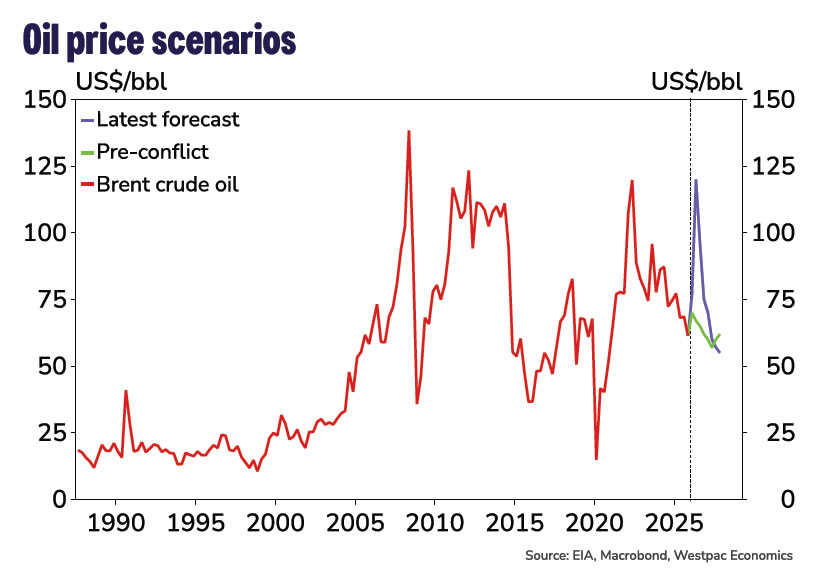

- Longer Middle East disruption lifts peak prices for oil and gas, lengthens recovery. Infrastructure damage exacerbates the shock. Brent oil now expected to peak at an average $120/bbl in Q2 and Japanese LNG prices at $26mmbtu.

- Australian CPI inflation now expected to peak at 5.4%yr in June quarter, and even higher on the monthly series, despite the announced cut to fuel excise. Trimmed mean inflation peaks around 4% in 2026 H2. Food prices a particular concern through to 2028, but broader passthrough to non-energy prices also an issue.

- RBA now expected to hike rates three times (May, June, August), revised up from one more (in May) previously. Peak cash rate now 4.85%, above previous peak.

- Supply shock and tight monetary policy drag on demand, especially consumption and other interest-sensitive sectors. GDP growth forecast to trough at 1%yr in 2027; unemployment rate peaks at 5% end-2026.

Energy situation

As previously highlighted, the key risk to our previous central case view (released on March 17) was that the Middle East conflict would prove to be more prolonged than assumed. With the conflict now entering its fifth week, it has become increasingly clear that the US/Israel–Iran confrontation is likely to result in a longer-lasting disruption to energy production in the Middle East and shipping through the Strait of Hormuz. We have therefore revised our baseline assumptions.

Specifically, we now assume the Strait of Hormuz remains effectively closed until the end of April, a total of eight weeks, and takes longer to reopen fully. This compares with our earlier assumption of a one-month disruption followed by a relatively rapid normalisation.

The slower recovery reflects several factors. Recent shipping traffic through the Strait has been limited to countries Iran deems friendly to it. Insurance premiums are expected to remain elevated given the risk of further attacks by regional factions. Shipping companies will also require time to re-establish vessel rotations and contractual delivery arrangements across energy and upstream industrial inputs.

As a result, we now assume traffic through the Strait reaches only around 20% of normal levels in May. Traffic is expected to continue to improve thereafter, although capacity is not expected to return to normal levels until end 2026.

The extension of the conflict and slower normalisation will lead to more ‘shut-ins’ (temporary stops in production due to storage capacity limits) among smaller Gulf producers. Coupled with some oil infrastructure damage, we now project this to see a shortfall in global oil production of around 6mb/d on average in Q2. This assumes Saudi Arabia and the UAE continue to divert exports via operational pipelines to partially bypass the Strait, with an available capacity at around 1.6–5.5 mbpd, alongside the release of IEA emergency stockpiles.

Risks around this path remain clearly skewed to the downside, particularly if there is more damage to port and energy infrastructure and/or shipping via the Red Sea is also impacted now that Yemen’s Houthi rebels have entered the conflict. This would represent a sharp escalation, but it could also see a faster resolution as it would bring more Gulf state countries into the fray against Iran.

Overall, the changes to our baseline assumptions imply a materially bigger and more persistent energy price shock than previously assumed.

Consequently, we now expect Brent crude oil prices to average around US$120/bbl in Q2, compared with US$90 previously. Prices are expected to remain elevated for longer, reflecting both ongoing physical disruptions and a sustained risk premium linked to security and insurance costs. Under our revised base case, oil prices ease only to around US$75/bbl in Q4, still US$13 above our pre conflict baseline, and do not converge back to pre conflict levels of around US$60/bbl until Q2 2027.

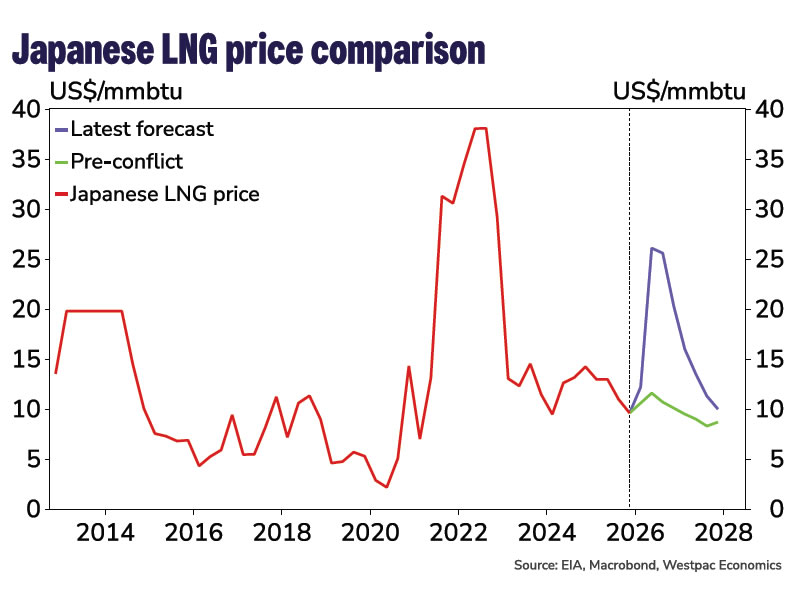

The impact on gas markets is even larger than for crude oil. LNG exports from the Middle East, particularly Qatar, have no viable alternative route that bypasses the Strait, leaving supply highly exposed to an extended disruption. Moreover, Qatar’s Ras Laffan LNG plant has suffered extensive damage halting production, with reports that it will potentially take up to five years to fully repair. As a result, Japanese LNG prices have surged above US$20mmbtu in recent weeks and are currently trading US$10 above pre-conflict levels. We forecast further increases as supply tightens to a quarterly average price of around US$26mmbtu over the next few quarters. Prices are projected to remain elevated even after oil markets begin to stabilise.

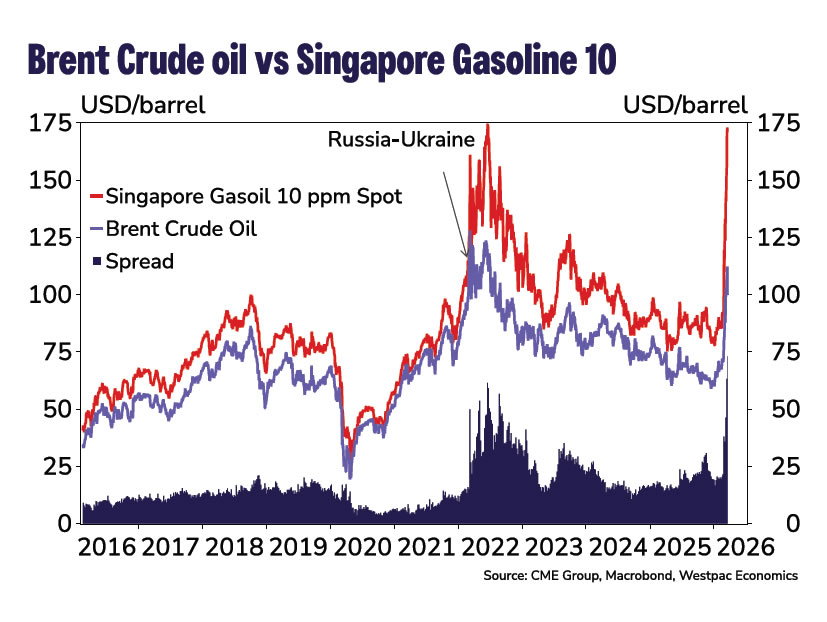

We have also made greater allowance for wider refinery margins than our previous forecasts. Disruptions to crude supply, combined with tight refined product inventories in Asia, have driven a sharp widening in the spread between Brent crude and Singapore Gas10, the key benchmark for Australian petrol and diesel prices. The spread has recently surged to around US$70/bbl, exceeding levels seen following Russia’s invasion of Ukraine. Given the importance of refined product availability and logistics, we expect margins to remain elevated even as the conflict eases, materially amplifying the pass through from higher crude prices to domestic fuel costs.

More acute pressures on supply chains

Given the prolonged closure, we now also assume supply chain pressures are more acute and persistent. Container freight rates have risen by 20% since the start of the conflict, reflecting longer shipping routes, higher fuel costs, insurance surcharges and booking constraints. While freight rates are still lower than the peaks in 2025 and significantly below the extraordinary peaks of 2021–22, Iran is reportedly extracting additional charges from non-hostile vessels negotiating passage through the Strait, further increasing transit costs even where shipping through the Strait is allowed.

The Middle East is also a key upstream supplier of industrial inputs, including fertilisers, chemicals, polymers and metals. Around 33% of global fertiliser trade, particularly urea and ammonia, transits the Strait. Disruptions are already pushing up prices for these inputs, with Egyptian urea prices, a global indicator for fertiliser prices, particularly nitrogen fertilisers, reaching its highest level in more than three years. That said, at around US$475/t, it is still significantly below its record of $1050 following Russia’s invasion of Ukraine.

Globally, manufacturing PMIs show a sharp re-acceleration in input cost growth, with energy, freight and intermediate goods cited as key drivers, alongside some lengthening in supplier delivery times. In Australia, the PMI manufacturing input price measure has risen to its highest level since August 2023.

However, while supply chain pressures are rising and are expected to remain elevated beyond the end of the conflict, they are expected to remain materially below the peak levels experienced in 2021–22. The port congestion, post-COVID reopening surge in demand and broad-based shortages that were features in this episode remain absent. The appreciation of the Australian dollar, both against the US dollar and on a trade weighted basis, will also provide a partial offset to imported cost pressures, reducing the local currency impact of higher global input prices. In contrast, the AUD/USD cross fell by 9% around during the 2022 episode, amplifying the rise in import costs.

Accordingly, while price pressures are rising, particularly for energy-intensive inputs such as fertilisers and aluminium, the impact on producer prices and the flow through to headline and core inflation is expected to be smaller than during the 2022 cost of living crisis.

Inflation impact

Both the Oxford Economics model and our bottom-up forecasts imply that higher energy, freight and upstream input costs are expected to lift headline inflation materially over 2026. The direct impact comes firstly through fuel and transport-related components before it broadens as higher distribution and input costs are passed on to a wider range of consumer prices.

Reacting to this, the Australian Government announced that from April 1, the fuel excise tax will be cut in half, reducing the pump price of petrol and diesel by 26¢/litre. We are now expecting headline CPI to peak at 5.4%yr in Q2 2026, up from 4.1% previously, with monthly inflation likely to be even higher breaking through 6%yr around April or May.

, revised up from one more (in May) previously. Peak cash rate now 4.85%, above previous peak.){kind=link}