Sample Category Title

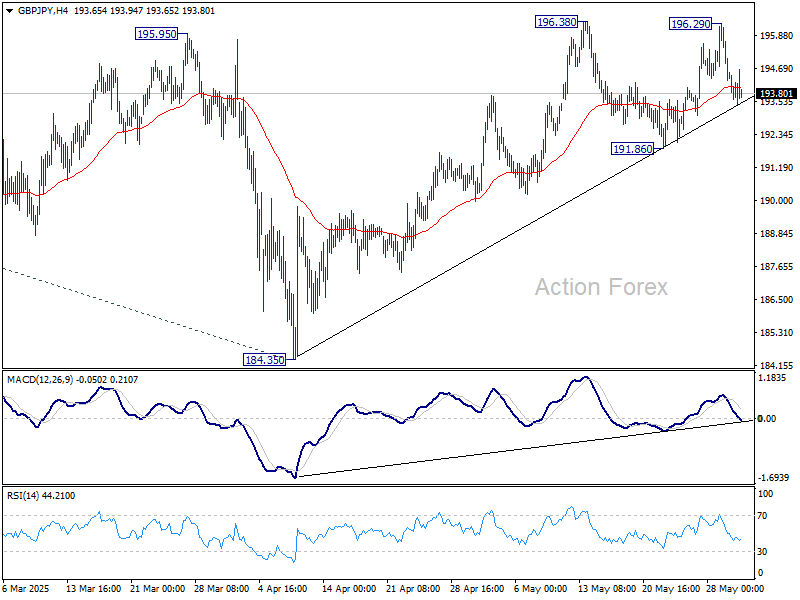

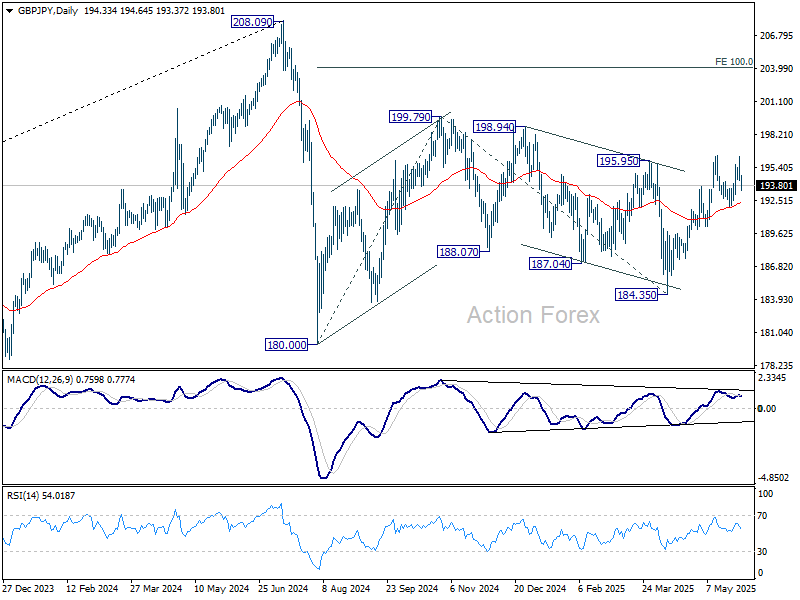

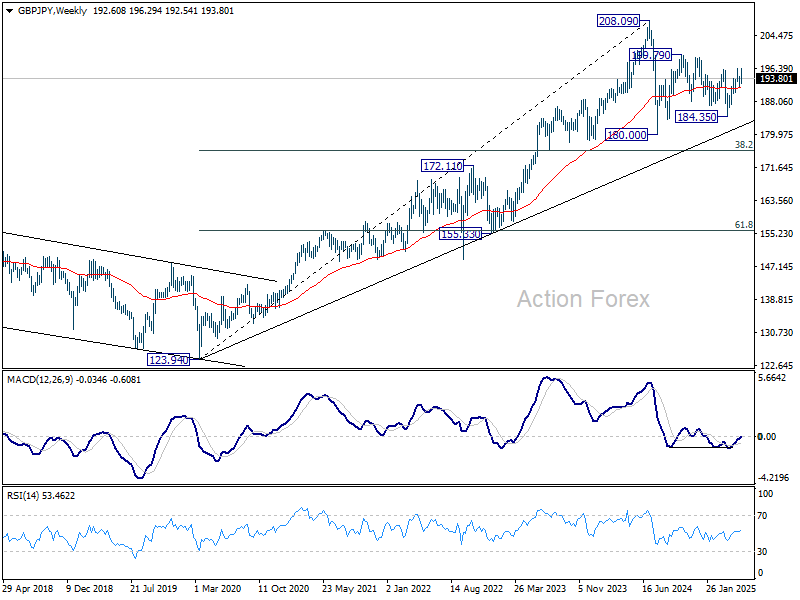

GBP/JPY Weekly Outlook

GBP/JPY rebounded notably last week but failed to break through 196.38 resistance. Initial bias remains neutral this week first. Further rise is in favor as long as 191.86 support holds. Firm break of 196.38 will resume whole rally from 184.35. However, firm break of 191.86 will indicate near term reversal and turn bias back to the downside.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 175.85).

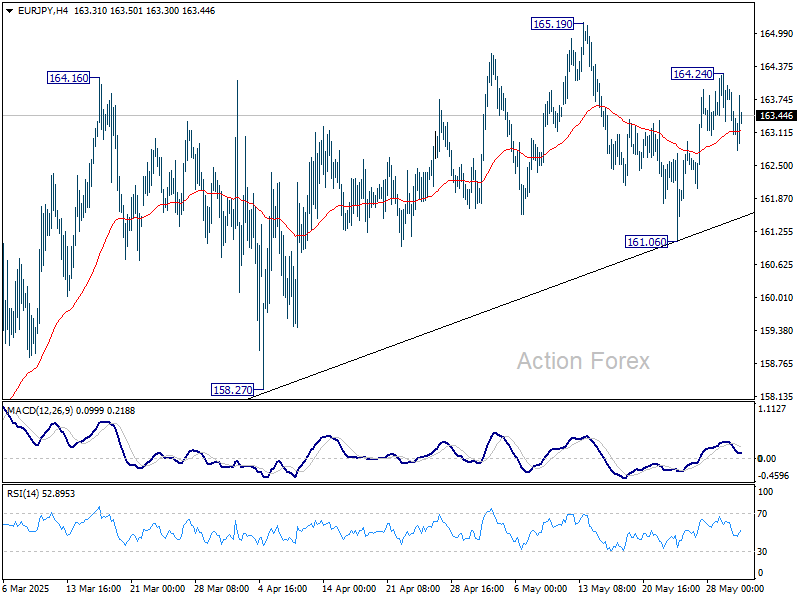

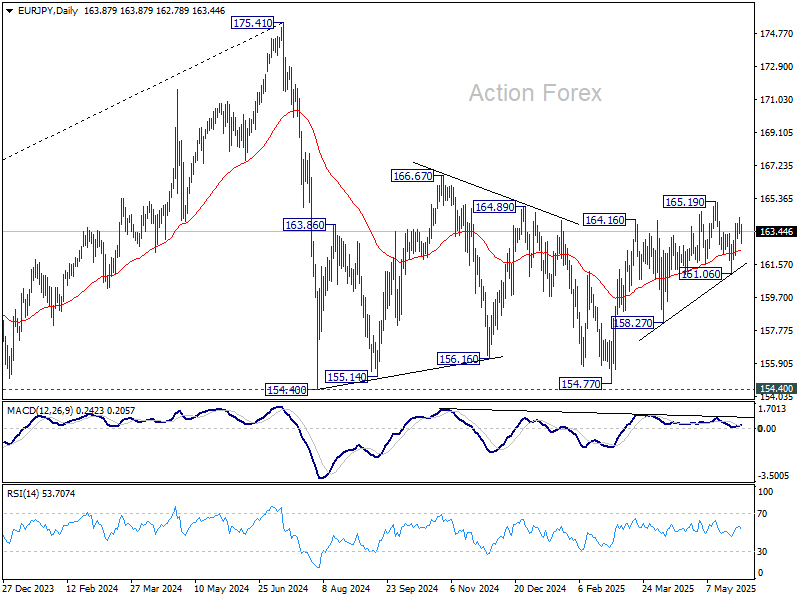

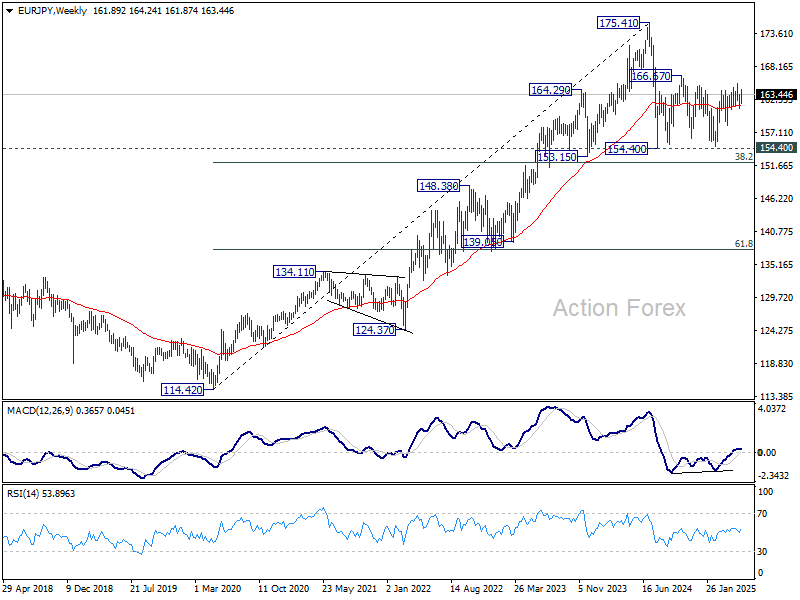

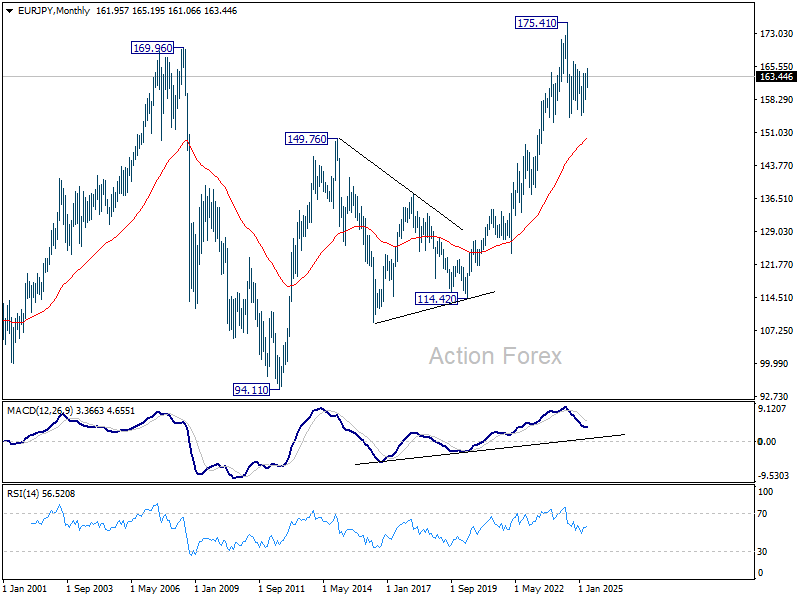

EUR/JPY Weekly Outlook

EUR/JPY extended the rebound from 161.06 last week but failed to break through 165.19 resistance. Initial bias remains neutral this week first. On the upside, above 164.24 will bring retest of 165.19 resistance first. Firm break there will resume while rise from 154.77 to 166.67 resistance. On the downside, however, break of 161.06 will resume the decline from 165.19 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 149.91).

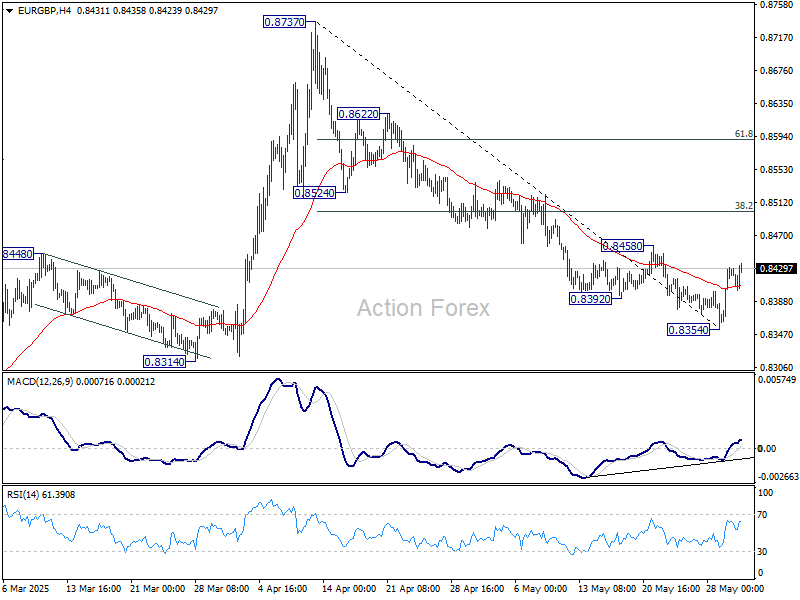

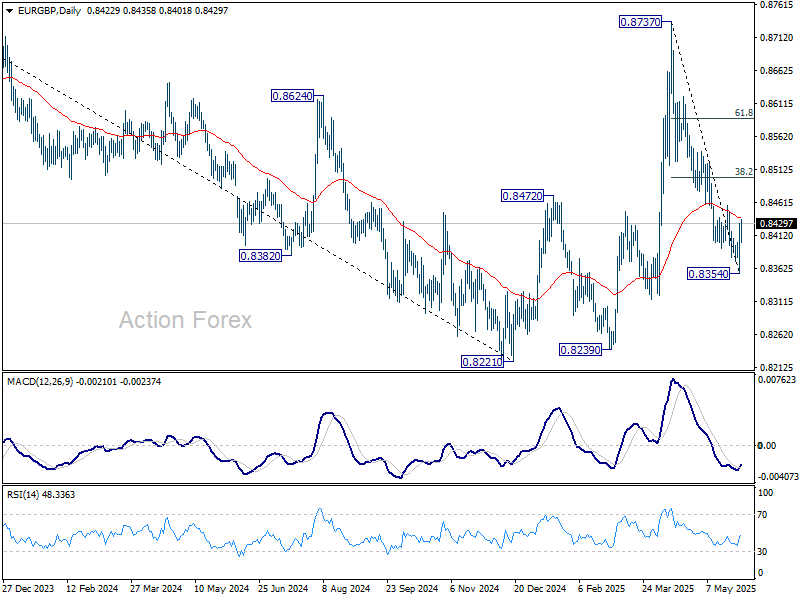

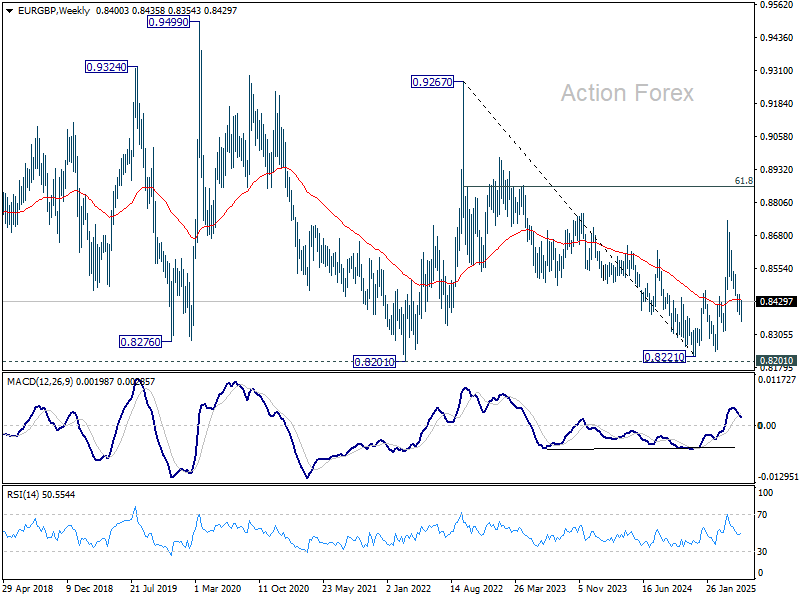

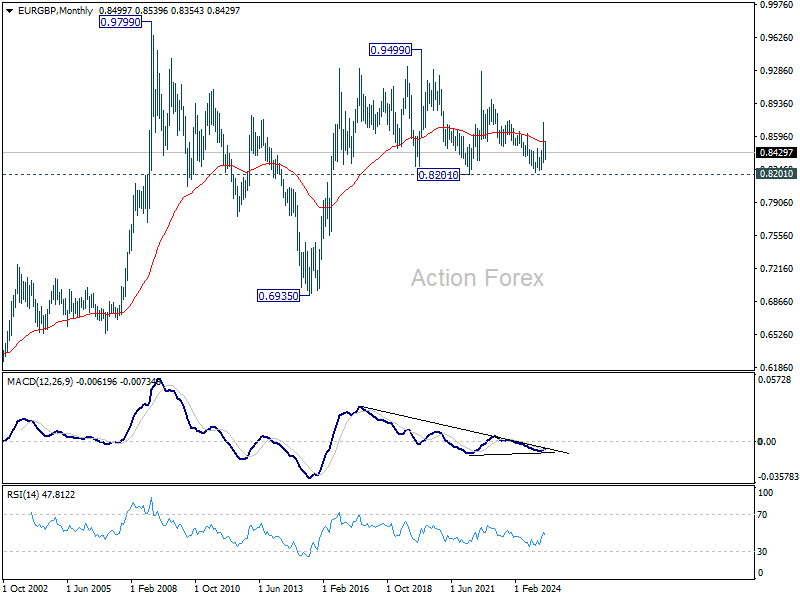

EUR/GBP Weekly Outlook

EUR/GBP's rebounded after dipping to 0.8354 last week. The development suggests that a short term bottom was formed, on bullish convergence condition in 4H MACD. Initial bias is mildly on the upside this week for 0.8458 resistance, and then 38.2% retracement of 0.8737 to 0.8354 at 0.8500. Nevertheless, break of 0.8354 will resume the decline from 0.8737 instead.

In the bigger picture, price actions from 0.8221 medium term bottom are merely forming a corrective pattern. There is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

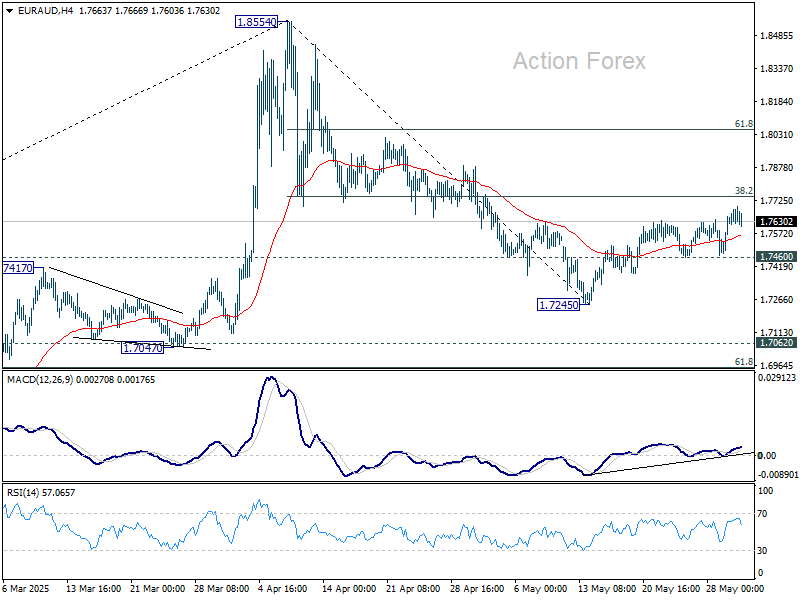

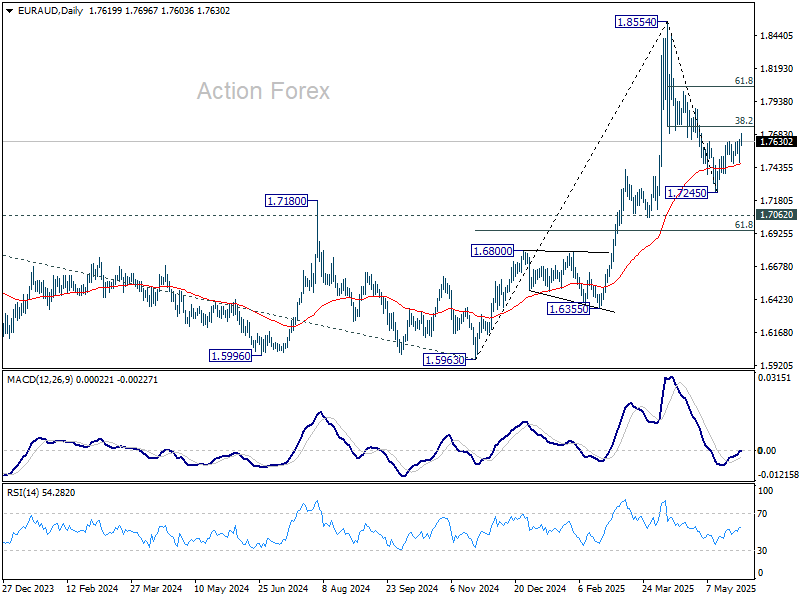

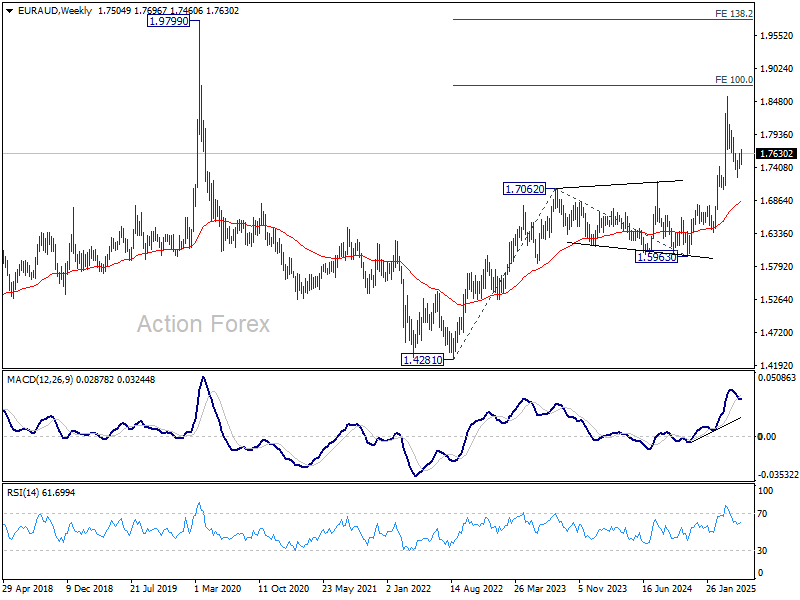

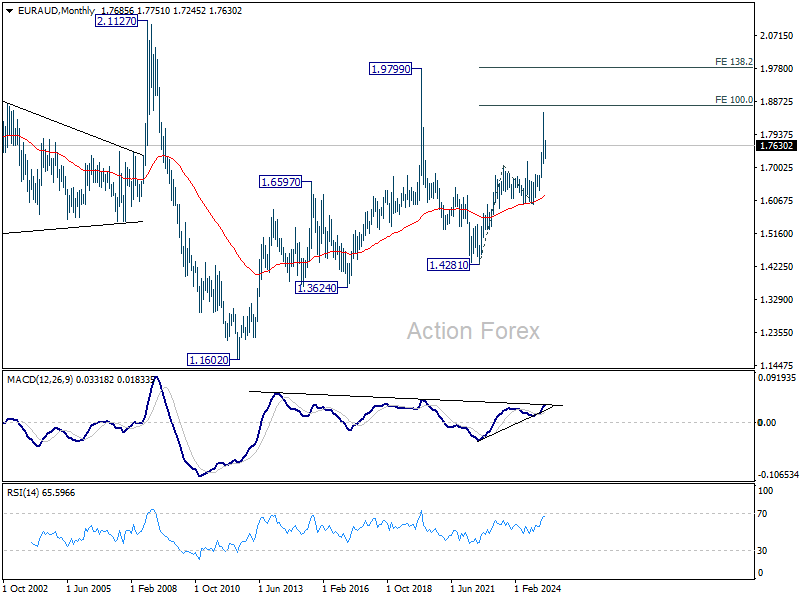

EUR/AUD Weekly Outlook

EUR/AUD's rebound from 1.7245 resumed last week and the development suggests that fall from 1.8554 might have completed as a correction. Initial bias stays on the upside this week for 38.2% retracement of 1.8554 to 1.7245 at 1.7745. Firm break there will solidify this bullish case and target 61.8% retracement at 1.8054. On the downside, however, break of 1.7460 support will bring retest of 1.7245 instead.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 is expected after the whole corrective pattern from there completes. However, sustained break of 1.7062 will bring deeper fall back to 1.5963 support.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6240) holds, this second leg could still extend higher. Break of 1.8554 will target 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. However, firm break of 1.8744 projection level with strong momentum will argue that it's indeed resuming the up trend from 1.1602 (2012 low).

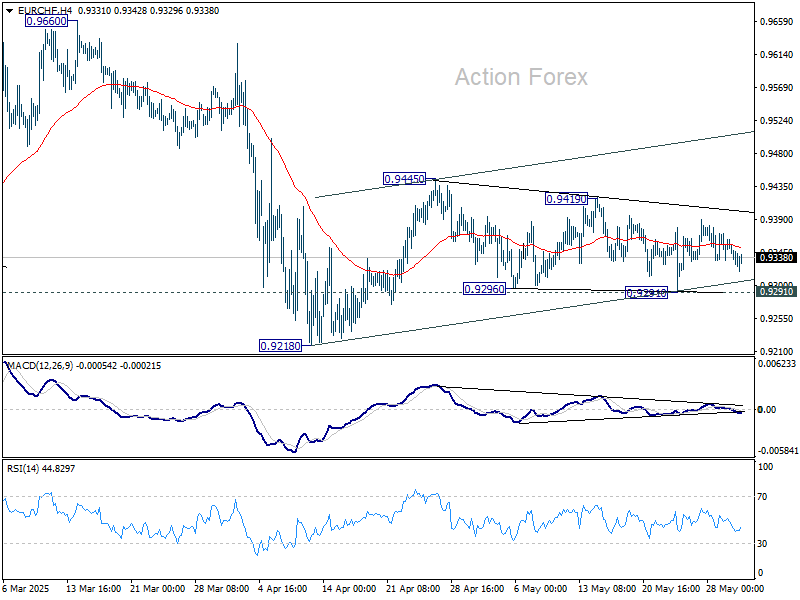

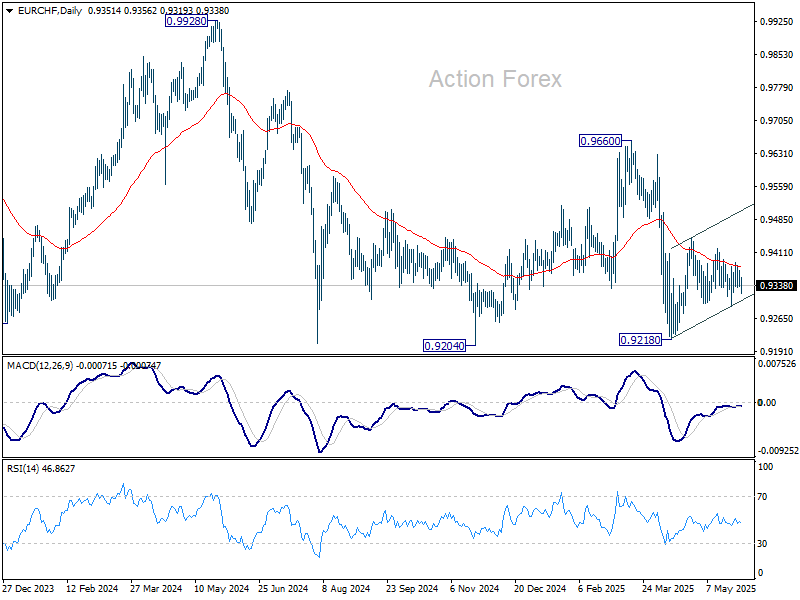

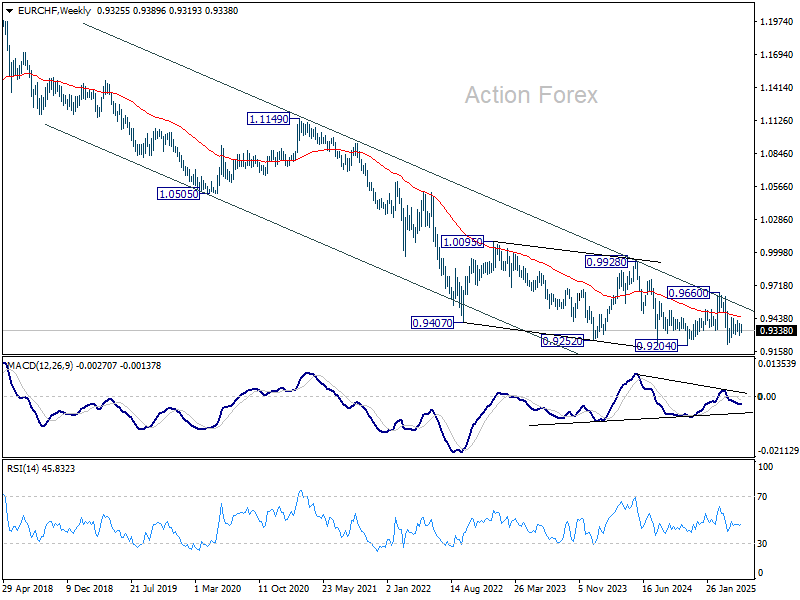

EUR/CHF Weekly Outlook

EUR/CHF continued to gyrate inside established range last week and outlook is unchanged. Initial bias remains neutral this week first. Rise from 0.9218 might continue, either as a correction to fall from 0.9660, or the third leg of the pattern from 0.9204. On the upside, above 0.9419 will target 0.9445 resistance and above. Nevertheless, on the downside, firm break of 0.9291 will bring retest of 0.9218 low.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9527) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

In the long term picture, overall long term down trend is still in force in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9919) holds.

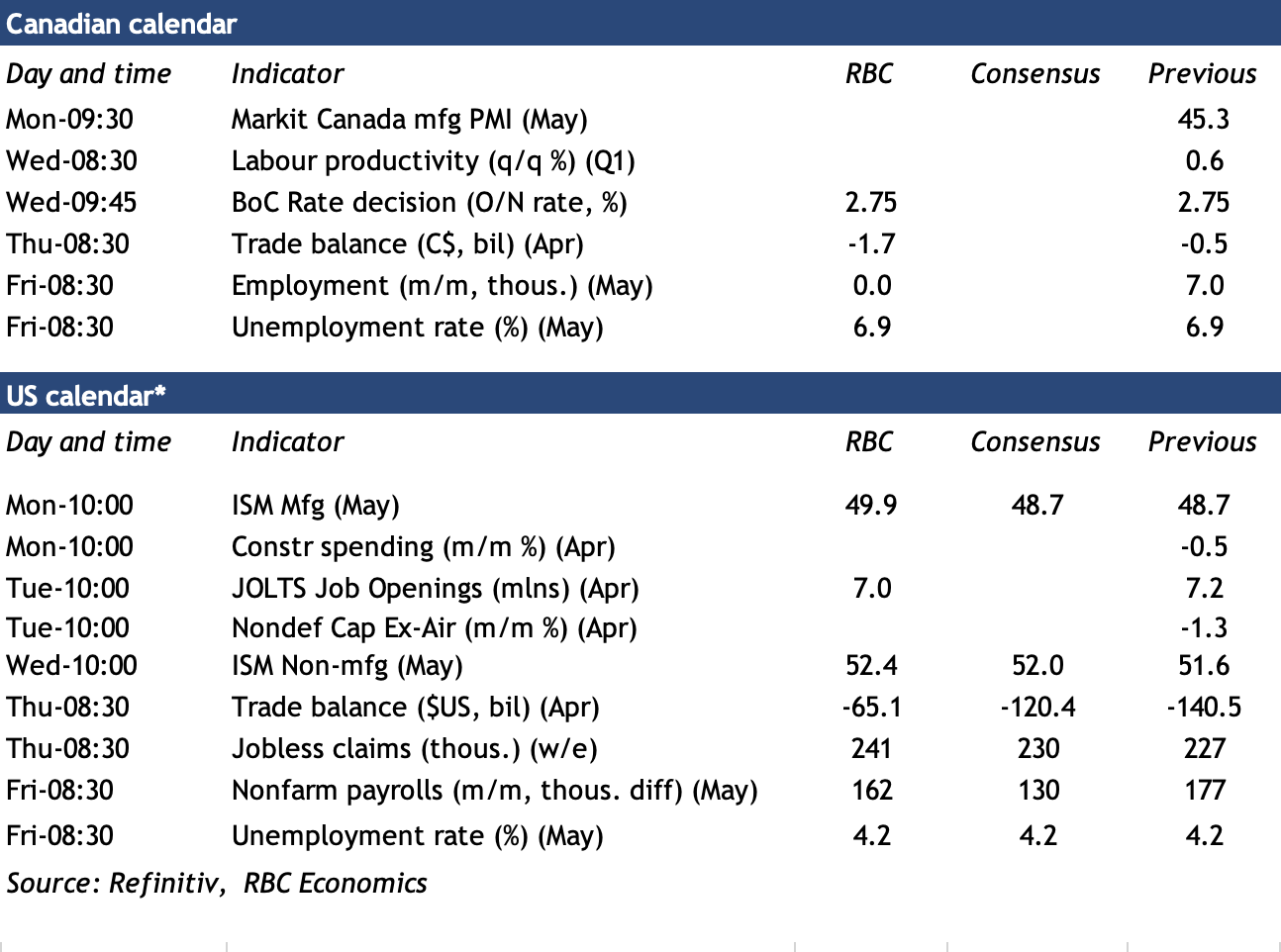

Week Ahead: May NFP, Bank of Canada and ECB Rate Decisions

Week in Review: Trump Taco, USD indecision and RBNZ Rate decision

This week was once again filled with tradable action in markets.

The week started off with closed US and UK markets, a broadly positive sentiment taking global indices higher in the beginning of the week with the Nikkei 225 leading the charge.

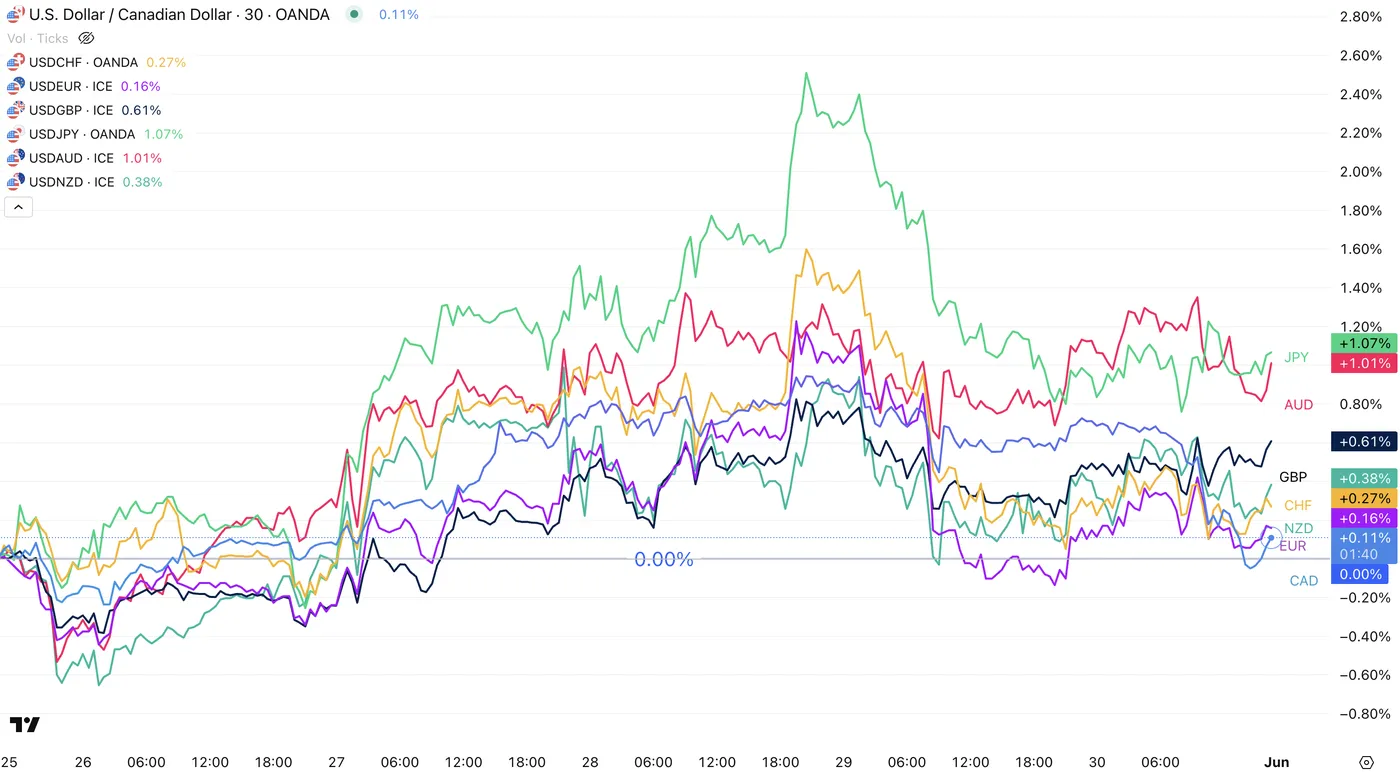

The US Dollar also started the week on a good note, although things have since changed with Wednesday evening Taco Trump headlines: The US Federal Court have cancelled the US President's plan to impose record tariffs on key economic partners.

A picture of the USD performance vs all majors, May 30. Source: TradingView

Indices all around the globe have finished the week green though off their highs. It was a week packed with earnings as we have observed releases for big names such as Nvidia, Dell and Costco who all beat their expectations.

The Nasdaq is beating all US Indices having enjoyed the earnings beats from NVDA and DELL. It is finishing the week up 1.96%

One of the themes that did not help to continue the good news was more uncertainty, as equity markets were on the road to return to their all-time highs though failed to do so.

In the currency space, the US dollar ended up leading—not by strength, but by being the least weak in a choppy week.

The Japanese yen took the biggest hit, following Monday evening remarks from Japan’s Finance Minister that triggered a notable drop in the currency.

We can't forget the biggest headline, the previously mentioned Taco Trump.

This story refers to the U.S. Federal Court’s recent rejection of former President Donald Trump’s trade tariff policies. The court ruled that Trump had overstepped his authority when imposing certain import taxes.

This led to major swings in the Dollar Index as it seesawed above the 100.00 level, then came right back below. The index is closing around 99.40.

For commodities, Gold held around the $3,300 level and stays close to $200 below its all-time high. It seems that the market is awaiting for more news before taking a clear direction. The precious metal still finishes down 2% on the week.

Oil is down almost the same, with fears of higher supply. The price is still constrained between a 60.5 and 64 range.

Bitcoin on the other hand is down above 3.5% on the week, slightly rejecting the all-time highs though prices are still above the key mark of $100,000.

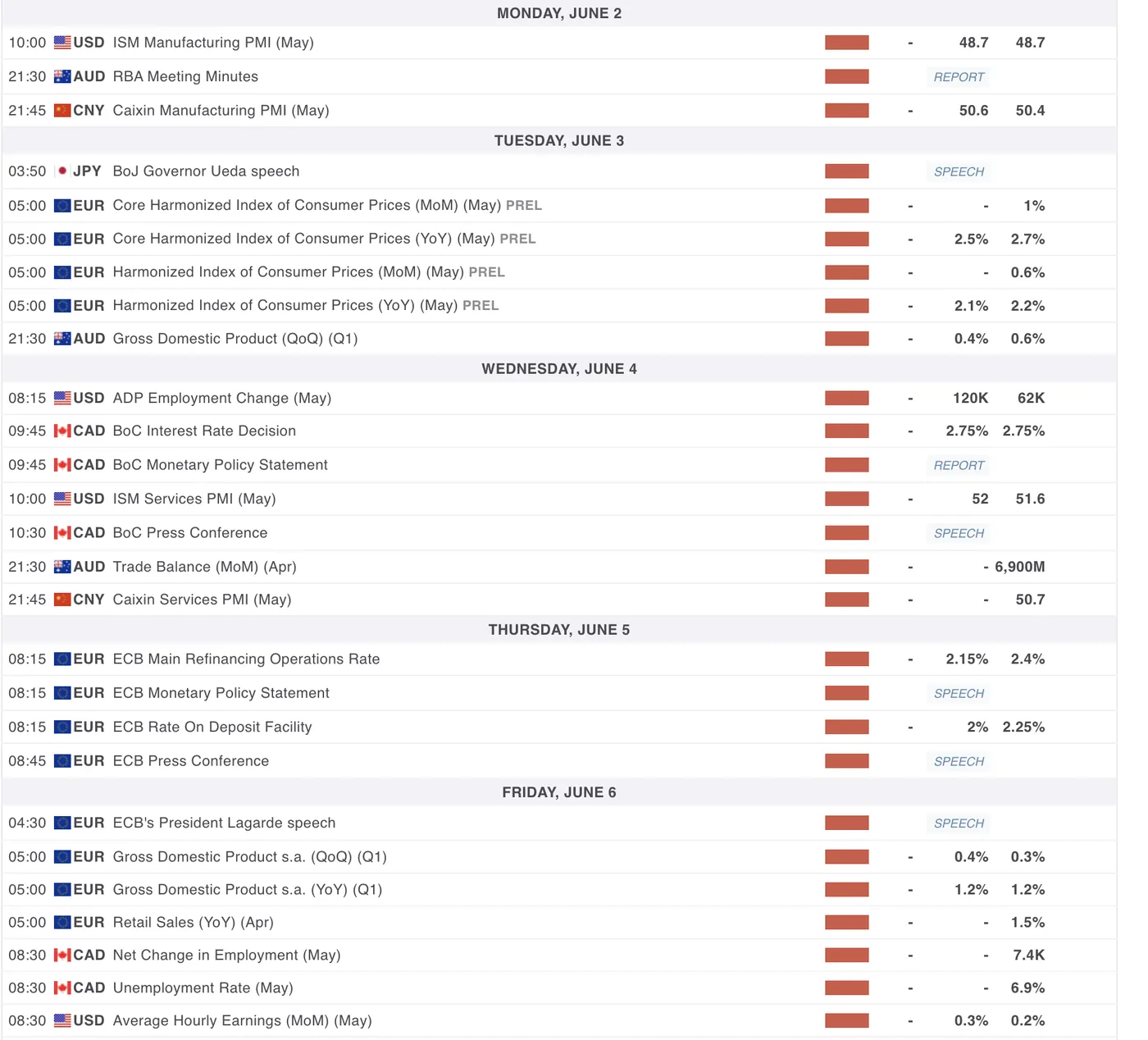

The Week Ahead: May NFP and Rate Decisions for the BoC and ECB

Next week is packed with key data compared to last week. We will see the release of high impact data from the US, China, Canada and Europe. This should be more fuel for volatility, especially if we see any data that provides more clarity on the impact of the most recent Trade Wars.

Asia Pacific Markets Outlook

The week won't be as packed with data for the APAC compared to last week.

We will start off with Minutes from the last RBA Meeting to see if the Australian Central Bank confirms their dovish tone from the May 21 meeting - reminder that they have cut rates by 25 bps at that meeting taking their core policy rate to 3.85%.

We will also see the Caixin Manufacturing PMI Release from China, expected at 50.6, followed by the Services data on Wednesday 4th of June expected at 50.7.

We will observe how tariff menaces impacted the top global exporter.

Finally we are expecting the Australian release for PMIs and Import/Export data.

Do not forget the speech from the BoJ Governor Ueda at 3:50 AM E.T. during the night on Tuesday June 3rd.

Europe, US and UK Market Outlook

Expect a big week for European and North-American markets.

The week starts with PMI Data from Italy, Germany, Canada and the more market-moving US ISM Manufacturing, releasing on Monday June 2nd at 10:00 - Consensus is at 48.7.

Tuesday June 3rd will see the release of the Eurozone CPI which doesn't tend to move markets too much as it is an aggregate of all European countries' CPIs - it may although still impact EUR currency pairs.

Wednesday's most important event will be the Bank of Canada Rate Decision at 9:30, expected to stay put- Rates are at 2.75%.

The Press conference at 10:30 might be more important though to monitor where Governor Macklem is standing regarding his views on the Canadian economy.

We will also have the US Services PMI Release expected at 52.

Thursday we will have the ECB Rate Decision, expected to cut by 25 bps to from 2.4% to 2.15% (Main Refinancing Operations Rate) though the decision is not unanimous. The decision will be out at 8:15 A.M E.T. on the 5th of June.

The rate decision will be followed by mid-tier data from Canada (Ivey PMIs) and the weekly Jobless Claims report.

And to conclude the week, for Friday June 6th, the biggest data will be the release of the US NFP report expected at 130K at 8:30, with the Canadian Jobs data released at the same time and being preceded by Europe Retail Sales at 5:00 E.T.

Most impactful Economic Calendar releases for Next Week

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Safe Trades for the week ahead!

The Weekly Bottom Line: President Trump, the King, and the BoC

Canadian Highlights

- A U.S. court decision to block U.S. IEEPA tariffs could be a win for Canadian manufacturers if it’s upheld. Still, the U.S. has other legal means to impose tariffs on Canada, and sector-specific ones remain in place.

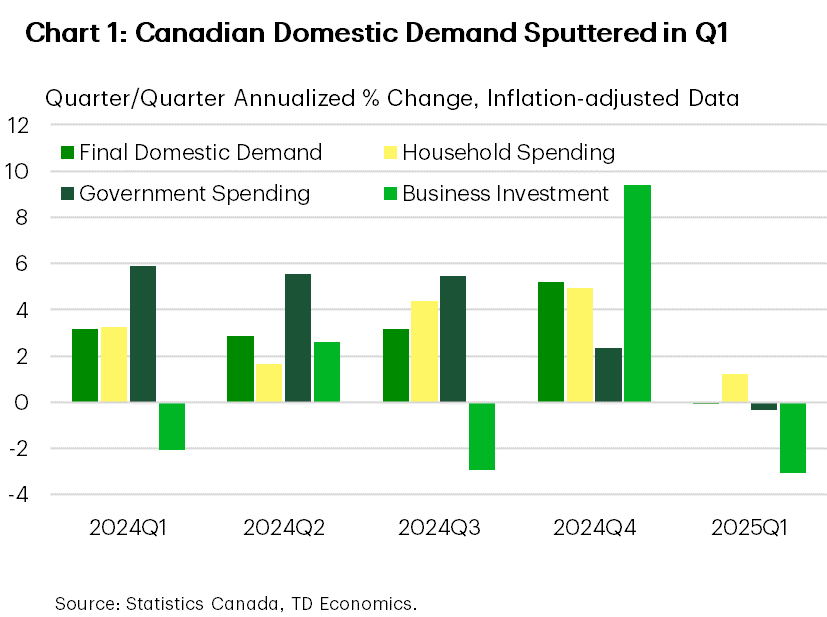

- Canadian GDP advanced at a reasonably firm 2.2% pace in Q1. However, domestic demand flatlined, reinforcing the narrative that Canada’s economy is softening.

- Markets expect Bank of Canada to hold the line on rates next week, although we still see two more cuts taking place this year as evidence of economic weakness mounts.

U.S. Highlights

- The tariff news felt like a tennis match this week. Tariff threats on the EU were paused. Then a court struck down the IEEPA tariffs, only to have an appeal court say they could remain in place.

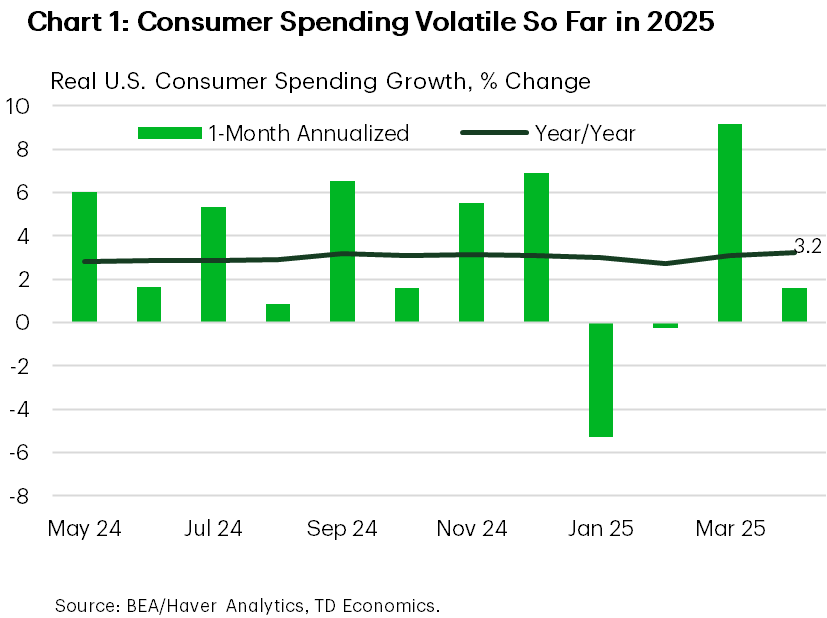

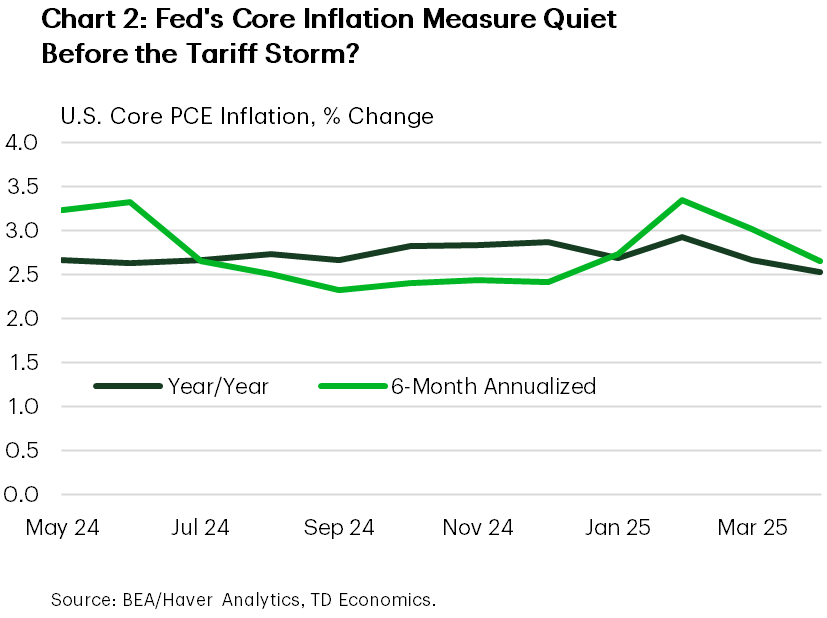

- The economic data showed that inflation pressures were steady through April, while consumer spending has been very volatile so far in 2025.

- President Trump also voiced his desire for rate cuts directly to the Fed Chair this week. Powell reinforced his message that the Fed will be guided by the data.

Canada – President Trump, the King, and the BoC

Canadian equities were certainly on their best behaviour the week of King Charles’ visit to open Canadian Parliament – a first for a monarch since 1977. The TSX surged, although this had little to do with the royal visit, but rather improved sentiment after President Trump’s announcement that the deadline for punishing tariffs on the European Union would be pushed back to allow more time for negotiations.

Probably more notable for Canada was a U.S. court’s decision to block tariffs imposed by the U.S. through its International Emergency Economic Powers Act (IEEPA). The tariffs are staying on for now as the U.S. government appeals the decision, but if the IEEPA tariffs are indeed struck down, that would mean the end to the reciprocal U.S. import taxes announced in April and the duties applied in response to fentanyl trafficking. In Canada’s case, this means the 25% tariffs on non-CUSMA compliant items (10% on energy and other critical minerals) would be gone. However, product-specific tariffs are unaffected by the decision, leaving Canadian steel, aluminum and autos still tariffed. What’s more, the U.S. can use other means to impose tariffs, so the global trading system is not out of the woods yet.

Pivoting back to the Monarch’s Canadian visit, his throne speech was largely a reiteration of policies we’ve heard from the federal government. However, he did make the notable point that Canada will be involved with the European Union’s plan to significantly bolster its defense spending. As of now, Canada is targeting an increase in its defense spending to 2% of Canada’s GDP. However, this week’s announcement from NATO that this target for member countries is likely to be raised to 5% could ramp up the pressure on Canada to spend a significant degree more.

Even getting Canada’s defense expenditures from 2.0% to 3.5% of GDP would require about $45 billion per year in additional spending, so this effort could lift economic growth over time. In the here and now, however, the domestic side of Canada’s economy is flagging. This morning’s GDP report showed that while topline economic growth exceeded expectations (driven by tariff-front running) domestic demand was flat (Chart 1). It wasn’t all bad news however, as Statcan’s preliminary estimate pointed to a 0.1% monthly gain in April’s GDP, offering some upside risk to our forecast for a Q2 contraction.

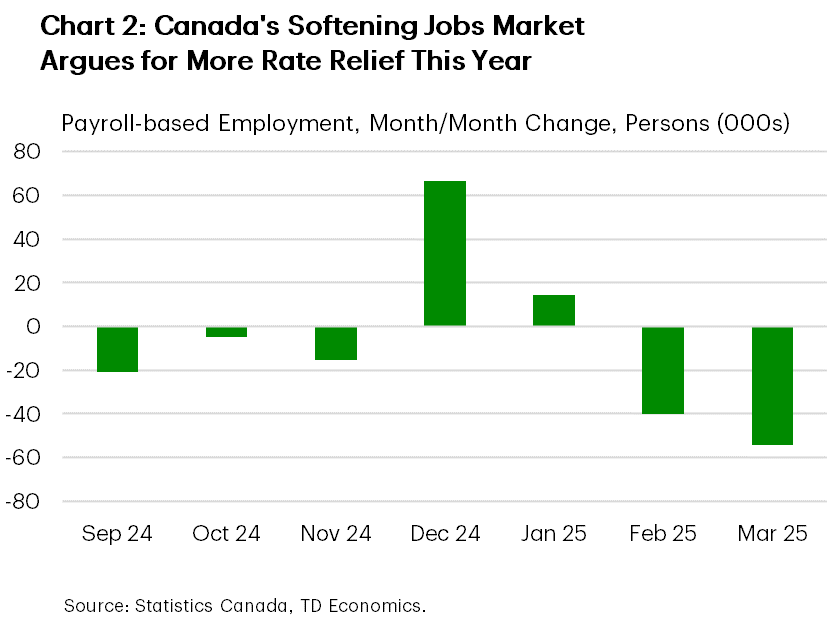

Next week, all eyes will be on the Bank of Canada’s interest rate decision. As it stands, markets expect policymakers to hold the line on rates, especially with a hot core inflation print in April, the federal election bringing the possibility of stimulus, and some global de-escalation in the trade war since the Bank’s last decision in April. On the other hand, Canada’s jobs market is weakening – a narrative reinforced by this week’s payroll data (Chart 2), and domestic activity flatlined in the first quarter. As Canada is likely entering a weak growth period, two more cuts are likely on tap for this year, even if the Bank stands pat next week.

U.S. – Tariff News Tennis Match Continues

Equity markets looked to end the week in the black as the tariff news tennis match seemed to net out on the good news side. The week started with a pause on Trump’s 50% tariff threat against the European Union, then a court struck down some of the Trump administrations’ tariffs before the appellate court deemed they could remain in place for now.

A U.S. trade court invalidated the Trump administration’s use of the International Emergency Economic Powers Act (IEEPA) to levy tariffs. These tariffs include the Canada/Mexico/China “fentanyl” tariffs and the 10% “reciprocal” tariffs. The court ruling has no impact on sectoral tariffs, including those on steel & aluminum and autos. These court battles don’t make it any clearer what will happen with tariffs in the near-term. The administration has other tools they could use to implement tariffs, so this may just be a bump in the road.

The revisions to first quarter economic growth didn’t really change the narrative. The slight contraction in the economy was due to a huge surge in imports, while the domestic economy was still running at a solid 2.5% pace. However, some of that growth was likely due to tariff front-running. These distortions make it harder to get a read on underlying momentum in the economy.

One potential warning sign in the first quarter data was a decline in corporate profits. The drop was seen in nonfinancial firms, which may be a signal that they are coming under pressure. However, April’s personal income data showed that income gains on the household side have been resilient. Incomes were boosted by the implementation of the Social Security Fairness Act, which provided a one-time lift. But even so, wages and salaries continue to grow at a healthy clip. Combined with softer spending growth, the personal savings rate ticked up to its highest level in a year, suggesting consumers have some gas in the tank.

Consumers did take a bit of a breather in April after a solid increase in outlays in March (Chart 1). Consumer spending has been quite volatile so far in 2025, whipsawed by natural disasters and swings in durable goods purchases on things like autos as they try to front run tariffs. This makes it difficult to discern a trend in consumer spending. Even so, we expect that weaker sentiment and a softer labor market ahead will cool the pace of spending in the coming quarters.

The inflation news was steady-as-she goes in April (Chart 2). However, it is a bit early yet to see much inflation pressure from tariffs. We expect inflation will be lifted above 3% later this year as companies pass along higher tariffs to consumers.

President Trump met with Fed Chair Powell for the first time in his second term, reiterating his view that the Fed is making a mistake by not lowering interest rates. Powell stressed that policy decisions would be dependent on the economic data. The Fed minutes from their decision in early May suggested that they are in no hurry to cut rates as they wait for more clarity on the tariff front. Volatility is making it difficult to get clarity on the economic data these days. Add it all up, and the Fed’s wait and see approach is warranted for now.

Weekly Economic & Financial Commentary: A Bump in the Tariff Road

Summary

United States: Waiting for Clarity

- Uncertainty continues to shape economic data. Personal spending was revised lower in Q1 but rose at a modest pace in April amid sturdy income growth. Inflation also remains in check, but we expect to see a tariff-driven bounce in goods prices in the coming months. Meanwhile, the appetite for large capex is generally weak and the housing market remains on ice.

- Next week: ISM Manufacturing (Mon.), ISM Services (Wed.), Employment (Fri.)

International: Global GDP Growth Galore!

- GDP growth data for the first quarter were released from countries all over the world this week. Canada's figures were somewhat mixed, but showed enough resilience in our view for the Bank of Canada to remain on hold next week. Sweden's growth printed to the soft side, potentially reviving the possibility of one final rate cut from the central bank. Brazil's economy continued to show resilience and India's report was mixed, but solid overall.

- Next week: Switzerland CPI (Tue.), Bank of Canada (Wed.), European Central Bank (Thu.)

Interest Rate Watch: Mortgage Rates Move Back Up

- Mortgage rates are back on the rise. According to Freddie Mac, the average 30-year commitment rate climbed to 6.89% during the week of May 29, the highest level since early February. Stepping back, mortgage rates are little changed over the past year. High financing costs remain a significant constraint on residential activity.

Credit Market Insights: Consumer Balancing Act

- Betting against the U.S. consumer still looks like a losing strategy. Across several surveys, consumer credit fundamentals have stabilized over the past year after marginally weakening throughout 2022-2023.

Topic of the Week: A Bump in the Tariff Road

- A U.S. trade court blocked the tariffs President Trump implemented under the International Emergency Economic Powers Act of 1977 (IEEPA) this week. While this provides tariff-rate relief, there remains considerable uncertainty around the future of trade policy.

BoC to Leave Rates Unchanged Ahead of Key Trade and Labour Market Updates

We expect the Bank of Canada will forego an interest rate cut on Wednesday in another close call following April's pause after seven consecutive cuts.

Arguments for a rate cut still remain. Labour markets have weakened, particularly in manufacturing where jobs dropped by 30,600 in April—the largest one-month decline since the pandemic—pushing unemployment to 6.9% from 6.6% in Q1. Housing markets have cooled, reducing the risk that lower rates would reignite surging prices. Gross domestic product growth has remained positive, but the monthly pace slowed sharply after a surge in production in January.

However, the limited data since the BoC’s last decision in April hasn't been entirely negative. Our RBC cardholder tracking shows consumer spending held up better than expected in March and April despite lower survey-based confidence measures.

Friday's Canadian employment report for May (following the BoC decision) will likely show continued weakness in the industrial sector, but recent job postings on Indeed.com suggests hiring demand may be stabilizing. We expect employment to hold steady in May with the unemployment rate remaining at 6.9%.

April’s inflation data also surprised to the upside after accounting for the eliminated consumer carbon tax, driven more by domestic services growth than the impact of tariffs on imports.

Meanwhile, Thursday's international trade data will likely show a widening Canadian trade deficit with exports falling more than imports. U.S. imports plunged 19.8% in April as the U.S. administration imposed reciprocal tariffs on most U.S. trade partners.

Significant U.S. tariffs remain in place. A U.S. court ruling blocking some of the Trump administration’s tariffs (including blanket tariffs on most U.S. trade partners in April) is under appeal, and the tariffs are still in effect for now. But CUSMA-compliant Canadian exports were already exempt from those measures. Sector-specific U.S. tariffs on steel, aluminum and vehicles remain as well, but we estimate more than 86% of Canadian exports still receive duty-free U.S. market access under the current rules.

The BoC has already cut rates by 225 basis points over the past year—more than other central banks. It still has room for further cuts if economic conditions weaken, but will need to consider any government spending support measures, which are better suited to provide targeted, timely, and temporary assistance to affected sectors than interest rate cuts.

Week ahead data watch

We expect U.S. payrolls likely grew by 162,000 in May, slightly down from the 177,000 in April. We also believe the unemployment rate held steady at 4.2%. The details will be closely watched for signs of softening in trade-sensitive sectors like manufacturing, but weekly initial jobless claims have remained low.

The U.S. trade deficit narrowed sharply in April in advance estimates with goods imports plunging 19.8% to retrace a pre-tariff run up, and exports rose slightly by 3.4%. The drop in imports likely partially reflected a reversal of a pre-tariff surge in gold imports, which won’t pass through to GDP measures for Q2. But, imports of autos and (non-auto) consumer goods declined by 19.1% and 32.3%, respectively.

Summary 6/2 – 6/6

Monday, Jun 2, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | 3.80% | -0.20% |

| 00:30 | JPY | Manufacturing PMI May | 49 | 49 |

| 01:00 | AUD | TD-MI Inflation Gauge M/M May | 0.60% | |

| 06:30 | CHF | Real Retail Sales Y/Y Apr | 2.50% | 2.20% |

| 07:00 | CHF | GDP Q/Q Q1 | 0.40% | 0.20% |

| 07:30 | CHF | Manufacturing PMI May | 48.1 | 45.8 |

| 07:50 | EUR | France Manufacturing PMI May F | 49.5 | 49.5 |

| 07:55 | EUR | Germany Manufacturing PMI May F | 48.8 | 48.8 |

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 49.4 | 49.4 |

| 08:30 | GBP | Manufacturing PMI May F | 45.1 | 45.1 |

| 08:30 | GBP | Mortgage Approvals Apr | 65K | 64K |

| 08:30 | GBP | M4 Money Supply M/M Apr | 0.20% | 0.30% |

| 13:30 | CAD | Manufacturing PMI May | 45.3 | |

| 13:45 | USD | Manufacturing PMI May F | 52.3 | 52.3 |

| 14:00 | USD | ISM Manufacturing PMI May | 49.3 | 48.7 |

| 14:00 | USD | ISM Manufacturing Prices Paid May | 70.2 | 69.8 |

| 14:00 | USD | ISM Manufacturing Employment Index May | 46.5 | |

| 14:00 | USD | Construction Spending M/M Apr | 0.30% | -0.50% |

| 22:45 | NZD | Terms of Trade Index Q1 | 3.60% | 3.10% |

| 23:50 | JPY | Monetary Base Y/Y May | -4.20% | -4.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | |

| Forecast: 3.80% | Previous: -0.20% | ||

| 00:30 | JPY | Manufacturing PMI May | |

| Forecast: 49 | Previous: 49 | ||

| 01:00 | AUD | TD-MI Inflation Gauge M/M May | |

| Forecast: | Previous: 0.60% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Apr | |

| Forecast: 2.50% | Previous: 2.20% | ||

| 07:00 | CHF | GDP Q/Q Q1 | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 07:30 | CHF | Manufacturing PMI May | |

| Forecast: 48.1 | Previous: 45.8 | ||

| 07:50 | EUR | France Manufacturing PMI May F | |

| Forecast: 49.5 | Previous: 49.5 | ||

| 07:55 | EUR | Germany Manufacturing PMI May F | |

| Forecast: 48.8 | Previous: 48.8 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI May F | |

| Forecast: 49.4 | Previous: 49.4 | ||

| 08:30 | GBP | Manufacturing PMI May F | |

| Forecast: 45.1 | Previous: 45.1 | ||

| 08:30 | GBP | Mortgage Approvals Apr | |

| Forecast: 65K | Previous: 64K | ||

| 08:30 | GBP | M4 Money Supply M/M Apr | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:30 | CAD | Manufacturing PMI May | |

| Forecast: | Previous: 45.3 | ||

| 13:45 | USD | Manufacturing PMI May F | |

| Forecast: 52.3 | Previous: 52.3 | ||

| 14:00 | USD | ISM Manufacturing PMI May | |

| Forecast: 49.3 | Previous: 48.7 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid May | |

| Forecast: 70.2 | Previous: 69.8 | ||

| 14:00 | USD | ISM Manufacturing Employment Index May | |

| Forecast: | Previous: 46.5 | ||

| 14:00 | USD | Construction Spending M/M Apr | |

| Forecast: 0.30% | Previous: -0.50% | ||

| 22:45 | NZD | Terms of Trade Index Q1 | |

| Forecast: 3.60% | Previous: 3.10% | ||

| 23:50 | JPY | Monetary Base Y/Y May | |

| Forecast: -4.20% | Previous: -4.80% | ||

Tuesday, Jun 3, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||

| 01:30 | AUD | Current Account (AUD) Q1 | -12.0B | -12.5B |

| 01:45 | CNY | Caixin Manufacturing PMI May | 50.6 | 50.4 |

| 06:30 | CHF | CPI M/M May | 0.20% | 0.00% |

| 06:30 | CHF | CPI Y/Y May | 0% | |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.20% | 6.20% |

| 09:00 | EUR | Eurozone CPI Y/Y May P | 2.00% | 2.20% |

| 09:00 | EUR | Eurozone CPI Core Y/Y May P | 2.40% | 2.70% |

| 14:00 | USD | Factory Orders M/M Apr | -3.10% | 3.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | |

| Forecast: | Previous: | ||

| 01:30 | AUD | Current Account (AUD) Q1 | |

| Forecast: -12.0B | Previous: -12.5B | ||

| 01:45 | CNY | Caixin Manufacturing PMI May | |

| Forecast: 50.6 | Previous: 50.4 | ||

| 06:30 | CHF | CPI M/M May | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 06:30 | CHF | CPI Y/Y May | |

| Forecast: | Previous: 0% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Apr | |

| Forecast: 6.20% | Previous: 6.20% | ||

| 09:00 | EUR | Eurozone CPI Y/Y May P | |

| Forecast: 2.00% | Previous: 2.20% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May P | |

| Forecast: 2.40% | Previous: 2.70% | ||

| 14:00 | USD | Factory Orders M/M Apr | |

| Forecast: -3.10% | Previous: 3.40% | ||

Wednesday, Jun 4, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q1 | 0.40% | 0.60% |

| 07:50 | EUR | France Services PMI May F | 47.4 | 47.4 |

| 07:55 | EUR | Germany Services PMI May F | 47.2 | 47.2 |

| 08:00 | EUR | Eurozone Services PMI May F | 48.9 | 48.9 |

| 08:30 | GBP | Services PMI May F | 50.2 | 50.2 |

| 12:15 | USD | ADP Employment Change May | 120K | 62K |

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 0.40% | 0.60% |

| 13:45 | CAD | BoC Interest Rate Decision | 2.75% | 2.75% |

| 13:45 | USD | Services PMI May F | 52.3 | 52.3 |

| 14:00 | USD | ISM Services PMI May | 52 | 51.6 |

| 14:30 | CAD | BoC Press Conference | ||

| 14:30 | USD | Crude Oil Inventories | -2.8M | |

| 18:00 | USD | Fed's Beige Book | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Apr | 2.60% | 2.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q1 | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 07:50 | EUR | France Services PMI May F | |

| Forecast: 47.4 | Previous: 47.4 | ||

| 07:55 | EUR | Germany Services PMI May F | |

| Forecast: 47.2 | Previous: 47.2 | ||

| 08:00 | EUR | Eurozone Services PMI May F | |

| Forecast: 48.9 | Previous: 48.9 | ||

| 08:30 | GBP | Services PMI May F | |

| Forecast: 50.2 | Previous: 50.2 | ||

| 12:15 | USD | ADP Employment Change May | |

| Forecast: 120K | Previous: 62K | ||

| 12:30 | CAD | Labor Productivity Q/Q Q1 | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 13:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 2.75% | Previous: 2.75% | ||

| 13:45 | USD | Services PMI May F | |

| Forecast: 52.3 | Previous: 52.3 | ||

| 14:00 | USD | ISM Services PMI May | |

| Forecast: 52 | Previous: 51.6 | ||

| 14:30 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -2.8M | ||

| 18:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Apr | |

| Forecast: 2.60% | Previous: 2.30% | ||

Thursday, Jun 5, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Apr | 6.05B | 6.90B |

| 01:45 | CNY | Caixin Services PMI May | 51.1 | 50.7 |

| 05:45 | CHF | Unemployment Rate May | 2.80% | 2.80% |

| 06:00 | EUR | Germany Factory Orders M/M Apr | -1.10% | 3.60% |

| 08:30 | GBP | Construction PMI May | 47.2 | 46.6 |

| 11:30 | USD | Challenger Job Cuts Y/Y May | 62.70% | |

| 12:15 | EUR | ECB Deposit Rate | 2.00% | 2.25% |

| 12:30 | CAD | Trade Balance (CAD) Apr | 0.2B | -0.5B |

| 12:30 | USD | Initial Jobless Claims (May 30) | 235K | 240K |

| 12:30 | USD | Trade Balance (USD) Apr | -117.2B | -140.5B |

| 12:30 | USD | Nonfarm Productivity Q1 | -0.80% | -0.80% |

| 12:30 | USD | Unit Labor Costs Q1 | 5.70% | 5.70% |

| 12:45 | EUR | ECB Press Conference | ||

| 14:00 | CAD | Ivey PMI May | 48.3 | 47.9 |

| 14:30 | USD | Natural Gas Storage | 101B | |

| 23:30 | JPY | Overall Household Spending Y/Y Apr | 1.50% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Apr | |

| Forecast: 6.05B | Previous: 6.90B | ||

| 01:45 | CNY | Caixin Services PMI May | |

| Forecast: 51.1 | Previous: 50.7 | ||

| 05:45 | CHF | Unemployment Rate May | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 06:00 | EUR | Germany Factory Orders M/M Apr | |

| Forecast: -1.10% | Previous: 3.60% | ||

| 08:30 | GBP | Construction PMI May | |

| Forecast: 47.2 | Previous: 46.6 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y May | |

| Forecast: | Previous: 62.70% | ||

| 12:15 | EUR | ECB Deposit Rate | |

| Forecast: 2.00% | Previous: 2.25% | ||

| 12:30 | CAD | Trade Balance (CAD) Apr | |

| Forecast: 0.2B | Previous: -0.5B | ||

| 12:30 | USD | Initial Jobless Claims (May 30) | |

| Forecast: 235K | Previous: 240K | ||

| 12:30 | USD | Trade Balance (USD) Apr | |

| Forecast: -117.2B | Previous: -140.5B | ||

| 12:30 | USD | Nonfarm Productivity Q1 | |

| Forecast: -0.80% | Previous: -0.80% | ||

| 12:30 | USD | Unit Labor Costs Q1 | |

| Forecast: 5.70% | Previous: 5.70% | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:00 | CAD | Ivey PMI May | |

| Forecast: 48.3 | Previous: 47.9 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 101B | ||

| 23:30 | JPY | Overall Household Spending Y/Y Apr | |

| Forecast: 1.50% | Previous: 2.10% | ||

Friday, Jun 6, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Apr P | 104.1 | |

| 06:00 | EUR | Germany Industrial Production M/M Apr | -0.90% | 3.00% |

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | 20.2B | 21.1B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | 703B | |

| 09:00 | EUR | GDP Q/Q Q1 F | 0.40% | 0.30% |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 F | 0.30% | 0.30% |

| 09:00 | EUR | Eurozone PPI M/M Apr | -1.60% | |

| 09:00 | EUR | Eurozone PPI Y/Y Apr | 1.90% | |

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | 0.20% | -0.10% |

| 12:30 | CAD | Net Change in Employment May | 7.4K | |

| 12:30 | CAD | Unemployment Rate May | 6.90% | |

| 12:30 | USD | Nonfarm Payrolls May | 130K | 177K |

| 12:30 | USD | Unemployment Rate May | 4.20% | 4.20% |

| 12:30 | USD | Average Hourly Earnings M/M May | 0.30% | 0.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Apr P | |

| Forecast: | Previous: 104.1 | ||

| 06:00 | EUR | Germany Industrial Production M/M Apr | |

| Forecast: -0.90% | Previous: 3.00% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | |

| Forecast: 20.2B | Previous: 21.1B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | |

| Forecast: | Previous: 703B | ||

| 09:00 | EUR | GDP Q/Q Q1 F | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 09:00 | EUR | Eurozone PPI M/M Apr | |

| Forecast: | Previous: -1.60% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Apr | |

| Forecast: | Previous: 1.90% | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 12:30 | CAD | Net Change in Employment May | |

| Forecast: | Previous: 7.4K | ||

| 12:30 | CAD | Unemployment Rate May | |

| Forecast: | Previous: 6.90% | ||

| 12:30 | USD | Nonfarm Payrolls May | |

| Forecast: 130K | Previous: 177K | ||

| 12:30 | USD | Unemployment Rate May | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | |

| Forecast: 0.30% | Previous: 0.20% | ||