Sample Category Title

Pound Recovers as UK CPI Edges Lower

The British pound has stabilized on Wednesday. In the European session, GBP/USD is trading at 1.3551, up 0.28% on the day. The US dollar showed broad strength on Tuesday and GBP/USD declined 1.05% and fell to a three-week low.

UK inflation ticks lower to 3.4%

UK inflation for May edged lower to 3.4% y/y, down from 3.5% in April and matching the market estimate. The driver behind the deceleration was lower airline prices and petrol prices. Services inflation, which has been persistently high, eased to 4.7% from 5.4%. Monthly, CPI gained 0.2%, much lower than the 1.2% gain in April and matching the market estimate.

Core CPI, which excludes food and energy, fell to 3.5% in May, down from 3.8% a month earlier and below the market estimate of 3.6%. Monthly, the core rate rose 0.2%, sharply lower than the 1.4% spike in April and in line with the market estimate. This marked the lowest monthly increase in four months.

The Bank of England will be pleased that core CPI moved lower but the inflation numbers are still too high for its liking. Headline CPI had been below 3% for a year but has jumped well above 3% in the past two months.

BoE policymakers won't have much time to digest today's inflation report as the central bank makes its rate announcement on Thursday. The markets are widely expecting the BoE to maintain the cash rate at 4.25%,

Investors will be keeping a close eye on the meeting, looking for hints of a rate cut later in the year. The UK economy contracted in April and with wages falling and unemployment rising, there is pressure for the BoE to lower rates, but that is risky with inflation well above the BoE's 2% inflation target.

US retail sales sink

US retail sales slumped in May, falling 0.9% m/m. This was well below the revised -0.1% reading in April and worse than the market estimate of -0.7%. Annually, retail sales fell to 3.3%, down sharply from a revised 5.0%.

Consumers are wary about the economy and anxiety over Trump's tariffs has weighed on consumer spending. If additional key US data heads lower, this will increase pressure on the Federal Reserve to lower interest rates.

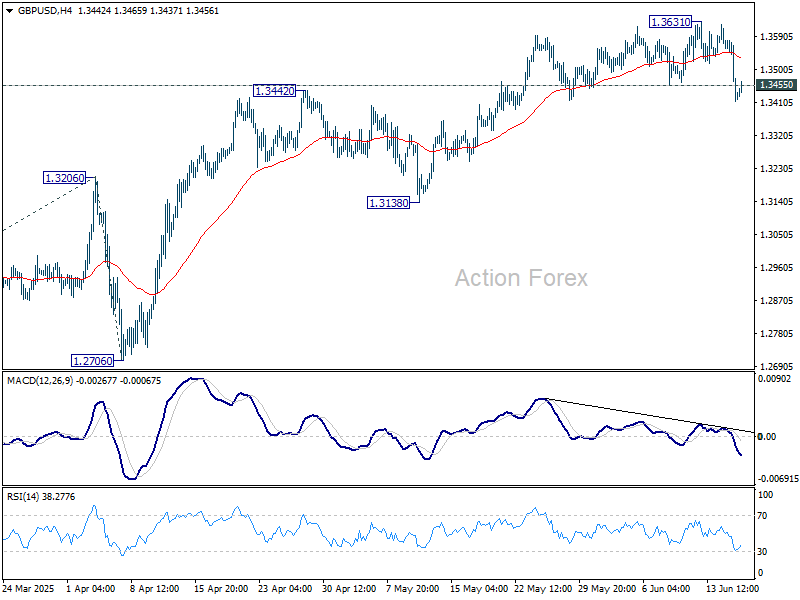

GBP/USD Technical

- GBP/US is putting pressure on resistance at 1.3480. Above, there is resistance at 1.3545

- 1.3364 and 1.3299 are providing support

GBPUSD 4-hour Chart, June 18, 2025

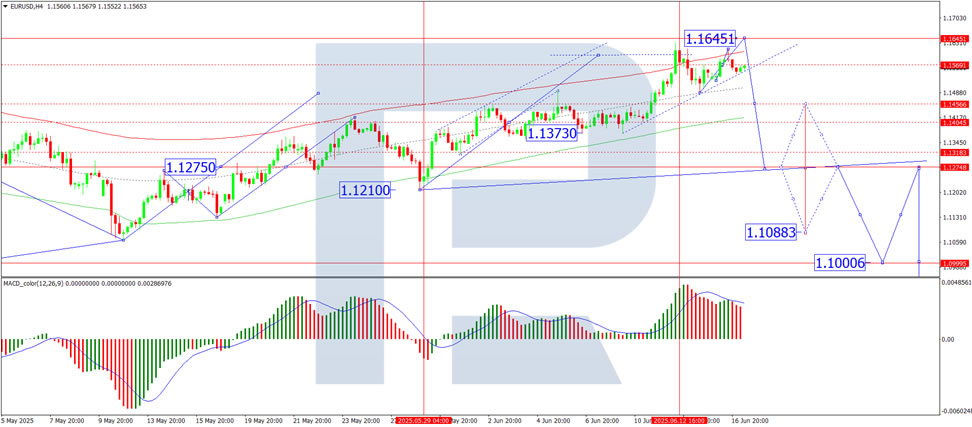

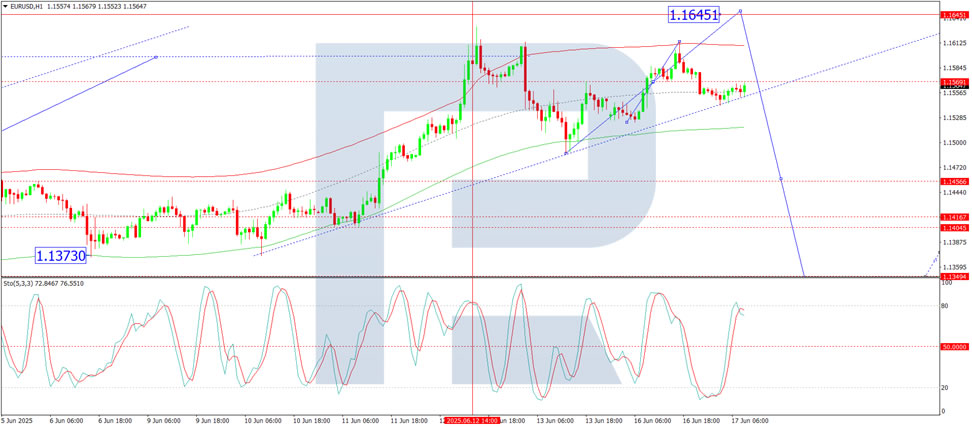

EUR/USD Faces Rejection, USD/JPY Recovers Above 145.00

EUR/USD declined from the 1.1640 resistance and traded below 1.1550. USD/JPY is rising and might gain pace above the 145.50 resistance.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline after a strong surge above the 1.1600 zone.

- There is a connecting bearish trend line forming with resistance at 1.1545 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 144.00 and 145.00 levels.

- There is a key bullish trend line forming with support at 144.80 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair rallied above the 1.1600 resistance zone before the bears appeared, as discussed in the previous analysis. The Euro started a fresh decline and traded below the 1.1550 support zone against the US Dollar.

The pair declined below 1.1520 and tested the 1.1475 zone. A low was formed near 1.1475 and the pair started a consolidation phase. There was a minor recovery wave above the 1.1495 level.

The pair tested the 23.6% Fib retracement level of the downward move from the 1.1614 swing high to the 1.1475 low. EUR/USD is now trading below 1.1550 and the 50-hour simple moving average. On the upside, the pair is now facing resistance near the 1.1505 level.

The next key resistance is at 1.1545 and the 50% Fib retracement level of the downward move from the 1.1614 swing high to the 1.1475 low. There is also a connecting bearish trend line forming with resistance at 1.1545.

The main resistance is near the 1.1580 level. A clear move above the 1.1580 level could send the pair toward the 1.1615 resistance. An upside break above 1.1615 could set the pace for another increase. In the stated case, the pair might rise toward 1.1650.

If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.1475. The next key support is at 1.1450. If there is a downside break below 1.1450, the pair could drop toward 1.1400. The next support is near 1.1350, below which the pair could start a major decline.

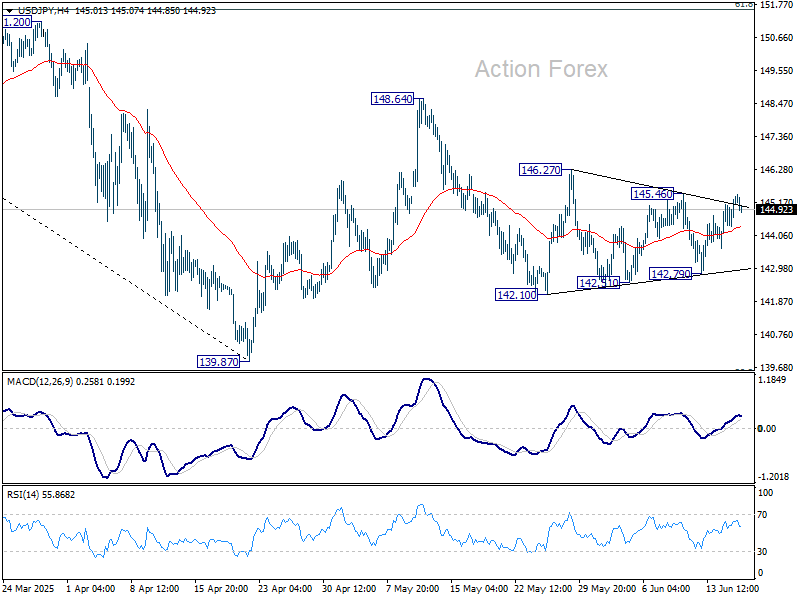

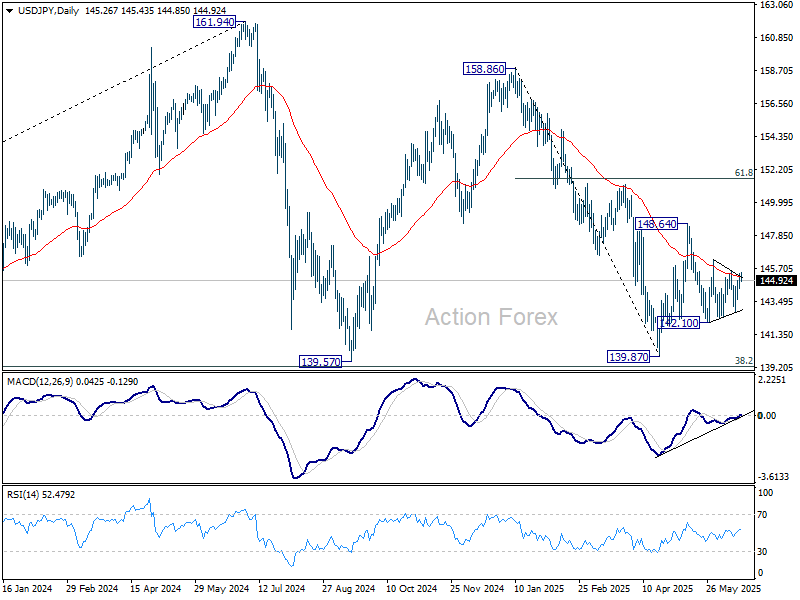

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a fresh upward move from the 142.80 zone. The US Dollar gained bullish momentum above 143.40 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 144.00. The pair climbed above 145.00 and traded as high as 145.43 before there was a downside correction. It is now moving lower toward the 23.6% Fib retracement level of the upward move from the 142.79 swing low to the 145.40 high.

The current price action above the 144.50 level is positive. There is also a key bullish trend line forming with support at 144.80. Immediate resistance on the USD/JPY chart is near 145.40.

The first major resistance is near 146.20. If there is a close above the 146.20 level and the RSI moves above 60, the pair could rise toward 147.50. The next major resistance is near 148.00, above which the pair could test 148.80 in the coming days.

On the downside, the first major support is 144.80 and the trend line. The next major support is visible near the 144.40 level. If there is a close below 144.40, the pair could decline steadily.

In the stated case, the pair might drop toward the 143.40 support zone and the 76.4% Fib retracement level of the upward move from the 142.79 swing low to the 145.40 high. The next stop for the bears may perhaps be near the 142.80 region.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

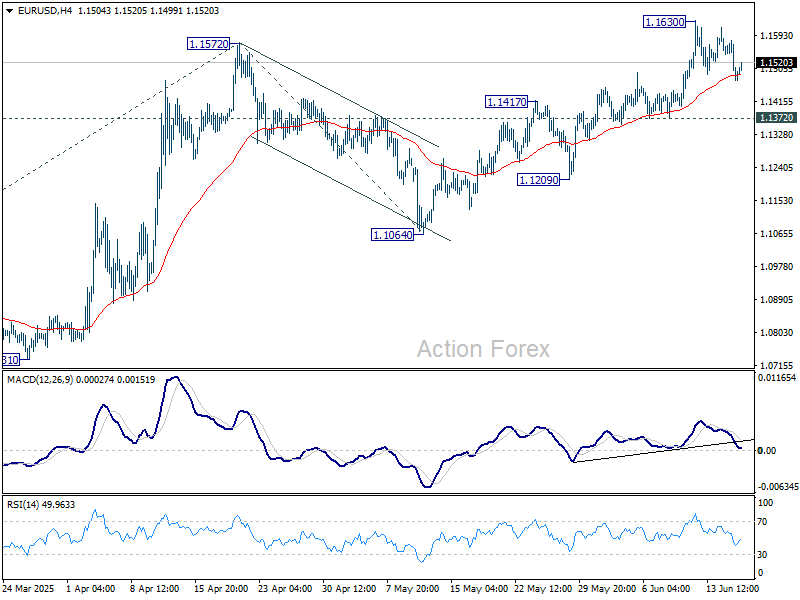

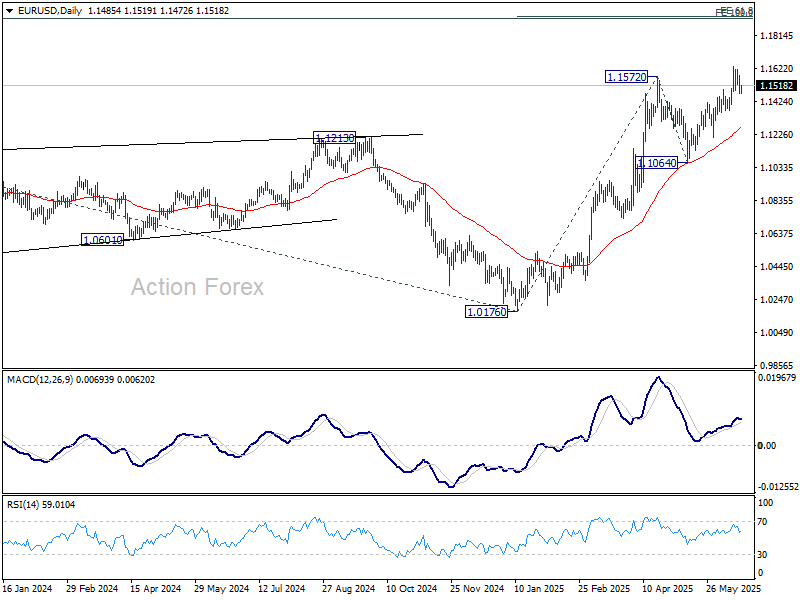

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1443; (P) 1.1512; (R1) 1.1548; More...

Intraday bias in EUR/USD remains neutral at this point. With 1.1372 support intact, further rally is expected. Break of 1.1572 will extend the rise from 1.0176. Next target is 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, break of 1.1372 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

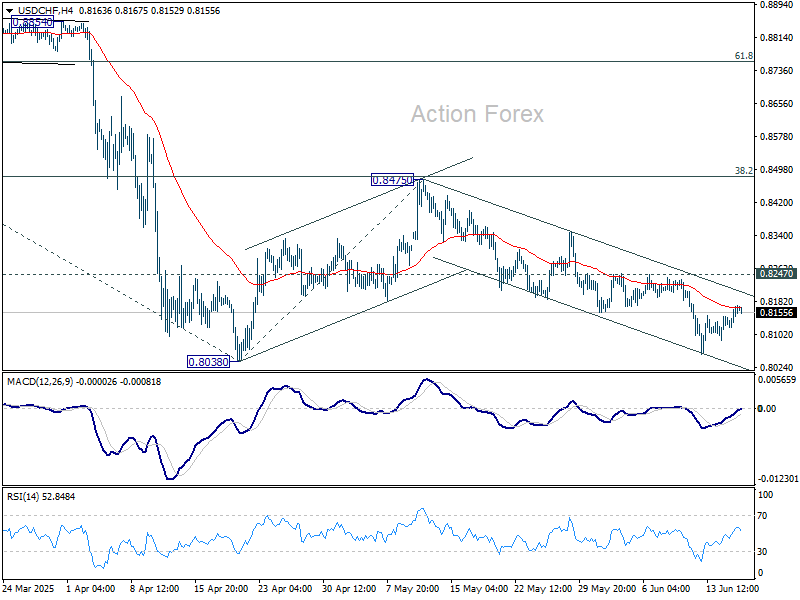

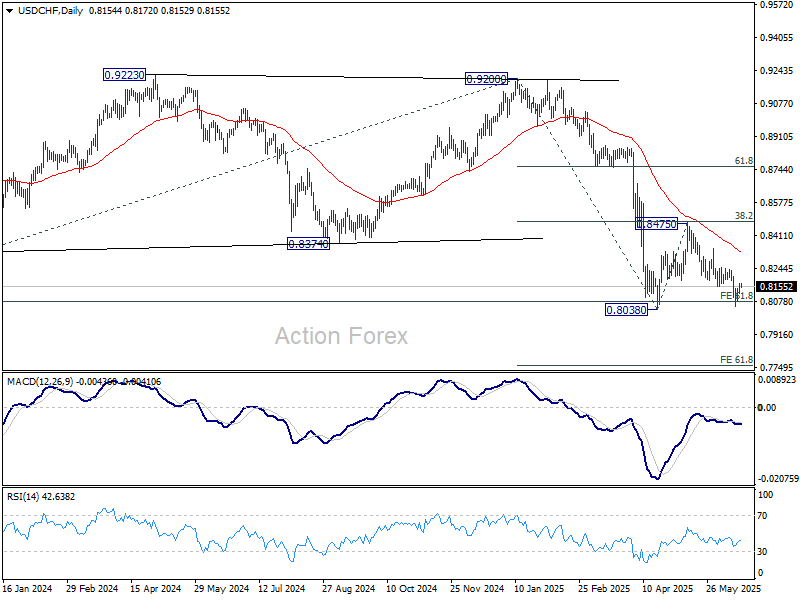

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8133; (P) 0.8153; (R1) 0.8184; More….

Intraday bias in USD/CHF remains neutral at this point. On the upside, break of 0.8247 resistance will argue that corrective pattern from 0.8038 is starting the third leg. Bias will be turned back to the upside for 0.8475 resistance again. However, firm break of 0.8038 will resume larger down trend. Next target will be 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8656) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.67; (P) 145.02; (R1) 145.65; More...

While USD/JPY's rebound from 142.79 extended higher, upside is capped by 145.46 resistance. Intraday bias stays neutral for the moment. On the downside, break of 142.10 support will resume the fall from 148.64 to retest 139.87 low. On the upside, above 145.46 will turn bias to the upside for 146.27 first. Firm break there will target 148.64 resistance.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

The Only Needle in Fed’s Compass is Inflation

Markets

Stronger than expected US retail sales in the control group briefly interrupted an outperformance of US Treasuries yesterday. Spending in these selected goods categories feeds into the government’s GDP calculation and rose by 0.4% M/M (vs 0.3% expected and with small upward revision to April numbers). It marked a contrast with headline retail sales falling by 0.9% M/M, dragged down in particular by auto and gas sales. Slightly weaker May industrial production numbers (-0.2% M/M) and further deteriorating homebuilder sentiment in June supported a rapid turnaround in the temporary setback for US Treasuries with the US yield curve significantly bull flattening during US trading hours. Turned out that something else was cooking. First it was confirmed that the Fed will meet on June 25 on changes to the supplementary ratio. Overnight, people close to discussions suggested that top US bank regulators want to change the enhanced supplementary ratio which applies to the largest US banks. They want to reduce this key capital buffer by up to 1.5 ppt from the current 5%. Whether or not US Treasuries will be carved out from the calculation isn’t clear. US Treasury Secretary Bessent last month suggested that lowering the eSLR rule could easily reduce Treasury yields by tens of basis points by freeing up balance sheet to enhance buying/liquidity in the Treasury market. Critics warn that banks might opt to use the additional room for capital distributions to shareholders rather than for Treasury market intermediation. Ongoing discussions in any case prove that authorities start using every trick in the book to prevent an unwarranted further increase in (LT) bond yields as monetary policy is focused on fighting (upside) inflation (risks). US yields lost 1.5 bps (2-yr) to 6.5 bps (30-yr) yesterday. The German yield curve bear flattened slightly with yields rising by up to 2.6 bps (2-yr). Stock markets and oil prices for now err on the side of caution when it comes to a possible escalation in the Israeli-Iran conflict. Key equities indices lost 0.5%-1% with Brent crude sticking above $75/b. The dollar profited from the risk/oil-combination and proposals to alleviate potential stress on the Treasury market with EUR/USD dipping towards 1.15.

The US central bank will keep its policy rate unchanged tonight (4.25%-4.50%). The updated Summary of Economic Projections likely shows downward GDP revision and upwardly changed CPI forecasts. As long as the US labour market shows no signs of cracking, the only needle in the Fed’s compass is inflation. Risks for the dot plot are equally skewed to the hawkish side. Despite the ongoing inflation crusade and while we’re convinced that the Fed will keep a steady course over summer, we have the feeling that markets are eager to react to any, if any, soft elements in the press statement or in Powell’s press conference. Together with geopolitical risks, it makes us err on the side of caution given tomorrow’s US public holiday (Juneteenth).

News & Views

Hungary’s parliament yesterday approved the budget for election year 2026. It entails what prime minister earlier called “Europe’s biggest family tax reduction programme”. From 2026 on, mothers <40 with two children will be exempt from personal income tax. This comes on top of an already-announced doubling of income tax benefits for families in two stages by January. Other key allocations of the budget include HUF 5600bn for family support programs, HUF 4000bn for education and around HUF 3900bn for healthcare. Defense spending should reach over HUF 2000bn, meeting the 2% NATO target. Minimum wages will increase by 13% and there’s a guaranteed 13th month pension. Hungary is targeting a budget deficit of 3.7%, down from an estimated 4.1% this year. Public debt is forecasted to drop from 73.1% this year to 72.3%. It assumes a 4.1% economic growth and inflation of 3.6%.

The EC proposes an overhaul to debt securitization rules in a move that could free up bank capital and stimulate lending as well as help integrate the currently fragmented EU capital markets. The plans include lowering capital charges for banks holding these securitized assets and cutting red tape for investors and issuers. A sense of urgency and political will for the reforms grew amongst others after Mario Draghi’s EU competition report in 2024. EU leaders earlier that year in a special Council meeting also mandated the Commission for “relaunching the European securitization market, including through regulatory and prudential changes, using available room for manoeuvre”. Industry officials welcomed the plans and say it could attract into the hundreds of billions in financing.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3364; (P) 1.3480; (R1) 1.3545; More...

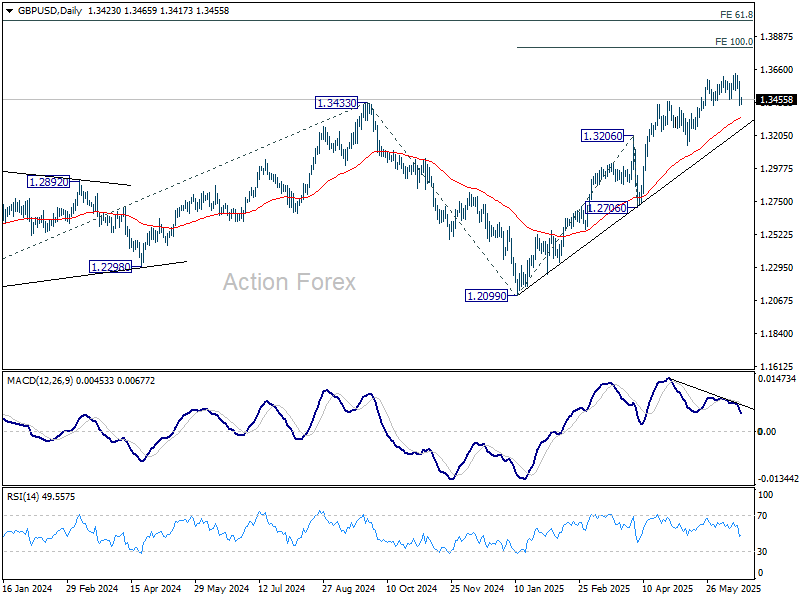

GBP/USD's steep decline confirms short term topping at 1.3631, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for correction to 55 D EMA (now at 1.3328). Strong support could be seen there to bring rebound. Brea of 1.3631 will resume the rally from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. However, sustained break of 55 D EMA will indicate that deeper correction is underway.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.

Sterling Caught Between Inflation Surprise and Escalating Global Tensions; FOMC Next

Sterling weakened sharply overnight as risk appetite deteriorated on growing fears of military escalation in the Middle East. US President Donald Trump raised the stakes with Iran, issuing a public ultimatum to Supreme Leader Khamenei for “unconditional surrender” after claiming “total control” over Iranian airspace. There are intensified concerns that the US could intervene directly.

The recent US–UK trade deal, while politically symbolic, has failed to offer material support to the Pound. Despite exemptions on aerospace and automobile tariffs, the unresolved dispute over steel and aluminum and the conditional structure of the agreement left investors unimpressed. Indeed, Sterling’s weak showing contrasts with resilience seen in Kiwi and Aussie, which benefits from relative insulation from the geopolitical flashpoints.

Yet Sterling found support as European trading got underway, thanks to a firmer-than-expected inflation report. Notably, goods inflation surged to a seven-month high of 2.0%, suggesting that the impact of global tariffs may be starting to show up in consumer prices. Markets still expect BoE to deliver a rate cut in August, but the MPC’s decision on Thursday will be closely watched for signs of shifting sentiment with the Committee

In the broader picture, today’s FOMC meeting may have little short-term impact unless the dot plot shifts decisively. With no surprises expected, traders may look elsewhere for direction. That “elsewhere” may once again be geopolitical developments and trade tensions. Trump continues to ramp up his rhetoric, the EU that they will either make a “fair deal” or pay “whatever we say.” A deadline of July 9 looms for reciprocal tariffs to resume, and negotiations remain mixed at best.

For the week so far, Kiwi and Aussie are currently the stronger ones. Dollar is also on the firmer side. Sterling is at the bottom, followed by Yen, and then Swiss Franc. Euro and Loonie are positioning in the middle.

In Asia, at the time of writing, Nikkei is up 0.77%. Hong Kong HSI is down -1.30%. China Shanghai SSE is up 0.04%. Singapore Strait Times is down -0.44%. Japan 10-year JGB yield is down -0.06 at 1.466. Overnight, DOW fell -0.7%. S&P 500 fell -0.84%. NASDAQ fell -0.91%. 10-year yield fell -0.059 to 4.393.

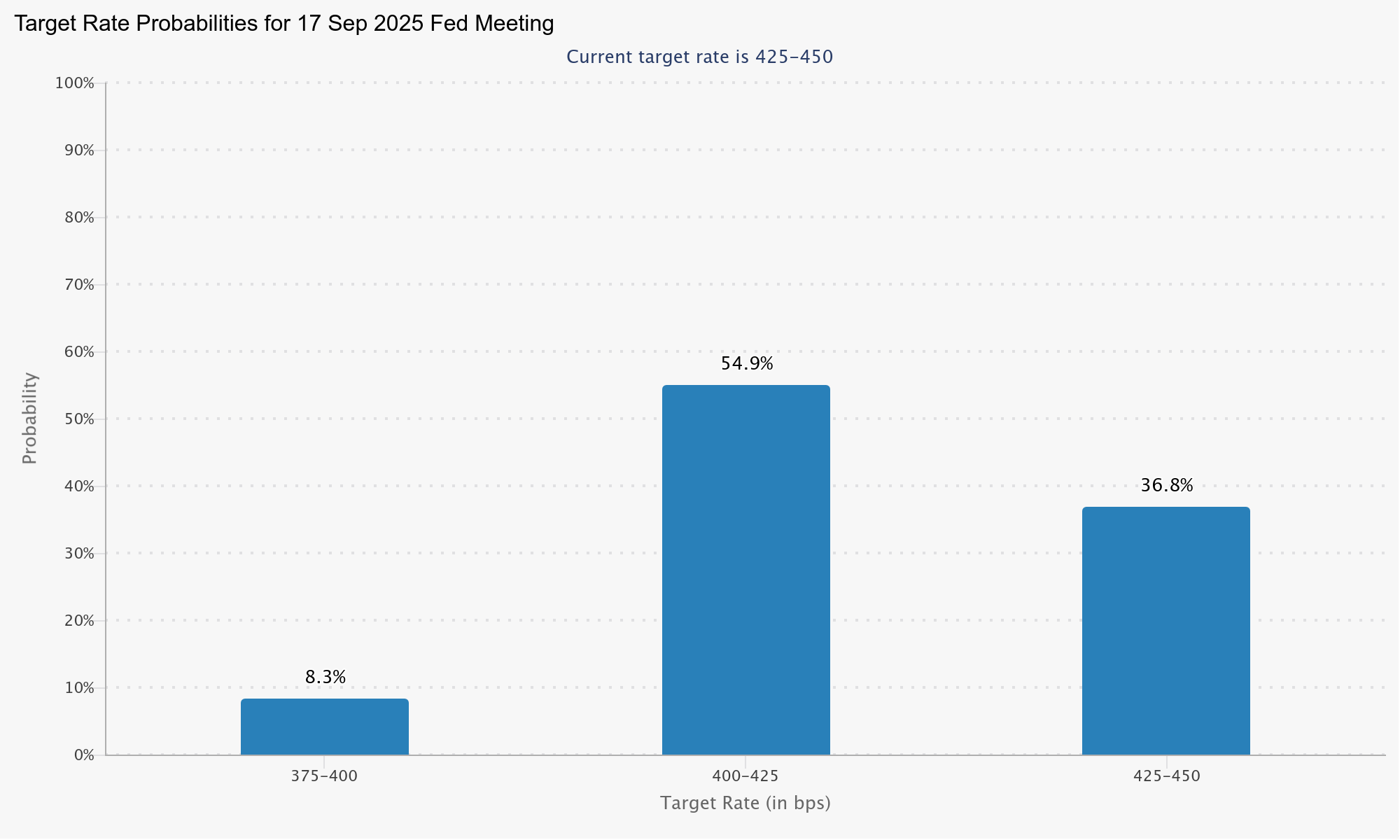

Fed to hold at 4.25–4.50%, eyes on (any) dot plot shift

Fed is all but certain to keep its target rate unchanged at 4.25–4.50% today, with fed fund futures assigning a near-unanimous 99.9% probability to that outcome. Similarly, the likelihood of any move in July is negligible, with markets pricing in an 85% chance that rates will remain on hold. Instead, the focus is on the September meeting, where futures suggest a roughly 63% chance of Fed resume its easing cycle.

The biggest variable in today’s announcement will be the updated Summary of Economic Projections, especially the dot plot. In March, the median forecast signaled two rate cuts in 2025. However, that view was narrowly held, and it would take just two FOMC members adjusting their dots to shift the median forecast to one cut.

However, the inflation and growth projections themselves may offer limited clarity due to the lingering uncertainty over trade policy. The 90-day reciprocal tariff truce expires in early July, and with no clear signal from Washington, Fed is unlikely to factor tariff impacts heavily into its base case just yet.

Chair Jerome Powell is expected to reiterate his recent message that “policy is in a good place” and that there is no rush to cut. Investors will watch closely for any tone shift in his comments on labor market softening and disinflation trends, but the overall message will likely reinforce Fed’s preference for patience. With no new direction expected, market reactions are likely to be limited in the immediate aftermath of the meeting.

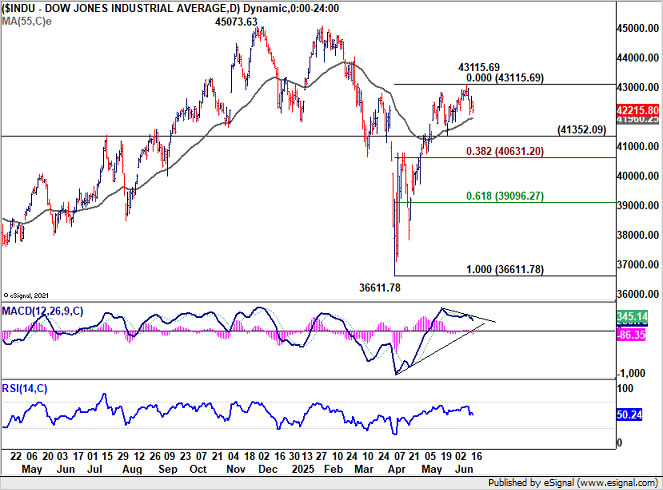

Technically, DOW's rally attempt this week lacks conviction. Bearish divergence condition in D MACD suggests that a short term top could have already formed at 43115.69. Deeper pull back is likely in the near term. Firm break of 41352.09 support will bring deeper fall to 38.2% retracement of 36611.78 to 43115.69 at 40631.20 at least, even still as a corrective move to the rally from 36611.78, not to mention that there is risk of near term bearish reversal.

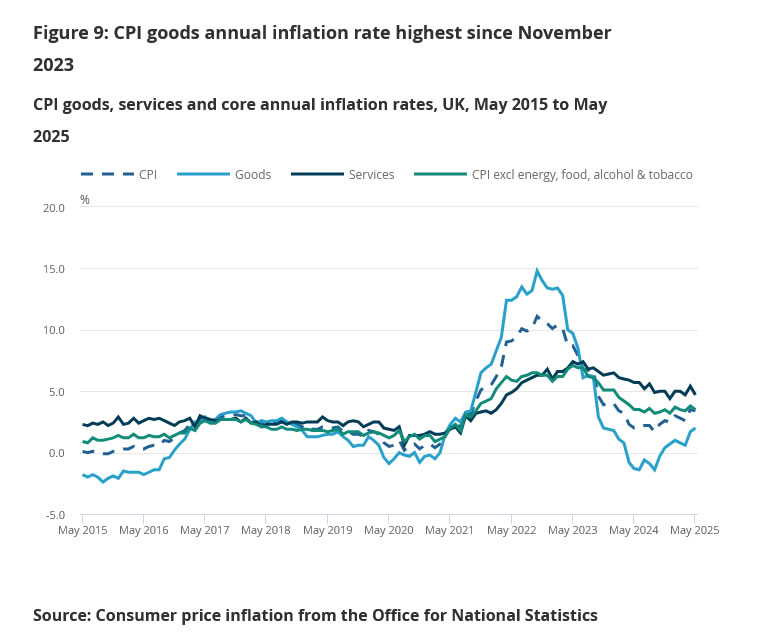

UK CPI slows to 3.3% in May, but goods prices surges to highest since late 2023

UK headline CPI eased from 3.5% yoy to yoy in May, slightly above expectations of 3.3% yoy. Core CPI (excluding energy, food, alcohol and tobacco) also slowed from 3.8% to 3.5%, in line with forecasts.

While the overall trend points to gradual disinflation, markets might pay more attention to the reacceleration in goods prices, which rose to 2.0% yoy, the highest rate since November 2023.

Services inflation, however, showed a more meaningful decline, falling from 5.4% yoy to 4.7% yoy, suggesting underlying pressures are softening.

On a monthly basis, CPI rose by 0.2% mom, matching expectations.

Japan’s exports slide - 1.7% yoy in May as auto tariffs from US take toll

Japan’s trade data for May revealed growing pressure on its export sector, with headline exports falling -1.7% yoy to JPY 8.135T. Imports dropped -7.7% yoy to JPY 8.773T. The resulting trade deficit stood at JPY -637.6B.

Of particular concern was the sharp -11.1% fall in exports to the US, where car shipments plunged -24.7% yoy on the immediate impact of US tariffs.

Despite posting a trade surplus of JPY 451.7B with the US, the bilateral trend was negative. Imports from the US dropped -13.5% yoy. Japanese exporters are now grappling with a 25% tariff on autos and auto parts, plus a 10% baseline levy on all other goods. Steel and aluminum products have also been hit with a 50% tariff in early June.

On a seasonally adjusted basis, exports edged up just 0.1% mom, while imports declined -0.3% mom, leaving a narrower but still negative trade balance of JPY -305B.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3364; (P) 1.3480; (R1) 1.3545; More...

GBP/USD's steep decline confirms short term topping at 1.3631, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for correction to 55 D EMA (now at 1.3328). Strong support could be seen there to bring rebound. Brea of 1.3631 will resume the rally from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. However, sustained break of 55 D EMA will indicate that deeper correction is underway.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.

UK CPI slows to 3.3% in May, but goods prices surges to highest since late 2023

UK headline CPI eased from 3.5% yoy to yoy in May, slightly above expectations of 3.3% yoy. Core CPI (excluding energy, food, alcohol and tobacco) also slowed from 3.8% to 3.5%, in line with forecasts.

While the overall trend points to gradual disinflation, markets might pay more attention to the reacceleration in goods prices, which rose to 2.0% yoy, the highest rate since November 2023.

Services inflation, however, showed a more meaningful decline, falling from 5.4% yoy to 4.7% yoy, suggesting underlying pressures are softening.

On a monthly basis, CPI rose by 0.2% mom, matching expectations.

US FOMC Meeting Takes the Evening Spotlight

In focus today

The main event will be in the US with the FOMC meeting this evening. We expect no changes to the policy rate in line with consensus and market pricing. FOMC participants will likely adjust their 2025 GDP forecasts lower due to the trade war, while other forecasts will see more modest adjustments. We expect the Fed to resume rate cuts from September and cut twice in 2025 followed by three more cuts in 2026 - slightly faster than what the March 'dots' implied. Read more from our Fed preview: Still on the sidelines, 13 June.

Fears of a wider conflict are growing in Middle East as it is starting to look increasingly likely that the US will get involved in the ongoing fighting between Israel in Iran. Apparently, Trump's inner circle, similarly as the Republican Party, is divided by the issue of whether to intervene or not. The US Director of National Intelligence, Tulsi Gabbard, who is known for his interventionist policy approach has said Iran was not close to having a nuclear weapon, but Trump has openly challenged her.

In the euro area, the final HICP data for May is released, which is expected to confirm the flash release. As services inflation drove the decline in May it will be interesting to see the measures of underlying inflation like 'LIMI' and 'super core' since the Lagarde has put more emphasis on these still elevated measures at the June meeting amid headline inflation undershooting the 2% target and staff projecting 1.6% inflation next year.

The Riksbank's rate decision is also due this morning at 09:30 CET. While consensus expectation is on a 25bp cut to 2.00%, we maintain our call for an unchanged policy rate and instead expect a cut later this summer in August. Historically the guidance from the Riksbank has been clearer ahead of policy rate cuts, although overall a cut in June or August makes little difference to the overall economy.

Economic and market news

What happened overnight

In Japan, May exports came in at -1.7% y/y (cons: -3.8% y/y). The print was stronger than expected, although the details also revealed that Japanese automakers were shouldering the bulk of tariff costs. Total exports to the US fell 11.1%, the value of automobile exports to the US were down 24.7%, while automobile volume to the US declined only 3.9%. Japan has yet to reach a trade deal with the US as tariffs continue to weigh on big automakers.

What happened yesterday

In the Middle East conflict, US Vice-President JD Vance said that US President Donald Trump may decide to take further action to end Iranian uranium enrichment. Trump also seemed somewhat unwilling to enter negotiations, adding that Iran giving up entirely would be a satisfactory outcome. At the same time G7 countries, including the US called for a de-escalation of the conflict and so a possible Trump involvement remains an open question.

In the US, retail sales were slightly weaker than expected on the headline, but actually a bit stronger than expected when looking at the 'control group' sales (the 'core' measure of retail sales). Overall, there were no big surprises in either direction though. The details were a bit to the soft side. Spending on discretionary categories, such as restaurants & bars and electronics & appliances declined, which could be a sign of consumers turning a bit more cautious with their spending behavior.

In Germany, the ZEW index rose more than expected in June in a positive print for the German economy. The expectations component rose to 47.5 (cons: 35.0) from 25.2 while the assessment of the current economic situation rose to -72.0 (cons: -75.0) from -82.0. The expectations component has now almost fully recovered from the 'Liberation Day' decline in April. The current situation remains very low in a historical perspective, but on a positive note, the small upward trend is continuing, leaving the index at the highest level in a year. We expect the German economy to stagnate in both Q2 and Q3 after a strong increase in the first quarter of the year, partly boosted by front-loading of exports to the US. We forecast 2025 GDP growth at 0.3% y/y.

In Sweden, the official labour market data (LFS) for May revealed a weaker-than-expected labour market. Employment declined to 5.231M from 5.261M in April, the unemployment rate SA climbed to 9.0% from 8.5% in April (cons: 8.6%). Employment is better than the Riksbank's forecast from March and one possible reason for the higher unemployment figure is likely an increase in the labour force, which makes the data slightly less soft than the headline numbers would otherwise suggest.

FI and FX: Rising tensions in the Iran-Israel conflict and weak US retail sales led to another day of negative risk sentiment yesterday. Equity indices fell by 0.5-1.0% across Western markets, and most of Asia is also showing blinking red this morning. US Treasury yields ended lower across the curve despite a significant increase in oil prices throughout the day. The Brent price closed up by USD4 at USD76.5/bbl., the highest level since February. The rise in oil price pushed EUR/USD below 1.15, while EUR/NOK continued its downward trend, closing at 11.41. USD/JPY remained relatively steady following the largely uneventful BoJ meeting. EUR/GBP moved higher ahead of today's CPI figures.