Sample Category Title

Investors Step Back From US Assets Ahead of Data Flood

Last week delivered what should have been a moment of relief for global markets: the US finally ended its historic government shutdown, clearing the way for normal economic data flow to resume. Yet instead of sparking a rally, the reopening brought little comfort.

U.S. assets struggled across the board. Equities came under pressure as investors reassessed the risks around Fed policy direction and stretched valuations in key growth sectors. Yields moved higher but offered no support to Dollar, which weakened broadly despite fading expectations of near-term Fed easing. Even the traditional safe-haven flows that typically favor the greenback failed to materialize in a meaningful way.

Currency markets delivered their own twist. Yen, often the first beneficiary of a risk-off wave, ended the week as the worst performer as traders pushed out expectations for a BoJ rate hike. Sterling suffered as well, pressured by weak economic data and growing conviction that the BoE would cut rates in December.

By contrast, Swiss Franc surged on a mix of safe-haven demand and positive trade developments. Australian and New Zealand Dollars found some early support but struggled to extend gains as sentiment darkened. Euro and Canadian Dollar sat in the middle of the pack.

Is ‘Sell America’ Returning, or Just a Pause Before the Data Storm?

The past week delivered an unusual alignment across U.S. assets: stocks, Treasuries, and Dollar all came under pressure at the same time. That pattern immediately drew comparisons to April, when markets reacted violently to President Donald Trump’s “Liberation Day” announcement, triggering the now-famous “Sell America” trade. While last week’s moves were nowhere near that magnitude, the directional similarity was difficult to ignore.

Still, calling it a revival of the same theme may be premature. Market positioning seems far more cautious than actively bearish. The historic government shutdown kept investors blind to key economic signals for weeks. With the data blackout now lifted, traders appear reluctant to make big commitments until a clearer macro picture emerges. The pullback in U.S. assets may simply reflect a desire to step aside before the next wave of information hits.

The coming week could prove decisive. With the government now reopened, the pipeline of U.S. economic releases is about to restart — and after several weeks of silence, the impact could be amplified. Volatility, which has softened noticeably during the shutdown, is likely to climb as markets digest a heavy flow of indicators that will reset expectations for both growth and inflation.

What those data reveal will determine whether last week’s moves were a temporary misalignment or the early stages of a more structural shift. A resilient economy with stable job growth could revive confidence in U.S. assets. A deteriorating backdrop could force a deeper repricing. Anything in between would keep traders directionally cautious but tactically reactive.

For now, the only certainty is uncertainty itself. Markets briefly lost their footing last week, and the synchronized weakness across U.S. stocks, bonds, and Dollar has raised legitimate questions about investor conviction. Whether that hesitation evolves into a broader “Sell America” theme could depend entirely on what the long-delayed data now reveal.

Fed Cut Odds Crumble, Yields Rebound

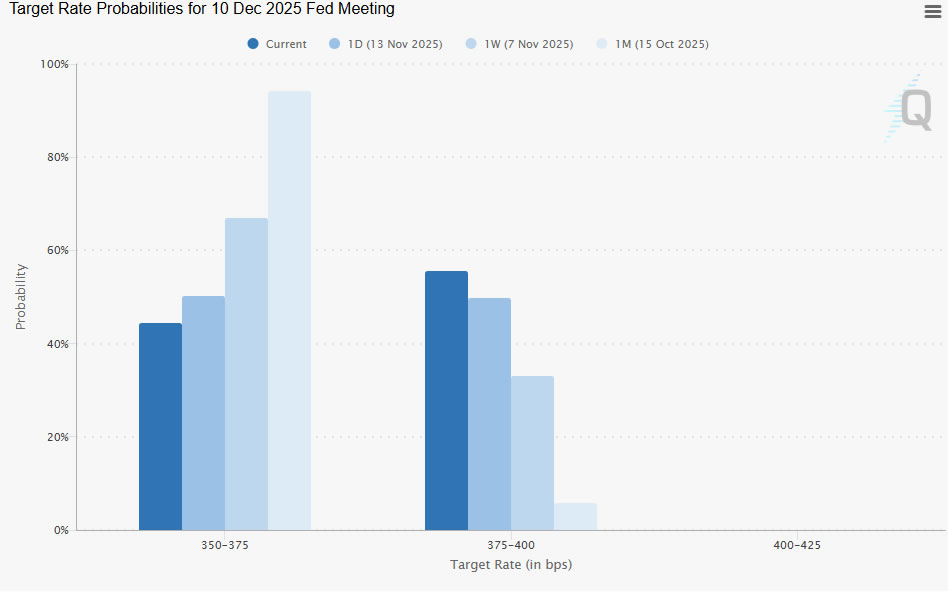

Expectations for a December Fed rate cut shifted sharply last week after a set of remarks from FOMC officials signaled that easing is far from guaranteed. What had looked like a near-certainty just a month ago is now a coin toss: market odds for a December cut have fallen to 44.4%, down from 66.9% a week earlier and 94.2% a month ago.

Some economists reinforced that view by noting that GDP prior to the shutdown was tracking at 3.5% to 4%, a pace more consistent with overheating than with urgency for additional stimulus. Financial conditions also remain unusually easy, leaving little justification for further policy accommodation. Lowering funding costs for banks at this stage risks could do more harm than good by reigniting price pressures just as progress toward 2% inflation remains uneven.

The repricing in expectations helped drive a meaningful move in Treasuries. 10-year yield jumped sharply on Friday, closing at 4.148. But for now, the rebound from 3.947 short term bottom is still viewed as a corrective move within the broader decline from 4.629.

Technically, resistance near 4.200 should form a formidable cap, with 4.205 support turned resistance and 38.2% retracement of 4.629 to 3.947 at 4.207. Break of 4.056 support will suggest that the corrective bounce has completed, and bring retest of 3.947 low.

However, decisive break above 4.200 would suggest the decline from 4.629 has run its course, and open way to 61.8% retracement at 4.368.

Tech Jitters Persist, But Dip Buyers Defend Key Support

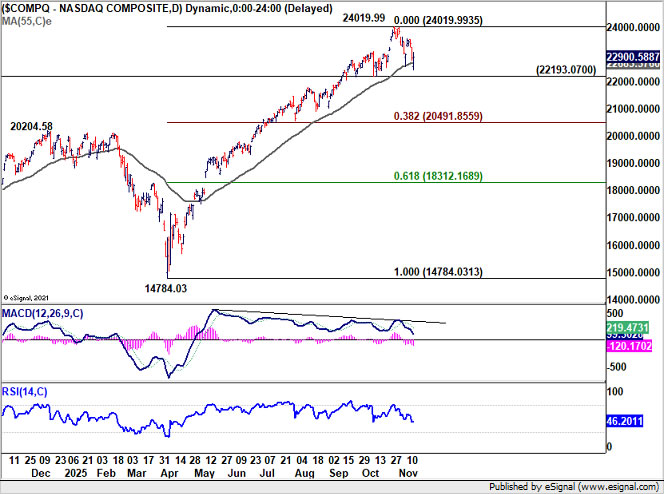

US equities spent latter part of last week struggling under the weight of shifting Fed expectations and the re-emergence of AI valuation concerns. Yet, just as in the prior week, buyers stepped in late on Friday, hinting that dip-buying appetite has not fully disappeared. NASDAQ closed at 22,900.58 after plunging to 22,436.79, a notable recovery given the earlier capitulation.

Technically, NASDAQ is still holding the line where it matters most. It remains above its 55 Day EMA (now at 22,683.37), and more importantly, above key structural support at 22,193.07. As long as these levels hold, the broader uptrend remains intact, and the path toward a fresh record high stays open.

However, D MACD continues to show bearish divergence, which adds uncertainty about the strength of the underlying trend. Decisive break of 22,193.07 will argue that it's at least correcting the rise from 14,784.03. In this case, deeper fall would be seen back to 38.2% retracement of 14,784.03 to 24,019.99 at 20,491.85.

DOW surged to a new record high of 48,435.57 mid-week, only to reverse sharply and finish at 47,147.48. Nevertheless, the broader technical picture remains bullish while support at 46,495.62 intact. Firm break of 61.8% projection of 36,611.78 to 44,885.83 from 43,340.68 will pave the way to 50k psychological level, and possibly further to 100% projection at 51,614.73.

Still, D MACD is showing bearish divergence condition, hinting that upward momentum is waning. Firm break of 46,495.62 support would confirm that a deeper correction is underway, sending the index back toward 44,885.83 resistance turned support.

Dollar Struggles Despite Shift in Fed Pricing

Dollar Index gyrated lower last week, failing to draw support from fading expectations of a December Fed rate cut, firmer Treasury yields, or the mild risk aversion that built into the Friday close.

Technically, with 98.56 support still intact, corrective rise from 96.21 short-term bottom remains in play. But any further upside should meet heavy resistance at 38.2% retracement of 110.17 to 96.21 at 101.54. On the downside, firm break of 98.56 would indicate that the bounce has already run its course, setting up a retest of the 96.21 low.

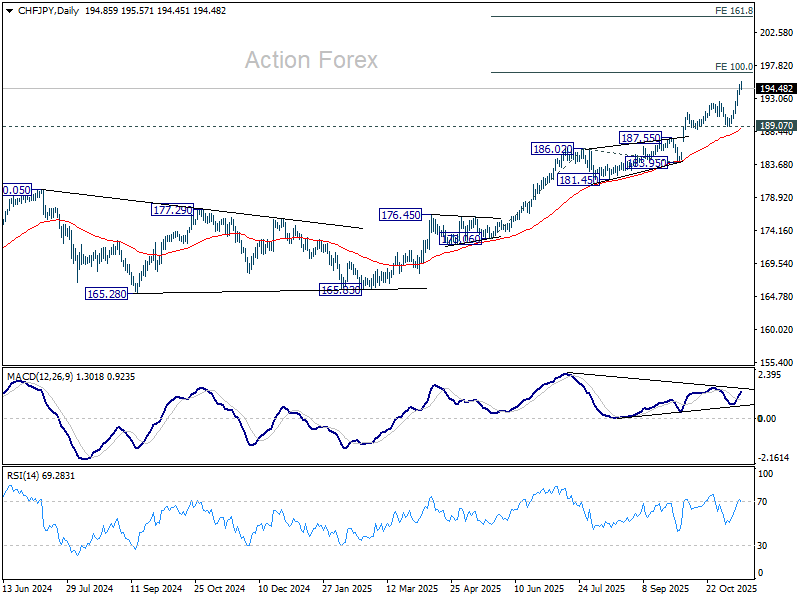

CHF/JPY Blasts to New Record

CHF/JPY exploded to new record highs last week, extending its already-impressive rally. The cross gained 2.11% and holds the number one position in the Top Movers chart.

Half of the move was driven by Swiss Franc strength as Switzerland and the U.S. reached a near-final framework to reduce tariffs on Swiss imports from 39% to 15%. This immediately leveled Switzerland with the EU’s trade treatment. Part of the also agreement includes a substantial Swiss pledge: USD 200B in investment into the U.S. by 2028, focused on pharmaceuticals, medical devices, aerospace and gold production.

Around 40% of Switzerland’s exports will benefit directly from the lower tariff regime. Officials said implementation could occur within “days, weeks,” once U.S. customs systems are updated.

Another half of the move was extended Yen weakness. The Japanese currency was weighed down broadly by increasingly explicit political pressure on the BoJ to delay rate hikes. Prime Minister Sanae Takaichi emphasized to parliament that Japan’s current inflation is driven primarily by food prices — the wrong kind of inflation — and warned of renewed deflation risks if monetary policy is tightened prematurely.

Economic Revitalization Minister Minoru Kiuchi captured the logic succinctly. Although the government watches Yen movements closely, he noted that Yen-based import prices have fallen for eight consecutive months, blunting the pass-through of currency weakness. Data later confirmed a ninth negative reading at -1.5% yoy. As long as Yen's decline remains measured and orderly, Tokyo is clearly willing to tolerate further weakness. Growth from monetary policy support clearly takes priority over currency strength.

Against that backdrop, CHF/JPY uptrend has powerful fundamental backing. Technically, the immediate focus is 100% projection of 173.06 to 186.02 from 183.95 at 196.91, where resistance could emerge due to bearish divergence condition in D MACD. But in any case, outlook will stay bullish as long as 189.07 support holds. Decisive break of 196.91 could invalidate the bearish divergence and unlock 161.8% projection at 204.91 as the next target.

EUR/USD Weekly Outlook

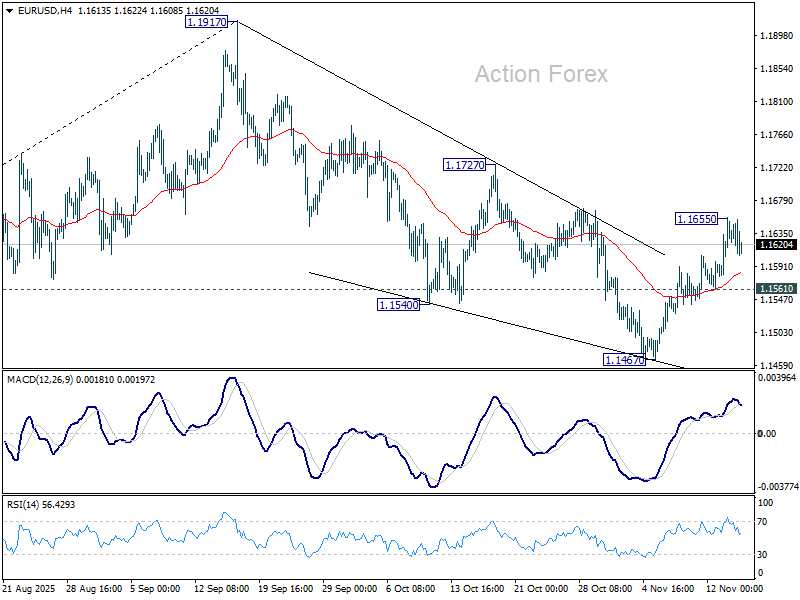

EUR/USD's rebound from 1.1467 extended higher last week retreated after hitting 1.1655. Initial bias is turned neutral this week first. Fall from 1.1917 might have completed as a three wave correction at 1.1467. Above 1.1655 will target 1.1727 resistance first. Firm break there will solidify this bullish case and bring retest of 1.1917 high. However, break of 1.1561 will revive near term bearishness and target 1.1467 low instead.

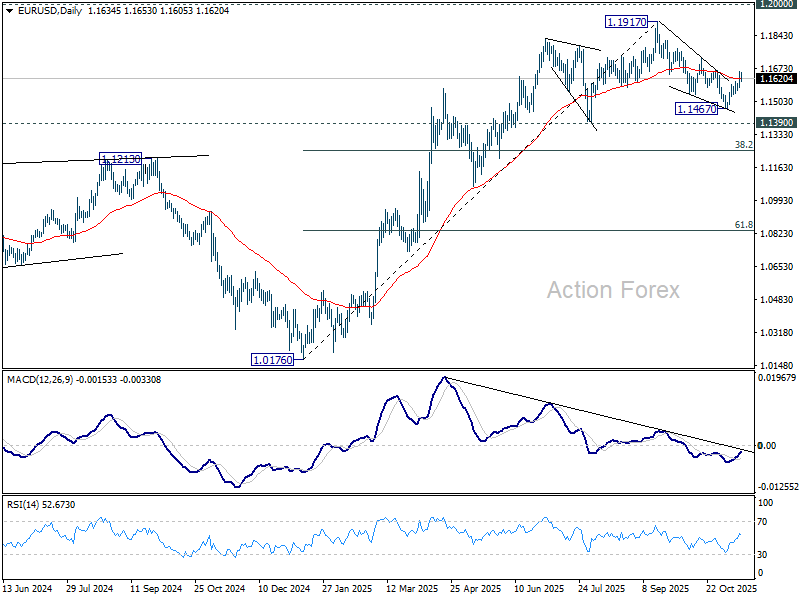

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1306) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

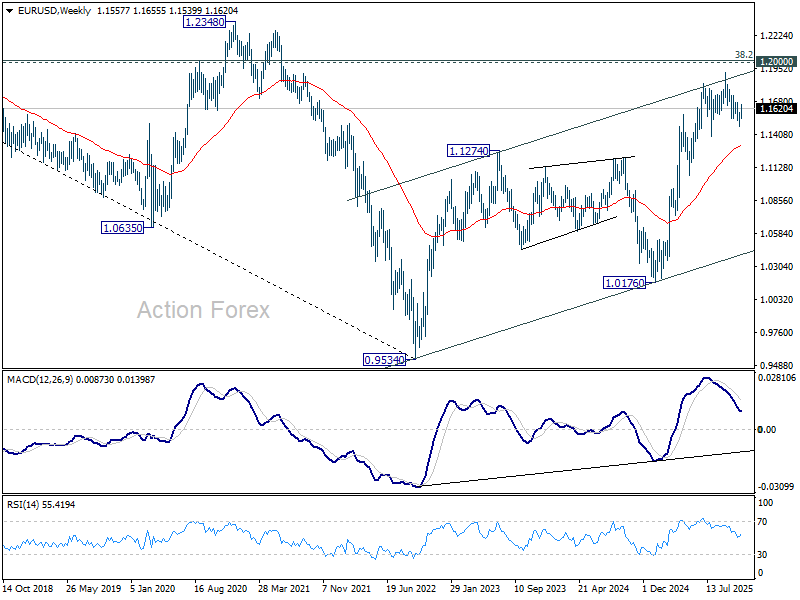

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

EUR/USD Weekly Outlook

EUR/USD's rebound from 1.1467 extended higher last week retreated after hitting 1.1655. Initial bias is turned neutral this week first. Fall from 1.1917 might have completed as a three wave correction at 1.1467. Above 1.1655 will target 1.1727 resistance first. Firm break there will solidify this bullish case and bring retest of 1.1917 high. However, break of 1.1561 will revive near term bearishness and target 1.1467 low instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1306) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

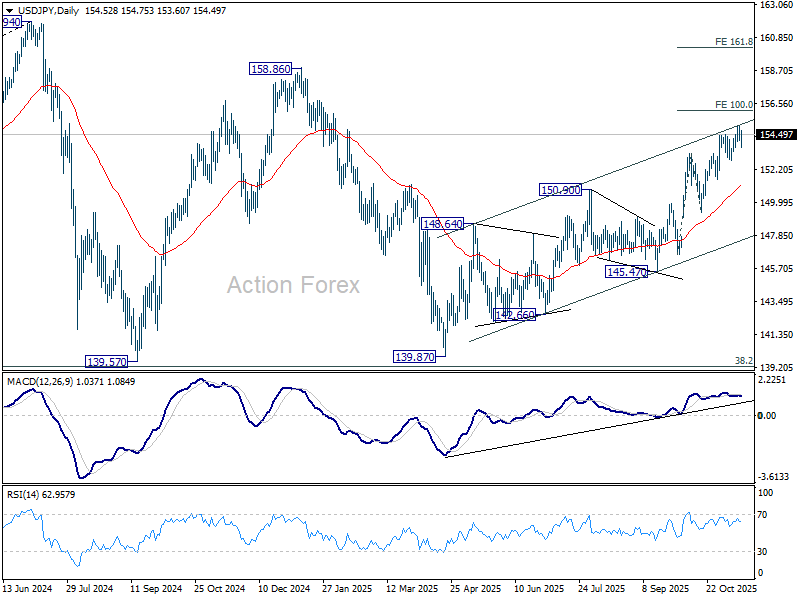

USD/JPY Weekly Outlook

USD/JPY edged higher again last week as rise from 139.87 extended, but retreated after hitting 155.03. Initial bias remains neutral this week first. On the upside, break of 155.03 will target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, considering bearish divergence condition in 4H MACD, firm break of 152.81 support will indicate short term topping, and bring deeper pullback to 55 D EMA (now at 151.05).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

In the long term picture, there is no sign that up trend from 75.56 (2011 low) has completed. But then, firm break of 161.94 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

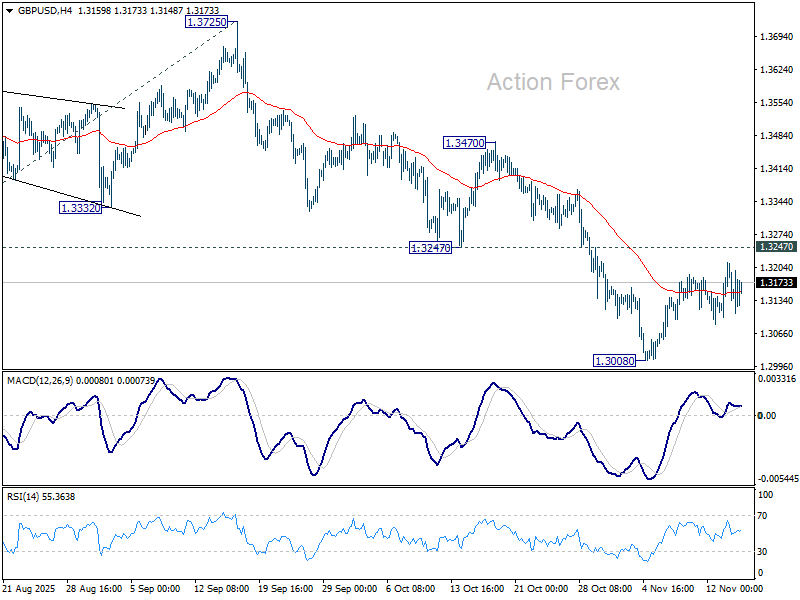

GBP/USD Weekly Outlook

GBP/USD stayed in consolidations above 1.3008 last week and outlook is unchanged. Further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will resume the fall from 1.3787, and target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831). Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

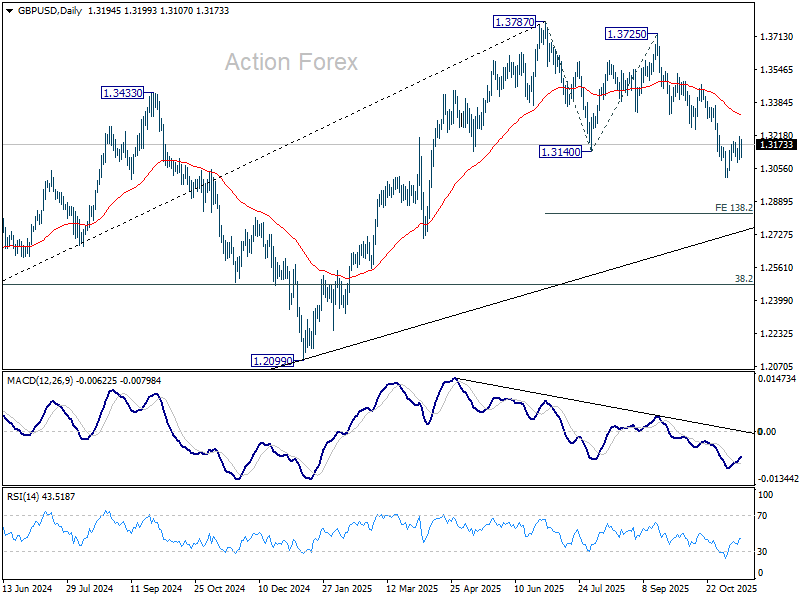

In the bigger picture, the break of 55 W EMA (now at 1.3185) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2824) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

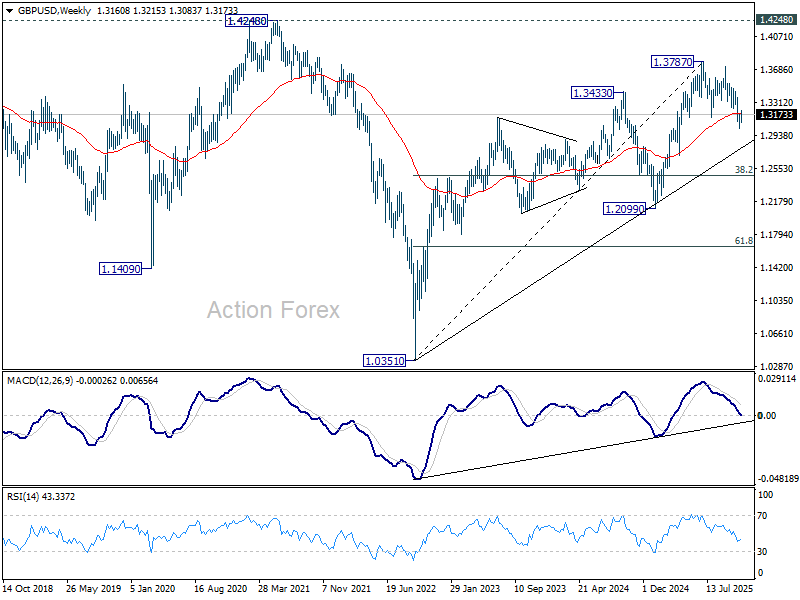

In the long term picture, as long as 1.4248/4480 resistance holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.3051 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

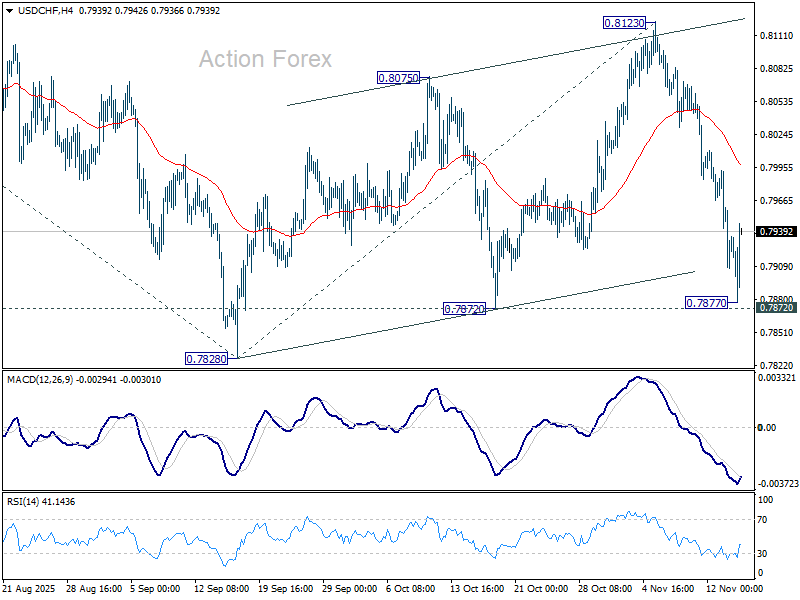

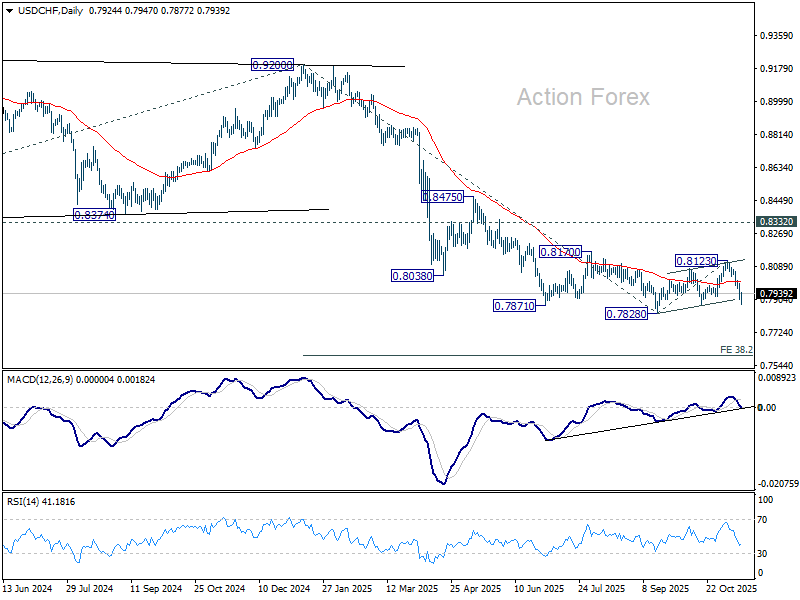

USD/CHF Weekly Outlook

USD/CHF's fall from 0.8123 accelerated to as low as 0.7877 last week but recovered ahead of 0.7872 support. Initial bias is turned neutral this week first. Current development suggests that corrective rebound from 0.7828 has completed with three waves up to 0.8123. Break of 0.7872 support will pave the way through 0.7828 to resume the larger down trend. Next near term target is 38.2% projection of 0.9200 to 0.7828 from 0.8123 at 0.7599. However, sustained break of 55 4H EMA (now at 0.7997) will mix up the outlook.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

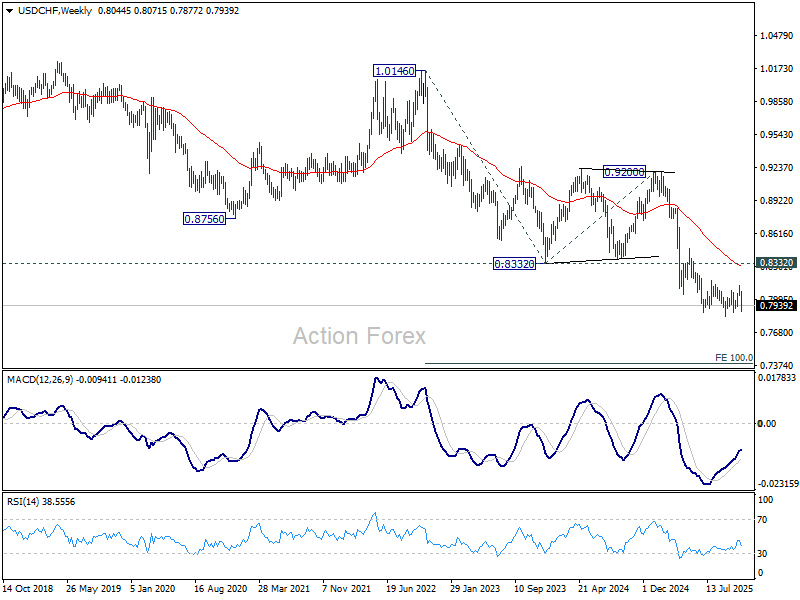

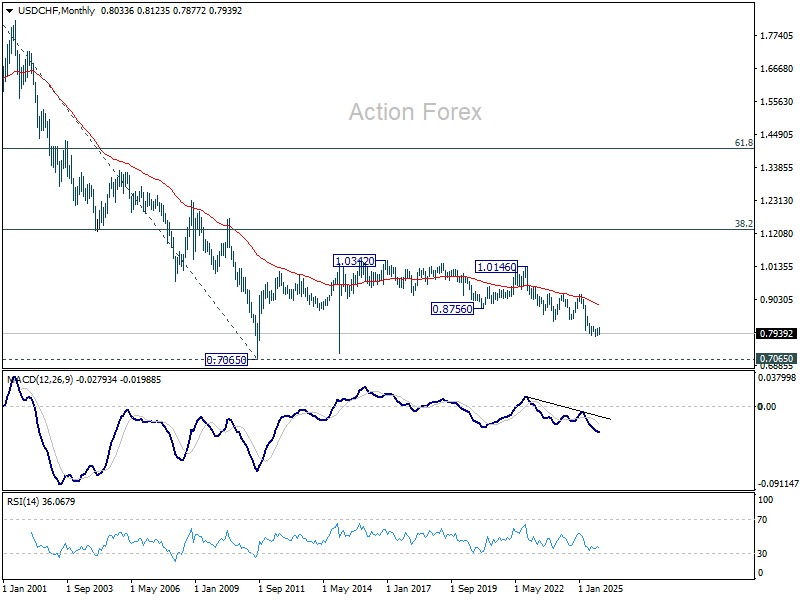

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

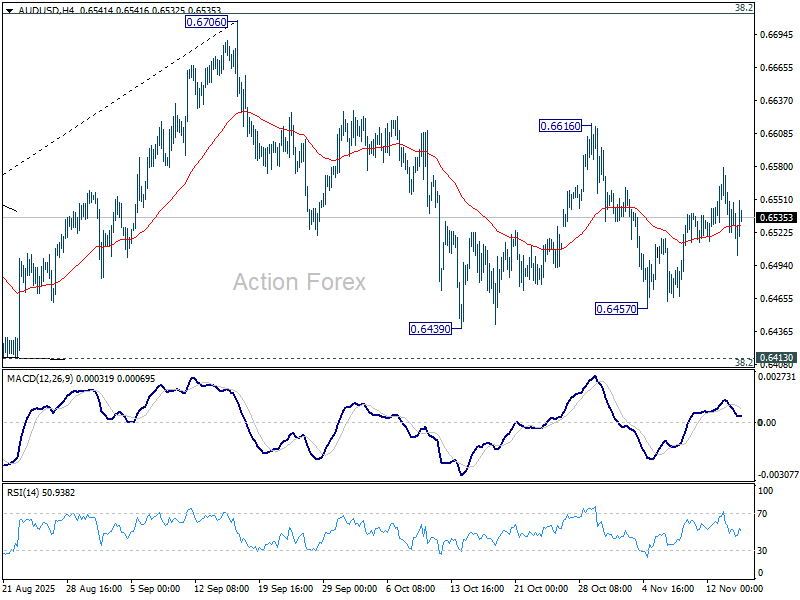

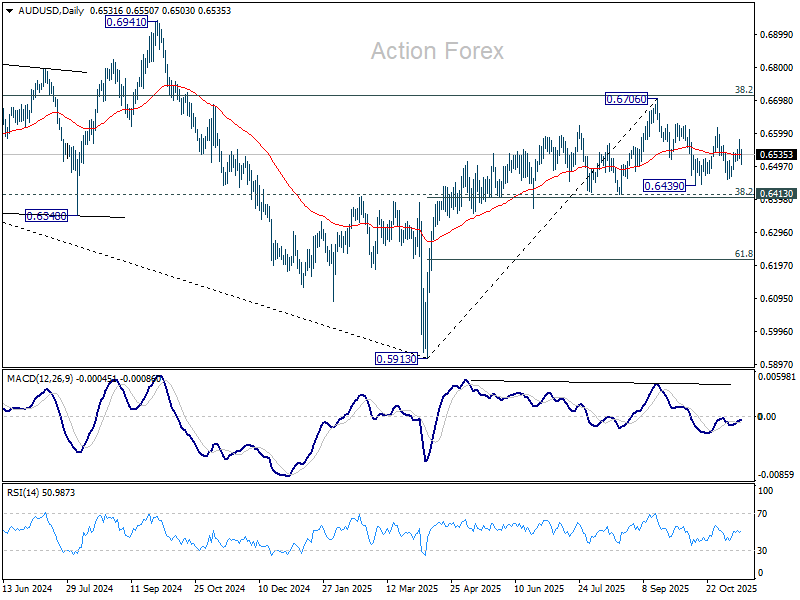

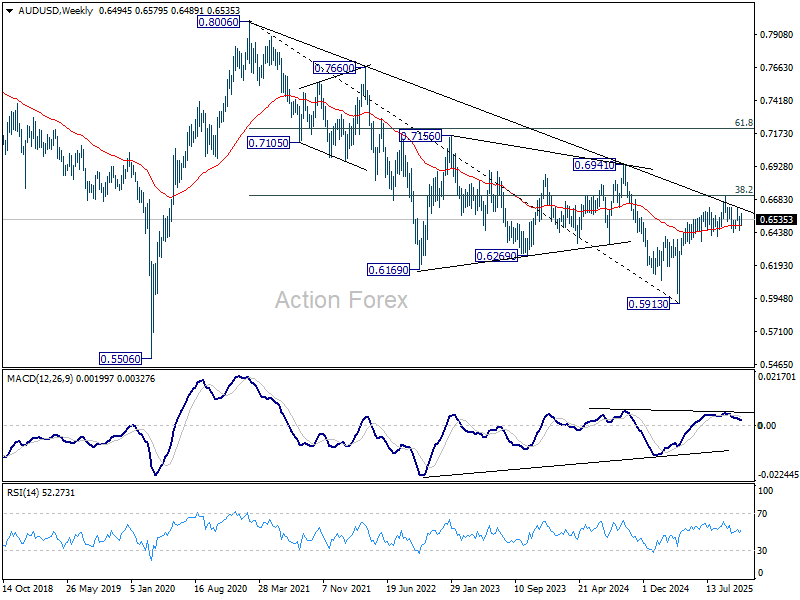

AUD/USD Weekly Report

AUD/USD stayed in range of 0.6457/6616 last week and outlook is unchanged. Initial bias stays neutral this week first. On the downside, break of 0.6457 will target 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403). Decisive break there will carry larger bearish implications. On the upside, break of 0.6616 will bring retest of 0.6706 high instead.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

In the long term picture, fall from 0.8006 is seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal. On the upside, firm break of 0.6941 will argue that the third leg has already started back to 0.8006.

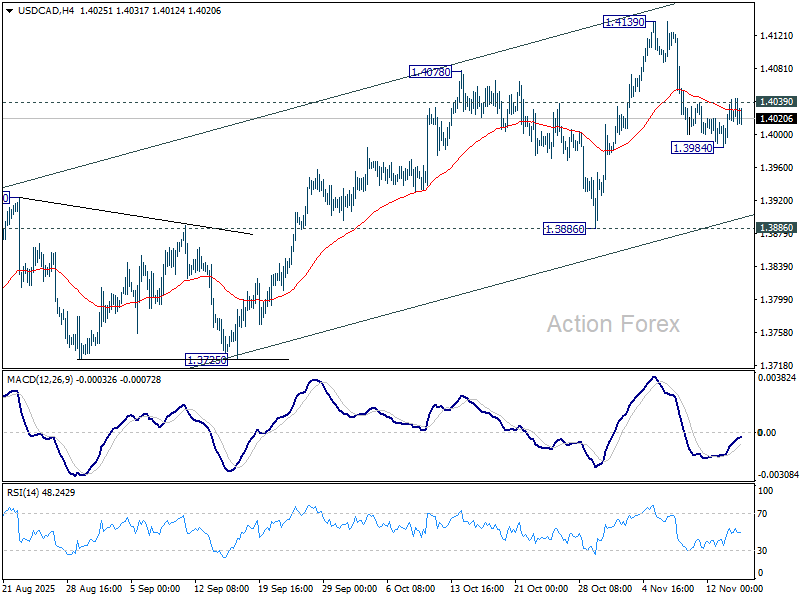

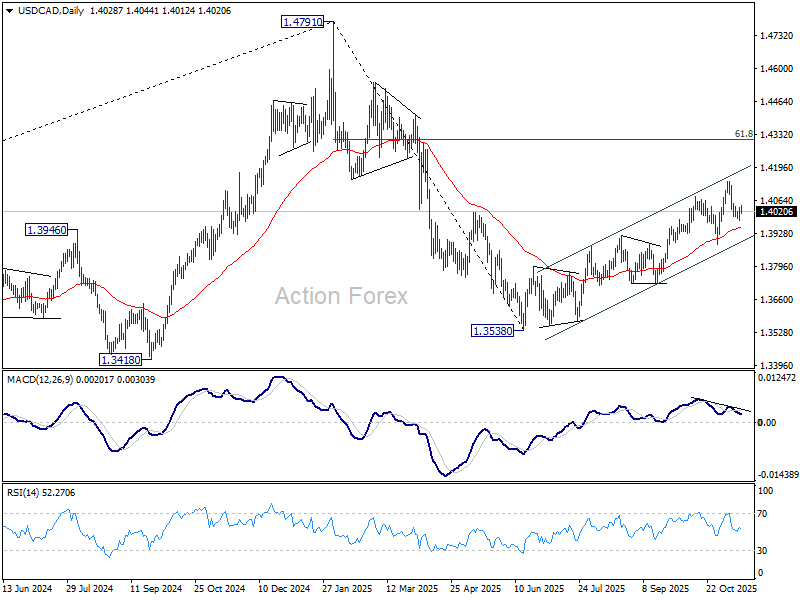

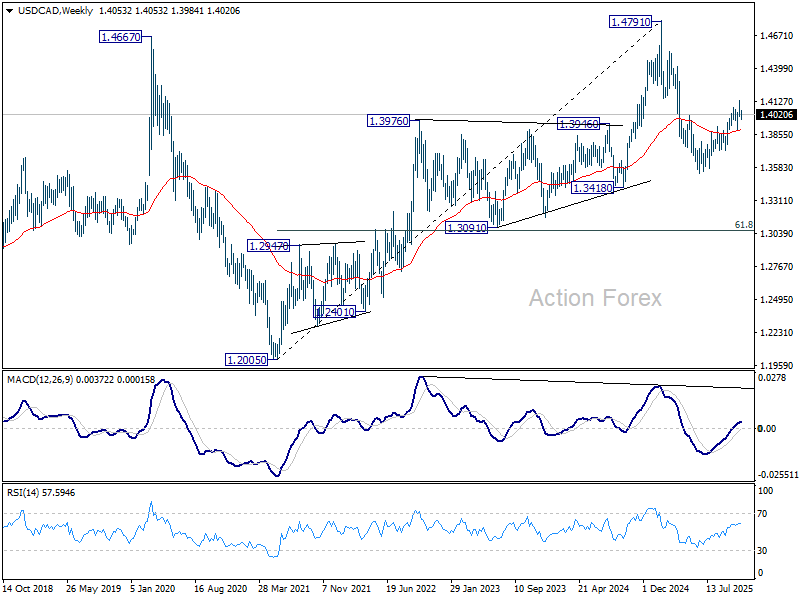

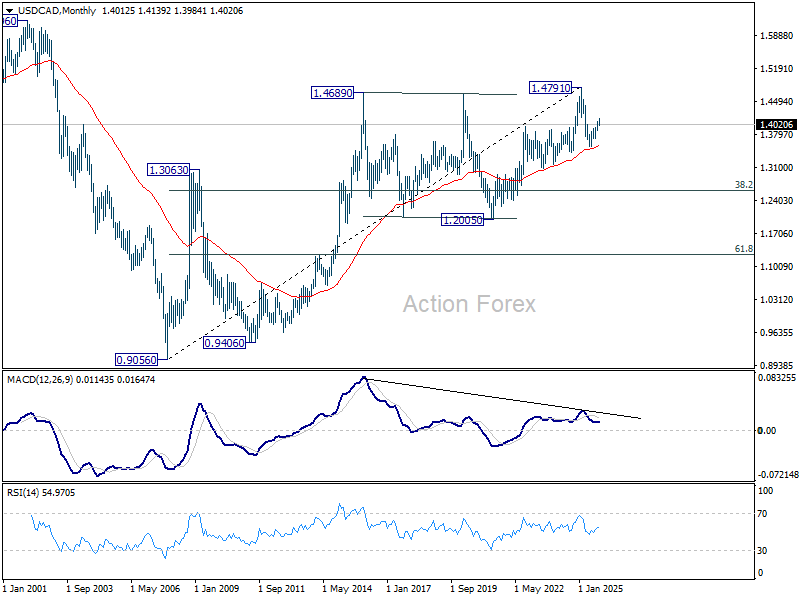

USD/CAD Weekly Outlook

USD/CAD's pullback from 1.4139 short term top extended lower to 1.3984 last week and recovered. Initial bias remains neutral this week first. Firm break of 1.4039 minor resistance will bring stronger rebound to retest 1.4139 high. On the downside, below 1.3984 will target 1.3886 support next. Overall, rise from 1.3538 is in favor to continue as long as 1.3886 support holds.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

In the long term picture, rising 55 M EMA (now at 1.3543) remains intact. Thus, up trend from 0.90567 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction.

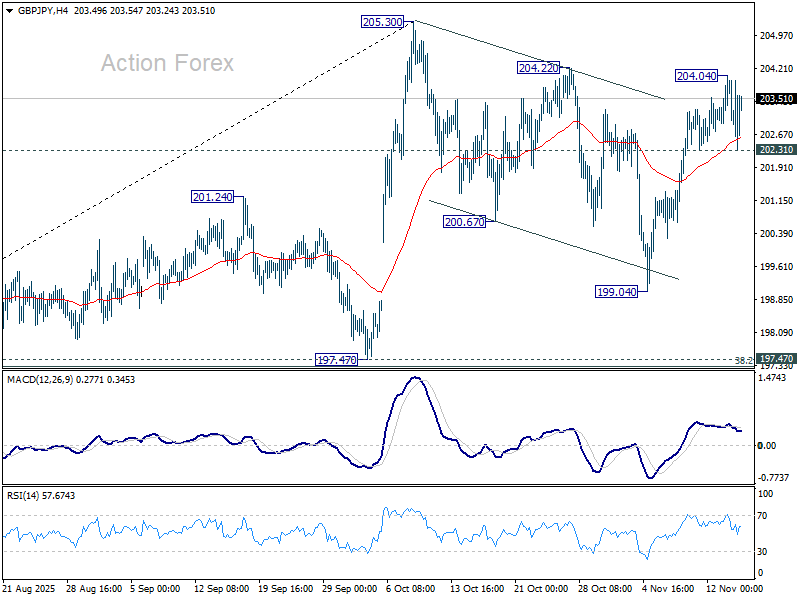

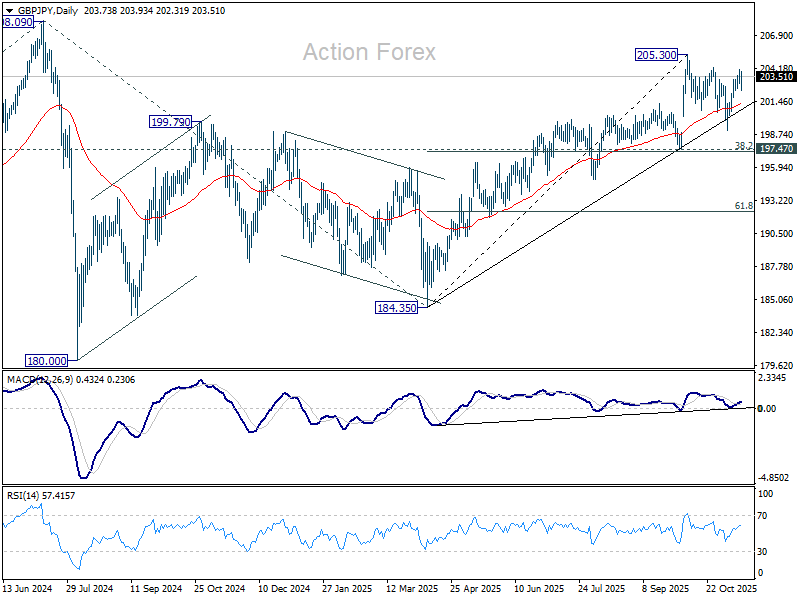

GBP/JPY Weekly Outlook

GBP/JPY roses strongly to 204.04 last week but failed to break through 204.22 resistance and retreated. Initial bias remains neutral this week first. On the upside, firm break of 204.22 will suggest that larger rally from 184.53 is ready to resume through 205.03. However, break of 202.31 minor support will turn bias to the downside towards 199.04, to extend the corrective pattern from 205.30 with another falling leg.

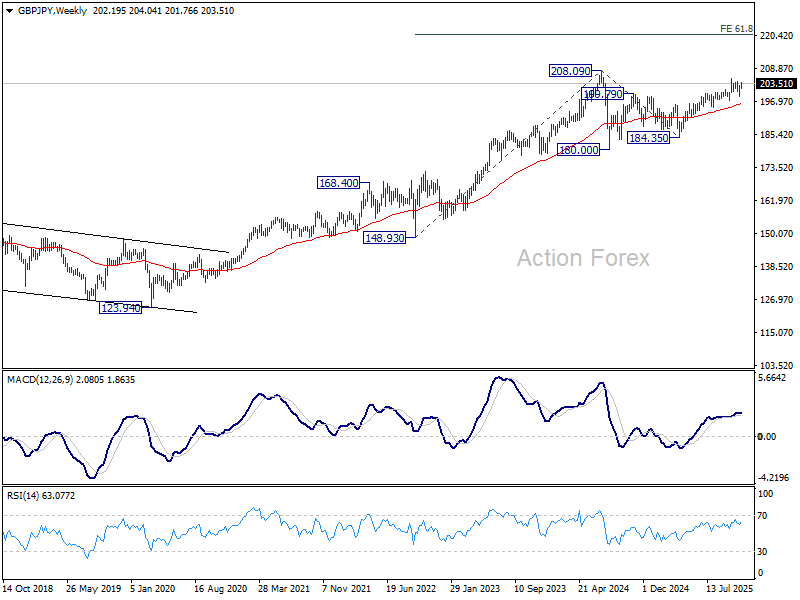

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

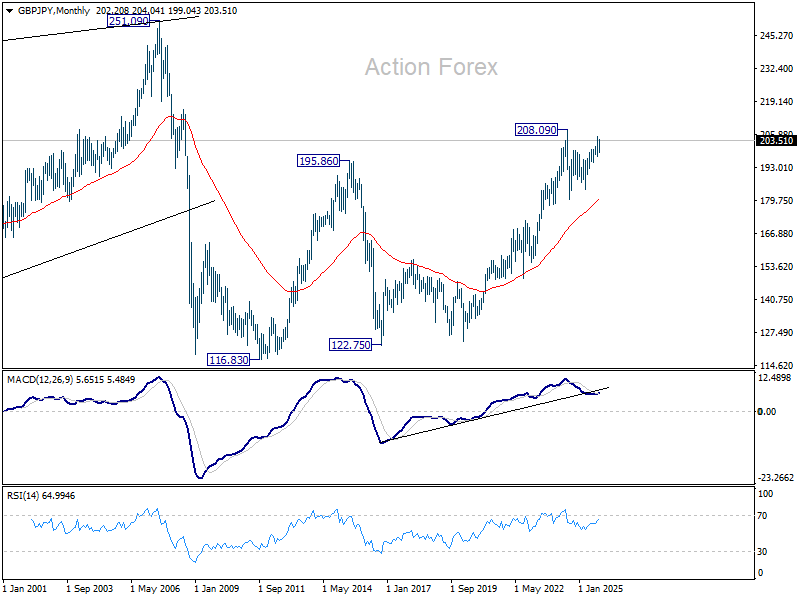

In the long term picture, there is no sign that the long term up trend from 122.75 (2016 low) has concluded. But firm break of 208.09 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

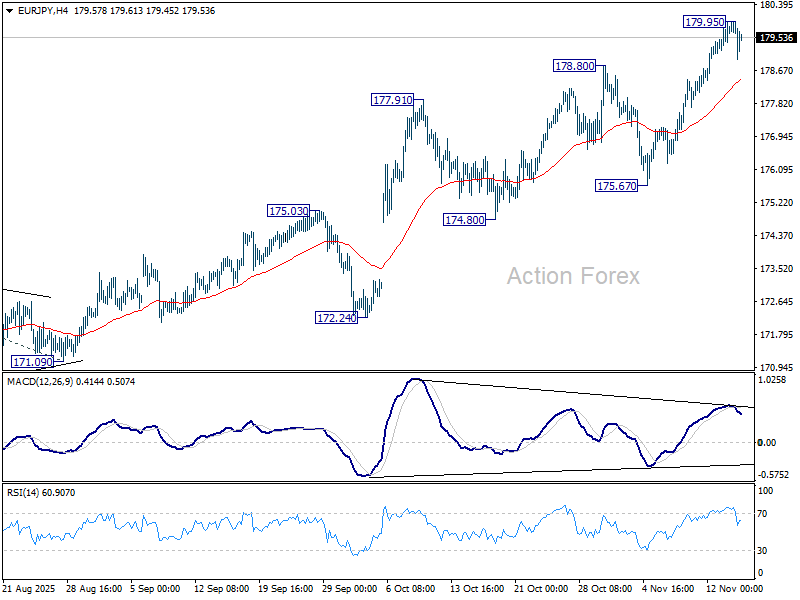

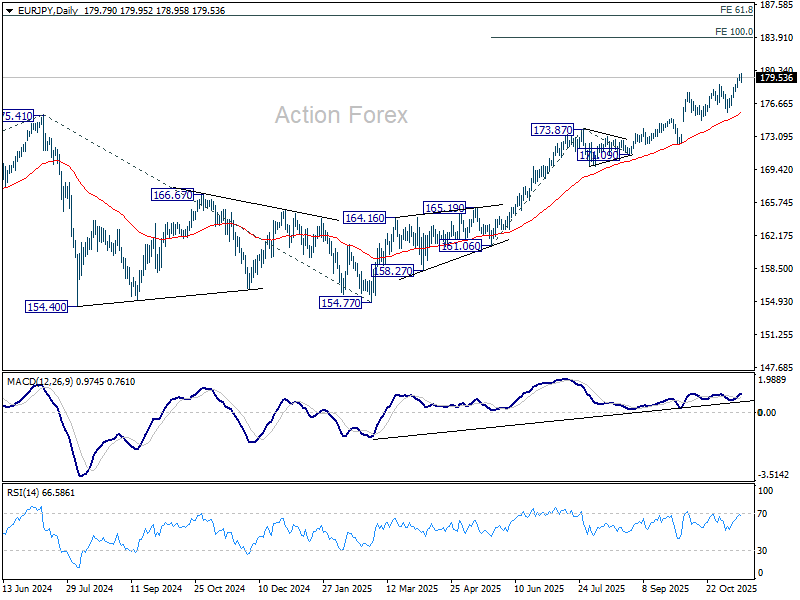

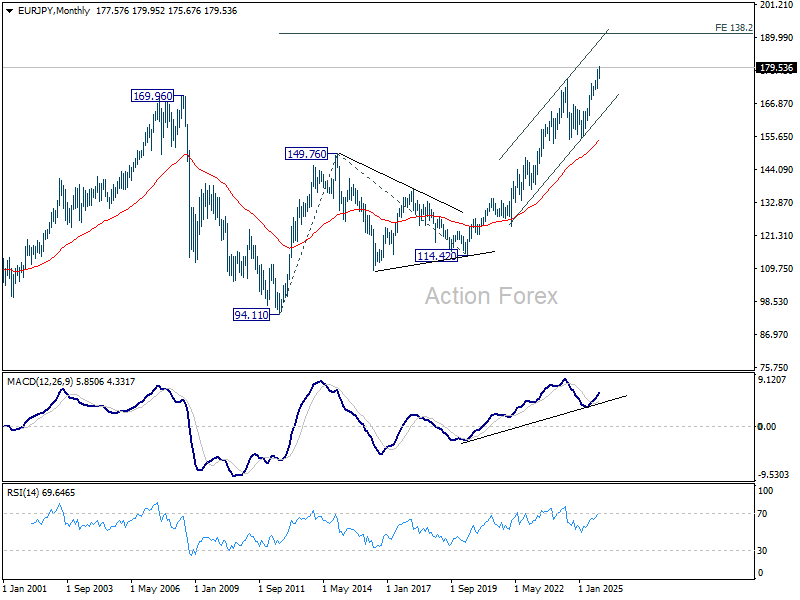

EUR/JPY Weekly Outlook

EUR/JPY's up trend resumed last week but lost momentum after hitting 179.95. Initial bias is turned neutral this week for consolidations. Downside of retreat should be contained well above 175.67 support. On the upside, break of 179.95 will target 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 168.61) holds, even in case of deep pullback.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

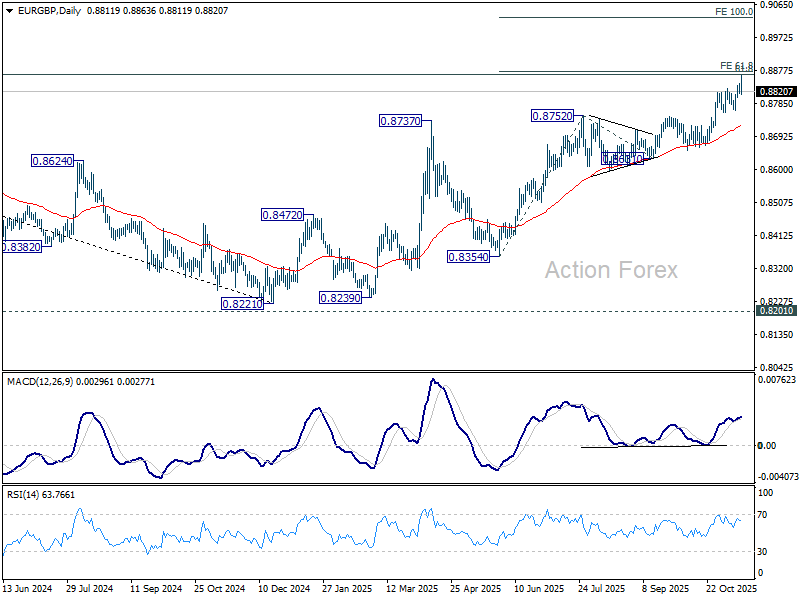

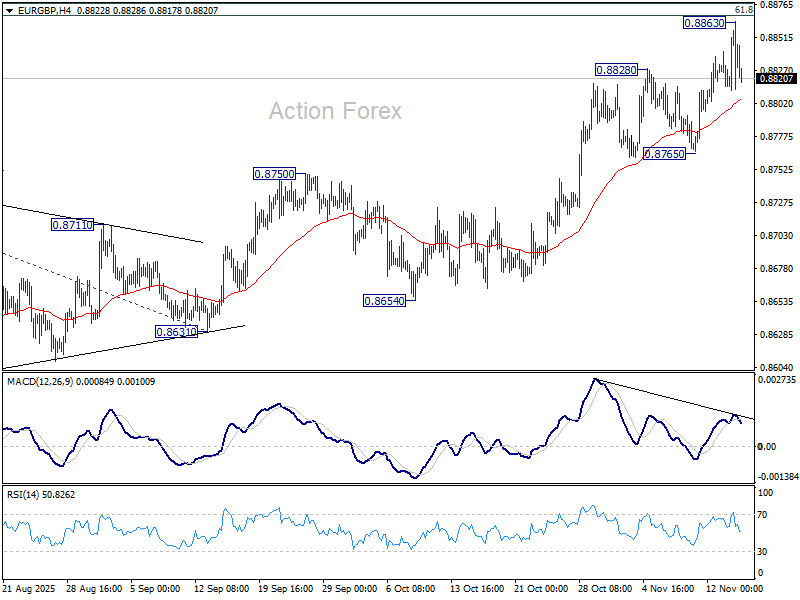

EUR/GBP Weekly Outlook

EUR/GBP's rally resumed to 0.8663 last week but retreated since then. Initial bias is turned neutral this week first. Considering bearish divergence condition in 4H MACD, firm break of 0.8765 support will confirm short term topping. Deeper fall should then be seen back to 55 D EMA (now at 0.8725) even still as a correction. On the upside, however, sustained trading above 0.8867 fibonacci level will carry larger bullish implications. Next near term target will be 100% projection of 0.8354 to 0.8752 from 0.8631 at 0.9029.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8571) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.