Australian Dollar is overwhelmingly the worst performing one today. It suffers heavy selling after much weaker than expected CPI raises the chance of RBA rate cut later this year. New Zealand Dollar follows as second as RBNZ is also expected to cut, just probably earlier in May. Canadian Dollar is the third weakest on anticipation that BoC would drop tightening bias with today’s rate decision statement.

On the other hand, Yen is the strongest one for today. Despite yesterday’s strong rally in US stocks, Asian markets are generally weaker. Dollar follows as the second strongest one. Solid corporate earnings are reducing the chance of a Fed cut, at least. Sterling is the third weakest strongest for today. While GBP/USD breaks 1.2960 key support, the Pound is still range bound against Euro and Yen.

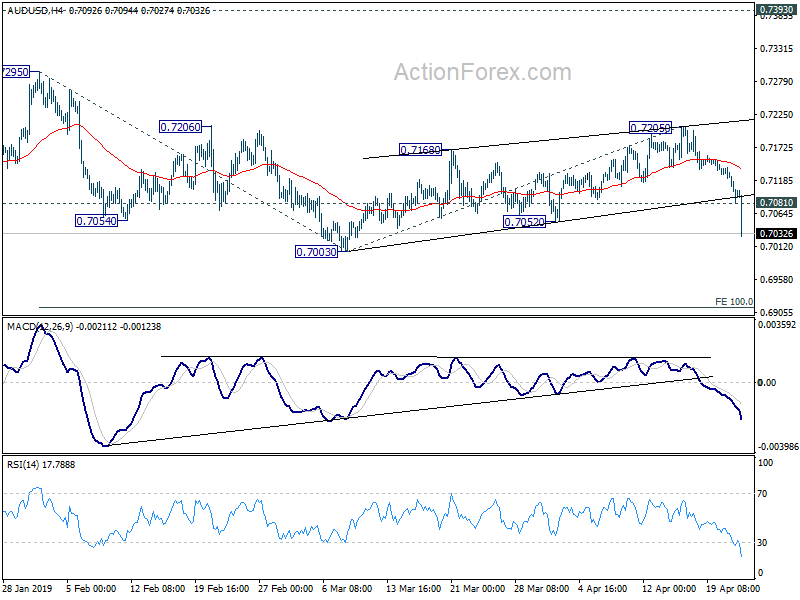

Technically, with today’s steep decline, AUD/USD is now likely resuming the decline from 0.7295. 0.7003 support will be an immediate focus and we’d expect a decisive break there to confirm near term bearishness. Similarly, AUD/JPY is heading towards 77.44 equivalent support while EUR/AUD is heading to 1.6122 equivalent resistance. EUR/USD recovers well ahead of 1.1176 low but this level will remain the focus in near term. USD/CAD breaches 1.3451 resistance and focus is immediately on 1.3467. Firm break will resume rebound from 1.3068 towards 1.3664 high.

Elsewhere, at the time of writing, Nikkei is down -0.56%. Hong Kong HSI is down -0.85%. China Shanghai SSE is down -0.92%. Singapore Strait Times is up 0.21%. Japan 10-year JGB yield is down -0.0096 at -0.04. Overnight, DOW closed up 0.55%. S&P 500 rose 0.88%. NASDAQ rose 1.32%. 10-year yield dropped -0.002 to 2.57, rejected by 2.6 handle again.

Big downside surprise in Australia CPI adds to case for RBA cut

Australian Dollar is sold off sharply after much weaker than expected consumer inflation data.

- Headline CPI rose 0.0% qoq, 1.3% yoy in Q1, down from 0.5% qoq, 1.8% yoy, missed expectation of 0.2% qoq, 1.5% yoy. The 1.3% annual rate is also the slowest since September 2016.

- RBA trimmed mean CPI rose 0.3% qoq, 1.6% yoy, below expectation of 0.4% qoq, 1.7% yoy. Annual rate is slowest since December 2016.

- RBA weighted median CPI rose 0.1% qoq, 1.2% yoy, well below expectation of 0.4% qoq, 1.6% yoy.

The weak inflation data heighten the prospect of RBA rate cut in May, together with RBNZ. But for now, it still seems a bit early for RBA to act given relative resilience in job data. May is more an ideal occasion for RBA to turn dovish with new economic projections and SoMP. If it happens, the case for a cut in August would be secured.

S&P 500 and NASDAQ closed at records, no follow through in Asia

US stocks enjoyed strong rally overnight as boosted by solid corporate earnings from Coca-Cola to Twitter. S&P 500 and NASDAQ closed at records of 2933.68 (up 0.88%) and 8120.82 (up 1.32%) respectively. Though, they’re both held below intraday highs. DOW also gained 0.55% to 26656.39.

Technically, the strong momentum suggests that both S&P 500 and NASDAQ will easily take out intraday records at 2490.91 and 8133.30. That could likely pull DOW upward to equivalent level at 26951.81. Yet, we’re still not too convinced that the indices are in long term up trend resumption yet.

Two developments give us some doubts over the underlying momentum of the global markets. Firstly, Asian markets are not following and with major indices, except Singapore Strait Times, turned red after initial gains today. Secondly, Yen is the strongest one for the week so far while USD/JPY is stuck in tight range only, which isn’t the usually development seen in strong risk on market. Thus, there will be a lot of caution in the next move up.

US-China trade talks to resume in Beijing on Apr 30, Kudlow said cautiously optimistic but not there yet

The White House announced that Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin will travel to Beijing to on April 30 to continue trade talks. China’s team will again be led by Vice Premier Liu He. Liu is expected to fly to Washington on May 8 for additional discussions. In the statement, it’s noted that “the subjects of next week’s discussions will cover trade issues including intellectual property, forced technology transfer, non-tariff barriers, agriculture, services, purchases, and enforcement.”

Earlier yesterday, Larry Kudlow, Director of the White House National Economic Council, said the negotiations were making progress and he was “cautiously optimistic” on striking a deal. He hailed that “we’ve come further and deeper, broader, larger-scale than anything in the history of U.S.-China trade.”

But Kudlow also noted that “We’re not there yet, but we’ve made a heck of a lot of progress”. “We’re still working on the issues, so-called structural issues, technology transfers”. Also, “ownership enforcement is absolutely crucial. Lowering barriers to buy and sell agriculture and industrial commodities. It’s all on the table.”

BoC to drop tightening bias, or would it?

BoC is widely expected to keep overnight rate unchanged at 1.75% today. Back in March, the central bank has already shifted to a more cautious stance and noted outlook “warrant a policy interest rate that is below its neutral range”. Also, given the mixed picture ” it will take time to gauge the persistence of below-potential growth and the implications for the inflation outlook.” But after all, tightening bias was maintained and there was just “increased uncertainty about the timing of future rate increases.”

Since then, data have been mixed. Headline CPI rose to 1.9% yoy in March, sharply higher than February’s 1.5% yoy. Core CPI also picked up slightly from 1.5% yoy to 1.6% yoy. Median CPI rose to 2.0% while trimmed mean CPI rose to 2.1% yoy. Job data remained resilient too. However, BoC’s Business Outlook Survey (BOS) disappointed with the overall business index falling to -0.6% in 1Q19. The result pointed to “a moderation from previously high levels of domestic and foreign demand for firms in most regions”.

There are speculations that BoC could totally drop tightening bias, and indicate that rates will stay there for longer. However, the recent data might not be giving enough pressure for BoC to do it. Also, oil price has been in strong rally since WTI bottomed at 42.05 last December. The current picture, with WTI back above 65, is drastically different from that one in January. Thus, the anticipated neutral shift is far from being certain. BoC will also release new economic projections. Today’s announcement is a wild card.

Some suggested readings:

- BoC Meeting: Cautious, But Less Than Markets Expect

- BOC to Look Through Strong March Inflation and Maintain Dovish Stance

- Forward Guidance: Bank of Canada Will Officially Shift to a Neutral Bias Next Week

Elsewhere

German Ifo business climate will also be watched closely today. ECB will release monthly bulletin. UK will release public sector net borrowing.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7075; (P) 0.7107; (R1) 0.7135; More…

AUD/USD’s decline accelerates to as low as 0.7027 so far. The strong break of 0.7052 support affirms the case of resumption of fall from 0.7295. Intraday bias remains on the downside for 0.7003 support first. Break will confirm and target 100% projection of 0.7295 to 0.7003 from 0.7205 at 0.6913. Decisive break there will indicate further downside acceleration. On the upside, above 0.7081 minor resistance will turn intraday bias neutral and bring consolidation, before staging another fall.

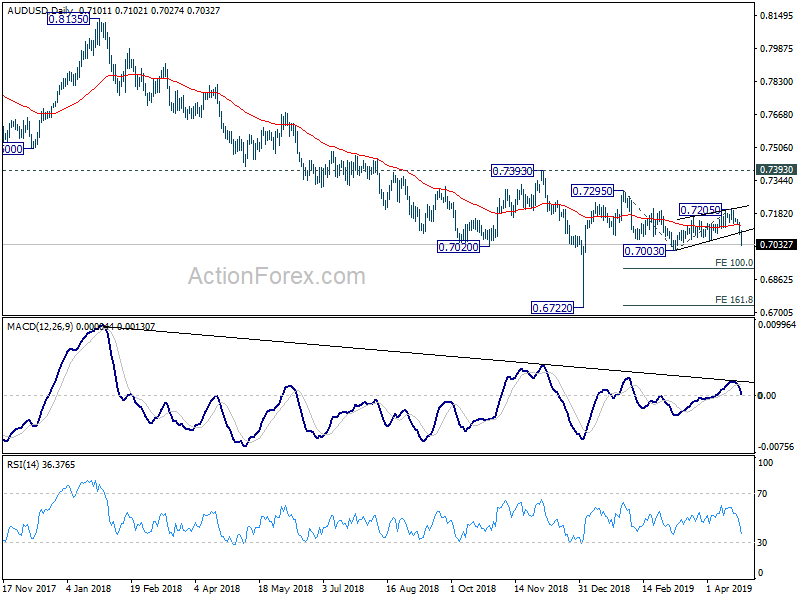

In the bigger picture, with 0.7393 key resistance intact, medium term outlook remains bearish. The decline from 0.8135 (2018 high) is seen as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Y/Y Mar | 1.10% | 1.00% | 1.10% | |

| 1:30 | AUD | CPI Q/Q Q1 | 0.00% | 0.20% | 0.50% | |

| 1:30 | AUD | CPI Y/Y Q1 | 1.30% | 1.50% | 1.80% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Q/Q Q1 | 0.30% | 0.40% | 0.40% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Y/Y Q1 | 1.60% | 1.70% | 1.80% | |

| 1:30 | AUD | CPI RBA Weighted Median Q/Q Q1 | 0.10% | 0.40% | 0.40% | |

| 1:30 | AUD | CPI RBA Weighted Median Y/Y Q1 | 1.20% | 1.60% | 1.70% | 1.60% |

| 4:30 | JPY | All Industry Activity Index M/M Feb | -0.20% | -0.20% | ||

| 5:00 | JPY | Leading Index CI Feb F | 97.4 | |||

| 8:00 | EUR | German IFO Business Climate Apr | 99.9 | 99.6 | ||

| 8:00 | EUR | German IFO Expectations Apr | 96 | 95.6 | ||

| 8:00 | EUR | German IFO Current Assessment Apr | 103.6 | 103.8 | ||

| 8:00 | EUR | ECB Economic Bulletin | ||||

| 8:30 | GBP | Public Sector Net Borrowing (GBP) Mar | -0.8B | -0.7B | ||

| 14:00 | CAD | BoC Rate Decision | 1.75% | 1.75% | ||

| 14:30 | USD | Crude Oil Inventories | -1.4M |

{kind=link}