Sample Category Title

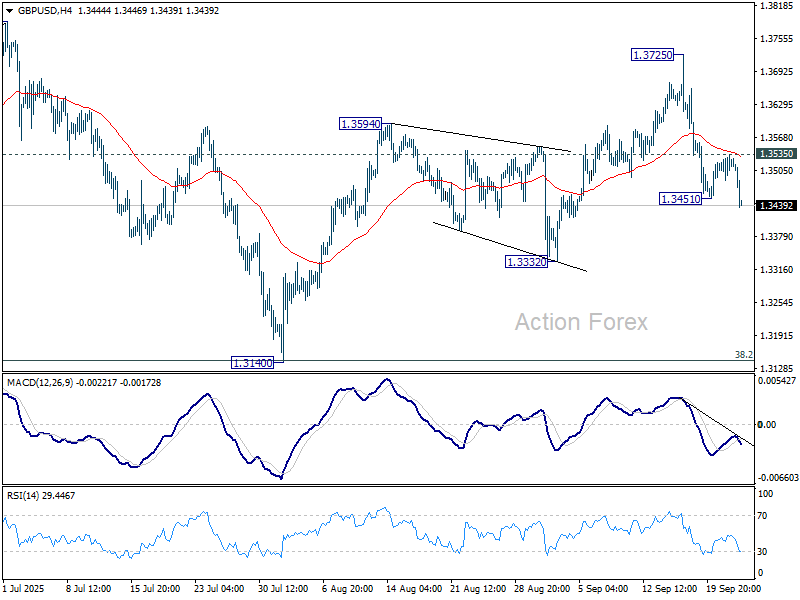

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3496; (P) 1.3517; (R1) 1.3546; More...

GBP/USD's fall from 1.3725 resumed by breaking through 1.3451 temporary low and intraday bias is back on the downside. Corrective pattern from 1.3787 is in the third leg, and deeper fall should be seen to 1.3332 support first. On the upside, above 1.3535 minor resistance will turn intraday bias neutral again first.

In the bigger picture, rise from 1.3051 (2022 low) is in progress, and would target 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. However, with 1.4248 resistance (2021 high) intact, this rally is more likely a corrective move. Sustained break of 55 W EMA (now at 1.3157) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

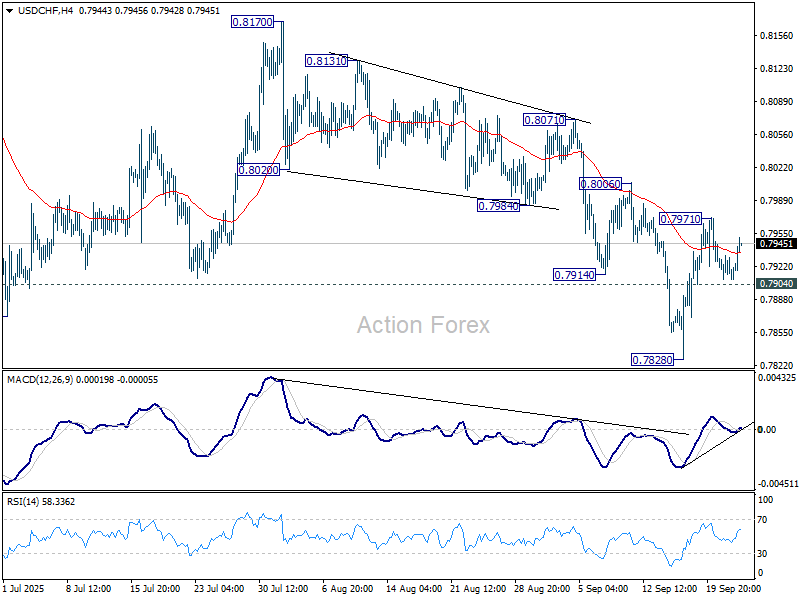

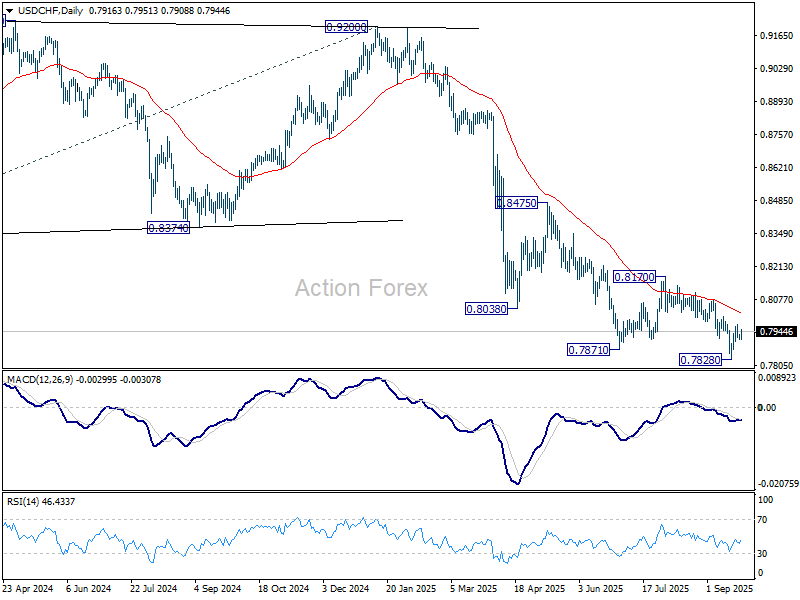

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7897; (P) 0.7925; (R1) 0.7940; More…

No change in USD/CHF's outlook and intraday bias stays neutral. On the upside, above 0.7971 will resume the rebound from 0.7828 short term bottom to 0.8006 resistance. Firm break there will bring stronger rise back to 0.8170. On the downside though, below 0.7904 minor support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

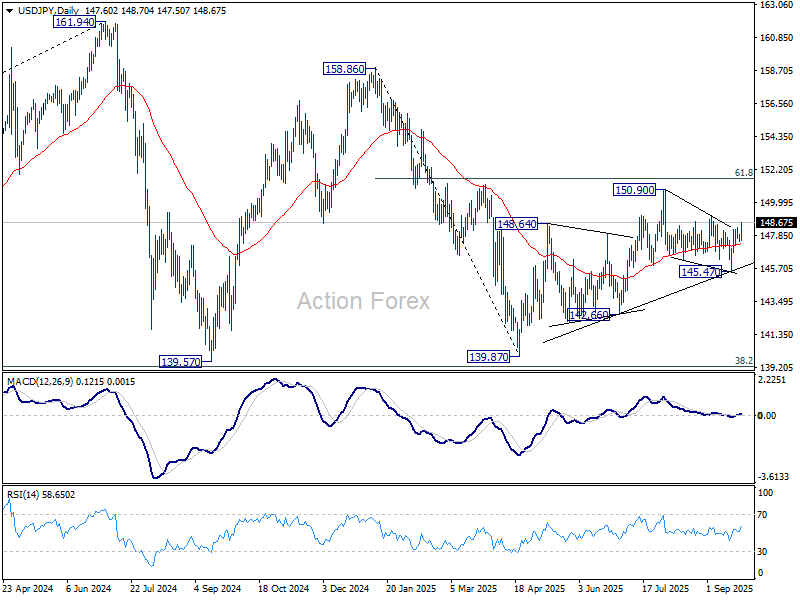

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.44; (P) 147.68; (R1) 147.91; More...

USD/JPY's rebound from 145.47 resumes today and the strong support from 55 4H EMA affirms near term bullishness. Intraday bias is now mildly on the upside for 149.12 resistance. Firm break there should confirm that correction from 150.90 has completed at 145.47. Rise from 139.87 should be ready to resume through 150.90. ON the downside, though, below 147.45 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Dollar Gains, Yen Slips as FX Flows Lack Unified Theme

Dollar strengthened broadly in European session despite limited fresh news flow, but it remains overshadowed by Australian Dollar. Aussie continued to draw support from today’s stronger-than-expected CPI release, which reinforced the view that the RBA will tread cautiously on rate cuts.

There is little sense of a unified theme across FX markets. Eurozone data have been inconsistent. Yesterday’s PMI surveys suggested Germany may be stabilizing, but today’s weaker Ifo survey reminded markets that the path to recovery remains fragile. Yen is under particular pressure today, probably with traders positioning for an extended rally in global equities and higher U.S. yields.

In relative terms, Aussie is the strongest currency so far this week, followed by Swiss Franc and Euro. At the other end, Loonie has been the weakest, with Yen and Kiwi also lagging. Dollar and Sterling remain mid-pack. But positioning is fluid as markets continue to digest diverging inflation and growth signals.

In Europe, at the time of writing, FTSE is up 0.01%. DAX is up 0.16%. CAC is down -0.60%. UK 10-year yield is up 0.004 at 4.687. Germany 10-year yield is up 0.002 at 2.756. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI rose 1.37%. China Shanghai SSE rose 0.83%. Singapore Strait Times fell -0.29%. Japan 10-year JGB yield fell -0.02 to 1.640.

Germany Ifo falls to 87.8, recovery prospects dim

Germany’s Ifo Business Climate Index fell to 87.8 in September from 88.9, with Current Situation Index slipping from 86.4 to 85.7 and Expectations falling from 91.4 to 89.7. The institute said prospects for recovery have "suffered a setback".

By sector, weakness was broad-based. Manufacturing sentiment dropped further, with companies reporting weaker orders and fading optimism among capital goods producers. Services took the hardest hit, plunging to -3.0, the lowest since February, as expectations grew more pessimistic. Trade sentiment also deteriorated, while construction offered a rare bright spot with modest improvement.

Japan's PMI composite falls to 51.1, services resilient as factories struggle

Japan’s private sector lost momentum in September, with the flash PMI Composite slipping from 52.0 to 51.1, the weakest in four months. Manufacturing was the clear drag, with the headline index down from 49.7 to 48.4 and output falling from 49.8 to 47.3. Services held broadly steady at 53.0, down from 53.1.

S&P Global’s Annabel Fiddes said services remain the “key growth engine,” offsetting a “deepening downturn” in manufacturing. Demand trends diverged sharply, with services seeing another solid rise in sales, but factories reporting the fastest drop in new orders since April.

Cost pressures also remain high. Input price inflation has eased from earlier in the year but is still consistent with a sharp rate overall, prompting firms to raise selling prices to protect margins. Companies were more cautious on hiring, with employment growth slowing to the weakest pace in two years.

Australia CPI surprises at 3.0% in August, RBA caution ahead

Australia’s monthly CPI accelerated from 2.8% yoy to 3.0% yoy in August, above expectations of 2.8% yoy and the highest reading since July 2024. The rise was driven by housing (+4.5%), food and non-alcoholic beverages (+3.0%), and alcohol and tobacco (+6.0%).

Core inflation showed stickier trends. CPI excluding volatile items and holiday travel rose from 3.2% yoy to 3.4% yoy. Trimmed mean edged down slightly to 2.6% from 2.7%, but remain well above June’s 2.1% yoy.

RBA is widely expected to hold interest rate unchanged next week. But the stronger core reading will keep November’s meeting live, with rate cut expectations now tempered by concerns that inflation may not be easing as quickly as hoped.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.44; (P) 147.68; (R1) 147.91; More...

USD/JPY's rebound from 145.47 resumes today and the strong support from 55 4H EMA affirms near term bullishness. Intraday bias is now mildly on the upside for 149.12 resistance. Firm break there should confirm that correction from 150.90 has completed at 145.47. Rise from 139.87 should be ready to resume through 150.90. On the downside, though, below 147.45 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Gold Rally Driven by Massive ETF Inflows

- Gold hits new record highs above $3,780 per ounce, up 43% YTD.

- Fed policy is not the only driver; ETF inflows are the key catalyst.

- SPDR Gold Shares absorbed 19 tons in a single day, boosting demand.

- Silver rallies above $44, eyeing its 2011 peak near $50.

Short Pause, Strong Rebound

The pause in gold’s rally after last week’s Fed meeting proved exceptionally brief. Prices surged in recent days, breaking above $3,780 per ounce, with today’s trading consolidating between $3,760 and $3,780. Since the start of the year, gold has gained an impressive 43%. While official commentary signals expectations for further Fed rate cuts, Fed Funds Futures remain stable, still pricing in less than 50 basis points of easing by year-end, in line with FOMC projections.

ETF Inflows as a Key Driver

This suggests that gold’s rally is not driven solely by monetary policy. The crucial factor lies in massive inflows into gold-backed ETFs. On Friday, Bloomberg reported inflows of nearly 27 tons — the strongest daily increase since January 2022 — with 19 tons going into the largest U.S. gold ETF, SPDR Gold Shares. Earlier this week, another 8.7 tons were added, bringing September’s total inflows to 88 tons. Strong institutional and retail demand is fueling the rally alongside concerns about Fed independence and rising geopolitical risks.

Overbought Market, Risk of Correction

With gold reaching new all-time highs, the market has entered overbought territory. This increases the likelihood of some speculative investors taking profits, potentially triggering a short-term correction. The pace of the current rally appears unsustainable in the long run.

Gold CFD chart, daily interval, source: Trading view

Silver Follows the Trend

Silver has also surged, rising above $44 per ounce to its highest level in 14 years. The gold-to-silver ratio temporarily fell below 85, its lowest in 2025. As long as gold remains in a strong uptrend, silver has room for further gains, with the historical resistance near $50 from April 2011 being a critical reference point.

Nasdaq 100: Short-Term Bullish Trend Remains Intact Above 24,535 Key Support

Key takeaways

- Bullish momentum intact above 24,535 key support despite recent profit-taking in mega-cap tech stocks.

- AI-driven optimism continues to fuel upside, supported by massive investments from Nvidia and Oracle into OpenAI.

- Positive market breadth as more Nasdaq 100 stocks are trading above 20- and 50-day moving averages.

- Next resistance zones at 24,890, 25,010/25,100, and 25,160/25,270.

The price actions of the US Nasdaq 100 CFD Index (a proxy of the Nasdaq 100 futures) have continued to soar and have printed three consecutive fresh all-time high closing highs since 18 September 2025.

The recent bout of risk-on behaviour has been attributed to the AI-driven productivity narrative embraced on Wall Street. AI juggernaut Nvidia has announced $100 billion worth of investments into OpenAI to support new data centres and other artificial intelligence infrastructure. Interestingly, this latest significant AI-related deal came after Oracle surprised Wall Street last week with a whopping $300 billion deal with OpenAI.

On Wednesday, 23 September 2025, the major US stock indices pulled back as profit-taking emerged in mega-cap technology names. The Nasdaq 100 led the decline, slipping -0.7%, while the S&P 500 lost -0.5%. The Dow Jones Industrial Average and small-cap Russell 2000 fared relatively better, each easing -0.2%.

Is this the start of a deeper, multi-week corrective decline for the US Nasdaq 100 CFD Index? Let’s break it down accordingly to its latest technical analysis elements, short-term trajectory (1 to 3 days), and relevant short-term key levels to watch.

Fig. 1: US Nasdaq 100 CFD Index minor trend as of 24 Sep 2025 (Source: TradingView)

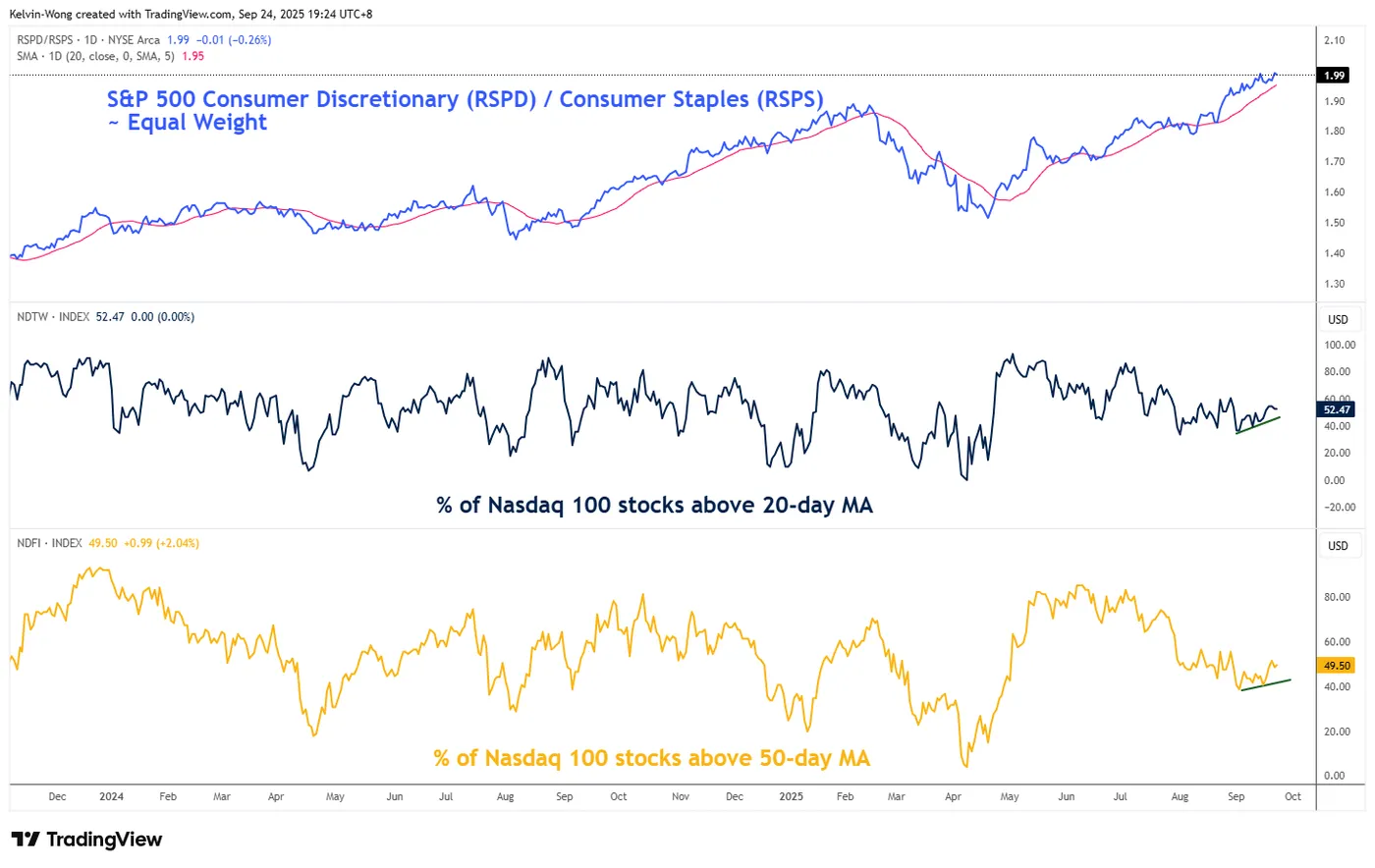

Fig. 2: Market breadth of Nasdaq 100 (% of stocks above 20-day/50-day MA) & relative performance of equal-weighted S&P 500 Consumer Discretionary sector ETF against equal-weighted S&P 500 Consumer Staples sector ETF as of 23 Sep 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

The short-term minor uptrend phase of the US Nasdaq 100 CFD Index remains intact from the 2 September 2025 low of 22,979.

Bullish bias above 24,535 short-term pivotal support for the next intermediate resistances to come in at 24,890, 25,010/25,100, and 25,160/25,270 (Fibonacci extension cluster) (see Fig. 1).

Key elements

- The price actions of the US Nasdaq 100 CFD Index have continued to trade above its 20-day and 50-day moving averages. These observations support a short-term and medium-term uptrend phase for the US Nasdaq 100 CFD Index (see Fig.1).

- The lower boundary of the minor ascending channel of the US Nasdaq 100 CFD Index confluences closely with the 24,535 short-term pivotal support (see Fig.1).

- The hourly RSI momentum indicator has just exited from its oversold region (below the 30 level), which indicates that yesterday’s bearish momentum has eased (see Fig.1).

- Market breadth remains positive in the Nasdaq 100 as the percentage of Nasdaq 100 component stocks trading above their respective 20-day and 50-day moving averages has increased steadily from 2 September 2025 to 23 September 2025 (% of stocks above 20-day moving averages jumped from 37% to 52%, and % of stocks above 50-day moving averages increased from 41% to 50% (see Fig.2).

- The higher beta equal-weighted S&P 500 Consumer Discretionary sector ETF has continued to outperform the defensive-oriented equal-weighted S&P 500 Consumer Staples sector ETF. This observation supports a bullish reversal scenario in the US Nasdaq 100 CFD Index (see Fig.2).

Alternative trend bias (1 to 3 days)

Failure to hold at the 24,535 key short-term support on the US Nasdaq100 CFD Index jeopardises its short-term minor uptrend phase to open scope for a deeper minor corrective decline sequence towards the next intermediate supports at 24,305 and 24,140/24,050 (also the rising 20-day moving average) (see Fig. 1).

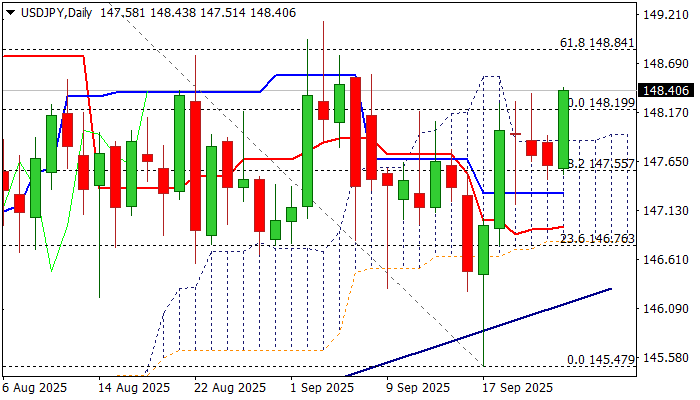

USD/JPY: Lift Above Daily Cloud Generates Fresh Bullish Signal

USDJPY rose on Wednesday, underpinned by more cautious tone on monetary policy by Fed Powell and increased purchases by Japanese importers.

The dollar regained traction after chief Powell signaled that the central bank needs to have balanced approach as it faces two strong and opposite forces – weakening of the labor sector from one side and elevated inflation on the other.

Although Powells’ remarks were diverging from his recent comments, markets still price in two more rate cuts by the end of the year.

The US dollar advanced 0.5% until mid-European session on Wednesday, as fresh strength reversed drop in past three days and generated bullish signal on break above daily Ichimoku cloud (cloud top lays at 147.88).

Daily close above cloud to verify signal and strengthen near term structure for probe through next barrier at 148.49 (200DMA, currently under increased pressure), violation of which to generate signal of bullish continuation of recovery leg from 145.47 (Sep 17 spike low) and expose 149.13 (Sep 3 lower top).

Technical picture on daily chart is improving as MA’s are almost in full bullish setup and 14-d momentum attempts to break into positive territory, while the price holds above the top of thick daily cloud.

Recent formation of a bull-trap under 100DMA also underpins the action.

Res: 148.49; 148.84; 149.13; 149.63.

Sup: 148.20; 147.88; 147.56; 147.19.

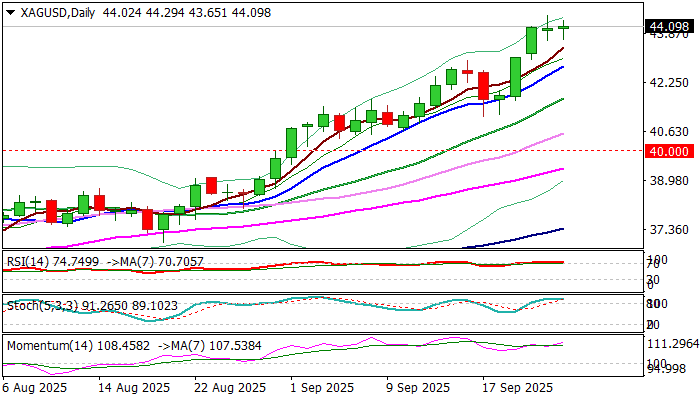

Silver: Bulls Take a Breather Under Psychological $45 Barrier

Silver price reduced pace after hitting new multi-year high ($44.46) on Tuesday but keeps firm bullish stance, lifted by recent rally in gold.

Tuesday’s Doji candle and Wednesday’s action, being so far in the same shape, signal indecision on approach to psychological $45.00 barrier.

Overbought conditions on daily chart suggest that bulls may take a breather for consolidation / shallow correction.

Higher base at $43.65 zone (Tue/Wed lows) offers immediate support with potential deeper dips to be ideally contained by rising 10DMA / 50% retracement of $41.11/$44.46 bull-leg) at $42.75 and keep bulls intact for fresh push higher, in the environment of strong positive sentiment.

Sustained break of $45.00 pivot to unmask Fibo projections at $45.51 and $45.94, along with nearby round-figure $46.00 resistance.

Alternatively, loss of $42.75 support would risk deeper pullback and expose targets at $41.70 (rising 20DMA) and 41.11/19 (Sep 17/18 higher base).

Res: 44.46; 45.00; 45.51; 45.94.

Sup: 43.65; 42.75; 41.70; 41.11.

Euro Returns to Yearly Highs: Continuation of the Rally or a Bull Trap?

European currencies are rebounding following a recent correction, with EUR/USD and EUR/JPY supported by last week’s interest rate cut by the US Federal Reserve. The Fed’s easing decision triggered a jump in the euro to a yearly high, although some of those gains were quickly pared back. The euro is now showing renewed upward momentum, but the further direction of the trend will depend on whether fresh data from the US and Europe confirm a continuation of the rally or trigger another pullback. In the coming sessions, markets will be watching the release of German business climate indices and US housing market data, which could set the tone for price movements.

EUR/USD

After a sharp rise to 1.1920, the EUR/USD pair retreated, losing around 200 points. Nevertheless, buyers of the single European currency found support just above 1.1700, and yesterday’s daily candle closed near 1.1800. Technical analysis of EUR/USD points to a possible continuation of the rise towards recent highs, as a “bullish engulfing” pattern has formed on the daily timeframe. A daily close below 1.1720 could open the way for a deeper correction, with initial targets around 1.1650.

Events likely to influence EUR/USD in the coming sessions:

- Today at 10:00 (GMT+3): Speech by B. Balz of the Bundesbank

- Today at 10:00 (GMT+3): European Central Bank meeting on non-monetary policy matters

- Today at 11:00 (GMT+3): Germany’s IFO Business Climate Index

EUR/JPY

Last week, EUR/JPY broke a key resistance level at 174.00 and has so far held above it. If the 173.40–173.80 range is confirmed as support, the pair could rise towards last year’s highs at 175.00–175.40. A close below 173.40 could pave the way for a decline towards 172.70.

Events likely to influence EUR/JPY in the coming sessions:

- Today at 17:00 (GMT+3): US new home sales

- Today at 23:10 (GMT+3): Speech by FOMC member Mary Daly

- Tomorrow at 02:50 (GMT+3): Bank of Japan Monetary Policy Meeting minutes

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

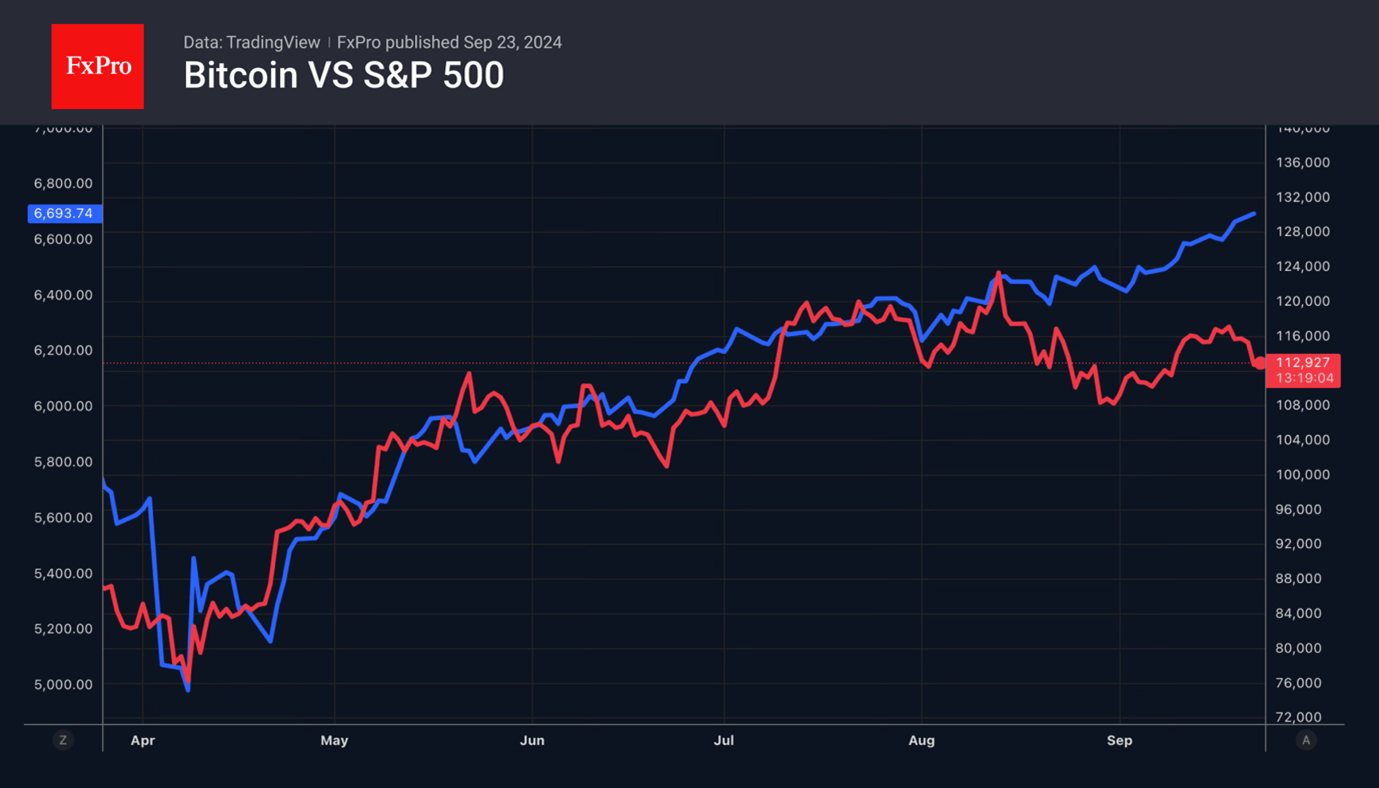

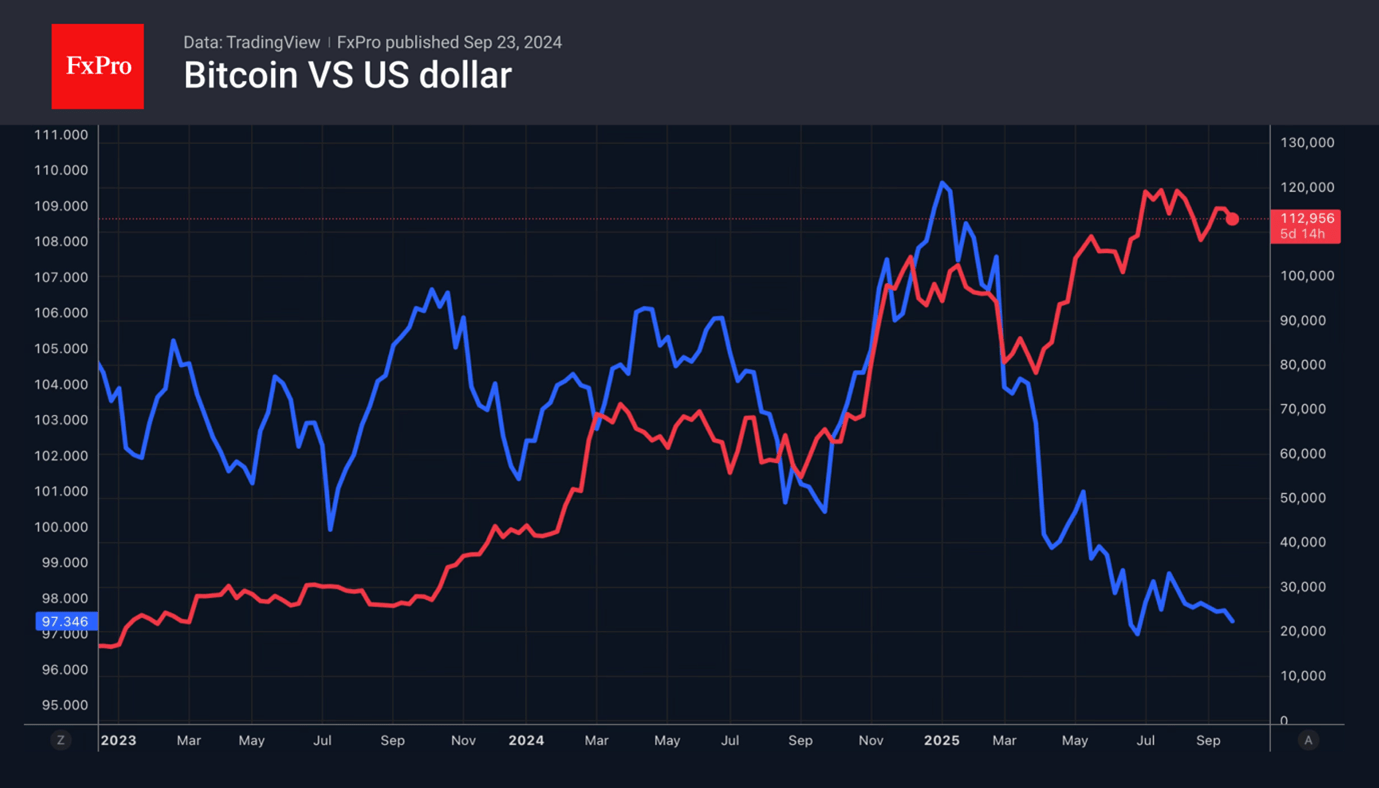

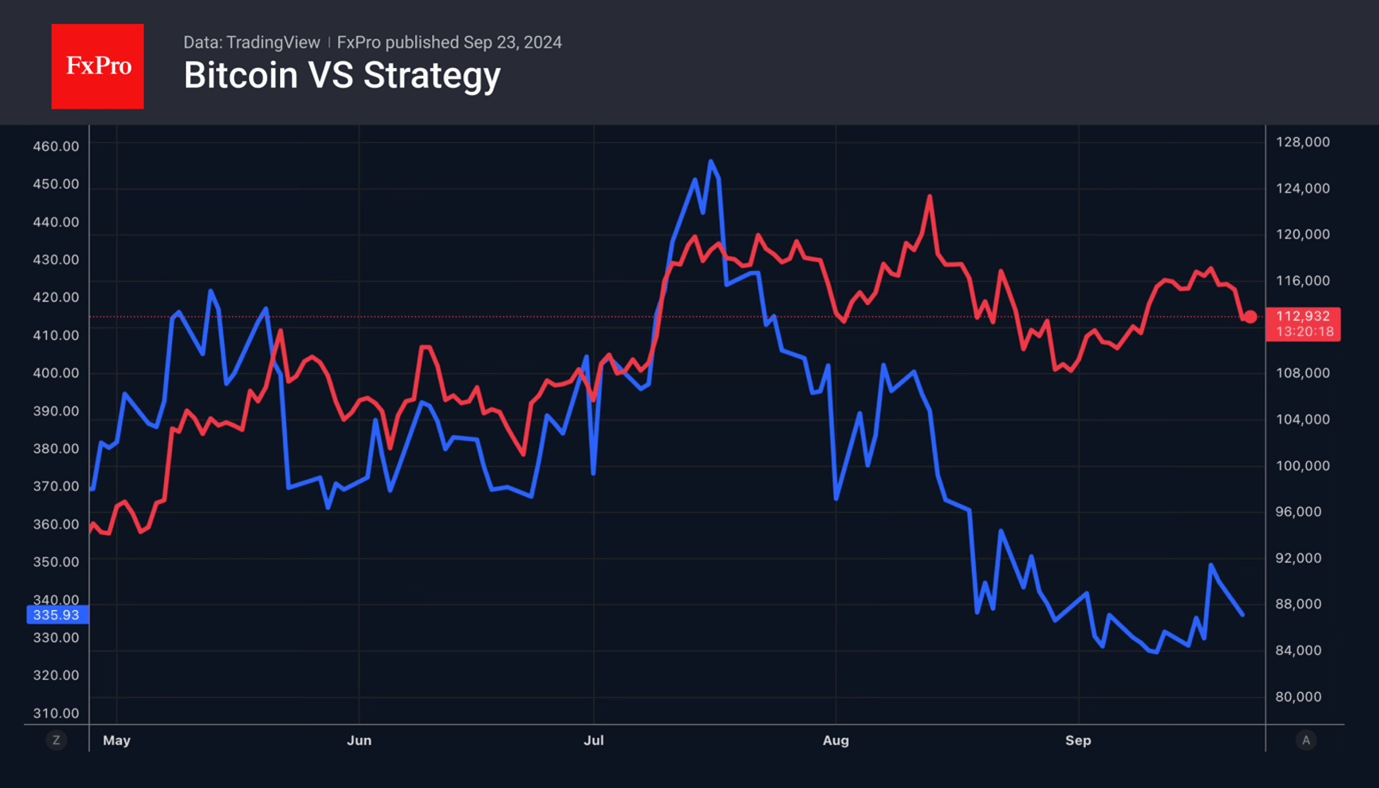

BTC Calm Breaks as Bulls Face Resistance

Digital assets have been hit by one of the biggest sell-offs since the beginning of the year. According to Coinglass, 1.5 billion dollars in long positions were liquidated at the start of this week. Bitcoin fell from its monthly highs due to a revision of market views on the fate of the federal funds rate, the strengthening of the US dollar, and concerns about a decline in demand.

Corporations have accumulated $116 billion worth of Bitcoin and have become serious players in the market. The fall in their shares, coupled with Nasdaq’s requirement for shareholder approval of new issues, has created real panic. If these financial institutions find it difficult to raise funds through securities issues, demand for digital assets will fall, and prices will also drop.

Optimists believe that this is not the case. There are also specialised exchange-traded funds and the resumption of the Fed’s monetary policy easing cycle is likely to increase demand for Bitcoin ETFs. The outflow of capital from money market funds will also play a role. Reserves increased to a whopping $7.7 trillion in 2025. The average yield was 4.1%, which is significantly higher than the average 0.6% on bank deposits. As the federal funds rate declines, yields will fall, and money will flow into other ETFs, including those related to cryptocurrency.

Investors believe that over time, the link between US stock indices and Bitcoin will be restored. However, while US stocks have such an important growth driver as artificial intelligence technology, Bitcoin does not. Companies from the S&P 500, especially tech giants, regularly report positive corporate reports. Interest in cryptocurrency purchases by corporations, on the contrary, is falling.

The cryptocurrency market is prone to extremes. The highest derivative bets are concentrated at the 95,000 and 140,000 levels. This means that after a long period of calm, investors are expecting to see a real storm. Much will depend on the ability of Bitcoin bulls to overcome important resistance levels at 113,500 and 115,000. If they succeed, there will be a chance to restore the uptrend. Failure will increase the risks of a Bitcoin correction.