Live Comments

US Initial Jobless Claims Edge Up to 119k, but Layoffs Remain Limited

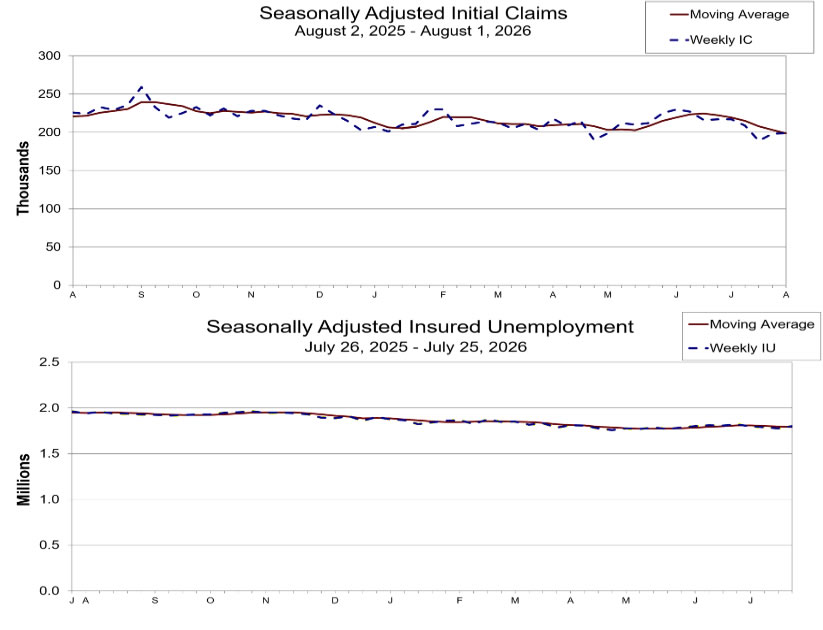

US initial jobless claims remained near historically low levels in the latest week, reinforcing the view that layoffs continue to be limited despite signs of slower hiring elsewhere in the labor market. Initial claims rose by just 1,000 to 199,000 in the week ended August 1, slightly below market expectations of 203,000. The previous week's figure was revised up modestly to 198,000, while the four-week moving average declined to 198,750, suggesting underlying labor market conditions remain broadly stable.

Continuing claims painted a slightly softer picture, rising 24,000 to 1.801 million in the week ended July 25, although the insured unemployment rate held steady at 1.2%. The increase suggests unemployed workers may be taking slightly longer to find new jobs, but the overall level remains consistent with a labor market that is cooling gradually rather than weakening abruptly.

The latest figures fit with other recent labor market indicators showing a "low-hire, low-fire" environment. While ADP employment and the ISM Services Employment Index pointed to softer hiring momentum, weekly claims continue to show employers are reluctant to shed workers.

Data Summary

| Indicator | Latest | Previous |

|---|---|---|

| Initial Jobless Claims | 199K | 198K |

| Market Expectation | 203K | — |

| 4-Week Average | 198.8K | 203.3K |

| Continuing Claims | 1.801M | 1.777M |

| 4-Week Avg. Continuing Claims | 1.791M | 1.796M |

| Insured Unemployment Rate | 1.2% | 1.2% |

Key Takeaways

- Initial jobless claims edged up to 199K, remaining below the 200K mark and beating expectations of 203K, indicating layoffs remain historically low.

- The four-week moving average fell to 198.8K, suggesting there has been no meaningful deterioration in underlying labor market conditions.

- Continuing claims rose by 24K to 1.801 million, hinting that unemployed workers may be taking slightly longer to secure new jobs.

- The insured unemployment rate held steady at 1.2%, reinforcing the picture of a labor market that remains fundamentally resilient.

- The report supports the recent "low-hire, low-fire" narrative emerging from JOLTS, ADP and Fed officials—hiring has slowed, but employers are generally reluctant to lay off workers.

Eurozone Retail Sales Fall -0.3% MoM in June as Food and Non-Food Demand Weakens

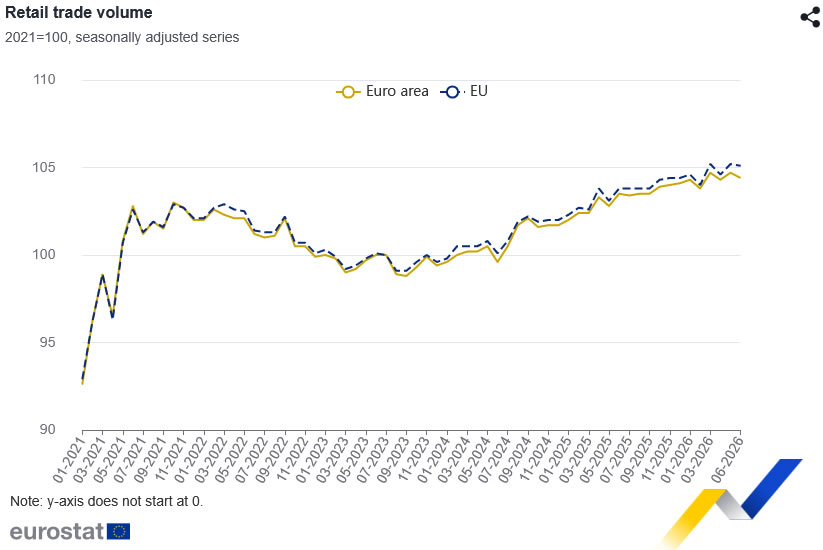

Eurozone retail sales weakened in June, adding to signs that household demand remains fragile despite improving business surveys. Retail trade volume fell -0.3% mom after rising 0.4% in May. Sales across EU declined -0.1% following 0.6% growth. On annual basis, retail sales still increased 0.7% yoy in Eurozone and 1.2% across EU, indicating consumer spending has not collapsed but continues to lack consistent momentum.

Weakness was broad across core spending categories. In Eurozone, food, drinks and tobacco sales fell -0.5% mom, while non-food sales declined -0.4%. Automotive fuel provided only offset, rising 1.5%. Pattern was similar across EU, where food sales dropped -0.4%, non-food purchases fell -0.3%, and fuel sales increased 1.7%. That composition suggests consumers remained cautious on discretionary and everyday spending even as driving-related demand improved.

National data also pointed to uneven conditions across region. Finland, Romania and Germany recorded largest monthly declines, while Luxembourg, Portugal, Croatia and Sweden posted strongest gains. For ECB, softer retail activity supports patience on further tightening, particularly while policymakers assess whether easing pipeline inflation can continue without renewed pressure from energy markets.

Data Summary

Eurozone Retail Sales

| Indicator | June 2026 | May 2026 | Trend |

|---|---|---|---|

| Total Retail Sales (m/m) | -0.3% | +0.4% | ▼ Weaker |

| Retail Sales (y/y) | +0.7% | — | ▲ Annual growth |

| Food, Drinks & Tobacco | -0.5% | +0.4% | ▼ Lower |

| Non-food (ex. Automotive Fuel) | -0.4% | +0.5% | ▼ Lower |

| Automotive Fuel | +1.5% | -1.8% | ▲ Rebounded |

EU Retail Sales

| Indicator | June 2026 | May 2026 | Trend |

|---|---|---|---|

| Total Retail Sales (m/m) | -0.1% | +0.6% | ▼ Weaker |

| Retail Sales (y/y) | +1.2% | — | ▲ Annual growth |

| Food, Drinks & Tobacco | -0.4% | +0.4% | ▼ Lower |

| Non-food (ex. Automotive Fuel) | -0.3% | +0.9% | ▼ Lower |

| Automotive Fuel | +1.7% | -1.4% | ▲ Rebounded |

Largest Monthly Changes by Member State

| Largest Declines | m/m | Largest Gains | m/m |

|---|---|---|---|

| Finland | -1.5% | Luxembourg | +2.5% |

| Romania | -1.2% | Portugal | +1.7% |

| Germany | -1.1% | Croatia | +1.5% |

| Sweden | +1.5% |

Key Takeaways

- Eurozone retail sales fell 0.3% m/m in June after a 0.4% increase in May, while EU retail sales slipped 0.1% following 0.6% growth.

- Despite the monthly setback, retail sales remained higher than a year earlier, rising 0.7% y/y in the Eurozone and 1.2% y/y across the EU.

- The decline was broad-based, with both food, drinks and tobacco (-0.5%) and non-food products (-0.4%) weakening in the Eurozone.

- Automotive fuel sales rose 1.5% in the Eurozone and 1.7% in the EU, partially offsetting softer spending elsewhere.

- Germany, Finland and Romania recorded the largest monthly declines, highlighting continued weakness in several major consumer markets.

- The report suggests household demand remains subdued, reinforcing the divergence between improving business surveys and still-cautious consumers.

UK Construction PMI Improves to 44.7, but Sector Remains in Prolonged Contraction

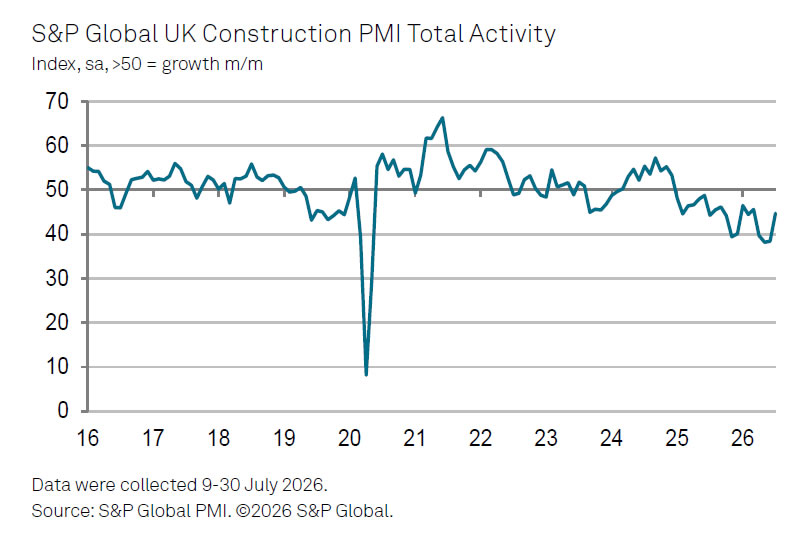

The UK construction sector showed further signs of stabilizing in July, although activity remained firmly in contraction for a nineteenth consecutive month. The S&P Global UK Construction PMI rose to 44.7 from 38.4 in June, its highest level in four months but still below the 50 threshold that separates expansion from contraction. While the reading points to another decline in overall activity, it also suggests the sharp downturn seen through the second quarter has begun to ease.

The improvement was broad-based across the sector. Commercial construction proved the most resilient, with its activity index rising to 46.8, while house building recorded its least severe contraction since October 2025 at 41.8. Civil engineering remained the weakest segment at 38.3, though even there the pace of decline moderated. According to S&P Global, the slower contraction reflected the smallest fall in new orders since September 2025, with some firms reporting improving client enquiries and a revival in tender opportunities despite generally subdued market conditions.

Encouragingly, business optimism strengthened to its highest level since February as firms became more confident about activity over the coming year. Construction companies also benefited from improving supplier performance and the slowest rise in input costs for five months. Although respondents continued to cite higher fuel and raw material costs linked to the Middle East conflict, easing cost pressures and tentative signs of recovering demand suggest the sector may be moving beyond its weakest phase, even if a sustained recovery has yet to take hold.

Data Summary

| Component | July | June | Trend |

|---|---|---|---|

| Construction PMI | 44.7 | 38.4 | ▲ Four-month high |

| Commercial Activity | 46.8 | N/A | ▲ Slowest contraction |

| House Building | 41.8 | N/A | ▲ Least severe decline since Oct 2025 |

| Civil Engineering | 38.3 | N/A | ▲ Contraction eased but remained weakest |

| Overall Activity | < 50 | < 50 | ▼ 19th consecutive month of contraction |

Key Takeaways

- UK Construction PMI rose to 44.7 in July from 38.4, reaching a four-month high and signalling that the sector's downturn is easing, although activity remains in contraction.

- The sector has now contracted continuously since January 2025, marking its longest period of decline since the Global Financial Crisis.

- All three major segments improved, with commercial construction proving the most resilient (46.8), while house building recorded its mildest contraction since October 2025.

- Survey respondents reported early signs of improving client demand and more tender opportunities, resulting in the smallest decline in new orders since September 2025.

- Business confidence climbed to its highest level since February, suggesting firms expect activity to improve over the coming year.

- Cost pressures eased to a five-month low, although companies continued to cite higher fuel and raw material prices linked to the Middle East conflict.