Dollar’s selloff continues in Asian session today as overall market sentiment is supported by further restriction easing in China. The improvement in sentiment is also reflected in some weakness in Yen and Swiss Franc. Australian Dollar and Canadian Dollar are trading generally higher, awaiting rate hike by RBA and BoC later in the week. Euro and Sterling are mixed for now.

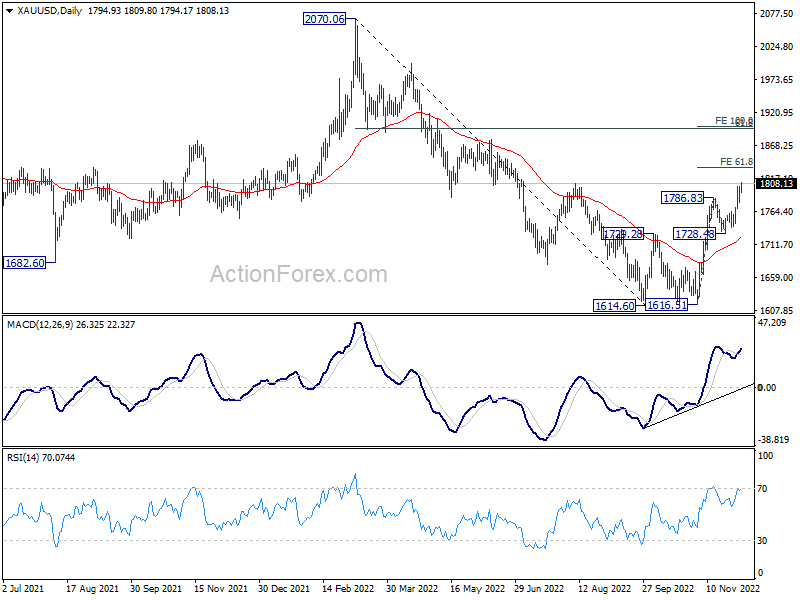

Technically, Gold is also extending the rise from 161.51. Next target is 61.8% projection of 1616.51 to 1786.83 from 1728.48 at 1833.73. Sustained break there could prompt acceleration to 100% projection at 1898.80, which is close to 1900 handle. If happens, that could be a confirming signal of Dollar’s selloff, which might be accompanied by EUR/USD’s firm break of 1.0609 fibonacci level.

In Asia, at the time of writing, Nikkei is down -0.03%. Hong Kong HSI is up 3.46%. China Shanghai SSE is up 1.56%. Singapore Strait Times is up 0.49%. Japan 10-year JBG yield is up 0.0026 at 0.254.

BoE Dhingra: Interest rate should peak below 4.5%

BoE MPC member Swati Dhingra said in an Observer interview that interest rate in the UK should peak below 4.5% to avoid deepening and prolonging a recession.

“You do see a much deeper and a longer recession with rates being much higher. That is what I think we should all be worried about … are we going to end up lengthening and deepening the recession if the tightening continues at the pace it is?” she said.

She added that those expecting more large rate hikes are not considering the fall in investment and employment as projected for the new two years. “These are not trivial numbers. The market has clearly not realized how pessimistic that could be for the UK economy,” she said. “The economic slowdown is here.”

ECB Villeroy backs 50bps hike this month to finish first half of the game

ECB Governing Council member Francois Villeroy de Galhau said in an interview on Sunday, for this month’s meeting, “it’s desirable to bring rates to 2%, so a rise of 0.5 or 50 basis points.”

Bringing interest rate to 2% will market the first half of the game of normalization. “In the second half of the match, rates will continue to rise but I can’t say where this will stop,” adding the the pace would be slower.

He also noted it would be “wise to start to reduce (the balance sheet) in 2023, beginning with the APP holdings in the “first half of the year, clearly but cautiously and progressively.”

China Caixin PMI services dropped to 46.7, third month of contraction

China Caixin PMI Services dropped from 48.4 to 46.7 in November, below expectation of 48.8. PMI Composite dropped from 48.3 to 47.0, signalling a third successive monthly contraction in business activity. The rate of decline was the strongest since May.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Manufacturing and services activity contracted in varying degrees, with the services sector hit harder by Covid outbreaks…. The prolonged pandemic has battered the economy. While the third wave has led to a softened slowdown on both supply and demand than the previous ones, there has been significant pain in the job market.”

RBA and BoC to continue tightening

Two central banks will meet this week. RBA is expected to hike by 25bps to 3.10%, maintaining a “consistent” pace. The statement should reflect that tightening bias is maintained for another hike in February. But beyond that, the path would depend on the new economic projections to be published in February.

BoC is also widely expected to deliver another rate hike. But with interest rate more in restrictive level at 3.75%, the central are having more options, and thus opinions are divided. The chances of a 25bps and 50bps are roughly equal. Another consideration is whether the pause in tightening would start after this week’s action, or next. So, there is room for some surprises.

Here are some highlights for the week:

- Monday: Australia AiG construction, MI inflation gauge; China Caixin PMI services; Eurozone PMI services final, Sentix investor confidence, retail sales; UK PMI services final; Canada building permits; US ISM services, factory orders.

- Tuesday: Japan labor cash earnings, household spending; RBA rate decision, Australia current account; UK PMI construction; Canada trade balance; US trade balance.

- Wednesday: Australia AiG services, GDP; China trade balance; Japan leading indicators; Swiss unemployment rate, foreign currency reserves; Germany industrial production; France trade balance; Italy retail sales; Eurozone GDP revision; US non-farm productivity; BoC rate decision.

- Thursday: Japan bank lending, current account, GDP final; Australia trade balance; US jobless claims; Canada Ivey PMI.

- Friday: New Zealand manufacturing sales; Japan M2; China CPI, PPI; Canada capacity utilization; US PPI, U of Michigan consumer sentiment.

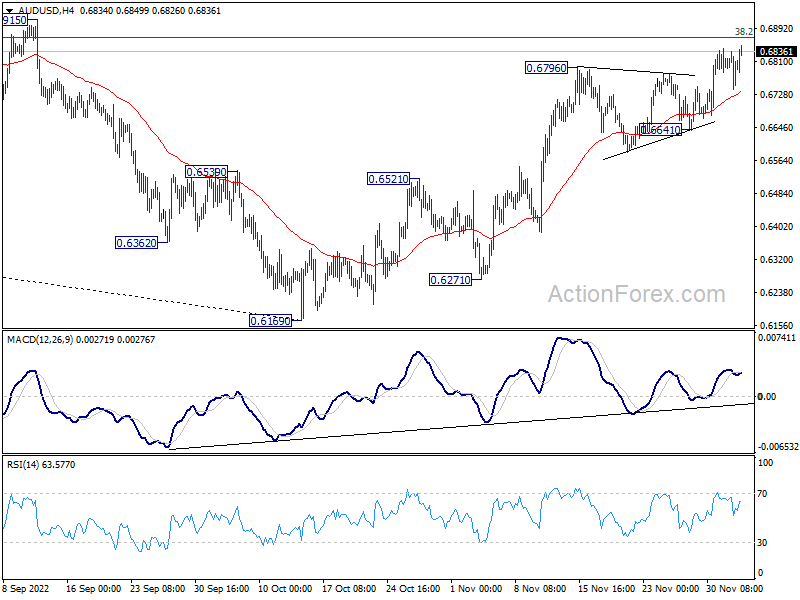

AUD/USD Daily Report

Daily Pivots: (S1) 0.6747; (P) 0.6791; (R1) 0.6840; More…

AUD/USD’s rally is resuming and intraday bias is back on the upside for 0.6871 fibonacci level. For now, outlook will remain bullish as long as 0.6641 support holds, in case of retreat. However, break of 0.6641 will indicate rejection by 0.6871 and turn bias back to the downside instead.

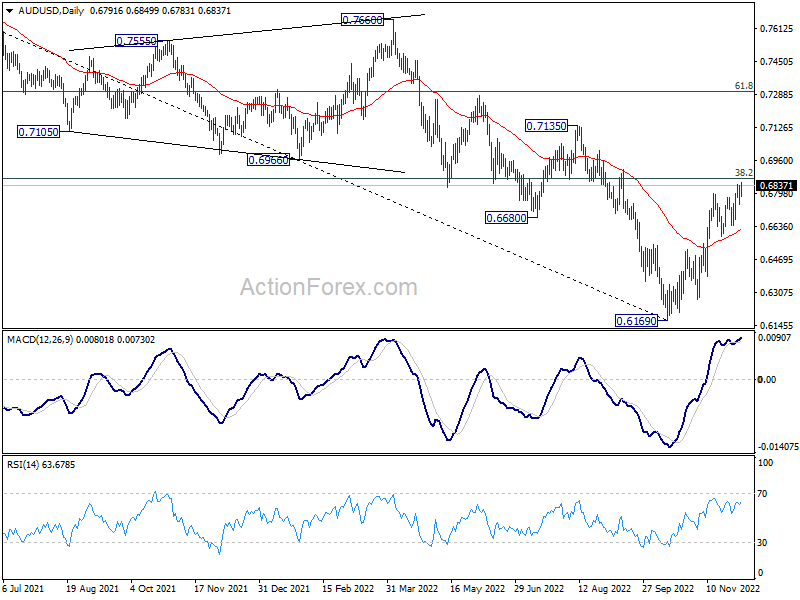

In the bigger picture, a medium term bottom is in place at 0.6160 already. But it’s too early to call for trend reversal. Nevertheless, even as a corrective move, rise from 0.6169 should target 38.2% retracement of 0.8006 to 0.6169 at 0.6871. Sustained trading above 55 week EMA (now at 0.6922) will raise the chance of the start of a bullish up trend. However, rejection by 0.6781 or 55 week EMA, followed by 0.6521 resistance turned support and retain medium term bearishness.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Nov | 48.2 | 43.3 | ||

| 00:00 | AUD | TD Securities Inflation M/M Nov | 1.00% | 0.40% | ||

| 00:30 | AUD | Company Gross Operating Profits Q/Q Q3 | -12.40% | -1.50% | 7.60% | 7.80% |

| 01:45 | CNY | Caixin Services PMI Nov | 46.7 | 48.8 | 48.4 | |

| 08:45 | EUR | Italy Services PMI Nov | 47.6 | 46.4 | ||

| 08:50 | EUR | France Services PMI Nov F | 49.4 | 49.4 | ||

| 08:55 | EUR | Germany Services PMI Nov F | 46.4 | 46.4 | ||

| 09:00 | EUR | Eurozone Services PMI Nov F | 48.6 | 48.6 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | -27.1 | -30.9 | ||

| 09:30 | GBP | Services PMI Nov F | 48.8 | 48.8 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | -1.60% | 0.40% | ||

| 13:30 | CAD | Building Permits M/M Oct | -2.00% | -17.50% | ||

| 14:45 | USD | Services PMI Nov F | 46.1 | 46.1 | ||

| 15:00 | USD | ISM Services PMI Nov | 53.5 | 54.4 | ||

| 15:00 | USD | Factory Orders M/M Oct | 0.00% | 0.30% |

{kind=link}