Sample Category Title

USD/CAD Weekly Outlook

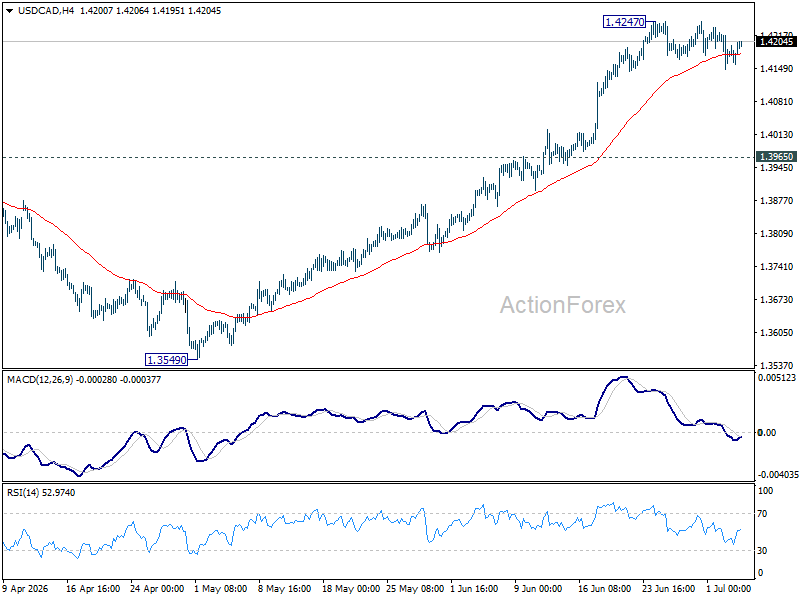

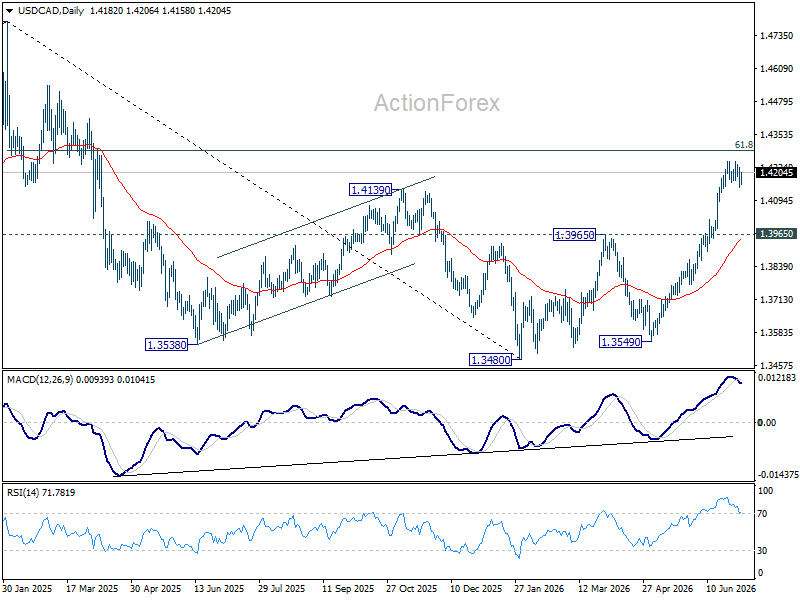

USD/CAD stayed in consolidations below 1.4247 last week and outlook is unchanged. Initial bias remains neutral this week first. While deeper pullback cannot be ruled out, downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

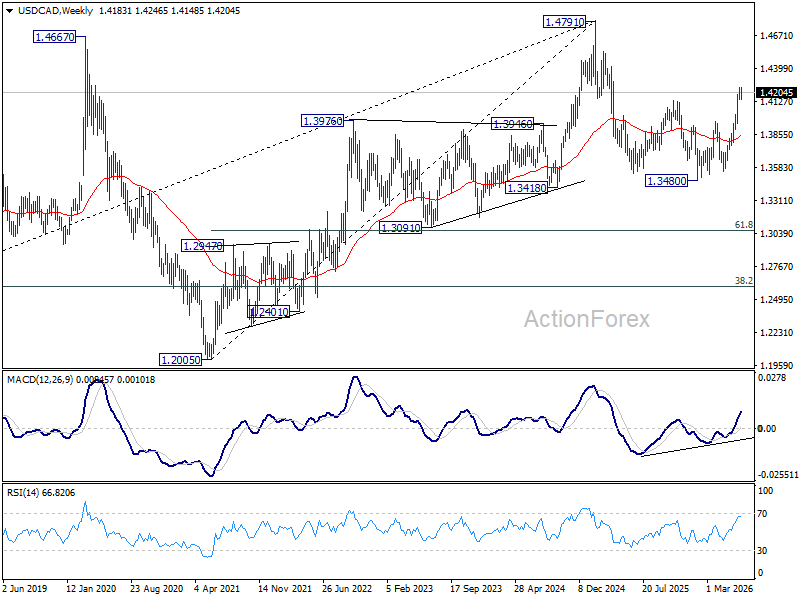

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It's still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.

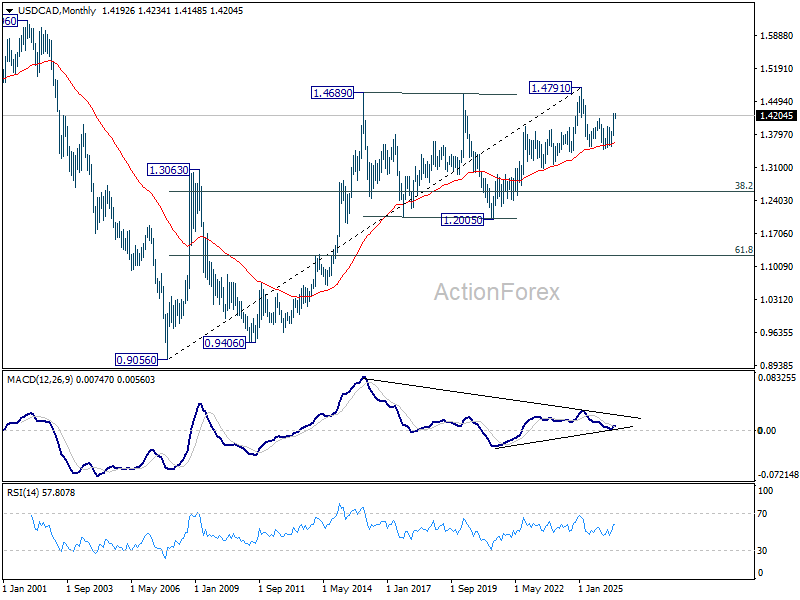

In the long term picture, rising 55 M EMA (now at 1.3631) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

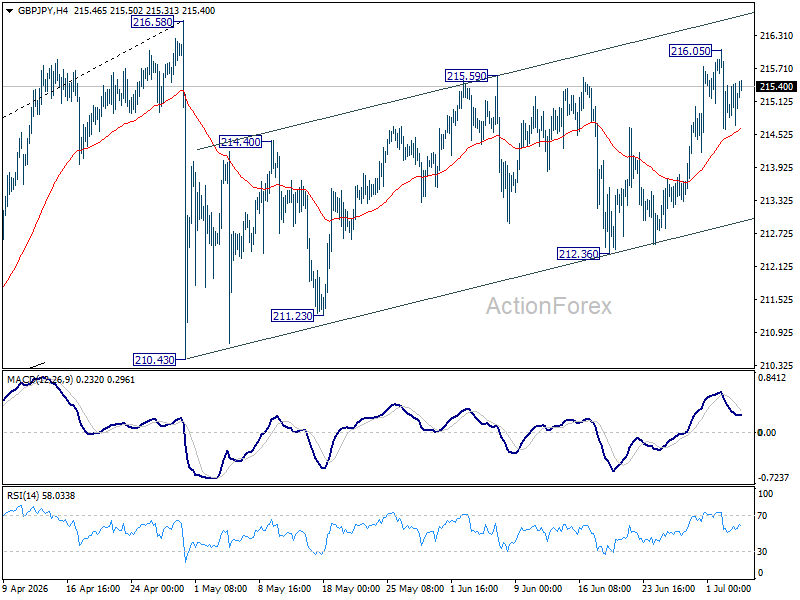

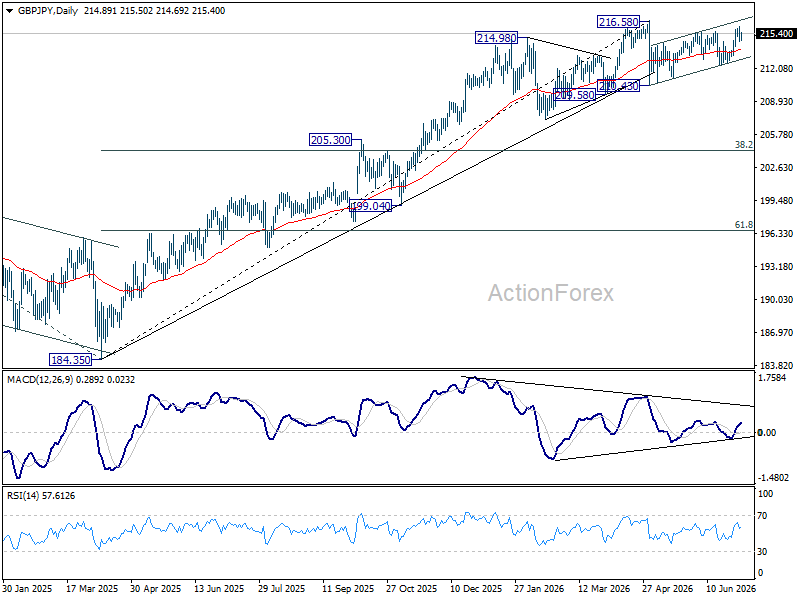

GBP/JPY Weekly Outlook

GBP/JPY edged higher to 216.05 last week but retreated since then. Initial bias remains neutral this week first. On the upside, above 216.05 will extend the rebound from 210.43 to retest 216.58 high. On the downside, break of 212.36 will bring deeper fall back towards 210.43 instead.

In the bigger picture, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 207.57) will argue that it's already in medium term down trend for 184.35 support.

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 188.85) holds.

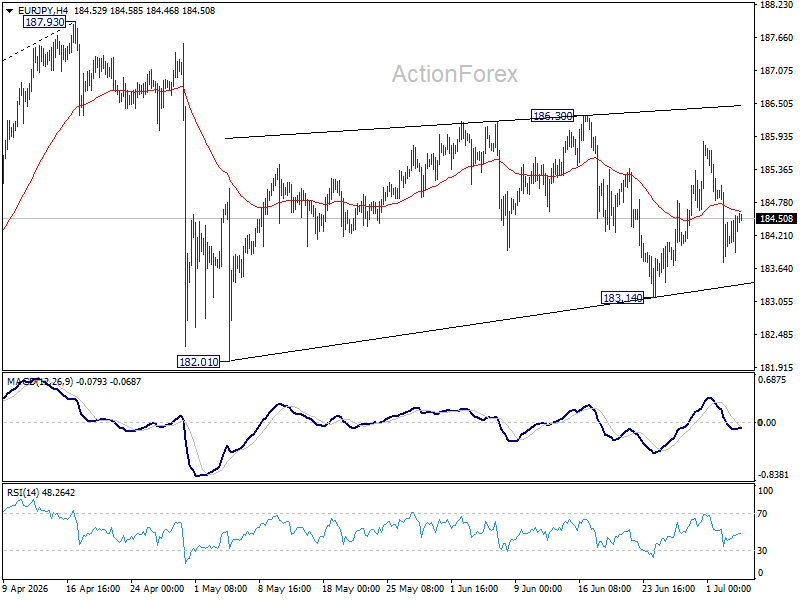

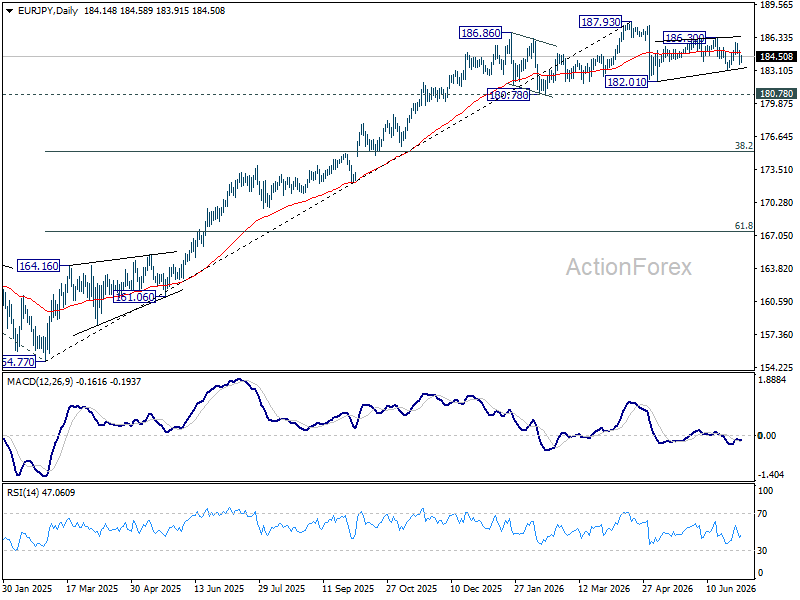

EUR/JPY Weekly Outlook

EUR/JPY stayed in range of 183.14/186.30 last week. Initial bias remains neutral this week first. Risk will stay mildly on the downside as long as 186.30 holds. Below 183.14 will target 182.10 support next. Nevertheless, break of 186.30 will extend the rebound from 182.10 towards 187.93 high.

In the bigger picture, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 179.55) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long 55 W EMA holds.

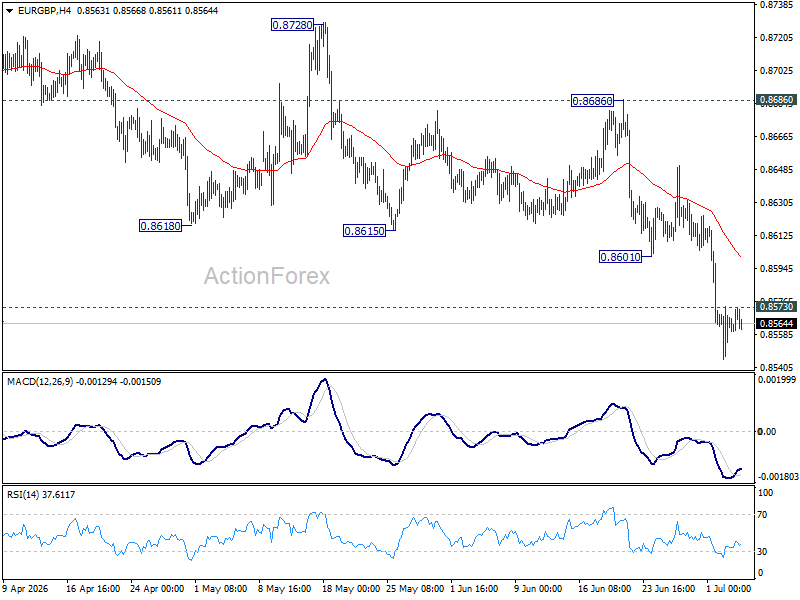

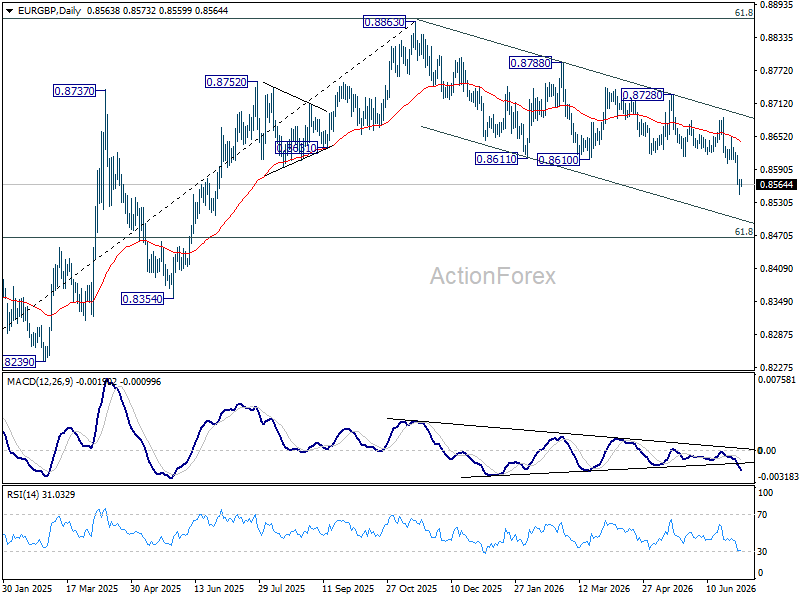

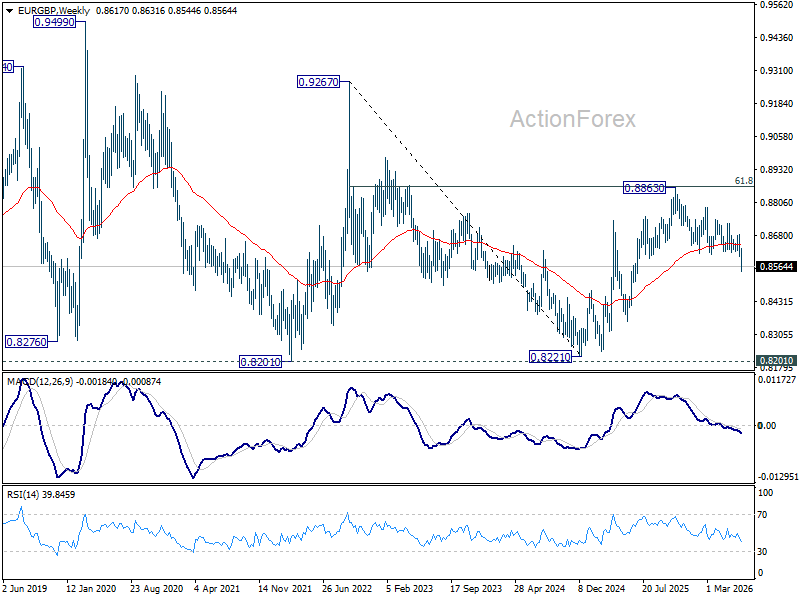

EUR/GBP Weekly Outlook

EUR/GBP's extended decline last week indicate that fall from 0.8663 is reversing whole up trend from 0.8221. Initial remains on the downside this week for 61.8% retracement of 0.8221 to 0.8863 at 0.8466 at next. On the upside, above 0.8573 minor resistance will turn bias neutral first. But risk will stay on the downside as long as 0.8686 resistance holds, in case of recovery.

In the bigger picture, current development suggests that rise from 0.8221 (2024 low) has completed at 0.8863, just ahead of 38.2% retracement of 0.8221 (2024 low) to 0.8863 (2025 high) at 0.8618. Deeper fall would be seen back to 0.8201 (2022 low). For now, outlook will be neutral at best as long as 0.8863 hold.

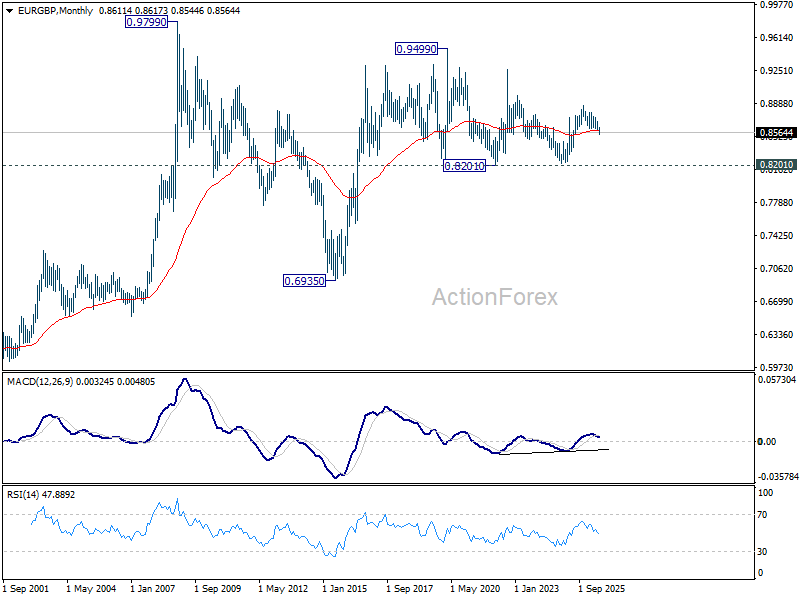

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

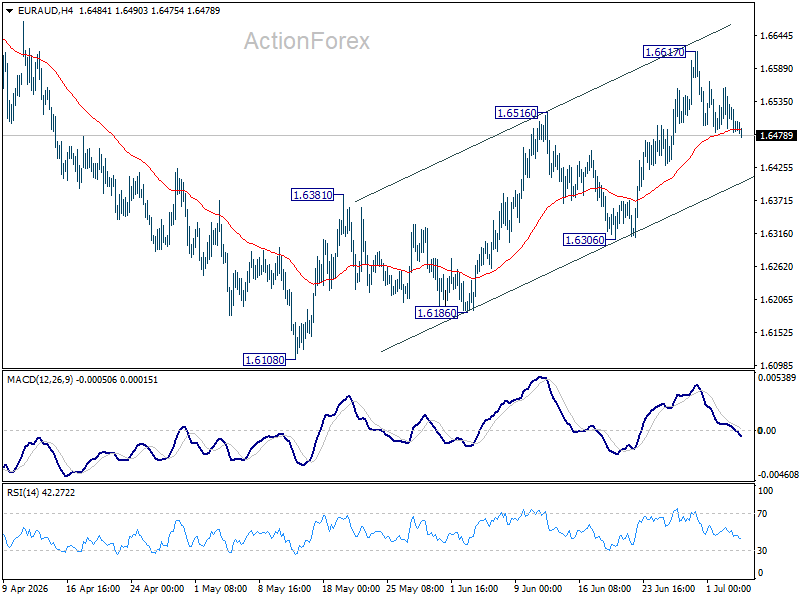

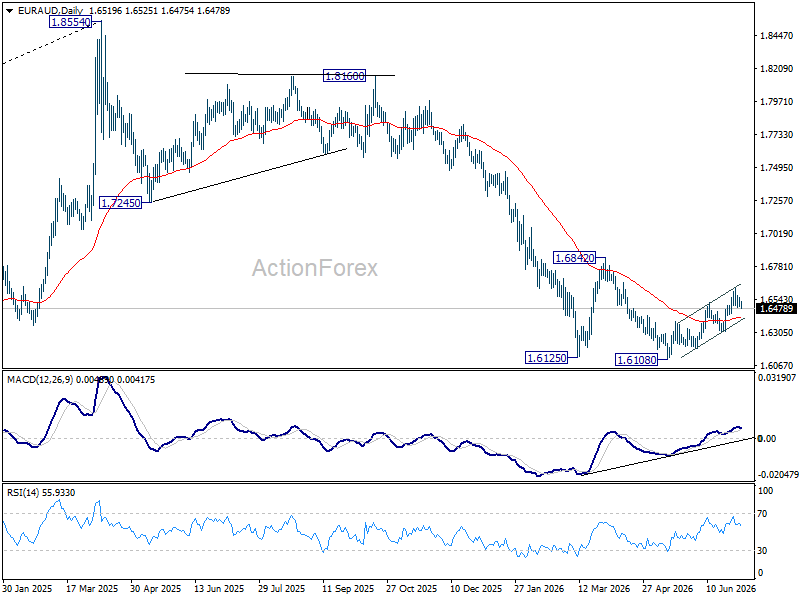

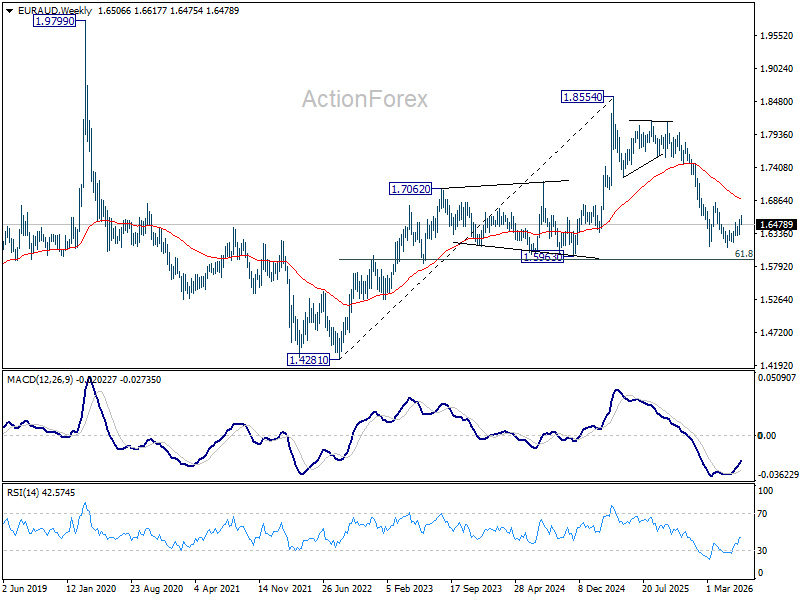

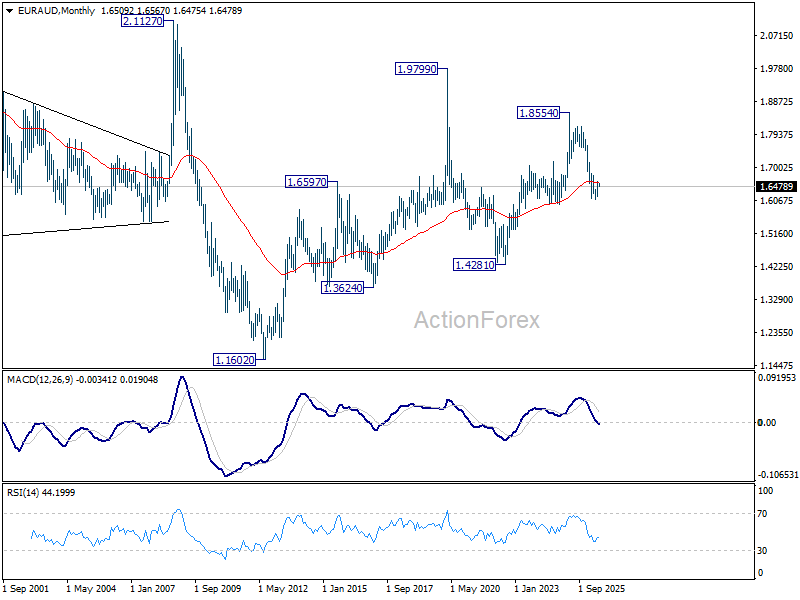

EUR/AUD Weekly Outlook

EUR/AUD edged higher to 1.6617 last week but retreated again. Initial bias remains neutral this week for some consolidations. Further rise is in favor as long as 1.6306 support holds. Above 1.6617 will extend the rebound from 1.6108 towards 1.6842 key structural resistance. However, firm break of 1.6306 will turn bias back to the downside for retesting 1.6108.

In the bigger picture, outlook will stay bearish as long as 1.6842 resistance holds. Fall from 1.8554 (2025 high) is expected to continue to 61.8% retracement of 1.4281 to 1.8554 at 1.5913. Decisive break there will pave the way back to 1.4281 (2022 low). However, firm break of 1.6842 should confirm medium term bottoming, and bring stronger rally.

In the longer term picture, fall from 1.8554 is seen as the third leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Sustained trading below 55 M EMA (now at 1.6577) will confirm this bearish case, and pave the way back towards 1.4281.

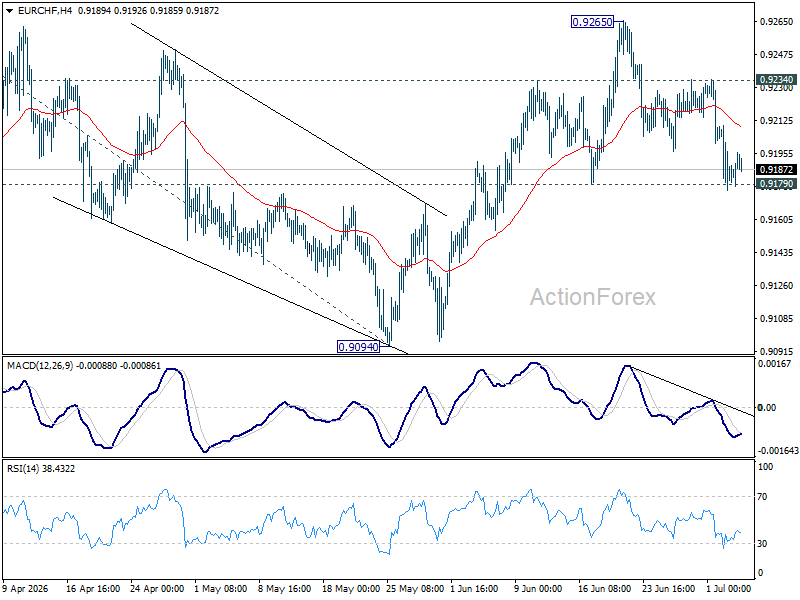

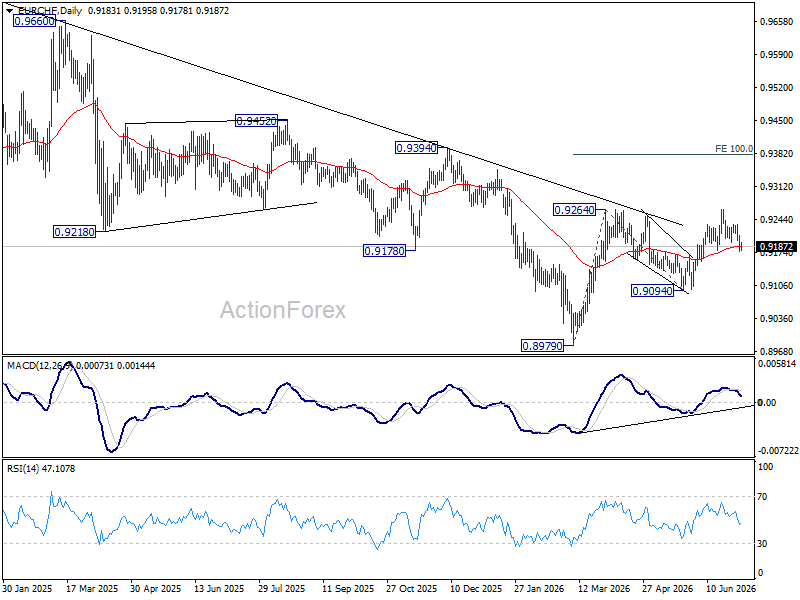

EUR/CHF Weekly Outlook

While EUR/CHF's pullback from 0.9265 extended lower last week, downside is still contained by 0.9179 support. Initial bias remains neutral this week and further rise is in favor. On the upside,a above 0.9234 will bring retest of 0.9265 resistance first. Firm break there will resume the rally from 0.8979 to 100% projection of 0.8979 to 0.9264 from 0.9094 at 0.9379. However, decisive break of 0.9179 will dampen this bullish view, and bring deeper fall back to 0.9094 support.

In the bigger picture, the break of medium term falling trend line resistance indicates that 0.8979 is already a medium term bottom. Considering bullish convergence condition in W MACD, rise from there should at least be reversing the fall from 0.9928, with prospect of developing into a medium term up trend. Firm break of 0.9394 resistance will add more credence to this case. For now risk will remain on the upside as long as 0.9094 support holds, in case of retreat.

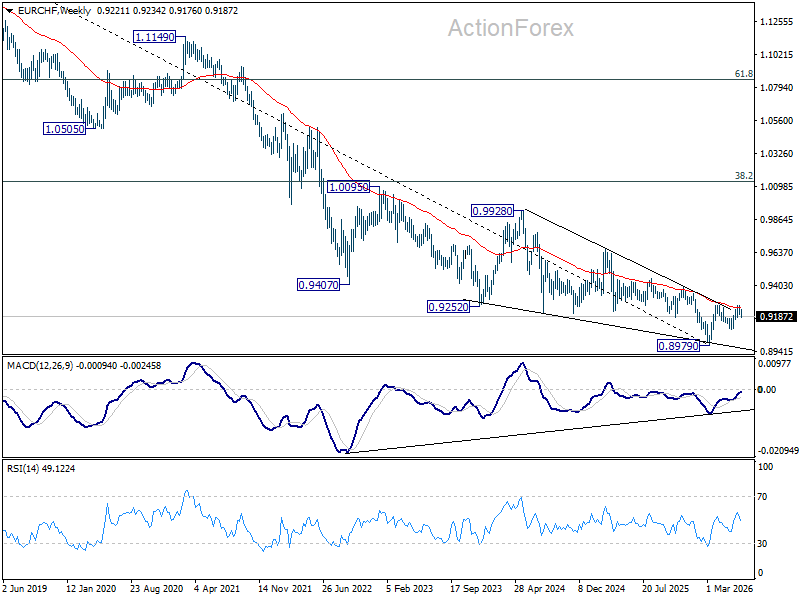

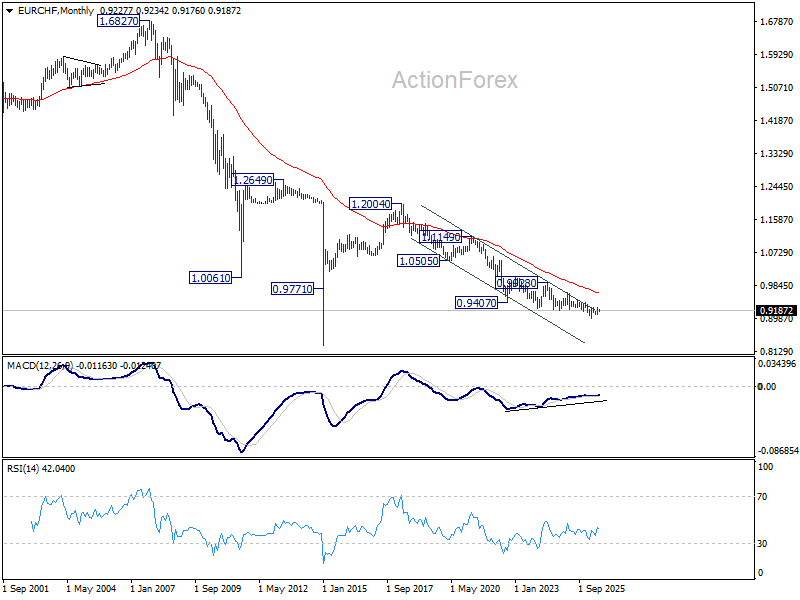

In the long term picture, outlook will stay bearish as long as 0.9407 support turned resistance (2022 low) holds. However, firm break of 0.9407 will argue that the down trend from 1.2004 (2018 high) has completed with five waves down to 0.8979. Stronger rebound should then be seen to 38.2% retracement of 1.2004 to 0.8979 at 1.0135 in the medium term.

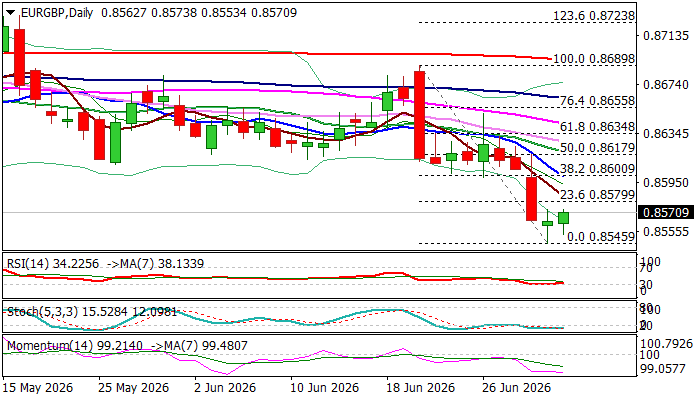

EURGBP – Larger Bears to Take a Breather

EURGBP edges higher on Friday after fresh acceleration lower in past three days failed to clearly break Fibo support at 0.8552 (50% retracement of 0.8239/0.8865 rally, also weekly Ichimoku cloud base) and formed a bear-trap pattern on daily chart that paves the way for recovery.

The Euro remained at the back foot due to significant slowdown in Eurozone economic growth, persisting geopolitical uncertainty and higher energy cost, while sterling received boost from easing political uncertainty and signals that the BoE may keep higher interest rates for some time as inflation remains elevated.

Reversal pattern is developing on daily chart, though still requiring verification on longer bullish daily candle on Friday and daily close minimum above 0.8580 Fibo 23.6% of 0.8689/0.8545 bear-leg).

Significant bullish developments can be seen on hourly chart that contribute to reversal scenario, while daily studies are still mixed (MAs in bearish configuration vs RSI reversing from oversold zone) that way obstruct recovery attempts.

Lift above 0.8580 to expose more significant barrier at 0.8600 (Fibo 38.2% / 10DMA), violation of which to generate stronger bullish signal.

On the other hand, recovery stall under 0.8600 to keep larger bears in play and provide better levels to re-enter bearish market.

Res: 0.8580; 0.8600; 0.8620; 0.8634

Sup: 0.8545; 0.8507; 0.8478; 0.8458

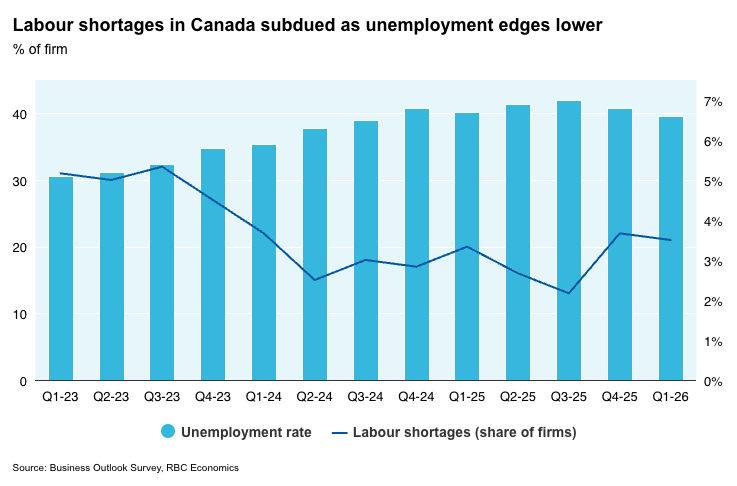

Labour Market and Business Sentiment in Focus as Canada’s Economy Stabilizes

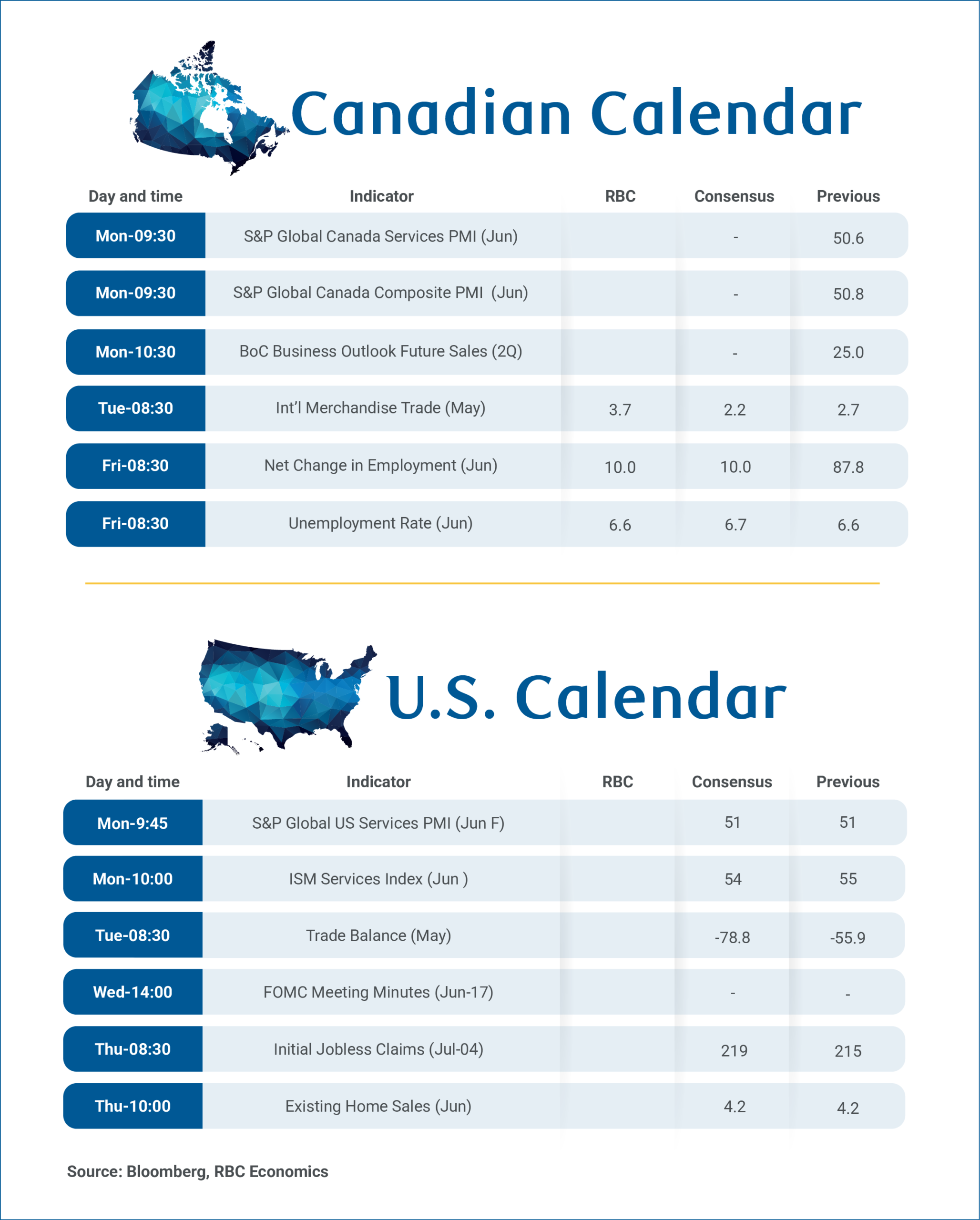

Canada’s employment report next Friday and the Bank of Canada’s Business Outlook Survey on Monday should provide important updates on the balance between labour market conditions, business confidence and inflation expectations.

We expect June’s labour market to broadly hold onto gains in the prior month that retraced much of the weak data over the first four months of the year. We look for jobs to edge higher by 10,000, and the unemployment rate to remain at 6.6% in June, matching May’s reading and down from 6.9% in April.

Unemployment is still elevated by historical standards, and volatile from month-to-month, but has mostly edged gradually lower since hitting a peak of 7.1% in August/September last year. We continue to expect a gradual improvement over the remainder of 2026.

Wage growth will also remain on the radar after slowing sharply in May. Monthly readings can be volatile, but a still-elevated unemployment rate should continue to keep underlying wage pressures contained in the near term.

Looking ahead, job growth is expected to remain soft, but an unprecedented pullback in Canada’s population is shrinking the labour force with per-worker labour market conditions showing more signs of improvement.

Business Outlook Survey to hint at confidence during oil price shock

The Q2 Business Outlook Survey will provide an early look at how business sentiment was impacted by the surge in energy prices in recent months. Survey responses were (at least initially) likely collected largely in May when oil prices were higher (West Texas Intermediate oil prices averaged just under US$100/barrel compared to under $70/bbl recently).

Results will still be reviewed for signs on whether inflation pressures broadened. But longer-term inflation expectations should remain well anchored as underlying pressures have continued to track close to the BoC's 2% target.

Measures of expected future sales, employment, and business investment intentions will also be key after showing signs of improvement in the Q1.

Continued labour market stabilization alongside broadly steady business sentiment and well-anchored inflation expectations would reinforce the view that interest rate changes are not needed at this stage.

May trade data will also be released on Tuesday. We expect exports to rise 0.6%, slowing from 1.6% in April, while imports are expected to edge down 0.8%. Softer energy price growth in May should temper the energy trade balance, while softer motor vehicle shipments suggest some moderation in auto trade.

Summary 7/6 – 7/10

Monday, Jul 6, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 01:00 | AUD | TD-MI Inflation Gauge M/M Jun | -0.30% | |

| 06:00 | EUR | Germany Factory Orders M/M May | 1.10% | -3.80% |

| 08:00 | CHF | Unemployment Rate Jun | 3.10% | 3.10% |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jul | -8.9 | -13.4 |

| 08:30 | GBP | Construction PMI Jun | 40.1 | 38.2 |

| 09:00 | EUR | Eurozone Retail Sales M/M May | 0.20% | -0.40% |

| 09:00 | EUR | Eurozone PPI M/M May | 0.20% | 0.60% |

| 09:00 | EUR | Eurozone PPI Y/Y May | 5.70% | 4.90% |

| 13:45 | USD | Services PMI Jun F | 51.4 | 51.3 |

| 14:00 | USD | ISM Services PMI Jun | 54.2 | 54.5 |

| 14:00 | USD | ISM Services Prices Paid Jun | 71.3 | |

| 14:00 | USD | ISM Services Employment Index Jun | 47.9 |

| 01:00 | AUD |

| TD-MI Inflation Gauge M/M Jun | |

| Consensus | |

| Previous | -0.30% |

| 06:00 | EUR |

| Germany Factory Orders M/M May | |

| Consensus | 1.10% |

| Previous | -3.80% |

| 08:00 | CHF |

| Unemployment Rate Jun | |

| Consensus | 3.10% |

| Previous | 3.10% |

| 08:30 | EUR |

| Eurozone Sentix Investor Confidence Jul | |

| Consensus | -8.9 |

| Previous | -13.4 |

| 08:30 | GBP |

| Construction PMI Jun | |

| Consensus | 40.1 |

| Previous | 38.2 |

| 09:00 | EUR |

| Eurozone Retail Sales M/M May | |

| Consensus | 0.20% |

| Previous | -0.40% |

| 09:00 | EUR |

| Eurozone PPI M/M May | |

| Consensus | 0.20% |

| Previous | 0.60% |

| 09:00 | EUR |

| Eurozone PPI Y/Y May | |

| Consensus | 5.70% |

| Previous | 4.90% |

| 13:45 | USD |

| Services PMI Jun F | |

| Consensus | 51.4 |

| Previous | 51.3 |

| 14:00 | USD |

| ISM Services PMI Jun | |

| Consensus | 54.2 |

| Previous | 54.5 |

| 14:00 | USD |

| ISM Services Prices Paid Jun | |

| Consensus | |

| Previous | 71.3 |

| 14:00 | USD |

| ISM Services Employment Index Jun | |

| Consensus | |

| Previous | 47.9 |

Tuesday, Jul 7, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y May | 3.40% | 3.50% |

| 23:30 | JPY | Overall Household Spending Y/Y May | -2.20% | -0.50% |

| 05:00 | JPY | Leading Economic Index May P | 116.9 | 116.1 |

| 06:00 | EUR | Germany Industrial Production M/M May | 0.40% | 0.40% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 711B | |

| 12:30 | CAD | Trade Balance (CAD) May | 2.8B | 2.7B |

| 12:30 | USD | Trade Balance (USD) May | -78.8B | -55.9B |

| 14:00 | CAD | Ivey PMI Jun | 59.1 | 58.2 |

| 23:30 | JPY |

| Labor Cash Earnings Y/Y May | |

| Consensus | 3.40% |

| Previous | 3.50% |

| 23:30 | JPY |

| Overall Household Spending Y/Y May | |

| Consensus | -2.20% |

| Previous | -0.50% |

| 05:00 | JPY |

| Leading Economic Index May P | |

| Consensus | 116.9 |

| Previous | 116.1 |

| 06:00 | EUR |

| Germany Industrial Production M/M May | |

| Consensus | 0.40% |

| Previous | 0.40% |

| 07:00 | CHF |

| Foreign Currency Reserves (CHF) Jun | |

| Consensus | |

| Previous | 711B |

| 12:30 | CAD |

| Trade Balance (CAD) May | |

| Consensus | 2.8B |

| Previous | 2.7B |

| 12:30 | USD |

| Trade Balance (USD) May | |

| Consensus | -78.8B |

| Previous | -55.9B |

| 14:00 | CAD |

| Ivey PMI Jun | |

| Consensus | 59.1 |

| Previous | 58.2 |

Wednesday, Jul 8, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jun | 5.80% | 5.70% |

| 02:00 | NZD | RBNZ Interest Rate Decision | 2.25% | 2.25% |

| 05:00 | JPY | Eco Watchers Survey: Current Jun | 44.6 | 43.6 |

| 14:00 | USD | Wholesale Inventories May F | 0.30% | 0.30% |

| 14:30 | USD | Crude Oil Inventories (Jul 3) | -1.9M | -3.8M |

| 18:00 | USD | FOMC Minutes |

| 23:50 | JPY |

| Bank Lending Y/Y Jun | |

| Consensus | 5.80% |

| Previous | 5.70% |

| 02:00 | NZD |

| RBNZ Interest Rate Decision | |

| Consensus | 2.25% |

| Previous | 2.25% |

| 05:00 | JPY |

| Eco Watchers Survey: Current Jun | |

| Consensus | 44.6 |

| Previous | 43.6 |

| 14:00 | USD |

| Wholesale Inventories May F | |

| Consensus | 0.30% |

| Previous | 0.30% |

| 14:30 | USD |

| Crude Oil Inventories (Jul 3) | |

| Consensus | -1.9M |

| Previous | -3.8M |

| 18:00 | USD |

| FOMC Minutes | |

| Consensus | |

| Previous | |

Thursday, Jul 9, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ PMI Jun | 49.9 | |

| 23:01 | GBP | RICS Housing Price Balance Jun | -34% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Jun | 2.50% | |

| 01:30 | CNY | CPI M/M Jun | -0.10% | |

| 01:30 | CNY | CPI Y/Y Jun | 1.20% | 1.20% |

| 01:30 | CNY | PPI Y/Y Jun | 4.10% | 3.90% |

| 06:00 | JPY | Machine Tool Orders Y/Y Jun | 37.40% | |

| 06:00 | EUR | Germany Trade Balance (EUR) May | 14.2B | 14.5B |

| 12:30 | USD | Initial Jobless Claims (Jul 3) | 210K | 215K |

| 14:00 | USD | Existing Home Sales Jun | 4.20M | 4.17M |

| 14:30 | USD | Natural Gas Storage (Jul 3) | 87B |

| 22:30 | NZD |

| BusinessNZ PMI Jun | |

| Consensus | |

| Previous | 49.9 |

| 23:01 | GBP |

| RICS Housing Price Balance Jun | |

| Consensus | |

| Previous | -34% |

| 23:50 | JPY |

| Money Supply M2+CD Y/Y Jun | |

| Consensus | |

| Previous | 2.50% |

| 01:30 | CNY |

| CPI M/M Jun | |

| Consensus | |

| Previous | -0.10% |

| 01:30 | CNY |

| CPI Y/Y Jun | |

| Consensus | 1.20% |

| Previous | 1.20% |

| 01:30 | CNY |

| PPI Y/Y Jun | |

| Consensus | 4.10% |

| Previous | 3.90% |

| 06:00 | JPY |

| Machine Tool Orders Y/Y Jun | |

| Consensus | |

| Previous | 37.40% |

| 06:00 | EUR |

| Germany Trade Balance (EUR) May | |

| Consensus | 14.2B |

| Previous | 14.5B |

| 12:30 | USD |

| Initial Jobless Claims (Jul 3) | |

| Consensus | 210K |

| Previous | 215K |

| 14:00 | USD |

| Existing Home Sales Jun | |

| Consensus | 4.20M |

| Previous | 4.17M |

| 14:30 | USD |

| Natural Gas Storage (Jul 3) | |

| Consensus | |

| Previous | 87B |

Friday, Jul 10, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:50 | JPY | PPI M/M Jun | 0.30% | 0.90% |

| 23:50 | JPY | PPI Y/Y Jun | 6.80% | 6.30% |

| 06:00 | EUR | Germany CPI M/M Jun F | -0.30% | -0.30% |

| 06:00 | EUR | Germany CPI Y/Y Jun F | 2.40% | 2.40% |

| 12:30 | CAD | Net Change in Employment Jun | 10.0K | 87.8K |

| 12:30 | CAD | Unemployment Rate Jun | 6.60% | 6.60% |

| 12:30 | CAD | Building Permits M/M May | 0.50% | -7.60% |

| 23:50 | JPY |

| PPI M/M Jun | |

| Consensus | 0.30% |

| Previous | 0.90% |

| 23:50 | JPY |

| PPI Y/Y Jun | |

| Consensus | 6.80% |

| Previous | 6.30% |

| 06:00 | EUR |

| Germany CPI M/M Jun F | |

| Consensus | -0.30% |

| Previous | -0.30% |

| 06:00 | EUR |

| Germany CPI Y/Y Jun F | |

| Consensus | 2.40% |

| Previous | 2.40% |

| 12:30 | CAD |

| Net Change in Employment Jun | |

| Consensus | 10.0K |

| Previous | 87.8K |

| 12:30 | CAD |

| Unemployment Rate Jun | |

| Consensus | 6.60% |

| Previous | 6.60% |

| 12:30 | CAD |

| Building Permits M/M May | |

| Consensus | 0.50% |

| Previous | -7.60% |

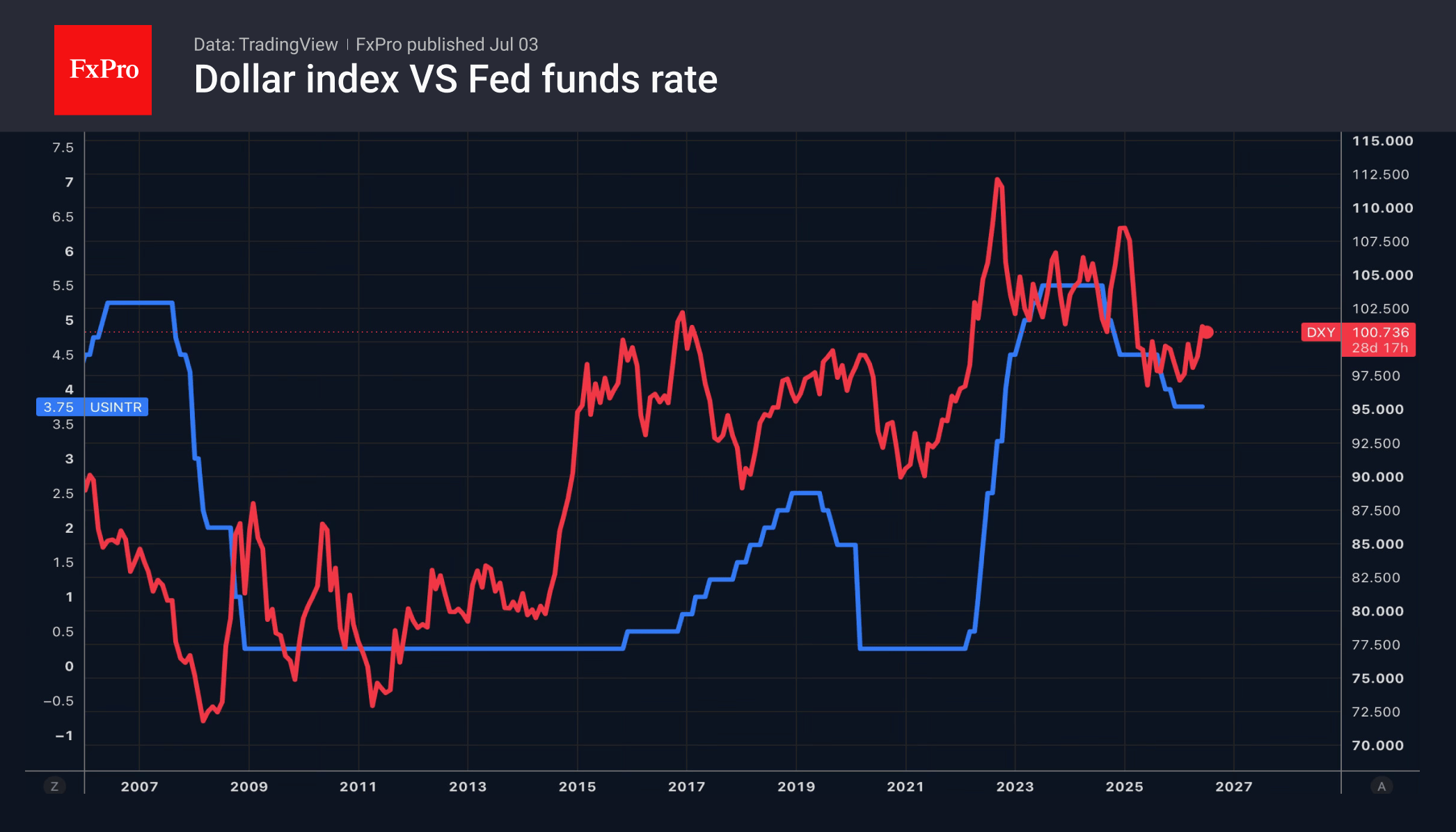

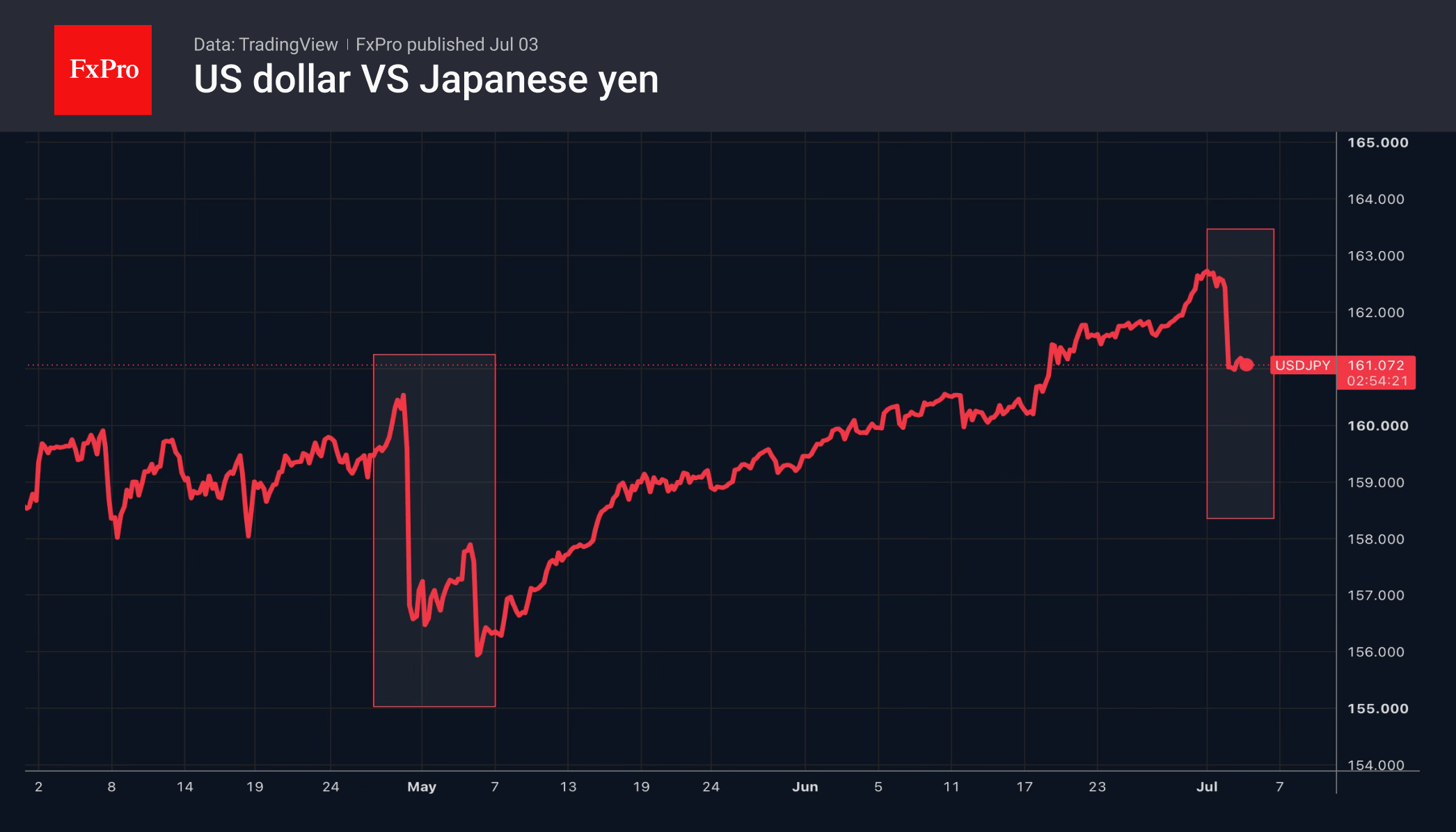

The Dollar: Has the Trend Been Broken?

- The fall in the USD index could mark the beginning of the end.

- Rumours of currency interventions sent USDJPY tumbling.

The US dollar plummeted to a two-week low amid disappointing labour market figures. Non-farm payrolls rose by 57,000 in June and were revised downwards by 74,000 for April and May. The fall in the unemployment rate to 4.2% was due to a reduction in the labour force rather than an acceleration in hiring.

Against the backdrop of these figures, the probability of a rate rise in July fell from 30% to 20% in the markets; the probability of a rise by September fell from 64% to 53%; and the probability of a rise by the end of the year fell from 83% to 78%. This put pressure on the dollar. Earlier, speculators had increased their net long positions in the US currency to a one-and-a-half-year high, making this trade heavily concentrated. Profit-taking became the catalyst for the rise in EURUSD.

According to Credit Agricole, the US dollar appears overbought and overvalued. The Fed may, in fact, not be as ‘hawkish’ as the markets believe. Eurizon SLJ Capital maintains that investors have already squeezed everything they can out of the USD index rally. The positive sentiment has been fully priced in; it is now time to take profits.

TD Securities argues that as global GDP accelerates and risk premiums narrow, the interest rate differential between the US and the rest of the world will narrow, leading to a weakening of the greenback in the second half of the year. The stabilisation of the international situation following turmoil caused by tariffs and the conflict in the Middle East could also trigger a depreciation of the dollar’s exchange rate.

Meanwhile, the sharpest fall in USDJPY since Japan’s currency interventions in April and May has prompted speculation about whether the authorities have resumed such practices. Was there intervention in the forex market, or did speculators’ fears prompt them to close out the short positions of their own accord?

A Reuters report and a speech by Atsushi Mimura triggered the sell-off in USDJPY. The news agency claims that the government has adopted a new tactic: rather than giving a warning of currency interventions, as it did at the end of April, it will now rely on the element of surprise. The chief currency official, the Vice Minister of Finance for International Affairs, stated that the previous intervention was justified, and that the US does not object to, but rather supports, such actions.

The FxPro Analyst Team