Sample Category Title

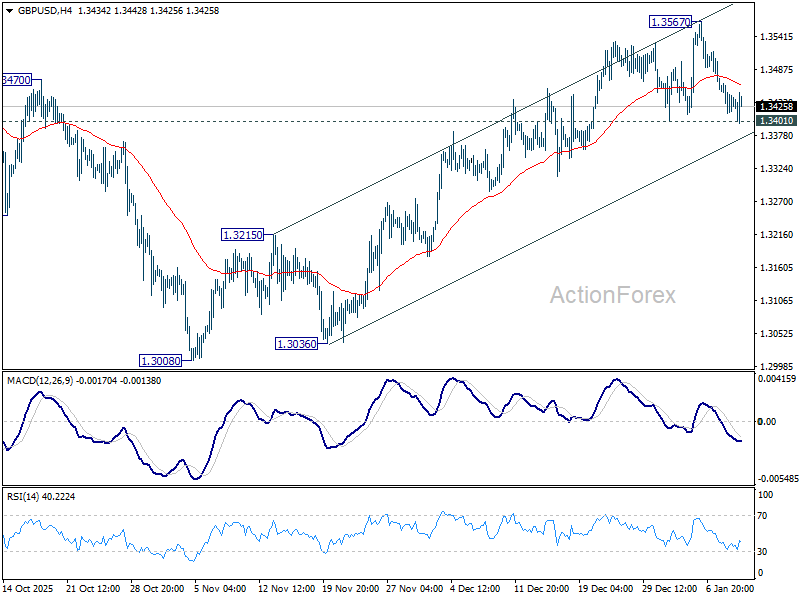

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3416; (P) 1.3440; (R1) 1.3465; More...

GBP/USD is still holding on to 1.3401 support and intraday bias remains neutral. Further rise is mildly in favor. On the upside, break of 1.3567 will resume the rise from 1.3008 to retest 1.3787 high. However, firm break of 1.3401 will confirm short term topping, and bring deeper fall back to 55 D EMA (now at 1.3367). Sustained break of 55 D EMA will argue that corrective pattern from 1.3787 is already extending with another falling leg, and target 1.3008.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

US Non-Farm Payrolls at + 50K (small) miss, Market Reactions – Get ready for Supreme Court Tariffs Decision!

US Non-Farm Payrolls release at +50K – A slight miss to the +60K Expectations

This takes the Unemployment Rate, most favored data since the Bureau of Labor Statistics shutdown affected data, to 4.4%, lower than the 4.5% expectations and lower than the past month.

Unrounded numbers show 4.375% vs 4.564% prior. Participation Rate is also slightly lower.

Average Hourly Earnings at 0.3% M/M and 3.8% Y/Y, a bit higher than expectations on the Y/Y number.

The report provides even less reasons for the Fed to cut rates in end-January.

You can get full access to the report right here.

Don't Forget that Markets will await the Supreme Court Tariffs Decision at 10:00 A.M.

It seems that traders are reacting counterintuitively to a not-so-dovish number with the Dollar falling, Gold rallying.

Keep an eye at the end of the hour and the 9:30 Market Open to see if such reactions fade.

Check out Market reactions:

US Dollar (Dollar Index DXY)

DXY 15 min Chart – January 9, 2026. Source: TradingView

Gold (XAU/USD)

Gold (XAU/USD) 15 min Chart – January 9, 2026. Source: TradingView

Pre-open Dow Jones (Futures and CFD)

Dow Jones 15 min Chart – January 9, 2026. Source: TradingView

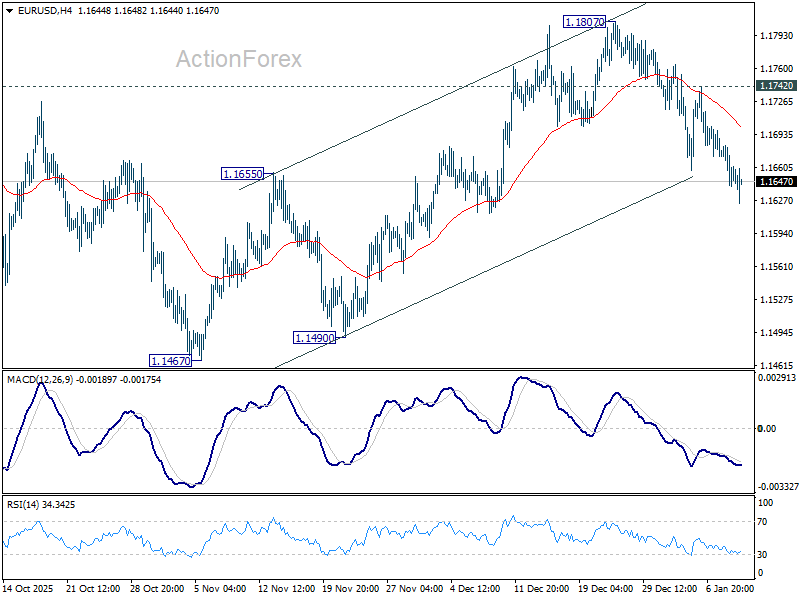

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1642; (P) 1.1663; (R1) 1.1682; More….

EUR/USD recovers mildly after NFP but overall outlook is unchanged. Intraday bias stays on the downside for the moment. Prior break of 55 D EMA (now at 1.1671) suggests that rebound from 1.1467 has already completed. Overall development indicates that corrective pattern from 1.1917 is already in the third leg. Further decline should be seen to 1.1467 support, and below. On the upside, though, break of 1.1742 will turn bias back to the upside for 1.1807 resistance instead.

In the bigger picture, as long as 55 W EMA (now at 1.1408) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Dollar Eases Slightly as NFP Fails to Deliver Upside Surprise

Dollar softened modestly in early US trading after the release of mixed December labor market data. The headline payroll gain undershot expectations, but the miss did little to challenge the broader narrative of a labor market that is slowing gradually rather than deteriorating abruptly.

More importantly, for monetary policy, the fall in the unemployment rate alongside still-solid wage growth points to lingering tightness beneath the surface. Labor demand may be cooling, but conditions remain firm enough to prevent a decisive shift in policy expectations.

As such, the report offered little that is materially decisive for the Fed’s easing plans. It neither strengthens the case for aggressive cuts nor signals an urgent need to respond to labor market weakness.

Dollar’s mild pullback appears more like a positioning adjustment than a change in conviction. Some traders had built long USD exposure ahead of the release, anticipating an upside surprise that ultimately failed to materialize.

With that risk removed, it is clear that US 10-year yield lacks the momentum needed to break decisively above 4.2% resistance zone, a development that could cap any renewed Dollar rally attempt. Meanwhile, US equity futures firmed as payrolls uncertainty passed. While there is no strong upside momentum in stocks yet, the clearance of event risk is offering some near-term relief, with DOW likely to have a serious test of the 50,000 level later in the month.

On weekly FX performance, Dollar still leads overall, followed by Aussie and Sterling. Loonie remains the weakest, with Swiss Franc and Euro also underperforming. Yen and Kiwi trade in the middle of the pack.

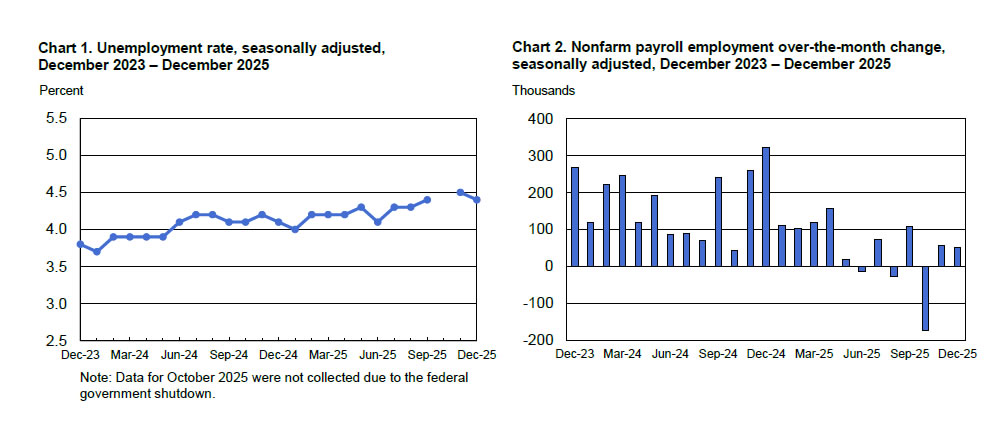

US NFP misses by rising 50k in December, but unemployment rate falls to 4.4%

US non-farm payrolls rose by 50k in December, undershooting expectations of 66k. Downward revisions to prior months added to the softer tone, with October employment revised lower by -68k to -173k, and November trimmed by -8k to 56k.

However, the unemployment rate fell unexpectedly from 4.6% to 4.4%, beating expectations and suggesting labor market conditions remain tight despite slower job growth. Average hourly earnings rose 0.3% mom, in line with forecasts, keeping annual wage growth elevated at 3.8% .

Payroll growth in 2025 totaled just 584k, sharply lower than the 2.0 million increase in 2024.

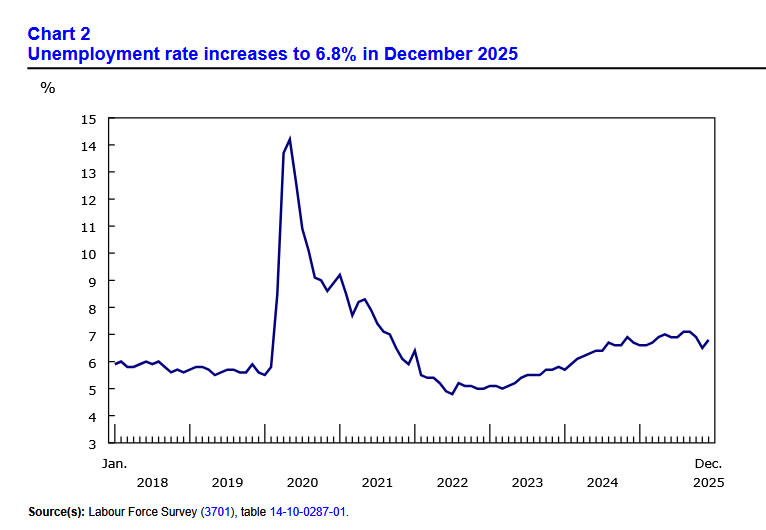

Canada jobs beat with 8.2k growth, masks rising unemployment

Canada’s labor market delivered a modest upside surprise in December, with employment rising 8.2k, defying expectations for -5k decline. The gain, however, marked a sharp slowdown after three strong months that added a combined 181k jobs through November, signaling that momentum is cooling into year-end.

Beneath the headline, job composition was mixed. Full-time employment surged by 50k, while part-time jobs fell by -42k, pointing to improving job quality even as overall growth slowed.

At the same time, the unemployment rate jumped to 6.8% from 6.5%, above forecasts, reflecting a notable increase in labor supply. Indeed, the participation rate rose 0.3ppt to 65.4%, while the employment rate held steady at 60.9%, suggesting new entrants are outpacing hiring.

Wage growth eased slightly to 3.4% yoy, down from 3.6% in November.

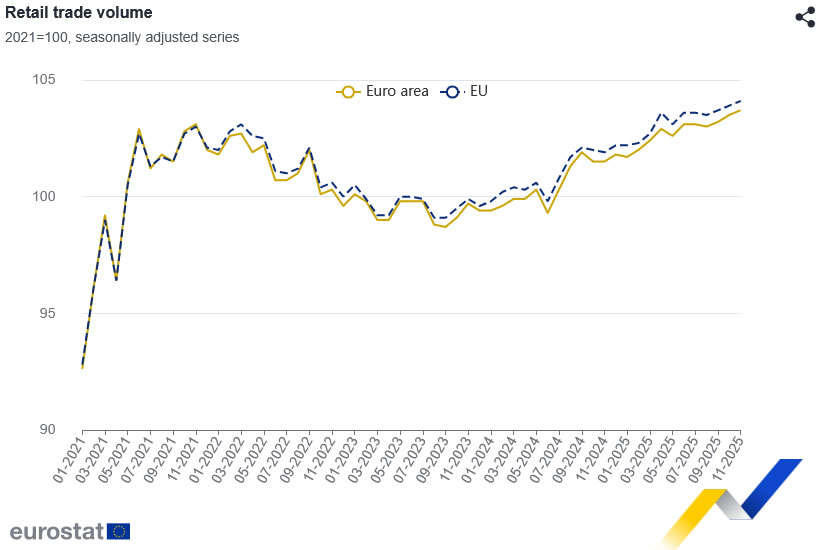

Eurozone retail sales rise 0.2% mom in November, as non-food demand improves

Eurozone retail sales volumes rose 0.2% mom in November, slightly above expectations of 0.1% increase. The improvement was driven primarily by non-food products, where sales increased 0.4% mom, offsetting weakness elsewhere. Sales of food, drinks and tobacco slipped -0.2%, while automotive fuel volumes fell -0.1%.

Across the broader EU, retail sales also rose 0.2% mom, but national divergences were stark. Luxembourg posted a sharp 5.8% surge, followed by Portugal (2.2%) and Denmark (1.9%). Croatia (-2.2%), Belgium (-1.6%) and Slovakia (-1.5%) recorded notable declines.

China CPI surprises to upside at 0.8%, but full-year picture weak

China’s consumer inflation accelerated in December, with CPI rising from 0.7% to 0.8% yoy, above expectations of 0.6% and marking a 34-month high. The increase was driven mainly by food prices, as fresh vegetables surged 18.2% and beef prices rose 6.9%, supported by pre-New Year holiday demand.

However, price pressures remained uneven. Pork prices continued to fall sharply, down -14.6% yoy, while prices of gold jewelry jumped 68.5%, reflecting strong investment and gifting demand rather than broad-based consumption. According to National Bureau of Statistics, holiday shopping and supportive policies helped lift prices, but the improvement remains selective.

Looking beyond December, the broader deflationary challenge persists. Full-year CPI growth in 2025 was flat, the weakest in 16 years and well below policymakers’ “around 2%” target.

At the producer level, deflation moderated only slightly. PPI improved to -1.9% yoy in December from -2.2%, aided by rising non-ferrous metal prices and capacity discipline in key industries. Still, PPI fell 2.6% for the full year.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1642; (P) 1.1663; (R1) 1.1682; More….

EUR/USD recovers mildly after NFP but overall outlook is unchanged. Intraday bias stays on the downside for the moment. Prior break of 55 D EMA (now at 1.1671) suggests that rebound from 1.1467 has already completed. Overall development indicates that corrective pattern from 1.1917 is already in the third leg. Further decline should be seen to 1.1467 support, and below. On the upside, though, break of 1.1742 will turn bias back to the upside for 1.1807 resistance instead.

In the bigger picture, as long as 55 W EMA (now at 1.1408) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Canada jobs beat with 8.2k growth, masks rising unemployment

Canada’s labor market delivered a modest upside surprise in December, with employment rising 8.2k, defying expectations for -5k decline. The gain, however, marked a sharp slowdown after three strong months that added a combined 181k jobs through November, signaling that momentum is cooling into year-end.

Beneath the headline, job composition was mixed. Full-time employment surged by 50k, while part-time jobs fell by -42k, pointing to improving job quality even as overall growth slowed.

At the same time, the unemployment rate jumped to 6.8% from 6.5%, above forecasts, reflecting a notable increase in labor supply. Indeed, the participation rate rose 0.3ppt to 65.4%, while the employment rate held steady at 60.9%, suggesting new entrants are outpacing hiring.

Wage growth eased slightly to 3.4% yoy, down from 3.6% in November.

US NFP misses by rising 50k in December, but unemployment rate falls to 4.4%

US non-farm payrolls rose by 50k in December, undershooting expectations of 66k. Downward revisions to prior months added to the softer tone, with October employment revised lower by -68k to -173k, and November trimmed by -8k to 56k.

However, the unemployment rate fell unexpectedly from 4.6% to 4.4%, beating expectations and suggesting labor market conditions remain tight despite slower job growth. Average hourly earnings rose 0.3% mom, in line with forecasts, keeping annual wage growth elevated at 3.8% .

Payroll growth in 2025 totaled just 584k, sharply lower than the 2.0 million increase in 2024.

Chart Alert: Silver (XAG/USD) Intraday Rally is Fast Approaching Key Resistance

Key takeaways

Rebound looks corrective, not impulsive: Silver’s ~6% intraday bounce from US$73.84 appears to be a countertrend rebound after a sharp 10.7% sell-off, with technical patterns suggesting a “dead cat bounce” rather than a trend resumption.

Key resistance and downside risk: The US$79.86 level is a critical inflection point. Failure there, followed by a break below US$74.07, would likely open another corrective leg toward US$70.52 and potentially the 50-day moving average zone.

Bullish structure intact but delayed: While the long-term secular uptrend remains intact, near-term momentum is fading, and a deeper mean-reversion decline may be needed before the next sustainable bullish impulsive move.

The earlier 10.7% drop in Silver (XAG/USD) from its 7 January 2026 high of US$82.77 to yesterday, Thursday, 8 January 2026 low of US$73.84 has started to evolve to see an intraday rally of 6% (low to high) to trade higher at US$78.05 at the time of writing ahead of today’s key risk event; the release of US non-farm payrolls and unemployment rate for December 2025.

However, technical analysis suggests that the short-term corrective decline structure of Silver (XAG/USD) may not have ended, with more potential weakness ahead to shape a mean reversion decline towards its 50-day moving average (around US$62.75/61.91 zone) before the start of a new bullish impulsive up move sequence within its long-term secular uptrend phase that remains intact since the 18 March 2020 low.

Short-term trend bias (1 to 3 days): Reaching the inflection point for another potential down leg

Fig. 1: Silver (XAG/USD) minor trend as of 9 Jan 2026 (Source: TradingView)

Watch the US$79.86 key short-term pivotal resistance on Silver (XAG/USD). A break below US$74.07 increases the odds of another corrective down leg towards the next intermediate support at US$70.52 (also the 20-day moving average) in the first step.

Key elements to support the bearish bias

- Today’s rally from Thursday, 8 January 2026, low of US$73.84 has taken the form of a minor bearish “Ascending Wedge” configuration, which suggests a potential “dead cat bounce”.

- The hourly Stochastic oscillator has flashed out an impending bearish divergence condition at its overbought region, which implies that the upside momentum of the rebound may be fading.

- The US$79.86 key short-term resistance (potential inflection level to end the rebound) is defined by the pull-back resistance of the former ascending support from 1 January 2026 low and close to the 61.8% Fibonacci retracement of the prior decline from 7 January 2026 high to 8 January 2026 low.

Alternative trend bias (1 to 3 days)

A clearance with an hourly close above US$79.86 key short-term resistance invalidates the bearish tone for a squeeze up to retest the US$84.03 key medium-term pivotal resistance (current all-time high of 29 December 2025).

US-China Relations Take a Hit After Venezuela Raid, PMIs Recover, CNY Strengthening Continues

Geopolitics and tech:

US capture of Maduro adds a new front in US-China rivalry: Much has already been said about the US raid in Venezuela but below are my two cents on the implications for China:

US-China relations: The Trump administration has supposedly told interim leader of Venezuela Delcy Rodriquez to kick out China, Russia, Iran and Cuba to avoid continued blockade of oil sales. However, China who has investments in the Venezuelan oil sector, is unlikely to accept its investment in the country basically being seized by the US. Foreign ministry spokesperson Mao Ning said on Wednesday that "Let me stress that China and other countries have legitimate rights in Venezuela, which must be protected."

It very much looks like the US has opened a new front in the US-China rivalry in its' pursuit of dominating the Western Hemisphere as set out in its National Security Strategy. China has major investments in other Latin American countries as well such as Chile, Peru and Bolivia and rely on access to resources from the region. More than 20 countries in Latin America and Caribbean have signed on to China's Belt and Road Initiative. This sets the stage for new confrontation between the US and China and puts renewed uncertainty over Trump's visit to Beijing in April. For now China is likely to take a wait-and-see stance and see how the Trump administration implements this policy across the region. But they are unlikely to bow to US pressure and stop investing in Latin America and they will aim to protect the investments they have already done.

It is uncertain Latin American countries react. Will they seek more investments from China (to reduce exposure to US) or less investments (out of fear of US response)? Mexico, being under strong pressure from Trump, leans towards the second option with a new 50% tariff on Chinese goods.

China and the Global South: The US raid fits perfect into what China has been saying for years: that US is a hegemon and imperialist willing to use ruthless power, economically and militarily, to hurt countries that don't walk to the beat of US drums. It could [RJ1] galvanize desires across the Global South to become less dependent on US, financially, militarily and technologically. This is a clear positive for China that will provide an alternative in all these areas.

Implications for Taiwan issue: My view on this topic, is that it makes little if any difference to Chinese leaders. China already sees the island as Chinese territory and an invasion would be protecting its' own sovereignty rather than breaching another nation's sovereignty. Hence, from China's point of view it would not be a breach of the UN Charter. Seen from Beijing, they do not need external legitimacy to protect what is already theirs, contrasting it to the US raid which was a clear violation of sovereign territory.

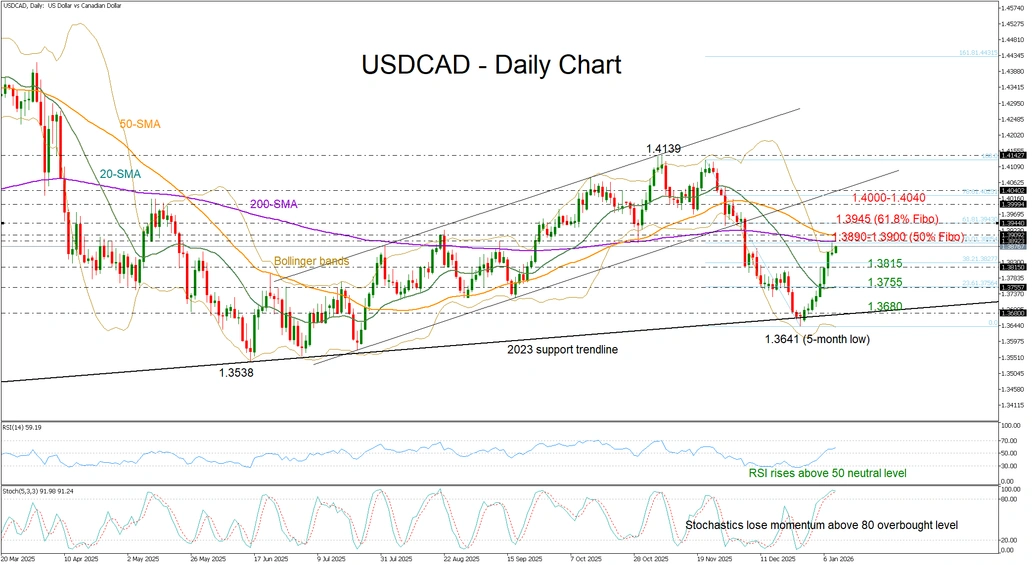

USD/CAD Bulls Gear Down Near 1.3900

- USD/CAD stabilizes ongoing recovery near 1.3900.

- Short-term bias is positive, but bulls may soon lose steam.

USD/CAD extended its post-Christmas rally to a one-month high of 1.3887 on Thursday, retracing half of the November–December decline as the US dollar strengthened and traders reduced exposure to risk-sensitive currencies such as the loonie.

With attention shifting to the US and Canadian jobs data and a possible Supreme Court ruling on Trump’s import tariffs, traders are watching the 1.3890–1.3900 zone, where the 50- and 200-day simple moving averages (SMAs) are converging. A break higher could target the 61.8% Fibonacci level at 1.3945 and potentially the 1.4000 psychological mark, with the broken support trendline at 1.4040 likely coming next on the radar.

However, upside momentum may fade as the stochastic oscillator is leaning to the downside in the overbought territory and the price itself is trading around the upper Bollinger band. Failure to clear 1.3900 could see support tested at 1.3815, with further losses exposing the 20-day SMA at 1.3755. If the latter gives way too, the bears may next head for the crucial 2023 support trendline seen near 1.3680.

Overall, USD/CAD is maintaining a positive short-term bias, though profit-taking may limit gains near the 1.3900 area.

Eurozone retail sales rise 0.2% mom in November, as non-food demand improves

Eurozone retail sales volumes rose 0.2% mom in November, slightly above expectations of 0.1% increase. The improvement was driven primarily by non-food products, where sales increased 0.4% mom, offsetting weakness elsewhere. Sales of food, drinks and tobacco slipped -0.2%, while automotive fuel volumes fell -0.1%.

Across the broader EU, retail sales also rose 0.2% mom, but national divergences were stark. Luxembourg posted a sharp 5.8% surge, followed by Portugal (2.2%) and Denmark (1.9%). Croatia (-2.2%), Belgium (-1.6%) and Slovakia (-1.5%) recorded notable declines.

Full Eurozone retail sales release here.