Sample Category Title

Markets Turn Cautious Again on Trade Stalemates; Euro Picking Up Momentum in Some Crosses

Asian markets returned to a risk-off tone today, with investor sentiment once again weighed down by the lack of clarity on the US tariff front and the apparent stalling of key trade negotiations. The week’s earlier relief rally following the U.S. court ruling against President Trump’s sweeping reciprocal tariffs has faded, as the legal battle drags on and policy direction remains uncertain. The result is renewed market hesitancy, with equities pulling back and safe-haven flows nudging Yen higher.

In currency markets, the tone is cautious and directionless, with almost all major pairs and crosses confined to last week's ranges. After a volatile stretch, there’s little momentum to drive breakouts. For the day, Yen is the strongest performer, supported by risk aversion, followed by the Dollar and Kiwi. On the weaker side, the Euro is underperforming, trailed by the Aussie and Sterling. Swiss Franc and Loonie are trading near the middle of the pack.

Thursday’s session in the US captured this shifting mood well as stocks closed well off their intraday highs. That optimism was first driven by the US Court of International Trade’s ruling that struck down most of Trump’s global tariff orders. However, the relief was short-lived. The US Court of Appeals paused that ruling to consider the administration’s appeal, setting a new timeline for responses from both plaintiffs and the government in early June. The pause has restored uncertainty to a situation markets briefly hoped was resolved.

Further dampening sentiment were remarks from US Treasury Secretary Scott Bessent, who confirmed that US-China trade talks are “a bit stalled.” He did, however, hold out the possibility of further engagement in the coming weeks, including a potential leader-level call. Still, Bessent acknowledged that the magnitude and complexity of the negotiations likely require direct involvement from both presidents, a signal that near-term breakthroughs remain unlikely.

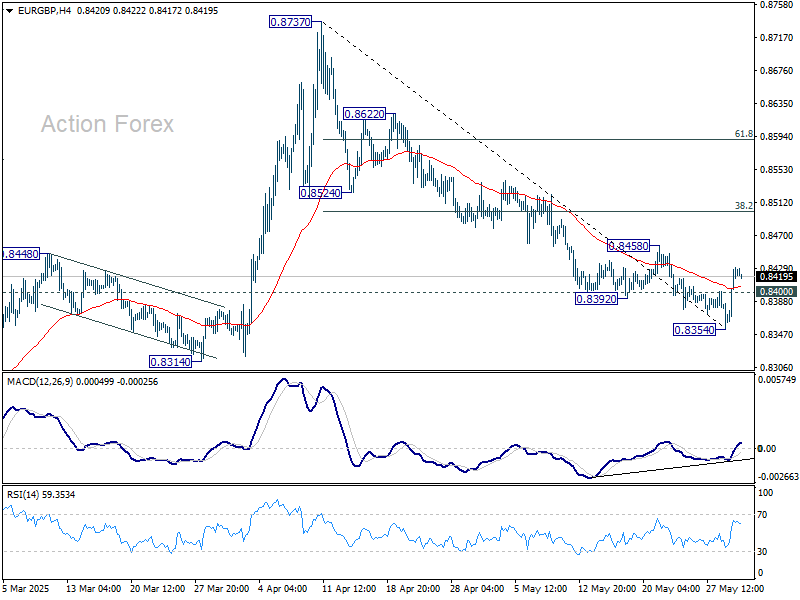

Technically, however, EUR/GBP's break of 0.8400 minor resistance suggests short term bottoming at 0.8354, on bullish convergence condition in 4H MACD. While the rebound might still be a corrective move, further rise is now in favor through 0.8458 resistance to 38.2% retracement of 0.8737 to 0.8354 at 0.8500.

In Asia, at the time of writing, Nikkei is down -1.08%. Hong Kong HSI is down -1.54%. China Shanghai SSE is down -0.30%. Singapore Strait Times is down -0.24%. Japan 10-year JGB yield is down -0.015 at 1.506. Overnight, DOW rose 0.28%. S&P 500 rose 0.40%. NASDAQ rose 0.39%. 10year yield fell -0.053 to 4.424.

Looking ahead, Germany CPI flash is the main focus in European sess. Switzerland will publish KOF economic barometer. Eurozone will release M3 money supply. Later in the day, attention will be on Canada GDP, and US PCE inflation.

Japan's industrial production falls -0.9% mom in April, but May rebound expected

Japan's industrial production fell by -0.9% mom in April, a milder decline than the expected -1.4%. The Ministry of Economy, Trade and Industry maintained its view that production "fluctuates indecisively," reflecting ongoing uncertainty, particularly around global trade developments.

While the ministry said the impact of US tariffs was limited in April, some firms have voiced concern about the manufacturing outlook as policy risks persist.

The breakdown of the data shows a mixed picture: six of 15 industrial sectors saw declines, including production machinery, fabricated metals, and transport equipment excluding motor vehicles. However, eight sectors recorded gains, with electronic parts and business-oriented machinery showing notable strength.

Manufacturers surveyed expect a sharp 9.0% rebound in May, followed by a -3.4% dip in June.

Also released, Japan's retail sales grew by a stronger-than-expected 3.3% yoy in April, outpacing the consensus of 2.9% yoy. Meanwhile, the unemployment rate remained steady at 2.5%.

Tokyo core inflation accelerates to 3.6%, driven by food and services costs

Tokyo's core CPI (excluding fresh food) accelerated to 3.6% yoy in May, up from 3.4% yoy and above market expectations of 3.5% yoy, marking the fastest pace since January 2023. This marks the third consecutive year that core inflation has exceeded the Bank of Japan’s 2% target.

While headline CPI ticked down slightly from 3.5% yoy to 3.4% yoy, the underlying core-core measure (excluding food and energy) also edged up fro 2.0% yoy to 2.1% yoy, suggesting broad-based inflation persistence.

The surge in non-fresh food prices, up 6.9% yoy, remains a dominant driver—highlighted by a staggering 93.2% yoy jump in rice prices.

Another notable development is the uptick in services inflation, which climbed to 2.2% yoy from 2.0% yoy , indicating that businesses are beginning to pass on higher labor costs.

Australia retail sales down -0.1% mom in April, weighed by weak clothing demand

Australia’s retail sales turnover unexpectedly declined by -0.1% mom in April, missing expectations for a 0.3% mom rise. On an annual basis, sales were up 3.8% compared to April 2024/

The Australian Bureau of Statistics noted that the decline was driven primarily by reduced spending on clothing. The weakness was partly offset by a rebound in Queensland, where businesses recovered from disruptions caused by ex-Tropical Cyclone Alfred in March.

RBNZ's Silk: Data to guide timing and need for further cuts

RBNZ Assistant Governor Karen Silk said that interest rates are currently within the estimated neutral band of 2.5% to 3.5%.

She noted that the full impact of previous easing has yet to filter through the economy, making any future adjustments highly dependent on incoming data.

The OCR track indicates "whatever we do is going to be data-dependent, and then we will be looking to the data to help us to decide when or if we cut further from here," she added.

Fed’s Logan: Policy well positioned, ready to respond to shifting risks

Dallas Fed President Lorie Logan said overnight that with inflation "trending gradually back to target", the labor market "holding strong", and risks to Fed’s dual mandate are "roughly balanced.

Speaking at an event, Logan emphasized that "monetary policy is in a good place", and there is no immediate need for a policy shift.

Logan also highlighted the potential impact of fiscal policy and regulatory changes, noting they could stimulate investment and consumer demand, while elevated economic uncertainty or financial volatility might dampen activity.

Fed's Daly: Modestly or moderately restrictive policy still needed

San Francisco Fed President Mary Daly, in a Reuters interview, emphasized that above-target inflation remains her "focus" while the labor market is in "solid shape".

With inflation still running above the Fed's 2% target and uncertainty around the pace of its decline, Daly said it's appropriate for monetary policy to remain in a “modestly or moderately restrictive” stance to guide inflation back to target.

Daly added that she's closely watching for any signs of labor market weakening but hasn’t observed such signals yet. At the same time, she remains attentive to whether inflation continues to gradually ease or risks becoming sticky or re-accelerating.

BoE's Bailey stresses caution on rate cuts amid inflation surprises and trade uncertainty

BoE Governor Andrew Bailey emphasized the need for a “gradual and careful” approach to future interest rate cuts in light of lingering global trade uncertainty and its impact on domestic inflation.

His comments follow last week’s stronger-than-expected inflation data, which showed UK CPI jumping to 3.5% in April from 2.6%. Bailey noted it remains unclear how much of the increase is due to seasonal factors, and said the BoE will closely examine the next set of inflation data ahead of its June policy decision.

Bailey acknowledged that while core inflation is "gradually grinding down", the pace of improvement remains sluggish. He also highlighted a renewed rise in food price inflation, which—although not unique to the UK—has a significant influence on public inflation perceptions.

EUR/AUD Daily Outlook

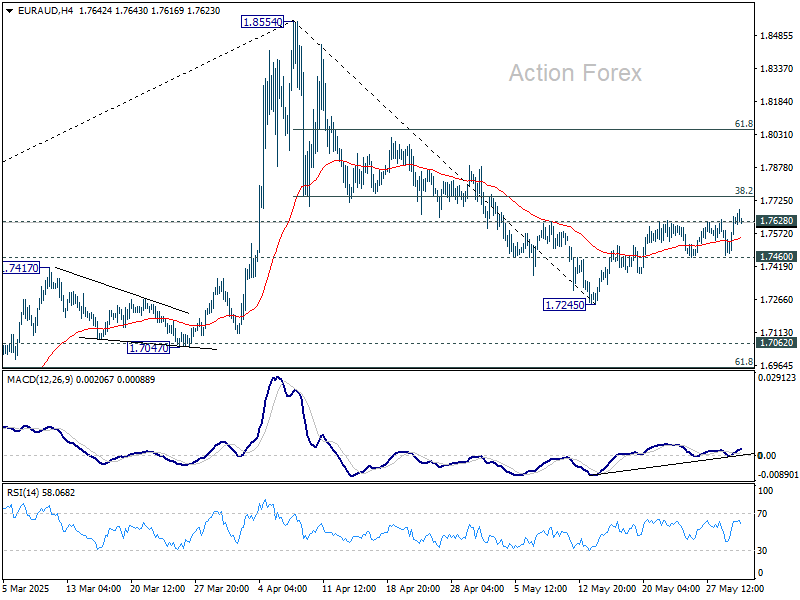

Daily Pivots: (S1) 1.7527; (P) 1.7591; (R1) 1.7709; More...

EUR/AUD's break of 1.7628 resistance argues that fall from 1.8554 might have completed as a correction at 1.7245. Intraday bias is back on the upside for 38.2% retracement of 1.8554 to 1.7245 at 1.7745. Firm break there will solidify this bullish case and target 61.8% retracement at 1.8054. On the downside, however, break of 1.7460 support will bring retest of 1.7245 instead.

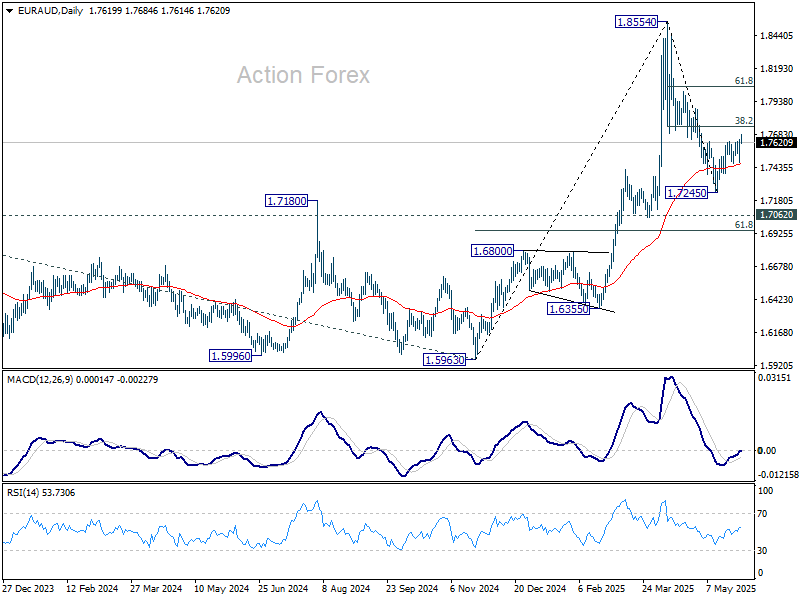

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 will target 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

Cliff Notes: Learning to Live with Uncertainty

Key insights from the week that was.

In Australia, the April Monthly CPI Indicator rose 0.8% in the month, leaving annual headline inflation steady at 2.4% – around the mid-point of the RBA’s target band. Being the first month of the quarter, the main updates of interest were on durable goods which are surveyed only once per quarter. There were a few upside surprises here relative to Westpac’s forecast, particularly around footwear, textiles and household contents. The monthly trimmed mean estimate consequently ticked up from 2.7%yr to 2.8%yr, posing some upside risk to our Q2 CPI forecast. As this indicator only provides a ‘partial’ look at inflation, the next two months’ releases are necessary to get a full view.

In the run-up to Q1 GDP next week, we also received two partial indicators of investment.

Construction activity was weaker than expected, holding flat in the quarter to be up 3.5% over the year to March. The main disappointment was the ‘lumpy’ infrastructure segment, down 1.0% in Q1 despite a healthy project pipeline of public sector and renewable initiatives. It was nonetheless encouraging to see residential construction hold to its uptrend, though the current rate of construction is still falling well short of the demands from a growing population. Thankfully, cost pressures look to be easing, suggesting the intense capacity constraints that plagued the sector over recent years are starting to abate.

Private CAPEX also subsequently disappointed, the –0.1% decline in Q1 bringing the annual pace down into negative territory at –0.5%yr. The non-mining sector was the chief culprit behind the weak print (–0.9%), reflecting a broad-based pull-back in equipment spending; the mining sector provided an offset (+1.9%). 2025-26 CAPEX plans continue to capture a subdued outlook for investment, but there hasn’t been a material response to the volatility in the global outlook brought about by President Trump’s trade actions. As detailed in our recent Quarterly Business Snapshot, Australian businesses are well placed overall; and, as discussed in talking about trade, resilient to current global trade uncertainty.

Our Q1 GDP preview will be published later today on Westpac IQ.

Offshore, the US was again the focus in a quiet week for data.

The FOMC's May meeting minutes showed FOMC members remain confident in the underlying health of the US economy, with economic activity and labour market conditions both characterised as "solid". Inflation was meanwhile described as "somewhat elevated" and the "significant uncertainties" for inflation and expectations from trade and migration policies called out. There was only limited discussion of the different activity scenarios constructed by staff, and FOMC members views also highlighted the high degree of uncertainty currently present. Staff projections for inflation lifted, but members also noted "significant uncertainty surrounded those effects". The committee is well aware of the difficult task in managing the dual mandate, noting that "Participants emphasized the importance of ensuring that longer-term inflation expectations remained well anchored... [and that] the Committee might face difficult trade-offs if inflation proves to be more persistent while the outlook for growth and employment weaken."

Overall, the minutes gave little away in forward guidance or a reaction function to tariff-related impacts on the economy. The FOMC is clearly in 'wait and see' mode, which seems appropriate given the uncertainty around bilateral trade negotiations; the potential for tariffs to again be lifted by President Trump; and now the uncertainty over the legal standing of the tariffs themselves, which is to be decided through the appeals process after the US Court of International Trade this week determined President Trump had exceeded his authority with the bilateral tariffs of Liberation Day and those related to fentanyl. President Trump and the administration believe they will win on appeal and President Trump continues to argue the FOMC should lower interest rates without delay, as made clear by reports after the first meeting for this term between President Trump and FOMC Chair Powell this week.

Closer to home, the Reserve Bank of New Zealand cut their overnight cash rate by 25bps to 3.25% in a 5-1 vote. The decision was accompanied by a fresh set of forecasts which showed a lower central expectation for GDP growth. They also showed inflation is expected to peak at 2.7% in the September quarter and decelerate to 1.9% by early 2026. Governor Hawkesby noted the RBNZ would begin the next meeting with "no bias", insinuating they are not on a pre-set path and will focus on the data between now and then. Most notably, the projected OCR was revised down with the low point for policy rate now 2.85% from 3.10% previously. In light of these views and recent data, our New Zealand colleagues have revised the timing of their call, now expecting the next cut to come in August instead of July.

RBNZ’s Silk: Data to guide timing and need for further cuts

RBNZ Assistant Governor Karen Silk said that interest rates are currently within the estimated neutral band of 2.5% to 3.5%.

She noted that the full impact of previous easing has yet to filter through the economy, making any future adjustments highly dependent on incoming data.

The OCR track indicates "whatever we do is going to be data-dependent, and then we will be looking to the data to help us to decide when or if we cut further from here," she added.

Australia retail sales down -0.1% mom in April, weighed by weak clothing demand

Australia’s retail sales turnover unexpectedly declined by -0.1% mom in April, missing expectations for a 0.3% mom rise. On an annual basis, sales were up 3.8% compared to April 2024/

The Australian Bureau of Statistics noted that the decline was driven primarily by reduced spending on clothing. The weakness was partly offset by a rebound in Queensland, where businesses recovered from disruptions caused by ex-Tropical Cyclone Alfred in March.

Japan’s industrial production falls -0.9% mom in April, but May rebound expected

Japan's industrial production fell by -0.9% mom in April, a milder decline than the expected -1.4%. The Ministry of Economy, Trade and Industry maintained its view that production "fluctuates indecisively," reflecting ongoing uncertainty, particularly around global trade developments.

While the ministry said the impact of US tariffs was limited in April, some firms have voiced concern about the manufacturing outlook as policy risks persist.

The breakdown of the data shows a mixed picture: six of 15 industrial sectors saw declines, including production machinery, fabricated metals, and transport equipment excluding motor vehicles. However, eight sectors recorded gains, with electronic parts and business-oriented machinery showing notable strength.

Manufacturers surveyed expect a sharp 9.0% rebound in May, followed by a -3.4% dip in June.

Also released, Japan's retail sales grew by a stronger-than-expected 3.3% yoy in April, outpacing the consensus of 2.9% yoy. Meanwhile, the unemployment rate remained steady at 2.5%.

Tokyo core inflation accelerates to 3.6%, driven by food and services costs

Tokyo's core CPI (excluding fresh food) accelerated to 3.6% yoy in May, up from 3.4% yoy and above market expectations of 3.5% yoy, marking the fastest pace since January 2023. This marks the third consecutive year that core inflation has exceeded the Bank of Japan’s 2% target.

While headline CPI ticked down slightly from 3.5% yoy to 3.4% yoy, the underlying core-core measure (excluding food and energy) also edged up fro 2.0% yoy to 2.1% yoy, suggesting broad-based inflation persistence.

The surge in non-fresh food prices, up 6.9% yoy, remains a dominant driver—highlighted by a staggering 93.2% yoy jump in rice prices.

Another notable development is the uptick in services inflation, which climbed to 2.2% yoy from 2.0% yoy , indicating that businesses are beginning to pass on higher labor costs.

Fed’s Logan: Policy well positioned, ready to respond to shifting risks

Dallas Fed President Lorie Logan said overnight that with inflation "trending gradually back to target", the labor market "holding strong", and risks to Fed’s dual mandate are "roughly balanced.

Speaking at an event, Logan emphasized that "monetary policy is in a good place", and there is no immediate need for a policy shift.

Logan also highlighted the potential impact of fiscal policy and regulatory changes, noting they could stimulate investment and consumer demand, while elevated economic uncertainty or financial volatility might dampen activity.

Fed’s Daly: Modestly or moderately restrictive policy still needed

San Francisco Fed President Mary Daly, in a Reuters interview, emphasized that above-target inflation remains her "focus" while the labor market is in "solid shape".

With inflation still running above the Fed's 2% target and uncertainty around the pace of its decline, Daly said it's appropriate for monetary policy to remain in a “modestly or moderately restrictive” stance to guide inflation back to target.

Daly added that she's closely watching for any signs of labor market weakening but hasn’t observed such signals yet. At the same time, she remains attentive to whether inflation continues to gradually ease or risks becoming sticky or re-accelerating.

BoE’s Bailey stresses caution on rate cuts amid inflation surprises and trade uncertainty

BoE Governor Andrew Bailey emphasized the need for a “gradual and careful” approach to future interest rate cuts in light of lingering global trade uncertainty and its impact on domestic inflation.

His comments follow last week’s stronger-than-expected inflation data, which showed UK CPI jumping to 3.5% in April from 2.6%. Bailey noted it remains unclear how much of the increase is due to seasonal factors, and said the BoE will closely examine the next set of inflation data ahead of its June policy decision.

Bailey acknowledged that while core inflation is "gradually grinding down", the pace of improvement remains sluggish. He also highlighted a renewed rise in food price inflation, which—although not unique to the UK—has a significant influence on public inflation perceptions.

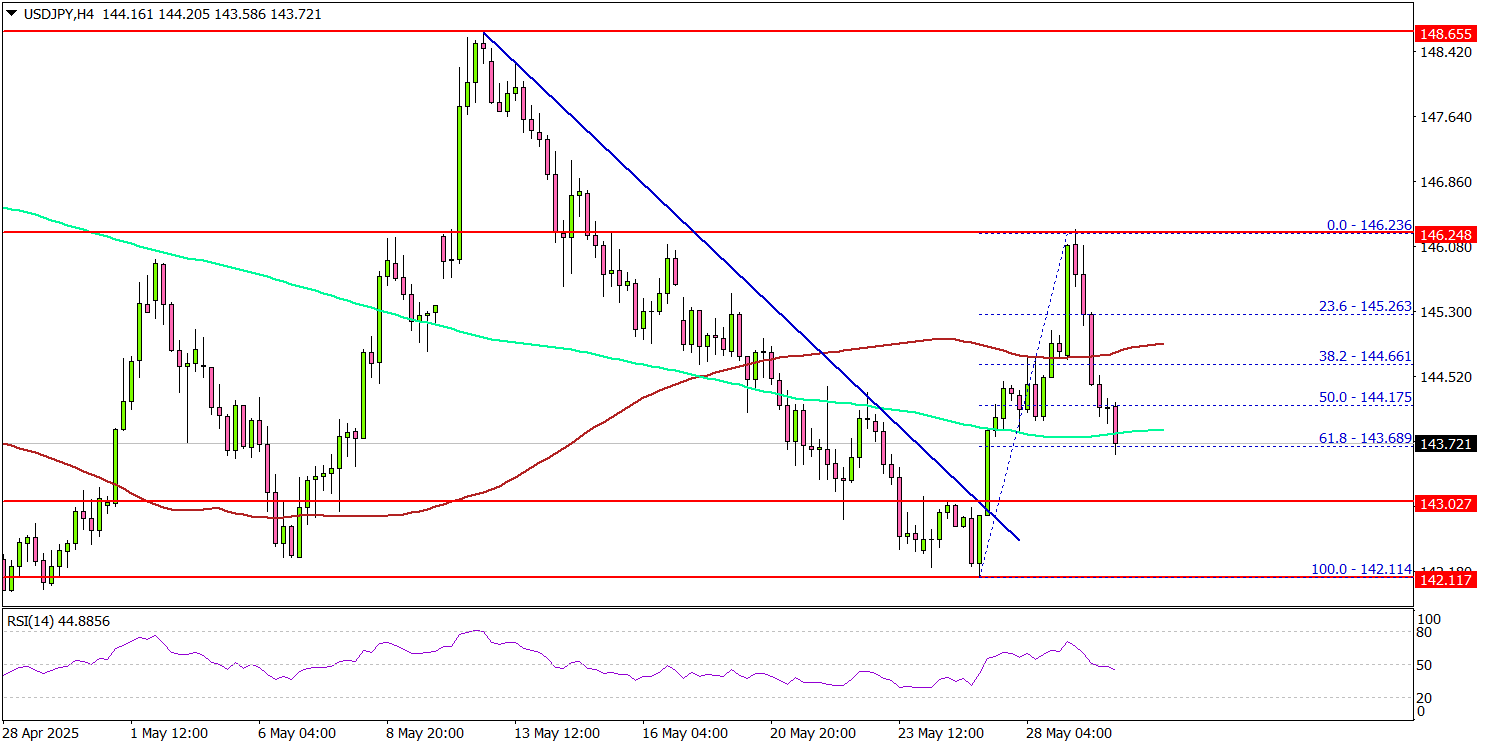

USD/JPY Struggles To Recover, Fresh Downside Ahead?

Key Highlights

- USD/JPY started a fresh decline and traded below the 144.00 level.

- It traded above a connecting bearish trend line with resistance at 143.05 on the 4-hour chart.

- EUR/USD is rising and might clear the 1.1420 resistance zone.

- GBP/USD is holding gains and could aim for a move above the 1.3600 resistance.

USD/JPY Technical Analysis

The US Dollar started a recovery wave from the 142.20 zone against the Japanese Yen. USD/JPY climbed above the 143.00 and 143.50 levels.

Looking at the 4-hour chart, the pair traded above a connecting bearish trend line with resistance at 143.05. It even climbed above the 146.00 level before the bears appeared. A high was formed at 146.23 and the price started a fresh decline.

There was a move below the 144.00 support, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

On the upside, the pair could face resistance near the 144.20 level. The next key resistance sits near the 144.50 level. The first major resistance sits at 145.00. A close above the 145.00 level could set the pace for another increase.

In the stated case, the pair could even clear the 146.00 resistance. The next major stop for the bulls could be near the 147.80 resistance.

On the downside, immediate support sits near the 143.00 level. The next key support sits near 142.50. Any more losses could send the pair toward the 141.20 pivot level in the near term. The main support could be near 140.00.

Looking at EUR/USD, the pair started another increase, and the bulls could now aim for a move above the 1.1420 resistance.

Upcoming Economic Events:

- US Personal Income for April 2025 (MoM) - Forecast +0.4%, versus +0.2% previous.

- US Core Personal Consumption Expenditure for April 2025 (MoM) - Forecast +0.1%, versus -0.1% previous.