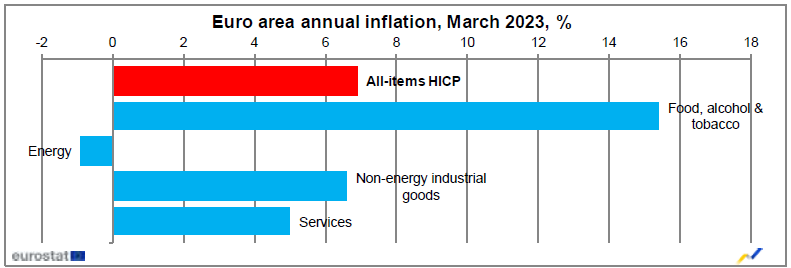

ECB President Christine Lagarde, in her address to a European Parliament committee, expressed confidence in the current policy rates, emphasizing their effectiveness in steering inflation back towards the intended target.

“Based on our latest assessment,” Lagarde mentioned, “we consider that our policy rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our target.”

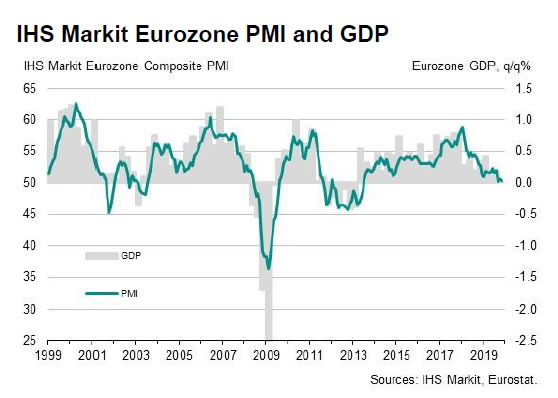

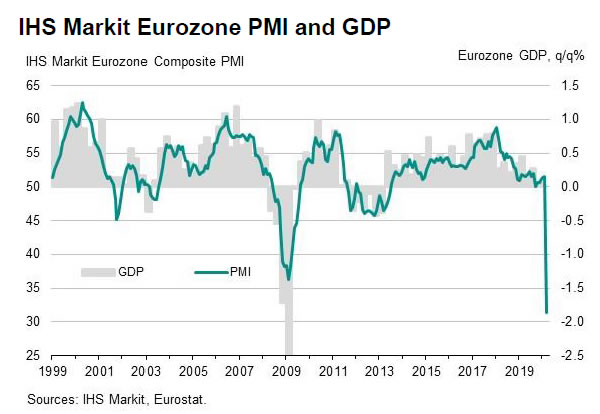

Lagarde also highlighted the headwinds faced by the euro area’s economy. After broadly stagnating during the first half of 2023, the economy has demonstrated signs of weakening further in the third quarter. This is particularly concerning given the previously resilient services sector, which is also starting to display weakness.

Lagarde elaborated, “The services sector, which had been resilient until recently, is now also weakening,” noting that “job creation in the services sector is moderating and overall momentum is slowing.”

Domestic price pressures, however, continue to remain formidable. A surge in holiday and travel spending combined with substantial wage growth is holding up services inflation.

Nevertheless, according to staff projections, “inflationary pressures are expected to moderate and that inflation is set to reach our target by the end of 2025.”

Eurozone unemployment rate dropped to 6.8% in January, EU down to 6.2%

Eurozone unemployment rate dropped from 7.0% to 6.8% in January, better than expectation of 6.9%. EU unemployment rate dropped from 6.3% to 6.2%.

Eurostat estimates that 13.346 million men and women in the EU, of whom 11.225 million in the euro area, were unemployed in January 2022. Compared with December 2021, the number of persons unemployed decreased by 216 000 in the EU and by 214 000 in the euro area. Compared with January 2021, unemployment decreased by 2.522 million in the EU and by 2.117 million in the euro area.

Full release here.