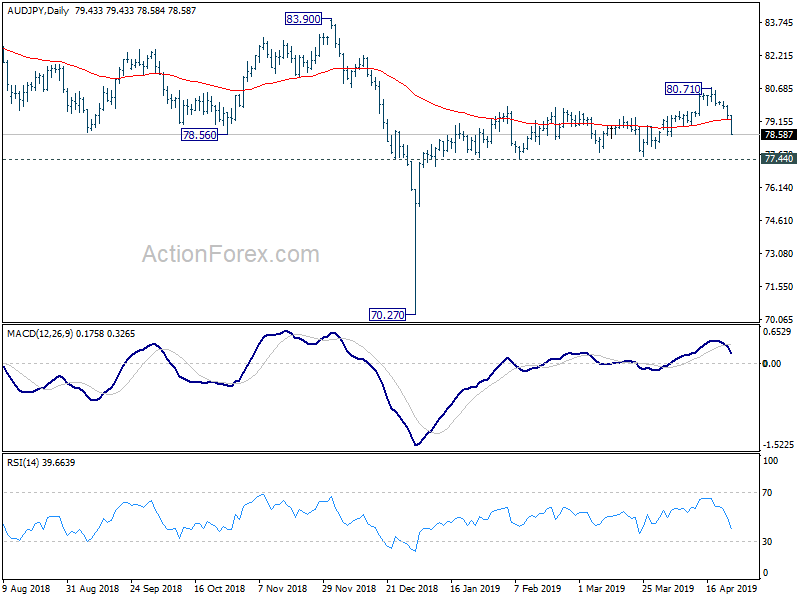

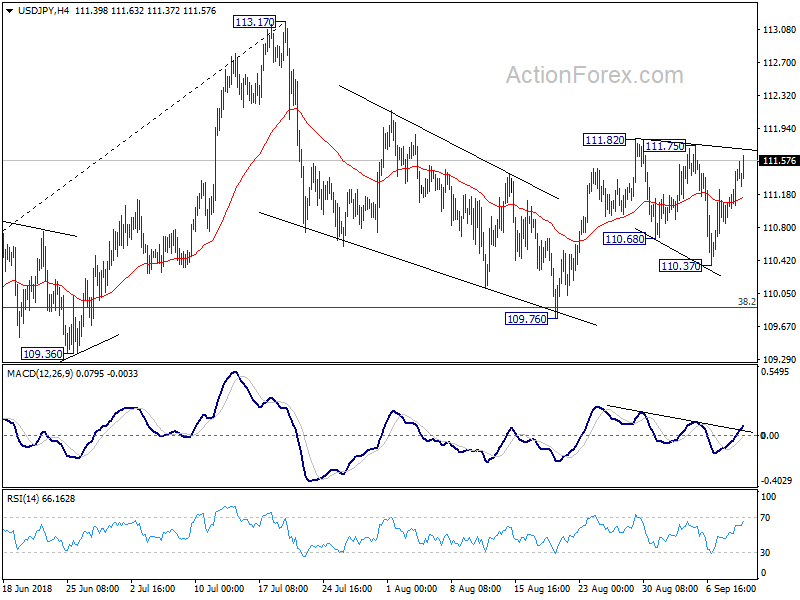

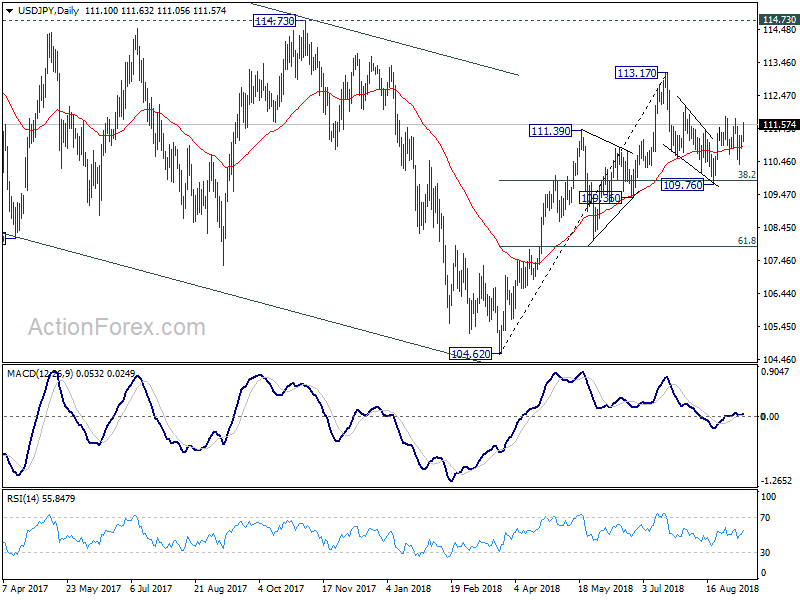

Entering into US session, Sterling is trading as the weakest one for today so far. Brexit concerns are weighing on the Pound. UK Prime Minister Theresa May is going to tell the parliament that 95% of the withdrawal agreement is done. But she continues to reject EU’s Irish backstop proposal. The deadlock remains a deadlock. Yen is among the weakest on strong global risk appetite, following rally in Chinese stocks and sharp fall in Italian yield. On the other hand, Canadian Dollar and Dollar are trading as the strongest ones. Canadian Dollar is trying to recover from Friday’s steep losses, with expectation that BoC will raise interest rate this week.

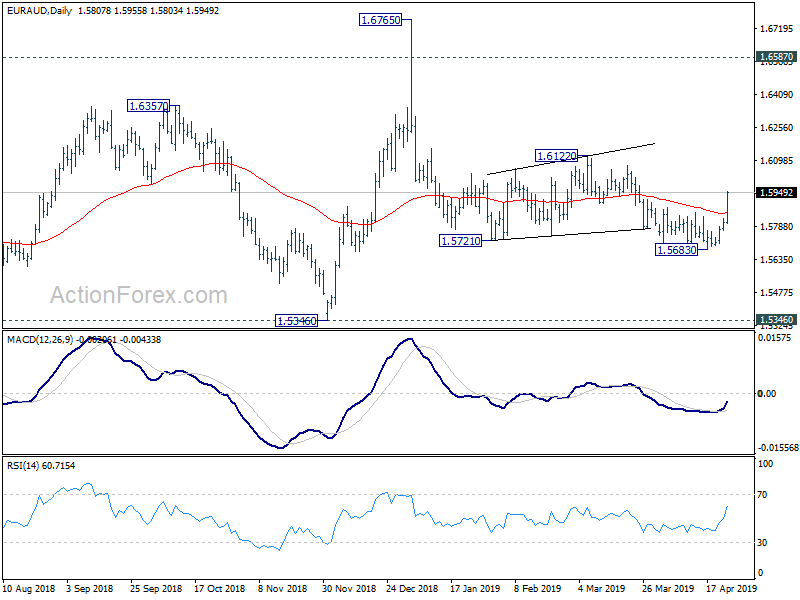

Euro is mixed at the time of writing. EUR/USD hit as high as 1.1550 today but reversed after Italy replied to the EU, insisting to stick to its “hard” but “necessary” budget. The sentiment is not totally reflected in Italian yield though. Italian 10 year yield is down -0.1358 at 0.3446 at the time of writing. However, we’d like to point out that German 10 year yield is now at 0.459, down -0.004. That is, German-Italian spread is still at 298, less alarming but still very alarming.

In European markets

- FTSE is up 0.88% at 7111.94

- DAX is up 0.81% at 11646.49

- CAC is up 0.49% at 5109.37.

Earlier in Asia,

- China Shanghai SSE rose 4.09% to 2654.88, should have confirmed medium term bottoming.

- Hong Kong HSI rose 2.32% to 26153.15

- Nikkei rose 0.37% to 22614.82

- Singapore Strait Times rose 0.51% to 3078.06.

- Japan 10 year JGB yield rose 0.0031 to 0.153

Australia’s PMI Composite slips to 50.6; firms cite election drag on demand

Australia’s private sector showed signs of slowing in May, with PMI Composite falling from 51.0 to a 3-month low of 50.6. Manufacturing index held steady at 51.7. But services weakened from 51.0 to 50.5, its lowest level in six months.

According to S&P Global’s Andrew Harker, the sluggishness may be tied in part to election-related uncertainty, which “contributed to slower growth of new orders”. Still, firms remained cautiously optimistic, continuing to hire at a “solid pace”. With the political noise expected to ease, attention will turn to whether demand picks up in the months ahead.

Full Australia PMI flash release here.