Sample Category Title

Silver XAG/USD Rockets to Fresh 14-Year Highs on Dovish Fed and Robust Fundamental Outlook

As I sit down to pen this article, I’m met with a feeling of déjà vu.

The difference is that I have actually been here before, many times in the last few months, in fact, with silver seemingly hitting new highs every time I check my charts.

Naturally, this time is no different, with silver rocketing to new highs in yesterday’s trading, while handsomely outperforming its yellow counterpart, gold, in the last seven days.

As is almost tradition by now, let’s discuss some of the fundamentals responsible for the recent moves in precious metal pricing.

Silver (XAG/USD), OANDA, TradingView,23/09/2025

Dust settles on dovish Fed, boosting silver prices

Let’s start by establishing a fundamental economic concept: in a total vacuum, lower interest rates benefit non-yielding assets like silver, since the opportunity cost for holding precious metals compared to cash is reduced.

So, why did the recent Federal Reserve rate cut hurt silver pricing?

The devil is, of course, in the details.

Naturally, nothing in the market is black and white; in this case, Fed Chair Jerome Powell described the cut as a ‘risk-management’ cut rather than a response to a weakening economy.

This would be a much more hawkish stance than previously thought, which, at least at first, would seriously temper expectations that this would mark the first cut of a deep-cutting cycle.

Considering the predicted trajectory of Fed interest rates before this, generally pegged at two further cuts before year-end, even the slightest suggestion that rates could be kept higher not only weakened demand for precious metals, but also simultaneously strengthened the dollar.

What’s happened since then, however, is a textbook example of reaction versus response.

Silver (XAG/USD) & DXY, OANDA & TVC, TradingView, 23/09/2025

Having had time to digest, it would seem that the market uncertainty has all but dissipated, with the recent rally in silver pricing a shining example.

While Powell’s recent ‘risk-management’ comments can’t be ignored, against the backdrop of recent US labour and GDP data, the numbers otherwise point to further rate cuts, assuming inflation remains under control.

While it would be fair to say that the financial markets’ collective hive mind is not always known for robust decision-making in light of shock economic news, the dust has now settled, with the narrative around Fed monetary policy returning essentially to the dovish angle held ahead of the recent decision.

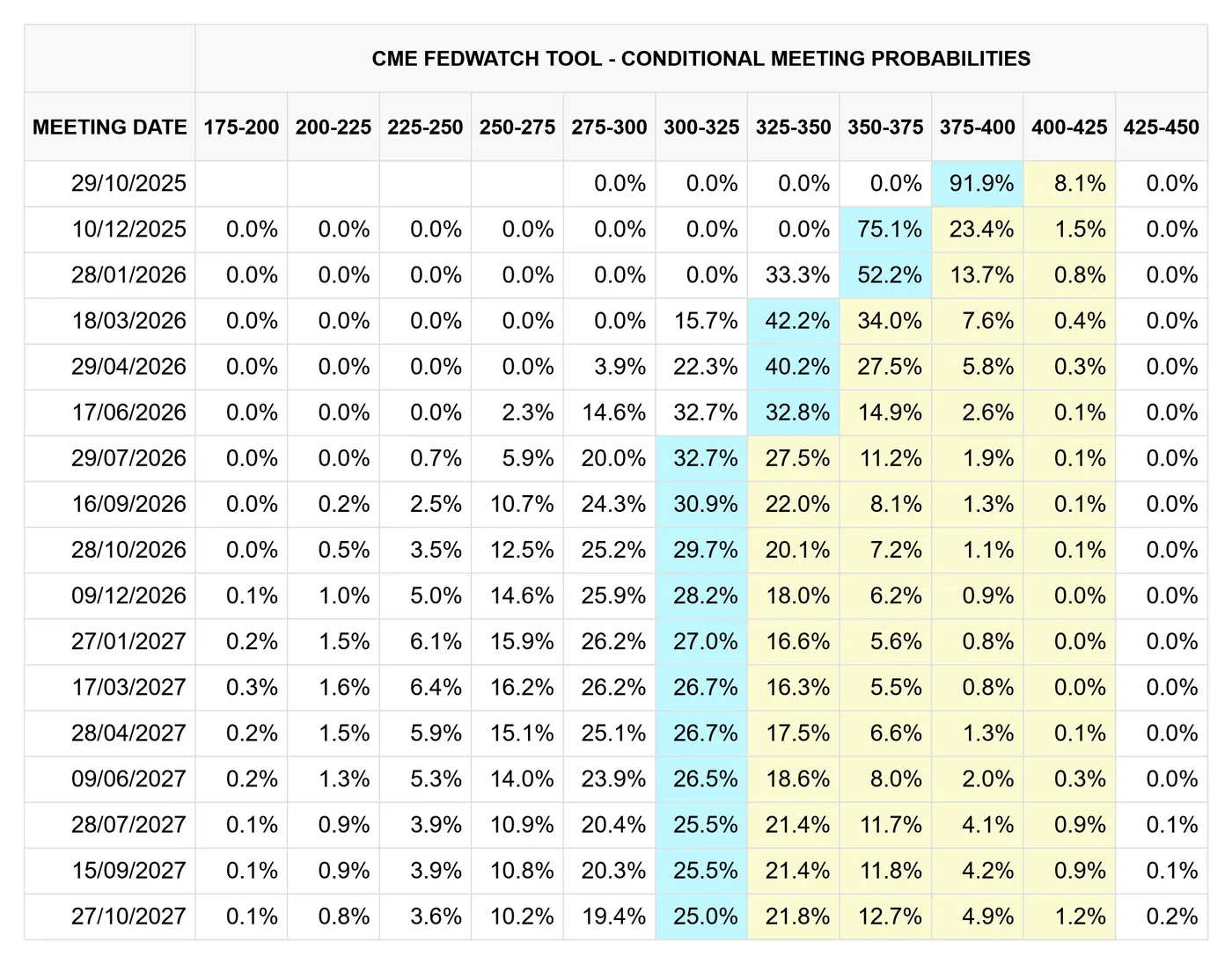

CME FedWatch, OANDA, TradingView, 23/09/2025

This goes double when considering dissent from FOMC member Stephen Miran, who voted for a more aggressive 50 basis point cut in the most recent decision, showing some support for further rate cuts already exists amongst decision-makers.

Strong fundamentals bolster silver prices

At risk of repeating myself from previous coverage, here’s a quick-fire round on the macro themes responsible for the current rally:

- Questions remain on sovereign debt, especially in United States, with the recent downgrade in credit rating fresh in the collective memory. Similar to 2011, uncertainty on the long-term solvency of major world economies, especially with no shortage of radical US policy changes, directly benefits silver pricing

- Silver demand continues to outstrip supply, which in and of itself is a relatively new phenomenon. Used both as a store of value and across industry alike, the recent classification of silver as a ‘critical mineral’ by the US Government further cements its use case on a significant scale. In line with the most basic principles of economic theory, if demand cannot be met by supply, prices rise, as seen particularly of recent

- Usually lumped under the moniker of ‘safe-haven flows’, precious metals like silver are often used as a reliable store of value in times of economic uncertainty. In 2025, there has been no shortage in demand for safe-haven assets, with increased geopolitical tensions, questions on sovereign debt, and, of course, US trade tariffs, all making valuable contributions

- Less so a macroeconomic factor, more so a consequence of the above, a weakening dollar has helped extend the current rally in precious metal pricing, since precious metals are typically priced in USD. So far, 2025 remains on record as one of the U.S. dollar’s worst-performing years in some time, helping boost silver prices

In a nutshell, and owing to the rock-solid fundamentals, markets have clearly shown their preference for higher silver pricing this year, with current prices on pace for their best percentage performance since 2010.

Since late August, it would appear that markets are ready to metaphorically bite the hand off any opportunity to push precious metals higher, with no obvious signs of slowing down any time soon.

Silver XAG/USD: Technical Analysis 23/09/2025

Silver (XAG/USD), OANDA, TradingView, 23/09/2025

- Renewing multi-year highs recently, XAG/USD currently trades toward the upper boundary of the upwards channel. Price may need to retrace lower before an attempt higher, with bulls likely to target $45 first, then onto $45.69

- According to the ADX, current trend strength is at its highest level since June 2024, suggesting conviction in market direction. For the contrarians, shorts should be approached with extreme caution

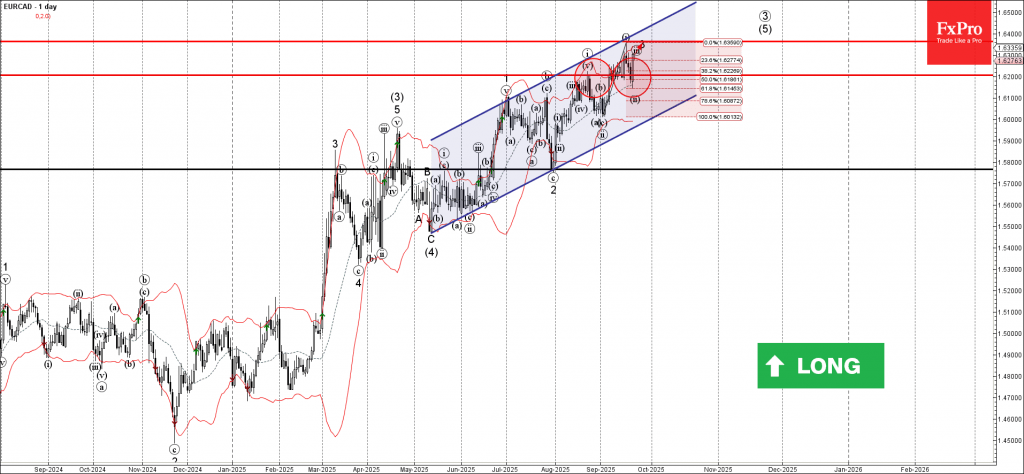

EURCAD Wave Analysis

EURCAD: ⬆️ Buy

- EURCAD reversed from key support level 1.6200

- Likely to rise to resistance level 1.6365

EURCAD currency pair recently reversed up from the key support level 1.6200 (former monthly high from August) intersecting with the 20-day moving average and the 50% Fibonacci correction of the upward impulse from the start of September.

The upward reversal from the support level 1.6200 continues the active impulse wave 3 which belongs to the extended upward impulse sequence (5) from May.

Given the clear daily uptrend, EURCAD currency pair can be expected to rise to the next resistance level 1.6365 (target price for the completion of the active impulse wave 3).

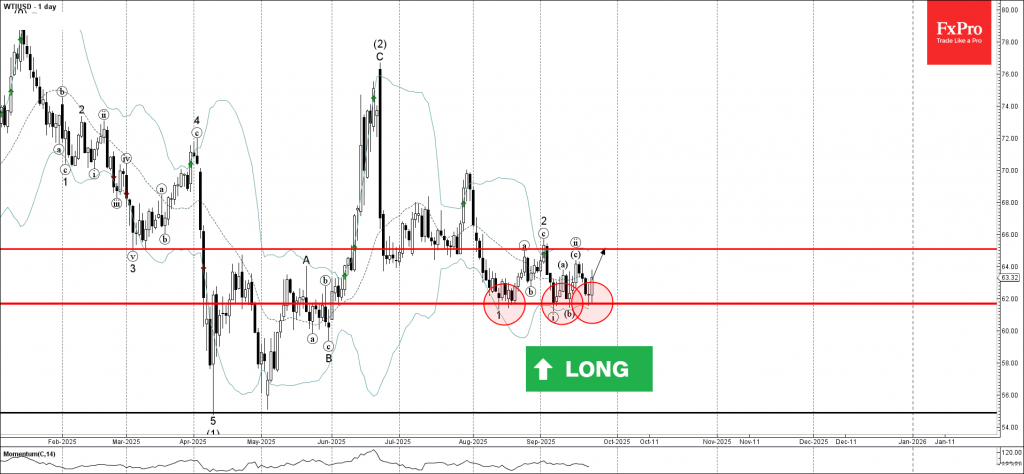

WTI Crude Oil Wave Analysis

WTI crude oil: ⬆️ Buy

- WTI crude oil reversed up from the key support level 61.70

- Likely to rise to resistance level 65.00

WTI crude oil recently reversed up from the key support level 61.70 (which has been reversing the price from the start of August) intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 61.70 will most likely form the daily Japanese candlesticks reversal pattern Morning Star – if the price closes today near the current levels.

Given the strength of the support level 61.70, WTI crude oil can be expected to rise to the next resistance level 65.00 (which stopped earlier waves a, 2 and ii).

Fed’s Goolsbee: Avoid getting too aggressive with cuts upfront

Chicago Fed President Austan Goolsbee said he sees scope for interest rates to come down “a fair amount” over time if stagflation risks fade, though the adjustment should be "gradual". Speaking to CNBC, he suggested neutral rate is 100–125bps below the current 4.00–4.25% range, implying a longer-run policy level around 3%.

Goolsbee stressed that inflation risks remain real, noting price growth has been above target for more than four years. He cautioned against being “overly upfront aggressive” with rate cuts despite growing confidence that inflation can ease back toward 2%.

At the same time, he highlighted that the labor market is cooling at a “mild to modest” pace, providing room for cautious policy adjustment.

Sunset Market Commentary

Markets

Eurozone business activity continued to rise in September, with the composite PMI reaching a 16-month high at 51.2 (from 51 in August). Details couldn’t convince though. New orders and employment stalled while business confidence dropped to a 4-month low. Declining orders and job cuts in manufacturing were balanced by modest expansions in services. Companies often used the clearance of outstanding business to support output growth with work-in-hand now depleting on a monthly basis for the past two-and-a-half years. The manufacturing PMI dipped back into recessionary territory (49.5 from 50.7) after staying north of the 50 boom/bust mark for only the first month since the post-Covid recovery. Purchasing activity, stocks of purchases and stocks of finished goods keep depleting. The EMU services PMI hit a 9-month high at 51.4 (from 50.5). Cost inflation in the services sector eased slightly but remains unusually high. Selling prices cooled more notably. On a national level, Germany was a key driver of growth in September (52.4 from 50.5), recording a solid increase in output that was the joint-fastest since May 2023. France saw activity decrease for the thirteenth consecutive month, and at the sharpest pace since April (48.4 from 49.8), as the government shake-up likely threw a wrench into companies’ production plans. The rest of the Eurozone registered continued growth of output, but the rate of expansion moderated. Today’s PMI’s perfectly fit with the ECB view to keep its deposit rate steady at 2% for the time being. They didn’t impact trading on European bond or FX markets (EUR/USD 1.18) and didn’t spoil positive risk sentiment on European stock markets (+0.5%-+1%). The steady EMU composite PMI contrasted with a significant setback in the UK PMI (51 from 53.5). The latter was “a litany of worrying news including weakening growth, slumping overseas trade, worsening business confidence (fear of Budget measures outweighing BoE rate cuts) and further steep job losses”. September data indicated another sharp increase in average cost burdens across the private sector economy. When it comes to selling prices, service sector firms recorded a solid rise in their prices while manufacturers saw a marked slowdown in factory gate inflation. The weak UK PMI triggered temporary GBP-weakness with EUR/GBP jumping from 0.8720 to 0.8745, without testing the 0.8769 YtD top.

In other news, Washington-based Fed governor Bowman ruffled her dovish feathers. She dissented in July in favour of a 25 bps rate cut and joined last week’s consensus decision. Bowman believes the Fed is seriously at risk of falling behind the curve and said it’s time for the FOMC to act “decisively and proactively to address decreasing labor market dynamisms and emerging signs of fragility. Tariffs won’t have a significant effect on inflation according to her. US markets were unnerved on the comments going into tonight’s economic outlook by Fed Chair Powell.

News & Views

The Riksbank cut the policy rate by 25 bps to 1.75%. Sweden’s central bank expects it to remain there for some time to come, provided the outlook for the economy and inflation holds. The policy rate forecast suggests no changes through 2026. The semi-unexpected (hawkish) rate cut comes with the Riksbank growing more confident that still-high inflation (CPIF 3.2%) is transitory. It referred to a decline in companies’ pricing plans and the stronger currency. The Riksbank added that the tax cuts announced by the government wouldn’t materially affect inflationary pressures apart from slowing down price rises temporarily next year. Growth meanwhile is showing signs of improving but it has been weak for a long time and the timing of the expected recovery has been pushed forward several times. With the cut, the Riksbank aims to facilitate the process. The clear end to the easing cycle is lifting the Swedish crown, pushing EUR/SEK to around 11.

The OECD in its Interim Economic Outlook Report forecasts a 3.2% global expansion this year (up from 2.9% in June. The organization said the economy proved more resilient to tariffs than anticipated, adding, however, that the full impact of the increases has yet to be felt. The 2026 outlook stood unchanged at 2.9%. Among the largest countries, US growth was beefed up to 1.8% (+0.2 ppts) for this year with the 2026 forecast left at 1.5%. A 0.2 ppts bump to 1.2% for this year in the EMU came with a same-sized downward revision for the next (1%). UK activity should end up the second-highest in the G7 (1.4% in 2025) but the country is suffering from the highest inflation rate. The 3.5% for 2025 would ease to 2.7% next year. This compares to 2.7%-3% for the US and 2.1%-1.9% for the EMU.

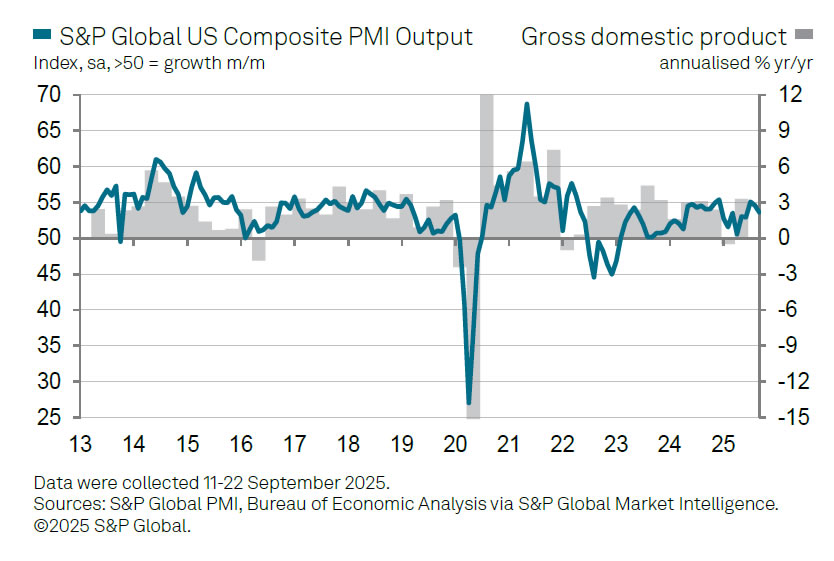

US PMI composite falls to 53.6, still indicative of 2.2% annualized GDP growth in Q3

US business activity softened in September, with PMI Composite falling from 54.6 to 53.6. Manufacturing slipped from 53.0 to 52.0, while services eased from 54.5 to 53.9. Despite the slowdown, the surveys still indicate the economy expanded at a solid 2.2% annualized pace in Q3.

Chris Williamson of S&P Global noted that growth has cooled since peaking in July, with hiring momentum also weakening. Firms reported softer demand conditions, limiting their ability to raise prices.

Tariffs continued to push up input costs across manufacturing and services, but fewer companies were able to pass those costs on, hinting at "squeezed margins but boding well for inflation to moderate"..

The survey suggested consumer inflation will remain above the Fed’s 2% target in the near term, though signs of inventory accumulation in manufacturing could further dampen price pressures ahead.

Bowman warns Fed could be behind the curve on jobs

Fed Governor Michelle Bowman said in a speech that she welcomes the Fed’s decision to start easing last week, noting that the balance of risks between inflation and employment has shifted. She said tariffs no longer appear likely to deliver a persistent inflation shock, which has reduced upside risks to price stability.

With demand softening and labor market conditions turning fragile, Bowman emphasized that the Fed must focus on its employment mandate. She cited benchmark payroll revisions as a clear warning, saying the Fed is at “serious risk of already being behind the curve” in addressing job market deterioration.

She argued the Fed should “preemptively stabilize and support labor market conditions.” If the current conditions continue, Bowman said, “we will need to adjust policy at a faster pace and to a larger degree going forward.”

Additionally, Bowman cautioned against a strict, backward-looking interpretation of data dependence, saying it could force the Fed to implement "abrupt and dramatic policy actions" later if it delays action now. Instead, Bowsheman urged a more "proactive forward-looking approach" framework, one that accounts for how the economy is likely to evolve rather than relying solely on the latest data points.

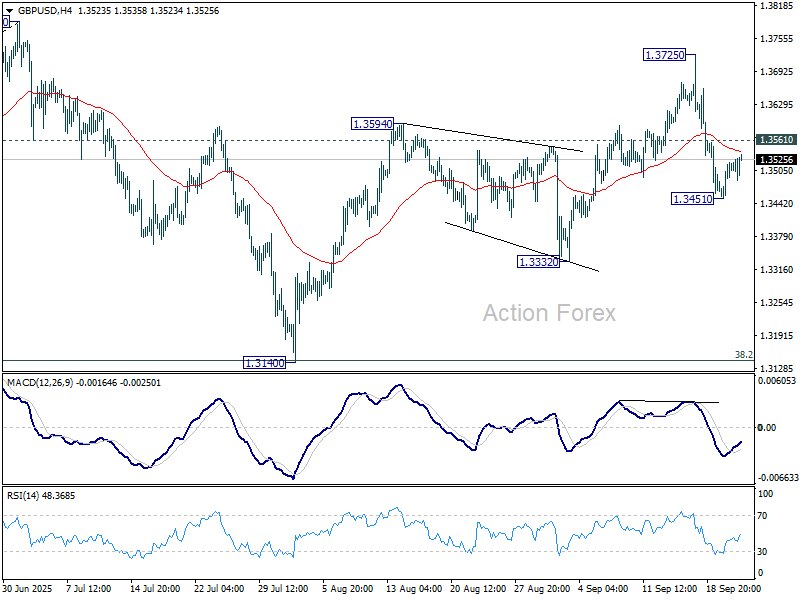

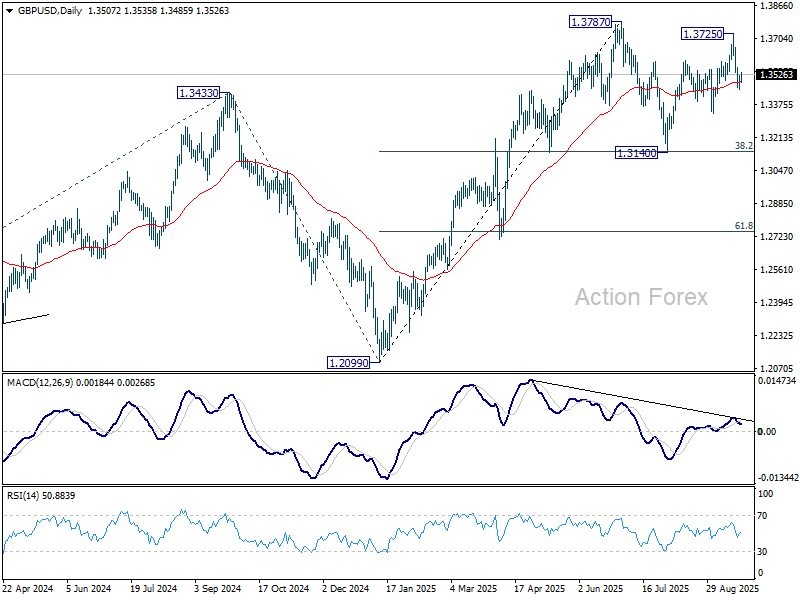

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3471; (P) 1.3496; (R1) 1.3538; More...

Intraday bias in GBP/USD stays neutral for the moment. On the downside, below 1.3451 will resume the fall from 1.3725, as the third leg of the pattern from 1.3787, and target 1.3332 support first. Nevertheless, decisive break of 1.3561 will turn bias back to the upside for retesting 1.3725 instead.

In the bigger picture, rise from 1.3051 (2022 low) is in progress, and would target 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. However, with 1.4248 resistance (2021 high) intact, this rally is more likely a corrective move. Sustained break of 55 W EMA (now at 1.3157) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

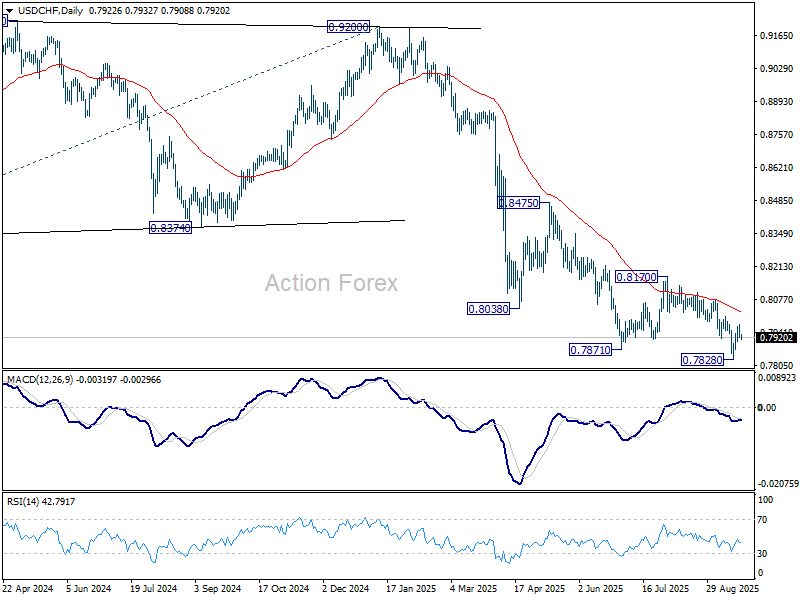

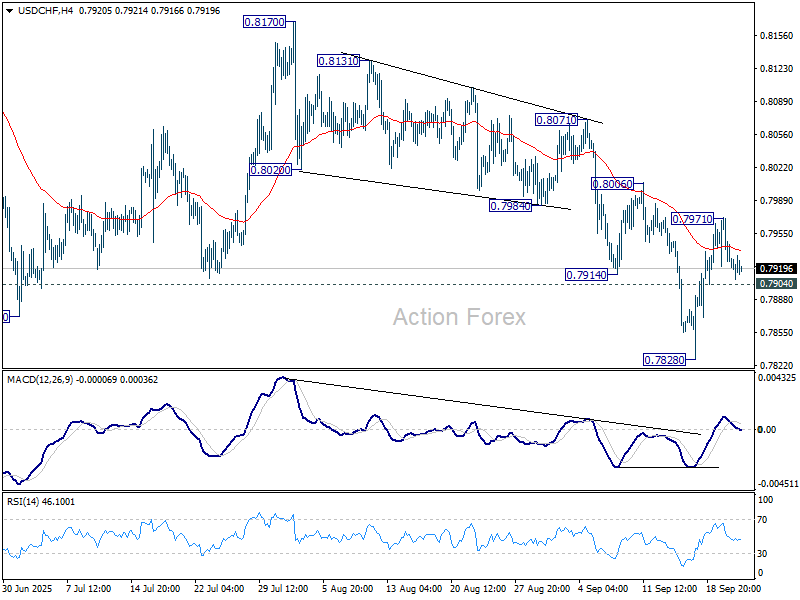

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7906; (P) 0.7940; (R1) 0.7958; More…

Intraday bias in USDCHF remains neutral for the moment. On the upside, above 0.7971 will resume the rebound from 0.7828 short term bottom to 0.8006 resistance. Firm break there will bring stronger rise back to 0.8170. On the downside though, below 0.7904 minor support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).