{kind=link}

- US shutdown reaches a critical stage; dollar benefits from lingering uncertainty.

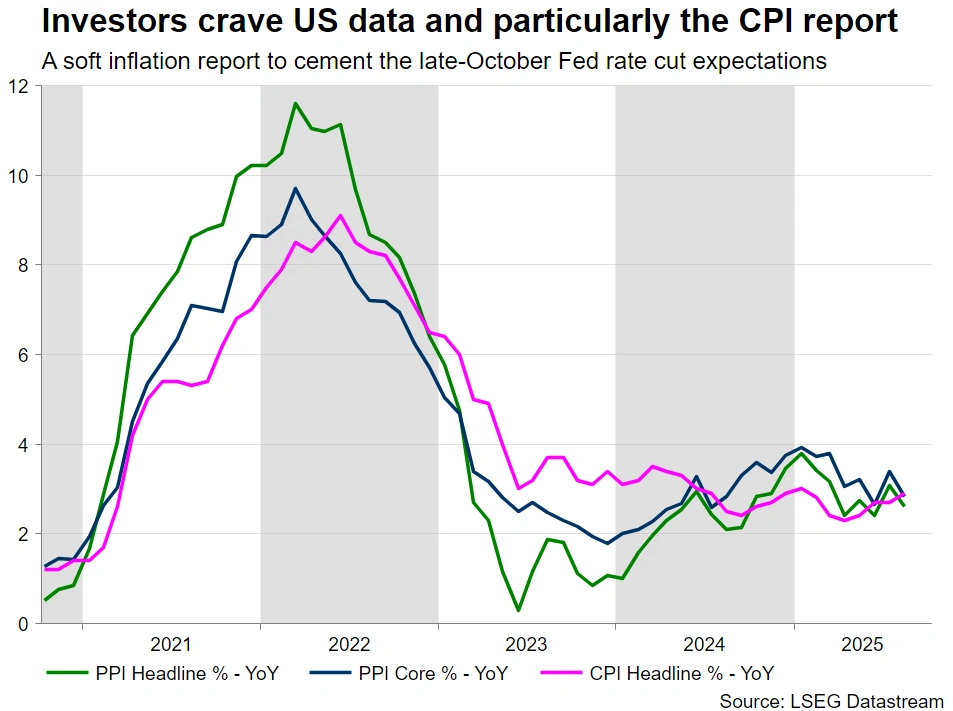

- US CPI report may be published but the Fed needs more data to justify the rate cut.

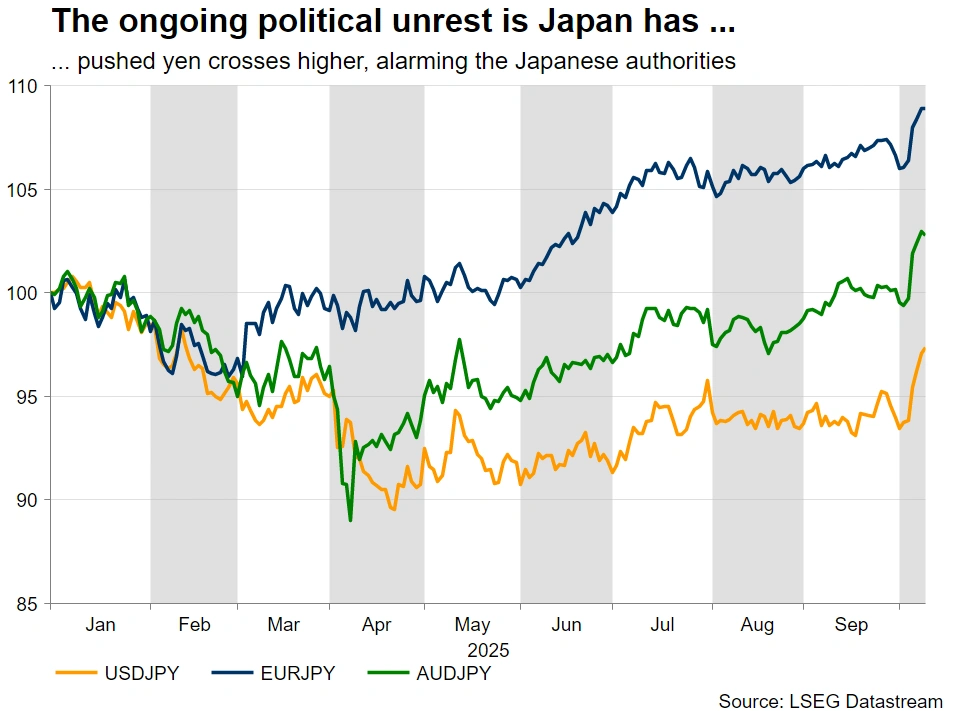

- No end to the yen’s suffering, as dollar/yen trades at intervention territory.

- China is potentially preparing for new support measures and a looser PBoC stance.

- Key jobs data in the UK and Australia; commodity currencies in need of a boost.

Political risks in the spotlight

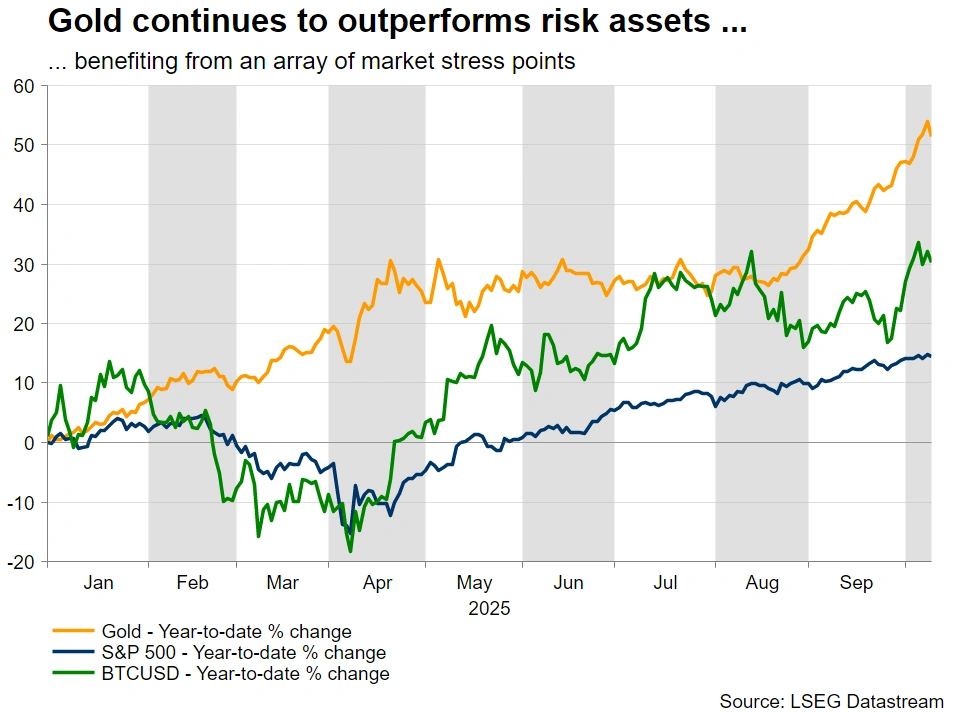

Following a Fed-dominated period, political risks have been monopolizing market attention. The US government shutdown and developments in both France and Japan have been fueling an atypical risk-off reaction, with the US dollar, gold and US equities surging. In particular, gold has been generating headlines with its continued rally, only to ease in the past two sessions on news of a ceasefire agreement in Gaza.

Could the US shutdown continue into a third week?

While most investors have taken the US federal government shutdown lightly, assuming that it will prove a short-term affair, little progress has been made since October 1. Both Democrats and Republicans remain unyielding at this stage, despite voices on both sides calling for a quick reconciliation before the shutdown damages the US economy.

Multiple Senate votes have failed so far, which could mean that Trump’s involvement is potentially necessary to get the show on the road, assuming he is interested in finding common ground. Behind-the-door discussions are expected to intensify going into next week, but the outcome is uncertain.

Markets reacted calmly to the absence of the early October jobs data, however, next week the CPI and PPI reports along with retail sales data are scheduled for release. Another week without official data could raise questions about the 25bps Fed rate cut expectations. Interestingly, reports point to an effort by the Bureau of Labour Statistics to compile the CPI report, but its publication date remains unknown and could even take place just ahead of the October 29 Fed meeting.

That said, if the shutdown concludes next week, it might be extremely challenging for the BLS to meet its own data calendar. This means that an amended calendar will be announced, potentially extending until year-end to normalize releases, with a strong possibility of two Nonfarm Payrolls reports in the same calendar month.

Meanwhile, with the next blackout period starting on October 18, both Fed doves and hawks are expected to carefully lay their arguments. Quite notably, since September 19, Fedspeak has not been overly dovish, with most centrist members trying to muddle the waters and make the October rate decision less predictable. Markets, though, appear adamant that another rate cut will be announced.

The dollar has had a good week, posting sizeable gains particularly against the euro and the yen. A continuation of the shutdown might not clip its wings despite concerns about the impact on the US economy, especially if Fedspeak remains balanced throughout the next week and the positive momentum in US stocks persists.

Part of the reason US politicians are relatively relaxed about the shutdown is the strong performance of US equity indices. That said, a reversal of the current bullish trend, such as a couple of strongly negative sessions, could prove to be a powerful catalyst for getting the funding bill negotiations back on track.

No end to Japan’s political unrest

It has been a week since Sanae Takaichi won the LDP leadership contest, but her future is already looking bleak. Following the breakup of the long-standing coalition between the LDP and Komeito parties – assuming there is no U-tern from Komeito over the weekend – Takaichi has two options: seek support elsewhere – specifically from the right-wing DPP party – or resign and allow the LDP to select a new leader who could reset the LDP-Komeito relationship.

Meanwhile, the DPP appears to be the kingmaker. The main opposition parties have proposed nominating Tamaki as a candidate in the upcoming PM vote against Takaichi, but the DPP head is not agreeable to this proposal. Similarly, he has excluded the possibility of an LDP-DPP coalition that would lack a majority in the Diet.

The yen has reacted slightly positively to the LDP-Komeito breakup, but Japan’s outlook has just become more clouded. The Japanese Finance Ministry, in cooperation with the BoJ, will most likely keep tabs on yen underperformance, but a new PM has to be elected soon. In the meantime, an October BoJ rate hike appears to be out of the question, but December remains a ‘live’ month.

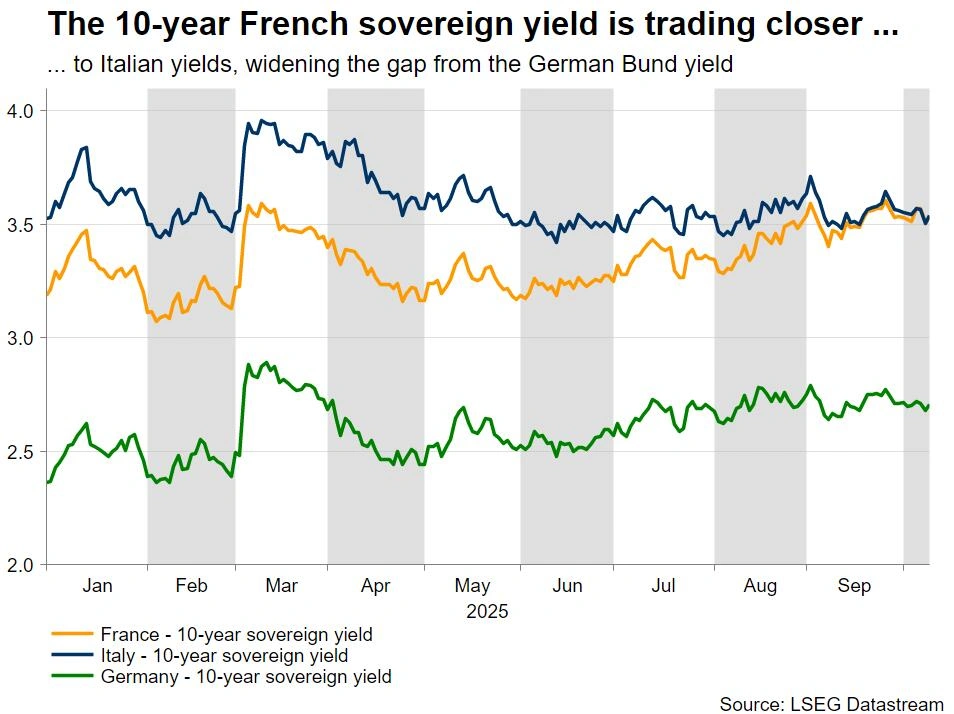

Developments in France dent Euro’s appeal

Political developments in France have disrupted the relative calmness in the eurozone. President Macron has to pick another PM, but the left-wing Popular Front and Le Pen’s National Rally continue to hold the keys to the National Assembly. Therefore, the path ahead will remain tricky, with the 2026 budget deadline pushed back to mid-December.

With French sovereign bond yields edging higher, and the euro underperforming versus the dollar, a credible solution to the French political deadlock is needed. Fresh parliamentary elections are less likely at this stage, since the two aforementioned parties are expected to dominate again. Therefore, Macron might decide to break the deadlock by calling snap presidential elections. But this is probably a scenario that may materialize in 2026.

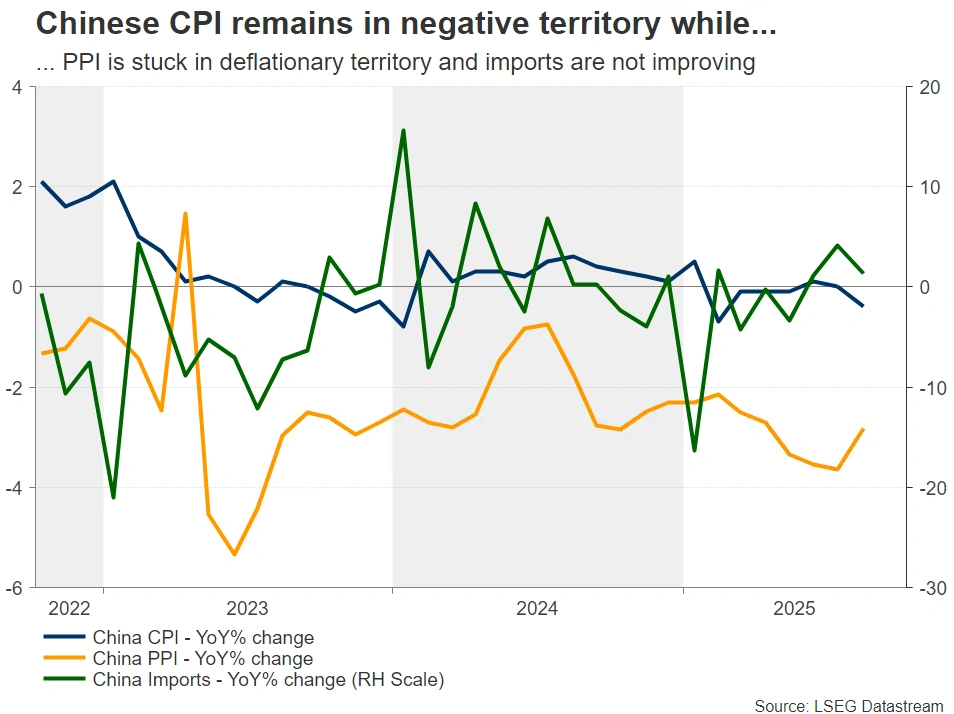

Is China gearing for new support measures and a looser PBoC stance?

With the Golden Week completed, it is back to business for China. Next week’s calendar includes trade balance figures, and, most importantly, the September CPI and PPI reports. China continues to battle deflation, with the numerous support packages so far failing to boost the domestic economy. Notably, Chinese authorities are preparing for the Fourth Plenum of the 20th Central Committee of the Communist Party scheduled for October 20–23, which could unlock further actions.

Interestingly, the World Bank upgraded its 2025 and 2026 GDP projections this week, citing strong consumption, resilient exports and further policy support. During next week’s annual IMF-WB meeting, the October 2025 World Economic Outlook (WEO) will be published, with a strong possibility of a similar upgrade in, partly recognizing that tariffs are probably going to be less disruptive than widely anticipated.

Additionally, the channel of communication between China and the US will be activated again, as despite numerous meetings, a comprehensive agreement is still elusive. Hence, trade-related headlines could make their way to the top of daily news reports.

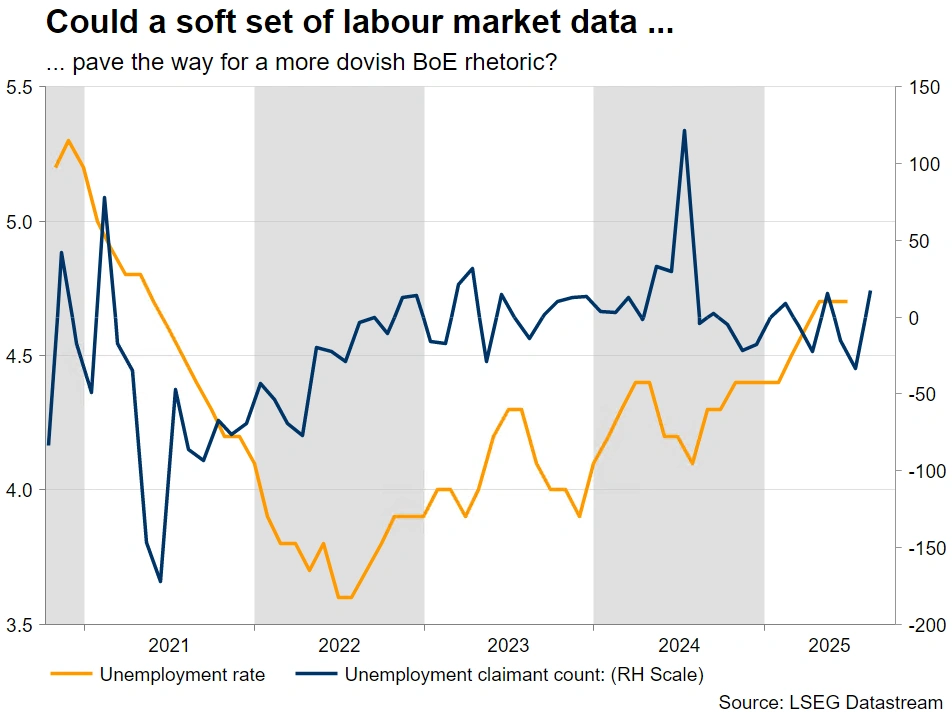

Key UK jobs data, Pound is in need of a boost

With the market confident that the early November meeting will not produce a rate move, key UK labour market data will be in the spotlight next week. Following the strong Q2 performance, momentum has probably stalled in the third quarter of 2025, as seen by monthly GDP industrial production and S&P Global PMI surveys. A negative print in Tuesday’s claimant count change could render the August positive figure an outlier to the recent improving trend.

Meanwhile, the Labour government is preparing for the late November budget, with tax increases looking unavoidable. Such an outcome might force the BoE to adopt a more dovish stance, acting as an extra headwind for the pound, which has managed to recover some of the lost ground against the euro, on the back of rising political risks in the eurozone.

Mixed fortunes for commodity currencies

While the kiwi has been underperforming against the US dollar following the surprising 50bps RBNZ rate cut, both the loonie and the aussie have fared better. Starting with the former, there have been a slight infusion of confidence following Wednesday’s US-Canada meeting about tariffs and the USMCA, putting a pause to the recent US dollar strength.

Similarly, aussie/dollar has stabilized, retracing from a one-year high, as the RBA continues to stay on the sidelines following the somewhat hawkish meeting in late September. This week’s inflation-related releases supported the RBA’s view that the inflation deceleration has slowed, with the focus now shifting to next week’s jobs data.

The RBA also believes that the “labour market conditions remain a little tight”. Thursday’s employment data could further support this view, keeping the chances of another RBA cut low and potentially boosting the aussie – especially if the US dollar weakens following the likely US government reopening and investors begin to price in softer US data.