Sample Category Title

(SNB) Swiss National Bank leaves SNB policy rate unchanged at 0%

The Swiss National Bank is leaving the SNB policy rate unchanged at 0%. Banks' sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold. The discount for sight deposits above this threshold still stands at 0.25 percentage points. The SNB remains willing to be active in the foreign exchange market as necessary.

Inflationary pressure is virtually unchanged compared to the previous quarter. Monetary policy helps to keep inflation within the range consistent with price stability and supports economic development. The SNB will continue to monitor the situation and adjust its monetary policy if necessary, in order to ensure price stability.

Inflation has increased slightly since the last monetary policy assessment. It rose from -0.1% in May to 0.2% in August. This increase was mainly attributable to higher inflation in tourism and on imported goods.

Inflationary pressure has barely changed compared to June. While inflation is likely to be slightly higher in the short term, in the medium term the conditional inflation forecast remains unchanged. The forecast is within the range of price stability over the entire forecast horizon (cf. chart). As in the previous quarter, it puts average annual inflation at 0.2% for 2025, 0.5% for 2026 and 0.7% for 2027 (cf. table). The forecast is based on the assumption that the SNB policy rate is 0% over the entire forecast horizon.

Global economic growth slowed somewhat in the first half of 2025. Global economic developments are being dampened by US tariffs and ongoing high uncertainty.

In its baseline scenario, the SNB anticipates that growth in the global economy will be subdued over the coming quarters. Inflation in the US is likely to remain elevated for some time. In the euro area, on the other hand, inflation is expected to stay close to target.

The scenario for the global economy remains subject to high uncertainty. For example, trade barriers could be raised further, leading to a more pronounced slowdown in the global economy. However, it also cannot be ruled out that the global economy will prove more resilient than expected.

Economic growth in Switzerland was weak in the second quarter. After increasing strongly in the first quarter, GDP expanded by just 0.5%. The major fluctuations in the first half of the year were principally due to the pharmaceuticals industry. Value added there rose strongly in the first quarter because deliveries to the US were brought forward. A corresponding countermovement occurred in the second quarter, while the services sectors supported the economy. Unemployment has risen further in recent months.

The economic outlook for Switzerland has deteriorated due to significantly higher US tariffs. The tariffs are likely to dampen exports and investment especially. Companies in the machinery and watchmaking industries are particularly affected. To date, the impact on other industries - notably in the services sector - has been limited. Many economic indicators therefore still point to a stable situation and moderate growth. The SNB continues to expect GDP growth of 1% to 1.5% for 2025 as a whole. As a result of the tariffs and the high level of uncertainty, the SNB expects growth of just under 1% for 2026. In this environment, unemployment is likely to continue rising.

The economic outlook for Switzerland remains uncertain. The main risks are US trade policy and global economic developments.

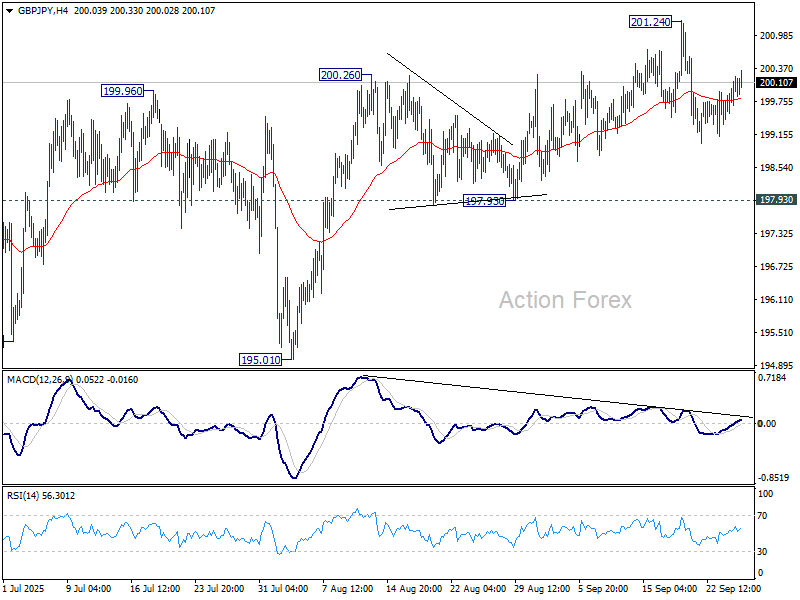

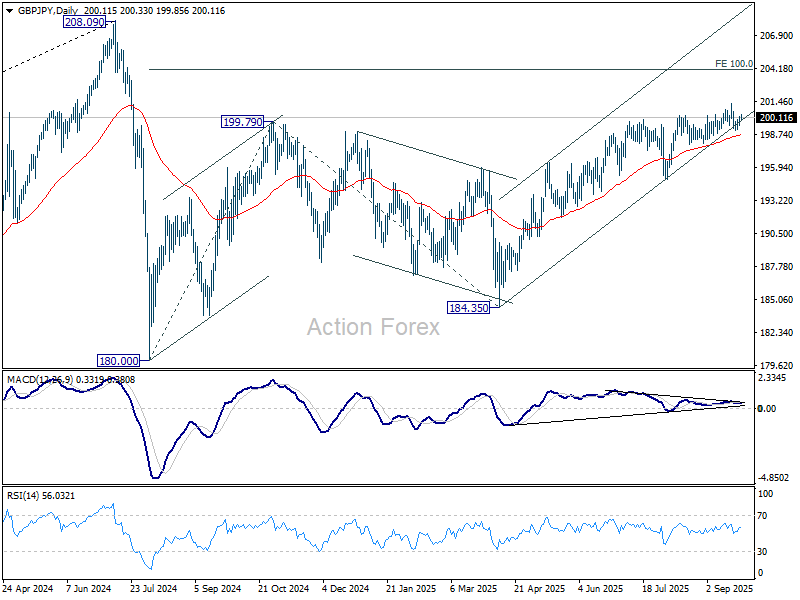

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.67; (P) 199.96; (R1) 200.53; More...

Range trading continues in GBP/JPY and intraday bias remains neutral. Further rise is expected as long as 197.93 support holds. Firm break of 201.24 will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. However, considering bearish divergence condition in both D and 4H MACD, firm break of 197.93 will indicate bearish reversal and bring deeper fall back to 195.01 support first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

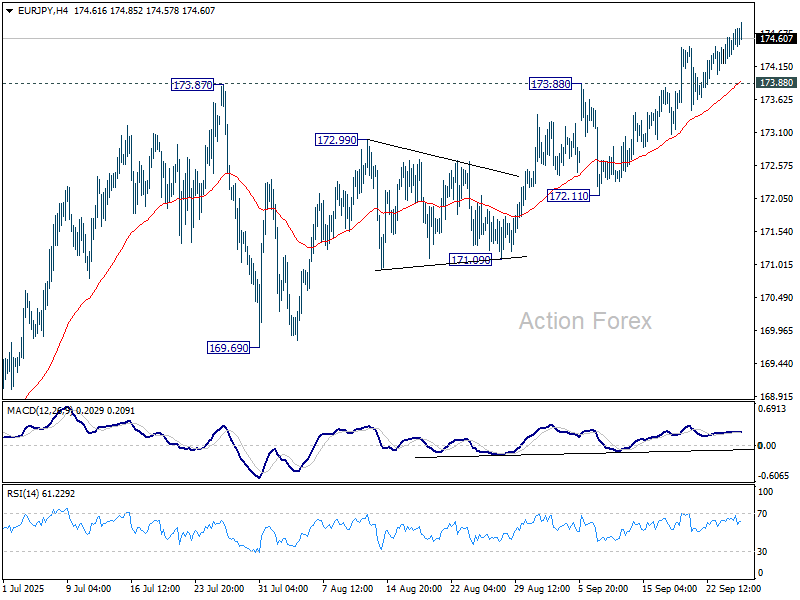

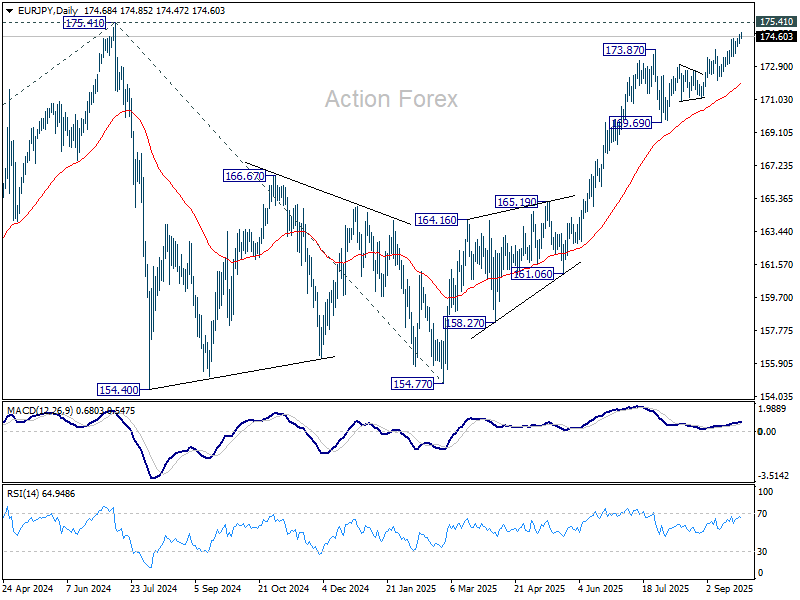

EUR/JPY Daily Outlook

Daily Pivots: (S1) 174.40; (P) 174.60; (R1) 174.98; More...

EUR/JPY's rally continues today and intraday bias stays on the upside for retesting 175.41 high. Decisive break there will resume larger up trend. On the downside, however, firm break of 173.88 resistance turned support will turn bias back to the downside for deeper pullback to 172.11 support instead.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 (2022 low) to 175.41 from 154.77 (2025 low) at 186.31. However, sustained break of 169.69 support will delay this bullish case, and probably extend the correction from 175.41 with another fall.

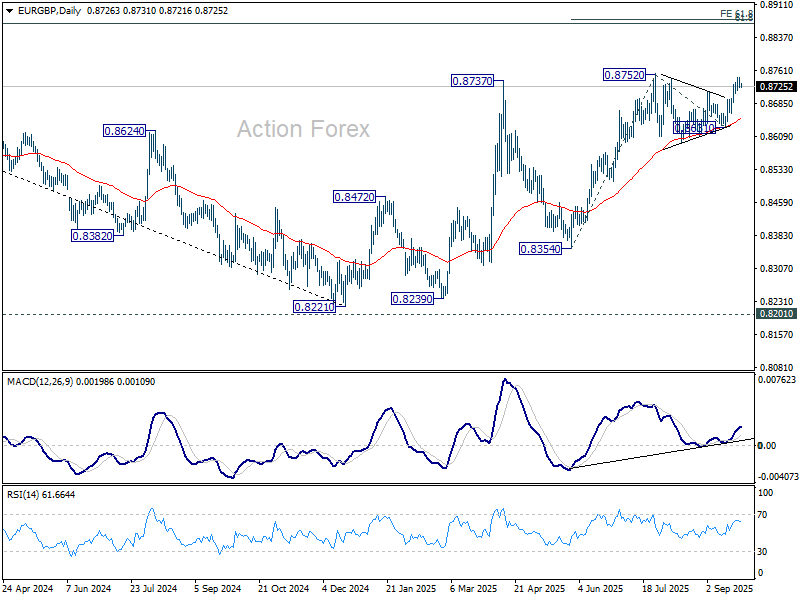

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8720; (P) 0.8732; (R1) 0.8742; More...

EUR/GBP retreated ahead of 0.8752 key resistance and intraday bias is turned neutral first. Further rise is expected as long as 0..8694 support holds. Decisive break of 0.8752 will resume larger rally to 61.8% projection of 0.8354 to 0.8752 from 0.8631 at 0.8877, which is close to 0.8867 fibonacci level. However, break of 0.8694 will turn bias back to the downside for 0.8631 support, to extend near term sideway trading.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8518) will argue that the pattern has completed and bring retest of 0.8221 low.

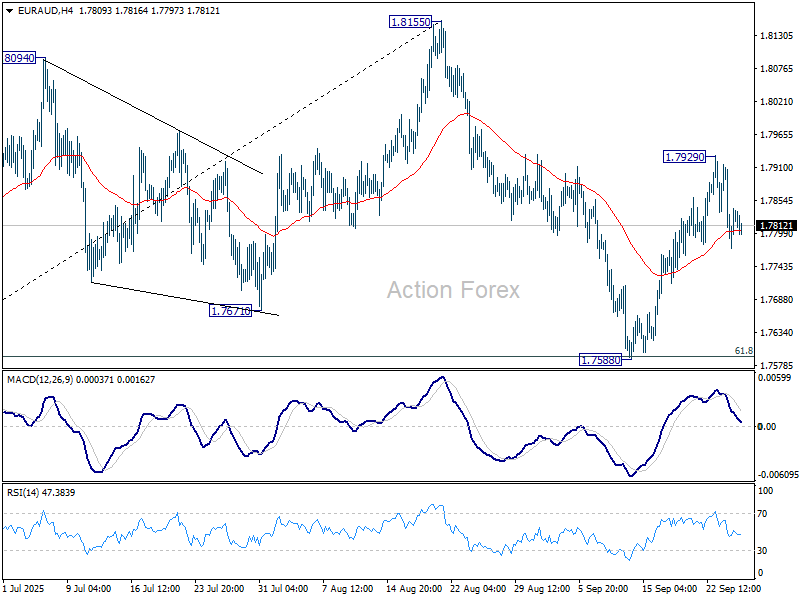

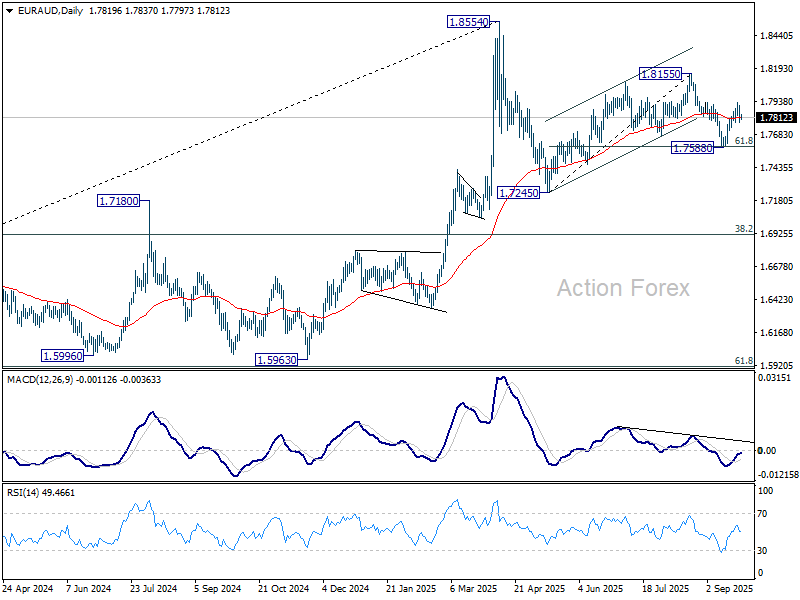

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7764; (P) 1.7843; (R1) 1.7910; More...

Intraday bias in EUR/AUD stays neutral first and some more consolidations could be seen below 1.7929. On the upside, break of 1.7929 temporary top will resume the rebound from 1.7588 to retest 1.8155 high. Firm break there will resume the whole rise from 1.7245. However, break of 1.7588 will resume the fall from 1.8155 instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

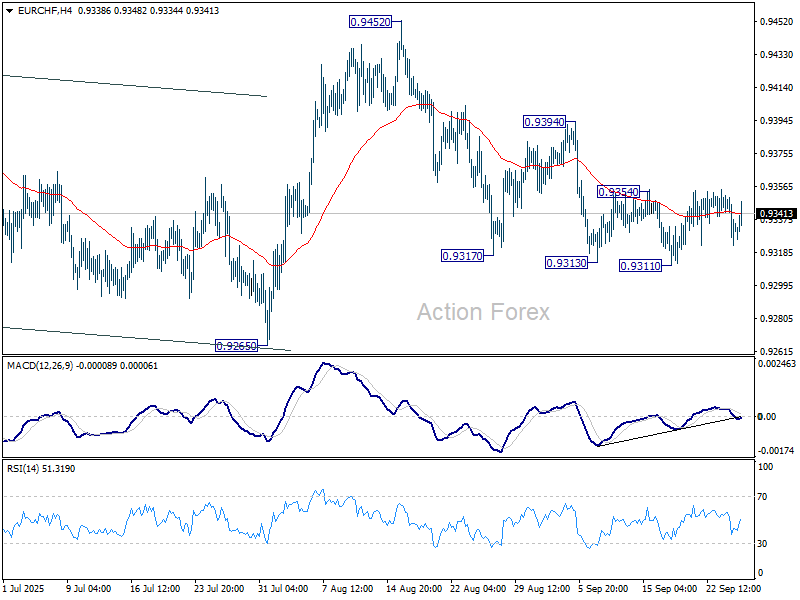

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9320; (P) 0.9338; (R1) 0.9353; More...

Range trading continues in EUR/CHF and intraday bias stays neutral. Considering bullish convergence condition in 4H MACD, firm break of 0.9354 resistance will confirm short term bottoming, and bring stronger rebound to 0.9394 resistance. On the downside, break of 0.9311 will resume the fall from 0.9452 to 0.9265 support.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

A Lot of Fed Policymakers Again Hit the Wires Today

Markets

The US dollar spared no one yesterday. Backed by some UST underperformance, the greenback rallied against all of its major peers. The trade-weighted index rose towards but nevertheless closed below 98. EUR/USD wiped out the gains of the previous two sessions by declining from 1.18+ to 1.1738, losing the short-term upward trendline in the process. Cable (GBP/USD) finished at the lowest level in three weeks (1.3447) and USD/JPY tested the highest levels in around two months. The pair pushed beyond the 200dMA with a close at 148.9. US yields marched higher, locking in gains between 1.8 and 4.9 bps, the belly underperforming the winds. This contrasted with the yields status quo in Europe and Germany or the slight decline at the long end in the UK. With views at the Fed differing so much, US yields find it difficult to find a balance the way European ones do. Chicago Fed Goolsbee was the latest one to challenge the Fed’s median dot plot (showing two more cuts this year). He’s uncomfortable to overly frontload rate cuts “on the presumption that inflation will probably just be transitory and go away”. Goolsbee was less concerned on the labour market, in a view that chimes with the one from Daly. The SF Fed supported last week’s cut and said that further adjustments may be necessary but it should be approached with caution. Daly noted the labour market has slowed but was not weak and the economy not at risk of a recession. It’s these kind of comments that help yields bottom out for the time being. A lot of Fed policymakers again hit the wires today, capable of triggering some intraday volatility. Economic data includes the weekly jobless claims, durable goods orders and housing data. Usually of second-tier importance, although last week’s sharp drop in jobless claims didn’t go unnoticed. Both the US dollar and yields are steady going into the releases. A strong auction this morning of very long-term Japanese bonds (40-yr) eased some demand concerns for now. Japanese yields drop a few bps in a flattening move in response. A mixed equity performance in Asia this morning offers little guidance for the European open. Wall Street indices yesterday struggled near the record highs. Oil prices hover near yesterday’s close. The black gold had a strong two days, potentially related to risks of the Russia-Ukraine war escalating (Brent $69/b). It chimes with the CE FX underperformance, particularly by the zloty yesterday.

News & Views

The Czech National Bank held its policy rate stable at 3.5% yesterday. In order to maintain inflation near the 2% target in the long term, a relatively tight monetary policy is still required. Latest data confirm an economic recovery primarily based on domestic demand while inflation is expected to stay in the upper half of the tolerance band for the rest of the year (2-3%). Risks around the outlook are inflationary overall stemming from food prices, inertia in services inflation including imputed rent, rapid wage growth in a tight labour market, the potential economic boost growth from domestic and European fiscal spending, a recovery in lending activity and the launch of the EU Emissions Trading System 2 in 2027. A stronger CZK FX rate fails to compensate for these potential inflationary pressures. Czech money markets don’t expect policy rate stability over the next year or so. CNB governor Michl said at the press conference that the central bank leaves all options open though and that it can’t be ruled out that the next step will be either lowering or increasing rates. This caused some weakness in CZK with EUR/CZK closing 24.31 up from a 19-month low at 24.21.

New EU car registrations rose by 5.3% Y/Y, but are 0.1% lower YtD compared to the same period last year. Up until August, hybrid electric vehicles (HEV) are the preferred choice amongst consumers. This time around last year, these were still petrol cars (34.9%). HEV’s EU market share rises from 29.7% in the Jan-Aug 2024 period to 34.7% YtD in 2025. Battery-electric cars accounted for 15.8% of market share (up from 12.6%). Germany, Belgium, the Netherlands and France together account for 62% of BEV registrations. The combined share of petrol and diesel cars fell to 37.5%, down from 47.6% over the same period in 2024. In Belgium, petrol cars retain the biggest market share with 42.3% of new registrations YtD (42.6% last year). BEV’s and HEV’s rank 2nd and 3rd with respectively 32.9% (from 25.9%) and 11.4% (from 9.1%) of registrations.

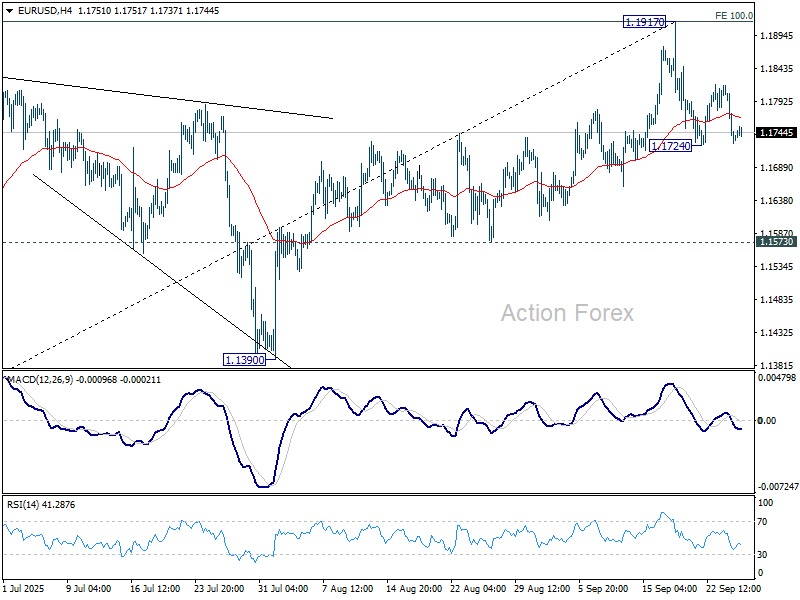

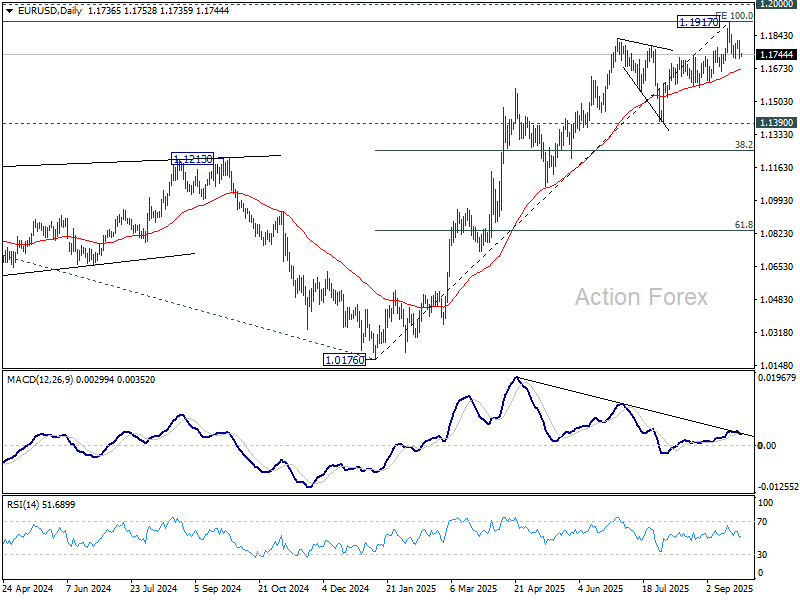

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1704; (P) 1.1762; (R1) 1.1795; More...

Intraday bias in EUR/USD remains neutral for the moment. On the downside, break of 1.1724 will resume the fall from 1.1917 to 55 D EMA (now at 1.1668). Considering bearish divergence condition in D MACD, sustained break of 55 D EMA will argue that 1.1917 is already a medium term top. Deeper fall should then be seen to 1.1390 support next. However, sustained break of 1.1917 will resume larger up trend to 1.2 psychological level.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1214).

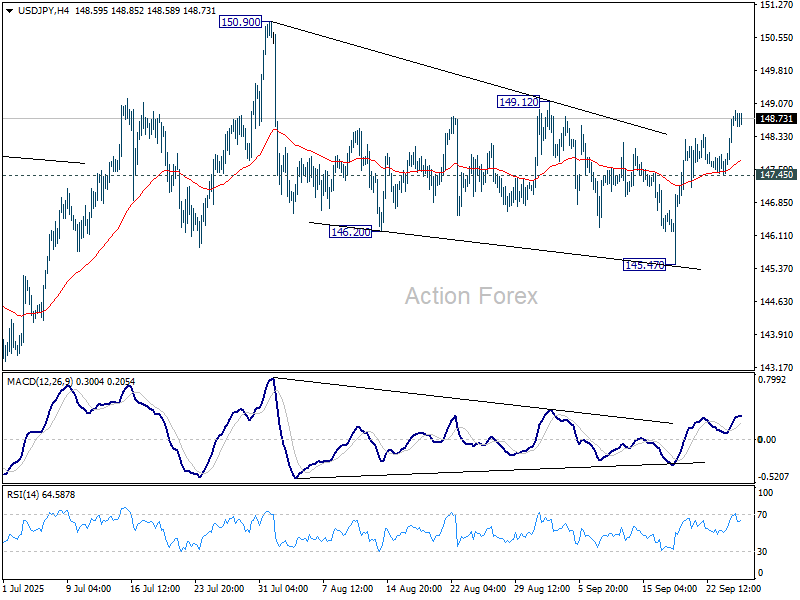

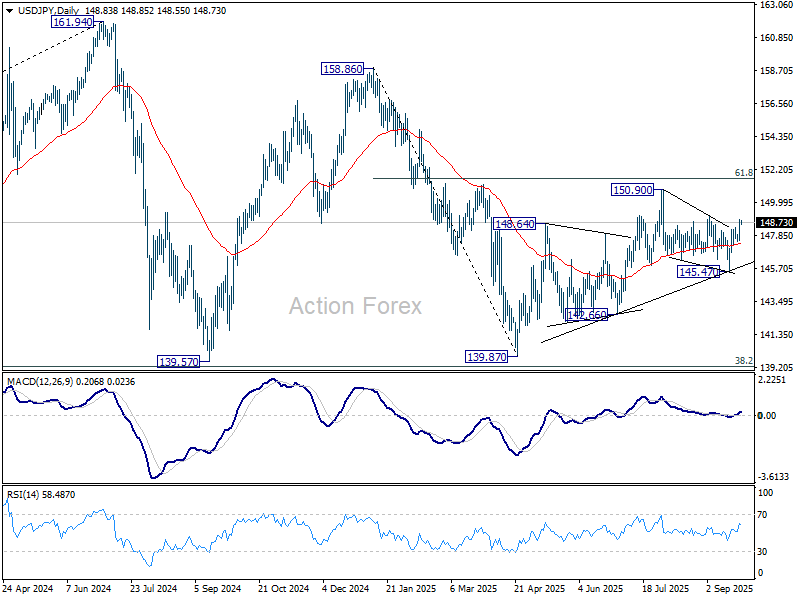

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.98; (P) 148.45; (R1) 149.38; More...

Intraday bias in USD/JPY remains on the upside for 149.12 resistance. Decisive break there should confirm that correction from 150.90 has completed at 145.47. Rise from 139.87 should be ready to resume through 150.90. On the downside, though, below 147.45 support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

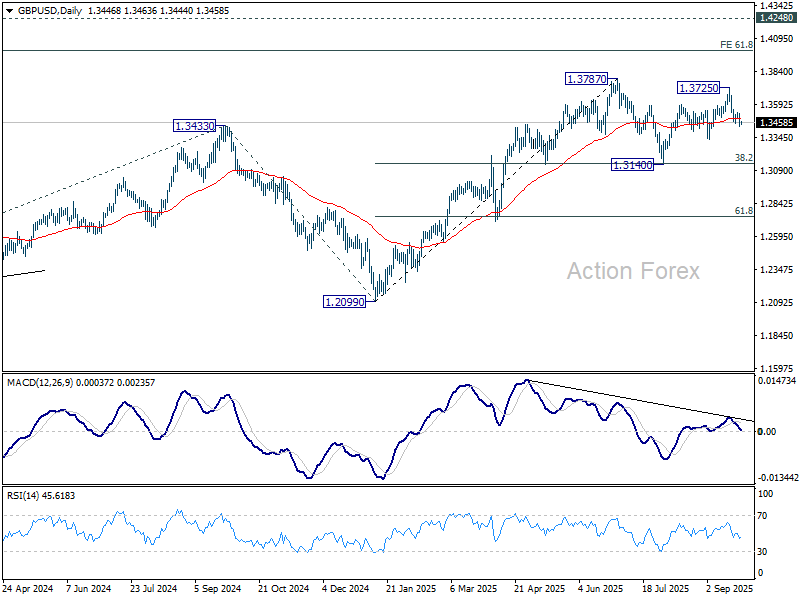

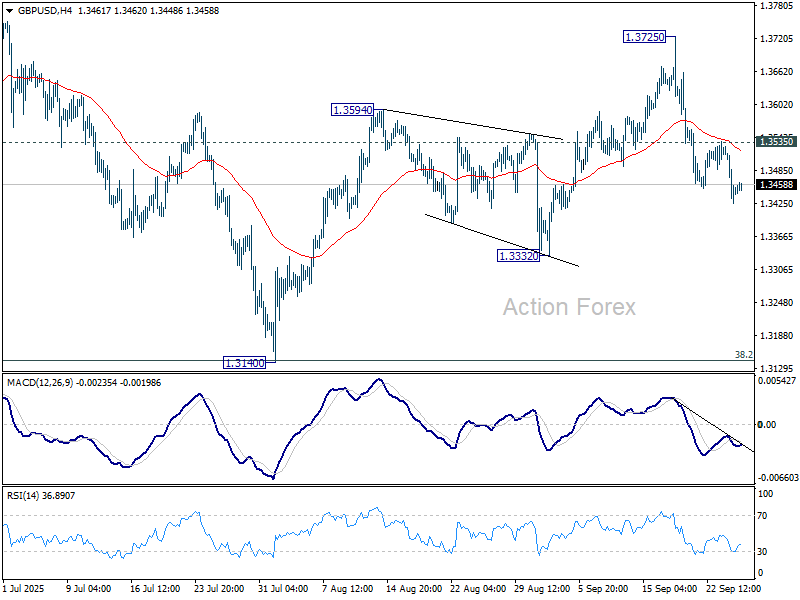

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3405; (P) 1.3467; (R1) 1.3509; More...

Intraday bias in GBP/USD remains on the downside for the moment. Fall from 1.3725, as the third leg of the corrective pattern from 1.3787, is in progress to 1.3332 support. Break there will target 1.3140. On the upside, above 1.3535 minor resistance will turn intraday bias neutral again first.

In the bigger picture, rise from 1.3051 (2022 low) is in progress, and would target 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. However, with 1.4248 resistance (2021 high) intact, this rally is more likely a corrective move. Sustained break of 55 W EMA (now at 1.3157) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.