Sample Category Title

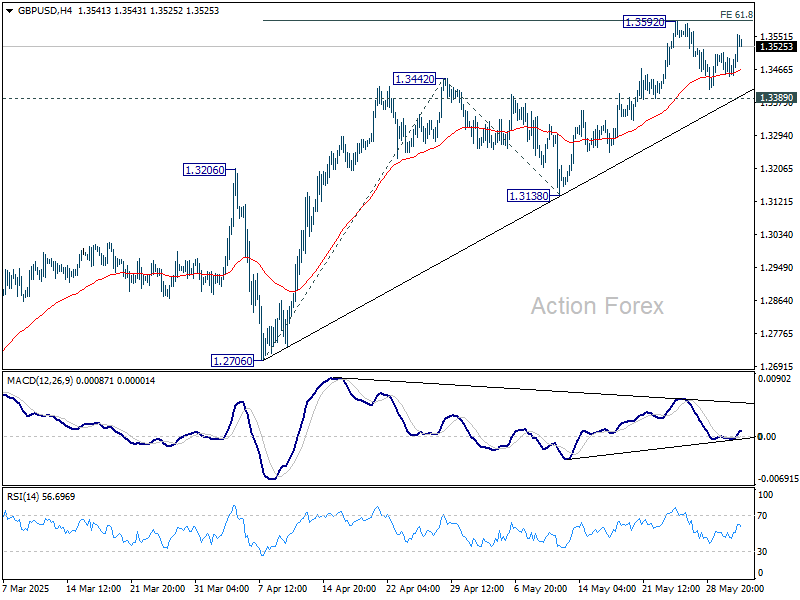

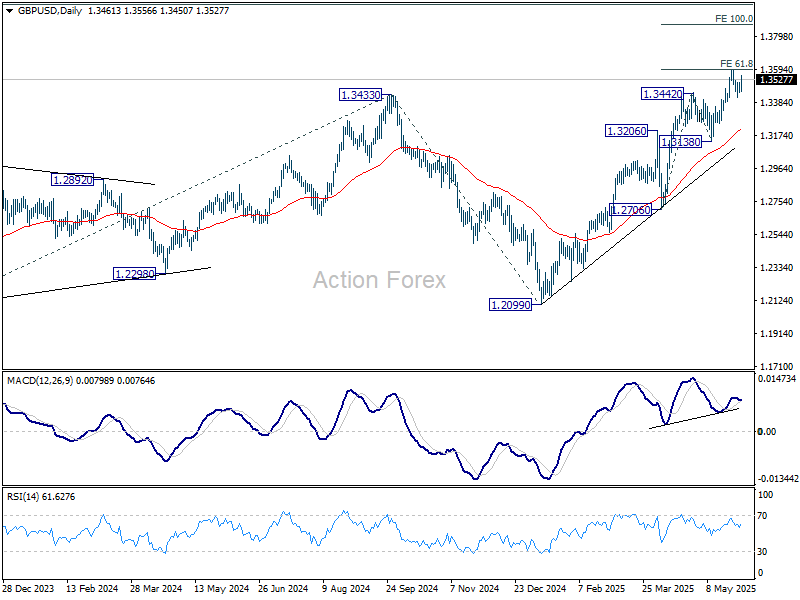

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3431; (P) 1.3471; (R1) 1.3494; More...

Range trading continues in GBP/USD and intraday bias remains neutral. Further rally is expected with 1.3389 support intact. On the upside, firm break of 1.3592 will resume larger up trend to 100% projection of 1.2706 to 1.3442 from 1.3138 at 1.3874. However, decisive break of 1.3389 will confirm short term topping, and turn bias back to the downside for 1.3138 support instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2866) holds, even in case of deep pullback.

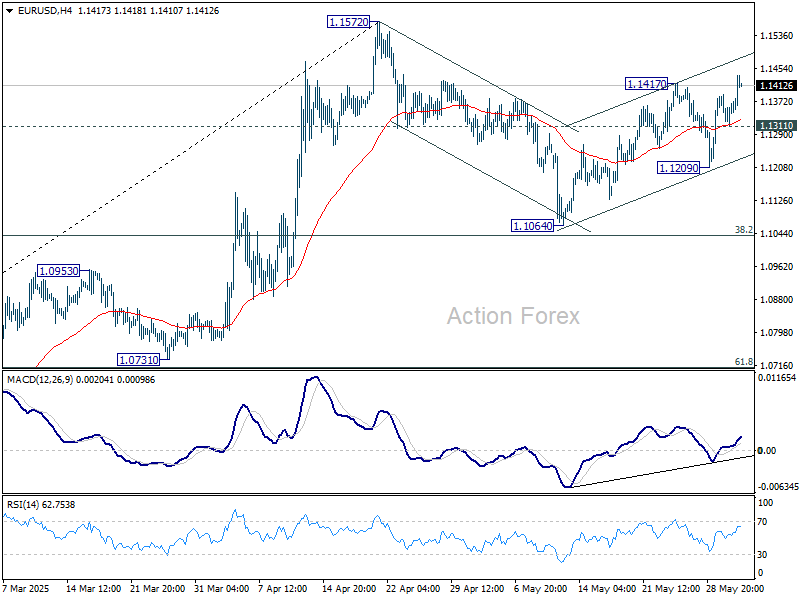

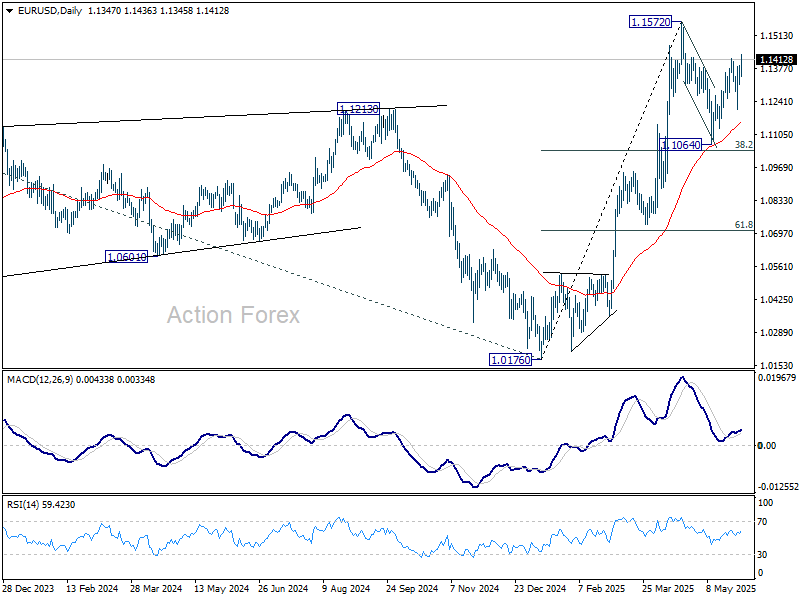

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1310; (P) 1.1350; (R1) 1.1387; More...

Intraday bias in EUR/USD is back on the upside as rebound from 1.1064 resumed by breaking through 1.1417. Further rise would be seen to retest 1.1572. Strong resistance could be seen there to limit upside at first attempt. Below 1.1311 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 1.1572 will confirm larger up trend resumption.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

Trade Tensions Drag Dollar While Oil Jumps on OPEC+ Hold

Risk sentiment remains fragile as the US session gets underway, with equity markets under pressure from renewed tariff threats. European stocks are particularly heavy after US President Donald Trump threatened to double tariffs on imported steel. UK equities, however, are finding some support from Prime Minister Keir Starmer’s announcement of increased defense spending.

In the currency markets, Dollar is under broad pressure, currently the weakest performer of the day as traders react to the heightened trade uncertainty again. Loonie and Swiss Franc are also underperforming. Kiwi leads gains, followed by Yen and Aussie. Sterling and Euro sit in the middle.

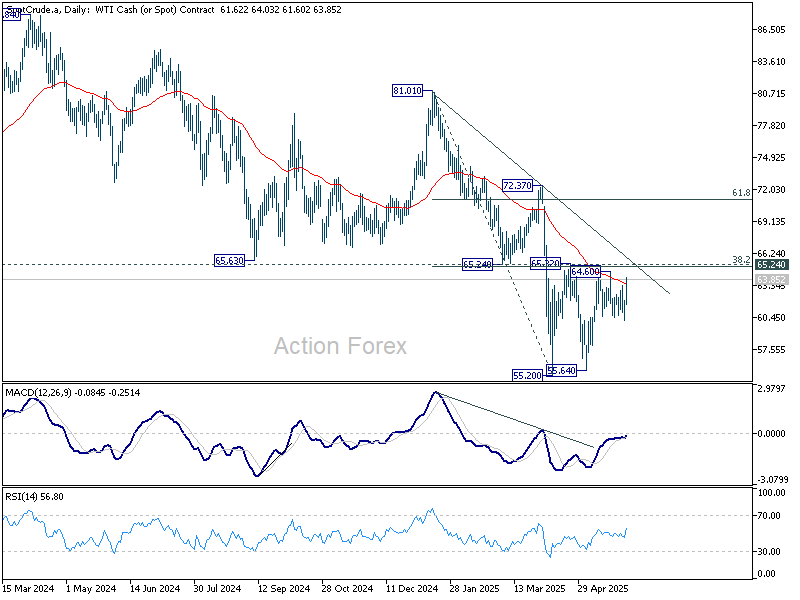

Meanwhile, oil prices have jumped after OPEC+ confirmed it would maintain output increases in July at pace of 411k barrels per day. Markets had been wary of a possible larger hike, as hinted by sources late last week. That outcome would have likely sparked a sharp bearish gap on Monday’s open. The restraint from OPEC+ has thus supported a modest rebound in crude.

Technically, despite the rebound, WTI crude remains capped below key cluster resistance at 65.24 (38.2% retracement of 81.01 to 55.20 at 65.05. As long as this resistance zone holds, outlook will stay bearish for down trend resumption through 55.20 at a later stage. Nevertheless, firm break of 65.05/24 would bring strong rally to 61.8% retracement at 71.15, with risk of bullish trend reversal.

In Europe, at the time of writing, FTSE is up 0.08%. DAX is down -0.45%. CAC is down -0.58%. UK 10-year yield is up 0.025 at 4.674. Germany 10-year yield is up 0.036 at 2.541. Earlier in Asia, Nikkei fell -1.30%. Hong Kong HSI fell -0.57%. Singapore Strait Times fell -0.10%. Japan 10-year JGB yield rose 0.004 to 1.509.

UK PMI manufacturing finalized at 46.4, with tentative signs of stabilization

UK manufacturing activity remained in contraction in May, with PMI finalized at 46.4, up modestly from April’s 45.4.

The data indicate that the sector continues to face “major challenges,” according to S&P Global’s Rob Dobson, citing turbulent domestic and global conditions, trade uncertainty, subdued client confidence, and increased wage costs tied to tax changes.

Still, there are early signs that the worst of the downturn may be easing. The indexes for output and new orders have risen for two consecutive months and were stronger than the initial flash estimates, hinting at possible stabilization.

However, Dobson warned that the sector could either steady or slip further depending on how trading conditions evolve in the coming months.

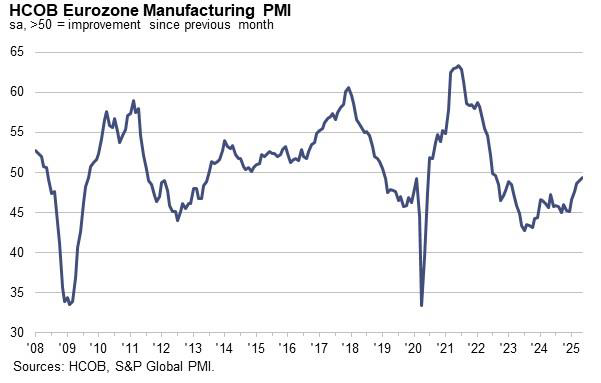

Eurozone PMI manufacturing finalized at 49.4, recovery progressing

Eurozone PMI manufacturing was finalized at 49.4 in May, up from April’s 49.0 and marking the highest level in 33 months.

Production increased across all four major economies: Germany, France, Italy, and Spain, supporting economist Cyrus de la Rubia's view that the recovery is gaining traction.

De la Rubia also noted that output has now risen for three straight months, reinforcing the view that the recovery is gaining traction. Historical data suggests a 72% chance of another output increase next month.

Falling input costs, driven by lower energy prices, have enabled manufacturers to cut selling prices again, offering the ECB more flexibility for its expected interest rate cuts.

However, the outlook remains clouded by external risks, particularly the threat of higher US tariffs on EU goods. Any escalation in transatlantic trade tensions could quickly derail the fragile rebound.

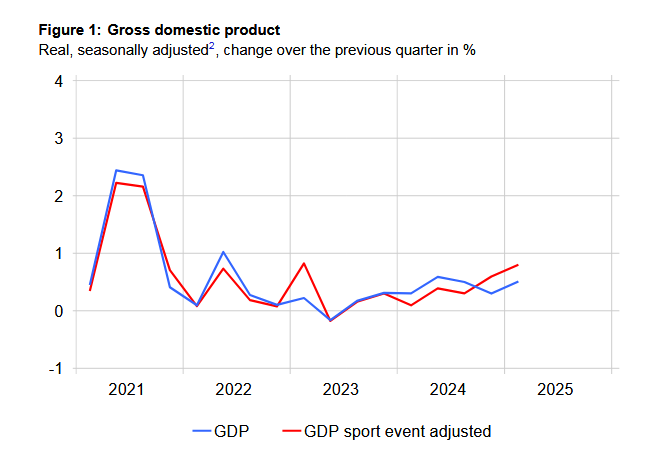

Swiss GDP grew 0.5% in Q1, pharma exports surge on tariff frontloading

Switzerland's GDP expanded by 0.5% qoq in Q1, beating market expectations of 0.4% qoq. When adjusted for the impact of major sporting events, GDP growth came in even stronger at 0.8% qoq. The State Secretariat for Economic Affairs noted that the services sector posted broad-based gains and domestic demand remained firm, contributing to the overall solid performance.

A standout was the chemical and pharmaceutical sector, which surged 7.5% in the quarter, driven by a sharp rise in pharmaceutical exports. This lifted overall manufacturing output by 2.1% and goods exports by 5.0%. Notably, exports to the US jumped significantly, suggesting possible front-loading in anticipation of evolving US trade policy.

Japan’s PMI manufacturing finalized at 49.5, firms eye recovery despite trade headwinds

Japan's PMI Manufacturing was finalized at 49.5 in May, up from April's 48.7. S&P Global’s Annabel Fiddes noted that business conditions “moved closer to stabilisation,” as declines in sales eased and firms reported improved hiring activity.

Global trade tensions stemming from US tariffs continue to weigh on demand, with businesses citing "increased client hesitancy" and weaker orders.

Despite persistent external challenges around tariffs, sentiment around future output improved, and hiring rose at the fastest pace in over a year.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1310; (P) 1.1350; (R1) 1.1387; More...

Intraday bias in EUR/USD is back on the upside as rebound from 1.1064 resumed by breaking through 1.1417. Further rise would be seen to retest 1.1572. Strong resistance could be seen there to limit upside at first attempt. Below 1.1311 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 1.1572 will confirm larger up trend resumption.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

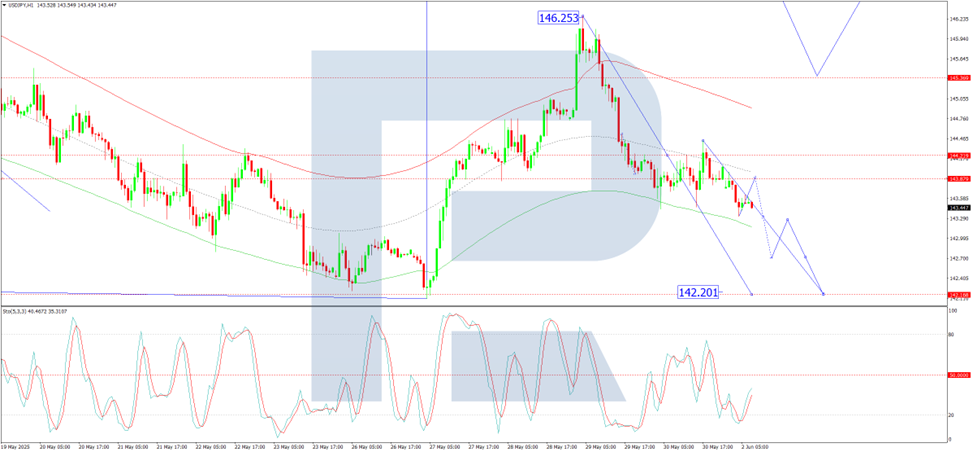

USD/JPY Declines for the Third Consecutive Day as Safe-Haven Demand Rises

The USD/JPY pair fell to 143.58, marking its third consecutive day of losses. The Japanese yen continues to gain ground as demand for safe-haven assets rises amid escalating global trade tensions.

Trade risks boost yen demand

Demand for safe-haven currencies surged after US President Donald Trump threatened to double tariffs on steel and aluminium imports to 50% from 4 June. This announcement weighed on Japanese steelmakers, with JFE Holdings and Kobe Steel potentially facing headwinds. Nippon Steel may fare better, thanks to Trump’s favourable comments regarding its planned merger with US Steel.

Meanwhile, tensions between the US and China escalated further as Beijing rejected Trump’s accusations of breaching the recently negotiated trade agreement in Geneva.

Domestic data supports the yen

Japan’s latest data revealed stronger-than-expected capital expenditure growth in Q1. Investment activity increased across both the manufacturing and non-manufacturing sectors, reinforcing domestic fundamentals amid global headwinds.

With uncertainty lingering and market preference shifting towards defensive assets, the yen continues to show resilience and may remain firm if current conditions persist.

Technical analysis of USD/JPY

On the H4 chart, USD/JPY formed a narrow consolidation range around 144.22, which the market broke below earlier today. This breakout opens the way for a continued move down towards 142.20. After reaching this level, a corrective rebound to 144.22 is possible. The MACD indicator confirms this scenario, with its signal line below zero and pointing steeply downwards, indicating strong bearish momentum.

On the H1 chart, the pair is forming the fifth wave of the current downtrend, targeting 142.20. A temporary rebound to 143.88 is expected today, followed by a continuation of the decline to 142.70, with the potential for further movement down to 142.20. The Stochastic oscillator supports this outlook, with its signal line rising above 20 towards 50, suggesting a brief corrective move before further downside.

Conclusion

The USD/JPY pair remains under pressure due to heightened trade-related risk and growing demand for safe-haven assets such as the Japanese yen. Technically, the pair is poised for further decline, with 142.20 as the next key target. While a short-lived rebound may occur, broader sentiment continues to favour yen strength as long as global trade concerns persist.

XAU/USD: Gold Price Surges on Fresh Tariff Worries, Geopolitical Factors

Gold opened with gap higher and surged in early Monday trading, lifted by escalation of war in Ukraine, President Trump’s fresh threats of doubling current tariffs on imports of steel and aluminium and victory of Eurosceptic candidate in Poland’s Presidential election.

Worsened conditions provided fresh boost to safe haven demand, with gold price advancing nearly 1.8% since opening today.

Bulls pressure key barrier at $3365 (May 23 high), break of which to signal an end of near-term corrective phase ($3365/$3245) and further brighten near-term outlook, with targets at $3400 (round figure) and $3437 (May 7 lower top) expected to come in focus.

Daily studies turned to full bullish setup, with thick rising daily cloud (which contained several attack recently) continuing to underpin, along with diverging daily Tenkan/Kijun-sen, after formation of bull-cross, with breach of the upper boundary of triangle ($3343) contributing to positive signals.

Corrective action should be anticipated in the near term as hourly studies are strongly overbought, with dips likely to shallow in current strongly bullish sentiment.

Broken triangle’s upper trendline turned to initial support, followed by supports at $3330/20 zone, which should ideally contain dips and keep fresh bulls intact.

Res: 3358; 3365; 3400; 3414.

Sup: 3343; 3330; 3322; 3311.

EUR/USD Rises to 4-Week High

As shown on the EUR/USD chart today, the euro rose to a 4-week high against the US dollar this morning.

The euro's strength relative to the US dollar is supported by traders’ expectations ahead of the ECB's interest rate decision, scheduled for Thursday at 15:15 GMT+3.

This upcoming event is notable not only because the ECB is expected to cut rates from 2.40% to 2.15% (for the seventh consecutive time), but also due to the broader context shaped by ECB President Christine Lagarde’s recent remarks on the euro’s status as a reserve currency.

At the same time, the US dollar is weakening amid growing trade concerns—on Friday, the US President Donald Trump announced plans to double tariffs on steel and aluminum to 50%. He also accused China of breaching the recent trade truce.

Technical Analysis of the EUR/USD Chart

Seven days ago, when analysing the EUR/USD chart, we:

→ observed bullish sentiment;

→ highlighted the importance of the 1.1400 resistance level;

→ suggested that bears might attempt to strike back.

Since then, the price has pulled back from the mentioned level (as indicated by the arrow), but found support at the lower boundary of the ascending channel. The current bullish momentum could push EUR/USD towards the psychological level of 1.1500 during the week ahead.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Sentiment Takes a Hit on Trump’s Latest Tariffs, Gold Rises, DAX Slips

Asian Market Wrap

Markets are on the backfoot this morning as US tariffs and trade tensions are once again in focus, denting risk appetite.

The Asian session reflected this with risk assets struggling while haven flows have returned with a bang. Gold is up as much as $60 from Friday's close, trading around $3350 an ounce at the time of writing.

Tariffs are back in the spotlight after recent legal debates about Trump-era tariffs, which are at record-high levels. Investors worry these tariffs could push the US into a recession. At the same time, uncertainties around US trade policies and talks with countries like China are adding to the tension.

On top of this, a major tax plan is being watched closely, as it could significantly increase the US deficit.

In Asia, Steel and Aluminum stocks fell sharply following President Trump's plans to raise tariffs from 50% to 250%.

Elsewhere, US Equity futures were trading lower with the S&P 500 down about 0.5% and European indices looking weak heading into the European Open.

The US Dollar index remains under pressure while the safe haven Yen rose on haven demand. Crude Oil prices were also higher overnight as OPEC+ expanded production less than expected.

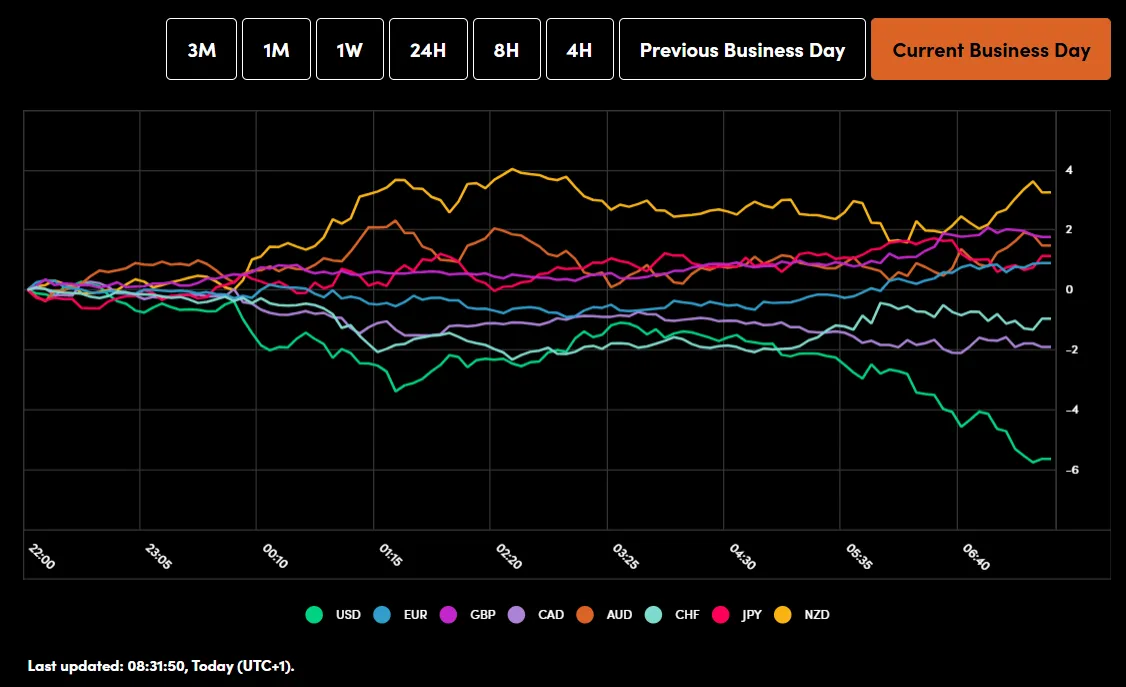

Currency Power Balance

Source: OANDA Labs

On the data front, Asia's factory activity slowed down in May due to weak demand in China and the effects of U.S. tariffs, according to private surveys. This points to a worsening outlook for the region, which used to grow quickly and heavily reliant on exports.

The European Open

European shares enjoyed a positive month of May but have opened lower this morning.

The European STOXX 600 index dropped by 0.2% early in the day. Steel companies like ArcelorMittal and Thyssenkrupp saw their shares fall by 1% and 1.1%, respectively. Tariffs affecting cars also hit automakers hard, causing their sector to drop by 1.2%.

On the data front, Swiss GDP was released a short while ago and showed the Swiss economy grew by 0.5% in the first quarter of 2025 compared to the previous quarter, which had slower growth of 0.3%. However, this growth was less than the earlier estimate of 0.7%.

Economic Data Releases and Final Thoughts

Looking at the economic calendar, and PMI data will be in focus today as a host of countries report their final numbers.

Following the drop off in Asia, it will be intriguing to see how the numbers shake up but there could be discrepancies as many companies sought to beat tariffs and upped their manufacturing activity in recent weeks.

Beyond that markets will be hoping that risk appetite is restored as the day progresses at least on the tariff front. China continues to talk diplomacy on the tariff front but did face accusations from US President Trump on Friday of not following through on its promise to scale back tariffs. The Chinese responded that they had maintained communication on trade with the United States

Developments in this regard is likely to be the major driving force for risk sentiment today and for the first half of the week.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - DAX Index

From a technical standpoint, the DAX had printed a fresh high last week around the 24387 but continues to struggle to hold convincingly above the 24000 handle.

The index is down around 0.8% at the time of writing with the 20-day MA currently providing support at the 23786 handle.

A break of this level could potentially open up further downside as risk appetite remains under pressure with support resting at 23500, 23200 and the 50 day MA around 22711.

If sentiment does improve, a move higher back toward the 24000 handle could materialize but this is dependent on developments around the US-China situation once more as well tariffs on steel and aluminum proposed by US President Donald Trump.

Source: TradingView.com (click to enlarge)

Trade safe!

UK PMI manufacturing finalized at 46.4, with tentative signs of stabilization

UK manufacturing activity remained in contraction in May, with PMI finalized at 46.4, up modestly from April’s 45.4.

The data indicate that the sector continues to face “major challenges,” according to S&P Global’s Rob Dobson, citing turbulent domestic and global conditions, trade uncertainty, subdued client confidence, and increased wage costs tied to tax changes.

Still, there are early signs that the worst of the downturn may be easing. The indexes for output and new orders have risen for two consecutive months and were stronger than the initial flash estimates, hinting at possible stabilization.

However, Dobson warned that the sector could either steady or slip further depending on how trading conditions evolve in the coming months.

Eurozone PMI manufacturing finalized at 49.4, recovery progressing

Eurozone PMI manufacturing was finalized at 49.4 in May, up from April’s 49.0 and marking the highest level in 33 months.

Production increased across all four major economies: Germany, France, Italy, and Spain, supporting economist Cyrus de la Rubia's view that the recovery is gaining traction.

De la Rubia also noted that output has now risen for three straight months, reinforcing the view that the recovery is gaining traction. Historical data suggests a 72% chance of another output increase next month.

Falling input costs, driven by lower energy prices, have enabled manufacturers to cut selling prices again, offering the ECB more flexibility for its expected interest rate cuts.

However, the outlook remains clouded by external risks, particularly the threat of higher US tariffs on EU goods. Any escalation in transatlantic trade tensions could quickly derail the fragile rebound.

Swiss GDP grew 0.5% in Q1, pharma exports surge on tariff frontloading

Switzerland's GDP expanded by 0.5% qoq in Q1, beating market expectations of 0.4% qoq. When adjusted for the impact of major sporting events, GDP growth came in even stronger at 0.8% qoq. The State Secretariat for Economic Affairs noted that the services sector posted broad-based gains and domestic demand remained firm, contributing to the overall solid performance.

A standout was the chemical and pharmaceutical sector, which surged 7.5% in the quarter, driven by a sharp rise in pharmaceutical exports. This lifted overall manufacturing output by 2.1% and goods exports by 5.0%. Notably, exports to the US jumped significantly, suggesting possible front-loading in anticipation of evolving US trade policy.