Sample Category Title

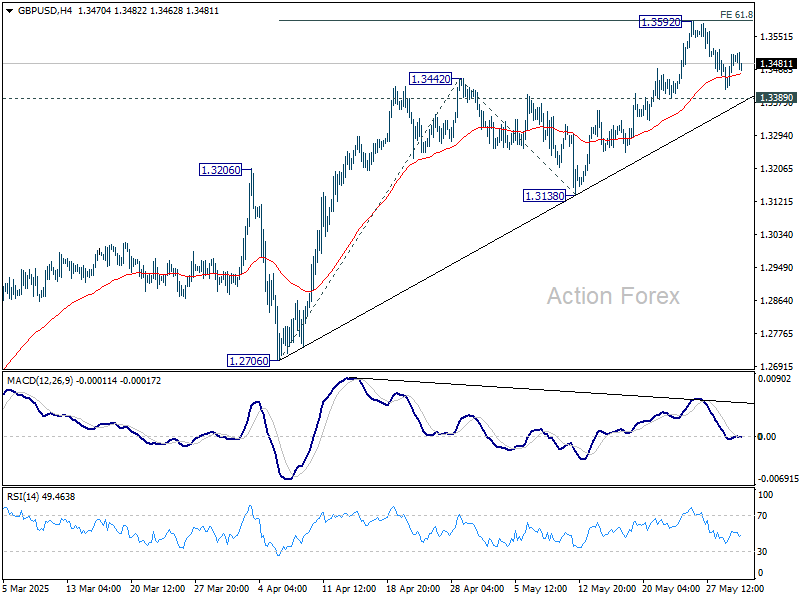

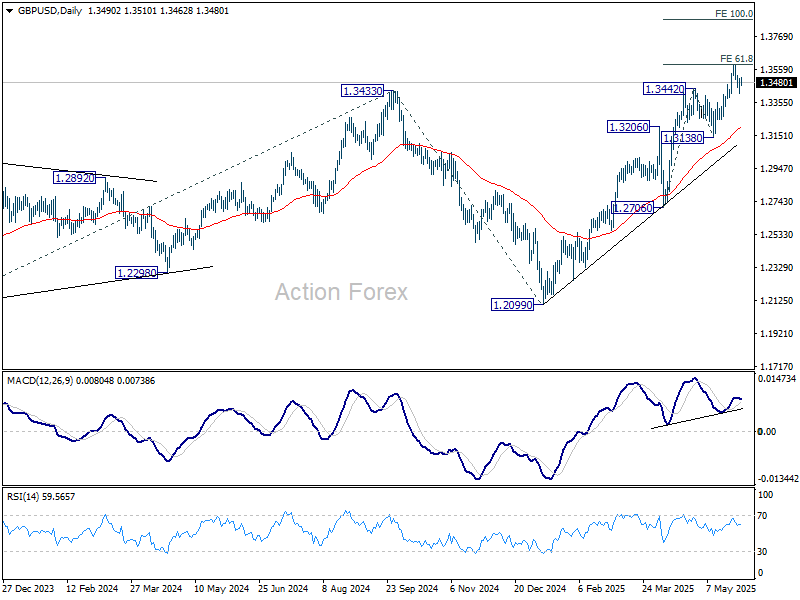

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3437; (P) 1.3472; (R1) 1.3529; More...

GBP/USD is staying in consolidation below 1.3592 and intraday bias stays neutral. With 1.3389 support intact, further rally is expected. On the upside, firm break of 1.3592 will resume larger rally for 100% projection of 1.2706 to 1.3442 from 1.3138 at 1.3874. However, decisive break of 1.3389 will confirm short term topping, and turn bias back to the downside for 1.3138 support instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2870) holds, even in case of deep pullback.

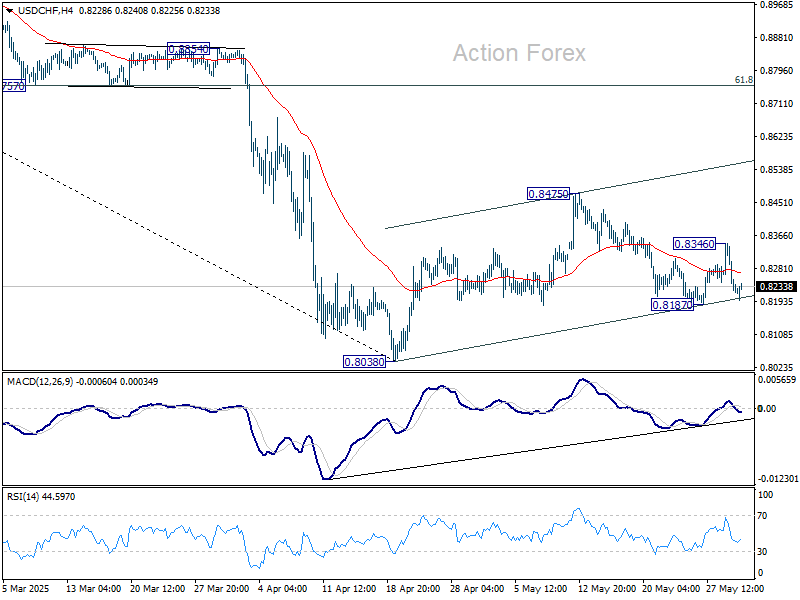

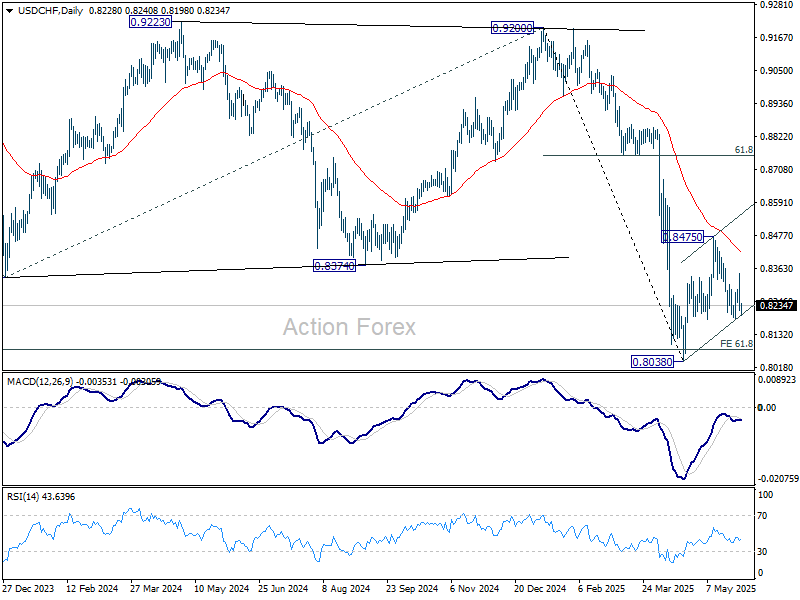

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8182; (P) 0.8265; (R1) 0.8312; More….

Intraday bias in USD/CHF remains neutral at this point. On the downside, break of 0.8187 will resume the fall from 0.8475 to retest 0.8038 low. On the upside, above 0.8346 will bring stronger rise to 0.8475. Firm break there will extend the corrective pattern from 0.8038 with another rising leg.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8713) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

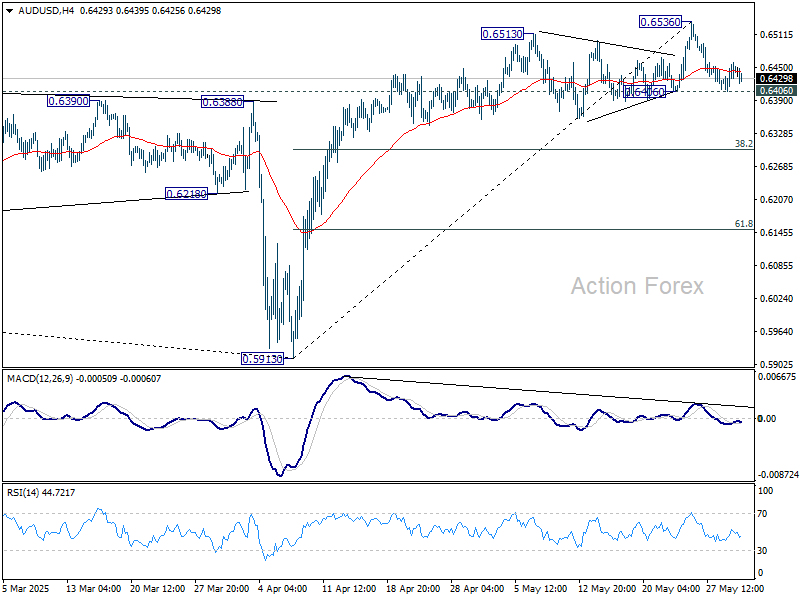

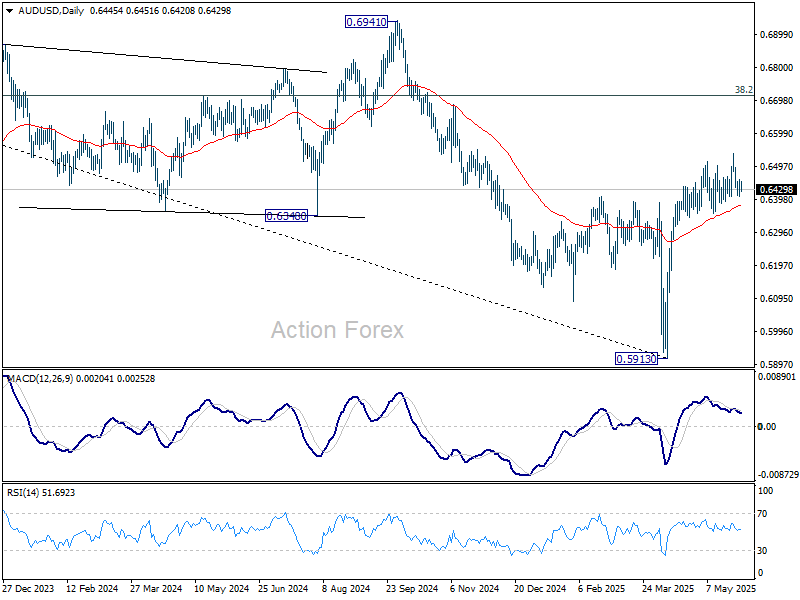

AUD/USD Daily Report

Daily Pivots: (S1) 0.6413; (P) 0.6436; (R1) 0.6466; More...

Intraday bias in AUD/USD remains neutral, and further rally is in favor with 0.6406 support intact. On the upside, break of 0.6536 will resume whole rally from 0.5913. However, firm break of 0.6406 will confirm short term topping, and turn bias back to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, 55 W EMA (now at 0.6439) is considered taken out. A medium term bottom should already be in place at 0.5913. Rise from there could either be a corrective move, or reversing whole down trend from 0.8006 (2021 high). In either case, further rise is now expected as long as 55 D EMA (now at 0.6376) holds. Next target is 38.2% retracement of 0.8006 to 0.5913 at 0.6713.

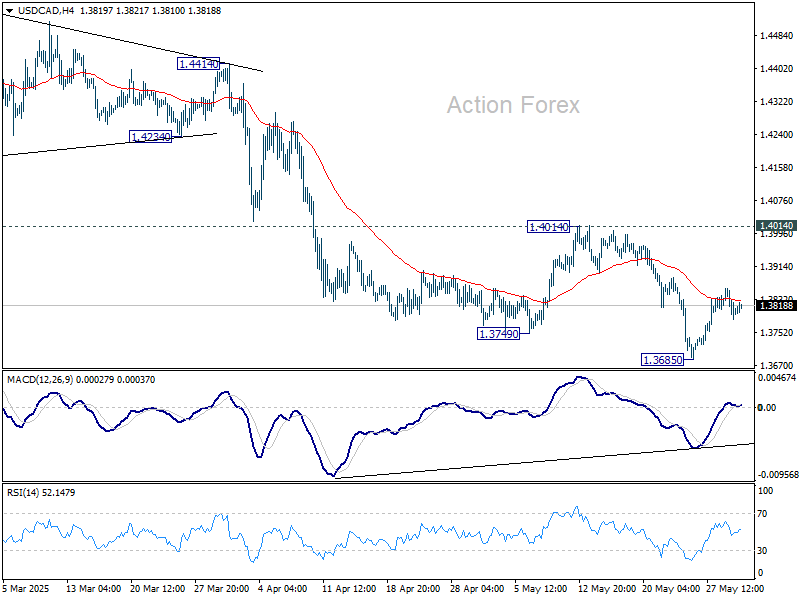

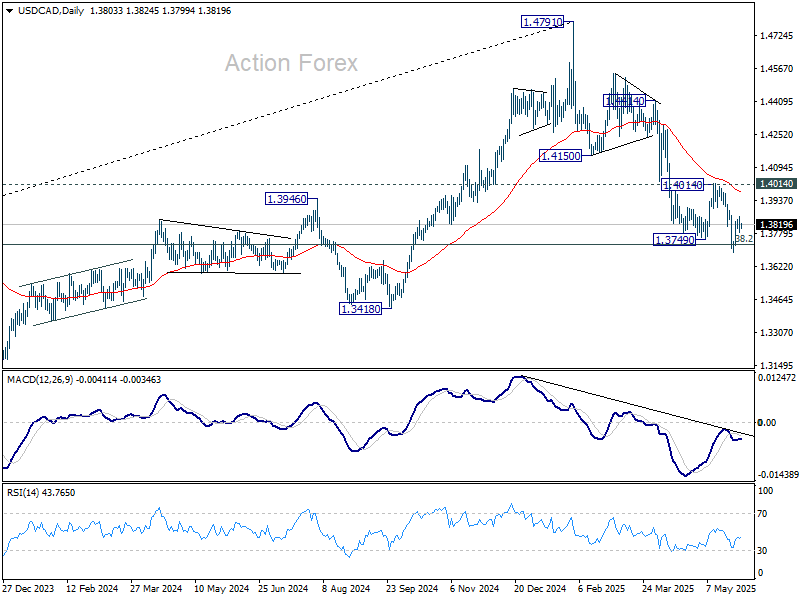

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3775; (P) 1.3818; (R1) 1.3852; More...

Intraday bias in USD/CAD stays neutral at this point. Consolidation from 1.3685 could extend further. But upside should be limited well below 1.4014 resistance to bring another fall. Break of 1.3685 will resume whole decline from 1.4791.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

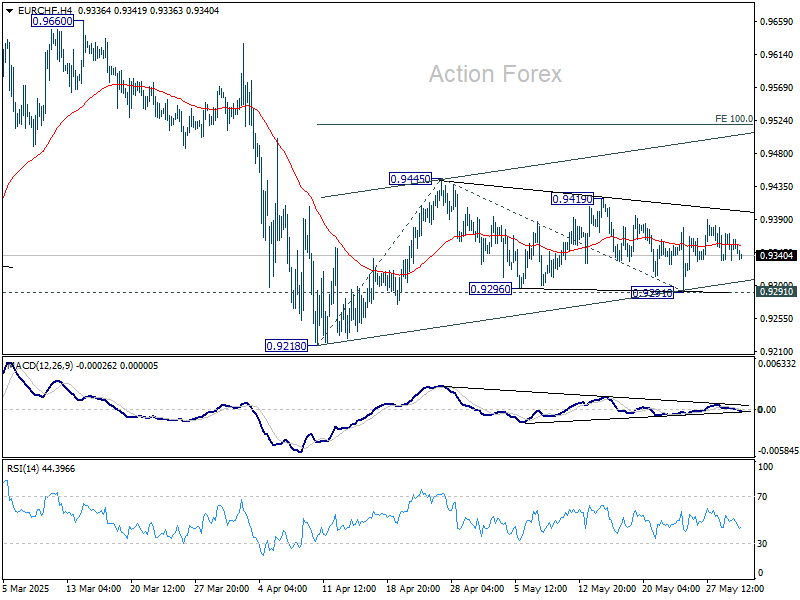

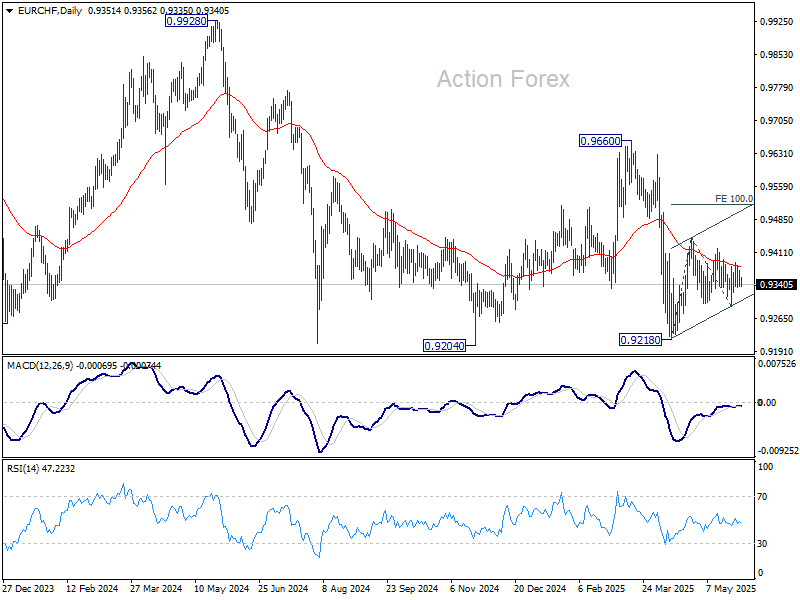

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9336; (P) 0.9354; (R1) 0.9373; More....

Intraday bias in EUR/CHF remains neutral for the moment as sideway trading is still in progress. Price actions from 0.9218 are seen as either a corrective move or the third leg of the pattern from 0.9204. On the upside, break of 0.9419 will resume the rise from 0.9218 through 0.9445 resistance. However, firm break of 0.9291 support will bring retest of 0.9218 low.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

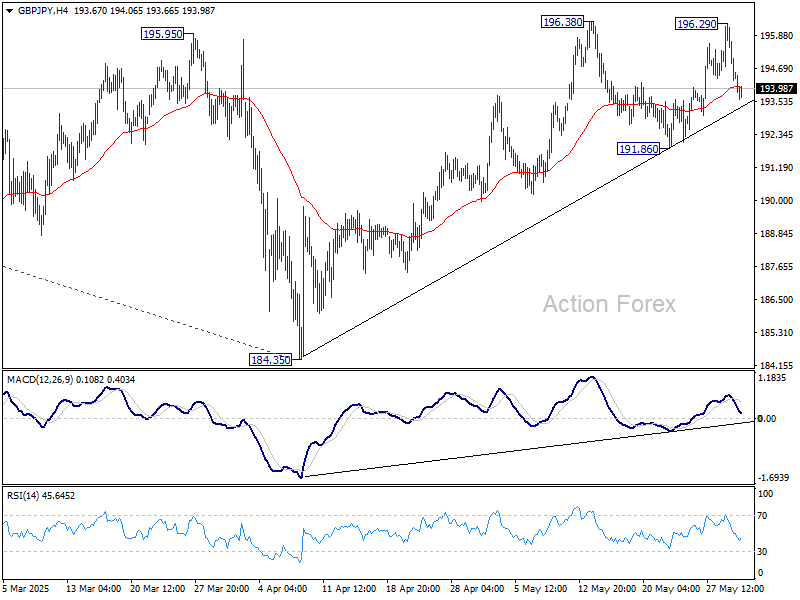

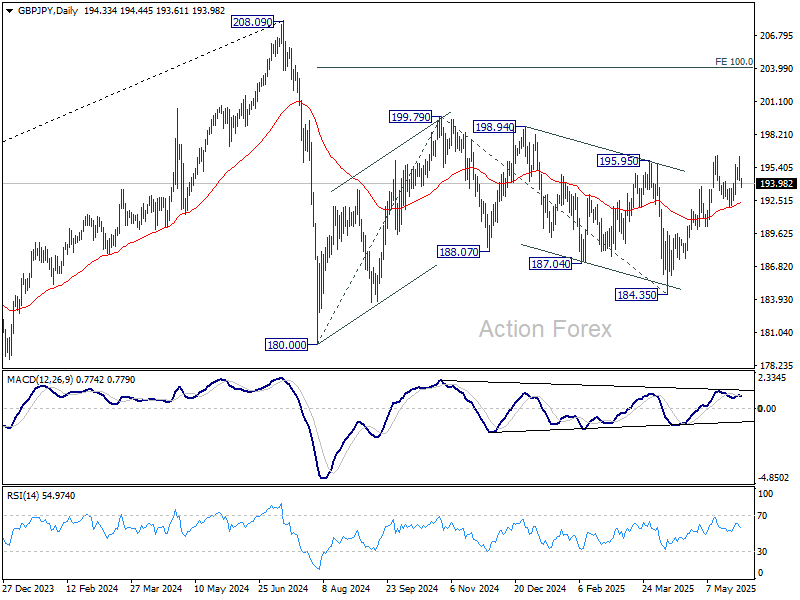

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.80; (P) 195.06; (R1) 195.83; More...

GBP/JPY reversed after failing to break through 196.38 resistance and intraday bias is turned neutral again. Further rise is in favor as long as 191.86 support holds. Firm break of 196.38 will resume whole rally from 184.35.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

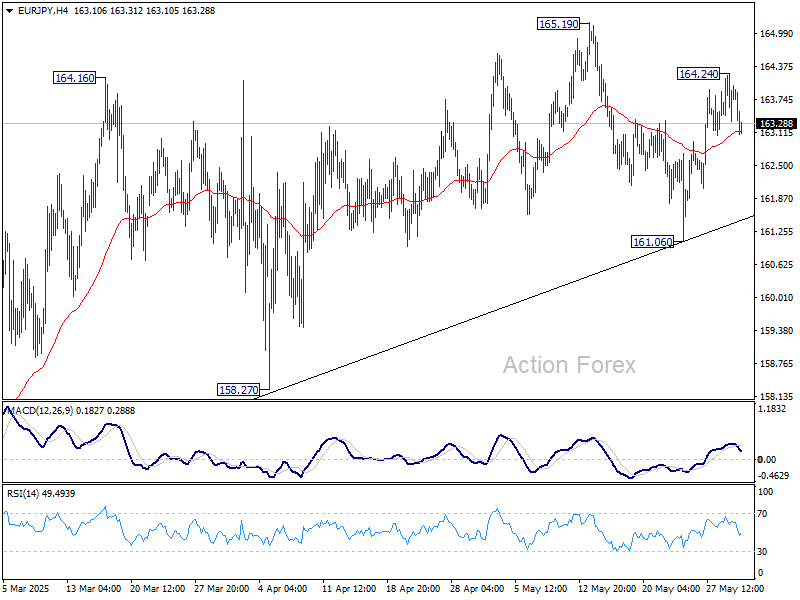

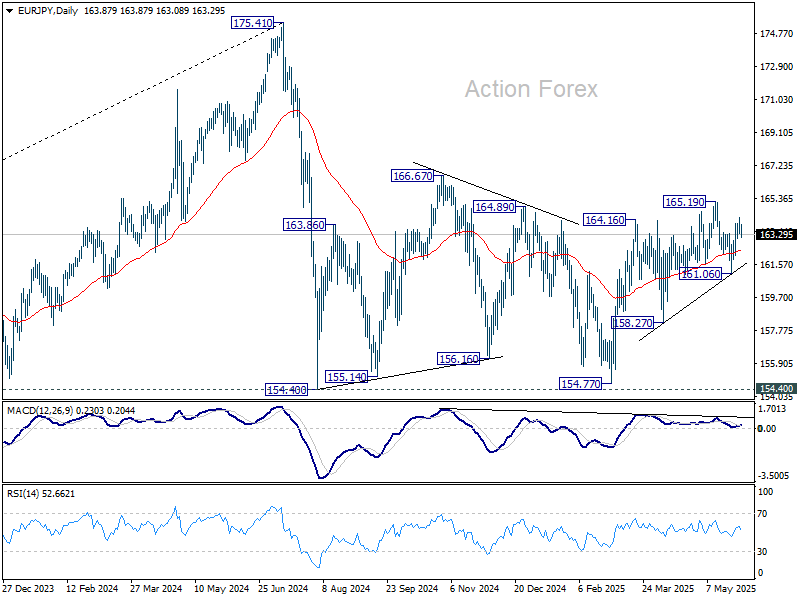

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.40; (P) 163.84; (R1) 164.32; More...

Intraday bias in EUR/JPY is turned neutral again with current retreat. On the upside, above 164.24 will bring retest of 165.19 resistance first. Firm break there will resume while rise from 154.77 to 166.67 resistance. On the downside, however, break of 161.06 will resume the decline from 165.19 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

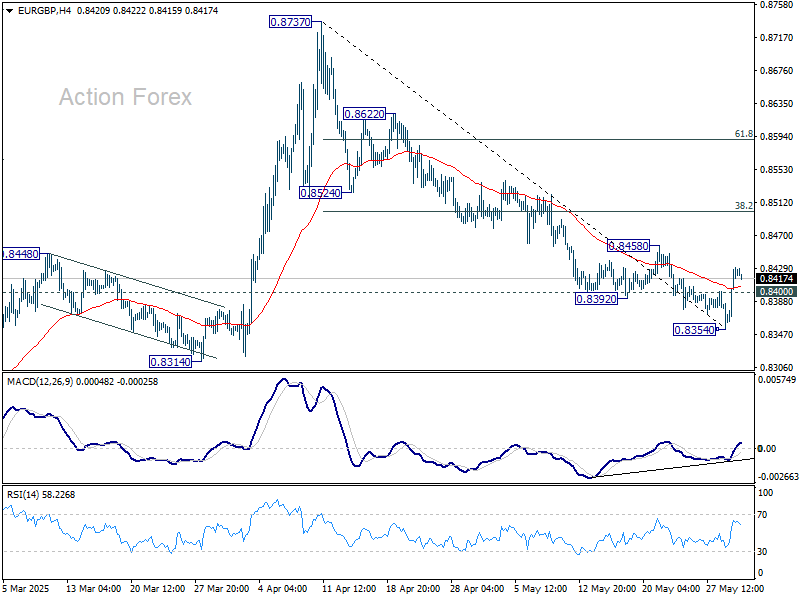

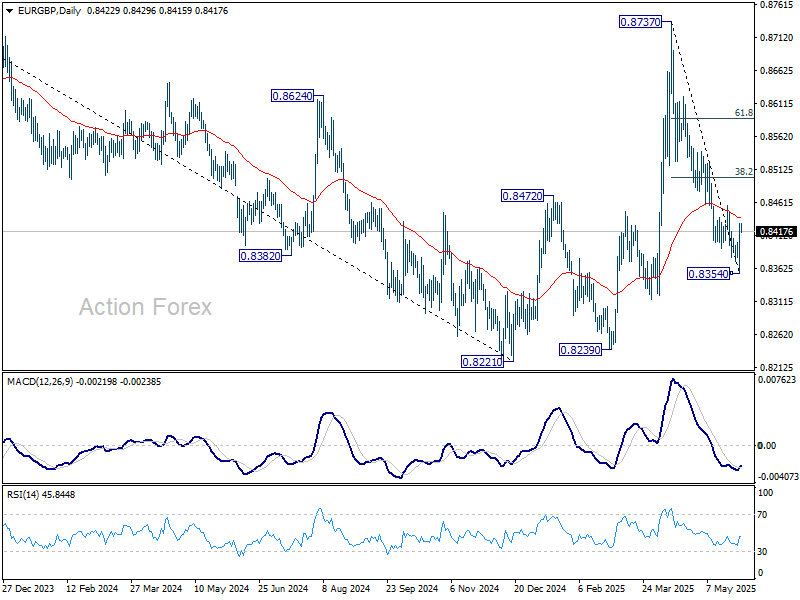

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8376; (P) 0.8404; (R1) 0.8452; More...

EUR/GBP's break of 0.8400 resistance indicates short term bottoming at 0.8354, on bullish convergence condition in 4H MACD. Rebound from there is seen as a corrective move first. Still, intraday bias is back on the upside for 0.8458 resistance and then 38.2% retracement of 0.8737 to 0.8354 at 0.8500.

In the bigger picture, current development suggests that price actions from 0.8221 medium term bottom are merely forming a corrective pattern. However, there is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

Tariff Saga Act Three: Legal Worries

What began as early trade optimism yesterday – triggered by the US Court of International Trade deeming Trump’s tariffs illegal – turned out to be too good to be true. Things quickly got messy when Trump appealed the decision, prompting the US Court of Appeals to pause the ruling in order to review arguments from both sides. Meanwhile, a separate federal court issued a similar but more limited decision on the tariffs. As a result, the initial ruling that had cancelled the tariffs is now effectively on hold.

As such, uncertainty has surged – no one is quite sure what’s legal and what’s not anymore. Some reports suggest the Trump administration could still find legal grounds to uphold its tariff policies. One of the most cited tools is Section 232 of the Trade Expansion Act of 1962, which allows for industry-specific tariffs on cars, steel, and aluminium on national security grounds. Other potential avenues include Section 301, which deals with unfair trade practices, and Section 122, apparently designed to manage trade deficits and defend the US dollar. In short, there are a lot of legal levers in the air – and most of us aren’t lawyers.

But you don’t need to be a lawyer to smell the thick uncertainty about what the US government might do next – and how trade partners will respond. If tariffs are ultimately found to be unlawful, the willingness of partners to make concessions during trade talks may shrink – not exactly ideal, especially given the critical window for negotiations. And whether there’ll be legal clarity ahead of the June 9th deadline for European trade negotiations – which could end with 50% tariffs, or not – is anyone’s guess.

So it’s under this heavy cloud of uncertainty that the early risk-on rally yesterday fizzled out. The S&P500 rapidly erased its earlier gains, though it still managed to close up around 0.40%. The Nasdaq held on to 0.21%, after earlier surging 2%, thanks in part to Nvidia, which ended the day over 3% higher and just below the $140/share mark.

Beyond better-than-expected earnings and forecasts that confirmed robust AI demand was enough to offset Chinese weakness, Nvidia also got a boost from a US Department of Energy announcement: the company, alongside Dell, has been awarded a contract to build a new flagship supercomputer for the National Energy Research Scientific Computing Center. Dell rose roughly 2% in after-hours trading and looks poised to break out of its one-year descending trend channel.

Elsewhere, the Dow Jones was little changed. Chinese and Japanese stocks gave back some of their recent gains, and both US and European futures are pointing slightly lower this morning. It’s not chaotic – but it’s far from ideal.

In the FX

Ongoing uncertainty around US fiscal and trade policy continues to weigh on the US dollar. Meanwhile, the economic impact of aggressive Trump policies – both on trade and government offices – is starting to show in the data. Figures released yesterday confirmed a contraction in US GDP in Q1, with spending growth more than halving and the trade deficit ballooning as firms rushed to import goods ahead of possible tariffs. Inventories rose. A key price gauge showed a sharp reversal in inflation pressures.

Donald Trump reportedly met with Federal Reserve (Fed) Chair Jerome Powell to press for rate cuts. The US 2-year yield dipped below 4% as markets ramped up dovish bets. But the man is unlikely to give Trump the rate support he wants while trade uncertainty and inflation pressures mount. Most US companies have already said they’ll pass tariff costs onto consumers. Their international counterparts say they’ll do the same. Add in rising shipping costs driven by trade flow disruptions, and the conclusion is clear: prices will rise. Whether that spike is temporary remains to be seen – but either way, it complicates the Fed’s job.

Today’s PCE data – the Fed’s preferred inflation gauge – could surprise to the downside or meet expectations, but the full effects of the ‘tariff tsunami’ likely haven’t reached shore yet. The data will need to be taken with a pinch of salt.

In Europe, the inflation outlook is heading in the opposite direction. The tariffs won’t affect European consumers, and the euro’s recent appreciation is helping lower energy and commodity costs. April inflation numbers across the Eurozone – due today – are expected to show further softening in European price dynamics. Sufficiently weak figures should keep European Central Bank (ECB) doves comfortable with the easing path, which in turn supports the EZ growth narrative and the euro.

OPEC decision in sight

US crude is wavering just above the critical $60/barrel level this week. OPEC is preparing to announce its third major output restoration over the weekend. The cartel is expected to bring an additional 411,000 barrels per day to the market starting in July – about 1% of current production – citing ‘rising demand as official justification. But the official statement feels thin, given waning demand prospects amid global trade tensions. OPEC may simply be trying to appease Trump – or punish member states that failed to comply with past quotas. Whatever the rationale, if trade tensions persist, the rising supply could send oil prices meaningfully lower. A drop of another $10/barrel in the second half of the year can’t be ruled out.

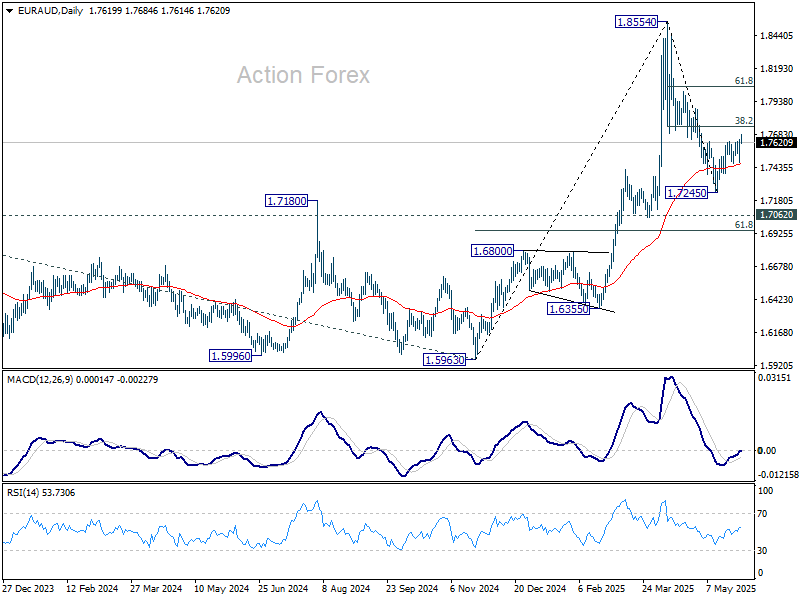

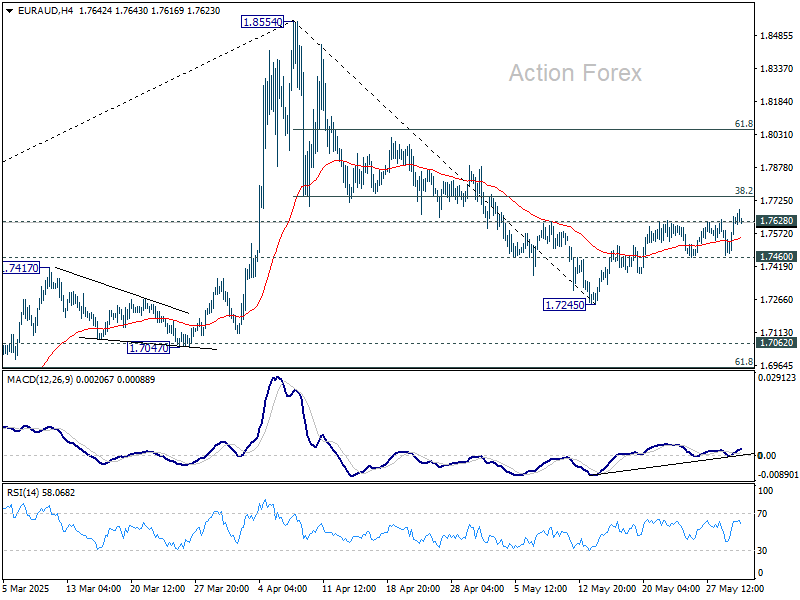

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7527; (P) 1.7591; (R1) 1.7709; More...

EUR/AUD's break of 1.7628 resistance argues that fall from 1.8554 might have completed as a correction at 1.7245. Intraday bias is back on the upside for 38.2% retracement of 1.8554 to 1.7245 at 1.7745. Firm break there will solidify this bullish case and target 61.8% retracement at 1.8054. On the downside, however, break of 1.7460 support will bring retest of 1.7245 instead.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 will target 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.