Sample Category Title

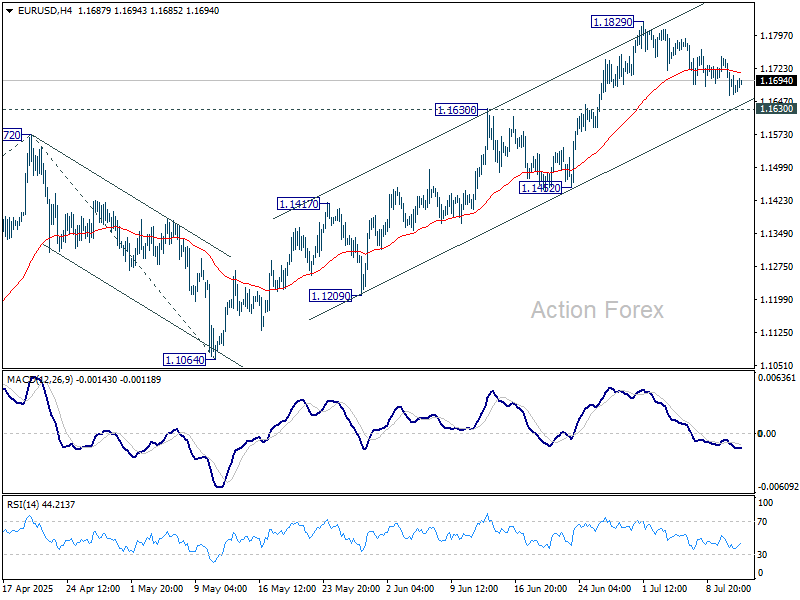

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1659; (P) 1.1705; (R1) 1.1746; More...

EUR/USD is still extending correction from 1.1829 and intraday bias stays neutral. Strong support is expected from 1.1630 resistance turned support to bring rebound. On the upside, firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, sustained break of 1.1630 will bring deeper fall to 55 D EMA (now at 1.1459) instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

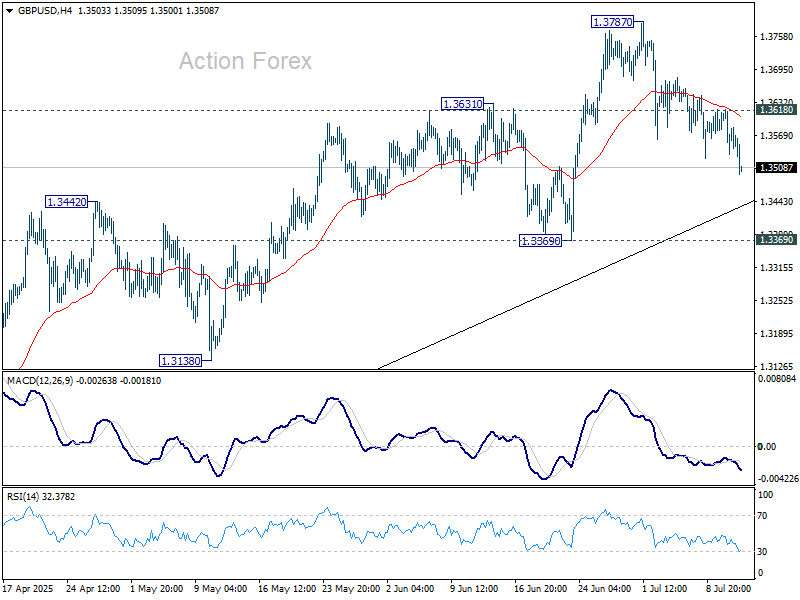

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3534; (P) 1.3577; (R1) 1.3620; More...

Intraday bias in GBP/USD remains neutral for the moment. Corrective pullback from 1.3787 could extend lower. But downside is expected to be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2985) holds, even in case of deep pullback.

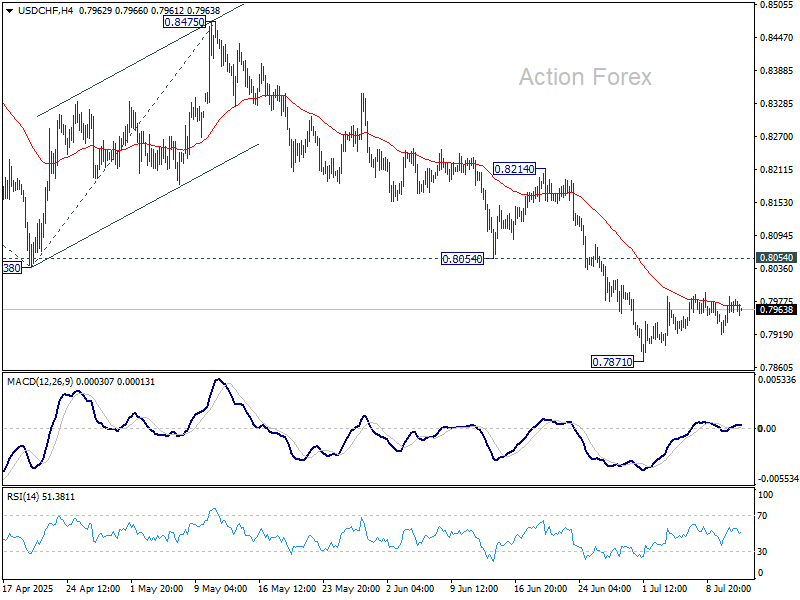

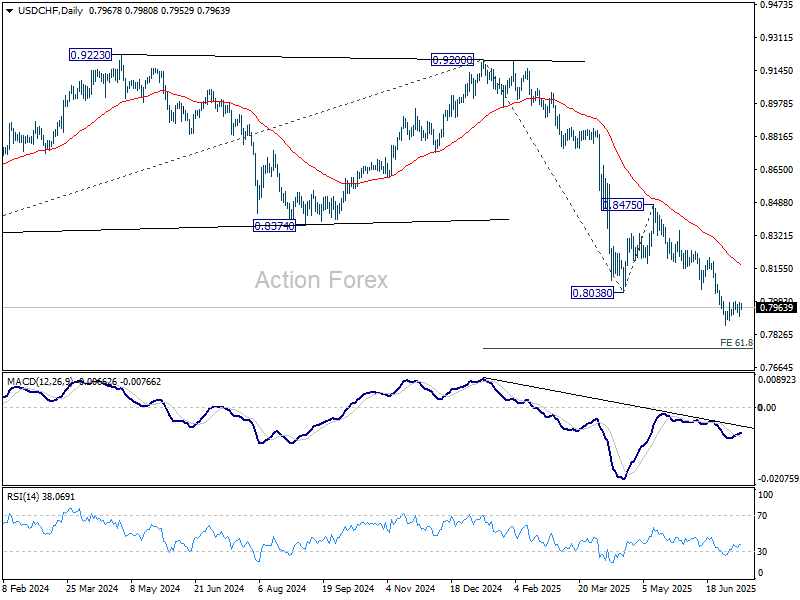

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7930; (P) 0.7959; (R1) 0.7998; More….

Intraday bias in USD/CHF stays neutral and outlook is unchanged. Corrective pattern from 0.7871 could extend higher. But upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

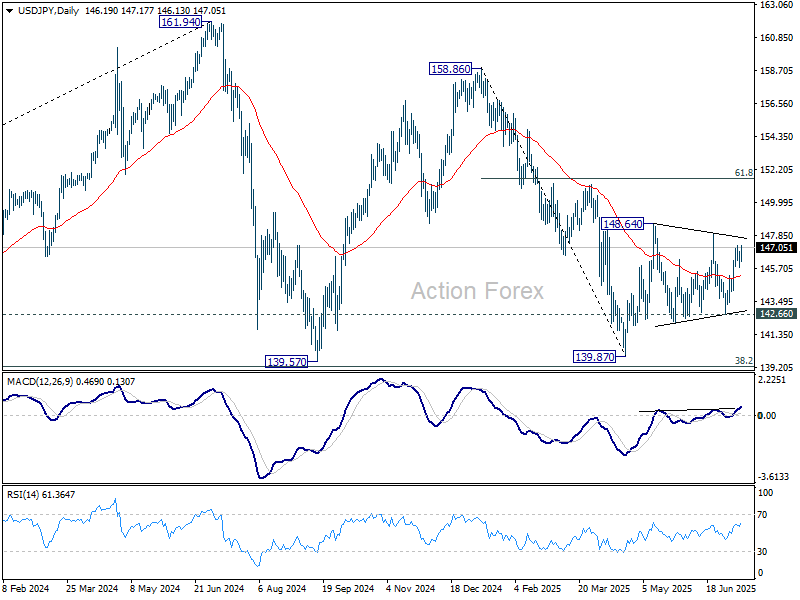

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.74; (P) 146.27; (R1) 146.77; More...

Outlook in USD/JPY remains unchanged as range trading continues. Intraday bias stays neutral. On the upside, firm break of 148.01 resistance will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.66 will bring deeper fall back to retest 139.87 low.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Canada’s Economy Surprises With a Healthy Job Gain in June

Surprise! Canada's economy generated 83k new jobs in June (+0.4% month/month), much better than the consensus expectation for a flat reading. However, the gains were driven by a 70K gain in part-time positions.

The unemployment rate fell one tick to 6.9% after trending upwards for three months. Despite the labour force continuing to grow faster than we had expected (+0.3% m/m), employment gains outpaced it.

Looking by sector, wholesale and retail trade led the way, gaining 34k jobs (+1.1% m/m), followed by gains in health care and social assistance (17k, +0.6% m/m). Notably, manufacturing gained 10.5k jobs, although, employment there is still down 1.4% versus a year ago. Most other industries gained jobs, with agriculture (-12.5k, -2.6% m/m), and "other" services standing out with losses (-8.5k, -1.1% m/m).

Wage growth cooled in June. Average hourly wages rose 3.2% versus a year ago, down from 3.4% in May.

Key Implications

Canada's labour market bucked its weakening trend in June. The unemployment rate fell, and most sectors saw job gains. However, one month isn't going to turn the page on what is a much cooler labour market relative to a year ago. With President Trump making new threats for a higher 35% tariff rate on Canadian goods just last night, certainty for many Canadian businesses doesn't appear to be improving any time soon.

The Bank of Canada gets its next kick at the can on July 30th . Today's jobs report is another tick in the resilience tally, but next Tuesday's June inflation report is likely to be the bigger factor in the Bank's deliberations, given recent hotter-than-expected inflation readings. We think a strong argument for further rate cuts remains in Canada, we'll soon see if the BoC agrees.

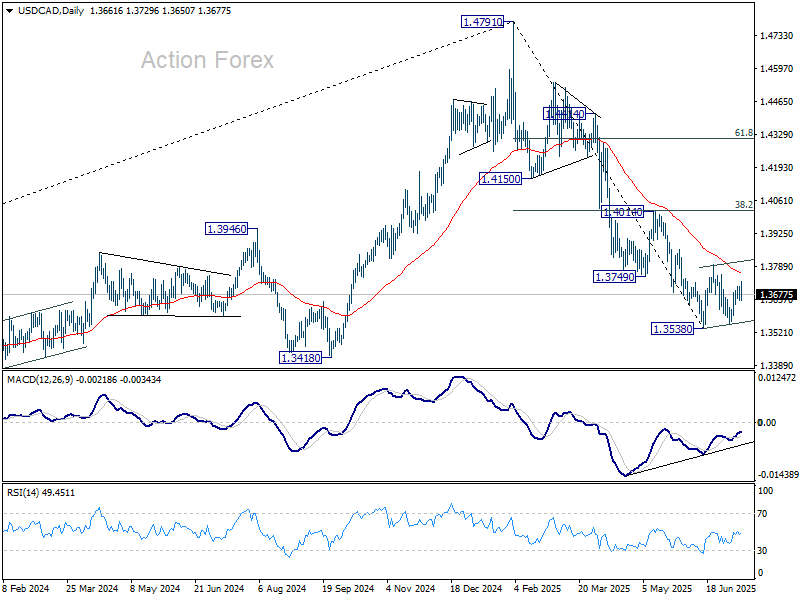

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3636; (P) 1.3666; (R1) 1.3692; More...

USD/CAD retreated after a brief spike to 1.3729 and intraday bias is turned neutral again. Overall, consolidation pattern from 1.3538 could still extend. Above 1.3729 will target 1.3797 resistance and possibly above. On the downside, however, break of 1.3637 minor support will bring retest of 1.3538/55 support zone instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Loonie Rebounds on Strong Jobs Data, Sterling Hit by GDP Miss

Canadian Dollar staged an impressive rebound after June’s employment report far outpaced expectations, reviving hopes that BoC can stay on hold despite mounting trade pressures. The release comes just after US President Donald Trump announced sweeping 35% tariffs on Canadian imports, which initially drove the Loonie lower.

With interest rates sitting at 2.75%—a level seen as largely neutral, today's’s data gives BoC additional justification to delay any further policy action. Policymakers are likely to wait and evaluate the full effects of the tariffs before committing to the next move.

Meanwhile, in the UK, recession risks are rising after GDP contracted for a second straight month. The economic miss raises doubts about BoE’s current path of gradual, quarterly rate cuts. Market pricing now reflects over 75% odds of a 25-basis-point BoE cut in August. BoE had projected 0.25% GDP growth in Q2, but unless June’s GDP rebounds sharply, a quarterly contraction is now a real possibility.

On the FX front, Aussie remains the top performer of the week. while Dollar and Swiss Franc are next in line. Yen is stuck at the bottom, with Pound and Euro also under pressure. Loonie’s rebound keeps it in the middle, alongside Kiwi

As the week winds down, risk appetite appears to be cooling. US and European equities had powered ahead earlier, but signs of fatigue are emerging. Traders are lightening positions ahead of the weekend, especially as the European Union may be next in line to receive Trump’s tariff demands.

In Europe, at the time of writing, FTSE is down -0.56%. DAX is down -1.01%. CAC is down -1.09%. UK 10-year yield is up 0.005 at 4.606. Germany 10-year yield is up 0.008 at 2.713. Earlier in Asia, Nikkei fell -0.19%. Hong Kong HSI rose 0.46%. China Shanghai SSE rose 0.01%. Singapore Strait Times rose 0.30%. Japan 10-year JGB yield rose 0.009 to 1.506.

Canada job growth surges to 83k in June, unemployment rate unexpectedly falls

Canada's labor market posted a strong rebound in June, adding 83,000 jobs, far above expectations of just 900. Unemployment rate dipped from 7.0% to 6.9%, defying forecasts of an increase to 7.1%.

The decline ends a three-month stretch of rising joblessness and was supported by a 0.1 percentage point uptick in the employment rate to 60.9%. Total hours worked also rose by 0.5% on the month, putting them 1.6% higher than a year earlier—a sign of sustained underlying momentum.

Wage growth continued to moderate, with average hourly earnings rising 3.2% yoy from a year ago, down from May’s 3.4% yoy.

ECB’s Schnabel: Inflation on track, economy resilient, bar for further rate cut very high

ECB Executive Board member Isabel Schnabel signaled in an interview with Econostream Media that there is urgency for further easing. Schnabel noted that inflation is now projected to be at 2% target over the medium term, and expectations remain "well anchored", while interest rates are in a "good place". She added that "the bar for another rate cut is very high".

Schnabel emphasized that there is "no risk of a sustained undershooting" and that core inflation is forecast to meet target throughout the horizon. She also downplayed concerns over the disinflationary impact of Euro strength, calling such fears “exaggerated” given limited pass-through effects. Schnabel argued that temporary factors such as low energy inflation are unlikely to derail the ECB’s price stability goals.

On the growth front, Schnabel was notably upbeat. Recent PMI data suggesting further recovery ahead. Manufacturing indicators such as new orders and export demand have all reached three-year highs, pointing to more than just temporary momentum. Combined with record-low unemployment and the expectation of a large fiscal impulse, she argued that risks to the growth outlook are now "more balanced", reducing the case for near-term rate action.

UK GDP shrinks -0.1% mom in May, but underlying momentum still holds

UK GDP unexpectedly contracted by -0.1% mom in May, missing expectations for 0.1% mom growth. The weakness was driven by a sharp -0.9% mom drop in industrial production and a -0.6% mom fall in construction output, partially offset by a modest 0.1% mom gain in services—the largest sector of the economy.

Still, broader momentum remains positive. Real GDP rose 0.5% in the three months to May, thanks to steady growth in services (+0.4%) and solid gains in construction (+1.2%). Production also rose 0.2%.

New Zealand BNZ manufacturing rises to 48.8, conditions still very tough

New Zealand’s manufacturing sector showed modest signs of stabilization in June, with the BusinessNZ Performance of Manufacturing Index rising from 47.4 to 48.8. While still signaling contraction, the gain was underpinned by an encouraging rebound in new orders, which jumped from 45.4 to 51.2—breaking back into expansion. Employment (47.9) and production (48.6) also improved slightly, though both remained under the 50 threshold. The headline PMI remains well below the historical average of 52.5.

The proportion of negative comments from respondents held steady at 65.5% (May 64.5), with widespread concerns over weak consumer demand, high living costs, and a murky economic outlook. Input cost pressures and a drop in construction activity also continue to weigh on manufacturing sentiment.

BNZ Senior Economist Doug Steel said that despite hopes of recovery, "conditions are still very tough." All key sub-indices remain below their long-run averages, highlighting that while some green shoots are emerging, the overall manufacturing environment is still struggling to gain traction.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3636; (P) 1.3666; (R1) 1.3692; More...

USD/CAD retreated after a brief spike to 1.3729 and intraday bias is turned neutral again. Overall, consolidation pattern from 1.3538 could still extend. Above 1.3729 will target 1.3797 resistance and possibly above. On the downside, however, break of 1.3637 minor support will bring retest of 1.3538/55 support zone instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Canada job growth surges to 83k in June, unemployment rate unexpectedly falls

Canada's labor market posted a strong rebound in June, adding 83,000 jobs, far above expectations of just 900. Unemployment rate dipped from 7.0% to 6.9%, defying forecasts of an increase to 7.1%.

The decline ends a three-month stretch of rising joblessness and was supported by a 0.1 percentage point uptick in the employment rate to 60.9%. Total hours worked also rose by 0.5% on the month, putting them 1.6% higher than a year earlier—a sign of sustained underlying momentum.

Wage growth continued to moderate, with average hourly earnings rising 3.2% yoy from a year ago, down from May’s 3.4% yoy.

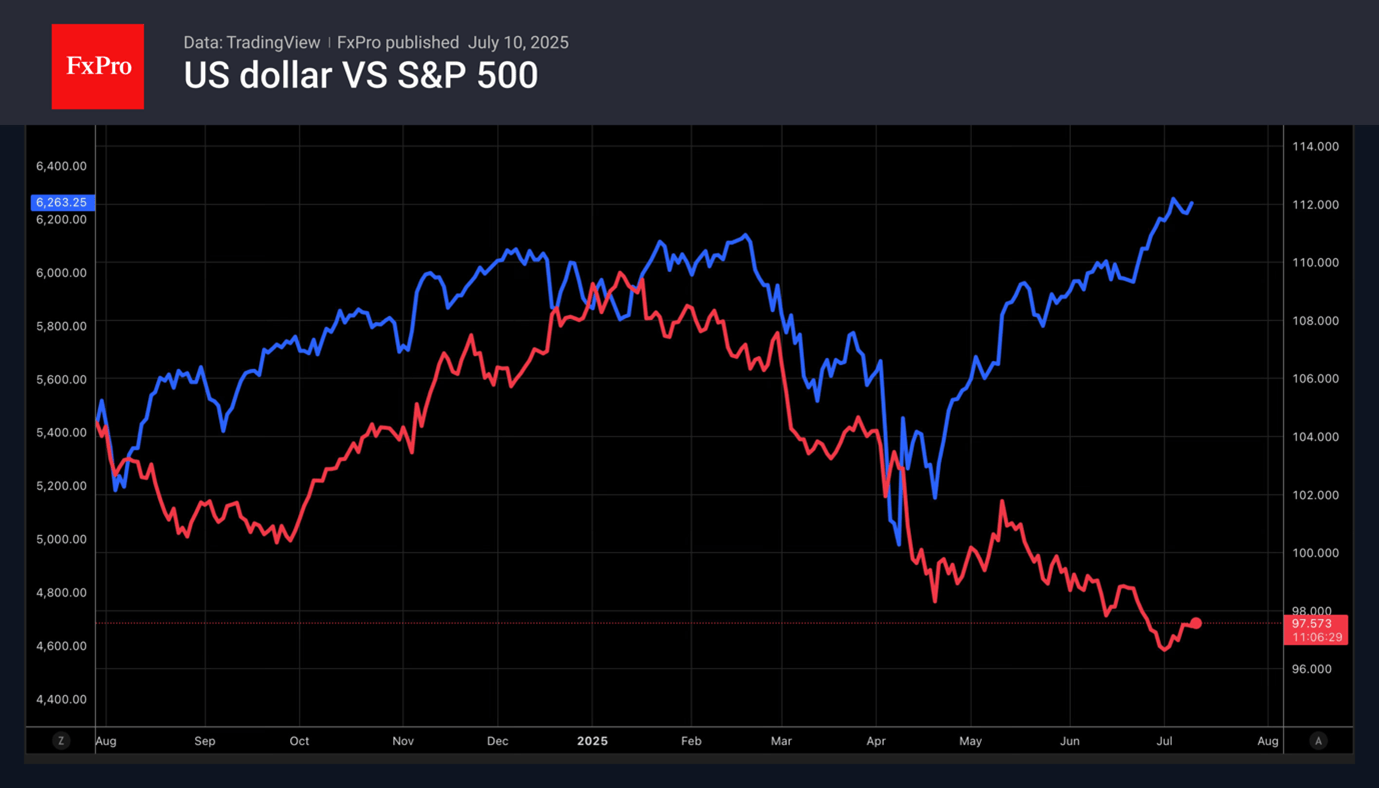

Markets Again in Risk-on/Risk-off Mode

US dollar

The escalation of trade conflicts has led to a temporary strengthening of the US dollar. Donald Trump has sent numerous letters to various countries specifying the size of tariffs. They will come into effect on August 1st. Until then, the White House is open to negotiations. There are rumours in the market that the United States will soon conclude trade deals with India, Taiwan, and the European Union.

According to Deutsche Bank, the average US tariff is 18.7%. This is lower than the 22% that was in place on Independence Day. However, the figure is still high. Such import duties increase the risks of an economic slowdown and accelerating inflation, but there is no talk of a recession. Therefore, the USD index did not fall as it did in April.

Investors have moved away from the ‘sell America’ strategy. As a result, the dollar and US stock indices have diverged. The greenback is once again behaving as a safe-haven asset, falling when risk appetite rises and vice versa.

Stock indices

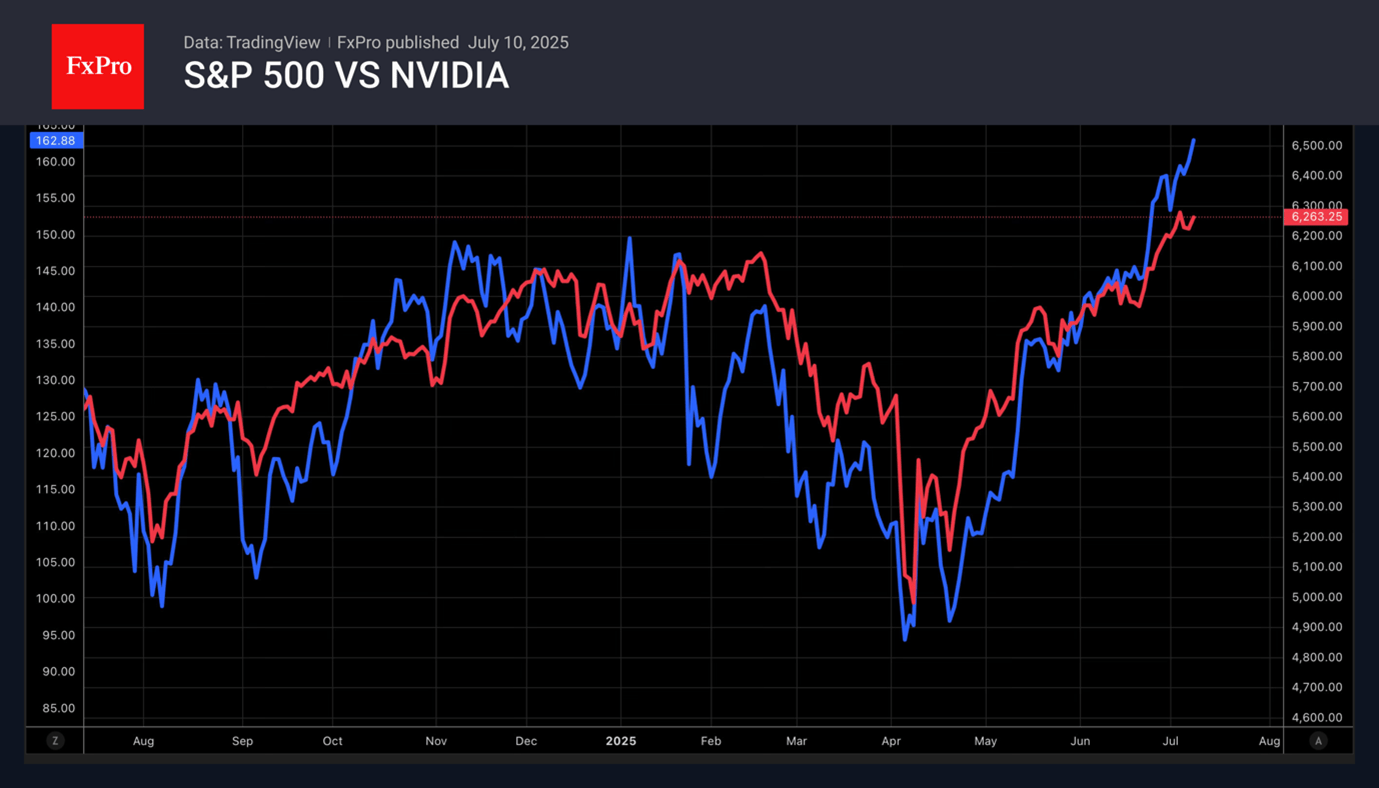

After a slight dip due to Donald Trump’s letters, the S&P 500 began to rise again. The stock market perceived the escalation of the trade conflict as prolonging the delay. Investors bought up the dip. The US economy is strong, inflation is slowing, and corporate profits are high. In such conditions, the potential for a correction in the broad stock index is limited. Bank of America raised its forecasts for the index of the 500 largest companies to 6,300 and 6,600 at the end of the year and in 12 months. Goldman Sachs sees the market at 6,600 and 6,900.

Technology corporations are leading the stock market rally. NVIDIA became the first company in the world whose capitalisation exceeded $4 trillion. Since the beginning of the year, its shares have risen by 20%, and since 2023 by more than 1000%. This allowed the Nasdaq Composite to update its record highs. The S&P 500 came within arm’s reach of them.

Stock indices are supported by expectations of a resumption of the Fed’s monetary policy easing cycle and a successful auction of $39 billion in 10-year Treasury bonds. High demand led to a decline in yields, and the S&P 500 is seeing new record highs.

UK GDP Contracts, Pound Dips

The British pound continues to have a quiet week. In the European session, GBP/USD is trading at 1.3530, down 0.30% on the day.

UK economy contracts in May

The UK wrapped up the week on a down note, as GDP contracted in May by 0.1% m/m. This followed a 0.3% decline in April and missed the consensus of 0.1%. The decline was driven by a 1% decline in manufacturing and a 0.6% contraction in construction, which cancelled out a 0.1% expansion in services.

The GDP contractions in April and May point to a weak second quarter of growth, after an impressive 0.7% gain in the first quarter. The economic landscape remains uncertain and the Bank of England has projected weak growth of 1% for 2025. Governor Bailey has said that the rate path will be "gradually downwards" but hasn't hinted as to the timing of the next cut.

The weak GDP data supports the case for an August rate cut, even though headline inflation is running at 3.4% and core inflation at 3.5%, well above the BoE's target of 2%. The money markets have priced in a quarter-point cut in August at 80%, which would lower the cash rate to 4.0%.

The BoE released its financial stability report earlier in the week, noting that the outlook for UK growth over the coming year is "a little weaker and more uncertain". The Bank highlighted President Trump's tariffs and the conflict in the Middle East. The UK has recently signed a trade deal with the US but some tariffs on UK products remain in effect.

GBPUSD Technical

- GBP/USD is testing support at 1.3534. Below, there is support at 1.3491

- The next resistance lines are 1.3577 and 1.3620

GBPUSD 1-Day Chart, July 11, 2025