Sample Category Title

Trump’s Import Tariff Raise on Steel and Aluminum Kicks in Today

Markets

Strong JOLTS data kicked of the US economic calendar yesterday. Job openings in April unexpectedly rose from an upwardly revised 7.2 mln to just shy of 7.4 mln. The broader trend – fluctuating between 7-8 mln and near the pre-pandemic high – is indicative of ongoing labour market resilience and strengthens ongoing Fed talk of “wait and see”. US yields turned a small intraday 2-3 bps decline into 1-2 bps rise. European yield changes were negligible on a net daily basis. Below-consensus European inflation numbers barely changed money market rate cut bets. Tomorrow’s 25 bps reduction is fully priced in with at least another such move discounted for later this year. Gilts outperformed both Bunds and Treasuries with the long end of the curve showing declines of up to 4.3 bps. We suspect it is related to Bank of England Mann’s speech that opened the debate for a slower QT pace. The US dollar advanced against all of its most important peers in a technically insignificant move that was drawn out across the session. The trade-weighted index rose from 98.6 to 99.24, EUR/USD ventured from 1.144 to 1.137. Sterling withstood the relative interest rate support loss well. EUR/GBP slid from 0.844+ to 0.841.

Trump’s import tariff raise on steel and aluminum to 50% from 25% kicks in from today. It sets a challenging stage for the freshly elected South Korean president Lee Jae-myung. SK is a key steel exporter to the US and additionally faces an across-the-board Liberation Day 25% levy if trade talks with the US fail. Lee during his campaign over the last couple of weeks promised a $25bn stimulus package (>1% of GDP) to revive the economy and created a sense of a generally looser fiscal policy than under his predecessor. Lee’s victory is sending reflationary vibes through SK markets. Stocks outperform (2.5%), the SK currency leads the Asian scoreboard and government bond yields rise up to 14 bps at the long end. Moves in core bond and FX markets are muted ahead of another batch of US eco data. The ADP job report (+114k expected) serves as a prelude to the official payrolls report this Friday. The May services ISM (seen at 52.0 from 51.6) is of bigger importance to markets. A stagflation narrative similar to Monday’s manufacturing ISM could again weigh both the dollar and US Treasuries. EUR/USD 1.1473 is intermediate resistance ahead of the April 1.1573 high. The Fed’s Beige Book release marks the start of the June policy meeting cycle.

News & Views

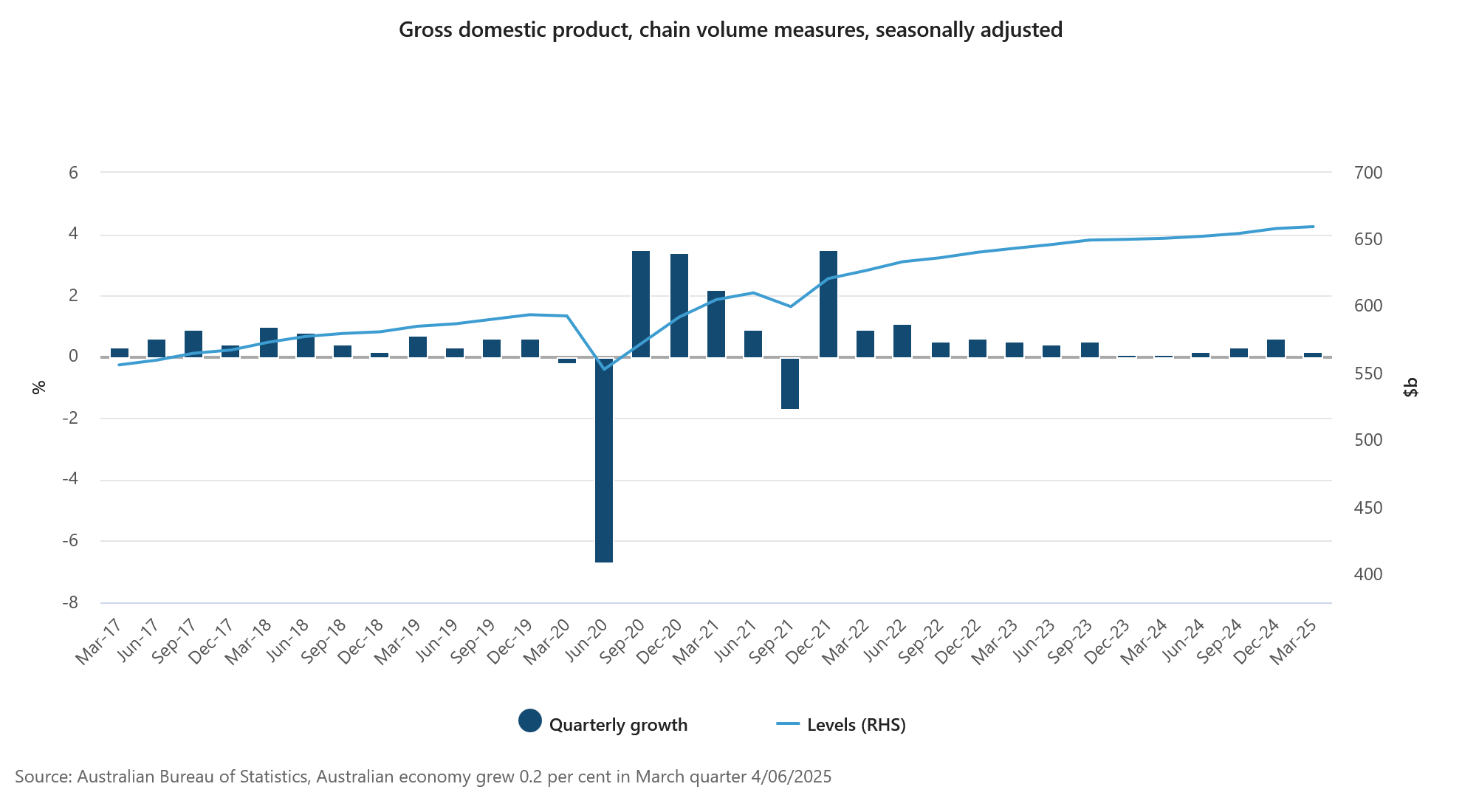

Australian GDP growth slowed down more than expected in Q1 2025: from 0.6% Q/Q in Q4 2024 to 0.2% Q/Q (+1.3% Y/Y). The Bureau of Statistics indicated that public spending recorded the largest detraction from growth since the Q3 2017. Government spending remained flat while investments declined by 2% on the quarter. Extreme weather events reduced domestic final demand and exports. Weather impacts were particularly evident in mining, tourism and shipping. Household spending slowed from 0.7% Q/Q to 0.4% with spending on essentials continuing to be amongst the highest contributors. Households also spent more on energy because of warmer than average weather and a decline in electricity rebates. The household saving ratio rose from 3.9% to 5.2% with gross disposable income up 2.4%. Net trade detracted 0.1 ppt from growth especially as coal and LNG exports were impacted by weather disruptions to production and shipping. Private investments rose by 0.7% Q/Q, led by housing. The weather-influenced GDP data don’t rule anything in or out for the Reserve Bank of Australia. They cut the policy rate twice now (February & May), with money markets convinced that the central bank has room to accelerate with first back-to-back action in July. AUD/USD sticks within the extremely tight 0.6350-0.6550 range in place since mid-April.

German Finance minister Klingbeil will today present corporate tax incentives at a cabinet meeting which could cost around €46bn in total by 2029 according to government estimates seen by the Financial Times. The tax breaks come on top of the >€1tn debt-funded public spending plans. According to the FT, companies would be able to deduct 30% of the cost of new machinery and other equipment from their tax bill annually between 2025 and 2027 (starting July 1st). From 2028, the federal corporate tax rate of 15% would then decrease by one point each year to 10%. Companies will also be allowed to depreciate 75% of the purchase price of new electric vehicles on year one, and thus reduce their taxable income. The government also intends to introduce more advantageous tax incentives for R&D spending.

Equities Up Regardless of Trade Worries, Mixed Data

Market performance was surprisingly strong yesterday, especially considering the day began in the US with a sharp downgrade in global growth projections from the OECD. The organization cited ‘substantial increases in trade barriers, tighter financial conditions, and weakened business and consumer confidence’ as key concerns. That neatly sums up why many expect a global economic slowdown this year—led by the US.

As such, the OECD expects the US to be the hardest hit among major economies. Japan is also seen feeling the pinch of trade tensions, while projections for Europe remain relatively steady. The euro area is expected to continue growing slowly, and the gap between US and European growth should narrow as the US economy decelerates. That’s also what the euro’s appreciation against the dollar has been signaling since the start of the year.

The EURUSD pair struggles to break through the 1.15 psychological level, with strong offers above 1.1450. But if US trade disruptions persist, those offers could give way, sending the pair into the 1.15–1.20 range by summer. Judging by the latest developments, that scenario looks increasingly plausible—if undesirable. As of today, Trump’s new tariffs on steel and aluminium—doubling the rate from 25% to 50%—take effect.

So why are US stocks still being bought? There are several explanations: FOMO: Fear of missing out on the rally, TACO: Trump Always Chickens Out, or economic data/Federal Reserve (Fed) hopes?

But trade headlines were negative yesterday while the economic data was mixed and the Federal Reserve (Fed) is reluctant to move due to rising inflation expectations. So it’s probably FOMO—and it feels fragile.

Today, investors will watch the ADP employment report and ISM non-manufacturing data for fresh insights into US economic strength. Strong numbers may support further gains while soft figures Maybe could trigger a pullback. Or maybe not. Markets seem to have their own agenda, and the fear of missing a potential rally appears enough to fuel optimism—no matter how weak the forecasts, or the data.

And the economic data is more concerning than encouraging: following a surprise contraction in Chinese manufacturing PMI earlier this week, Australia reported softer-than-expected Q1 growth this morning. The Bank of Canada (BoC) also meets today, with some expecting a 25bp rate cut. Since surveys are split, the move isn’t fully priced in. A cut could lift the loonie by fueling growth optimism, while a hold could prompt a bit of re-positioning. But with the US dollar under pressure, the USDCAD looks ready for further declines. In June 2021—four years ago—the pair traded near the 1.20 level. It now sits at a critical juncture. A break below 1.37—the 38.2% Fibonacci retracement of the four-year rise - would put the pair into a long-term bearish consolidation phase, possibly driving it toward the 1.30–1.33 range. That would fit the broader narrative of expected US dollar weakness.

In equities, US stocks remain in demand, with tech leading the charge. The Nasdaq is inching toward its February all-time high, driven by Nvidia’s rally past $140. Nvidia has now overtaken Microsoft to become the world’s most valuable company, with a market cap around $3.45 trillion. Its P/E ratio sits near 45—not extreme for a speculative tech name with real earnings behind the story. For AI investors, Nvidia remains a strong conviction play. In Europe, luxury goods are losing ground to defense names. Germany’s Rheinmetall has joined the Euro Stoxx 50, while Kering has dropped out. Weak demand from Chinese consumers and higher US import taxes are weighing on the luxury sector. Meanwhile, rising geopolitical risks and European pledges to boost defense spending are attracting flows into defense stocks. Beyond that, softer inflation and looming European Central Bank (ECB) rate cuts continue to support Stoxx 600 valuations, though the upside in most of these names can’t match the momentum of US tech leaders, and there are concerns that the European defense spending plans may have already been mostly priced in.

EA Inflation Declined, and US JOLTS Surprised to the Topside

In focus today

In the US, the ADP private sector employment report will provide markets with the first sense of what to expect from Friday's upcoming May Jobs Report. The ISM services index for May will also be released, the flash PMI pointed towards a small uptick. Atlanta Fed's Bostic is scheduled to give remarks at a local Fed Listens event.

In the euro area, we receive the final services and composite PMI data for May. The final manufacturing PMI on Monday showed the same reading as the preliminary release, namely 49.4, so we also expect the composite PMI to be close to the preliminary data.

In Canada, the Bank of Canada will publish its interest rate decision. Analysts are split on an unchanged decision and a 25bp cut. We lean towards the former but highlight that it is a low-conviction call amid continued trade uncertainty.

In China, PMI service from Caixin will be released overnight.

In Denmark, we will receive the unemployment indicator for May from the Danish Agency for Labour Market, our first status on the Danish labour market in May.

In Sweden, we will receive services PMI for May at 8.30 CET. The manufacturing sector saw a slight decline (staying nearly unchanged on Monday), maintaining a solid figure of 53.6. The service sector has been weaker compared to manufacturing, staying below 50 for two consecutive months. Employment has risen in manufacturing but has been weak in the service sector.

The Danske Morning Mail will not be released tomorrow, 5 June, due to Constitution Day, but we are back with an update on Friday. Tomorrow, we will look out for the ECB monetary policy meeting, where we anticipate a 25bp cut in the leading policy rate to 2.0%. Also, in the US, the May Challenger report for layoff announcements as well as the weekly jobless claims will provide further sense of the status of labour markets.

Economic and market news

What happened overnight

At Danske Bank, we published our new macro forecasts for the Nordic countries and the major economies. Read more in Nordic Outlook - Normalisation with tariff risks, 4 June.

What happened yesterday

In the euro area, inflation declined to 1.9% y/y in May, in line with most recent forecasts following country data but below the initial consensus forecast of 2.0% y/y. Core inflation declines to 2.3% y/y from 2.7% y/y, below expectations of a decline to 2.4%. The decline in both headline and core inflation was mainly due to services inflation, that fell from 4.0% y/y to 3.2% y/y. Euro area unemployment in April remained unchanged at 6.2%, in line with expectations.

In the US, JOLTS job openings surprised to the topside, coming in at 7.391M in April (prior: 7.2M., cons.: 7.1M). Hiring also ticked a bit higher against expectations after 'Liberation Day'. That said, involuntary layoffs edged modestly higher as well (1.79M, from 1.59M).

In Switzerland, inflation decreased in line with expectations, reaching deflationary territory for the first time since 2021. Headline inflation came in at -0.1% y/y (cons: -0.1%, prior: 0.0%) and core inflation at 0.5% y/y (prior: 0.6% y/y). With this print, inflation has come in lower than SNB projections yet again and we expect a 25bp cut at the next meeting on 19 June, bringing the policy rate to 0%.

The OECD has lowered its global growth forecast to 2.9% for 2025-2026, citing the impact of Trump's trade policies. US growth is expected to slow to 1.6% this year due to tariff-related uncertainties. China's growth is partly offset by subsidies and welfare spending, while the euro area's outlook remains stable. Increased protectionism could further weaken growth and heighten inflation pressures.

In the Netherlands, the Dutch government collapsed after Geert Wilders' PVV party left the coalition, likely leading to new elections in October or November. Wilders accused coalition partners of not supporting his strict immigration policies. Prime Minister Dick Schoof resigned, leaving a caretaker administration that may delay NATO-related defence spending decisions. The political landscape remains divided, with immigration a longstanding contentious issue in Dutch politics.

Equities: Equities were higher, and cyclicals made a comeback on Tuesday. S&P 500 added 0.6% (Russell 2000 1.6%) while Europe lagged with Stoxx 600 0.1%. This was the first time in a week that cyclicals did better than defensives on a global scale. It has been three weeks since cyclicals beat defensives numerous sessions in a row. Similarly, investors looked for beta in small caps for the first time in a long time yesterday, with small caps outperforming cyclicals by the double. Although headline indices have carried on, the de-risking taking place in sectors and styles has brought technicals to more sustainable levels. Just take the Fear and Greed index which has returned to almost neutral levels. Asian markets are in risk-on this morning (Taiwan and Kospi up 2-3%) as investors are cheering the election outcome, as it is likely to entail more fiscal stimulus. US futures are a notch lower this morning, while European futures indicate some catch-up.

FI and FX: Stronger domestic data, with hirings advancing to the highest level in almost a year, prompted a turnaround in the greenback yesterday. EUR/USD fell back below 1.14 again and USD/JPY breached 144 anew. 30Y US treasuries are once again testing the 5%-level, which we expect to be breached as investors require a higher premium for buying US treasuries currently. EUR/CHF rose on the back of deflationary Swiss inflation data, opening the door for a potential 50bp cut at the SNB meeting later this month. The SEK underperformed G10 peers with selling persisting through the session, making NOK/SEK briefly trading above 0.9500 before falling back slightly. We have updated our Riksbank call and now expect the rate to be cut by 25bp, to 2%, in August. As for NBP, we expect them to leave the key rate unchanged at 5.25% at today's monetary policy meeting. This morning, we have released updated macro forecasts, to be found in Nordic Outlook - June 2025.

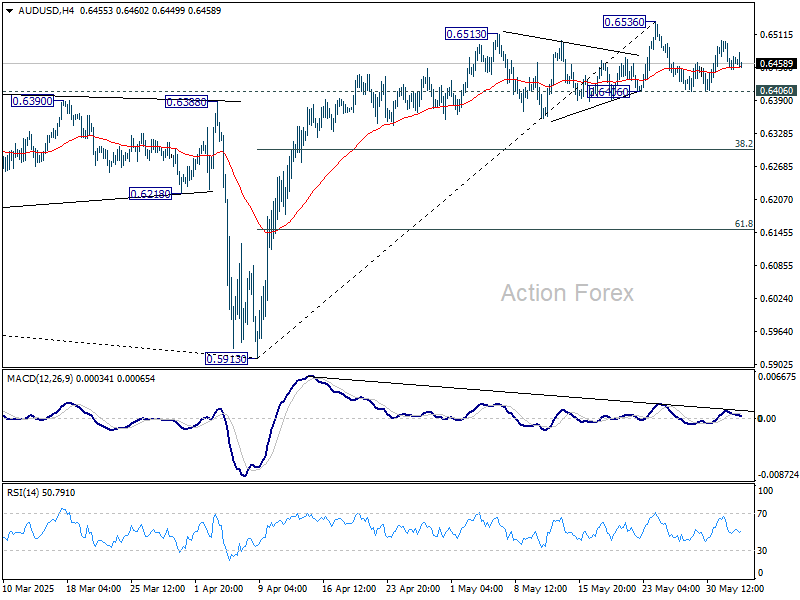

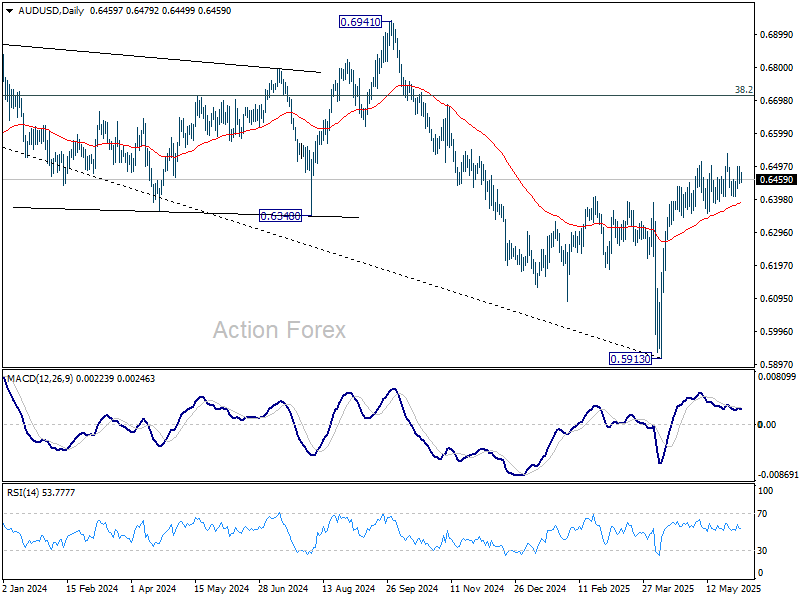

AUD/USD Daily Report

Daily Pivots: (S1) 0.6439; (P) 0.6470; (R1) 0.6492; More...

Intraday bias sin AUD/USD remains neutral for the moment. With 0.6406 support intact, further rally is expected. ON the upside, firm break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, decisive break of 0.6406 will confirm short term topping, and turn bias back to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6441) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fail through 0.5913 at a later stage.

Subdued Markets Drift as Tariff Tensions Resurface and BoC Decision Looms

Global markets remain subdued as investors struggle to find a firm direction. US stocks closed higher overnight, with NASDAQ extending to fresh multi-week highs, suggesting some resilience in tech-led risk appetite. Asian equities followed suit to some extent, but the overall momentum has been tepid.

In the currency markets, Dollar is attempting to recover from recent losses, though the rebound so far lacks strong conviction. Loonie and Kiwi are mildly firmer. However, Aussie and Yen are both underperforming, sitting at the bottom of the performance table and highlighting the absence of a coherent risk-on or risk-off narrative. European majors are positioned in the middle of the pack, with Swiss Franc slightly outperforming.

The trade backdrop remains tense. US President Donald Trump’s decision to double tariffs on most imported steel and aluminum to 50% took effect on today, marking a new escalation in the global trade conflict. According to economic adviser Kevin Hassett, the initial 25% steel tariffs delivered partial support, but "more help is needed," hence the decision to double the rates. The move came just as the White House also demanded "best offers" from trade partners ahead of a self-imposed early July deadline. Attention now turns to the European Union, with markets awaiting any formal response or retaliatory measures.

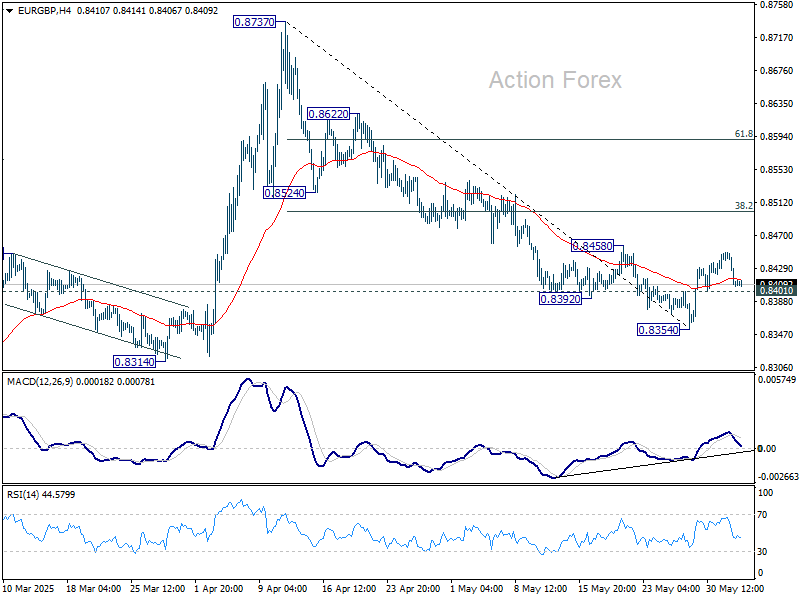

Technically, EUR/GBP's recovery has stalled ahead of 0.8458 resistance and retreated notably. Focus is back on 0.8401 support. Firm break there will argue that fall from 0.8737 might be ready to resume through 0.8354. That, if happens, might be accompanied by extended pullback in EUR/USD or upside break out in GBP/USD, or both.

In Asia, at the time of writing, Nikkei is up 0.92%. Hong Kong HSI is up 0.47%. China Shanghai SSE is up 0.36%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.014 at 1.495. Overnight, DOW rose 0.51%. S&P 500 rose 0.58%. NASDAQ rose 0.81%. 10-year yield fell -0.002 to 4.460.

Looking ahead, final PMI Services data from both the Eurozone and the UK will be released in European session. In the US, markets will closely watch the ADP employment report and ISM services index for clues on labor market momentum and service sector resilience. Still, the day’s main event is BoC policy decision, where the central bank is widely expected to hold, but guidance could lean dovish as trade risks intensify.

BoC to hold rates at 2.75%, maintain dovish bias

BoC is widely expected to leave interest rate unchanged at 2.75% for the second consecutive meeting today.

While Q1 GDP surprised to the upside at 2.2% annualized, the growth was heavily front-loaded by export activity as US buyers rushed to stockpile Canadian goods ahead of impending tariffs. That one-off boost is unlikely to alter the central bank’s cautious stance in light of growing global and domestic uncertainties. Meanwhile, core inflation rose back to near the top of BoC’s 1-3% target range, offering a reasonable basis for a continued pause.

Overall, expectations are firmly anchored toward further easing later this year. A Reuters poll found that 75% (17 of 23) of economists anticipate at least two more cuts in 2025, with two of them forecasting as many as four.

Given the high degree of trade uncertainty, particularly around tariffs, BoC is likely to keep a flexible tone in its communication. While the rate is on hold today, policymakers are expected to leave the door open for adjustments ahead, depending on how the trade situation evolves.

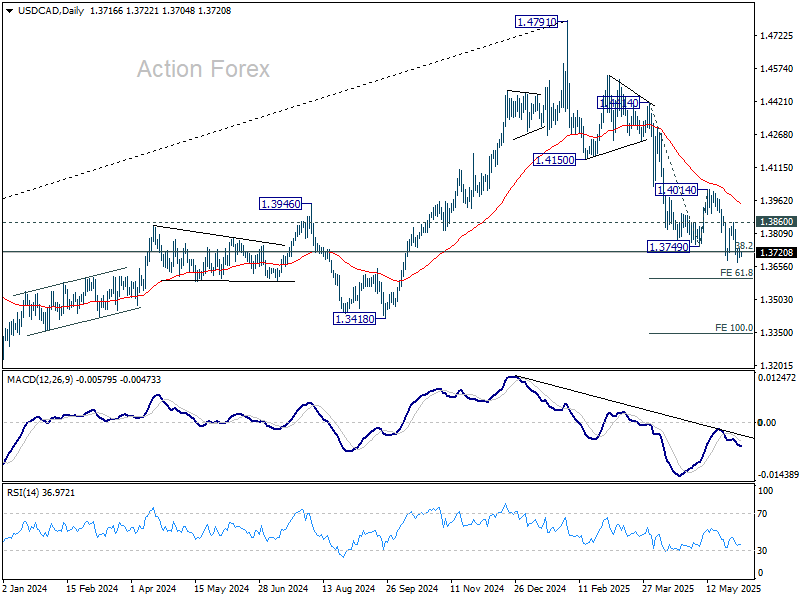

In the currently markets, today's BoC decision may not be the key driver for USD/CAD. Instead, market direction is still largely dictated by sentiment around US trade policy.

Technically, further decline is expected as long as 1.3860 resistance holds, to 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603. There might be some support from 1.3603 to contain downside and bring a rebound, as a correction to the five wave decline from 1.4791 high. However, decisive break there could prompt downside acceleration to 100% projection at 1.3349 rather quickly.

Australia’s GDP grows only 0.2% qoq in Q1, as weather and public investment drag

Australia’s GDP expanded just 0.2% qoq in Q1, falling short of expectations for 0.4% qoq growth. On an annual basis, GDP rose 1.3% yoy. However, GDP per capita declined by -0.2% qoq, marking a renewed contraction in individual economic output.

The ABS noted that severe weather disrupted key sectors including mining, tourism, and shipping, while also impacting domestic demand and exports.

The most notable drag came from public investment, which fell -2.0%, contributing to the largest negative impact from public spending since Q3 2017. Net exports also weighed slightly, subtracting -0.1 percentage points from quarterly growth.

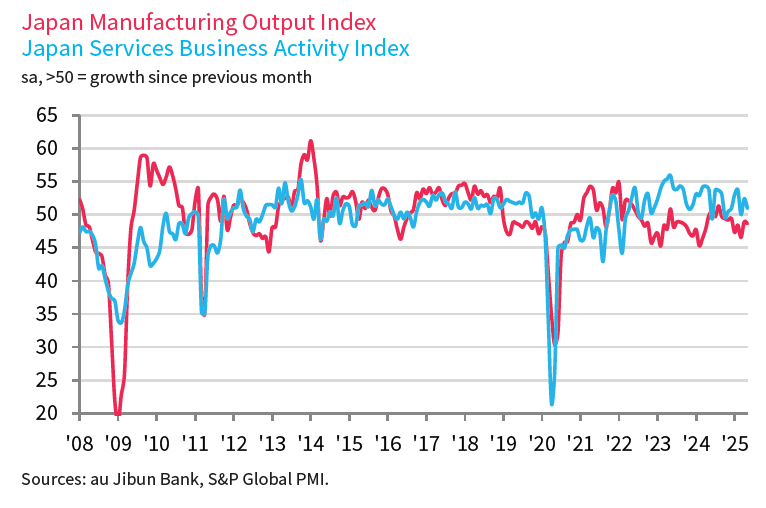

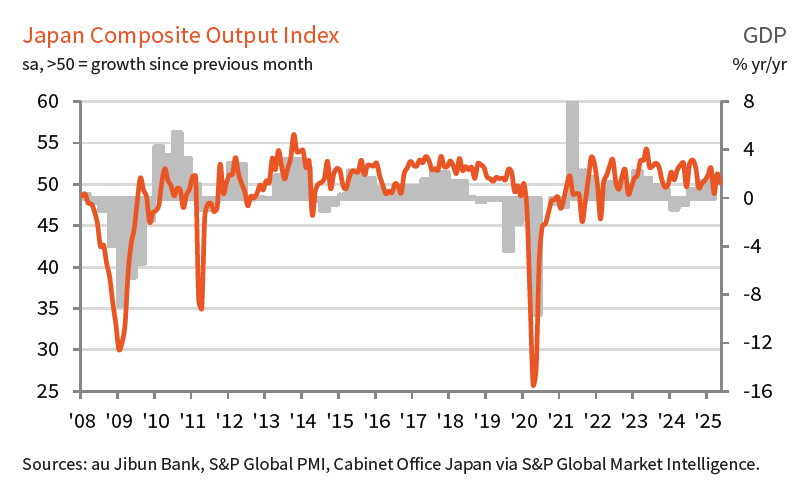

Japan’s PMI composite finalized at 50.2, growth momentum falters

Japan’s private sector lost steam in May as final PMI Services reading slipped to 51.0 from April’s 52.4, while Composite PMI declined to 50.2 from 51.2. The data point to only marginal growth in overall activity, with a slowdown in services combining with a mild deterioration in manufacturing output.

S&P Global’s Annabel Fiddes noted that the rise in total new orders "moved closer to stagnation, as service sector sales grew at their slowest pace in six months and factory demand continued to decline. This moderation suggests that Japan’s private sector "may struggle to bounce back in the near-term".

Underlying concerns were linked to external and structural factors, including an uncertain global demand outlook, persistent labor shortages, and mounting cost pressures.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6439; (P) 0.6470; (R1) 0.6492; More...

Intraday bias sin AUD/USD remains neutral for the moment. With 0.6406 support intact, further rally is expected. ON the upside, firm break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, decisive break of 0.6406 will confirm short term topping, and turn bias back to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6441) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fail through 0.5913 at a later stage.

BoC to hold rates at 2.75%, maintain dovish bias

BoC is widely expected to leave interest rate unchanged at 2.75% for the second consecutive meeting today.

While Q1 GDP surprised to the upside at 2.2% annualized, the growth was heavily front-loaded by export activity as US buyers rushed to stockpile Canadian goods ahead of impending tariffs. That one-off boost is unlikely to alter the central bank’s cautious stance in light of growing global and domestic uncertainties. Meanwhile, core inflation rose back to near the top of BoC’s 1-3% target range, offering a reasonable basis for a continued pause.

Overall, expectations are firmly anchored toward further easing later this year. A Reuters poll found that 75% (17 of 23) of economists anticipate at least two more cuts in 2025, with two of them forecasting as many as four.

Given the high degree of trade uncertainty, particularly around tariffs, BoC is likely to keep a flexible tone in its communication. While the rate is on hold today, policymakers are expected to leave the door open for adjustments ahead, depending on how the trade situation evolves.

In the currently markets, today's BoC decision may not be the key driver for USD/CAD. Instead, market direction is still largely dictated by sentiment around US trade policy.

Technically, further decline is expected as long as 1.3860 resistance holds, to 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603. There might be some support from 1.3603 to contain downside and bring a rebound, as a correction to the five wave decline from 1.4791 high. However, decisive break there could prompt downside acceleration to 100% projection at 1.3349 rather quickly.

Japan’s PMI composite finalized at 50.2, growth momentum falters

Japan’s private sector lost steam in May as final PMI Services reading slipped to 51.0 from April’s 52.4, while Composite PMI declined to 50.2 from 51.2. The data point to only marginal growth in overall activity, with a slowdown in services combining with a mild deterioration in manufacturing output.

S&P Global’s Annabel Fiddes noted that the rise in total new orders "moved closer to stagnation, as service sector sales grew at their slowest pace in six months and factory demand continued to decline. This moderation suggests that Japan’s private sector "may struggle to bounce back in the near-term".

Underlying concerns were linked to external and structural factors, including an uncertain global demand outlook, persistent labor shortages, and mounting cost pressures.

Australia’s GDP grows only 0.2% qoq in Q1, as weather and public investment drag

Australia’s GDP expanded just 0.2% qoq in Q1, falling short of expectations for 0.4% qoq growth. On an annual basis, GDP rose 1.3% yoy. However, GDP per capita declined by -0.2% qoq, marking a renewed contraction in individual economic output.

The ABS noted that severe weather disrupted key sectors including mining, tourism, and shipping, while also impacting domestic demand and exports.

The most notable drag came from public investment, which fell -2.0%, contributing to the largest negative impact from public spending since Q3 2017. Net exports also weighed slightly, subtracting -0.1 percentage points from quarterly growth.

Ethereum Poised To Surge — Key Resistance In Sight

Key Highlights

- Ethereum started a fresh increase above the $2,500 resistance.

- ETH is following a short-term contracting triangle forming with resistance at $2,800 on the daily chart.

- Bitcoin price is facing hurdles near the $107,000 resistance.

- XRP is showing positive signs and might soon aim for a move above $2.35.

Ethereum Technical Analysis

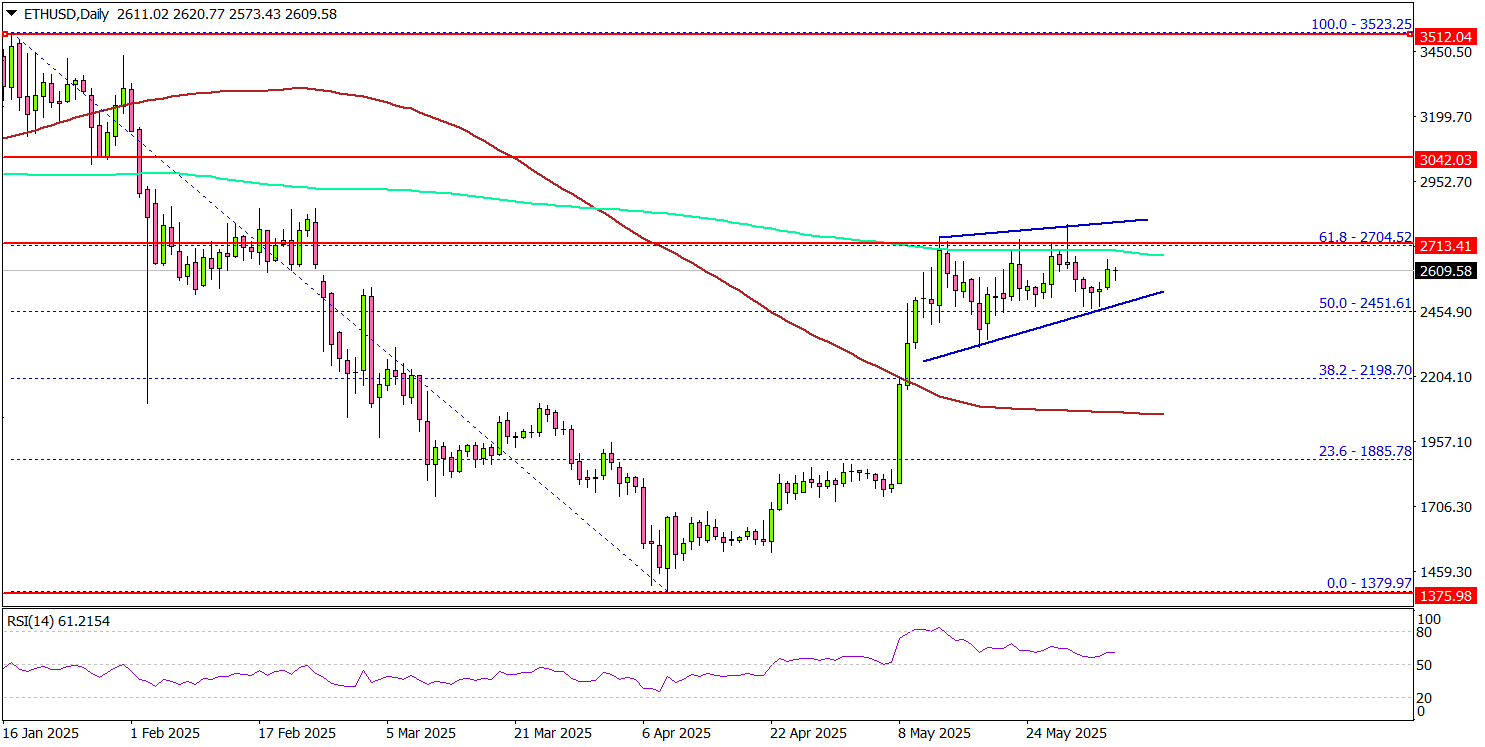

Ethereum remained stable above $1,800 and started a fresh increase. ETH cleared a few key hurdles near $2,200 to start a fresh surge.

Looking at the daily chart, the price surpassed the 50% Fib retracement level of the downward wave from the $3,740 swing high to the $1,379 low. ETH settled above the 100-day simple moving average (red) and now approaches the 200-day simple moving average (green).

It is now facing resistance near the $2,700 zone and the 61.8% Fib retracement level of the downward wave from the $3,740 swing high to the $1,379 low.

The next major resistance is near the $2,800 level. There is also a short-term contracting triangle forming with resistance at $2,800 on the daily chart. A daily close above the $2,800 resistance zone could start another steady increase.

In the stated case, the price may perhaps rise toward the $3,000 level. The next stop for the bulls may perhaps be $3,120. On the downside, Ethereum might find support near the $2,450 level.

The next major support is $2,320, below which the price could slide toward $2,120. Any more losses might call for a move toward the $2,000 level.

Looking at Bitcoin, there was a steady increase above the $103,200 level, and the price is now facing hurdles near the $107,000 level.

Economic Releases

- Fed's Bostic speech.

- Fed's Cook speech.

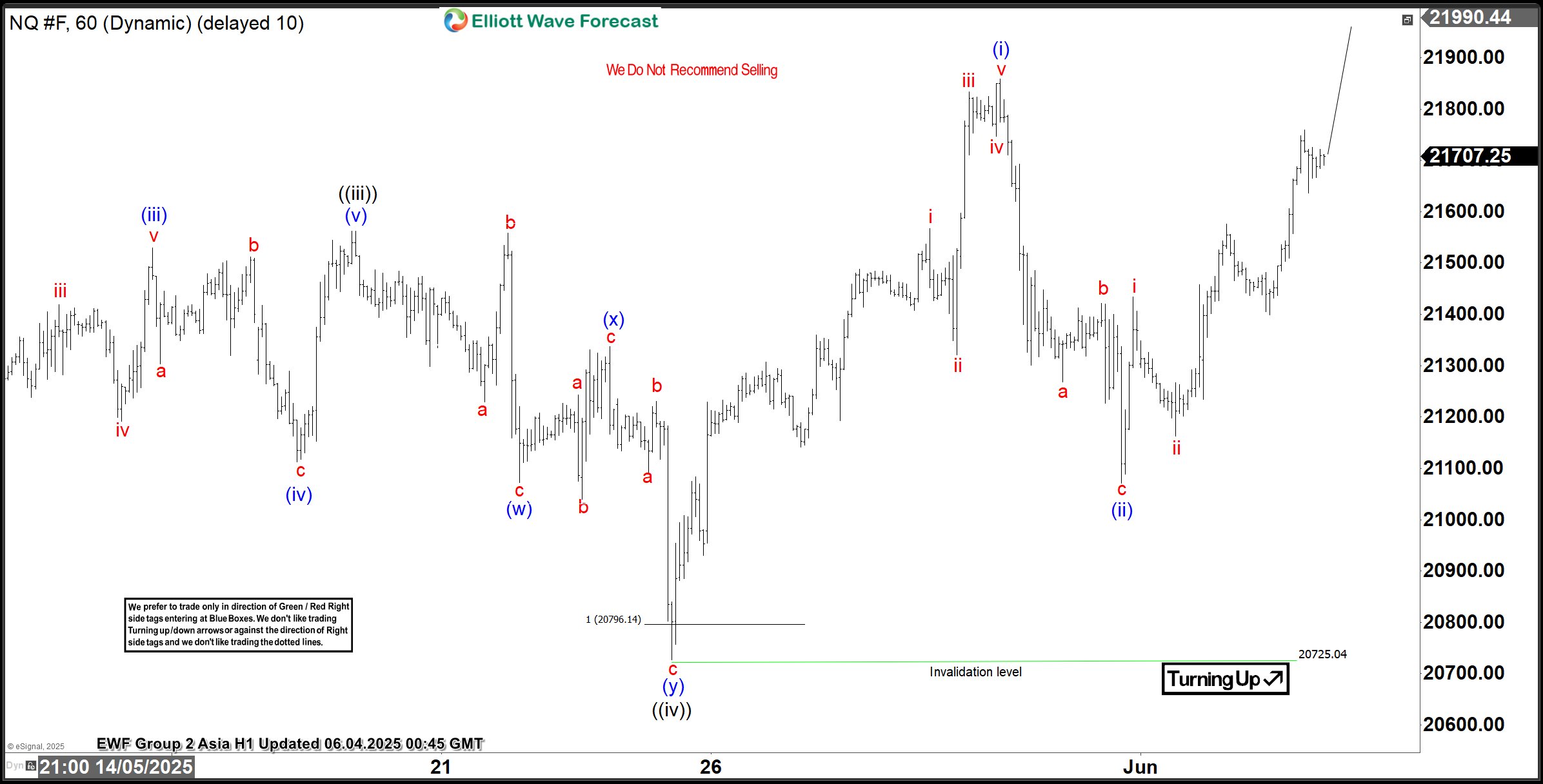

Elliott Wave Analysis: Nasdaq (NQ) Set to Complete 5 Waves Impulse, Defining Bullish Trend

On April 7, 2025, the Nasdaq (NQ), like other major global indices, marked a significant low, setting the stage for a potential bullish trend. From this low, the index has embarked on a five-wave impulsive rally. This a hallmark of bullish momentum in Elliott Wave theory. The initial advance, wave 1, peaked at 18,361.5. It was then followed by a corrective pullback in wave 2, which found support at 16,735. From there, the index resumed its upward trajectory in wave 3. The move up in wave 3 has an internal five-wave structure, signaling strong bullish momentum.

Within wave 3, the first sub-wave, ((i)), concluded at 19,386.75. Subsequent pullback in wave ((ii)) found support at 17,700. The index then surged higher in wave ((iii)), reaching 21,562. Afterwards, a corrective dip in wave ((iv)) ended at 20,725.04, as illustrated on the one-hour chart. This wave ((iv)) correction unfolded as a double-three Elliott Wave pattern. Wave (w) bottomed at 21,072.75 and wave (x) peaked at 21,337.5. The final leg, wave (y), concluded at 20,725.04, completing the correction.

The Nasdaq has since turned higher in wave ((v)). From the wave ((iv)) low, wave (i) advanced to 21,858.75, followed by a pullback in wave (ii) to 21,071.5. The index is now poised to extend higher in wave (iii) of ((v)), continuing the impulsive rally from the April 7 low. In the near term, as long as the pivotal low at 20,725.04 holds, any pullbacks are expected to find support in a 3, 7, or 11-swing pattern, paving the way for further upside. This technical setup suggests the Nasdaq is well-positioned to sustain its bullish momentum in the coming sessions, provided key support levels remain intact.

Nasdaq 60-Minute Elliott Wave Technical Chart

Nasdaq (NQ) Elliott Wave Technical Video

https://www.youtube.com/watch?v=afkDPGxtLkI