Sample Category Title

Gold and WTI Crude Oil Prices Could Gain Bullish Pace

Gold started a fresh increase above the $3,300 resistance level. WTI Crude Oil is gaining bullish momentum and might even test $62.75.

Important Takeaways for Gold and WTI Crude Oil Price Analysis Today

- Gold price started a steady increase from the $3,250 zone against the US Dollar.

- A connecting bearish trend line is forming with resistance at $3,318 on the hourly chart of gold at FXOpen.

- WTI Crude Oil climbed above the $60.50 and $60.80 resistance levels.

- There was a break above a key bearish trend line with resistance at $60.80 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price found support near the $3,250 zone, formed a base, and started a fresh increase above the $3,280 level.

The bulls cleared the $3,300 zone and the 50-hour simple moving average. There was also a move above the 61.8% Fib retracement level of the downward move from the $3,331 swing high to the $3,271 low. The RSI is now above 50 and the price could aim for more gains.

Immediate resistance is near the 76.4% Fib retracement level of the downward move from the $3,331 swing high to the $3,271 low at $3,318. There is also a connecting bearish trend line forming with resistance at $3,318.

The next major resistance is near the $3,330 level. An upside break above the $3,330 resistance could send Gold price toward $3,382. Any more gains may perhaps set the pace for an increase toward the $3,400 level.

Initial support on the downside is near the $3,300 zone. If there is a downside break below the $3,300 support, the price might decline further.

In the stated case, the price might drop toward the $3,270 support. The next major support sits at $3,250. Any more losses might send the price toward the $3,220 level.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a fresh upward move from $59.45 against the US Dollar. The price gained bullish momentum after it broke the $60.00 resistance.

The bulls pushed the price above the 50% Fib retracement level of the downward move from the $62.76 swing high to the $59.45 low. The price even climbed above the 50-hour simple moving average. Besides, there was a break above a key bearish trend line with resistance at $60.80.

It tested the $61.50 resistance zone and the 61.8% Fib retracement level of the downward move from the $62.76 swing high to the $59.45 low.

The RSI is now near the 50 level and the price could aim for more gains. If the price climbs higher again, it could face resistance near $62.00. The next major resistance is near the $62.75 level. Any more gains might send the price toward the $63.45 level or even $65.00.

Conversely, the price might correct gains and test the $60.80 support level. The next major support on the WTI Crude Oil chart is near the $59.45 zone, below which the price could test the $58.00 zone.

If there is a downside break, the price might decline toward $56.50. Any more losses may perhaps open the doors for a move toward the $55.50 support zone.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Trade-Related Uncertainty Continues Dominating Market Talk This Morning

Markets

‘Trade noise’ is moving again to the fore, further complicating any eco-driven market reaction function. Soft US data (US Q1 GDP was upwardly revised to -0.2% Q/Qa, but with a setback in private consumption and a soft core PCE deflator; claims were also higher than expected) triggered a setback in US yields on Thursday. April US PCE deflators, remained benign despite uncertainty on trade/tariffs and confirmed this yield decline/steepening on Friday. US yield changes ranged between 4.1 bps (2-y) and +1.4 bps (30-y). After a decline on Thursday, German yields ceded less than 1bp across the curve on Friday. German May inflation was close to expectations (0.2% M/M and 2.1 Y/Y). Aside from the data, headlines on trade showed that uncertainty on the topic is here to stay. A federal US court of appeal paused an earlier court ruling assessing the Liberation Day tariffs as being illegal. Still, the essence on the issue remains subject to further court decisions. On Friday, US president Trump openly accused China off violating the Geneva trade truce reached earlier last month. Comments from the US administration indicated that China exports of rare earths was a source of conflict. Uncertainty caused some investor caution going into the weekend (Nasdaq -0.32%). The dollar basically closed the session little changed (DXY 99.33, EUR/USD 1.135).

Trade-related uncertainty continues dominating the market talk this morning. US president Trump announced to raise the import duties on the import of steel and aluminum from 25% to 50% staring June 4. Chinese officials equally accused the US of violating the consensus reached in Geneva, warning they might take additional action to defend their interests. The flaring up of trade-related tensions causes markets to start the week with a risk-off bias. (Nikkei -1.3%, S&P 500 future -0.5%). The dollar is losing ground against the likes of the yen (USD/JPY 143.4) and the euro (EUR/USD 1.1375). For now, the uncertainty again hardly helps US Treasuries, with yields even rising marginally this morning. Trade uncertainty probably will continue to set the tone for trading today though the US manufacturing ISM is worth keeping an eye on. Later this week, we have US JOTS job openings (tomorrow), the ADP report and services ISM (Wednesday) and the payrolls (Friday). A big negative labour market surprise probably remains necessary for the Fed (and markets) to change their assessment on a cautious Fed approach also in H2. In Europe, May CPI inflation tomorrow (expected headline 2% and core 2.5%) is the final input ahead of Thursday’s ECB policy meeting. For now, we see stocks and the dollar as most vulnerable to the trade noise. The impact, especially on US interest markets is far less straightforward.

News & Views

The eight OPEC+ countries that in 2023 announced additional voluntary production cuts, will continue returning to normal output levels. In December of last year, they agreed to start a gradual and flexible return of the 2.2mn b/d of production cuts. They started the process with a larger than expected 320k b/d in April, followed by 411k b/d increases in May and June. Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria and Oman on Saturday agreed on a similar output hike for July (411k b/d) on Saturday. The gradual increases may be paused or reversed subject to evolving market conditions, allowing for flexibility to continue to support oil market stability. Oil prices trade higher this morning (Brent > $64/b) as markets were wrongfooted by earlier rumours that the eight OPEC+ countries could speed up the reversal of their additional cuts with an output hike of up to 600k b/d in for July.

Polish PM Tusk’s pro-European candidate Trzaskowski narrowly lost the second round of Polish presidential elections. The Warsaw mayor lost against the candidate of the previous, nationalist, Law and Justice party (PiS). Nawrocki won 50.9% of the vote against 49.1% for Trzaskowski. The outcome deals a blow to Tusk’s reform agenda which has been partly held hostage by a presidential veto since taking office in 2023. The previous Polish president, Duda, another PiS nominee, blocked amongst others the planned judicial overhaul. The Polish zloty loses ground this morning with EUR/PLN jumping from 4.24 to 4.27. A test of EUR/PLN 4.30 is in the cards..

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.24; (P) 193.95; (R1) 194.51; More...

Intraday bias in GBP/JPY remains neutral and more consolidations could be seen below 196.38. Further rise is in favor as long as 191.86 support holds. Firm break of 196.38 will resume whole rally from 184.35. However, firm break of 191.86 will indicate near term reversal and turn bias back to the downside.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

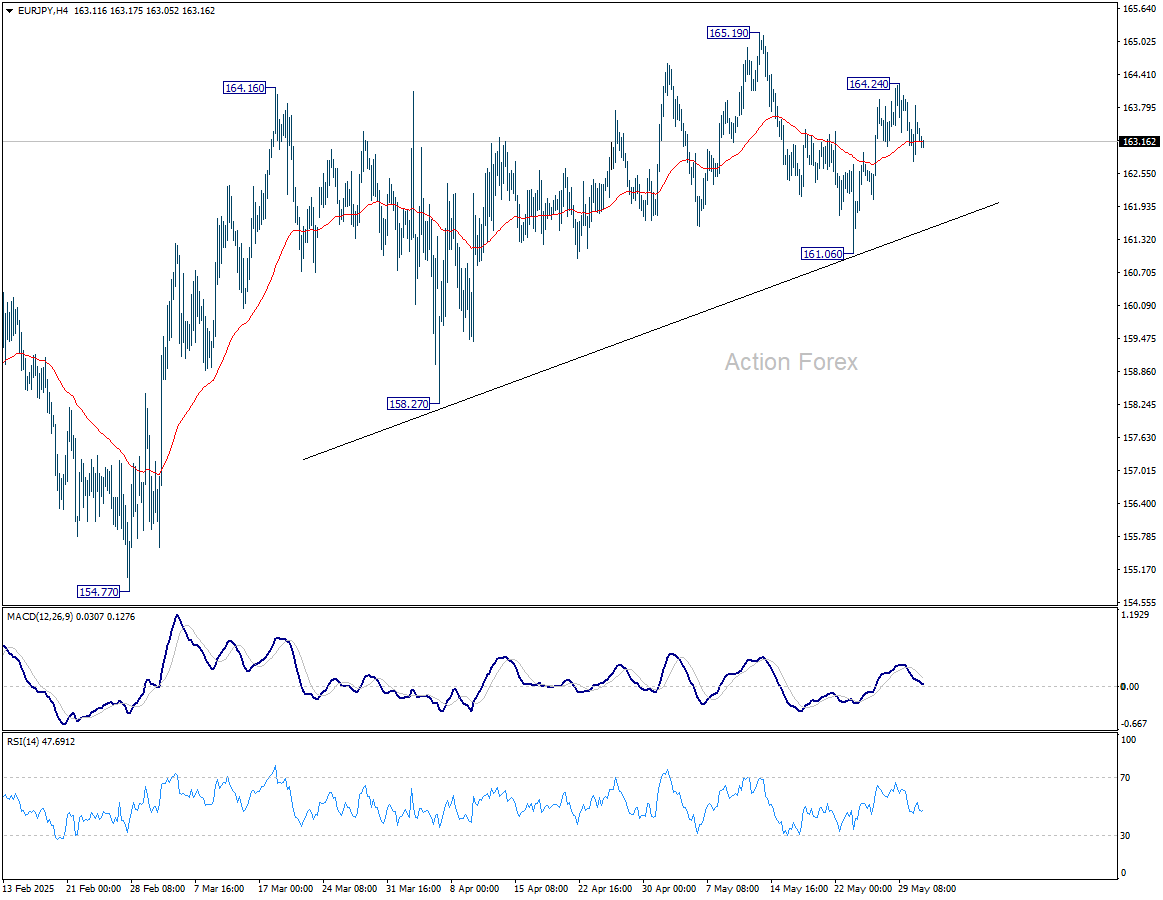

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.83; (P) 163.45; (R1) 164.09; More...

Intraday bias in EUR/JPY stays neutral. On the upside, above 164.24 will bring retest of 165.19 resistance first. Firm break there will resume while rise from 154.77 to 166.67 resistance. On the downside, however, break of 161.06 will resume the decline from 165.19 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

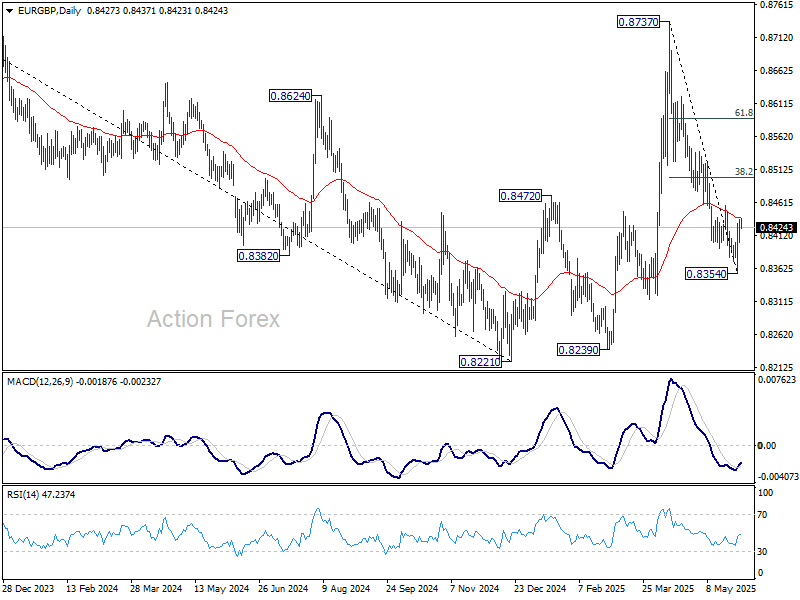

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8412; (P) 0.8425; (R1) 0.8446; More...

Intraday bias in EUR/GBP stays mildly on the upside at this point. Rebound from 0.8354 short term bottom should continue to 0.8458 resistance, and then 38.2% retracement of 0.8737 to 0.8354 at 0.8500. Nevertheless, break of 0.8354 will resume the decline from 0.8737 instead.

In the bigger picture, price actions from 0.8221 medium term bottom are merely forming a corrective pattern. There is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

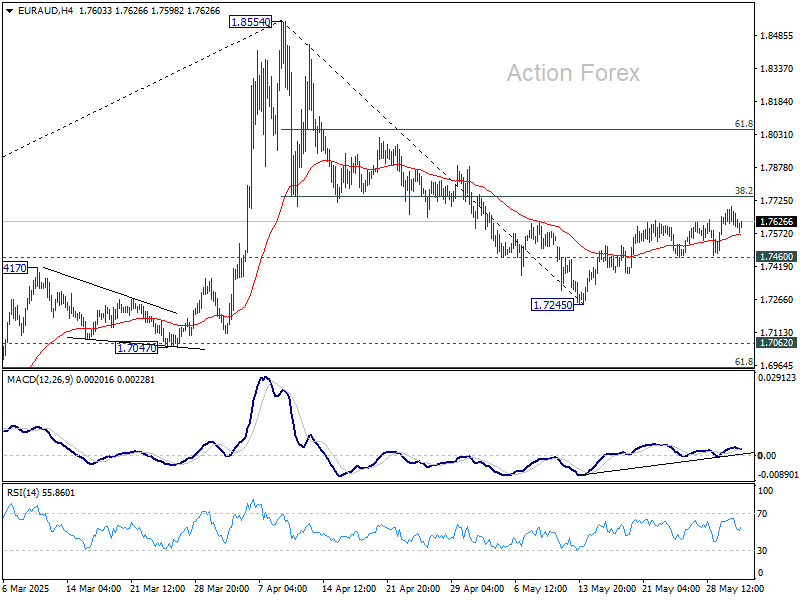

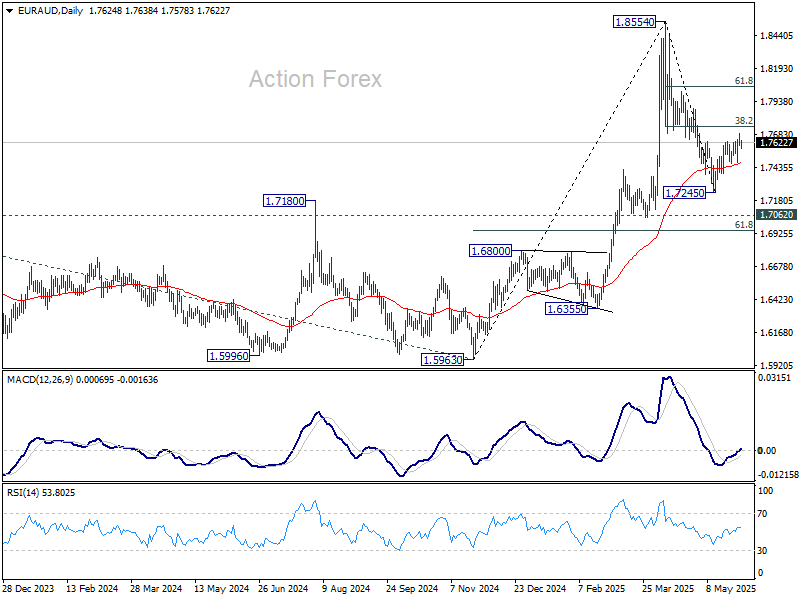

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7603; (P) 1.7651; (R1) 1.7690; More...

Intraday bias in EUR/AUD remains mildly on the upside at this point. Firm break of 38.2% retracement of 1.8554 to 1.7245 at 1.7745 will solidify the case that fall from 1.8554 has completed as a correction. Next target is 61.8% retracement at 1.8054. On the downside, however, break of 1.7460 support will bring retest of 1.7245 instead.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 is expected after the whole corrective pattern from there completes. However, sustained break of 1.7062 will bring deeper fall back to 1.5963 support.

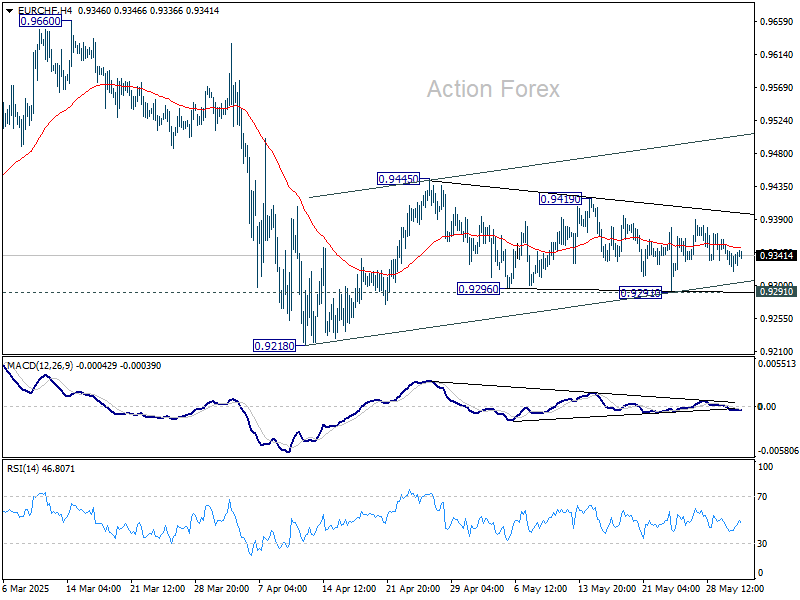

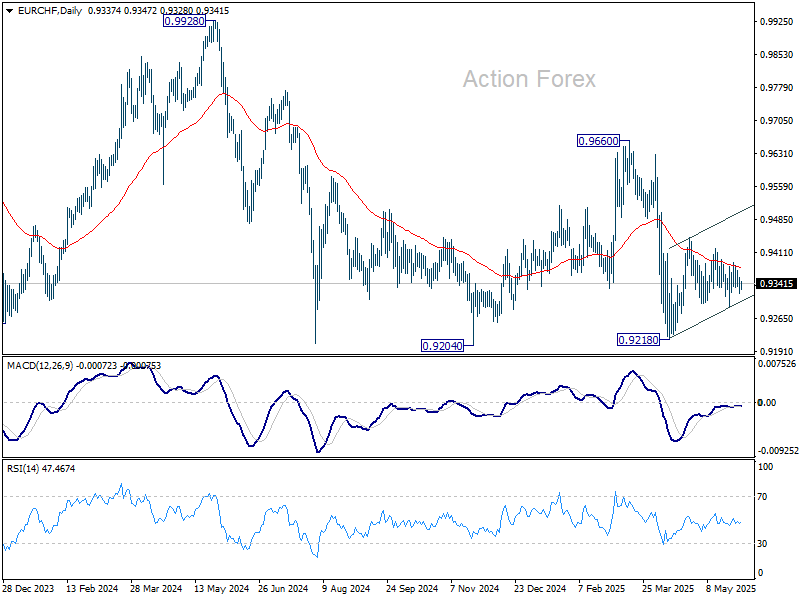

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9318; (P) 0.9339; (R1) 0.9356; More....

Intraday bias in EUR/CHF stays neutral as sideway trading continues. Rise from 0.9218 might continue, either as a correction to fall from 0.9660, or the third leg of the pattern from 0.9204. On the upside, above 0.9419 will target 0.9445 resistance and above. Nevertheless, on the downside, firm break of 0.9291 will bring retest of 0.9218 low.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9527) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

Rising Trade, Geopolitical Tensions Weigh on Risk Appetite

So we’re in June. The month of May ended with a whopping 6% advance for the S&P500, defying the ‘Sell in May and Go Away’ adage on Wall Street that points to a generally unfavourable seasonal trend for the month. But the S&P500’s performance is hiding a few issues on the US debt and global trade fronts. The past few weeks were marked by less-than-ideal developments for the US, despite the resilience of the bulls.

First, the US debt was downgraded by Moody’s two weeks ago. Combined with Trump’s ‘beautiful’ fiscal package ahead, this has raised worries about the sustainability of US debt. Add the relatively high interest rates to the mix and the outlook indeed looks scary. The US 30-year yield spiked past the 5% mark before easing back below that level in May. Elsewhere, the selloff in Japanese long-maturity debt also made headlines, hinting at falling confidence in some Western governments’ ability to finance unsustainable budgets. Europe, however, is benefiting from the outflows, as European governments have been stricter in containing debt levels. Even with prospects of increased spending, German debt looks like a go-to for investors who want to diversify holdings within the sovereign bond space. Others, of course, prefer gold and Bitcoin.

Trade tensions re-escalate

Trade tensions are heating up again. Not only does Donald Trump seem unfazed by growing questions around the legitimacy of his tariffs, but he also accused China of violating the trade truce they signed in Geneva earlier this month. The US spent the week cancelling Chinese student visas and imposing fresh restrictions on chip designers doing business in China. China responded, accusing the US of imposing ‘discriminatory restrictions.’

Cherry on top, the US announced an increase in tariffs on steel and aluminium imports to 50%, from the 25% previously in place — perhaps to help facilitate the recent deal between the US and Nippon Steel. Iron ore futures tanked 3% in Singapore last week and remain under pressure this morning. Meanwhile, WisdomTree’s industrial metals ETF has been unable to reverse its downtrend from the May trade optimism and is diving again on the back of rising global trade tensions.

The renewed tariffs on steel and aluminium will likely throw some cold water on negotiations between the EU and the US. The EU’s metal exports to the US represent around 1% of its total exports, but the move could still have severe consequences for Europe’s already struggling industrial sector. An affair to follow...

In FX

The US dollar opens the week under pressure. On the data front, Friday brought some good news for the US — and for Federal Reserve (Fed) watchers. The core PCE index – the Fed’s favourite gauge of inflation – came in line with expectations, while the headline PCE printed a softer-than-expected figure. That helped boost dovish Fed expectations and initially supported the dollar, but the greenback starts the week under pressure again, weighed by re-escalating trade tensions and US debt concerns. Asset managers remain heavily short the US dollar, and consensus still points to further losses for the greenback against most G7 majors.

In that respect, the EURUSD looks better bid in the early hours of the trading week, as a set of flash CPI figures from major eurozone economies came in soft enough to suggest inflation may be easing toward the European Central Bank’s (ECB) 2% target in May. The aggregate figure is due tomorrow, but ECB doves are already out and betting that the bank will cut interest rates by 25bp when it meets this Thursday.

Speaking of rate cuts, the Bank of Canada (BoC) is also expected to cut rates by 25bp on Wednesday to offset the economic damages from the heated trade war with the US and the impact of lower oil prices.

Oil jumps

Oil prices are up this morning on the back of rising tensions between Russia and Ukraine, as Ukraine launched drone attacks deep inside Russian territory. That is counterbalancing the weekend announcement of an additional 411,000 barrels per day that OPEC will bring to the market starting in July. But that announcement was expected and widely priced in. So the kneejerk reaction to that number is mildly positive — if anything — on relief that the number matched earlier guidance and wasn’t higher.

Still, price rallies driven by geopolitical tensions tend to be short-lived in the absence of significant escalation, and may serve as interesting top-selling opportunities for traders playing the higher-supply/lower-demand narrative of the moment. As such, a rise above the 50-DMA, which stands near $62.90pb, could offer interesting top-selling levels. The major resistance to the YTD decline stands near $65.35pb — the key 38.2% Fibonacci retracement.

Mood is so, so

Chinese and Japanese markets are down, while Hong Kong’s Hang Seng index fell nearly 2% on news that New World Development — a property developer — slid further into distress amid delayed interest payments on some bonds, reminding investors of China’s ongoing property crisis lurking beneath the AI shine.

Elsewhere, the ASX 200 is under pressure. Miners of industrial metals are struggling, while gold miners are supported by rising geopolitical and trade tensions. European and US futures point to a bearish start to the new month, with the exception of FTSE futures, which are slightly in the positive at the time of writing, backed by an early rally in oil prices.

This week, we’ll be watching PMI numbers from around the world, the US jobs data, and the latest earnings from CrowdStrike and Broadcom — besides the trade headlines, which will probably dominate overall sentiment and continue to set the global tone.

A Week of Important Data Releases Amid Ongoing Tariff Uncertainty

In focus today

In the euro area, focus turns to the final manufacturing PMI data for May. Manufacturing rose more than expected to 49.4 in the flash release showing limited signs of trade uncertainty.

From the US, ISM manufacturing survey for May is due for release in the afternoon. Regional Fed manufacturing indices and the flash PMI released earlier pointed towards a modest rebound, which could be partially explained by renewed front-loading after the US-China trade deal. Federal Reserve's Powell, Goolsbee and Logan are scheduled to give speeches in the evening.

Overnight, China releases PMI manufacturing from Caixin, the private version. After dropping in April on the back of a big drop in export orders, we look for a rebound in May following the US-China deal on a 90-day truce in the trade war. This should lead to a lift in export orders and the overall PMI level.

In Sweden, manufacturing PMIs are due today. Swedish manufacturing PMIs have stayed above 50 since mid-2024 and April marked its fourth straight monthly increase. We expect the main index to remain in expansionary territory, albeit sub-indices such as prices paid are likely to be even more interesting as markets are concerned given the upcoming Riksbank meeting and the fact that inflation remains above target.

After the sharp drop in Norwegian PMI in April, we expect a solid rebound as trade worries have eased significantly.

Throughout the rest of the week there are several interesting data releases and meetings to look forward to. Most important, we look out for the May euro area inflation and the April US JOLTS Job Openings report on Tuesday. On Wednesday, the Bank of Canada will publish a statement on the rate decision, while the ECB board meets on Thursday, where we expect a 25bp cut in the policy rate to 2.0%. We will also look out for the release of the Chinese services PMI from Caixin on Thursday. Friday's releases include May US non-farm payrolls and a revision of Q1 euro area GDP.

Economic and market news

What happened since Wednesday

In the global trade war, several big stories have unfolded since our latest Danske Morning Mail. On Friday evening, Trump announced a doubling of the earlier tariffs on steel and aluminium to 50% on 4 June. The announcement came just a few hours after he accused China of violating an agreement with the US on Truth Social. Last week, the US Trade Court ruled against tariffs imposed with the authority of International Economic Emergency Powers Act (IEEPA), but the product-specific tariffs imposed under Section 232 authority were not part of the ruling. As such, we could see more product-specific tariffs replacing the current country-specific measures, if the US Supreme Court ends up confirming the Trade Court ruling over summer. These legal challenges have introduced considerable uncertainty into ongoing trade negotiations, with US trading partners now reassessing the most likely outcomes.

In the US, the tariff uncertainty continues to distort US macro data. University of Michigan's May consumer sentiment rebounded, and inflation expectations declined in the final release as these also contained responses collected after the US-China trade deal. The Atlanta Fed's 'nowcast' model for Q2 GDP growth rebounded sharply to 3.8% (from 2.2%), but underlying growth remains weaker. The uptick was purely driven by the preliminary April trade balance data showing a rapid narrowing in US trade deficit after the Q1 import front-loading ended around the 'Liberation Day'.

Core PCE inflation landed close to expectations in April. Real consumption slowed down to just 0.1% m/m SA (from +0.7%) despite a decent uptick in personal income. As such, the savings rate ticked up to 4.9% (from 3.9%), which is the highest since May 2024.

In Sweden, final Q1 GDP growth surprised to the downside, coming in at -0.2% q/q (cons. +0.1% q/q), amid a decline in fixed investments and household spending, marking the first contraction in GDP since Q4 2023. Conversely, April saw quite strong retail sales, a +0.9% m/m growth led by non-durables rising by 1.3%. Over the most recent three-month period (Feb-April) we have seen retail sales volumes growing by 1.1% compared to previous 3m-window (Nov-Jan), highlighting a discrepancy between household sentiment (c.f the NIER ETS release) and spending behaviour.

In Norway, retail sales increased +0.7 % m/m in April, taking the 3M/3M average growth to 1.5 %. Hence, the decent upward trend seen since last autumn continued into Q2. High real wage growth, fading headwinds from higher mortgage rates, strong employment growth and a normalisation of the saving ratio are all contributing to this trend. Furthermore, unemployment (SA) rose from 2.0% to 2.1% in May, marking the first sign of weakness in the labour market since last August. That said, the number of unfilled vacancies is still elevated, signalling continued strong demand for labour.

In the euro area, Spanish inflation in May came in slightly lower than expected (+1.9% y/y, cons. 2.0% y/y), while Italian inflation came in as expected, also at +1.9% y/y. Despite German May inflation coming in at bit higher than expected at 2.1% y/y in May, we still expect euro area HICP in May to decline to 2.0% y/y when it releases tomorrow.

In China, non-manufacturing PMI from NBS surprised to the downside, declining to 50.3 in May (prior 50.4, cons. 50.6). The latest reading underscored concerns over the impact of rising US tariffs on China's service sector, despite a temporary trade war pause between Beijing and Washington. The manufacturing PMI came in as expected, increasing to 49.5 in May (prior 49.0).

In Oil, OPEC+, announced a production increase of 411,000 barrels per day for July, aiming to regain market share and address over-production by members like Iraq and Kazakhstan.

Equities: Investors locked in solid gains last week (MSCI World +1.6%). The strong performance abated over the course of the week, however. Defensives outperformed cyclicals on Thursday and Friday, while Nordics were closed for holidays. Drivers were many; Nvidia earnings, upset tariff tweets and court rulings whiplashed investors. VIX worth noting in this regard, which, despite all the tariff noise, remained stubbornly below 20 over the last week, in a sign that investors put less emphasis on the Trump trade. US and European futures are half a percent lower this morning, while Asian markets are selling off 1-2% following Trump tweets over weekend.

FI and FX: Tariff uncertainty is on the rise again following Trump's Friday evening announcement of a doubling of the steel and aluminium tariffs, to 50% starting 4 June. EUR/USD is back above 1.1350 and US yields are ticking higher, all whilst equity futures are well in red. The Scandies are up for some interesting weeks to come, and EUR/NOK has found its way back to 11.60 whilst NOK/SEK has reversed down to 0.94. Nationalist candidate Karol Nawrocki, backed by Donald Trump, won the polish presidential election, a heavy blow against PM Tusk's ambition for closer ties between Poland and EU. The result is likely to weigh on the Zloty, with EUR/PLN potentially moving to 4.30 once again.

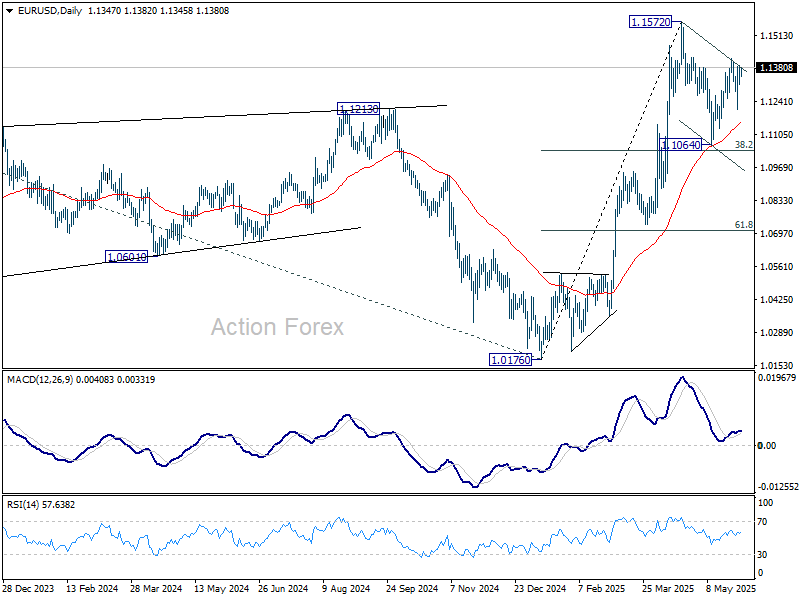

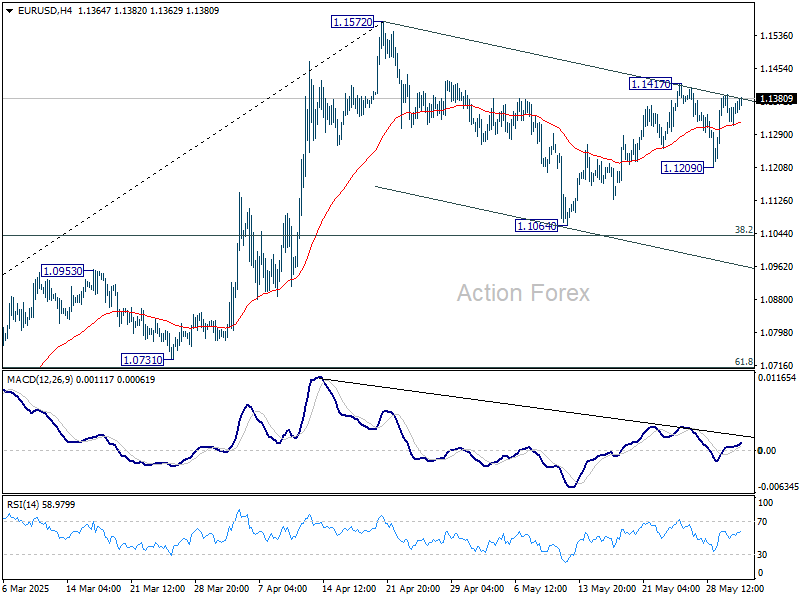

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1310; (P) 1.1350; (R1) 1.1387; More...

Intraday bias in EUR/USD remains neutral for the moment. Price actions from 1.1572 are seen as a corrective pattern to rally from 1.0176, which might still be extending. On the upside, above 1.1417 will bring retest of 1.1572 first. On the downside, below 1.1209 will target 1.1064 again. But overall, rise from 1.0176 is expected to resume after the correction completes at a later stage.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.