Sample Category Title

EURUSD Rises to 5-Week High as Dollar Suffers from Fresh Tariff Threats

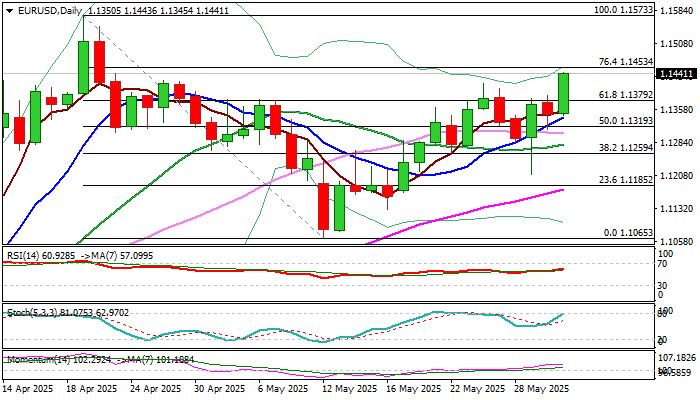

EURUSD hit the highest in over five weeks on Monday, inflated by weaker dollar on the latest threats of doubling import duties on steel and aluminium.

The pair gained around 0.8% by the mid-US session and pressure strong resistance at 1.1453 (Fibo 76.4% of 1.1573/1.1065, reinforced by the upper 20-d Bollinger band.

Bulls may face increased headwinds here as bullish momentum started to fade and daily stochastic cracks the border of overbought territory.

Overall picture, however, remains positive with near term action being underpinned by thick daily cloud and MA’s back to full bullish configuration, suggesting that bulls may take a breather for consolidation before resuming.

Broken Fibo 61.8% (1.1379) reverted to solid support which should ideally hold, although bullish near term bias expected while the price stays above rising daily Tenkan-sen (1.1327).

Firm break of 1.1453 to open way for retest of 2025 peak (1.1573).

Res: 1.1453; 1.1500; 1.1547; 1.1573

Sup: 1.1418; 1.1379; 1.1355; 1.1327

USD/CHF Breaks Consolidation to Downside on Renewed Safe-Haven Demand

Trading in the region of ~0.81694, a decisive move in this morning’s trading sees USD/CHF surpass monthly lows and break previously held consolidation to the downside. Amidst an increase in general safe-haven demand, trade tariff uncertainty, mixed US economic data, and a dovish stance from the SNB weighs on dollar-franc price action.

USD/CHF: Key Takeaways

- Breaking down in this morning’s trading, USD/CHF trades 0.71% lower, facing further selling pressure amid an increase in demand for safe-haven assets

- US trade policy, especially regarding uncertainty on future inflation and economic growth, is adding to USD/CHF selling pressure

- While the Federal Reserve remains committed to a ‘wait-and-see’ approach to monetary policy, the SNB has openly discussed negative rates to combat deflationary pressures, potentially limiting franc upside

USD/CHF loses ground on continued US trade policy uncertainty

Renewing tariff fears courtesy of a recent spat with the European Union, USD/CHF remains at the mercy of the success, or lack thereof, of tariff negotiations in the coming month.

With recent progress failing to inspire market confidence, negotiation deadlines now loom, the most significant being the 90-day deferral of far-reaching ‘reciprocal’ tariffs scheduled to expire July 8th.

Understandably, President Trump will likely want to show he’s firm on deadlines to promote serious negotiations, but given past deferrals, some might question his resolve.

While recent commentary from the White House suggests tariffs are “not going away,” developments in trade agreements, especially with key partners like China, are likely to remain a hot topic throughout June, with USD/CHF amongst some of the currency pairs most affected.

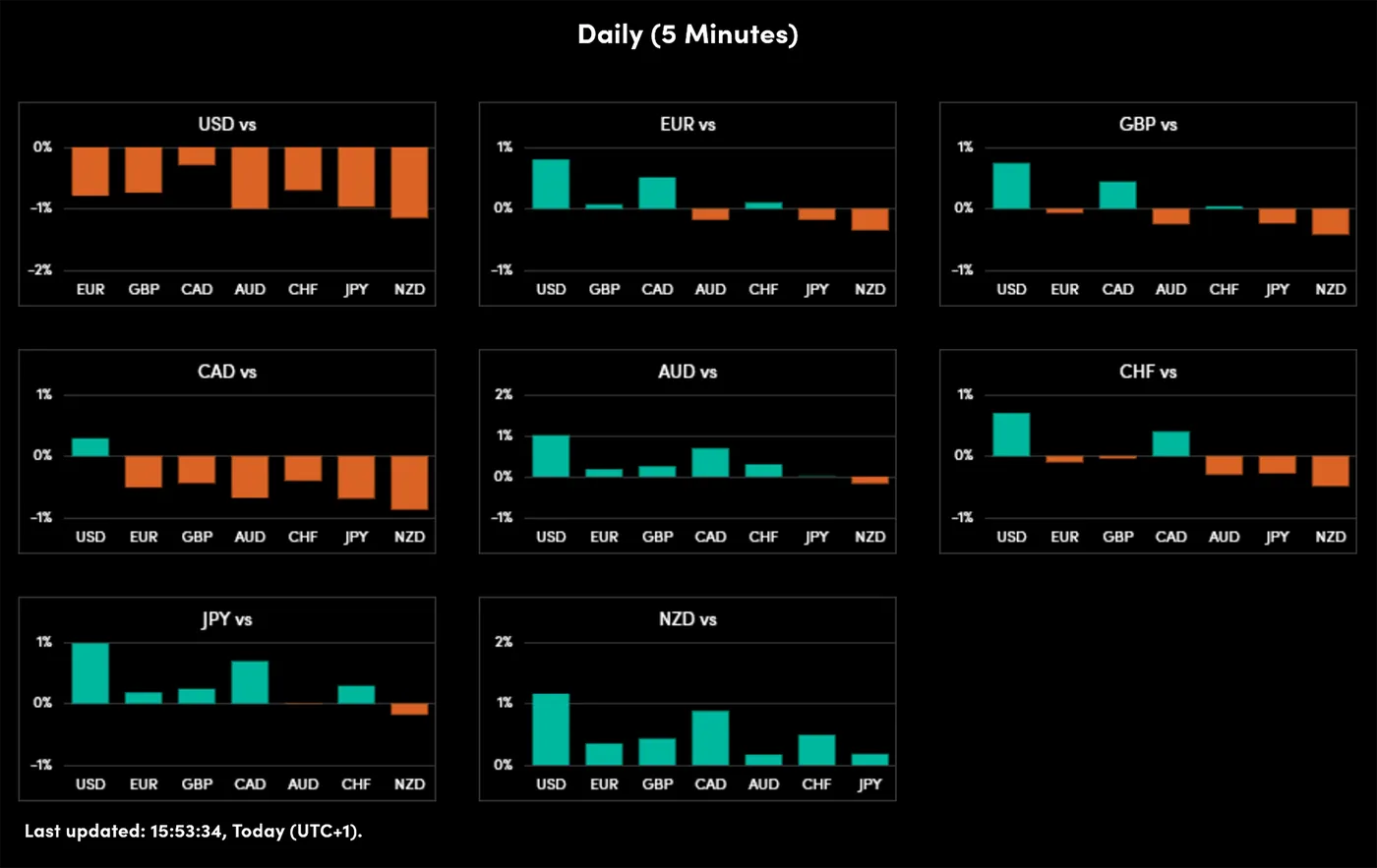

An image showing the Currency Strength Tool, OANDA Global Markets, 02/06/2025.

USD/CHF: Mixed US economic data sparks further dollar weakness

While last week’s economic event calendar proved active for the United States, the resulting data has encouraged a somewhat mixed perspective on the US economy, ultimately weighing negatively on dollar value:

Tuesday May 27th, US CB Consumer Confidence, +12.3

Amongst the first high-impact events last week, US consumer confidence rose by 12.3 points in May, snapping a five-month streak of decline. Linked to the pause in higher US-China tariff rates and positive US-EU trade developments, a rising consumer confidence is typically positive for USD value.

Thursday May 29th, US Gross Domestic Product Growth Rate QoQ Q1, -0.2%

Perhaps the most significant release last week, US GDP decreased at an annual rate of 0.2% in Q1, which, despite beating expectations, remains a contraction. Some reports suggested this was primarily due to increased imports, with US companies rushing to acquire foreign goods ahead of tariffs, which may have distorted otherwise accurate economic data. Regardless, a headline GDP contraction can be interpreted as dollar-negative.

Thursday May 29th,US Initial Jobless Claims, +14,000

Exceeding analyst expectations by 10,000, 14,000 initial jobless claims were made in the week ending 24th. Purportedly remaining in a “historically healthy range”, the latest increase shows insured employment rising to its highest level in over three years, adding to the case for Fed interest rate cuts. As can be expected, this is fundamentally negative for the dollar.

Friday May 30th, US Core Personal Consumption Expenditures PI (PCE) YoY, -0.2%

Significant to future Fed policy decisions, PCE data released on Friday showed inflation continuing to slow, down -0.2% YoY in March to reach 2.5%, its lowest level since April 2021. Moving closer towards the Fed target of 2%, the resulting increase in rate-cut bets can be interpreted as generally dollar-negative.'

USD/CHF: Fed and SNB policy become increasingly divergent

While the Fed remains committed to a “wait-and-see” approach to monetary policy, recent commentary from the Swiss National Bank suggests that a return to negative rates is a real possibility in their upcoming decision.

Despite cutting rates by 0.25% in March, citing “increased downside risks to inflation in the medium term,” the SNB remains under pressure from persistent deflation and a relative strengthening of the franc.

For now, a 25 BPS cut appears likely in their upcoming June 19th decision, but any further falls in USD/CHF pricing will increase bets of a 50 BPS cut, representing a potential return to negative rates for the first time since 2022.

As for USD/CHF pricing, we can expect long-term downside to be somewhat limited while the SNB maintains a more dovish stance than the Federal Reserve.

A chart showing the recent price action of USDCHF. OANDA,TradingView, 02/06/2025

USD/CHF: Technical analysis

- In today’s session, USD/CHF has broken previously held consolidation to the downside and trades at 40-day lows. If bearish momentum continues, bears will likely target ~0.81326, then ~0.81000 before an attempt on yearly lows

- Should today’s daily candle maintain or close lower in price than current levels, the 12-26 period MACD will become decisively bearish, suggesting short-term price movement is returning to the long-term downtrend

Dollar Under Pressure — Multi-Timeframe USD Breakdown

The US Dollar is beginning the week on a tough note as the White House appealed the Federal Court decision to block US tariffs - which has also dampened the risk-appetite on the week.

All majors are higher with the Asian-Pacific currencies leading the charge - NZD and JPY are both up above 0.80% against the USD in the morning session.

Gold is also much higher +2.40% on the day, with Bitcoin and Stock Indices down (though not by too much).

Let's dive into a DXY Analysis starting from the Monthly timeframe.

US Dollar Monthly, Weekly and Daily Analysis

Monthly Chart

Dollar Index Monthly Chart, June 2, 2025. Source: TradingView

A weaker US Dollar is one of the technical themes moving forex markets.

The Index is still at a relatively high level especially when compared to the 2010 decade where the USD was still recovering from the damages done by the 2008 Financial Crisis and the QE that followed.

The 2010 decade low for the DXY was at 72.80!

For a reminder, Quantitative Easing is a policy to "print" money to buy government bonds or other assets. This helps lower interest rates and boost the economy when growth is slow - like after 2008.

We can see that the monthly MA 200 is closer to 91.50 - levels last seen in October 2021. Especially with the FED not having began its cut cycle, it's too early to say the Dollar is already weak.

A zone to look out for in the upcoming weeks would be the lower key support at 95.50. We'll see better on a weekly chart.

Weekly Chart

Dollar Index Weekly Chart, June 2, 2025. Source: TradingView

After hanging around here for the last two months, we spent most of last week below the 100.00 Psychological level, and Moving Averages are now all above current prices.

They will now act as resistance instead of support, though they may magnet the Index higher on retracements.

Prices were in a solid range—100.00 to 106.00—between 2022 to 2024, and a breakout to the upside at the end of last year was rejected, as prices have gone down sharply since the 110.00 highs in February 2025.

In the meantime, a deeper selloff in the Dollar index points at a new range forming between 95.50 and 100 - these prices are still far, though more uncertainty and tariffs may accelerate this.

Daily Chart

Dollar Index Daily Chart, June 2, 2025. Source: TradingView

We officially completed the U-turn from the September 2024 rise in the DXY to its ongoing fall.

There is a key pivot zone between 100.00 to 100.75 that was breached and is now acting as resistance as prices already bounced from there last week.

The descending trendline and MAs acting as resistances seem to be applying more pressure though as observed, the Daily MA 20 seems to be a candidate for retracements. It's hanging around just above the 100.00 level.

We are currently trading in the immediate Support Zone between 98.50 to 99.00, a break trough here would point towards the April Lows at 97.20.

However, a rebound from here could point to a return to the key pivot zone and a consolidation of current prices.

Let's see how to Trump Tariffs unfold as this will surely influence the appetite for the Dollar. Also don't forget the key events of the week with the Bank of Canada and ECB in the middle of the week and May NFP on Friday.

Safe Trades!

U.S. Manufacturing Slump Worsens in May, Dow Jones (DJIA) Steady

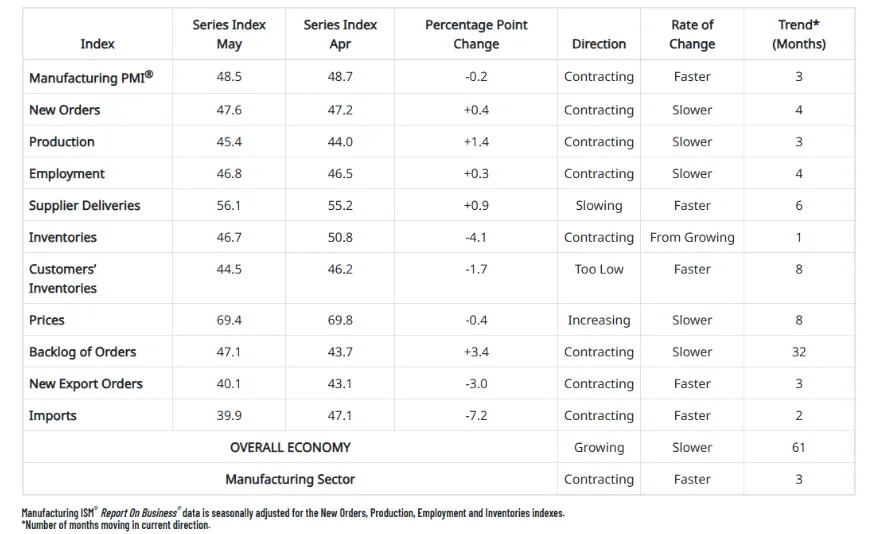

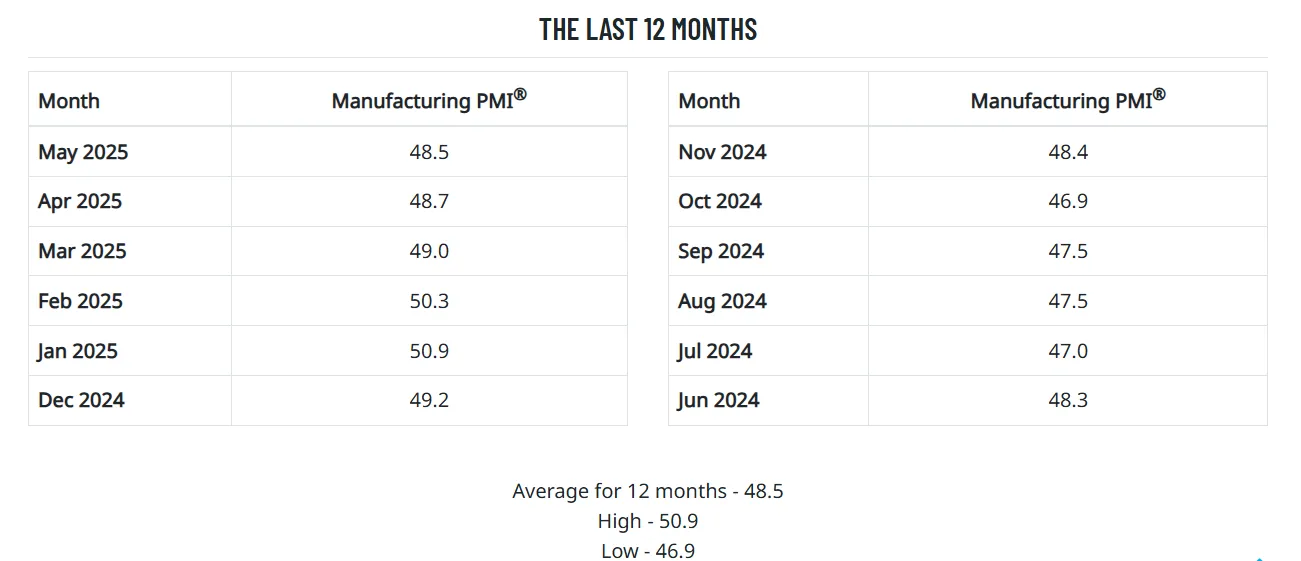

The ISM Manufacturing PMI in the U.S. dropped to 48.5 in May 2025, down from 48.7 in April and below the expected 49.5. This marks the third straight month of decline in the manufacturing sector and the biggest drop since November 2024, showing growing economic uncertainty and ongoing cost pressures, partly due to unpredictable trade policies under the Trump administration.

Production, new orders, jobs, and backlogs all fell, though not as quickly as before, while export sales saw a sharper decline. Inventories shrank after previously growing because companies stocked up ahead of tariffs. Supplier delays continued due to port bottlenecks, and while tariff-related price increases slowed slightly, they remained high overall.

The report was issued today by Susan Spence, MBA, Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

Source: ISM

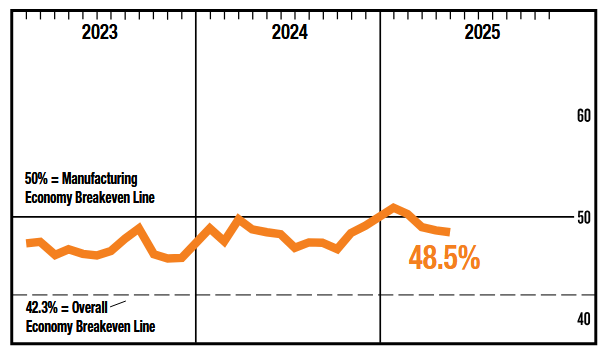

A reading above 50 percent indicates that the manufacturing sector is generally expanding; below 50 percent indicates that it is generally contracting.

A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the May Manufacturing PMI® indicates the overall economy grew for the 61st straight month after last contracting in April 2020. “The past relationship between the Manufacturing PMI® and the overall economy indicates that the May reading (48.5 percent) corresponds to a change of plus-1.7 percent in real gross domestic product (GDP) on an annualized basis,” says Spence.

Source: ISM

Impact of the ISM Report Moving Forward

The report adds further pressure on the US economy which is already facing growth questions as tariff debates continue to rumble on and the US-China relationship has come under renewed strain following what seemed to be a breakthrough in discussions.

This weekend saw accusations from both sides that they have not adhered to terms of an interim 90-day deal struck thanks to recent dialogue.

The renewed tension has been reflected in markets with a risk off tone dominating the start of the week and month as market participants continue to wait for clarity regarding trade deals. This morning we heard from US Deputy Treasury Secretary Faulkender who said: “I think we will see deals before July 9th, Some trade deals should be imminent.”

If trade deals are imminent and an announcement comes this week it could help improve overall sentiment which has faced growing challenges of late.

For the full ISM report, click here: https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business/pmi/may/

Market Reaction - Dow Jones (DJIA)

The Dow Jones Index is in the red today thanks in large part to overall risk off sentiment.

The data however, saw an initial spike lower before recovering to trade slightly higher once markets digested the news.

Overall sentiment and pressure on steel and aluminum stocks are having an impact on indexes across the globe this morning, with the Dow proving to be no exception.

Market participants expecting US data to provide a bit of optimism will likely be glad that the Dow Jones did not record a particularly bad reaction to the data.

Immediate intraday resistance rests at 42144 before the 42192 and 42270 handles come into focus.

Immediate support rests at 41900 before the 41780 and 41660 handles may come into play.

Dow Jones M15 Chart, June 2, 2025

Source: TradingView

US: ISM Manufacturing Index Contracts for Fourth Consecutive Month in May

The ISM Manufacturing Index fell to 48.5 in May, down from 48.7 in April.

Seven of 18 industries reported growth for the month, down from eleven in April. Furthermore, 57% of manufacturing GDP contracted in May, well above the 41% share recorded in April.

Demand conditions continued to be weak on aggregate, but some improvement was seen in May. The new orders index improved marginally but remained in contraction territory (47.6 vs. 47.2 in April), while new export orders declined further into contraction (40.1 vs. 43.1 in April). The backlog of orders also continued to contract, but at a slower pace (47.1 vs. 43.7 in April) while imports collapsed (39.9 vs. 47.1 in April), sinking below pandemic levels.

The production index also saw a slowing pace of contraction in May, rising to 45.4 from 44.0, marking the first increase in the index since January. Employment contracted at a slower pace than in April as well, ticking up to 46.8.

Price gains remained on par with that seen in April, coming in at 69.4. The prices index remains near a three-year high.

Key Implications

Manufacturing activity continued to slow in May as elevated uncertainty related to trade policies continued to disrupt supply chains and production schedules. Respondents indicated minimal relief from the temporary suspension of higher tariffs earlier in the month, as the threat of higher levies continued to require contingency planning and existing tariffs continued to push input costs higher.

With most tariff policies now in effect for two months we have seen the feedthrough to prices have a dampening effect on demand and by extension production. The slowing pace of contraction in most demand categories in May indicates the initial drawdown has likely passed. But with the Federal Reserve maintaining a restrictive policy stance and the administration looking to double steel & aluminum tariffs later this week, activity is likely to remain soft through the remainer of the year barring a material shift in trade policy.

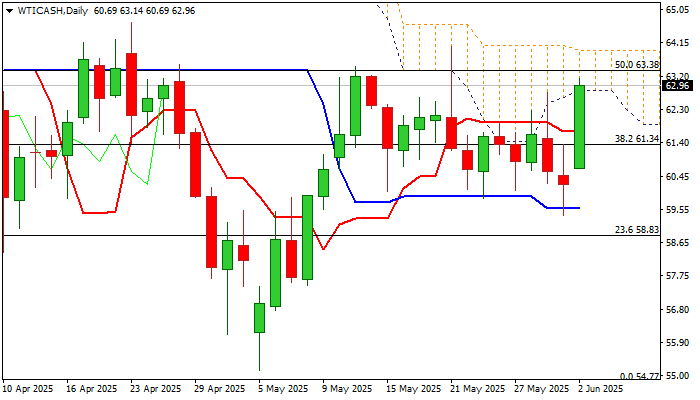

WTI Oil: Oil Price Rises Nearly 4%, Key Barriers Under Pressure

WTI oil price jumped around 3.7% and hit the highest in almost two weeks on Monday, on track for the biggest daily gain since April 9.

Fresh advance penetrated daily cloud (spanned between $62.83 and $63.92) and cracked psychological $63.00 level.

Near term focus shifts to key resistances at $63.92 /$64.03 (cloud top / ceiling of recent four-week congestion) break of which to generate stronger bullish signal for continuation of recovery from $55.14 (May 5 low).

Technical picture on daily chart is improving, as momentum studies are turning positive and daily Tenkan/Kijun-sen are in bullish configuration and below the price, but more work at the upside is still required to further firm the structure.

Sustained break of pivotal $64.00 zone to expose targets at $64.70 (April 23 top) and $65.00 (psychological).

Hourly higher base at $61.68 offers solid support which should contain dips and guard $61.34 (broken Fibo 38.2% of $71.98/$54.77, reinforced by 10DMA),

Res: 63.14; 63.38; 64.03; 64.70.

Sup: 62.24; 62.00; 61.68; 61.34.

Sunset Market Commentary

Markets

Investor reluctance towards US assets still proves the path of least resistance, as US president Trump warned on higher tariffs for steel (and aluminum) and as US-China trade talks apparently hit a roadblock causing mutual allegations. US equities, bonds and the dollar are all trading in red. Admittedly, losses remain orderly and the move also spills over to other (equity) markets, including Europe (EuroStoxx 50 -0.5%). Other core bonds (Bunds, gilts, Japanese bonds) also show more or less similar losses today. However, especially German Bund levels don’t trade at ‘near stress levels’ like their US counterparts. In this move the currency remains the key discriminating factor. USD weakness remains a by default means for investors to give their appreciation on the unpredictable swings in the Trump administration’s trade policy. In addition to the trade war and the risks it might cause for the US economy; markets are also pondering the idea of the trade war potentially turning into a capital market war. In its proposed Budget Bill; the Trump administration also included an item ‘ Enforcement of Remedies against unfair foreign taxes’ (Section 899). This might include additional taxing on foreign investors of countries that the administration deems to have discriminatory tax policies (e.g. a digital services tax on major US tech companies, minimum corporate taxes etc). The jury is still out whether and how such a measures might be implemented, but it adds another layer of uncertainty for investing in US assets whatsoever. In the run-up to publication of the US manufacturing ISM, US yields add between 3 bps (2-y) and 4 bps (30-y, 4.97%) with the 5% barrier again within reach. German yields add between 2.5 bps (2-y) and 3.5 bps (30-y). Aside from spillovers from the US, tomorrow’s EMU flash CPI and Thursday’s ECB meeting are a good reason for markets not to push further beyond ‘rich’ ECB easing that is currently discounted (ECB cycle low <1.75%). On FX markets, DXY is testing last week’s low near 98.7, the final ‘hurdle’ on the way back to the 97.92 YTD low. EUR/USD in a similar way is challenging the 1.1418 resistance. with the YTD top at 1.1573. The gain of Conservative candidate Nawrocki in the Polish presidential election doesn’t help a unified European approach to geopolitical challenges. Even so, for now the outcome only has a (modestly) negative impact on the zloty (EUR/PLN 4.2675), not on the euro. Still, in this context of USD weakness, the yen outperforms the euro (USD/JPY 143 from 144.0, EUR/JPY 163.2 from 163.4). At the time of finishing this report, the US Manufacturing ISM prints at a weaker than expected 48.5 (from 48.7). Employment also remains in contraction territory at 47.6 (from 47.2). At the same time, price pressures remain elevated with prices paid holding at 69.4 from 69.8. In a first reaction, equities and the dollar declines accelerate. Yields ease off the intraday highs, but stay in positive territory.

News & Views

Swiss GDP growth adjusted for sporting events accelerated from a strong 0.6% Q/Q pace in Q4 2024 to an even better 0.8% Q/Q in Q1 2025. That’s an upward revision from the previously reported 0.7%. The demand-side breakdown showed moderate growth in private consumption (+0.2%) supported particularly by expenses on health and housing. Investments in equipment and software rose by 0.4% Q/Q with construction investment 0.8% higher. Government spending rose by 0.4% as well. The production view showed that the services sector delivered broad-based growth. The chemical and pharmaceutical industry also expanded at an above-average rate (+7.5% Q/Q). Value added in other industrial sectors continued to fall. Overall, this resulted in strong growth for manufacturing (+2.1%) and goods exports (+5%). In particular, exports to the US rose sharply, pointing to possible front-loading in connection with US trade policy. The Swiss franc (EUR/CHF 0.9345) is unmoved by today’s numbers.

The Czech manufacturing PMI slipped again in May, from 48.9 to 48. Consensus hoped for a modest improvement to 49.3. The overall downturn worsened amid a faster fall in output levels and a renewed drop in new orders. Weak demand conditions and client uncertainty reportedly drove the decrease in new sales. Moreover, firms remained in retrenchment mode, as input buying and employment contracted again. Renewed delays to supplier delivery times amid shortages put pressure on capacity. Firms remained upbeat in the year-ahead outlook for output, however, as confidence rose to the highest in over three years. At the same time, inflationary pressures built as input costs (material shortages and higher energy bills) and output charges rose at faster, but still historically soft, rates. EUR/CZK is marginally lower on the day at 24.90.

US manufacturing remains subdued as ISM PMI falls to 48.5

US ISM Manufacturing PMI edged down to 48.5 in May from 48.7, falling short of expectations and marking the lowest reading since November. This marks the third straight month of contraction, with underlying components still signaling broad-based weakness.

New orders and production remained in negative territory, at 47.6 and 45.4 respectively, suggesting that demand conditions are still under pressure. Employment also stayed weak at 46.8, contracting for a fourth straight month.

Prices Index slipped marginally to 69.4 from 69.8, but remains elevated. Over the last six months, price pressures have surged by over 19 points, bringing the index to its highest readings since mid-2022.

The external sector delivered particularly concerning signals, with new export orders plunging to 40.1, the lowest level since the pandemic and, excluding COVID-19, the weakest since the Great Recession. Imports also collapsed, down sharply to 39.9.

Despite the weak headline number, ISM noted that the PMI reading still corresponds to roughly +1.7% real GDP growth on an annualized basis.

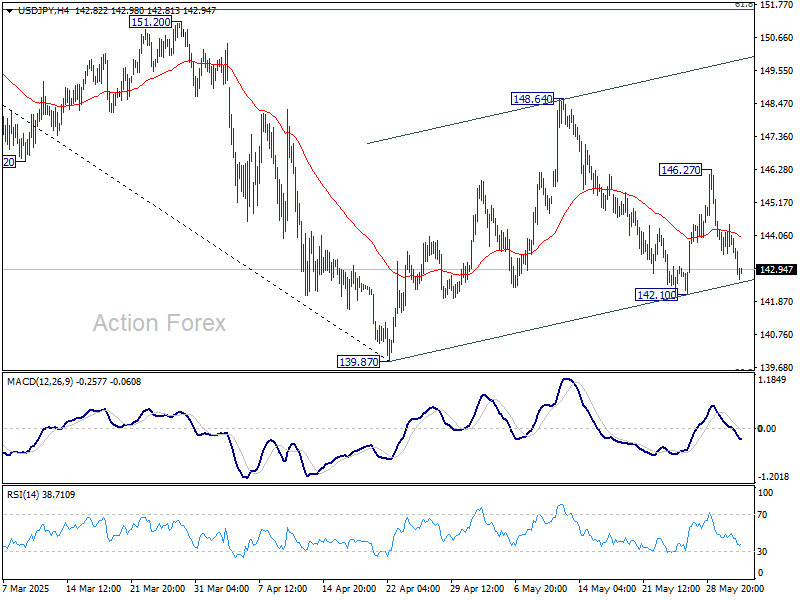

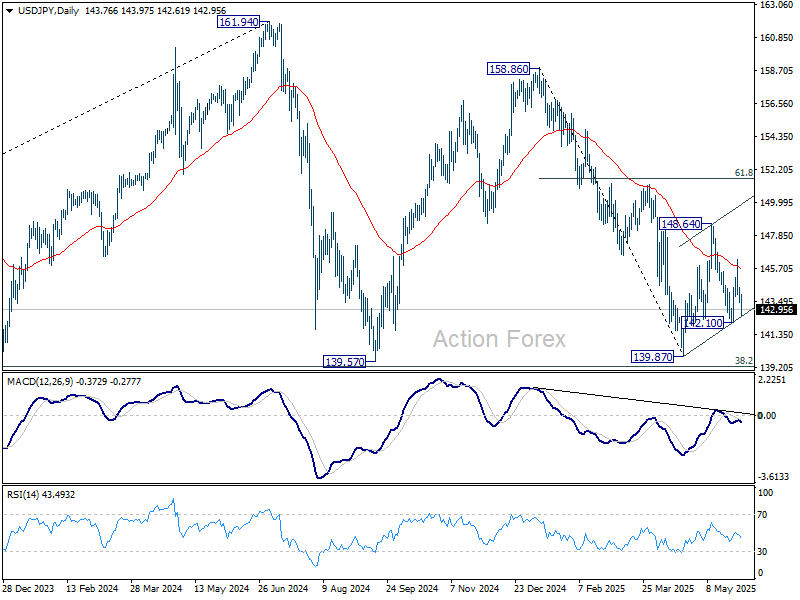

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.51; (P) 143.98; (R1) 144.51; More...

No change in USD/JPY's outlook and intraday bias stays neutral at this point. On the upside, above 146.27 will target 148.64 resistance first. Firm break there will resume the rebound from 139.87. Nevertheless, break of 142.10 will bring deeper fall back to 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

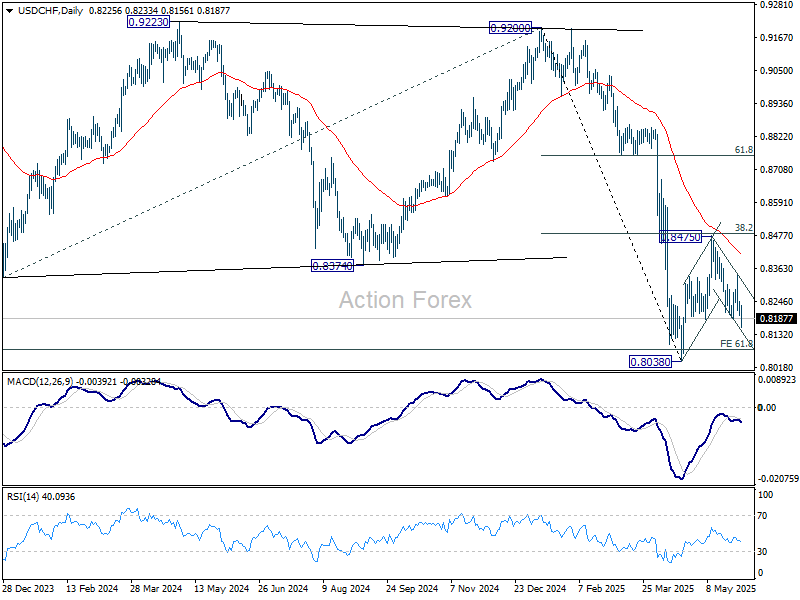

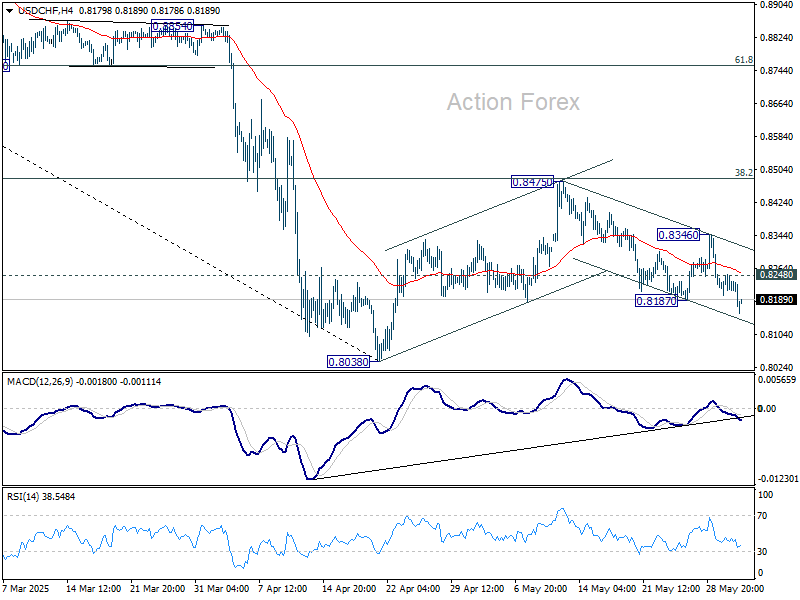

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8202; (P) 0.8226; (R1) 0.8252; More….

Intraday bias in USD/CHF is back on the downside, as fall from 0.8475 resumed by breaking through 0.8187. Deeper fall should be seen to 0.8038 low. But strong support could be seen from there to bring rebound, on first attempt. On the upside, above 0.8248 minor resistance will turn intraday bias neutral first. However, decisive break of 0.8038 will confirm larger down trend resumption.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8732) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.