Sample Category Title

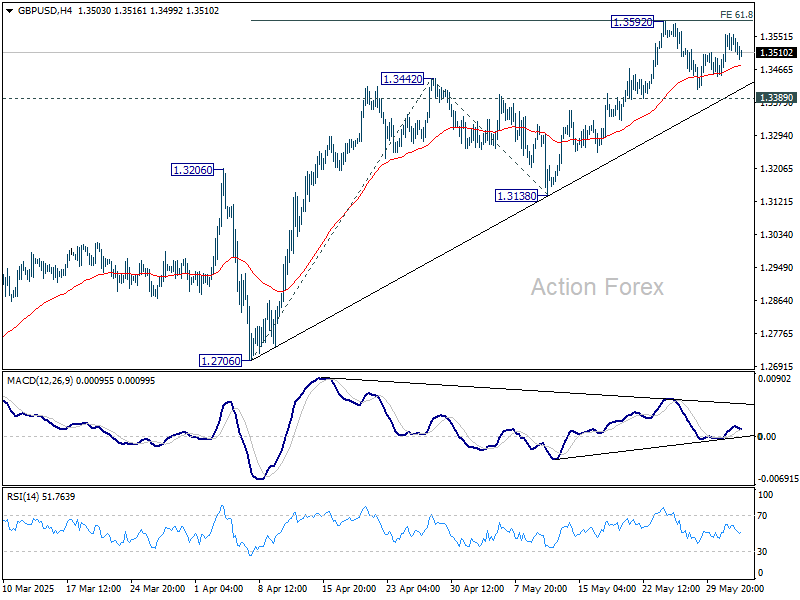

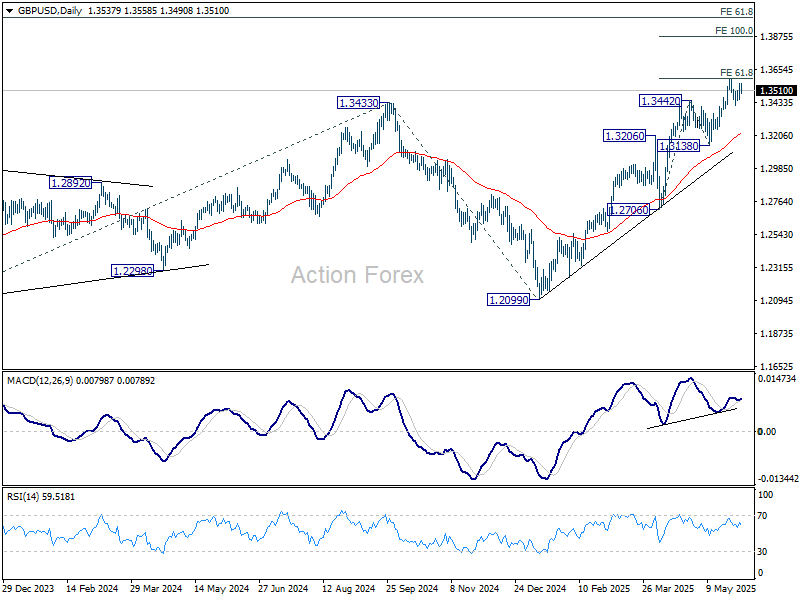

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3478; (P) 1.3519; (R1) 1.3585; More...

Intraday bias in GBP/USD remains neutral for the moment. With 1.3389 support intact, further rise is expected. On the upside, firm break of 1.3592 will resume larger up trend to 100% projection of 1.2706 to 1.3442 from 1.3138 at 1.3874. However, decisive break of 1.3389 will confirm short term topping, and turn bias back to the downside for 1.3138 support instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2866) holds, even in case of deep pullback.

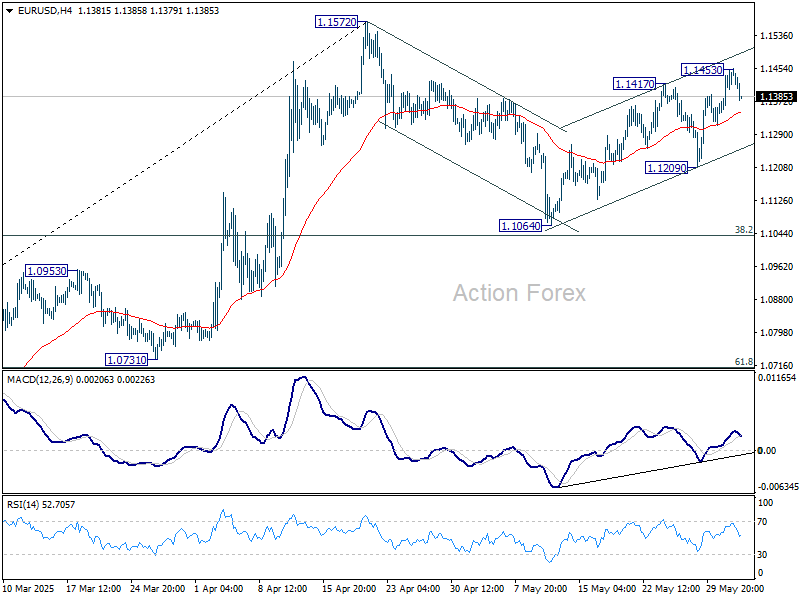

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1377; (P) 1.1413; (R1) 1.1480; More...

Intraday bias in EUR/USD is turned neutral with current retreat. Rebound from 1.1064 could extend higher, but strong resistance should be seen from 1.1572 to limit upside, at least on first attempt. On the downside, break of 1.1209 support will indicate that the corrective pattern from 1.1572 has started the third leg, and target 1.1064 support.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

Euro Slips on Softer CPI, But Trading Largely Listless

The currency markets remain largely listless today, with all major pairs and crosses still trapped within last week's ranges. Euro edged slightly lower following the release of Eurozone CPI data, which showed inflation falling below the ECB’s 2% target for the first time since September last year. The core measure also softened notably, reinforcing the view that disinflationary pressures—particularly within services—are well entrenched. With inflation now comfortably back within target, markets have little doubt that ECB will proceed with a 25bps rate cut this Thursday.

Uncertainty over tariffs continues to hover as a key wildcard. With little clarity on whether the US will escalate its trade actions further, markets are reluctant to commit. A July pause from ECB remains the base case, but further action could hinge on whether tariffs ultimately push inflation up through cost channels—or suppress demand and contribute to disinflation. This dilemma is front and center as policymakers navigate crosscurrents in growth and prices.

Adding to the cautious mood, the OECD revised its global growth forecasts downward. It now sees world GDP expanding just 2.9% in both 2025 and 2026, citing increased trade barriers and lingering policy uncertainty as key drags. OECD Secretary General Mathias Cormann warned that a further 10 percentage point hike in US bilateral tariffs could shave 0.3% off global output over two years, while likely adding to inflation in affected countries.

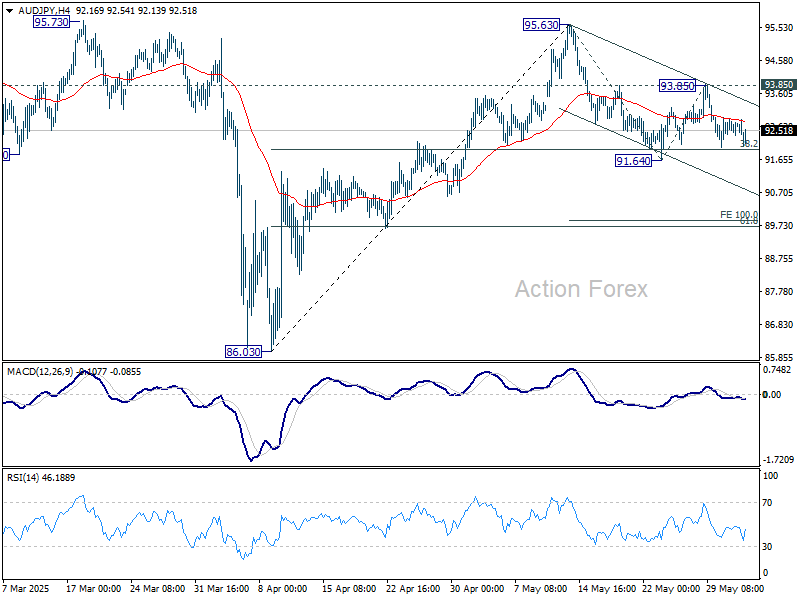

Technically, AUD/JPY continues to press 38.2% retracement of 86.03 to 95.63 at 91.96. Firm break of this fibonacci level will extend the correction from 95.63 to 100% projection of 95.63 to 91.64 from 93.85 at 89.86. Nevertheless, strong bounce from current level, followed by break of 93.85 resistance, will argue that rise from 86.03 is ready to resume through 95.63.

In Europe, at the time of writing, FTSE is up 0.17%. DAX is up 0.16%. CAC is down -0.15%. UK 10-year yield is down -0.038 at 4.632. Germany 10-year yield is down -0.019 at 2.51. Earlier in Asia, Nikkei fell -0.06%. Hong Kong HSI rose 1.53%. China Shanghai SSE rose 0.43%. Singapore Strait times rose 0.10%. Japan 10-year JGB yield fell -0.27 to 1.482.

BoE's Bailey: Rate path still downward, but clouded by unpredictability

BoE Governor Andrew Bailey told the Treasury Committee today that while the direction for interest rates remains downward, the outlook has become increasingly uncertain.

Declining to pre-commit to a vote at the upcoming June meeting, Bailey said, “the path remains downwards, but how far and how quickly is now shrouded in a lot more uncertainty.”

He emphasized the role of external forces, noting that the Bank has revised its language to reflect the “unpredictable” nature of the current global environment.

His comments were echoed by fellow policymakers Catherine Mann and Sarah Breeden, who both acknowledged that rates are likely headed lower but stressed the difficulty in forecasting the exact pace or scale of future cuts.

Mann warned against assuming a fixed glide path, while Breeden said “there is uncertainty about how far, how fast.”

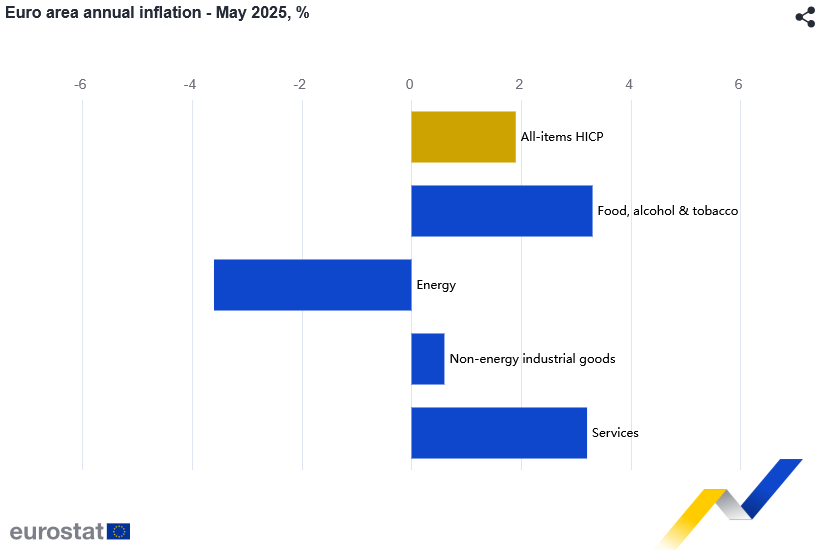

Eurozone CPI falls to 1.9%, below ECB target for first time since Sep 2024

Eurozone inflation dipped back below the ECB’s 2% target for the first time since September 2024. Headline CPI fell from 2.2% yoy to 1.9% yoy in May, undershooting expectations of 2.0%. Core CPI (ex-energy, food, alcohol & tobacco) also eased more than forecast to 2.3% from 2.7%.

The disinflation was led by a sharp slowdown in services inflation, which dropped from 4.0% yoy to 3.2% yoy. Non-energy industrial goods remained unchanged at 0.6% yoy. Energy prices continued to contract at -3.6% yoy, reinforcing the broader downward pressure. Despite a slight uptick in food and alcohol inflation to 3.3% yoy, the overall picture confirms easing price momentum across key sectors.

Swiss CPI falls to -0.1% yoy, first negative since 2021

Swiss consumer inflation turned negative in May for the first time since March 2021, with headline CPI falling -0.1% yoy, down from 0.0% in April yoy. Core inflation, which strips out volatile components such as fresh food and energy, slipped to 0.5% yoy from 0.6% yoy previously.

On a monthly basis, both headline and core CPI rose 0.1%, in line with expectations.

The breakdown reveals that domestic product prices grew just 0.2% mom and decelerated to from 0.8% yoy to 0.6% yoy. Imported goods prices were flat on the month and fell -2.4% yoy, ticked up from -2.5% yoy.

BoJ's Ueda: Ready to hike if wage growth recovers from tariff drag

BoJ Governor Kazuo Ueda told parliament today that recently imposed U.S. tariffs could weigh on Japanese corporate sentiment, potentially impacting winter bonus payments and next year’s wage negotiations.

He acknowledged that wage growth may "slow somewhat" in the near term due to these external pressures. However, Ueda expressed confidence that wage momentum would eventually "re-accelerate", helping to sustain a moderate growth in household consumption.

Looking ahead, Ueda reiterated the BoJ’s readiness to adjust its ultra-loose policy if the economy evolves in line with its projections. “If we're convinced our forecast will materialize, we will adjust the degree of monetary support by raising interest rates,” he said.

However, he cautioned that uncertainty surrounding the economic outlook remains “extremely high.”

RBA's Hunter: AUD’s recent resilience linked to global shift away from USD exposure

RBA Chief Economist Sarah Hunter addressed the unusual behavior of the Australian Dollar in recent months in a speech today. She highlighted that while initial moves were consistent with past risk-off episodes, the currency’s subsequent rebound against the US Dollar stood out as "more unusual".

On a "trade-weighted" basis, AUD has remained broadly stable, even though it has appreciated against the greenback and the Chinese renminbi, while weakening against most other major currencies.

This divergence, Hunter explained, stems from "offsetting factors". Global growth concerns have pressured the AUD against safe-haven and cyclical peers, while simultaneous outflows from US assets have weakened the US Dollar.

Hunter cautioned that it's too soon to tell whether this trend will persist, but acknowledged that recent market behavior reflects shifting investor sentiment, particularly toward capital reallocation away from US assets. As a result, Australian Dollar’s relative resilience against USD may be underpinned by portfolio rebalancing and perceived relative economic stability.

Hunter noted that the trade-weighted index has reverted to "pre-shock values", suggesting minimal net change in the foreign-currency value of Australian exports. However, the "relative move of capital" into Australia, at a time when the US is facing policy and tariff-related volatility, could offer some support to "domestic investment activity", providing a cushion to the broader economy amid global uncertainties.

RBA Minutes: 25bps cut chosen for caution and predictability after debating hold and 50bps options

RBA’s May 20 meeting minutes revealed that policymakers weighed three policy options—holding rates, a 25bps cut, or a larger 50bps reduction—before ultimately opting for a modest 25bps cut to 3.85%.

The case for easing hinged on three key factors: sustained progress in bringing inflation back toward target without upside surprises, weakening global conditions and household consumption, and the view that a cut would be the “path of least regret” given the risk distribution.

While members discussed a 50bps reduction after deciding to ease, they found the case for a larger move unconvincing. Australian data at the time showed little evidence that trade-related global uncertainty was materially harming domestic activity. Furthermore, some scenarios might even result in upward pressure on inflation, prompting caution. The Board also assessed that it was "not yet time to move monetary policy to an expansionary stance".

Ultimately, the Board judged that to move "cautiously and predictably" was more appropriate.

Caixin PMI manufacturing drops to 48.3, as China faces marked weakening at start of Q2

China's manufacturing sector unexpectedly shrank in May, with Caixin PMI falling to 48.3 from 50.4, well below market expectations of 50.6. This marked the first contraction in eight months and the lowest reading since September 2022.

According to Caixin Insight’s Wang Zhe, both supply and demand weakened, with a particularly notable drag from overseas demand. Employment continued to contract, pricing pressures remained subdued, and logistics saw moderate delays. Although business optimism saw a marginal recovery, the broader picture points to intensifying headwinds.

The report highlights the fragile start to Q2, with Wang pointing to a "marked weakening" in key economic indicators and a "significantly intensified" level of downward pressure.

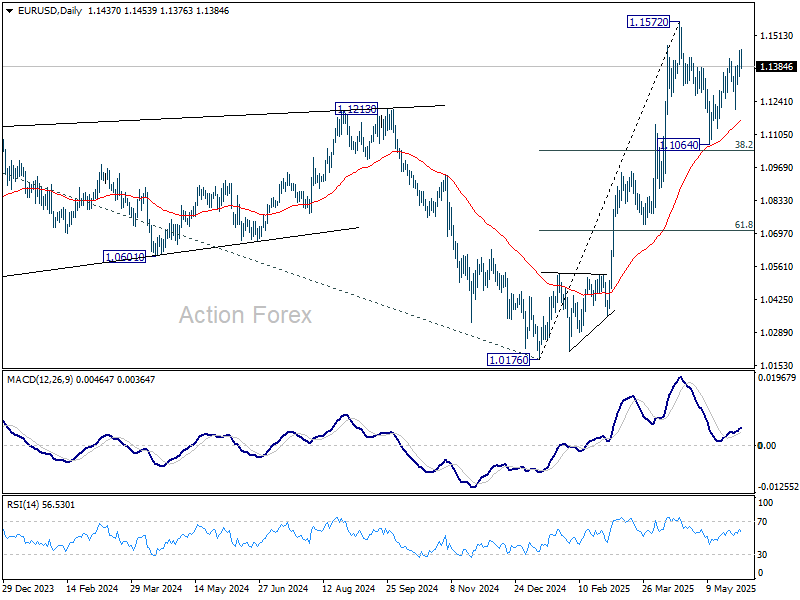

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1377; (P) 1.1413; (R1) 1.1480; More...

Intraday bias in EUR/USD is turned neutral with current retreat. Rebound from 1.1064 could extend higher, but strong resistance should be seen from 1.1572 to limit upside, at least on first attempt. On the downside, break of 1.1209 support will indicate that the corrective pattern from 1.1572 has started the third leg, and target 1.1064 support.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

BoE’s Bailey: Rate path still downward, but clouded by unpredictability

BoE Governor Andrew Bailey told the Treasury Committee today that while the direction for interest rates remains downward, the outlook has become increasingly uncertain.

Declining to pre-commit to a vote at the upcoming June meeting, Bailey said, “the path remains downwards, but how far and how quickly is now shrouded in a lot more uncertainty.”

He emphasized the role of external forces, noting that the Bank has revised its language to reflect the “unpredictable” nature of the current global environment.

His comments were echoed by fellow policymakers Catherine Mann and Sarah Breeden, who both acknowledged that rates are likely headed lower but stressed the difficulty in forecasting the exact pace or scale of future cuts.

Mann warned against assuming a fixed glide path, while Breeden said “there is uncertainty about how far, how fast.”

Markets Today: Euro Area Inflation Drops, OECD Downgrades Growth and Trump-Xi Meeting

Asian Session Market Wrap

Markets failed to hold onto late US session gains as markets were hoping for positive news regarding a potential Trump-Xi meeting.

US Equity Futures are down in the Asian session with the S&P 500 down around approximately 0.6%. In Asia, a key measure of regional stocks went up by 0.1%, breaking a three-day losing streak. Chinese stocks in Hong Kong rose as investors hoped for more government support after factory activity unexpectedly dropped in May.

The US Dollar is on the up this morning, with the greenback gaining against the majority of its G10 counterparts.

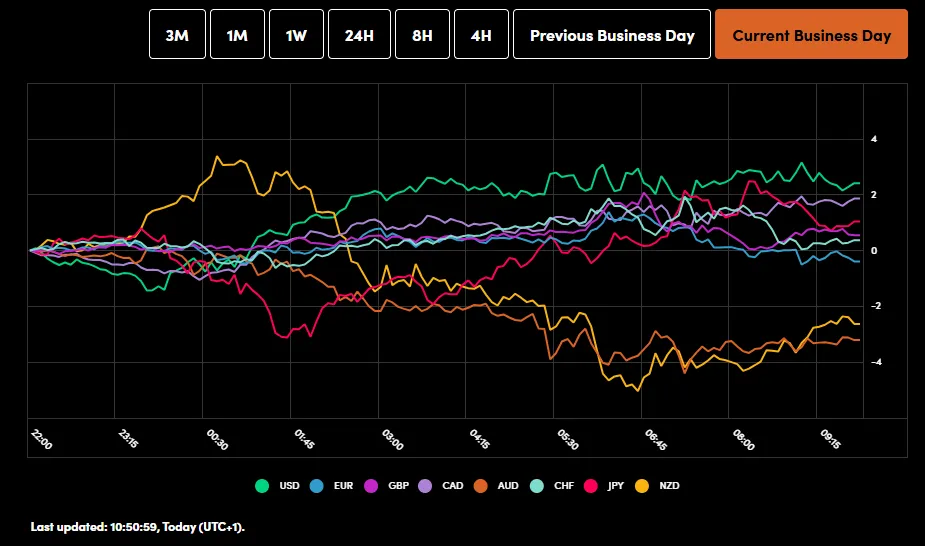

Power Currency Balance

Source: OANDA Labs

The European Open

It has been a busy start to the European Session this morning.

European shares fell on Tuesday, dragged down by banks and mining companies, which are sensitive to economic changes, as investors waited for news on the trade war affecting global growth. The pan-European STOXX 600 index lost 0.5% after an earlier rise, adding to Monday's losses. Banks dropped 1.4%, and mining stocks fell 2.3%.

OECD Downgrades Global Growth Forecast

According to the Organisation for Economic Cooperation and Development (OECD) the global economy is expected to grow more slowly this year, with growth predicted to be 2.9% in both 2025 and 2026, compared to 3.3% last year.

The OECD cited growing uncertainty on the back of US trade policies under the Trump administration as a major cause. If there is one thing that has always been clear, it is that market participants hate uncertainty.

The report warns that more trade barriers could hurt growth, lower incomes, and slow job creation. The U.S. economy is expected to grow only 1.6% this year, down from 3.3% in 2024, due to tariffs, less immigration, and government job cuts.

The OECD noted that higher trade costs, especially in countries raising tariffs, will increase inflation, though weaker commodity prices will help offset this. While inflation is slowing in many areas, service prices remain high, and rising government spending, especially on defense, needs careful management.

These developments will only serve to reinforce the belief that a global slowdown may be on the way and could weigh further on the already fragile market sentiment we have seen at the start of the week.

Potential trade deal announcements are sorely needed to allay the fears of market participants as anticipation and anxiety continue to build.

Euro Area Inflation Drops Below ECB Target, ECB Rate Meeting Next

Inflation in the euro zone dropped below the European Central Bank's target last month, according to data on Tuesday. This supports expectations for another interest rate cut this week, even as global trade tensions create long-term price pressures.

Consumer inflation in the 20 euro-using countries fell to 1.9% in May, down from 2.2% in April, due to lower energy prices and a big drop in services inflation.

Core inflation, which excludes fuel and food prices, also slowed to 2.3% from 2.7%, mainly because services price growth dropped to 3.2% from 4.0%, according to Eurostat, the EU's statistics agency.

Markets were already expecting a rate cut from the ECB on Thursday. The question following today's inflation release is whether or not ECB President Lagarde will adopt a more dovish tone regarding the ECB outlook moving forward. Will market participants begin to price in more aggressive rate cuts from the ECB for the rest of 2025?

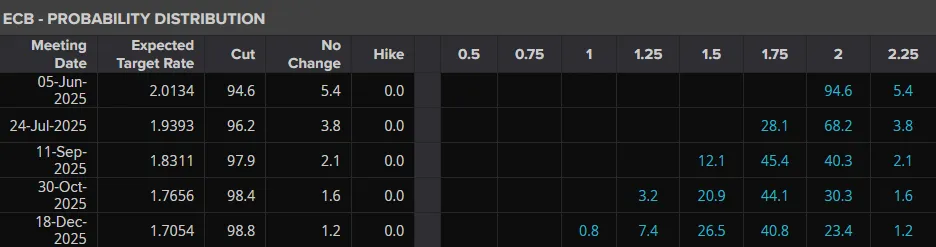

ECB Interest Rate Probabilities

Source: LSEG

Economic Data Releases and Final Thoughts

Looking at the economic calendar, the rest of the day sees focus shift to US data.

The US session will bring JOLTS job openings and US Factory Orders which will give more insight into the US economy from a demand perspective. The question will be whether these numbers may be skewed as consumers rush to purchase ahead of impending tariffs on imported goods and raw materials.

We will also hear comments from a host of Federal Reserve Policymakers and the Chair of the SEC who testifies today before the House Appropriations Committee today. His testimony is part of the House Appropriations Committee's oversight of the SEC and its budget.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - DAX Index

From a technical standpoint, the Dax had printed a fresh high last week around the 24387 but continues to struggle to hold convincingly above the 24000 handle.

The index is down around 0.4% at the time of writing with the 20-day MA currently providing support at the 23786 handle. This is similar to yesterday where the index bounced of the 20-day MA but failed to build on a daily candle close above the 24000 handle. Is today the day we get a sustainable move?

I would like to believe it is but given all the dynamics at play the move faces significant resistance.

Immediate support rests at 23830, 23500 and the 50 day MA around 22740.

A move beyond 24000 needs to break yesterdays highs at 24090 before a move beyond toward the 24300 and 24500 handles which could provide some resistance to bulls.

DAX Index Daily Chart, June 3, 2025

Source: TradingView.com (click to enlarge)

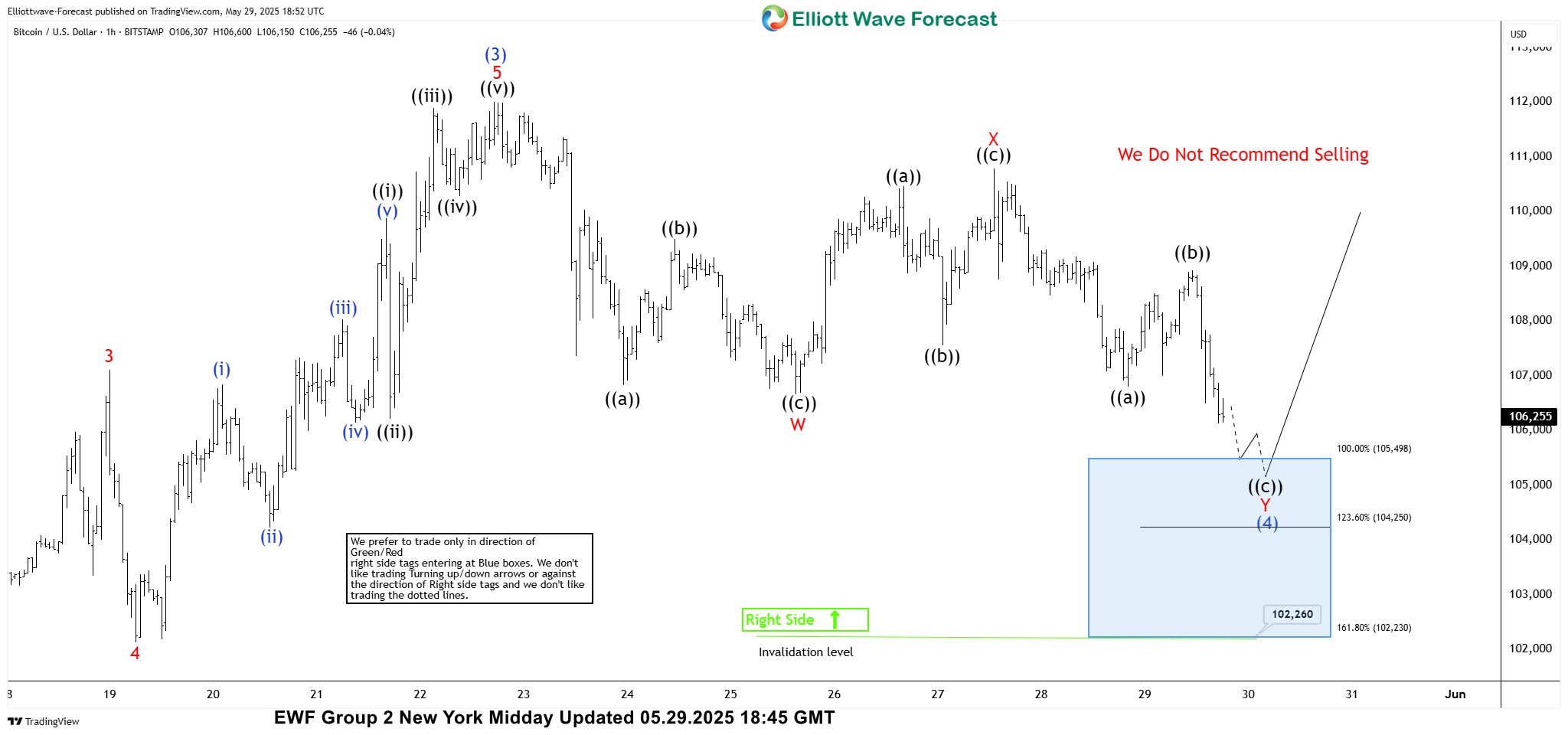

Bitcoin (BTCUSD) Elliott Wave : Buying the Dips at the Blue Box Zone

In this article we’re going to take a quick look at the Elliott Wave charts of Bitcoin BTCUSD published in members area of the website. BTCUSD is showing impulsive bullish sequences in the cycles from the 74,535 low, that are calling for a further strength. Recently we got a pull back that has reached the Blue Box zone,our buying area. In the following text, we will explain the Elliott Wave trading setup, including the target areas.

BTCUSD Elliott Wave 1 Hour Chart 05.29.2025

BTCUSD is showing an incomplete structure from the May 22nd high . The current Elliott Wave count suggests we should ideally see more downside in the short term, toward the 105,498-102,230 area -Blue Box (buying zone). As the main trend is bullish, we expect to see at least a 3 waves bounce from the buying zone. This setup could ideally lead to a rally toward new highs. We advise against selling and prefer the long side from the marked blue box (buying zone).

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

Trading Setup Reminder

Quick reminder on how to trade our charts :

- Red bearish stamp + blue box = Selling Setup

- Green bullish stamp + blue box = Buying Setup

- Charts with Black stamps are not tradable.

BTCUSD Elliott Wave 4 Hour Chart 06.03.2025

BTCUSD made an extension toward our buying zone: 105,498-102,230 . The crypto found buyers at the Blue Box as expected, and we got a good reaction from there. With the price holding above the 103,150 low, we expect further strength to follow. Next technical area to the upside comes at 114,085

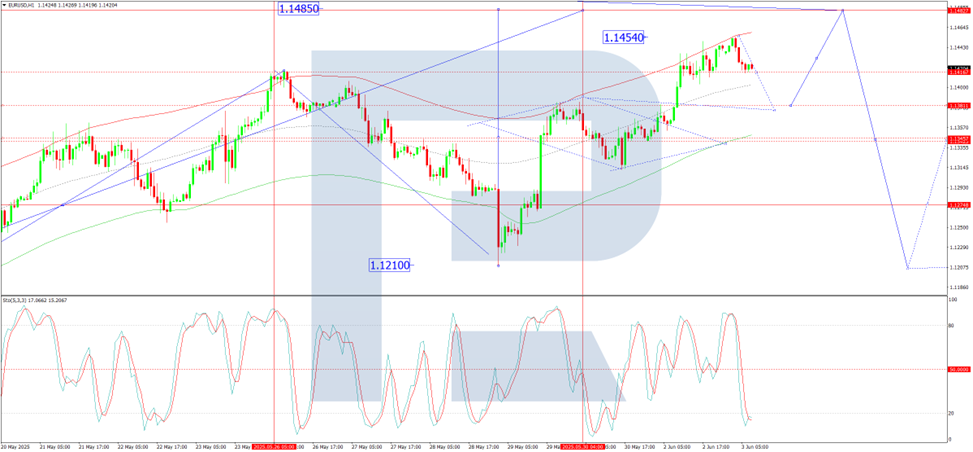

EUR/USD Set to Rise as Sentiment Turns Against the US Dollar

The EUR/USD pair rose to 1.1418 before pausing, as bearish sentiment towards the US dollar intensified following the release of disappointing US macroeconomic data and escalating trade tensions.

The dollar is under pressure from weak data and trade uncertainty

The dollar came under renewed pressure after the release of weaker-than-expected US manufacturing activity data for May, which pointed to a deeper-than-anticipated slowdown. These figures indicate that economic risks remain elevated, particularly amid continued trade policy uncertainty under President Donald Trump.

Trump’s recent decision to raise steel import tariffs to 50% sparked fresh concerns and drew sharp criticism from major trading partners, further heightening investor unease.

Tensions with China have also escalated, with Beijing rejecting Trump’s accusations of violating the interim trade deal and vowing retaliatory measures to defend its interests.

Looking ahead, markets will closely monitor a series of US macroeconomic releases due on Tuesday, including job openings, durable goods orders, and factory orders – all of which will help assess the health of the US economy.

The eurozone is also set to publish preliminary inflation data for May, which may influence euro sentiment. However, for now, investors remain optimistic about EUR/USD. Barring any surprises, the pair appears well-supported.

Technical analysis of EUR/USD

On the H4 chart, EUR/USD is extending the fifth wave of growth towards 1.1485. The market has already met the local target at 1.1450, and a short-term correction to 1.1380 is expected next. Once this pullback concludes, a final push towards 1.1485 is likely, marking the end of the current growth wave. From there, a new downward phase may begin, with a target at 1.1210. The MACD indicator supports this scenario, with its signal line above zero and pointing sharply upwards, indicating continued bullish momentum.

On the H1 chart, EUR/USD formed a consolidation range around 1.1350, broke to the upside, and completed the growth structure, reaching a local target of 1.1450 within the fifth wave. A correction to 1.1380 is anticipated, followed by another growth wave towards 1.1485. The Stochastic oscillator confirms this outlook, with its signal line below 20 and preparing to rise towards 80, signalling a potential bullish continuation after the correction.

Conclusion

EUR/USD remains well-positioned for further gains amid mounting US economic concerns and renewed trade tensions. The pair has short-term support at 1.1380 and faces resistance at 1.1485. A reversal could occur once the current growth wave is exhausted, with 1.1210 as a longer-term downside target. For now, technical indicators and market sentiment continue to point to further upside, particularly if upcoming US data confirms a weakening economic outlook.

Eurozone CPI falls to 1.9%, below ECB target for first time since Sep 2024

Eurozone inflation dipped back below the ECB’s 2% target for the first time since September 2024. Headline CPI fell from 2.2% yoy to 1.9% yoy in May, undershooting expectations of 2.0%. Core CPI (ex-energy, food, alcohol & tobacco) also eased more than forecast to 2.3% from 2.7%.

The disinflation was led by a sharp slowdown in services inflation, which dropped from 4.0% yoy to 3.2% yoy. Non-energy industrial goods remained unchanged at 0.6% yoy. Energy prices continued to contract at -3.6% yoy, reinforcing the broader downward pressure. Despite a slight uptick in food and alcohol inflation to 3.3% yoy, the overall picture confirms easing price momentum across key sectors.

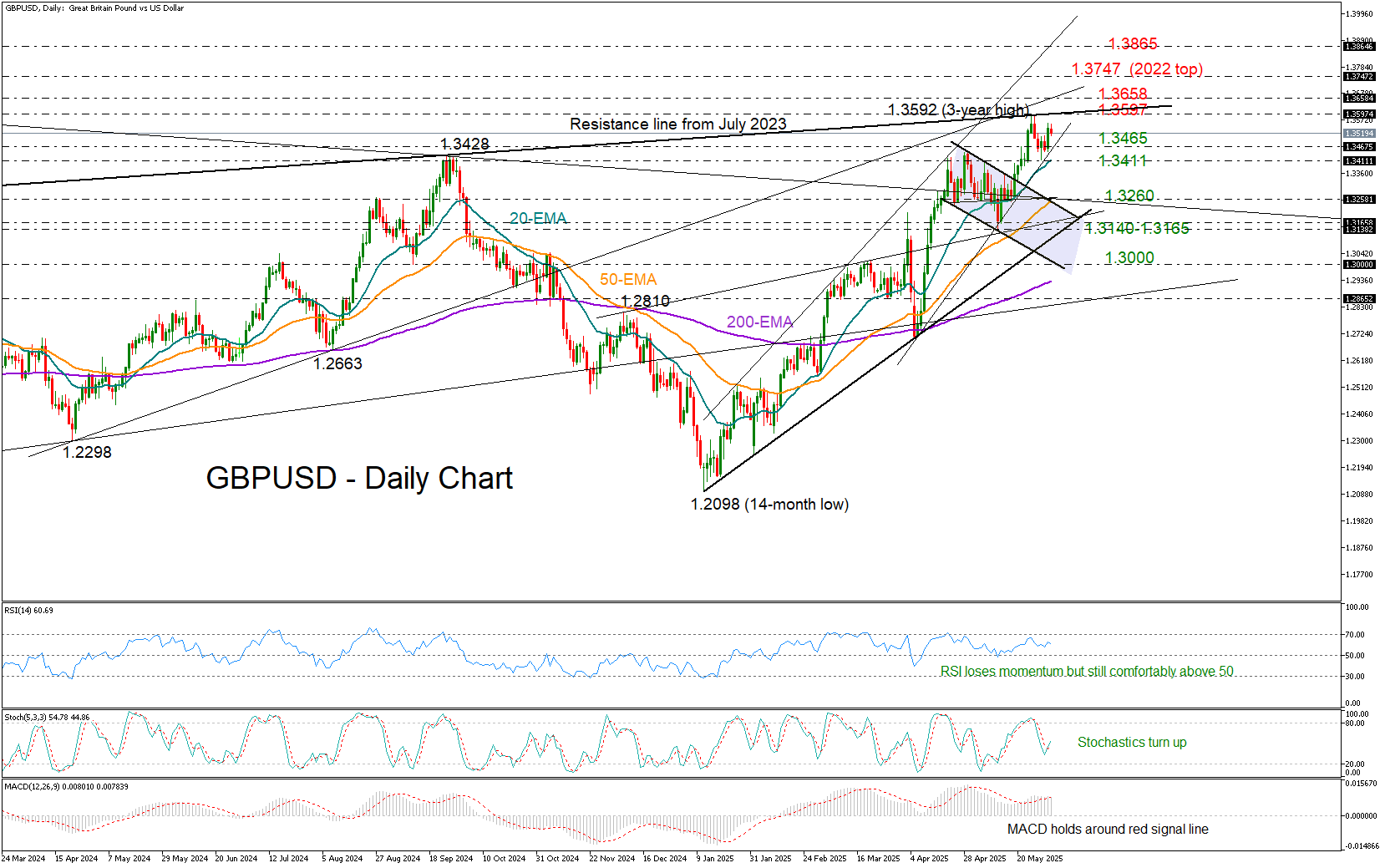

GBP/USD Takes a Breather Before Next Bullish Move

- GBP/USD consolidates gains near 3-year high.

- Short-term bias remains positive; focus on 1.3597 resistance.

GBPUSD has eased slightly below May’s three-year high of 1.3592, but Monday’s solid rebound has renewed optimism that the bulls are still in control.

For further upside momentum, the price needs a decisive close above the resistance line from July 2023 at 1.3597, which capped gains last week. A breakout above the key constraining zone of 1.3658 could trigger a more exciting rally toward the 2022 peak at 1.3747. Beyond that, attention could shift to the ascending trendline around 1.3865.

From a technical perspective, the short-term risk remains skewed to the upside, supported by the upturn in the stochastic oscillator and the fact that the RSI continues to hover comfortably above its neutral 50 level, despite showing signs of fatigue.

Should the support trendline near 1.3465 or the 20-day exponential moving average (EMA) provide a solid base—much like in mid-May—the bulls may regain control. Otherwise, increased selling pressure could push the pair down to the 1.3260 area, where the 50-day EMA currently lies. The 1.3240–1.3165 trendline zone may serve as the last line of defense before the broader uptrend entirely loses its shine.

In summary, GBP/USD remains in a consolidation phase, with the potential for fresh highs if the 1.3597 resistance is convincingly broken.

Silver Price Hits Year-to-Date High

As shown on the XAG/USD chart, silver prices rose on Monday, surpassing the previous high of the year, which was set on 28th March at around $33.50 per ounce.

Why Is Silver Rising?

A bullish driver came from statements made by the White House. According to media reports:

→ US President Donald Trump announced on Friday evening plans to double tariffs on steel and aluminium imports to 50%, starting 4th June. This intervention in the global metals market may have also impacted silver prices, given silver’s significant industrial value.

→ Trump's claims that China violated the trade agreement reached in Geneva last month further cast doubt on the prospects of a phone call between Trump and Chinese President Xi Jinping.

Technical Analysis of the XAG/USD Chart

Today’s bearish candlestick (marked with a red arrow) indicates that sellers are becoming active, willing to open short positions near the 2025 high. From a technical analysis perspective, there are signs of:

→ a bearish engulfing candlestick pattern forming;

→ a false breakout above the March high (trapping bullish traders).

However, the bulls may attempt to keep the price in the upper half of the emerging ascending channel (shown in blue), relying on support from the former resistance level at $33.67.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.