Swiss Franc rebounded broadly on Thursday after SNB delivered a widely expected 25bps rate cut to 0.00%. Some trade had speculated on either a stronger dovish signal or even surprise action aimed at curbing Franc strength. Instead, SNB refrained from anything bold, and the post-meeting move in Franc reflected such disappointment. Also, in a global environment marked by elevated uncertainty, particularly with ongoing Middle East tensions, the safe-haven demand for the Swiss Franc remains intact.

Meanwhile, Sterling also found some footing after BoE held rates steady at 4.25%. The 6-3 split on the Monetary Policy Committee leaned dovish, with three members voting for a cut. Still, the overall tone remains consistent with its “gradual and careful” easing stance. There was no sense of urgency in the statement, and policymakers continue to stress flexibility in the face of heightened geopolitical and inflation uncertainty.

For the day so far, Swiss Franc is the strongest performer, followed by Sterling and Dollar. At the other end of the spectrum, Kiwi and Aussie lag, followed by Yen. Euro and Loonie are positioning in the middle.

Technically, one focus is AUD/USD’s reaction to 0.6455 support as selloff pick up momentum after weaker than expected job data. Sustained break there will confirm short term topping at 0.6551. That would open up deeper fall to 38.2% retracement of 0.5913 to 0.6551 at 0.6307, even as a correction.

In Europe, at the time of writing, FTSE is down -0.15%. DAX is down -0.68%. CAC is down -0.81%. UK 10-year yield is up 0.005 at 4.503. Germany 10-year yield is down -0.007 at 2.507. Earlier in Asia, Nikkei fell -1.02%. Hong Kong HSI fell -1.99%. China Shanghai SSE fell -0.79%. Singapore Strait Times fell -0.68%. Japan 10-year JGB yield fell -0.045 to 1.411.

BoE on hold, dovish undercurrent builds with 3 votes for cut

BoE left its policy rate unchanged at 4.25% today, as expected. The vote came in at 6–3, with Swati Dhingra, Dave Ramsden, and Alan Taylor opting for a 25bps cut. Known doves Dhingra and Taylor had pushed for a larger 50bps cut at last meeting. A surprise was that Ramsden who aligned with the majority last time and supported the 25bps cut. The voting marked a slight shift toward a more dovish stance.

In its accompanying statement, BoE acknowledged that underlying UK GDP growth has remained weak, and that labor market slack is becoming more evident. Inflation jumped to 3.4% in May, largely as expected. BoE expects inflation to hover around current levels through year-end before gradually falling toward the 2% target in 2026.

The statement also pointed to heightened geopolitical risks, particularly from the Middle East, as a complicating factor for inflation and energy costs. In light of this backdrop, the BoE reaffirmed that its next moves will be “gradual and careful” and emphasized that monetary policy decisions are “not on a pre-set path”.

SNB cuts to zero, sees subdued growth as tariff front-loading fades

SNB lowered its policy rate by 25 bps to 0.00%, as widely expected. The move came as inflation pressures continue to ease and growth momentum slows following a front-loaded export boost in Q1. SNB noted that its conditional inflation forecast has been revised downward for 2025 and 2026, but still sees average inflation staying well within its price stability range through the forecast horizon.

The new projections put inflation at just 0.2% in 2025 (down from 0.4%), 0.5% in 2026 (down from 0.8%) and 0.7% in 2027 (down slightly from 0.8%). These figures assume that the policy rate remains at zero throughout the period. SNB said that without today’s cut, the forecast would have been even lower.

On the growth side, SNB acknowledged that the strength in Q1 GDP was driven largely by a pull-forward of US-bound exports — a pattern mirrored in other economies. When adjusted for these front-loaded flows, underlying momentum was “more moderate”.. As a result, growth is expected to slow again and remain “rather subdued” over the remainder of the year. SNB projected GDP to rise just 1% to 1.5% this year and next.

ECB’s Nagel: Monetary policy is on the right track

German ECB Governing Council member Joachim Nagel remarked today that with inflation nearing 2% on average this year, ECB is “more or less mission accomplished” on the price stability front. He added that rates are now in “neutral territory,” and monetary policy is “on the right track.

At the same conference, Vice President Luis de Guindos reiterated that the path forward will be data-dependent and decided on a meeting-by-meeting basis. He warned of elevated geopolitical risks, including trade tensions and Middle East conflict, which could alter both inflation and economic outlook.

ECB’s Villeroy: Next move could be a cut amid sub-2% inflation risks

French ECB Governing Council member Francois Villeroy de Galhau further easing could be on the table if inflation continues to drift below target.

“Barring a major exogenous shock, including possible new military developments in the Middle East, if monetary policy were to move in the next six months, it could be more in the direction of accommodation,” Villeroy said in a speech.

He highlighted that investors are increasingly concerned inflation could settle below ECB’s 2% target, not above it.

Australia jobs fall -2.5k in May, but full-time hiring and hours worked offer Support

May’s Australian employment data surprised to the downside, with a -2.5k decline compared to expectations of a 19.9k gain. Yet beneath the weak headline, the composition was stronger than it appears: full-time jobs surged 38.7k while part-time jobs plunged by -41.1k.

Unemployment rate was unchanged at 4.1%, and the participation rate edged down from 67.1%to 67.0%, both suggesting a labor market that’s cooling slightly, but not cracking.

A sharp 1.3% mom rebound in total hours worked provides further reassurance, marking a recovery from recent holiday and weather-driven softness.

NZ GDP tops forecasts with 0.8% growth in Q1

New Zealand’s GDP grew 0.8% qoq in Q1, slightly ahead of expectations of 0.7% qoq. On a per capita basis, output rose 0.5% qoq.

Gains were broad-based, with all major sectors contributing positively: goods-producing industries led the way at 1.3% qoq, followed by primary industries at 0.8% qoq, and services at 0.4% qoq. Manufacturing and business services were standout performers among the detailed industries, helping to drive the recovery.

Despite the quarterly uptick, GDP contracted by 1.1% over the year to March 2025.

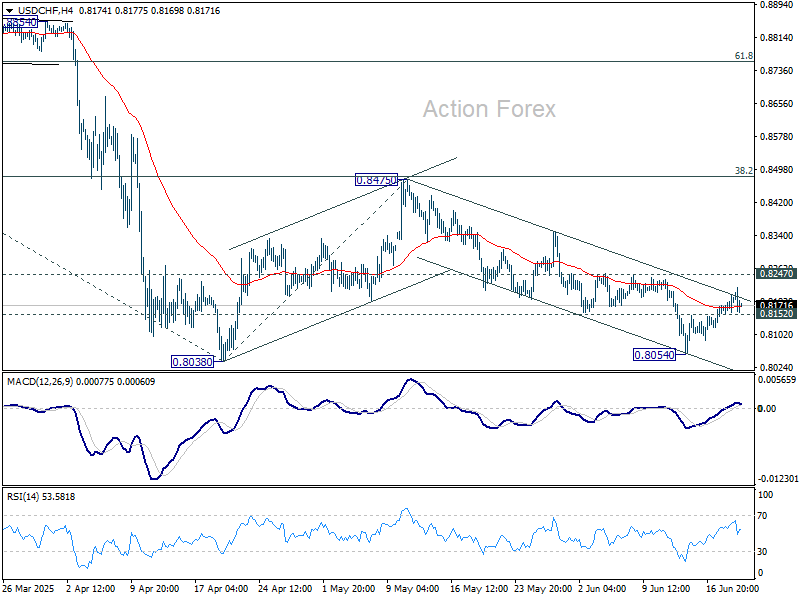

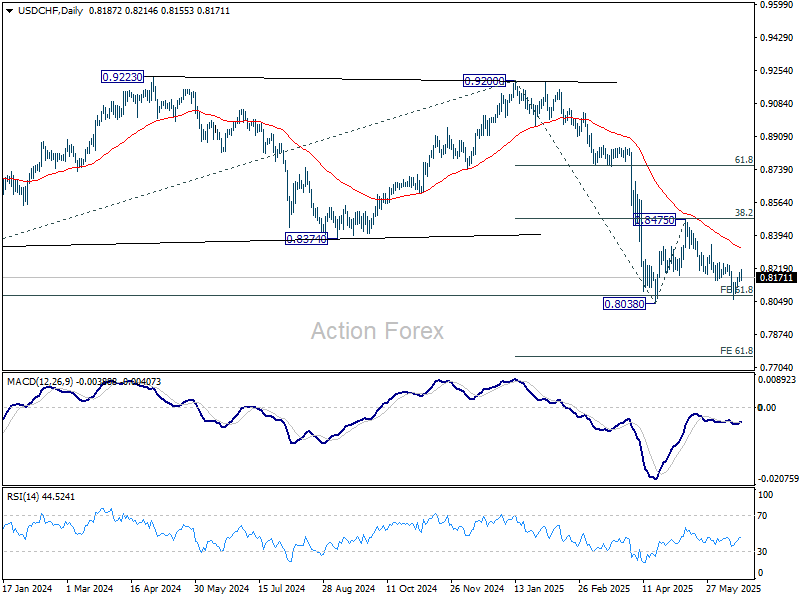

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8133; (P) 0.8153; (R1) 0.8184; More….

Intraday bias in USD/CHF stays neutral at this point. On the downside, break of 0.8152 minor support will argue that recovery from 0.8054 has completed after failing 0.8247 resistance. Deeper fall should be see to 0.8038/54 support zone. Firm break there will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Nevertheless, break of 0.8247 resistance will argue that corrective pattern from 0.8038 is starting the third leg. Bias will be turned back to the upside for 0.8475 resistance again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8656) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

{kind=link}