Dollar strengthened broadly in the wake of Fed’s policy decision overnight, although upside momentum remains measured. On the one hand, the updated dot plot maintained projection of two rate cuts in 2025. On the other hand, Chair Jerome Powell offered little to reinforce that view. Instead, he bluntly acknowledged that none of the rate path projections are held “with a great deal of conviction”. His message was clear: monetary policy will remain on hold until the inflationary effects of tariffs are more fully understood.

Powell’s remarks were notably direct regarding tariffs, warning that a “meaningful increase in inflation” is widely expected in the coming months as costs ripple through supply chains. He stressed that Fed needs to observe how this pass-through plays out before taking action. “We’ll make smarter and better decisions if we just wait a couple of months,” Powell stated. The remark underlined a broader message of caution and patience, especially as the 90-day tariff truce edges toward expiration.

With Fed now behind, attention turns to SNB and BoE, both announcing decisions today. SNB is widely expected to cut its policy rate to zero amid rising deflation risks and sustained strength in Swiss Franc. For BoE, the market is looking beyond an expected hold at 4.25% to the internal vote composition and tone of guidance. Most analysts still expect the next rate cut to arrive in August, but divisions within the MPC remain a key focus.

In currency markets, Dollar has emerged as the week’s top performer so far, lifted by Powell’s pragmatism and Fed’s refusal to front-run uncertain inflation developments. Aussie and Kiwi are also holding firm. At the other end, Sterling remains the weakest major, followed by Swiss Franc and Loonie. Euro and Yen are trading mid-pack.

Overall, price action across the board reflects the continued hesitancy among traders to take strong directional views. Major pairs remain largely within recent ranges, but the Dollar’s mild bullish drift signals that in times of uncertainty, the greenback still commands safe-haven preference, particularly with the Fed anchoring policy to incoming inflation clarity.

In Asia, at the time of writing, Nikkei is down -0.88%. Hong Kong HSI is down -1.72%. China Shanghai SSE is down -0.66%. Singapore Strait Times is down -0.34%. Japan 10-year JGB yield is down -0.02 at 1.436. Overnight, DOW fell -0.10%. S&P 500 fell -0.03%. NASDAQ rose 0.13%. 10-year yield rose 0.004 to 4.397.

Fed holds steady but upgrades inflation path, slower easing ahead

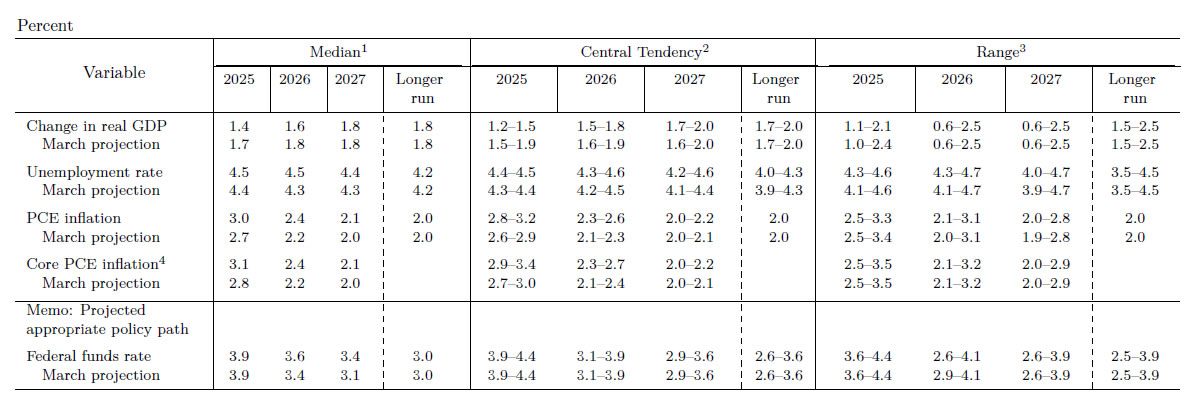

As expected, Fed left interest rates unchanged at 4.25%–4.50%, with all FOMC members voting in favor of the decision. The real focus was on the revised projections, which revealed a cautious shift: while two rate cuts remain penciled in for 2025, the pace of easing slows meaningfully beyond that.

The median forecast now puts the federal funds rate at 3.6% by the end of 2026, up from 3.4% previously, and 3.4% by the end of 2027, up from 3.1%. This implies only one cut per year after 2025. The change suggests that the Fed is growing more concerned about stickier inflation, particularly as tariff-related price effects take longer to dissipate.

Inflation forecasts were lifted meaningfully. Headline PCE inflation is now expected to run at 3.0% in 2025, up from 2.7% previously, before easing to 2.4% in 2026 and 2.1% in 2027. Core PCE projections followed a similar pattern, raised to 3.1% in 2025 from 2.8% in March. These changes reflect Fed’s acknowledgment of tariff-related price pressures filtering through the economy more persistently than previously assumed.

Meanwhile, growth forecasts were trimmed, with real GDP now seen expanding just 1.4% in 2025, down from 1.7%. The 2026 estimate was also reduced from 1.8% to 1.6%. However, the unemployment rate is expected to remain relatively stable, only nudging up to 4.5% in 2025 and holding near that level through 2027.

The slight upward drift in the unemployment forecast likely reflects this softer growth outlook, though the impact is not severe enough to force Fed’s hand.

Overall, the message is clear: while cuts are still on the table, the Fed is prepared to ease more slowly and less deeply than markets had hoped. With tariffs adding upward pressure on prices but not severely denting the labor market, policymakers are likely to remain in wait-and-see mode, calibrating their response carefully.

SNB Poised to Cut, BoE Faces Divided Path

Attention is on two key central bank decisions today, SNB and BoE.

SNB kicks off at 7:30 GMT and is widely expected to deliver a 25bps rate cut, bringing the policy rate back to 0.00%. Speculation about a return to negative rates has intensified after Swiss CPI dipped into deflation at -0.1% yoy in May. While Chair Martin Schlegel has downplayed the importance of a single data point, he has remained open to using negative rates again if disinflation proves persistent.

The Swiss central bank faces a complicated backdrop. A stronger Swiss Franc—driven by haven flows amid the global trade war, Middle East conflict, and lingering Russia-Ukraine war—has intensified deflation risks. Euro’s strength on the back of expected fiscal expansion in Germany and the EU has provided some breathing room. Still, deflation pressures remain elevated. SNB is likely to signal readiness to act further, whether through rate cuts or FX intervention, should inflation remain subdued.

Later in the day, BoE takes the stage at 11:00 GMT. The Bank is expected to keep its policy rate unchanged at 4.25%, with Governor Andrew Bailey maintaining a message of “gradual and cautious” easing. While recent economic data—including GDP and labor market indicators—have disappointed, BoE faces added complexity from surging oil prices driven by geopolitical tensions. The central bank may be wary of loosening policy too quickly under such volatile global conditions.

Internal divisions remain a key story at the BoE. In May, the vote was notably split: five members favored a 25bps cut, two wanted a larger 50bps move, and two preferred holding. Today’s voting breakdown will give a clearer view of where consensus is forming. While a Reuters poll suggests most economists expect cuts in August and again in Q4, much will depend on how services inflation evolves and whether external shocks abate.

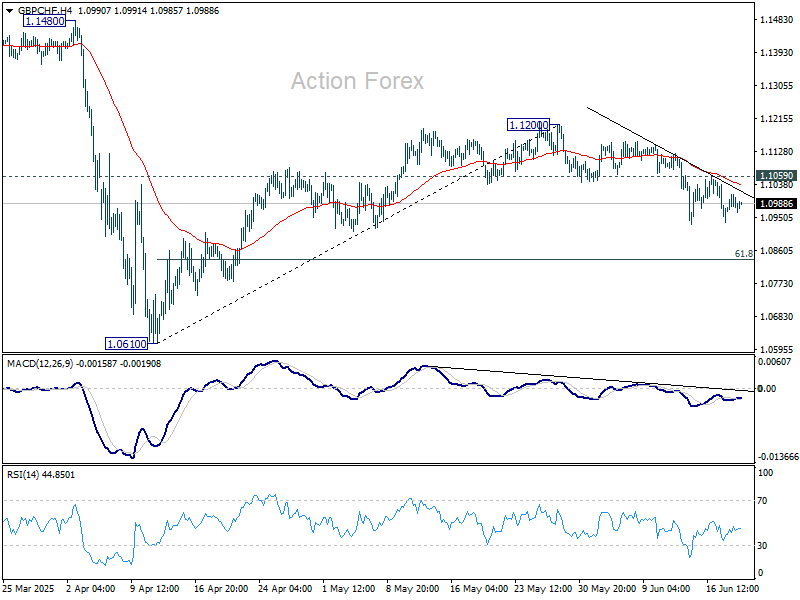

Technically, GBP/CHF’s decline from 1.1200 is still in progress. Deeper fall is in favor as long as 1.1059 resistance holds. Next target is 61.8% retracement of 1.0610 to 1.1200 at 1.0835.

Considering GBP/CHF was rejected by 55 W EMA as seen in the weekly chart, firm break of 1.0835 would argue that fall from 1.1675 is ready to resume through 1.0610 low.

Australia jobs fall -2.5k in May, but full-time hiring and hours worked offer Support

May’s Australian employment data surprised to the downside, with a -2.5k decline compared to expectations of a 19.9k gain. Yet beneath the weak headline, the composition was stronger than it appears: full-time jobs surged 38.7k while part-time jobs plunged by -41.1k.

Unemployment rate was unchanged at 4.1%, and the participation rate edged down from 67.1%to 67.0%, both suggesting a labor market that’s cooling slightly, but not cracking.

A sharp 1.3% mom rebound in total hours worked provides further reassurance, marking a recovery from recent holiday and weather-driven softness.

NZ GDP tops forecasts with 0.8% growth in Q1

New Zealand’s GDP grew 0.8% qoq in Q1, slightly ahead of expectations of 0.7% qoq. On a per capita basis, output rose 0.5% qoq.

Gains were broad-based, with all major sectors contributing positively: goods-producing industries led the way at 1.3% qoq, followed by primary industries at 0.8% qoq, and services at 0.4% qoq. Manufacturing and business services were standout performers among the detailed industries, helping to drive the recovery.

Despite the quarterly uptick, GDP contracted by 1.1% over the year to March 2025.

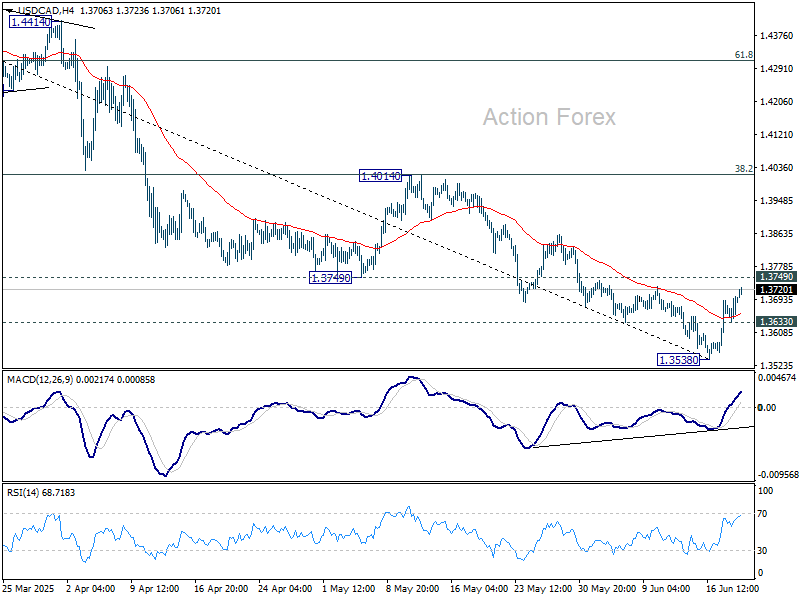

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3650; (P) 1.3677; (R1) 1.3718; More…

USD/CAD’s rebound from 1.3538 extended higher, but stays below 1.3749 support turned resistance. Intraday bias remains neutral, and further decline is expected. On the downside, below 1.3633 minor support will bring retest of 1.3538 first. Firm break there will resume larger fall from 1.4791. However, considering bullish convergence condition in 4H MACD, firm break of 1.3749 will indicate short term bottoming, and bring stronger rebound back to 1.4014 resistance.

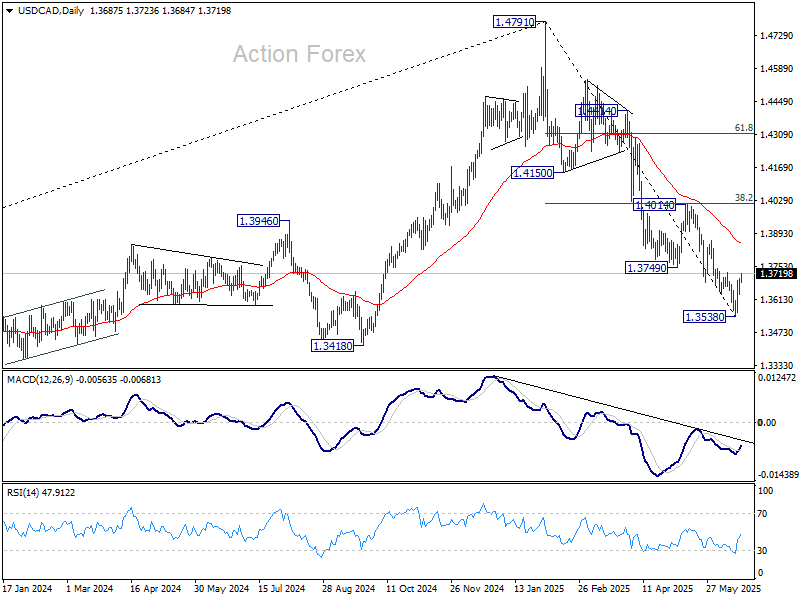

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

{kind=link}