Sample Category Title

Cautiously and Predictably, RBA Minutes Confirm a Moderate Path

The minutes for the May 2025 RBA Monetary Policy Board meeting and speech by Assistant Governor Hunter reveal that the RBA is not panicking about the world and recognises the domestic case for policy normalisation, not expansion.

The policy and market volatility since the 2 April ‘Liberation Day’ tariff announcements has all happened since the April RBA meeting. Accordingly, the section of the minutes on financial conditions indicates that the Board received an extensive briefing on these developments. The initial sell-offs and deteriorations in liquidity, both globally and in Australia, had mostly retraced by the time of the May meeting. However, the Board expressed some scepticism about the extent of the rebound, particularly insofar as it relied on stimulatory fiscal or monetary policy globally or deregulation in the US. It sounded a note of scepticism about the US more broadly, highlighting that the US’s poor fiscal position might be contributing to higher term premia. It also noted that reallocation of global investors’ previously overweight US exposures might be weighing on the US dollar. The minutes highlighted that the US dollar depreciation runs against the expected pattern where lower imports induce an appreciation of a tariffing country’s exchange rate.

The Minutes also noted that market pricing on policy rates had initially reacted more sharply to tariff news in Australia than in some peer economies. While some of this might have been a separate reaction to domestic data, some market participants may have viewed Australia as being particularly vulnerable, because of our close economic linkages with China. By contrast, the Board views China as being well placed to withstand the tariff turmoil and maintain growth. The minutes noted that the Chinese authorities ‘authorities there appeared to be both committed to their growth target of around 5 per cent and able to provide more stimulus to the economy if required.’

Turning to the domestic economy, the Minutes highlighted that growth, inflation and the labour market were all evolving broadly as expected. They also noted that the Board ‘welcomed’ the broad-based easing in underlying inflation. These outcomes provided ‘welcome confirmation’ that upside inflationary risks had not crystallised. Contrary to the Governor’s comments in the media conference downplaying the use of shorter-run calculations, the minutes highlighted that on a six-month-annualised basis, trimmed mean inflation was in the middle of the RBA’s 2–3% target range.

The domestic growth outlook was scaled back a little, both because of weaker global demand for Australian exports and some possible uncertainty effects weighing on domestic investment; today’s speech by RBA Assistant Governor Sarah Hunter also touched on these potential uncertainty effects. A lower cash rate assumption offset these external effects to some extent.

Given these developments, the staff forecasts were characterised similarly to the post-meeting communication, with underlying inflation now expected to be around the midpoint of the target range. For a 0.1ppt revision to the forecast relative to the February round, this is a significant change in language. The determination to get exactly to 2.5% declared in the wake of the February meeting, to maximise the chance of being in the target range, was nowhere to be seen in any of the communication after the May meeting.

The minutes also noted comments that wages growth might ‘slow more noticeably than currently forecast’. Although the staff assessment remains that the labour market is tighter than full employment, the minutes again suggested not all Board members were convinced. Members noted signs of easing pressure, such as a greater focus on job security in bargaining agreements. Subsequent to the RBA meeting, the Fair Work Commission (FWC)

handed down its 2025 National Wage Case decision. As Westpac Senior Economist Justin Smirk notes in his commentary on the decision, the 3.5% increase to minimum and award wages is consistent with our forecast moderation in overall wages growth.

The FWC emphasised that slow growth in labour productivity was mostly an outworking of the expansion in the care economy. We have been highlighting this for some time (see here, here and here). It is a multi-decade trend as well as reflecting the more recent ramp-up in the NDIS. Some drag on economy-wide measures of productivity might therefore be expected to continue. Importantly, though, this will have almost no implications for labour costs in the sectors where rising labour costs might actually influence prices and so inflation, such as business services. The RBA has increasingly recognised this over the past year. The minutes did note that productivity growth has yet to pick up and that this is a potential upside risk to inflation. However, this is a far cry from the comments in the August 2024 minutes about ‘the need for productivity growth to recover in order to help reduce growth in unit labour costs.’

Turning to the policy decision, as in the post-meeting media conference, there is a hint in the minutes that the staff went to the meeting with either an open recommendation, or at least a weaker steer than a specific recommendation would normally imply.

The Board clearly considered the case for a hold. This case rests on a view that domestic labour and product markets are still tight and policy not that restrictive. Tactical considerations also entered into the debate, including an argument to ‘wait and see’ given the current uncertainty. The minutes also cited concerns about near-term fluctuations in headline inflation. Note that this argument runs counter to a more standard view that monetary policy should focus on keeping inflation sustainably inside the target range.

Having dismissed the case to hold, the Board acknowledged that ‘trends in domestic conditions could, on their own, justify some degree of reduction in the cash rate target at this meeting.’ It was therefore ‘no longer necessary to be as restrictive’. This was a point we noted in our discussion at the time of the meeting, though it came out less clearly in the post-meeting RBA communication; for example, the Overview of the Statement on Monetary Policy concluded ‘that it was appropriate to ease monetary policy at this meeting. The Board nevertheless remains cautious about the outlook’.

Developments overseas strengthened the case for a rate cut. As we noted post-meeting, the RBA now views the tariffs and broader trade dispute as being more likely to reduce inflation than add to it. This is a shift from the more equivocal language in April, that ‘the implications for inflation would be more complicated’.

The minutes record a fairly open discussion about the appropriate size of the cut. The case for a larger-sized 50bp cut rested on the idea that the downside risks were large enough that some of the future easing path should be front-loaded. Given the Board’s views of the impact on the Australian economy – and especially its views on China – this argument was unlikely to resonate with members. The minutes were also clear that the Board would not want to give the impression that a large cut now meant a larger overall easing phase and lower landing point. As we argued ahead of the meeting, it was a bridge too far to expect the RBA’s thinking to pivot all the way from hawkish cut in February to going hard in May. Consistent with the circumspect reaction we identified then, the Minutes expressed a preference for moving ‘cautiously and predictably’. It also noted members’ judgement that ‘it was not yet time to move monetary policy to an expansionary stance’. This raises the question of where ‘neutral’ is, but for now we expect that the Board will tread carefully from here, given the uncertainties involved in assessing this.

Our read of the RBA’s recent communication remains that it will not rush further cuts. In particular, we expect that it is not looking to follow up the May cut with one at the July meeting. August remains the most likely date for the next cut.

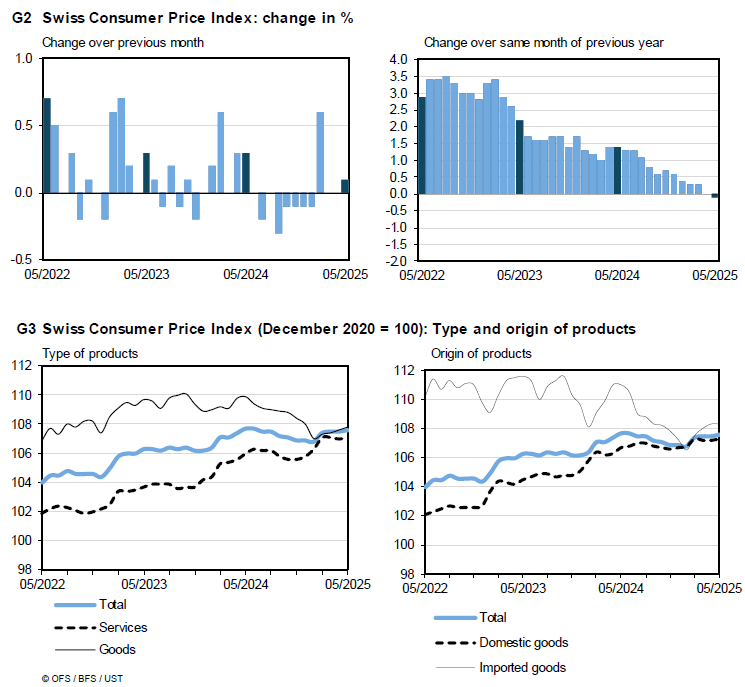

Swiss CPI falls to -0.1% yoy, first negative since 2021

Swiss consumer inflation turned negative in May for the first time since March 2021, with headline CPI falling -0.1% yoy, down from 0.0% in April yoy. Core inflation, which strips out volatile components such as fresh food and energy, slipped to 0.5% yoy from 0.6% yoy previously.

On a monthly basis, both headline and core CPI rose 0.1%, in line with expectations.

The breakdown reveals that domestic product prices grew just 0.2% mom and decelerated to from 0.8% yoy to 0.6% yoy. Imported goods prices were flat on the month and fell -2.4% yoy, ticked up from -2.5% yoy.

Markets Clearly Struggled to Find a Coherent Directional Storyline

Markets

Markets clearly struggled to find a coherent directional storyline yesterday. A new layer of trade uncertainty (US potentially raising steel tariffs to 50%, mutual US-China accusations of not meeting the Geneva agreements) caused investors to start with a guarded risk off bias, weighing on the dollar and on equities. Core yields kept an upward bias (higher risk premia? inflation fears?). The US manufacturing ISM confirmed the stagflationary risk related to US trade policy. Activity data disappointed. The headline index eased further in contraction territory (48.5), showing little relief from the truce in reciprocal tariffs. Some sub-series (production, orders, employment) were less negative but remain sub 50. A sharp decline in imports suggests further supply chain complications. Elevated prices paid (69.4) confirmed ongoing stagflationary risks. In a first reaction, yields, the dollar and equities declined further. Subsequent rebound, especially in equities, was a bit remarkable. US indices reversed losses and closed in positive territory (S&P 500 +0.41%). US yields added about 3-4 bps across the curve. We see the move mainly as technical in nature with markets holding recent ST ranges. In a similar move to the US, German yields added between 1.3 bps (2-y) and 3.2 bps (30-y). With respect to the risk persistent high long term yields, central bankers and government issuers recently indicated they might take action to restore the supply balance. In this respect, BOE’s Catherine Mann addressed the tensions between unwinding the BoE’s balance sheet via QT and at the same time easing policy via (gradual) rate cuts. This suggests some internal debate on the pace of QT to be decided for October. The minutes of a meeting between the BOJ and financial institutions this morning also illustrates this issue. Question is whether changing supply across the curve will be enough to manage the broader issue of excessive deficits risk premia. The dollar post-ISM closed near the intraday lows (DXY 98.7, EUR/USD 1.1441).

Asian markets show no clear trend this morning. A weak Caixin manufacturing PMI (cf infra) triggered further calls for new stimulus. A Japanese 10-y bond auction met decent demand. USD rebounds slightly. Today, the EMU flash May CPI is expected to print at 0.0% M/M and 2.0% Y/Y (core expected at 2.4% from 2.7%). We don’t expect the data to change markets’ assessment the Thursday’s expected 25 bps rate cut. The focus turns to the staff forecast and Lagarde’s guidance (pause?). In the US, JOLTS job openings are interesting, but markets probably will wait for Friday’s payrolls to draw any conclusion on the (length of the) Fed’s current wait-and-see stance. Even as there is some ‘improvement’ this morning YTD lows in the dollar (DXY, EUR/USD) stay within reach.

News & Views

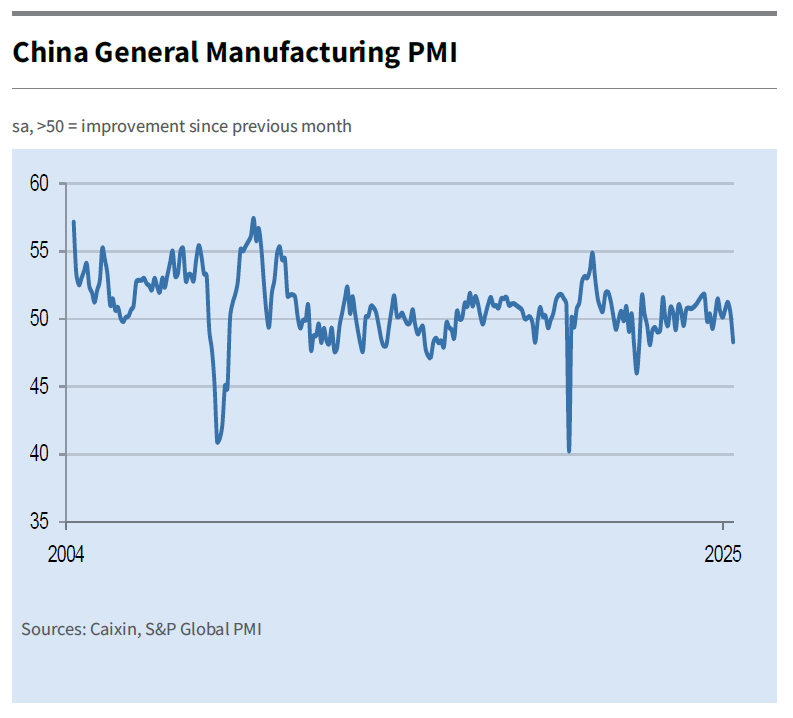

China’s Caixin manufacturing PMI signaled a first deterioration in operating conditions in eight months. The headline figure slumped from 50.4 to 48.3 (lowest since September 2022) with consensus expecting a slight improvement. Manufacturing output declined alongside a renewed fall in new orders. Incoming new work contracted at the quickest pace in over two-and-a-half years. Export orders also shrank at a faster pace. In line with reduced operations, firms cut back on their purchasing activity and lowered their staffing levels. Turning to prices, average input costs and output charges continued to decline. Moreover, the rates of reduction accelerated since April. Finally, optimism picked up since April as firms grew more hopeful that trade conditions can improve and the widening of export markets will help to drive sales in the year ahead. Caixin Insight Group suggested that Chinese policy needs further evaluation. “Follow-up actions should be introduced based on actual conditions. More importantly, boosting domestic demand should be grounded in increasing household incomes by improving employment environment, strengthening social security, raising household disposable income, improving market expectations, and ultimately driving a continued economic recovery.”

Polish PM Tusk will seek a confidence vote – which he’s unlikely to lose - to shore up support for his pro-European coalition government after his candidate narrowly lost presidential election against nationalist PiS-nominee Nawrocki. That way, the biggest opposition party holds on to a key mandate which is more than just ceremonial. PM Tusk said he has an “emergency plan” in case of a continued difficult cooperation with the (new) president. Nawrocki is unlikely to side with Tusk to support legislation and is for example strongly opposed to ease the country’s strict abortion law. Polish markets reacted orderly yesterday to the overall status quo. The zloty temporary spiked to EUR/PLN 4.27 before returning to the 4.24-area.

June Starts With Mixed Feelings

The month of June started on a bearish note, as renewed trade tensions and mixed economic data dominated the headlines. First, tensions between the US and China notched up another level, with both countries accusing each other of violating agreements and implementing discriminatory measures. It’s now uncertain whether Trump and Xi will meet to talk.

Then, not much progress has been made on the European front—aside from growing frustration in Brussels after the US doubled steel and aluminium tariffs to 50%, effective mid-June. Remember, the deadline for US–EU negotiations is July 9th—almost too soon to be optimistic. Meanwhile, tensions between the EU and China are also rising, with the EU deciding not to purchase medical equipment from China, citing ‘reciprocity of purchasing.’ If Europeans start playing by Trump’s rules, the next four years could turn into a global nightmare. At least everyone will get a slice of the horror pie—apparently, that’s what global politicians are aiming for.

Cherry on top, trade tensions are now accompanied by military tensions. The British PM announced yesterday at the government’s Strategic Defense Review that £15bn will be spent to bring Britain up to ‘war-fighting readiness’. Needless to say, European defense stocks cheered the news: Babcock—which makes submarines and warships—rallied more than 8% to a fresh all-time high. The Select Stoxx Europe Aerospace & Defense ETF gained another 1.63%, also reaching a new record, while the rest of the Stoxx 600 remained muted.

Gold rallied to a three-week high on the back of renewed geopolitical jitters, while USDCHF sank below the 0.82 mark amid flight to safety—toward the Swiss economy, which expanded by 2% in Q1. That growth was largely driven by a surge in exports to the US ahead of tariff implementation, suggesting it could be temporary. Swiss inflation data will likely show the first negative print since April 2021—fueling expectations that the Swiss National Bank (SNB) could cut rates back to 0% this month.

Elsewhere, the latest PMI figures signaled continued contraction in German manufacturing but a surprise improvement in Italy and Spain. Overall, the Eurozone’s manufacturing PMI beat expectations, while ISM data in the US hinted at slowing activity. That wasn't enough to stir the Federal Reserve (Fed) doves, though—the US 2-year yield rebounded 4bp on Monday, and the dollar is now poised to retest its YTD lows from April.

Most investors remain bearish on the US dollar, expecting continued debasement due to lackluster growth and a Fed unwilling to offer support amid an uncertain inflation outlook. As a result, EURUSD is consolidating gains above the 1.14 mark. The next natural target for bulls is 1.1573—the level reached on April 21, when the dollar index also touched its 2025 low. The euro outlook remains positive on expectations that near-target inflation will allow the European Central Bank (ECB) to deliver a comfortable 25bp cut this week—and possibly another one this summer. Euro traders will be watching closely for confirmation in today’s flash CPI update for May.

Across the Channel, persistent inflation remains a headache for Bank of England (BoE) doves. But many economists and investors worry that the BoE has fallen behind the curve, and that fiscal measures pose a serious risk to UK growth—demanding closer attention. Either way, dollar weakness is the primary driver of GBPUSD, which has climbed above 1.35 and could extend gains if the greenback continues to slump, as many expect. Interestingly, the FTSE 100 has remained resilient despite sterling’s strength. Defense stocks and gold miners are thriving in this climate—Fresnillo rose 6% yesterday and has been rising exponentially since the start of the year.

In commodities, US crude closed above its 50-day moving average for the first time since March 31. But weaker-than-expected Caixin manufacturing data from China is weighing on sentiment this morning. Copper futures—seen as a barometer of global economic health—are also under pressure. Meanwhile, VanEck’s rare earth and strategic metals ETF is stuck at multi-year lows. Appetite is depressed by Chinese export restrictions, which frustrate Trump’s USA, which needs these materials for its tech sector—and may not get them if trade tensions continue down their current destructive path.

In the US, however, the S&P500 managed to shrug off trade anxieties: steel and aluminium stocks rallied on the extra tariff news, Big Tech remained in demand, and large banks cheered reports that the Trump administration may ease regulations for major lenders. Traders may be explicitly betting that Trump will soften his tariff stance during the 90-day pause—now dubbed the “TACO” trade (Trump Always Chickens Out)—or they may simply be ignoring the trade risks out of FOMO. In either case, the rally looks fragile and risks remain.

Final note: the Japanese 10-year auction saw stronger-than-expected demand and pulled the 10-year JGB yield below the 1.50% mark. Notably, increased demand for Japanese government bonds has tended to coincide with selling pressure in the S&P500 since last summer—largely due to the unwinding of Japanese carry trades, which sent shockwaves through global financial markets. As such, relatively high Japanese yields increase the risk of reverse carry trades and should be watched closely.

All Eyes on US JOLTS and EA HICP Inflation

In focus today

In the euro area, focus turns to the May HICP inflation. We expect headline inflation to decline to 2.0% y/y from 2.2% y/y, driven mainly by core inflation falling from 2.7% y/y to 2.4% y/y, based on regional data already released. The expected decline in core inflation is due to base effects and as the monthly price growth in transport services will likely decline following the strong increases in April related to Easter. We expect energy inflation to remain negative due to the recent fall in energy prices and the strengthening of the euro.

Also in the euro area, we will receive data on the unemployment rate in April, which is expected to remain record low at 6.2% as indicated by survey data.

In the afternoon, US JOLTs labour turnover survey is due for release for April. We will keep a close eye on how the number of job openings as well as firms' hiring and layoffs evolved after the 'Liberation Day'. In the evening, the Fed's Cook and Logan will be on the wires.

In Sweden, the Riksbank board participates in an open parliamentary hearing on monetary policy (09:00-11:00 CET) as part of the annual evaluation conducted by external researchers. While it is 2024 that is up for scrutiny, there is always a chance of comments on current monetary policy,s which is extremely interesting two weeks ahead of the June meeting with still close to a 50/50 pricing of a cut.

Economic and market news

What happened overnight

In China, manufacturing PMIs from Caixin (private version) fell unexpectedly from 50.4 to a weak 48.3 in May, marking the first contraction in the sector in eight months and indicating US tariffs are now really starting to hit the Chinese manufacturing sector. The reading was the steepest decline since September 2022 and most sub-components fell sharply. However, business sentiment strengthened, supported by hopes of improvements in business conditions.

What happened yesterday

In the US, ISM manufacturing PMI in May came in at 48.5, thus surprising to the soft side relative to both consensus expectations and what regional Fed manufacturing indices were suggesting. Most sub-components remained relatively steady, but manufacturing firms reported the sharpest decline in imports since the financial crisis.

In the euro area, final manufacturing PMI for May confirmed the flash release of 49.4. The final release showed slightly weaker readings in Germany and Italy, compared to the flash release, while France and notably Spain were revised up. The data shows that the euro area manufacturing sector has had a strong improvement in 2025 rising from 45.1 in December 2024. Some front-loading to the US is explaining the improvement, which questions how far further it can go, but domestic factors such as lower ECB rates and rising credit growth is also supporting the sector.

In Sweden, manufacturing PMI eased from 54.2 to 53.6 in May, though remaining firmly in growth territory. The decline was mainly driven by weaker order intake and inventory stocks, but the index for suppliers' raw material and input prices also declined to a 7-month low, due to global raw material price increases.

In Norway, the PMI recovered from 46.2 to 51.2 in May, as expected. The improvement is probably a result of lower global risks as the trade war seems to be less devastating than expected only a month ago. Details a bit mixed with a solid recovery in production (46.5 to 53.4), still solid employment (52.9 to 52.3) whereas new orders improved but remained in contractionary terrain at 48.2.

In geopolitics, peace talks between Russia and Ukraine in Istanbul concluded swiftly amid tensions from a recent large-scale drone attack on Russian bombers. Despite the brief dialogue, both sides agreed to a new prisoner swap. Low expectations surrounded the talks, with Russia demanding Ukraine abandon NATO ambitions and withdraw from Russian-controlled territories. The US has warned of sanctions if progress is not made.

In international trade, the Trump administration is pushing countries to provide their best trade negotiation offers by Wednesday, aiming to wrap up talks within five weeks. The US seeks proposals on tariffs, quotas, digital trade, and economic security, and plans to evaluate responses swiftly to propose reciprocal tariff rates. Active negotiations involve the EU, Japan, Vietnam, and India.

Equities: European- and Nordic equities started the week lower, but US investors shook off the weakness. S&P 500 closed 0.4% and Stoxx 600 -0.1%. However, common for both regions was a defensive preference. Value cyclicals such as banks and industrials were at the bottom, while tech and energy led the US gains. We must admit that the US growth stocks have performed much better than we thought in this rising long-end yields regime. Futures are a notch lower again this morning.

FI and FX: US yields rose some 4-6bp across the curve in yesterday's session, but despite this we saw continued USD weakness as the broad dollar clocked in its weakest level since 2023. The NOK emerged as the top-performing G10 currency, supported by rising oil prices, with USD/NOK trading 15 figures lower during the session and NOK/SEK establishing above 0.9450 once more.

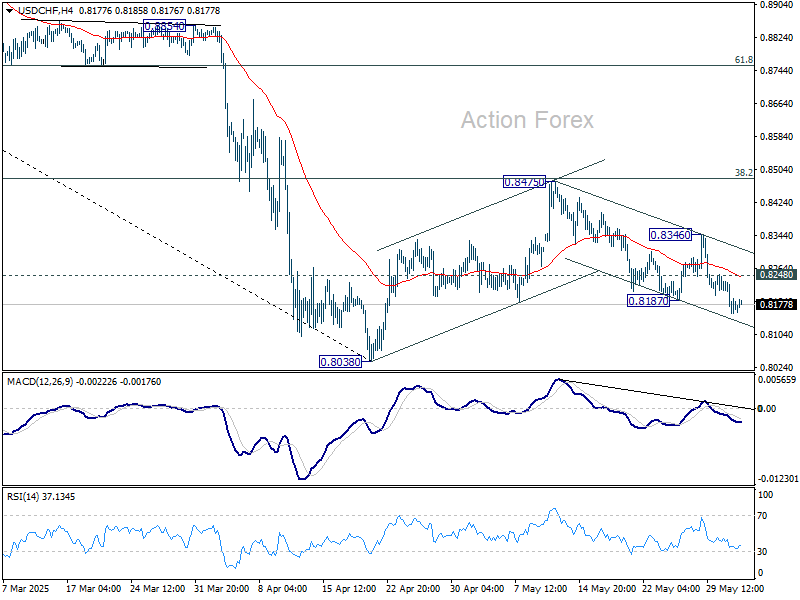

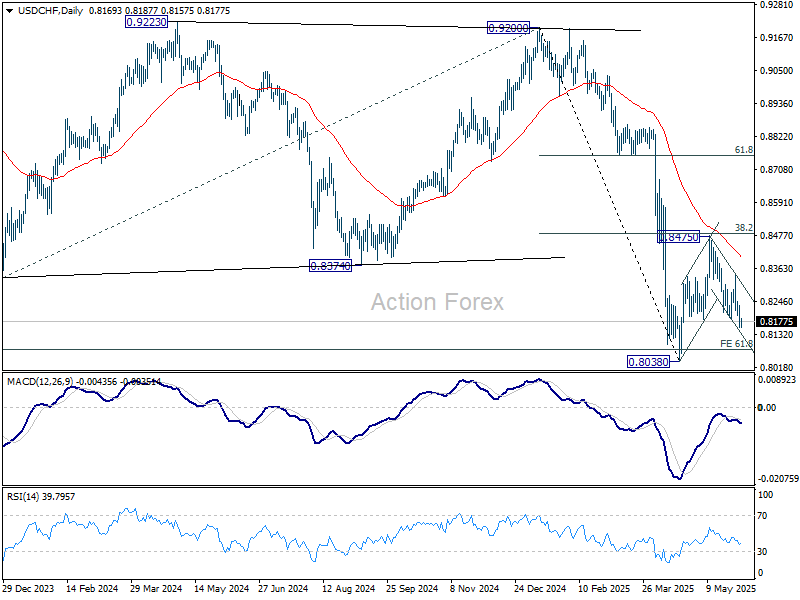

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8139; (P) 0.8189; (R1) 0.8222; More….

Intraday bias in USD/CHF stays on the downside as fall from 0.8475 is in progress for 0.8038 low. Strong support could be seen from there to bring rebound, on first attempt. On the upside, above 0.8248 minor resistance will turn intraday bias neutral first. However, decisive break of 0.8038 will confirm larger down trend resumption.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8732) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

Dollar Struggles, Gold Rally Stalls, Trade Uncertainty Caps Conviction

Global markets remain mixed, reflecting a cautious investor mood amid heightened trade uncertainty and a lack of clear directional drivers. US stocks closed modestly higher overnight, reversing losses from earlier in the session. Asian equities broadly followed the rebound, seemingly brushing off disappointing Chinese manufacturing data. The overall tone, however, remains indecisive, with no strong commitment to risk assets or safe havens.

In the currency markets, Dollar is recovering slightly after a brief selloff, but still stands as the week’s worst performer. Loonie and Aussie follow behind. Yen continues to lead on safe-haven demand. Kiwi and Euro are also holding firmer, with Sterling and Swiss Franc sitting mid-pack. The lack of clear directional bias reflects the broader market indecision, as traders await clarity on the outcome of key trade negotiations.

Underlying this market hesitation is persistent uncertainty surrounding global trade. According to a Reuters report, the Trump administration is pressing trading partners to submit their "best offers" by Wednesday, as it pushes to fast-track negotiations ahead of the July 9 expiry of the current 90-day reciprocal tariff truce. The US is requesting commitments on tariff and quota concessions, along with action plans on non-tariff barriers.

The draft communication from the US Trade Representative warns countries not to assume tariffs will be halted, even if court rulings go against the administration. The letter asserts that the White House intends to continue the tariff program under "other robust legal authorities" if necessary, signaling that tariffs remain a core policy tool in negotiations.

With legal and diplomatic fronts both in flux, traders are taking a wait-and-see approach. Until there is clarity on the direction of US trade policy—particularly with key partners like China and the EU—market participants are likely to stay sidelined. For now, short-term positioning continues to be dictated more by event risk management than conviction.

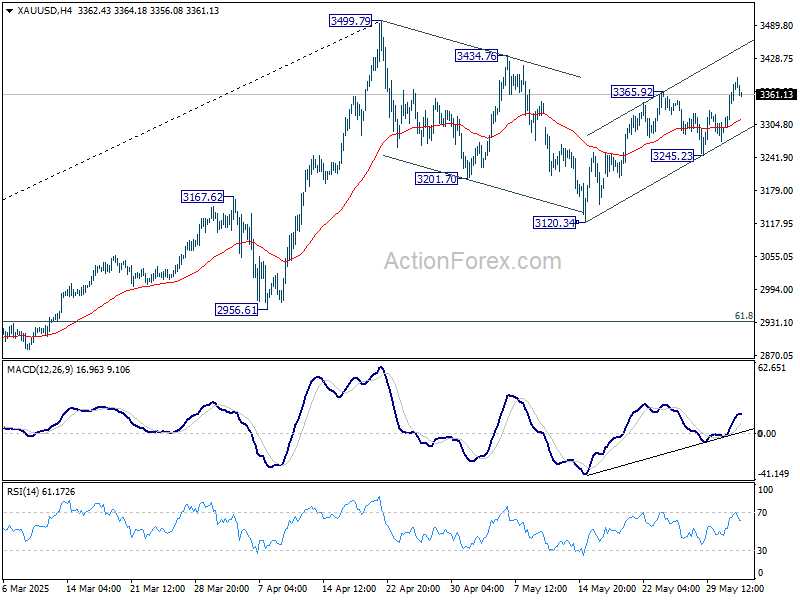

Technically, Gold's rise from 3120.34 resumed by breaking through 3365.92 resistance. Further rally should be seen to retest 3499.79 high. but strong resistance could be seen there to limit upside on first attempt, to bring more sideway trading in the near term. Nevertheless, decisive break of 3499.79 will confirm larger up trend resumption.

In Asia, at the time of writing, Nikkei is up 0.07%. Hong Kong HSI is up 1.10%. China Shanghai SSE is up 0.36%. Singapore Strait Times is down -0.26%. Japan 10-year JGB yield is down -0.025 at 1.484. Overnight, DOW rose 0.08%. S&P 500 rose 0.41%. NASDAQ rose 0.67%. 10-year yield rose 0.046 to 4.462.

Looking ahead, Swiss CPI and Eurozone CPI flash are the main focuses in European session. US will release factory orders later in the day.

BoJ's Ueda: Ready to hike if wage growth recovers from tariff drag

BoJ Governor Kazuo Ueda told parliament today that recently imposed U.S. tariffs could weigh on Japanese corporate sentiment, potentially impacting winter bonus payments and next year’s wage negotiations.

He acknowledged that wage growth may "slow somewhat" in the near term due to these external pressures. However, Ueda expressed confidence that wage momentum would eventually "re-accelerate", helping to sustain a moderate growth in household consumption.

Looking ahead, Ueda reiterated the BoJ’s readiness to adjust its ultra-loose policy if the economy evolves in line with its projections. “If we're convinced our forecast will materialize, we will adjust the degree of monetary support by raising interest rates,” he said.

However, he cautioned that uncertainty surrounding the economic outlook remains “extremely high.”

RBA's Hunter: AUD’s recent resilience linked to global shift away from USD exposure

RBA Chief Economist Sarah Hunter addressed the unusual behavior of the Australian Dollar in recent months in a speech today. She highlighted that while initial moves were consistent with past risk-off episodes, the currency’s subsequent rebound against the US Dollar stood out as "more unusual".

On a "trade-weighted" basis, AUD has remained broadly stable, even though it has appreciated against the greenback and the Chinese renminbi, while weakening against most other major currencies.

This divergence, Hunter explained, stems from "offsetting factors". Global growth concerns have pressured the AUD against safe-haven and cyclical peers, while simultaneous outflows from US assets have weakened the US Dollar.

Hunter cautioned that it's too soon to tell whether this trend will persist, but acknowledged that recent market behavior reflects shifting investor sentiment, particularly toward capital reallocation away from US assets. As a result, Australian Dollar’s relative resilience against USD may be underpinned by portfolio rebalancing and perceived relative economic stability.

Hunter noted that the trade-weighted index has reverted to "pre-shock values", suggesting minimal net change in the foreign-currency value of Australian exports. However, the "relative move of capital" into Australia, at a time when the US is facing policy and tariff-related volatility, could offer some support to "domestic investment activity", providing a cushion to the broader economy amid global uncertainties.

RBA Minutes: 25bps cut chosen for caution and predictability after debating hold and 50bps options

RBA’s May 20 meeting minutes revealed that policymakers weighed three policy options—holding rates, a 25bps cut, or a larger 50bps reduction—before ultimately opting for a modest 25bps cut to 3.85%.

The case for easing hinged on three key factors: sustained progress in bringing inflation back toward target without upside surprises, weakening global conditions and household consumption, and the view that a cut would be the “path of least regret” given the risk distribution.

While members discussed a 50bps reduction after deciding to ease, they found the case for a larger move unconvincing. Australian data at the time showed little evidence that trade-related global uncertainty was materially harming domestic activity. Furthermore, some scenarios might even result in upward pressure on inflation, prompting caution. The Board also assessed that it was "not yet time to move monetary policy to an expansionary stance".

Ultimately, the Board judged that to move "cautiously and predictably" was more appropriate.

Caixin PMI manufacturing drops to 48.3, as China faces marked weakening at start of Q2

China's manufacturing sector unexpectedly shrank in May, with Caixin PMI falling to 48.3 from 50.4, well below market expectations of 50.6. This marked the first contraction in eight months and the lowest reading since September 2022.

According to Caixin Insight’s Wang Zhe, both supply and demand weakened, with a particularly notable drag from overseas demand. Employment continued to contract, pricing pressures remained subdued, and logistics saw moderate delays. Although business optimism saw a marginal recovery, the broader picture points to intensifying headwinds.

The report highlights the fragile start to Q2, with Wang pointing to a "marked weakening" in key economic indicators and a "significantly intensified" level of downward pressure.

Fed’s Goolsbee warns against repeating ‘transitory’ mistake on tariff inflation

Chicago Fed President Austan Goolsbee said in a webcast overnight that tariffs typically lead to a one-time price increase rather than sustained inflation.

Drawing on textbook theory, he said a 10% tariff would create a 10% rise in prices for imported goods for "one year", after which the inflationary effect dissipates. Such shocks are usually seen as "transitory" by central banks, Goolsbee explained.

However, he warned against underestimating potential risks, citing lessons from the pandemic-era supply chain disruptions. “We learned the last time around” not to dismiss inflation too quickly, Goolsbee said, referencing how persistent inflation caught the Fed off guard.

He added that scenarios combining rising prices and weakening labor markets, a stagflationary mix, present the most difficult challenge for monetary policy, as "there’s not an obvious playbook”.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8139; (P) 0.8189; (R1) 0.8222; More….

Intraday bias in USD/CHF stays on the downside as fall from 0.8475 is in progress for 0.8038 low. Strong support could be seen from there to bring rebound, on first attempt. On the upside, above 0.8248 minor resistance will turn intraday bias neutral first. However, decisive break of 0.8038 will confirm larger down trend resumption.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8732) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

RBA’s Hunter: AUD’s recent resilience linked to global shift away from USD exposure

RBA Chief Economist Sarah Hunter addressed the unusual behavior of the Australian Dollar in recent months in a speech today. She highlighted that while initial moves were consistent with past risk-off episodes, the currency’s subsequent rebound against the US Dollar stood out as "more unusual".

On a "trade-weighted" basis, AUD has remained broadly stable, even though it has appreciated against the greenback and the Chinese renminbi, while weakening against most other major currencies.

This divergence, Hunter explained, stems from "offsetting factors". Global growth concerns have pressured the AUD against safe-haven and cyclical peers, while simultaneous outflows from US assets have weakened the US Dollar.

Hunter cautioned that it's too soon to tell whether this trend will persist, but acknowledged that recent market behavior reflects shifting investor sentiment, particularly toward capital reallocation away from US assets. As a result, Australian Dollar’s relative resilience against USD may be underpinned by portfolio rebalancing and perceived relative economic stability.

Hunter noted that the trade-weighted index has reverted to "pre-shock values", suggesting minimal net change in the foreign-currency value of Australian exports. However, the "relative move of capital" into Australia, at a time when the US is facing policy and tariff-related volatility, could offer some support to "domestic investment activity", providing a cushion to the broader economy amid global uncertainties.

BoJ’s Ueda: Ready to hike if wage growth recovers from tariff drag

BoJ Governor Kazuo Ueda told parliament today that recently imposed U.S. tariffs could weigh on Japanese corporate sentiment, potentially impacting winter bonus payments and next year’s wage negotiations.

He acknowledged that wage growth may "slow somewhat" in the near term due to these external pressures. However, Ueda expressed confidence that wage momentum would eventually "re-accelerate", helping to sustain a moderate growth in household consumption.

Looking ahead, Ueda reiterated the BoJ’s readiness to adjust its ultra-loose policy if the economy evolves in line with its projections. “If we're convinced our forecast will materialize, we will adjust the degree of monetary support by raising interest rates,” he said.

However, he cautioned that uncertainty surrounding the economic outlook remains “extremely high.”

Caixin PMI manufacturing drops to 48.3, as China faces marked weakening at start of Q2

China's manufacturing sector unexpectedly shrank in May, with Caixin PMI falling to 48.3 from 50.4, well below market expectations of 50.6. This marked the first contraction in eight months and the lowest reading since September 2022.

According to Caixin Insight’s Wang Zhe, both supply and demand weakened, with a particularly notable drag from overseas demand. Employment continued to contract, pricing pressures remained subdued, and logistics saw moderate delays. Although business optimism saw a marginal recovery, the broader picture points to intensifying headwinds.

The report highlights the fragile start to Q2, with Wang pointing to a "marked weakening" in key economic indicators and a "significantly intensified" level of downward pressure.