Sample Category Title

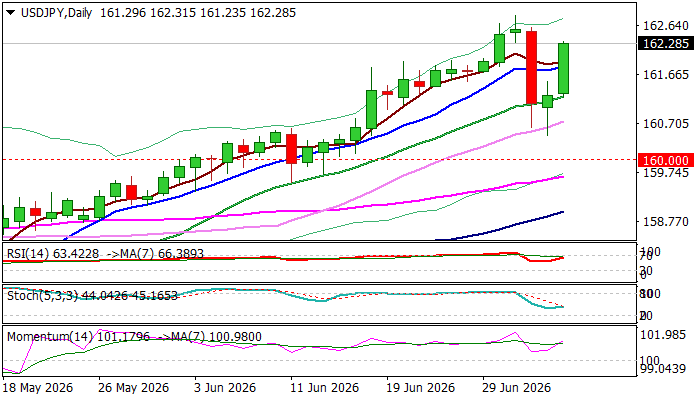

USDJPY – Bulls Regain Control After Limited Correction, Eye Multi-Decade Peak

Strong rise in early Monday trading is about to fully reverse last week’s 162.84/160.47 pullback, which marked a healthy correction (contained by Fibo 23.6% of 155.02/162.84 upleg) of larger uptrend.

Completion of reversal pattern on daily chart confirms scenario as traders entered fresh longs at better levels, encouraged by absence of real action from Japan’s authorities, although they kept expressing their readiness to intervene, almost daily.

The latest correction has improved technical picture, as daily studies returned to full bullish setup and opened space for fresh advance and possible retest of multi-decade peak at 162.84, hit last week and possible extension into the zone, last traded in 1986.

However, traders remain cautious on persisting intervention threats and await release of FOMC minutes (due on Wednesday) for more details about Fed’s stance on interest rates, following recent dovish steer from Fed Chair, as well as waning rate hike bets (especially after soft NFP) that may further overshadow bets for September rate hike.

Res: 162.84; 163.57; 164.24; 164.50

Sup: 161.83; 161.24; 161.00; 160.47

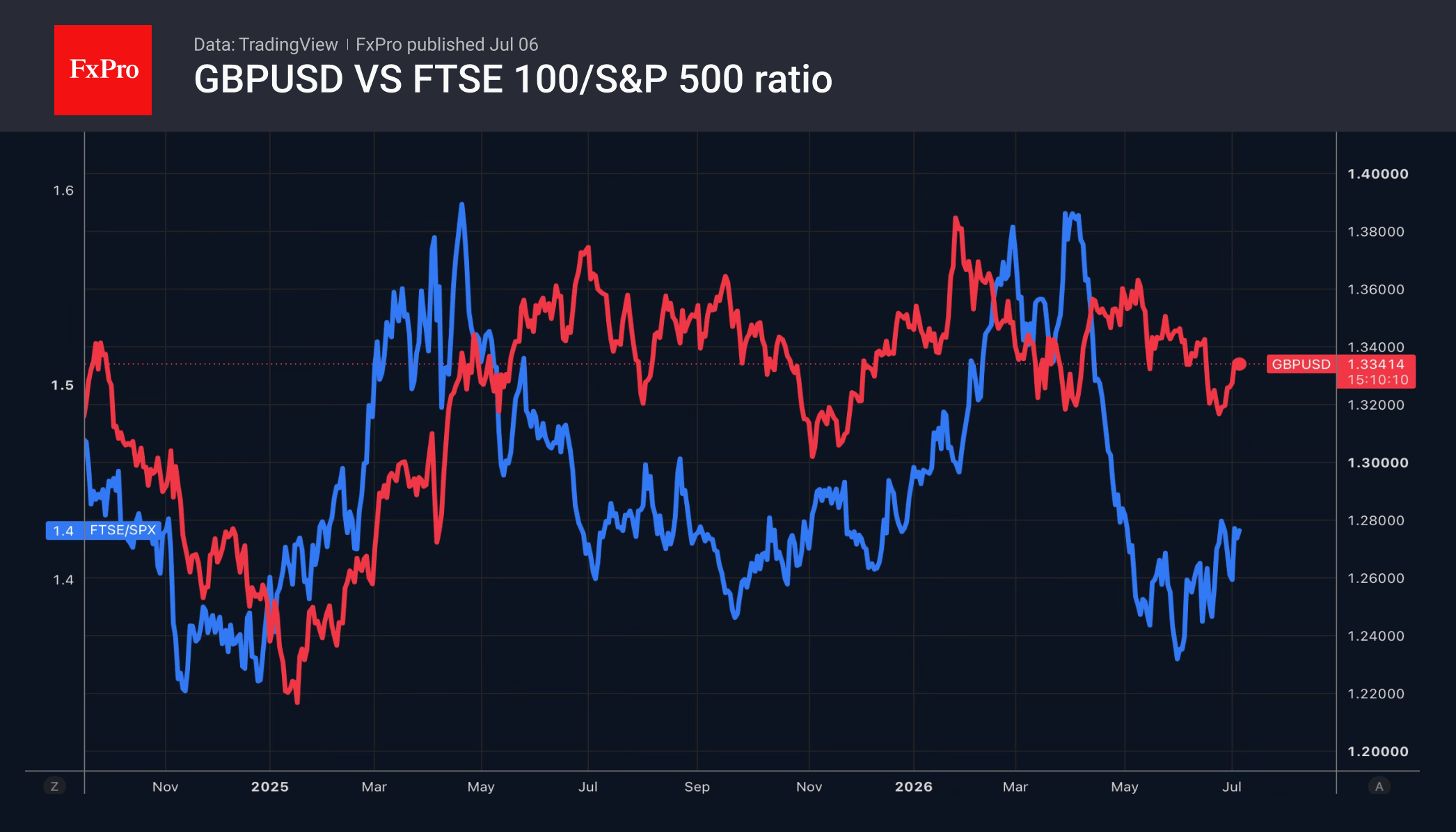

The Pound: Politics Comes to the Rescue

- The stabilisation of the political situation in Britain is driving the GBPUSD rally.

- Traders are wondering: Were there currency interventions in Japan? Or is fear to blame?

The US dollar managed to recover towards the end of its worst week since April, as US equity markets closed ahead of Independence Day. Investors continue to reassess the likelihood of the Fed tightening monetary policy and are preparing to analyse the minutes of the June FOMC meeting. It will be more difficult to identify divisions within the Committee this time round due to the document’s reduced length. Concision is Kevin Warsh’s hallmark.

The greenback’s retreat has given other currencies a chance to shine. The pound has posted its best performance in the last 12 weeks against the backdrop of a stabilising political situation in Britain. In the run-up to his appointment, the incoming Prime Minister, Andy Burnham, is set to adhere to existing fiscal requirements, which reduces the risk premium demanded by investors and boosts demand for domestic assets.

The yen has strengthened at its fastest pace since the currency interventions at the turn of April and May. This has led traders to wonder whether Japan intervened or if speculators were so frightened that they began unwinding their long positions in USDJPY themselves. These positions had reached their highest level since 2017. In such conditions, the triggering of stop-loss orders turns the pair’s decline into an avalanche.

Goldman Sachs has raised its USDJPY forecast from 155 to 165 by mid-2027. The bank believes that the Bank of Japan’s reluctance to tighten monetary policy, high Fed rates and Treasury yields, and the active use of the yen in carry trades will contribute to further weakness in the yen. The 3-month and 6-month forecasts stand at 162 and 163, respectively. US interest rate markets are pricing in a 72% chance that the US dollar will trade at ¥165 by mid next year.

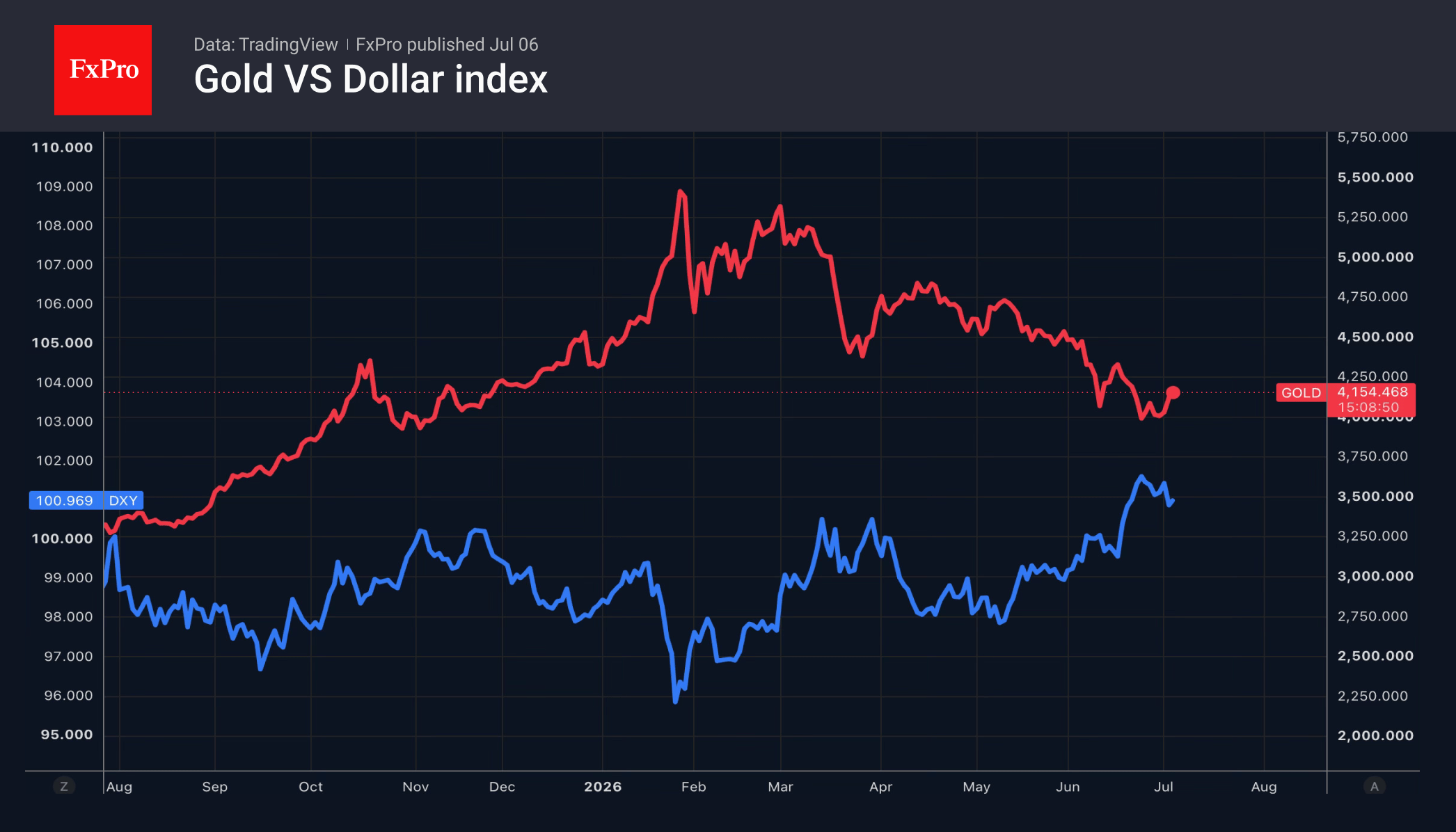

The fall in the USD index and Treasury yields has shifted the balance of power in the gold market. The precious metal briefly returned above $4,200 per ounce but was unable to hold. Bloomberg’s updated forecast suggests that central banks will keep interest rates at high levels for longer than expected due to the delayed impact of the conflict in the Middle East on inflation. Under these circumstances, it will be difficult for Gold to return to the record highs seen at the start of the year.

The FxPro Analyst Team

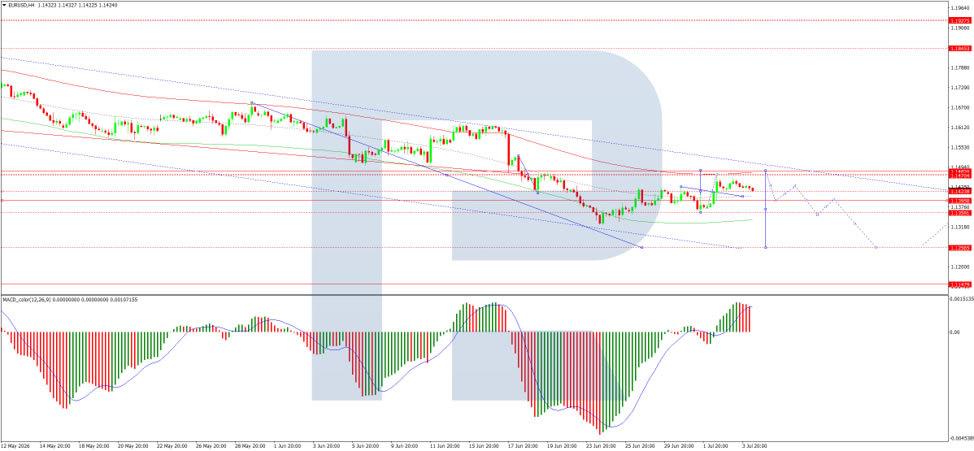

EUR/USD in a Narrow Range: Focus on Fed Minutes

EUR/USD is trading around 1.1432 on Monday. At the end of last week, the main currency pair posted modest gains. Weaker-than-expected US labour market data and lower oil prices have weighed on the US dollar, prompting investors to reconsider expectations for further Federal Reserve policy tightening.

The Non-Farm Payrolls report released last week showed that the US economy added only 57,000 new jobs in June, falling well short of the 110,000 forecast – the weakest result in four months. This outcome has reduced the likelihood of a Fed rate hike as early as September.

An additional factor weighing on the dollar was the decline in oil prices. The restoration of supplies through the Strait of Hormuz, along with expectations of increased OPEC+ production, has raised concerns about a potential global oversupply. This dynamic is helping to reduce inflation risks and the need for further rate increases.

The market's focus this week is on the release of the June Federal Reserve meeting minutes. Investors are hoping for additional signals on the future trajectory of US monetary policy and the outlook for interest rates.

Technical Analysis

On the H4 chart of EUR/USD, the pair is trading within a consolidation range around 1.1422, currently extending between 1.1422 and 1.1470. An upside breakout from this range would suggest a corrective move towards 1.1480, followed by a decline to 1.1260. A downside breakout would open the way for a direct move to 1.1260. The MACD indicator supports this scenario, with its signal line above zero but pointing firmly downwards, reflecting continued bearish momentum.

On the H1 chart, EUR/USD has reached 1.1470 and is now forming a consolidation range below this level. A range expansion down to 1.1408 and up to 1.1480 is expected, followed by a decline to 1.1260. The Stochastic oscillator confirms this scenario, with its signal line at 50 and pointing downwards towards 20.

Conclusion

EUR/USD remains in a narrow range as markets await fresh catalysts, with focus turning to the release of the Fed minutes later this week. Last week's weaker-than-expected US jobs data and falling oil prices have eased pressure on the euro, reducing the likelihood of a September rate hike. The restoration of Hormuz shipments and potential OPEC+ supply increases have further dampened inflation concerns. However, the broader technical picture remains bearish, with indicators pointing towards a potential decline to 1.1260 in the medium term. The Fed minutes will be closely scrutinised for any shifts in the policy outlook that could determine the pair's next directional move.

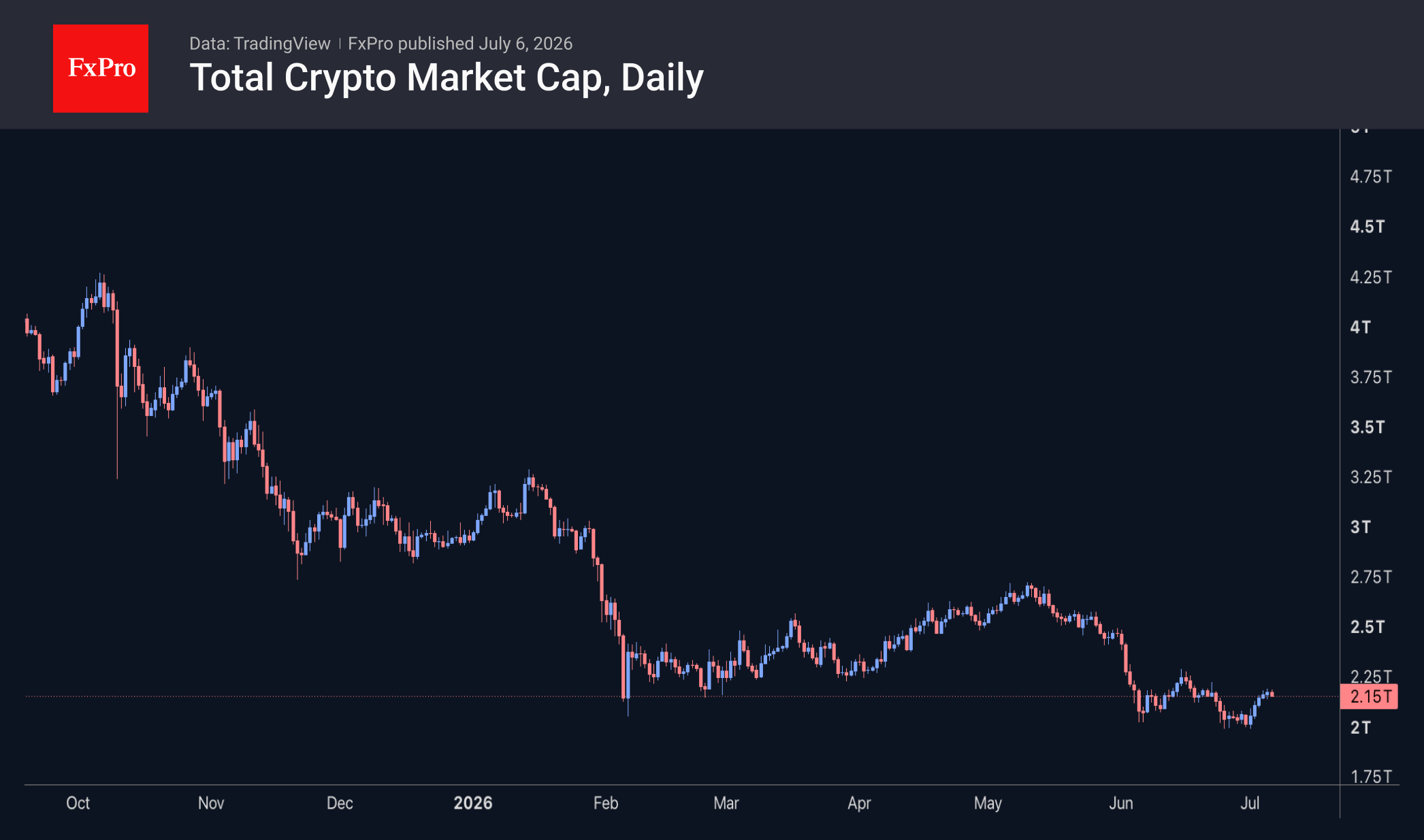

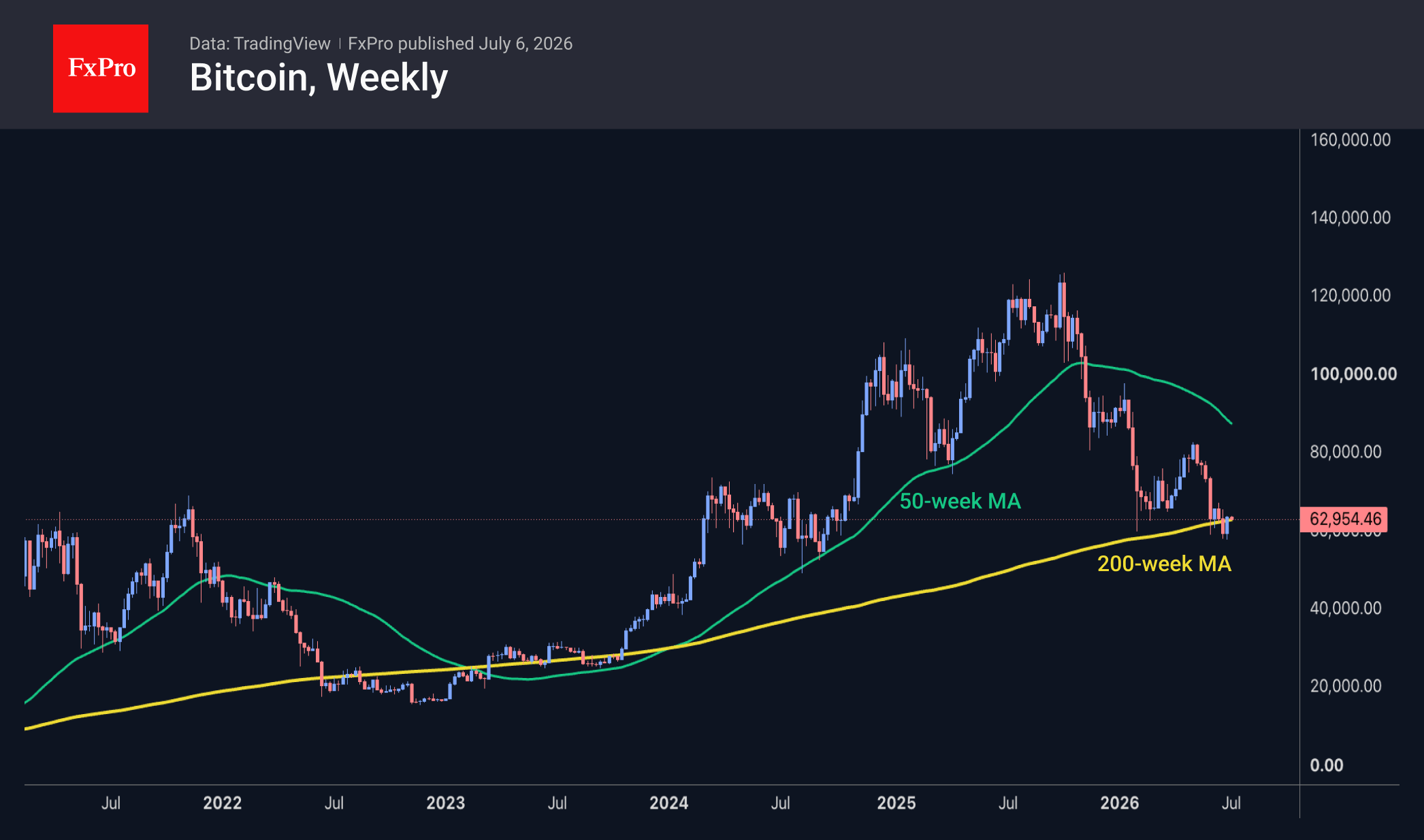

Bitcoin Returns to $63K: Eight Weeks of Outflows from ETFs Are Weighing on

Market Overview

The crypto market capitalisation rose to $2.21T at the start of trading on Monday, but soon corrected to $2.18T, while still up by over 5% from the previous week’s levels. Despite the positive momentum, the situation remains within the bounds of a corrective rebound, having failed to climb even above the region of previous local highs at $2.27T. Without consolidating above this level, the market remains in a downtrend characterised by a sequence of lower highs and lower lows.

The sentiment index has been rising by 1 point per day since 3 July, reaching 24 by the start of 6 July. Remaining in the ‘extreme fear’ zone, the index is now at its highest level in over a month, clearly reflecting the gloomy sentiment.

Bitcoin closed last week near $63K, having recovered to the 200-week moving average, a key historical support level. At its peak on Sunday, the price approached $64K. However, by Monday, the bulls had run out of steam, and the market came under selling pressure once again, pushing the price back by about $1K.

News Background

According to SoSoValue, net outflows from spot BTC ETFs totalled $526.6 million over the shortened week. The negative trend has continued for eight consecutive weeks. Net outflows from ETH-ETFs amounted to a modest $13.7 million for the week.

The volume of deposits in Bitcoin and altcoins on exchanges has risen sharply, which historically signals periods of heightened volatility in the crypto market, CryptoQuant warns. A similar surge was observed before BTC’s decline from $82K in early May to levels below $58K by the end of June.

The current situation in Bitcoin is similar to that of 2022, according to an analyst at Rekt Capital, who expects BTC’s decline to continue. In past crypto cycles, the market bottom was reached approximately one year after the last peak.

The launch of Strategy’s Bitcoin reserve sell-off mechanism has created an “avoidable two-way risk” for the market, according to JPMorgan. The very possibility of such trades increases uncertainty and volatility.

Japanese financial conglomerate SBI has announced the closure of its mining pool. The SBI Crypto platform, which accounts for 2 per cent of the Bitcoin network’s hash rate, will cease operations on 31 July.

Ethereum co-founder Vitalik Buterin outlined the project’s key development areas as part of the Lean Ethereum concept. The focus is on quantum resilience, privacy, scalability and the restructuring of key protocol elements.

The FxPro Analyst Team

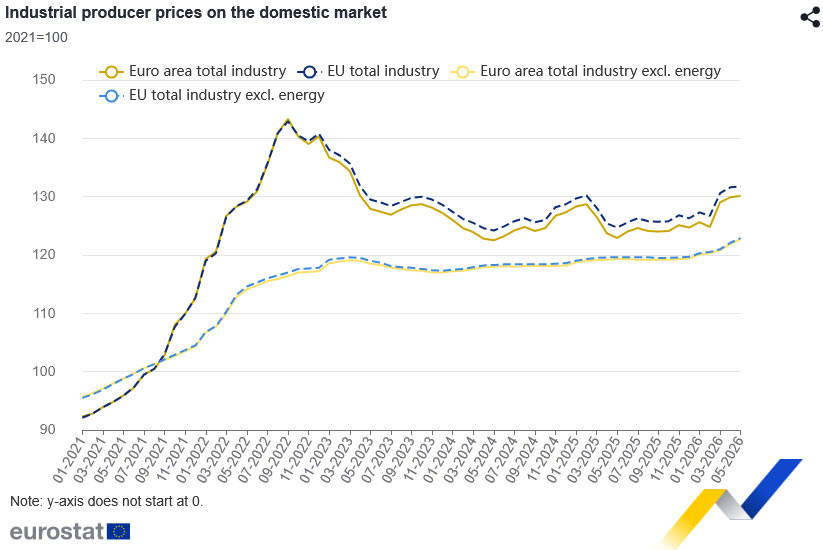

Eurozone Producer Inflation Holds Firm as Core Factory Prices Continue to Rise

Eurozone PPI rose 0.2% mom in May, matching market expectations, while annual producer inflation accelerated from 5.0% yoy to 5.9% yoy, slightly above the 5.7% yoy consensus. The data suggest producer price pressures remained elevated even as monthly price growth moderated from April's 0.7% increase.

The monthly increase reflected diverging trends across sectors. Prices for intermediate goods rose 1.4% mom, providing the strongest upward contribution, while capital goods and durable consumer goods increased 0.2% mom and 0.3% mom, respectively. These gains were partly offset by a -1.0% mom decline in energy prices and a -0.1% mom fall in non-durable consumer goods. Excluding energy, industrial producer prices rose a solid 0.7% mom, pointing to continued underlying pipeline inflation.

Across the broader EU, producer prices also increased 0.2% mom and 5.7% yoy. Cyprus, Ireland and the Netherlands recorded the largest monthly increases, while Croatia, Hungary and Italy posted the biggest declines. On an annual basis, Bulgaria, Romania and Lithuania saw the strongest producer price growth, with Luxembourg the only member state to record a year-on-year decline.

Eurozone Producer Price Index (PPI) — May 2026

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| PPI (MoM) | 0.7% | 0.2% | 0.2% |

| PPI (YoY) | 5.0% | 5.9% | 5.7% |

Eurozone PPI Breakdown (Month-on-Month)

| Category | Monthly Change |

|---|---|

| Intermediate Goods | 1.4% |

| Capital Goods | 0.2% |

| Durable Consumer Goods | 0.3% |

| Non-durable Consumer Goods | -0.1% |

| Energy | -1.0% |

| PPI Excluding Energy | 0.7% |

Eurozone PPI Breakdown (Year-on-Year)

| Category | Annual Change |

|---|---|

| Energy | 14.0% |

| Intermediate Goods | 5.5% |

| Durable Consumer Goods | 2.8% |

| PPI Excluding Energy | 2.8% |

| Capital Goods | 2.2% |

| Non-durable Consumer Goods | -0.5% |

EU Member States

| Largest Monthly Increases | MoM | Largest Monthly Declines | MoM |

|---|---|---|---|

| Cyprus | 3.6% | Croatia | -2.1% |

| Ireland | 2.8% | Hungary | -1.3% |

| Netherlands | 1.9% | Italy | -0.5% |

| Highest Annual Increases | YoY | Annual Decline | YoY |

|---|---|---|---|

| Bulgaria | 19.3% | Luxembourg | -3.2% |

| Romania | 13.5% | ||

| Lithuania | 12.3% |

Eurozone Retail Sales Rise 0.2% mom in May as Food Spending Leads Growth

Eurozone retail sales rose 0.2% mom in May, matching market expectations and pointing to continued resilience in consumer spending despite a mixed performance across retail categories. Across the broader EU, retail sales increased a stronger 0.5% mom, suggesting consumer demand remained relatively firm in several member states.

The monthly increase in the Eurozone was driven primarily by food, drinks and tobacco sales, which rose 0.6% mom. Sales of non-food products, excluding automotive fuel, also edged up 0.1% mom. However, purchases of automotive fuel fell -.5% mom, partially offsetting gains elsewhere.

Among EU member states, Cyprus recorded the strongest monthly increase in retail trade at 3.7%, followed by Luxembourg at 3.6% and Poland at 2.4%. In contrast, Estonia posted the largest decline at -2.2%, ahead of Croatia at -2.0%, while Belgium and Lithuania both recorded falls of -0.7%.

| Indicator | Latest | Market Expectation |

|---|---|---|

| Retail Sales (MoM) | 0.2% | 0.2% |

| EU Retail Sales (MoM) | 0.5% | N/A |

Retail Sales Breakdown (Eurozone)

| Eurozone Category | Monthly Change |

|---|---|

| Food, Drinks & Tobacco | 0.6% |

| Non-food Products (ex. Automotive Fuel) | 0.1% |

| Automotive Fuel | -0.5% |

Best & Worst Performing EU Member States

| Strongest Growth | MoM | Largest Declines | MoM |

|---|---|---|---|

| Cyprus | 3.7% | Estonia | -2.2% |

| Luxembourg | 3.6% | Croatia | -2.0% |

| Poland | 2.4% | Belgium | -0.7% |

| Lithuania | -0.7% |

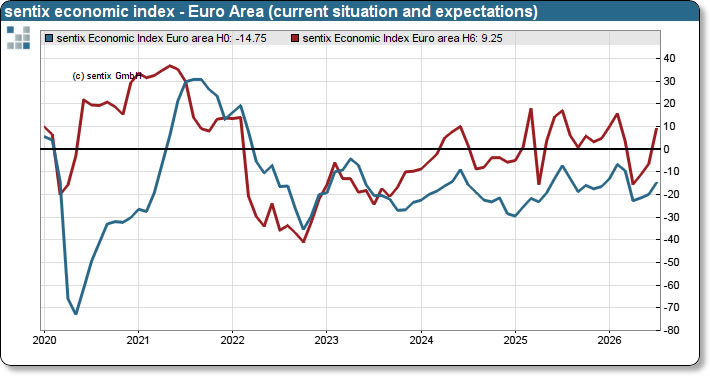

Eurozone Sentix Investor Confidence Surges to -3.1 as Germany’s Recovery Gains Traction

Eurozone investor confidence improved sharply in July, with the Sentix Investor Confidence Index rising from -13.4 to -3.1, marking a third consecutive monthly gain. The improvement was broad-based, with the Current Situation Index climbing from -20.0 to -14.8, while the Expectations Index jumped from -6.5 to 9.3, returning to positive territory as optimism over the region's economic outlook continued to build.

According to Sentix, the recovery is increasingly being driven by Germany, where recently announced policy measures have helped restore investor confidence after months of weak sentiment. While assessments of current conditions remain subdued, expectations improved markedly and turned positive for the first time since March, suggesting investors are becoming more confident that Germany is joining the broader global recovery already underway.

The survey also pointed to easing inflation concerns as falling oil prices following the de-escalation of the Iran conflict reduced pressure on prices. Sentix's inflation barometer improved sharply from -38.0 to -13.75, while its central bank policy gauge also strengthened, indicating investors see less urgency for additional policy tightening. The combination of improving growth expectations and moderating inflation could give the ECB greater flexibility in the months ahead.

| Indicator | Previous | Latest | Comments |

|---|---|---|---|

| Sentix Investor Confidence | -13.4 | -3.1 | Third consecutive increase |

| Current Situation Index | -20.0 | -14.8 | Third consecutive increase |

| Expectations Index | -6.5 | 9.3 | Third consecutive increase; back in positive territory |

S&P 500: Index Narrows Its Range as the Labour Market Cools

The broad US market index, the S&P 500, has entered July against a backdrop of mixed signals from the labour market. The Bureau of Labor Statistics report released on 2 July showed that just 57,000 jobs were added in June, well below market expectations, while the unemployment rate stood at 4.2%. Following the release, markets scaled back expectations of a Federal Reserve rate hike in September, although the possibility of an October increase remains. At the same time, the current 10% global tariff is due to expire at the end of July, and markets are gradually pricing in uncertainty surrounding future trade policy decisions.

Technical Outlook

On the four-hour chart, the S&P 500 (SPXm on FXOpen) remains in a consolidation phase following the uptrend that began on 31 March. After peaking near 7,600, the index declined to around 7,250 before forming a symmetrical triangle, with the descending upper trendline and the ascending lower trendline gradually converging. Since the beginning of July, the price has remained above the upper boundary of the current market profile at 7,460, repeatedly testing the triangle's descending trendline but failing to break above it. Resistance is located around 7,580.

The narrowing range has been accompanied by declining volume, with the latest wave of the triangle noticeably quieter than the previous one, a typical feature of a maturing consolidation pattern. The highest concentration of horizontal volume (POC) is located near 7,394, while the lower boundary of the current profile sits around 7,300. Should the index move lower, these areas could provide support before any attempt to break below the ascending side of the triangle and potentially reach the 7,260 support level. The RSI + MAs indicator currently reads 59, 57 and 55. Although all three values remain above the neutral zone, they do not yet indicate a clear directional bias.

Summary

The POC zone remains the key reference point if the rejection from the triangle boundary develops into a broader decline. Meanwhile, the RSI + MAs indicator continues to hold above neutral without showing a strong trend. Looking ahead, tariff-related uncertainty may become the more significant driver for the index over the coming weeks, as the expiry of the current 10% global tariff at the end of July could trigger a shift in market sentiment.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Finds Support at $4,000, but Only Softer Inflation Can Fuel the Next Rally

Gold found its footing above $4,000 after June's disappointing US payrolls report triggered broad-based Dollar selling and eased expectations for a near-term Fed rate hike. But the rebound is already losing momentum this week. The reason is simple: while payrolls surprised on the downside, the Fed's bigger concern is not employment—it's inflation.

The post-NFP rally illustrated that tension perfectly. Dollar Index slipped to a two-week low near 100.75 after the jobs report, allowing Gold to climb back above $4,200. Yet the move quickly stalled. By Monday, the Dollar was already recovering. Rather than extending higher, Gold struggled to capitalize on last week's softer labor data, suggesting the market has already moved beyond the initial payroll-driven reaction.

The bigger story lies in the Fed's June policy projections. Two weeks before the payroll report, policymakers delivered a meaningful hawkish shift by raising the median 2026 federal funds rate projection from 3.4% to 3.8%. That was more than a routine adjustment. It transformed the committee's central outlook from one additional rate cut to one additional hike. Nine officials now expect rates to rise further, eight see policy staying unchanged, and only one continues to project another cut.

Against that backdrop, one weak employment report was never likely to overturn the Fed's broader inflation narrative. Markets have delayed expectations for the next hike from September toward December, but they have not abandoned the idea altogether. As long as investors continue to believe the next policy move is more likely to be another hike than a cut, Gold will struggle to build a sustained rally.

That is why this week's ISM Services PMI and Wednesday's FOMC minutes may have only limited influence. They can shape short-term sentiment, but neither is likely to change the market's broader view of Fed policy. The more important event arrives on July 14, when the June CPI report will provide the clearest evidence yet of whether the Fed's inflation concerns are justified.

The stakes are unusually high. The June Summary of Economic Projections lifted the Fed's forecasts for 2026 headline and core PCE inflation sharply higher, while May CPI had already accelerated to 4.2%. If June inflation surprises to the upside, policymakers will have fresh evidence that inflation pressures are proving more persistent than hoped. That would reinforce expectations for another rate hike, supporting the Dollar and Treasury yields while limiting Gold's upside. On the other hand, a softer CPI report would undermine the Fed's inflation thesis and could finally give Gold the catalyst needed to break convincingly above recent resistance.

Until that verdict arrives, Gold may struggle to escape its current range. The market appears caught between two competing narratives: a labor market that is gradually cooling and a central bank that is still more worried about inflation than growth. Without clearer evidence that inflation is easing, the recent rebound risks becoming little more than a pause within a broader decline.

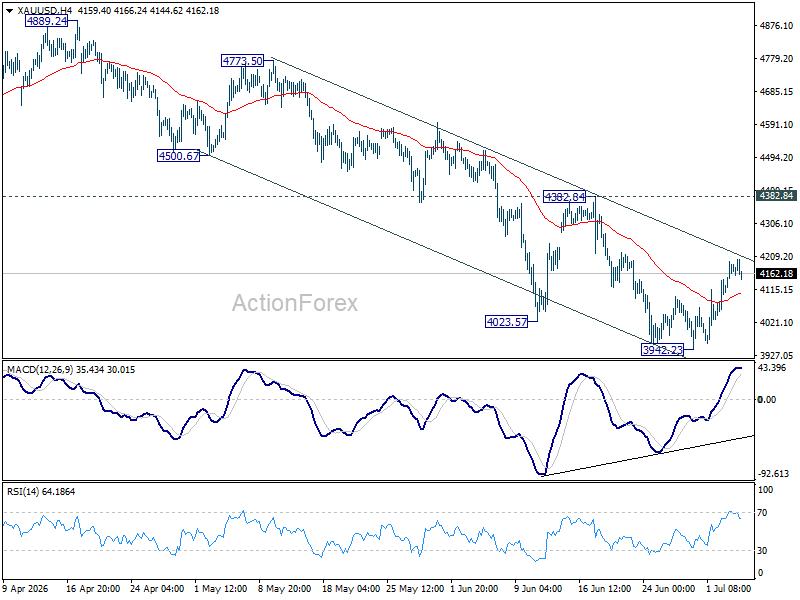

Technically, Gold appears to have established a short-term floor at 3942.23, supported by bullish convergence on 4H MACD. Additional consolidation is possible in the near term, but the broader outlook remains bearish while 4,382.84 caps the recovery. Failure there would keep the downtrend from 5,598.38 intact and maintain the risk of another decline through 3,942.23 toward the 50% retracement of 1,614.60 to 5,998.38 at 3,606.49.

Even so, the daily chart also shows bullish convergence developing on the MACD, suggesting downside momentum is gradually fading. Decisive break above 4382.84, followed by sustained trading above the 55 D EMA, now at 4364.94, would provide the first meaningful evidence that a medium-term trend reversal is underway, opening the way toward the descending trend line near 4,630.

Sunrise Market Commentary

Markets

The US was busy on Friday observing the Fourth of July so doors were shut. Moves during the European session deserve little more than a nutshell recap: stocks up (0.8%), yields up (2–3.8 bps) and the dollar mostly flat. USD/JPY was an exception with initial yen gains evaporating throughout the day. The Japanese currency is extending losses further this morning, pushing USD/JPY back towards the 162 area. So much for the payrolls-driven relief for JPY. EUR/GBP finished the week (well) below the 0.86 support zone. The technical picture as such has deteriorated (improved for GBP) with the next levels to watch now being around the 0.85 big figure. In the core bond space, our attention for the time being is shifting from the front- to the long end of the curve. ECB policymakers downplayed the probability for a back-to-back rate hike in July, citing the ceasefire and coinciding oil price drop as removing the urgency of such a move. Yet it is interesting to see how long-term inflation expectations (e.g. 10-yr) have recently found a bottom around 2%. It suggests the room for further oil-price-driven declines is limited. Add the public finances narrative and there's enough reason to believe the downside in long-term yields is well protected.

US Treasuries reopen little changed this morning after the weekend festivities. There is little market-relevant news to begin the new week with. The contentious reversal of USA Balogun's suspension appearing on virtually all financial media front pages serves as a case in point. We do note the ongoing rise in long-term Japanese yields. It's pushing the likes of the 10-yr and 20-yr to new multi-decade highs. We'll be looking for this steepening trend to spill over to Europe and the US as well. The US dollar inches higher in technically insignificant trading. The risk backdrop is mixed with some rotation out of the AI sphere. The economic calendar centers around the US services ISM for June. Consensus expects more or less stable sentiment (54.1 from 54.5). Risks, if any, are tilted to the upside with the oil price drop and World Cup potentially causing a boost. A research policy panel in Rome featuring Fed's Waller, ECB's Wunsch and Schnabel is worth mentioning too.

News & Views

According to a budget draft seen by Reuters at the end of last week, Germany plans to lift 2027 net borrowing to more than €203 bn. This compares to a €196.5 bn estimate signaled in April. The previous government in 2024 only borrowed €50.5 bn. The 2027 draft budget reportedly allocates total spending of €555.4 billion, more than the €543.3 billion approved in April. Total investment will be €117.5 bn, about €40 bn more than originally planned. New borrowing in the core budget is reported to increase to €118.7 billion, with €54.9 billion borrowed on top through the infrastructure fund and €30 billion through the special fund for defence approved by former Chancellor Scholz. Core defence spending is set to climb to €109 billion in 2027 from €82 billion in 2026 in the core budget. Adding €11.6 billion in funds for Ukraine and €9.4 billion in other security-related spending, such as civil protection, intelligence and IT security, defence spending rises to €130.1 billion. Reuters reports that the approval of this first draft might take place as soon as today.

At the virtual meeting on Sunday, OPEC+ reviewed the global oil market conditions and outlook. The group decided to further raise output/reduce production restrictions decided in 2023 by 188,000 barrels per day. The production hike will start on August 1. The seven countries of the cartel will again meet on August 2. The impact of the decision on global oil supply still remains highly uncertain, dependent on how much oil regional exporters can ship through the Strait of Hormuz as the US and Iran signed a memorandum of understanding that should lead to a permanent halt of the war in the region. After a protracted decline in the oil price since end of April, the price of a barrel of Brent oil currently stabilizes near $72/b.