Markets open the week in a surprisingly calm tone, but the stability masks a high-stakes setup ahead of US President Donald Trump’s Iran deadline. Investors are not facing a simple binary outcome. Instead, markets are positioned within a three-way risk structure, where the interpretation of escalation—not just escalation itself—will dictate the next move.

Trump’s deadline for Iran to reopen the Strait of Hormuz by April 7, 8pm E.T. has introduced a clear event risk. His warning of strikes on civilian infrastructure, framed as “Power Plant Day,” has raised the stakes significantly. Yet markets are not reacting with panic, suggesting that investors are leaning toward a contained outcome.

The focus is squarely on oil price as the decision trigger. The key thresholds are clear: 120+ in Brent crude as disruption threshold, 90 as resolution signal. Which side breaks will determine whether markets are forced into a deeper repricing.

So far, the tone across assets points to cautious optimism. Stocks in Japan and South Korea are trading higher today, while other regional markets remain closed for holidays. Gold is holding in a narrow range and Bitcoin is recovering modestly. Most notably, oil has stabilized after a brief spike. But there is a critical question: is the bounce in equities the start of a sustainable rally, or simply a “dead cat bounce driven” by positioning? The answer hinges not only on whether escalation occurs, but on how it is interpreted.

At the center of the current positioning is the “Short War” narrative. Some instituationl investors could be betting that any escalation will be intense but contained, with a defined timeline rather than a prolonged conflict. This belief has encouraged dip-buying behavior even as geopolitical risks remain elevated.

Two factors underpin this view:

- First, Trump’s own “2–3 week” timeline has shaped expectations that the conflict could be resolved relatively quickly once key infrastructure targets are addressed. This has created an environment where investors are pricing containment vs disruption, leaning toward the former.

- Second, there is a widespread perception that Iran’s capacity to sustain a prolonged war is limited. While Tehran has rejected the ultimatum and continued strikes across the region, including attacks on Kuwait’s oil facilities, markets appear to assume that escalation will ultimately force a negotiated outcome.

However, this view creates asymmetric risk. If escalation deviates from the short war narrative, markets may be forced into a rapid repricing. In such a scenario, a break above 120 in oil would signal that disruption—not containment—is being priced. That shift would likely trigger a broader risk-off move. Equities would come under pressure, bond yields would rise on inflation concerns, and safe-haven assets would regain traction. The current calm would quickly give way to volatility. Conversely, a de-escalation outcome—such as a reopening of the Strait of Hormuz—would likely send oil back toward 90. This would ease inflation fears, pull yields lower, and support a broader risk-on rally across equities and high-beta currencies.

Currency markets are already reflecting a tentative risk-on bias. Kiwi is leading gains for the day, followed by Aussie and Sterling, while Swiss Franc and Dollar are lagging. This suggests that markets are leaning toward a benign outcome, at least for now. Ultimately, the calm in Asia is less about confidence and more about positioning ahead of a decisive event. Markets are not stable—they are compressed. And as the deadline approaches, oil will determine whether investors’ short war bet holds—or is proven wrong.

Bitcoin Finds Structural Demand Floor on ETF Inflows During War Shock, Eyes 76K

Bitcoin has built a structural demand floor near 60K as ETF-driven inflows return, even amid war-driven volatility. But upside remains capped, with a 70K breakout needed to target 76K, while the 80K zone stands as a major institutional supply wall under higher-for-longer Fed expectations. Read More.

Week Ahead: Critical Inflation Test for Fed as Oil Price Shock Moves from Fear to Data

Markets shift from pricing oil-driven risk to testing real inflation impact as US CPI takes focus. With Brent above $100, the key question is whether rising energy costs are feeding into core prices and forcing a rethink of Fed policy parth. This week’s data could confirm the stagflation trade—or challenge it. Read More.

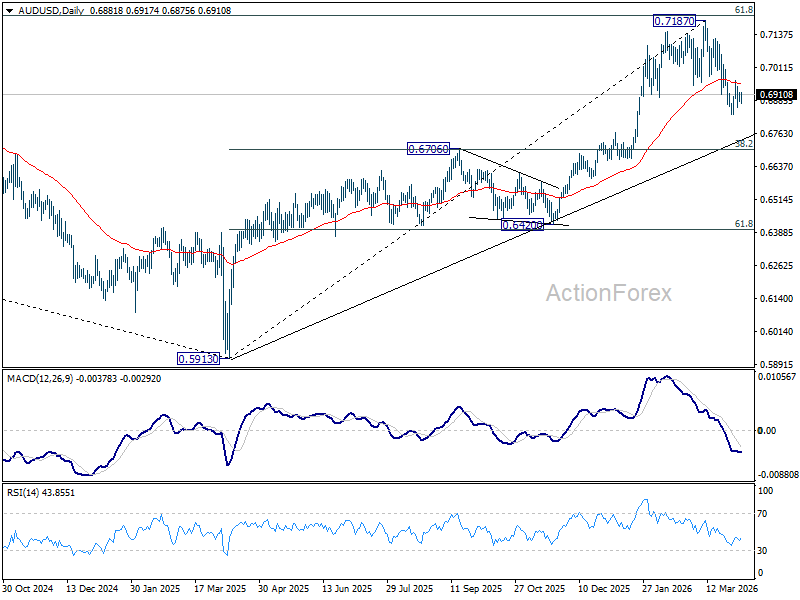

AUD/USD Daily Report

Daily Pivots: (S1) 0.6880; (P) 0.6899; (R1) 0.6913; More...

AUD/USD recovers mildly today but remains bounded in range above 0.6832. Intraday bias remains neutral for the moment. On the downside, below 0.6832 will extend the decline from 0.7187 to 38.2% retracement of 0.5913 to 0.7187 at 0.6700. However, firm break of 0.6978 will argue that the correction has completed, and bring retest of 0.7817 high.

In the bigger picture, as long as 0.6706 cluster support holds, rise from 0.5913 (2024 low) should still be in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it’s already reversing the down trend from 0.8006 (2021 high). However, firm break of 0.6706 will dampen this bullish case, and bring deeper fall back to 0.6420 support, and possibly below.

{kind=link}