Sample Category Title

RBA Minutes: 25bps cut chosen for caution and predictability after debating hold and 50bps options

RBA’s May 20 meeting minutes revealed that policymakers weighed three policy options—holding rates, a 25bps cut, or a larger 50bps reduction—before ultimately opting for a modest 25bps cut to 3.85%.

The case for easing hinged on three key factors: sustained progress in bringing inflation back toward target without upside surprises, weakening global conditions and household consumption, and the view that a cut would be the “path of least regret” given the risk distribution.

While members discussed a 50bps reduction after deciding to ease, they found the case for a larger move unconvincing. Australian data at the time showed little evidence that trade-related global uncertainty was materially harming domestic activity. Furthermore, some scenarios might even result in upward pressure on inflation, prompting caution. The Board also assessed that it was "not yet time to move monetary policy to an expansionary stance".

Ultimately, the Board judged that to move "cautiously and predictably" was more appropriate.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Hybrid – 19 and 20 May 2025

Members participating

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor and Deputy Chair), Marnie Baker, Renée Fry‑McKibbin, Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Alison Watkins AM

Others participating

Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Head, Monetary Policy Strategy), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department)

Financial conditions

Members began their discussion by considering the evolving news on US tariff policy and its impact on global financial markets. The tariffs announced by the US administration on 2 April and subsequent days had been much higher than expected and had led to retaliation in kind by China. Subsequent decisions had paused or reduced some of these increases, at least temporarily; however, at the time of the meeting tariffs were still well above previous levels and future tariff decisions remained highly unpredictable. In response, financial markets had been turbulent. Equity prices, bond yields and many commodity prices had initially fallen quite sharply, and expected volatility in US equity markets had risen to levels only exceeded in recent decades during the global financial crisis and the early days of the COVID-19 pandemic. However, these moves had all been largely or fully unwound, leaving pricing in many global financial markets only modestly changed compared with the time of the previous meeting.

Financial market participants’ expectations for central bank policy rates in many advanced economies had also declined initially and then recovered, but the recovery in policy rate expectations had generally been incomplete. Markets expected most central banks to continue lowering interest rates from their current levels.

Longer term government bond yields in advanced economies had initially declined following the tariff announcements but were generally higher than at the time of the previous meeting, especially in the United States. Market functioning had been somewhat strained at times. Members noted that concerns about the US fiscal position appeared to have contributed to rising term premia. Measures of inflation compensation on US bonds had increased at shorter terms but had fallen over longer horizons, perhaps reflecting an expectation that current tariff settings would be reversed. Inflation compensation on bonds issued by most other countries had declined, driven by falling oil prices and concerns over the impact of tariffs on growth.

In corporate funding markets, both equity prices and spreads on corporate bonds had largely recovered from sharp sell-offs immediately following the 2 April tariffs announcement. In several markets, including Australia, equity prices were now higher than before that announcement. Members discussed how the rebound could be reconciled with the likely adverse effects on global growth of persistently higher tariffs and policy uncertainty. One possibility was that market participants expected further reversals in tariffs. Another was that they expected the effects of tariffs to be more or less offset by stimulatory fiscal and monetary policy in the United States, China and elsewhere, or by the US administration’s planned deregulation agenda. Members noted that such assumptions might prove overly optimistic. They also noted that an adverse global economic outlook was likely to be worse for smaller businesses (which typically are not represented on public equity markets), given they generally have smaller cash buffers.

The Australian dollar had also been volatile, depreciating sharply in early April before rebounding. On a trade-weighted basis, the Australian dollar was around the same level as it was in late 2024. A broad-based depreciation of the US dollar and the Chinese renminbi since early April had offset depreciation of the Australian dollar against the currencies of most other trading partners. Members discussed the somewhat unexpected depreciation of the US dollar in response to the announced increase in US tariffs, which might have been expected to produce an appreciation as the outlook for import growth worsened. The depreciation might reflect an uncertainty premium being applied to US-dollar assets, a correction of previously overweight exposures to US assets or changes in hedging behaviour.

Members then turned to consider how broader Australian financial conditions had evolved. Like the US dollar, Australian markets had been similarly volatile in response to the news about tariffs. Liquidity had declined sharply in the bond market for a time, as it had in other jurisdictions, as a significant number of participants sought to unwind common positions quickly. However, markets had continued to function adequately, and there had not been a broader shift to cash as seen during the global financial crisis or the pandemic. The demand for liquidity at the RBA’s operations had been little changed overall, in part because the level of reserves remains high.

Market expectations for future monetary policy in Australia had moved markedly lower for a time in early April but had partly retraced since then. The swing in policy expectations had been more amplified in Australia than in other economies, largely reflecting thin liquidity in markets but possibly also Australia’s greater trade exposure to China, the flow of domestic data and a perception that international developments were more likely to weigh on inflation in Australia. Policy rate expectations were now consistent with monetary policy being eased by a little more than had been expected at the previous meeting. Market pricing implied a total of around three 25 basis point reductions this year, a little more than expected at the time of the previous meeting. A 25 basis point reduction in the cash rate at the current meeting was widely anticipated. The shift lower in policy rate expectations had been due to both international developments and domestic data relating to consumption and inflation. Members noted that the market-implied path of the cash rate lay within the wide – and inherently uncertain – range of model-based and market economists’ estimates of the neutral interest rate.

Growth in housing credit had been stable in recent months, at around its post-2008 average and a little below growth in household incomes. By contrast, business credit growth had been running ahead of nominal GDP growth, despite weakness in business investment. Members discussed some potential explanations for this, including business credit growth being supported by firms seeking to raise previously low levels of leverage and strong competition among lenders. Issuance of corporate bonds had paused during the period of heightened volatility in early April but had since resumed.

Scheduled household debt payments had eased following the reduction in the cash rate in February but were still around their highest levels since 2012. Extra mortgage payments remained above their pre-pandemic average, consistent with the weakness seen in household consumption. Members noted that some banks do not automatically adjust mortgage payments following a reduction in lending rates, which would have mechanically increased extra payments into redraw accounts as interest rates fell.

Economic conditions

Members turned their discussion to how a persistent increase in trade barriers would affect the global economy. They noted that policy unpredictability had created a highly uncertain environment, depressing sentiment measures in several developed economies outside Australia; in itself, that could weigh on spending by businesses and households abroad. But the overall impact on global growth would also depend on a range of other factors, including the outcome of ongoing trade negotiations, how easily global trading patterns adjust to new tariff settings, and the fiscal and monetary policy response of authorities. Members noted that Chinese authorities had already eased monetary policy and had indicated their willingness to ease fiscal settings further to support economic growth. Authorities in some other economies (particularly in Europe) had also signalled that fiscal settings would be loosened.

Members considered the potential effects on global inflation, noting that these were ambiguous and likely to vary across countries. Inflation in the United States was expected to increase in the near term as higher tariffs would, to some extent, be passed through to consumer prices. Countries not levying new tariffs, including Australia, were more likely to see downward pressure on inflation as weaker global demand and the possible diversion of goods that would otherwise have been sold to the United States depressed prices. But it was also possible that tariffs could impair the complex interlinkages in global supply chains, in turn lifting the prices of traded goods globally.

Members noted that the available data suggested that, prior to the escalation in international trade tensions, economic activity in Australia had been evolving broadly as expected three months earlier. GDP growth had increased in the December quarter 2024 and year-ended growth looked to have picked up a little further in the March quarter. Within that aggregate, indicators of household spending suggested that growth in consumption in early 2025 had been a little lower than expected in February. In part that reflected the impact of flooding in Queensland and New South Wales. But underlying momentum also appeared to have been a little weaker, continuing a pattern that had been evident for some time. Members observed that earlier declines in real household disposable income remained a constraint on consumption, though higher household wealth provided some offset.

The limited information available for the June quarter suggested that recent international developments had so far had little impact on domestic activity. Survey measures of business and consumer sentiment had been little changed. While liaison contacts had noted uncertainty about the international outlook, they still perceived domestic conditions as generally favourable and most were not yet revising their investment or hiring decisions in response to global developments.

Labour market conditions had also so far remained in line with the previous forecasts. The unemployment rate had been around 4.1 per cent since the middle of 2024, while the underemployment rate had declined a little over that period. Employment had recovered from the surprising fall recorded in February. As expected, wages growth had increased slightly in the March quarter, owing to some administered wage decisions and new agreements coming into effect, but it remained lower than a year earlier. Members observed that the rate of voluntary job turnover had declined and that, anecdotally, the focus of wage bargaining and employment disputes had tilted in favour of workers seeking greater job security. Some questioned whether this might see wages growth slow more noticeably than currently forecast.

Members welcomed the broad-based easing in underlying inflation over the preceding year. Trimmed mean inflation had returned to the 2–3 per cent range for the first time since late 2021 and, in six-month annualised terms, was at the midpoint of that range. Although this path had been expected, it provided welcome confirmation that potential upside inflationary risks had not crystallised. Members noted that services price inflation had eased back to around its historical average and that new dwelling costs had fallen further. Headline CPI inflation had been unchanged at 2.4 per cent in year-ended terms in the March quarter and continued to be affected by the timing of payments under government cost-of-living relief measures to households.

Members considered what these developments implied for the degree of spare capacity in the economy. The staff’s assessment was that there was still some tightness in the labour market. This was consistent with a range of indicators, including survey measures of the share of firms reporting that labour availability is constraining output, the high level of job vacancies, and persistently high growth in unit labour costs. Members discussed the extent to which downward pressure on firms’ margins had weighed on inflation, including in house building, noting that there were reports from liaison that weak demand had limited the ability of firms to pass increases in input costs fully through to output prices. They acknowledged that, while broader capacity pressures in the economy appeared to have eased, there remained considerable uncertainty around assessments of the degree of spare capacity.

Outlook

Members noted that the outlook for the global economy had deteriorated over the preceding three months, given developments in trade policies, but that the extent of the deterioration was unusually uncertain. In the baseline forecast – which assumed that tariffs remain around their current levels and that policy uncertainty gradually falls but remains high – growth in Australia’s major trading partners (weighted by their share of Australia’s exports) was expected to slow in 2025 and 2026. The largest downgrades to the growth outlook had been for the United States and several other countries with a high reliance on goods trade. By contrast, the outlook for output growth in China was little changed, reflecting an assumption of increased policy stimulus. Members noted that sentiment in China had improved prior to the announcement of significantly higher-than-expected US tariffs on imports from China, and that authorities there appeared to be both committed to their growth target of around 5 per cent and able to provide more stimulus to the economy if required.

In light of those developments, and the most recent domestic data, the baseline forecast was for Australian GDP growth to pick up a little less rapidly than forecast three months earlier. That reflected three main assumptions: global demand for Australian exports was projected to be somewhat weaker; some weight was placed on the possibility that heightened policy uncertainty might dampen domestic investment and household spending; and near-term momentum in consumption was a little weaker. The technical assumption of a lower cash rate path than in the February forecasts provided some offset to the forecast for domestic activity.

The weaker outlook for Australian GDP growth in the baseline forecast resulted in the forecast rise in the unemployment rate being slightly larger than previously expected, and the forecast for inflation being slightly lower. Underlying inflation was now expected to be around the midpoint of the 2–3 per cent target range throughout the forecast period. Headline CPI inflation was forecast to be more volatile because of the effects of government energy rebates, and to exceed the target range for a time in early 2026.

Given that the rapidly evolving and unpredictable global policy environment was creating more uncertainty than usual around the baseline forecasts, members also considered a range of alternative scenarios for how the Australian economy might evolve under different policy assumptions. One of these scenarios involved an escalation of the trade conflict in which much higher levels of tariffs are imposed permanently, causing global sentiment, growth and asset prices to fall sharply. Absent a material policy response, this would be likely to cause a sharp slowing in Australian GDP growth and an associated sharp rise in the unemployment rate. By contrast, there were scenarios in which there was a swift easing in the trade conflict, which could reduce policy uncertainty. Such scenarios, if still accompanied by stronger policy stimulus abroad than previously expected, could result in a more pronounced recovery in Australian output growth and somewhat higher inflation.

Considerations for monetary policy

Turning to considerations for the monetary policy decision, members noted that there had been further welcome progress towards the Board’s objectives. Underlying inflation had continued to decline, in line with prior projections, and the forecasts were for it to remain close to the midpoint of the 2–3 per cent range over the forecast period. Activity had picked up and employment growth had remained solid. The labour market was still judged by the staff to be tight and the output gap slightly positive, although there remained significant uncertainty about these judgements.

In contrast with domestic conditions, which had evolved close to expectations, there had been significant and unexpectedly adverse developments in the global economy. It was challenging to predict how global trade policy would evolve, but most scenarios posed some downside risk to Australian activity and inflation – and there were some scenarios in which the impact could be significant. The uncertainty associated with global trade policy had also caused liquidity in financial markets to become strained for a time, though this had mostly recovered.

Members assessed monetary policy to be still somewhat restrictive at the current level of the cash rate, although the extent of that restrictiveness was subject to considerable uncertainty.

In light of these developments, members considered whether to leave the cash rate target unchanged at this meeting or to lower it.

The case to hold the cash rate target unchanged rested on three main considerations. First, while underlying inflation had returned to the 2–3 per cent range, headline inflation was expected to rise back up to the top of the target band as energy subsidies unwound. Moreover, labour and product markets remained relatively tight, implying some risk to inflation being contained. Second, there had so far been few observable effects on the Australian economy from developments in the global economy, and policy was evolving on an almost daily basis, so there could be a case for waiting to see if more convincing signs of a domestic impact emerged before adjusting policy. Third, to the extent that the stance of monetary policy was judged not to be very restrictive at its current level, it might not yet be appropriate to relax it.

The case to lower the cash rate target rested on three different considerations. First, the progress made in returning inflation to target without upside risks having crystalised. Second, an assessment that global developments and near-term trends in household consumption had shifted the balance of risks downwards. And third, the possibility that the prevailing uncertainty from global events might best be managed by adopting a path of least regret, which, given the current distribution of risks, would be likely to involve a lower cash rate.

In discussing the case to ease policy, members observed that trends in domestic conditions could, on their own, justify some degree of reduction in the cash rate target at this meeting. Underlying inflation had continued to ease as expected, was back at the midpoint of the 2–3 per cent range in six-month annualised terms and was forecast to remain close to the midpoint throughout the forecast period. The forecast was also conditioned on a technical assumption for the cash rate that incorporated a reduction at this meeting. And the downward revision to the staff’s forecast for consumption suggested there might be a little less momentum in private demand than previously assumed.

Developments in the global economy since the previous meeting strengthened the case for a reduction in the cash rate target. Members noted that the rise in global tariffs and increase in policy uncertainty had adversely changed the outlook for growth in Australia’s major trading partners. It was difficult to quantify the impact of this on Australian activity at this early stage, while international trade policy was still in flux. But the baseline forecast was for a negative effect; and there were scenarios in which output growth could be materially weaker than this. Members noted that, while it was possible that higher global tariffs could lift Australian inflation through impaired supply chains, it was more likely that they would prove to be disinflationary, through weaker aggregate demand.

Having weighed up these alternative arguments, members judged that the case to reduce the cash rate target was the stronger one. They agreed that monetary policy had been effective in bringing inflation back to target, and that it was no longer necessary to be as restrictive given the current rate of inflation and the staff’s assessment of spare capacity. In addition, members judged that a lower cash rate would also be an appropriate response to the downside risks that had emerged from international developments since the previous meeting.

Having determined that it was appropriate to lower the cash rate target at this meeting, members turned their attention to the size of the reduction.

A 25 basis point reduction in the cash rate target at this meeting would be consistent with the technical assumption for the path of the cash rate underpinning the baseline staff forecast, which had underlying inflation expected to remain around the midpoint of the target range over the forecast period. It would recognise the progress made on inflation and the slightly softer outlook for domestic consumption suggested by recent data. It would also give weight to the likelihood that global developments will slow the recovery in activity growth somewhat, while recognising that international trade policy settings were still fluctuating and that so far there were no data signalling an adverse impact on domestic demand in Australia. A 25 basis point reduction would ensure that monetary policy settings remained predictable at a time of heightened uncertainty, given market expectations. And it would leave the Board well placed to respond as needed as the economy evolved.

Limiting the reduction to 25 basis points could be justified by several key uncertainties to the outlook. There were concerns about the strength of the supply side of the Australian economy: for example, productivity growth so far had shown no signs of increasing, and uncertainty about the extent of tightness in the labour market was two-sided. It was also possible that the forecast increase in aggregate demand would facilitate a recovery in profit margins, which would provide more momentum to inflation than expected. And the imposition of higher tariffs in other countries might prove more disruptive for global supply chains than had been factored into the baseline forecasts, raising prices globally. More broadly, members observed that it could be challenging for households and firms if the Board subsequently sought to reverse a loosening in policy that, in hindsight, proved to be too rapid.

On the other hand, a larger reduction in the cash rate target at this meeting could be appropriate if members judged that the downside risks stemming from either global or domestic developments warranted easing monetary policy more quickly than assumed in the baseline forecast.

Members discussed scenarios in which global policy unpredictability had more negative consequences for the world economy than was assumed in the baseline, including the adverse scenario set out in the May Statement on Monetary Policy. They agreed that monetary policy would need to move to an expansionary setting in the event these scenarios materialised. Members observed that there were also downside risks to the outlook stemming from the domestic economy, including that household consumption does not pick up as quickly as envisaged in the baseline forecast or that wages growth slows by more than forecast alongside a softening labour market. In light of this, members noted that a reduction in the cash rate could be warranted on the basis of either domestic or global factors, and that the combination of these might therefore warrant a 50 basis point reduction at this meeting. Members noted that it would be important that a larger reduction at this meeting should not be taken as implying a view that the cash rate path should be lower over the entire forecast period, merely that it reaches the same level sooner to provide greater insurance against more adverse scenarios.

Having weighed up these alternative arguments, members decided that the case to lower the cash rate target by 25 basis points at this meeting was the stronger one. They agreed that developments in the domestic economy on their own justified a reduction in the cash rate target and that the case for that action was strengthened by developments in global trade policy. However, members were not persuaded that the combination of these was sufficient to warrant a 50 basis point reduction at this meeting. Members noted the absence of signs in the Australian data to date that global trade policy uncertainty was having a significant negative impact on the economy, and that some plausible adverse scenarios could see upward pressure on inflation. They also judged that it was not yet time to move monetary policy to an expansionary stance, taking account of the range of estimates involved, given that inflation was yet to return sustainably to the midpoint of the target range and the staff’s assessment that the labour market was still tight. These considerations and the prevailing global policy uncertainty led members to express a preference to move cautiously and predictably when withdrawing some of the current policy restriction.

In finalising the policy statement, members agreed that it was appropriate to convey their commitment to both of the Board’s objectives. They also agreed to convey that policy was well placed to respond decisively to international developments if they were to have material implications for activity and inflation of the kind described in the severe downside scenario set out in the May Statement on Monetary Policy. Members affirmed that future decisions will be guided by the incoming data and the evolving assessment of risks. They agreed that the Board should remain focused on its mandate to deliver both price stability and full employment and that it will do what it considers necessary to achieve that outcome.

The decision

The Board decided to lower the cash rate target by 25 basis points to 3.85 per cent.

Fed’s Goolsbee warns against repeating ‘transitory’ mistake on tariff inflation

Chicago Fed President Austan Goolsbee said in a webcast overnight that tariffs typically lead to a one-time price increase rather than sustained inflation.

Drawing on textbook theory, he said a 10% tariff would create a 10% rise in prices for imported goods for "one year", after which the inflationary effect dissipates. Such shocks are usually seen as "transitory" by central banks, Goolsbee explained.

However, he warned against underestimating potential risks, citing lessons from the pandemic-era supply chain disruptions. “We learned the last time around” not to dismiss inflation too quickly, Goolsbee said, referencing how persistent inflation caught the Fed off guard.

He added that scenarios combining rising prices and weakening labor markets, a stagflationary mix, present the most difficult challenge for monetary policy, as "there’s not an obvious playbook”.

Gold Back on The Move — Can Bulls Sustain The Push?

Key Highlights

- Gold found support near $3,240 and started a fresh increase.

- It cleared a key contracting triangle with resistance at $3,335 on the 4-hour chart.

- EUR/USD is moving higher above the 1.1380 resistance zone.

- WTI Crude Oil prices recovered and climbed above the $63.00 level.

Gold Price Technical Analysis

Gold prices remained supported above $3,220. The price formed a base and started a fresh increase above the $3,280 and $3,300 resistance levels.

The 4-hour chart of XAU/USD indicates that the price cleared a key contracting triangle with resistance at $3,335. There was a clear move above the 61.8% Fib retracement level of the downward move from the $3,438 swing high to the $3,120 low.

The price settled above the $3,350 level, the 200 Simple Moving Average (green, 4 hours), and the 100 Simple Moving Average (red, 4 hours). On the upside, immediate resistance is near the $3,385 level.

The next major resistance sits near the $3,400 level. A clear move above the $3,400 resistance could open the doors for more upsides. The next major resistance could be $3,420, above which the price could rally toward the milestone level of $3,440.

On the downside, initial support is near the $3,350 level. The first key support is near $3,335. The next major support is near the $3,320 level. The main support is now $3,300. A downside break below the $3,300 support might call for more downsides. The next major support is near the $3,250 level.

Looking at EUR/USD, the pair started a decent upward move and might soon aim for a fresh increase if it clears the 1.1420 resistance.

Economic Releases to Watch Today

- Fed's Goolsbee speech.

- ECB's President Lagarde speech.

- Fed's Cook speech.

Gold Surges on Safe-Haven Demand — On Track for New All-Time Highs?

Gold has been rallying consequently since the Sunday open after the Trump Administration decided to appeal the US Federal Court decision to block the Tariffs on Imports.

The precious metal is at the highs of the day following an ISM Manufacturing report that was not the best. You can read more on the Data Release here.

XAU/USD is breaking out to the upside and the buying candles are strong, we are now up 2.52% on the session.

Take a peek at a Gold Technical Analysis from the Daily to the Hourly timeframe.

Gold Technical Analysis - Daily, 4H and 1H Charts

Gold Daily Chart

Gold Daily Chart, June 2, 2025. Source: TradingView

What looked like a Downward channel looks more like a Bull Flag on the Daily Timeframe as prices are breaking out.

MA 20 and 50 are both sustaining the rally as prices consolidated towards the Moving averages.

The Daily 14-period RSI also came back to neutral from overbought levels in April and May and is now rising, giving more space for price movement.

Prices seem to be going towards the main Daily resistance Zone from 3,450 to 3,500.

There will be a few hurdles before which you will discover through 4H and 1H chart analyses.

Gold 4H Chart

Gold 4H Chart, June 2, 2025. Source: TradingView

Gold is breaking out from its downwards daily channel formed throughout the past two months as the risk-off move was another supporting theme.

A rebound on S1, after a bear momentum divergence, resumed the bullish train of action for the Bullion.

Both the 20 and 50 MA are acting as support and are sloping upwards.

The action is fundamentally and technically bullish though things may change with the key data that is coming through this week, particularly the NFP report on Friday expected at 130K.

A beat could change the risk-off sentiment, though there is plenty of time before that.

Key levels on the 4H Chart:

- Support 1 3,270 - 3,290

- Support 2 3,200 - 3,225

- Support 3 3,110 - 3,137

- Resistance 1 3,367 - 3,380

- Resistance 2 3,414 - 3,436

- Resistance 3 $3,500 (All-time Highs)

- Resistance 4 $3,595 - $4,000 (Potential Resistance on new ATH)

Gold 1H Chart

Gold 1H Chart, June 2, 2025. Source: TradingView

Gold is facing the current Resistance Zone R1 mentioned on the 4H Timeframe analysis.

A Inverse Head & Shoulders pattern materialized in the breakout and is pointing to a continuation of today's price action. If it the Inverse H&S completes, the Measured Move points at 3,415 to 3,420.

Gold prices gapped up on the Sunday open and have mostly been in a Tight bull channel since: Almost only green candles with the few red candles not subjecting a pullback.

Prices are broadly unchanged in the past two hours, momentum tends to calm after a volatile session.

A rejection of the Resistance 1 Zone points at the MA 20, currently at $3,336.

A continuation of the move from this morning aims at $3,415.

Safe Trades!

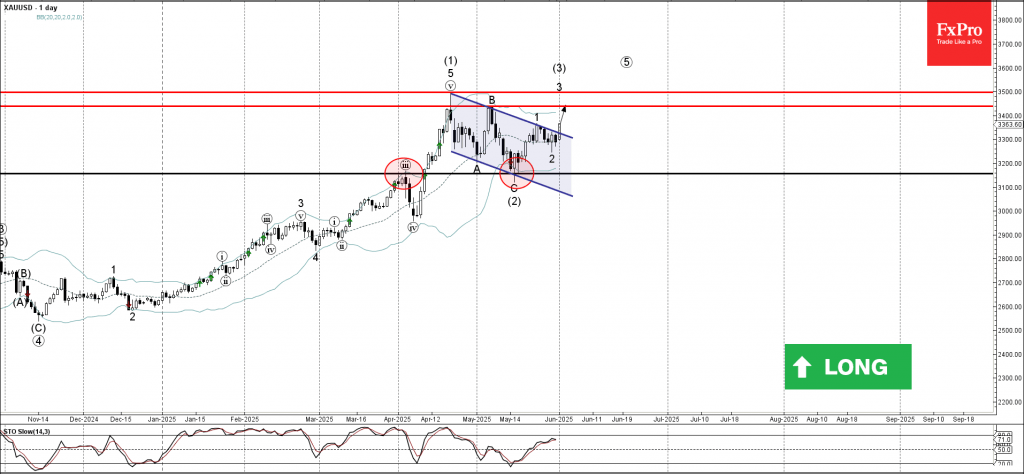

Gold (XAUUSD) Elliott Wave Outlook: Next Bullish Surge Underway

Gold (XAUUSD) has displayed a strong bullish trend since establishing a low on May 15, 2025, forming a sequence of higher highs that signals further upside potential. The rally from the May 15 low unfolded in a clear five-wave Elliott Wave structure, completing wave 1 at $3365.93. The initial advance, wave ((i)), peaked at $3252.05, followed by a corrective pullback in wave ((ii)) to $3153.47. The subsequent rally in wave ((iii)) reached $3345.40, with a minor dip in wave ((iv)) to $3278.79. A final leg, wave ((v)), concluded wave 1 at $3365.93.

Following the completion of wave 1, a corrective wave 2 developed as a double three Elliott Wave structure. From the wave 1 high, wave ((w)) declined to $3284.40, followed by a recovery in wave ((x)) to $3325.51. The subsequent decline in wave ((y)) bottomed at $3245.20, marking the end of wave 2. Gold then resumed its upward trajectory, initiating wave 3. Within this wave, wave ((i)) peaked at $3331.11, and a pullback in wave ((ii)) found support at $3271.09. The metal has since broken above the previous wave 1 high of $3365.93, confirming the start of wave ((iii)) and signaling further upside.

In the near term, as long as the pivot low at $3246 remains intact, pullbacks are expected to attract buyers in a 3, 7, or 11-swing corrective structure, supporting additional gains. Traders should monitor these levels for potential buying opportunities, with the bullish trend likely to persist as long as key support holds.

Gold 60-Minute Elliott Wave Technical Chart

Gold (XAUUSD) Elliott Wave Technical Video

https://www.youtube.com/watch?v=aUfen4kRTig

Gold Wave Analysis

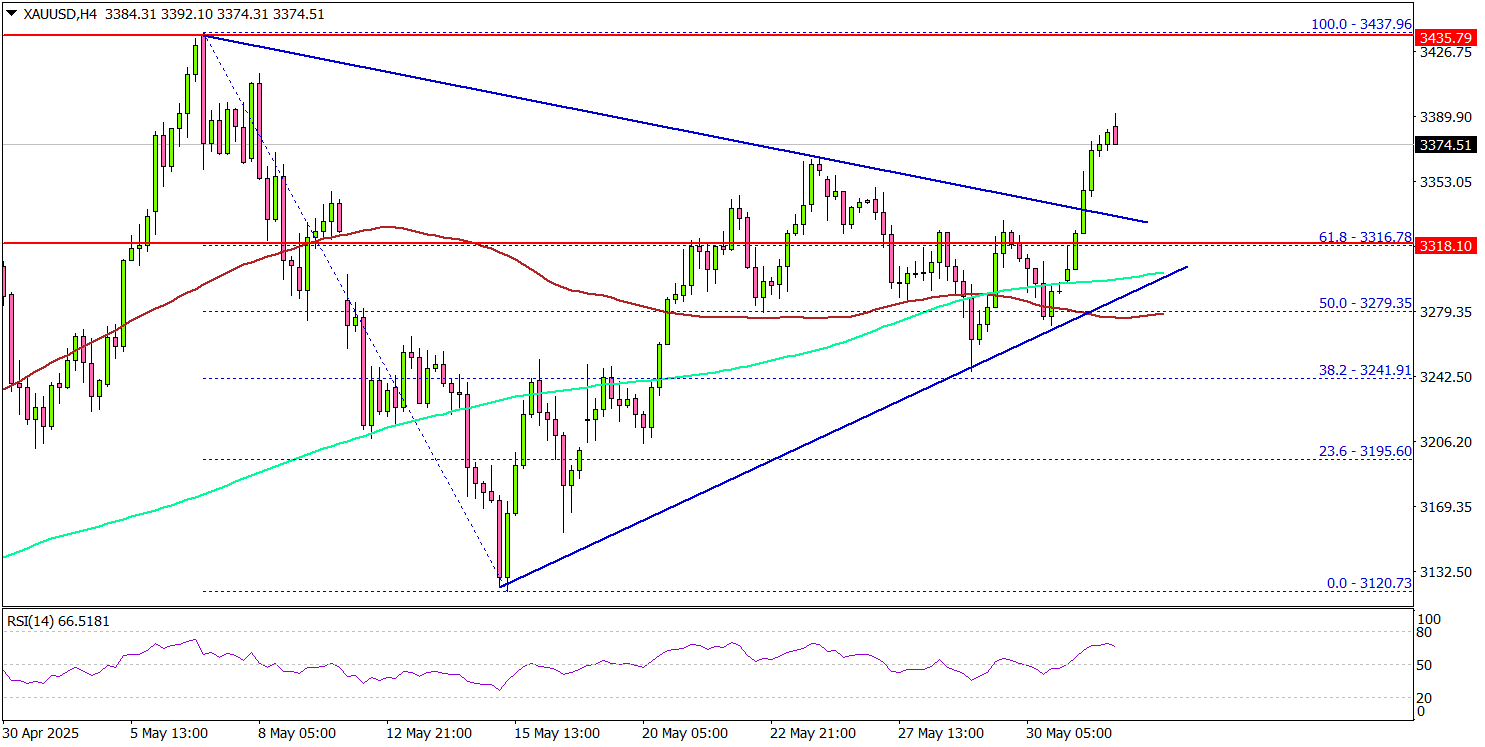

Gold: ⬆️ Buy

- Gold broke daily down channel

- Likely to rise to resistance level 3440.00

Gold recently broke the resistance trendline of the daily down channel from April (which enclosed the previous medium-term ABC correction (2)).

The breakout of this down channel should accelerate the active minor impulse wave 3 of the intermediate impulse wave (3) from May.

Given the clear daily uptrend, Gold can be expected to rise to the next resistance level 3440.00 (top of the B-wave from May).

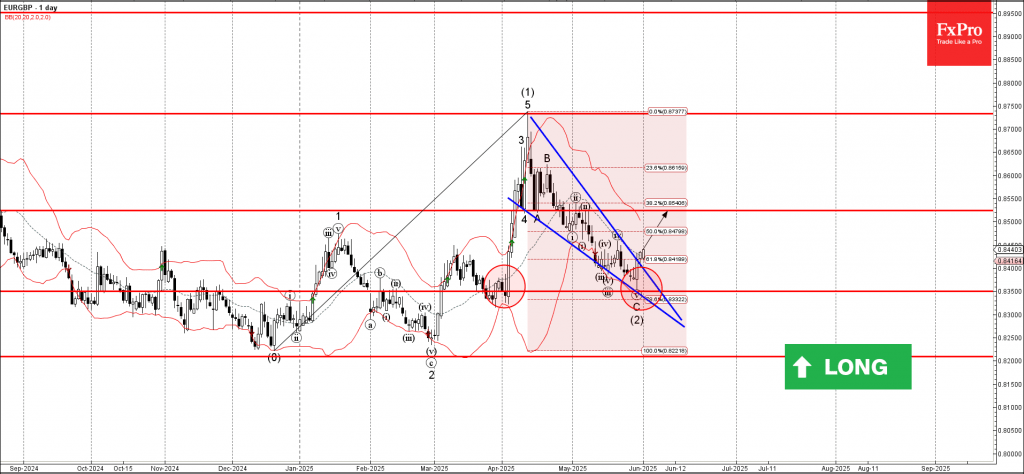

EURGBP Wave Analysis

EURGBP: ⬆️ Buy

- EURGBP broke daily Falling Wedge

- Likely to rise to resistance level 0.8525

EURGBP currency pair recently broke the resistance trendline of the daily Falling Wedge chart pattern from April, which encloses the earlier ABC correction (2).

The breakout of this Falling Wedge continues the active impulse wave (3), which started earlier from the key support level 0.8350.

EURGBP currency pair can be expected to rise to the next resistance level 0.8525 (which reversed the price twice at the start of May).

Fed’s Logan: Tariff-led price shocks must not become persistent inflation

Dallas Fed President Lorie Logan said the current monetary policy setting is "well-positioned to to shifting risks. Speaking at a conference, Logan emphasized that Fed's job is to prevent temporary price shocks, such as those from tariffs, from becoming an "ongoing persistent problem of inflation".

Logan highlighted that tariff-related inflation and broader policy uncertainty present dual threats: not only could they lift prices, but they might also undermine confidence and growth by generating market volatility.

However, she acknowledged that so far the economy has shown resilience, with labor markets remaining balanced and overall conditions stable.