets, reviving concerns that the central bank could face increasing political interference at a time when policy credibility remains critical.

The episode is widely seen as the latest salvo from the Donald Trump administration against the Fed. The central bank has been under sustained pressure to ease policy faster, even as policymakers remain wary of reigniting price pressures or undermining hard-won inflation progress.

Powell, in a statement released Sunday, confirmed that the Fed had received grand jury subpoenas and a threat of criminal indictment from the Justice Department. The matter relates to his testimony before Congress concerning a USD 2.5B renovation of the Fed’s headquarters, though Powell framed the move in a much broader political context.

He warned that the action should be seen against a backdrop of ongoing threats and pressure aimed at forcing lower interest rates and securing greater political control over monetary policy. He said bluntly, "this unprecedented action should be seen in the broader context of the administration’s threats and ongoing pressure".

Technically, Gold's up trend resumed and it's now on track to 61.8% projection of 3,267.90 to 4,381.22 from 3,997.73 at 4,685.76. Decisive break there will pave the way to 5,000 psychological level, and possible further to 100% projection at 5,111.05. Outlook will stay bullish as long as 4,381.22 resistance turned support holds, in case of retreat.

Silver is also trying to resume its long term up trend. Sustained trading above 83.94 resistance will pave the way to 261.8% projection of 36.93 to 54.44 from 48.50 at 94.34. Nevertheless, break of 73.80 will bring another pullback first.

Dancing to Unpredictable Tunes

The year continues at full speed, with data, political, and geopolitical headlines — all very interesting and worrying.

Last week, we were talking about oil — in the context of the U.S.’s capture of Maduro in an overseas operation that raised questions about international law and sovereignty. Oil and oil stocks fluctuated throughout the week as the U.S. said it wants to rebuild the country’s aging infrastructure to pump that oil and sell it. Exxon Mobil said last Friday that Venezuela was investable, and Trump quickly responded that they would keep Exxon out of Venezuela because he didn’t like their response. So, as everywhere, U.S. government intervention will heavily influence winners and losers. If you want to understand why stocks move the way they do, Trump’s Social Truth feed might give you a better explanation than traditional data and earnings.

SPDR’s energy ETF hit a record high last week, retreated, and closed the week on a positive note. Crude oil tested the 50-day moving average (DMA) and opened the week above it, but bullish bets remain very timid. Net bullish positions are around 15-year lows. That’s because oil supply is ample thanks to record U.S. pumping and OPEC’s restoration strategy. It’s hard to see oil bulls clearing key resistance levels: $62.50 per barrel (200-DMA) and $64 per barrel (38.2% Fib retracement of the June–December rally). Price rallies are being seen as opportunities to strengthen short positions, targeting the $53–55pb range.

This week, Jerome Powell is on the front page of Bloomberg news as the DOJ has targeted him and the Fed over his congressional testimony on ongoing renovations of the Federal Reserve’s (Fed) headquarters. That came on Friday. Powell hit back, saying this has little to do with the renovations, and more to do with Trump being unhappy with the Fed’s rate-setting policies — specifically, that they are not cutting rates as aggressively as he would like. Powell highlighted that the key issue is whether the Fed can continue setting interest rates based on economic data and evidence, or whether monetary policy will be directed by political pressure.

I’m afraid we may be moving toward the second scenario. If the Fed becomes a political tool, with its chair replaced by a government puppet, that could further weaken appetite for the U.S. dollar and U.S. bonds.

For those still following traditional economic news, last Friday’s U.S. jobs data was mixed. The economy added 50’000 jobs in December — fewer than analysts expected — but the unemployment rate fell and average earnings growth accelerated. Overall, the jobs market is weakening moderately, and with inflation risks looming, the Fed may wait before cutting rates. The U.S. 2-year yield jumped to 3.54%, and the probability of a March rate cut fell to 30% from around 50% a week ago. Equity markets reacted positively: the small-cap index added 0.78%, and the Nasdaq 100 gained more than 1%.

Part of the support comes from the Fed injecting liquidity through its RMPs, and the U.S. government now suggesting to buy $200 billion in mortgage bonds to reduce housing costs. It’s not officially QE, but the mechanics resemble the Fed’s bond and MBS purchases under QE, which injected tens of billions into the system through government and MBS purchases. Regardless of who injects cash — the Fed or the government — the outcome is ample liquidity, which markets are loving. So there’s no reason to exit equities. In theory, these measures could further boost inflation pressures, and equities could help investors manage that risk.

Speaking of inflation, the U.S. inflation data will be a major highlight this week. The previous CPI report was questionable, with housing inflation held at 0% due to missing data, resulting in unusually low numbers. This week, fresh data is expected, with the headline figure seen stable near 2.7%. Higher-than-expected numbers would likely temper Fed rate-cut expectations, and analysts will scrutinize the methodology to see if it reflects reality.

Again, if the Fed can’t set policy based on economic data and inflation picks up, you want assets that temper inflation risks: gold, commodities, inflation-linked bonds, dividend-paying stocks, and tech.

Asian tech kicked off the year outperforming U.S. peers. TSMC revenues topped estimates last week, and the company will release earnings this week, highlighting continued AI-related revenue growth. The valuation gap between U.S. and Asian tech suggests further inflows toward the latter, which are supported by earnings growth expectations: EPS is expected to grow 79% in South Korea, 36% in Taiwan, and 28% for the Nasdaq, according to Bloomberg. The Korean Kospi started the new week at a fresh record high, while the Chinese Hang Seng is up 1.2% at the time of writing.

Powell Investigation Casts Spotlight on Fed

In focus today

In the euro area, the Sentix indicator is released today, providing the first estimate of investor confidence in 2026. While confidence improved in 2025 compared to 2024, it ended the year on a downward trajectory.

In Denmark, December inflation data is released. We expect a decline to 1.9% from 2.1% in November, driven by falling fuel prices. It will also be interesting to see if December's butter sales confirm the recent trend of lower food prices.

The week's economic calendar is light, with key US data releases including CPI on Tuesday, followed by PPI and retail sales on Wednesday. Also on Wednesday, the Supreme Court is expected to issue its next ruling on President Trump's use of emergency tariff powers under IEEPA. On Thursday, Germany's statistics agency will publish a full-year 2025 GDP estimate, offering insight into Q4 growth, while the UK's November GDP data is released.

The year 2026 has begun with significant developments, particularly in geopolitics rather than economics. In our latest report, Geopolitical Radar: What's next after US assault on Venezuela?, 9 January, we explore these dynamics further. We kindly invite you to share your insights by participating in our Reader Prediction Survey 2026.

Economic and market news

What happened over the weekend

In the US, Fed Reserve Chair Powell is under investigation regarding his testimony last summer about the central bank's building renovation project. In a video statement released last night, Powell described the investigation as a pretext for Trump's ongoing efforts to pressure the Fed to lower interest rates and undermine its independence.

In geopolitics, Iran warned the US against military intervention amidst widespread protests, following Trump's statement that Washington is 'ready to help'. As noted in our Geopolitical Radar, the US may target Iran's regime next. While June's bombing of nuclear facilities caused only a temporary setback, the US's access to Venezuelan oil may reduce concerns about Iranian retaliation. The ongoing protests in Iran could provide a pretext for US-Israeli intervention. According to US officials, Trump is set to be briefed on Tuesday regarding potential responses to the protests in Iran.

What happened Friday

In the US, the December jobs report came in close to expectations, with nonfarm payrolls (NFP) increasing by 50k jobs (consensus: 60k). The unemployment rate declined to 4.4% from 4.6%, supported by solid job growth (+232k) in the household survey and a shrinkage in labour supply (-46k), which explains the drop in the unemployment rate. Similar to the ADP survey, job growth was concentrated in a few sectors, particularly services such as leisure, hospitality, education, and healthcare, while the manufacturing sector recorded job losses (-8k).

On Friday, the preliminary January result of the University of Michigan survey showed that consumers' long-term inflation expectations (5-year) edged up slightly to 3.4% from 3.2% in December, while 1-year inflation expectations remained stable at 4.2%. Consumers showed slightly improved optimism, reflected in the recovery of both current conditions and future expectations in the consumer sentiment component. However, uncertainty around IEEPA tariffs persists and may influence sentiment going forward.

In Norway, core inflation rose slightly to 3.1% y/y in December, driven by higher food prices due to fewer pre-Christmas discounts compared to 2024. Imported inflation appears to be rising again, while domestic inflation remains around 4%. Rent inflation eased to 3.6%, despite signs of higher market-based rents. The December print of 3.1% y/y is marginally above Norges Bank's estimate from the December MPR (3.0%), but unlikely to affect expectations of a rate cut in June.

In Sweden, the GDP indicator for November showed robust growth, rising by 0.9% m/m and 2.7% y/y, driven primarily by the service sector. Private sector production (PVI) grew by 0.5% in November, with the service sector up by 0.7%, while the industrial sector declined by 0.1%. These results align with our forecast and further confirm the ongoing Swedish recovery, though volatility in the GDP indicator remains a consideration.

In the euro area, retail sales exceeded expectations in November, rising by 0.2% m/m (cons: 0.1% m/m) and 2.3% y/y, significantly above forecasted 1.6% y/y due to a major upward revision of October's figures. This is an encouraging sign, indicating that businesses and consumers are adapting well to external shocks such as tariffs.

Equities: Global equities had a strong day on Friday with the cyclicals outperforming the defensives. Tech was once again not in the top performers, extending the pattern we have observed since the start of the year. S&P500 rose 0.6%, Nasdaq +0.8%, Russell2000 +0.8% and Stoxx600 rising 1%. Materials was clearly the outperformer on Friday rising 1.8%. Year to date, Russell2000 has been off to a strong start rising almost 5%, well above the 1.5% rise in S&P500. Asian markets are in green this morning.

FI and FX: Over the weekend, the Federal Reserve was served with subpoenas from the Justice Department threatening a criminal indictment, related to Chairman Powell's testimony in Congress regarding the Fed headquarters' renovations. Chairman Powell has pushed back on this in a video and statement, saying that it is a consequence of the Fed setting monetary policy that will best suit the public, rather than the preferences of the US President. The dollar weakened on the news, with EUR/USD moving from a low of 1.1622 to 1.1663. Gold prices are about 1.5% higher and US equity futures are trading lower (S&P -0.6%). There has been no UST cash trading overnight as Japan has been closed.